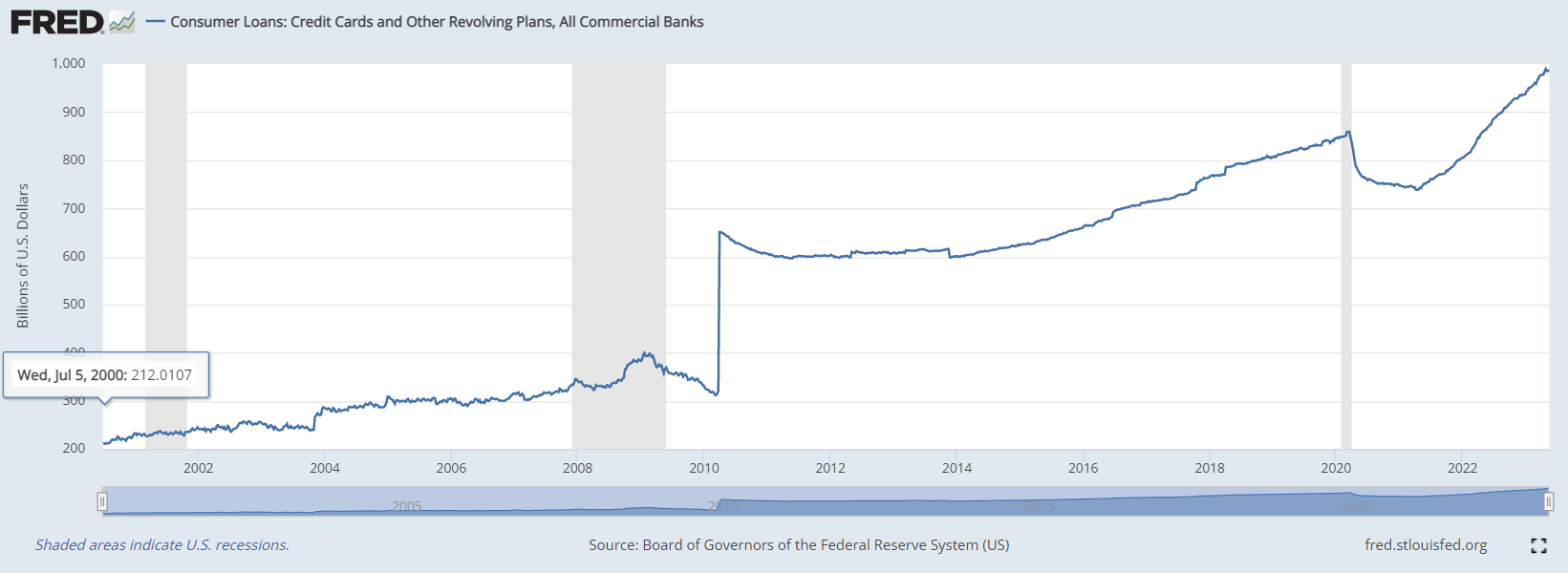

Credit card debt in the US spiked to its highest quarterly level in Q4 2022 after increasing by $85.8 billion. The average American household has about $10,000 in credit card debt, marking an 8.9% YoY increase. Now, Americans are facing $1 trillion in credit card debt due to rising APR and inflation.

The Federal Reserve reported that credit card debt has risen by $250 billion over the past two years amid record inflation. Consumer spending declined during the pandemic, as did credit card debt. However, inflation was nowhere close to what it is today. Credit balances declined by $100 billion from Q1 of 2020 to Q2 of 2021. Consumers were paying off their debts during this time, aided by numerous stimulus packages provided by the government.

Everything changed when Biden took office, killed America’s energy independence, and inflation began to spike. The central bank raised rates right before the war in Ukraine broke out, and have continued to do so at every meeting since. Various data collectors noted that consumers are not using their credit cards for luxury goods – they’re using credit to simply get by and pay for essentials.

Bankrate reported that 46% of cardholders cannot pay off their monthly credit card payments, up 7% from last year. The average APR is around 24% as of May 2023. The US Bureau of Labor Statistics claims that the CPI rose 0.4% in April after increasing 0.1% in March. I reported how the true inflation rate is over 30%; they do not want to scare the public by posting the real data. Food, energy, shelter, and all the essentials to survival have reached historic levels. If nearly half of people cannot pay their credit card balances off each month, and interest is at a record high, consumer debt is guaranteed to rise continually. Nothing is more inflationary than war, and our war cycle is picking up going into 2024. So not only is the US government drowning in debt, but the average American is also struggling to make ends meet.

Posted originally on the CTH on May 1, 2023 | Sundance

The topline story from the announcement by JPMorgan Chase [SEE HERE] there are no banking rules/laws in the Biden Fed/Treasury system.

The Dodd-Frank laws are still on the books, but the FDIC decision to insure all deposits, regardless of size, now means those laws, rules and regulations are not required to be followed. Additionally, as a result of JPMorgan gaining another $100+/- billion in deposit assets, the law(s) surrounding the 10% U.S. deposit maximum, within too big to fail banks, no longer exists. Noted in the announcement, “JPMorgan Chase is assuming all deposits – insured and uninsured.”

JPMorgan is also assuming assets consisting of $173 billion in loans and approximately $30 billion in securities. The FDIC is going to assume risk (with a risk sharing agreement) for current First Republic Bank mortgage and commercial loans acquired by JPMorgan, guaranteeing JPMorgan a 5-year fed fixed rate on $50 billion in mortgage bonds.

The Federal Deposit Insurance Corporation (FDIC) rule requiring the holding of 1.5% of deposits for all depositors up to $250k in all institutions is now essentially moot. If the FDIC is guaranteeing all deposits, there’s no way for the insurance corporation to capture or hold $1.5% of all banking deposits. The law is in conflict with the outcome action of the Fed/Treasury and ultimately the FDIC, ergo the law is nulled by the ignoring of it.

Mohamed El-Erian gives his take below, but seemingly missed the part of the announcement where JPMorgan states, “no systemic risk exception was required” in the deal. This means the FDIC is completely free-range with the agreement, they are not even trying to justify why they would make a too big to fail bank even bigger. WATCH:

.

The only reason the FDIC violated its own rules and banking regulations, was because the FDIC didn’t, likely -almost certainly- couldn’t, take the financial hit from a full takeover of First Republic Bank against the backdrop of the prior terms for Silicon Valley Bank (SVB).

When the FDIC made the (SVB) decision to guarantee all deposits regardless of size, they put themselves in a position of an insurance declaration they could never fulfill. The FDIC cannot structurally guarantee all of the First Republic Bank (FRB) deposits; they need a structure to avoid the government regulators absorbing the bank. This reality is also why the FDIC violated their own laws, rules and regulations in allowing JPM to exceed the legal U.S. deposits maximum.

In essence, what the FDIC is saying is they cannot maintain the premise of their charter without the big banks helping them. The biggest banks now control all of the leverage, with JPMorgan Chase and Jamie Dimon now controlling more financial power than the government that is supposed to regulate them.

FUBAR… All of it. Everything Biden touches turns to shit.

This is going to be a major hot mess now for Main Street investment and borrowing needs. The economy is going to feel the ramifications of this in less financing available to maintain domestic investment.

Last point. Look at the big picture, there’s no intervention protocol the legislative branch can trigger as a security against the reckless decisions of the FDIC (Fed and Treasury), without creating even bigger issues that could collapse the banking system. If the legislative branch forced the FDIC to follow the laws currently on the books, the domino of banks starts to collapse.

Posted originally on CTH on April 2, 2023 | Sundance

Before getting to the headline, I want to remind you what CTH outlined two years ago about these massive food price increases.

You might remember me saying that processed food prices will increase at a much greater rate than fresh or lesser processed foods. Factually, even organic products (ie. produce) could/would end up less expensive (in relative terms) to the increase in price at your supermarket, as compared to the price increases for the more processed foods.

The reason is simple, processed food use more energy; energy prices are skyrocketing; the processing costs (packaging, transportation, freezing, sanitizing, storage, warehousing and distribution etc.), at each step of the processing cycle, in addition to higher labor costs, drive up the end result of the price.

In this energy driven inflationary environment, less processing and handling equals lower overall cost increases from field to fork. More processing, handling, distribution equals higher overall costs. This is simply a supply chain, truism.

Into this issue comes McDonald’s Corp. Last I heard, approximately 85% of McDonald’s business was franchise. The franchise has to purchase the product (food) from the main company. Supply side cost increases in the food are transferred from the company to the franchisee via higher product costs. The restaurant is then forced to raise prices to accommodate their increased costs. A portion of the revenue from sales then flows back to the main company.

It is important to note here, there is a natural disconnect in supply side price increases within the franchise model. The parent company must, must, negotiate the best possible contract terms with the suppliers because the increases in costs are passed directly to the franchise. The parent company doesn’t immediately feel any problem until the revenue from the franchise drops due to the forced raising of retail prices and diminished sales. There is a lag.

McDonald’s is extremely exposed to processed food price increases.

McDonald’s franchises were forced by supply cost increases to raise retail prices. The retail prices were raised into a primary customer base that is already under extreme inflationary pressure. The average McDonald’s customer is exposed to inflation at almost every level of their life.

A typical family of four will now pay between $30 to $40 dollars for a single meal at a McDonald’s restaurant. That is not practical for the customer base. The result is lowered sales at retail, as eating a meal at home becomes the less costly option. The downstream consequence is lower revenue returned to the parent company.

The only way the parent company can offset the supply side costs to the franchisee is to lower overall operating costs. Expenses have to be cut. Advertising budgets reduced. Administration costs reduced. Administrative staffing levels reduced. Supply contracts renegotiated. Packing, warehousing, distribution and all vendor contracts renegotiated, consistently looking for better terms.

(Wall Street Journal) McDonald’s Corp. is temporarily closing its U.S. offices this week as it prepares to inform corporate employees about layoffs undertaken by the burger giant as part of a broader company restructuring.

The Chicago-based fast-food chain said in an internal email last week to U.S. employees and some international staff that they should work from home from Monday through Wednesday so it can deliver staffing decisions virtually. The company, in the message, asked employees to cancel all in-person meetings with vendors and other outside parties at its headquarters.

“During the week of April 3, we will communicate key decisions related to roles and staffing levels across the organization,” the company said in the message viewed by The Wall Street Journal. McDonald’s declined to comment Sunday on the number of employees being laid off.

McDonald’s in January said that it planned to make “difficult” decisions about changes to its corporate staffing levels by April, as part of a broader strategic plan for the burger chain.

Chief Executive Chris Kempczinski said in an interview at the time that he expected to save money as part of the workforce assessment, but said then he didn’t have a set dollar amount or number of jobs he was looking to cut. “Some jobs that are existing today are either going to get moved or those jobs may go away,” Mr. Kempczinski said.

McDonald’s employs more than 150,000 people globally in corporate roles and its owned restaurants, with 70% of them located outside of the U.S., the chain said in February.

McDonald’s in the message acknowledged that the week of April 3 would be a busy one for personal travel, which it said contributed to the decision to deliver the news remotely. Workers who wouldn’t have access to a computer during the week should provide personal contact information to their manager, the company said. (read more)

There is an onslaught of misinformation about the Federal Reserve from everything that it can go bankrupt, and the Treasury will become a second central bank, and of course, the Fed is really the cause of inflation and its balance sheet. The proposal by Janey Yellen to buy in long-term debt and swap it with short-term is not “creating” money for the Treasury has no such power. It was a proposal for a debt swap to shorten the yield curve. The first proposition that the Fed can go bankrupt only suggests that people do not comprehend that the Fed is different entirely from the European Central Bank.

The Fed has the authority to create elastic money for it followed the very idea of J.P. Morgan and how he saved the economy during the Panic of 1907. The Fed can create money when there is a shortage due to economic contractions, and it can then reduce its balance sheet reducing the money supply. When the Fed was created, it was established with branches around the country because the Panic of 1907 exposed that there were regional capital flow problems. The 1906 San Francisco Earthquake drained the cash from the East where all the insurance companies were.

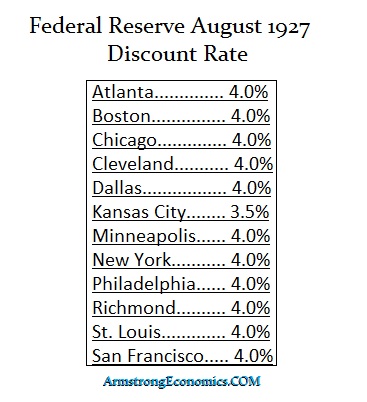

As we can see from this clip of rates in 1927, each branch was independent. There was an excess case in Kansas City so they lowered the interest rates there in hopes that capital would migrate to the other districts to earn more interest. All of that was eliminated by Franklin D. Roosevelt who wanted (1) to stack the Supreme Court to approve his Marxist agenda, which failed, and then he usurped all the power of the Federal Reserve and created the Washington headquarters and the President then was to appoint the head of the Federal Reserve and to illegally lobby him to ensure that his presidential agenda was to be the policy at the Federal Reserve. There was no more independence of the branches.

When Biden was running in 2020, he actually proposed requiring the Federal Reserve to regularly report on what they are doing to close economic gaps that exist along racial lines in the United States. Biden has viewed the Fed as a social tool and he has been making efforts to manipulate the Federal Reserve which will be extremely dangerous if they are carried out. Now, the Biden Administration is talking about closing branches of the Federal Reserve and replacing those board members with his hand-picked political cronies. In January 2022, he was pushing for black economists to be appointed to the Federal Reserve Board. My concern is that academics have ZERO experience and do not really understand the global economy trapped by domestic Keynesian Economics.

It was Paul Volcker who Chaired the Fed into the high in the interest rates back in 1981 who concluded in his Rediscovery of the Business Cycle that “it was not until the events of 1974 and 1975, when a recession sprung on an unsuspecting world with an intensity unmatched in the post-World War II period, that the lessons of the ‘New Economics’ were seriously challenged.” However, former Fed Chair Ben Bernanke has suggested that the Fed’s failure to contain inflation during the 1970s traced back to the political forces that shaped the Fed chairs in charge that he expressed in his book “21st Century Monetary Policy.” He wrote that the inflation of the ’70s puzzled economists relying on the 1958-ventage Phillips Curve, which would have predicted high inflation only in combination with extremely low unemployment rates. Bernanke admitted that the Phillips curve had “broken down” during the 1970s.

The critical problem with the entire way we view inflation rests on the QTM (Quantity Theory of Money) and the assumption that a mere increase in supply must produce inflation. There is absolutely nothing in the economic data that supports these old theories that were based upon (1) fixed exchange rates, and (2) the supply & demand theory dates back to the days of coinage. It was John Law who came up with the supply/demand theory that everyone else plagiarized, including Adam Smith. John Law’s writings influenced many, although they would never admit it. He was clearly the FIRST to use the term DEMAND and he was certainly the FIRST to join it with the word SUPPLY, for only a trader could have seen this connection in the price movements of anything.

The greatest fallacy of Keynesian Economics, Supply v Demand, and the Phillips Curve is that they have ALL failed because the US dollar is the reserve currency of the world and by default, the Federal Reserve has become the central bank of the world. With Biden desperate to get his hands around the neck of the Federal Reserve and force it to yield to his political agenda, threatens more than merely the US economy – but the entire world. Bernanke acknowledges in his book:

“Martin, my boys are dying in Vietnam, and you won’t print the money I need,” President Lyndon B. Johnson reportedly told then-Fed Chair William McChesney Martin Jr. at his Texas ranch after the central bank announced a half-point increase to its key discount rate over inflation fears, Bernanke writes. White House tapes, meanwhile, reveal President Richard Nixon frequently appealing to Fed Chair Arthur Burns’ Republican-party ties to clear the runway for more easy-money policies, with one call going as far as urging the Fed chair not to make any policy decisions that could “hurt us” in the November 1972 election.

I warned the Fed back then that buying in 30-year bonds during the 2007-2009 Financial Crisis, would NOT stimulate the domestic economy for one simple reason and this is why both the goldbugs and central bankers have been wrong. The domestic money supply DID NOT increase to stimulate when China was saying thank you very much and swapping their 30-year holdings for 10-year or less. The assumption that any central bank can control the domestic economy is absurd. The holdings of debt are global. Therefore, buying in 30-year bonds to reduce the supply in hopes of reducing the mortgage rates failed because the money did not stay in the USA. That is why the Fed then began to buy the mortgaged-backed securities because that was a more direct impact domestically.

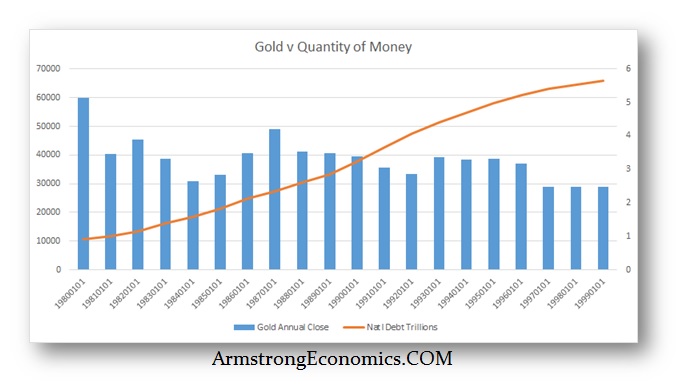

As the money supply increased and the national debt rose consistently, gold declined from 1980 into 1999 for 19 years. All the theories of inflation driving gold higher were simply wrong just as the central bankers relied on the very same theories.

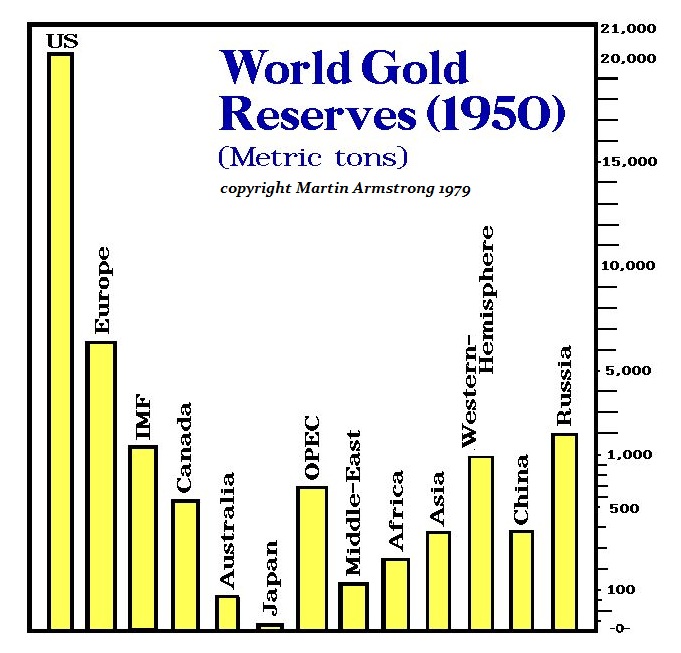

It was World War I and II that drove the gold to flee to the United States so by 1950, there was no choice but to make the dollar the reserve currency. Yet more significant was the realization that the factor which produced that result was ENTIRELY external to the domestic economy. Therefore, all the economic theories were bogus because they were all focused on domestic policy thanks to Karl Marx whose central theory was the government possessed the power to eliminate the business cycle by confiscating all private assets. That altered human nature and created economic stagnation. Nevertheless, Keynes and everyone else have sought to accomplish the very same authority that Marx maintained existed.

This focus on GDP (Gross Domestic Product) has reversed the GNP (Gross National Product), which was more global in its scope. If we attributed world trade to the flag the company flies rather than where it sets up a plant, then you would see that the United States has a trade surplus and not a trade deficit. This is also a backdrop to the reserve status of the dollar. Perhaps the greatest of all the wild proposals is that somehow Bitcoin will rise from the ashes and become the new Reserve Currency of the world. So all governments will issue debt in Bitcoin? Politicians will never be able to run for office and Socialism must collapse.

Rather than betting on the power grid to survive if governments collapse, I think we will see the pre-1965 silver coins return for a medium of exchange and gold for larger transactions. I have said plenty of times, GOLD will NOT rise as a hedge against inflation, it is a hedge against the collapse in confidence of the government.

As I have written before, when the Japanese government lost the confidence of the people, they lost the ability to produce any money for 600 years. The people used the coins of China and bags of rice – no Japanese coins were ever acceptable for 600 years which was the same time interval it took to reestablish gold in Europe following the fall of the Roman Empire.

Armstrong Economics Blog/Interest Rates Re-Posted Dec 14, 2022 by Martin Armstrongpread the love

The Central Bank Dilemma has become a major crisis in and of itself. I have been warning these past years that the ONLY tool a central bank has is manipulating the interest rates. Quantitative Easing was primarily to influence long-term rates indirectly since the Fed can only set short-term rates. During the past nine months, Fed Chairman Jerome Powell has raised interest rates at the fastest pace of any Federal Reserve chair since the 1980s. While some complain that this has triggered a stock market rout, and caused the housing market to come to a standstill, others argue that he has increased the fears of an imminent recession.

That was the domestic part. The Fed’s raising of interest rates has impacted the emerging markets including contributing to the chaos in the financial markets in China since many banks and provinces borrowed in dollars to save interest rates – or so they thought. It has forced the European Central Bank to raise interest rates and the net result was to unleash a crisis in long-term debt where life companies and pension funds cannot continue to buy the long-term with rates rising and bonds declining the day after you just bought a traunch.

Janet Yellen, who wants to hunt down everyone who sold a used bike on eBay for $600, understands the crisis we have erupting in debt because of rising interest rates and investors are afraid of the long end. Her proposal to buy in the long-term and swap it for the short-term recognizes the fact that we have a major debt crisis unfolding and she has come up with another scheme to keep kicking the can down the road.

Consequently, with inflation hitting 40-year highs, the warning signs are there that the central banks cannot do anything to address the economic crisis. Hence, initially, Fed officials were unanimous that rates needed to rise aggressively. Now, however, there are cracks in that view. These cracks will become fissures over how this type of inflation is NOT speculative but shortages set in motion by COVID and then accelerated by this drive for war with Russia and the insane sanctions they imposed on even private citizens.

While some expect inflation to cool steadily next year and want to stop raising rates soon, the problem is that inflation driven by shortages will not subside with a reduction in demand. Even real estate replacement costs have risen despite the fact that the market has started to pause. The cost to build a home in many areas is already higher than existing homes, which tends to create a floor before prices. Others worry inflation won’t ease enough next year in the face of a war that is escalating, and they defer to the old standard of raising interest rates to temper inflation.

That leaves Chairman Powell struggling in the eternal seas of politics lost in the middle as the arguments get louder on both sides. Powell will be challenged trying to chart a course through war, stagflations, and complete fiscal mismanagement by our politicians. The next stage of interest-rate policy presents very difficult questions concerning how high to raise rates from here, and how long to hold them at that level in this Pyhric War against Inflation.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America