I first had the idea of writing a book such as this about ten years ago. It seemed to me that each of us learns something of value as we go through life, but most of us do not succeed in passing along our knowledge to others before we die. This, then, is my attempt to pass on to others what I, over my fifty-odd years, have come to believe are the truths of life and what I believe may be a path into a better future. Much of what I write about involves economic issues, since I am an economist by training. Economics, however, is a social science, and my excursions into other areas of the social sciences are therefore not totally out of line.

I have had a great deal of “life” experience (both educational and professional) and this book thus covers many subject areas. While analyzing these subjects, I have tried to be logical and objective (as I have tried to be all my life), and hopefully this proclivity is reflected herein. You, the reader, will probably disagree with some or much of what I have written. That’s fine if your disagreement is based on fact; it’s unacceptable, however, if your disagreement is the result of prejudice and preconceived ideas. Throughout this book, I have included editorial writings, which I felt were astute, and which help to illuminate my ideas. In each case, I have credited the author and distinguished his/her writing from my own.

Much of what I write about could be construed as anti-religious; it is not. It has not been my intention to support or deny the existence of God or a Supreme Being. A thought that should be kept in mind when reading this book is that virtually nothing we do today is done as it was in the past. By this I mean the “near past”–remember that radio was invented only ninety-nine years ago, and it has been only ninety-one years since the first powered flight. Most of the technology that we now take for granted has been developed in the past fifty years. The corollary to this is that our ideas and attitudes must also be different from those of the past. Try to imagine how people will regard the “absurdly primitive” last decade of the twentieth century in the year 2045 (when all that we know today will have been gone for fifty years). The point is to keep an open mind, don’t pre-judge, and don’t be too certain about anything.

We live in a world of fantastic ideas if only we can keep an open mind!

The link below will allow you to download the book, if you want, and at no cost.

Posted originally on the CTH on September 22, 2024 | Sundance

Mike Rowe brought Victor Davis Hanson onto his podcast for an interview to discuss Class Warfare as contrast against the 2024 election stakes. The impetus for the interview was an article written by VDH a few months ago about the shift in the American electorate – SEE HERE.

Within the interview VDH walks through a summary of how a modern muscular tech industry replaced Mainstreet on the financial side of financial economics and American wealth. Essentially, how a small group of tech companies replaced the blue chip titans and industrialists on the global wealth scale.

As 8 billion people started being able to purchase the goods and services of a small American group of entrepreneurs, all focused heavily inside the tech and finance sector, the people who owned wealth shifted dramatically. Decades later, against the backdrop of globalism, the issue surfaces as the industrialists (Main Street corps) offshored their manufacturing, while the tech industrialists (Muscular Wall Street) started to be the wealthiest people in the USA as a result of selling their tech products to the world.

Within the discussion, the academically disposed VDH points out empirical data that bolsters his theories and analysis. Rowe is in general agreement as they both discuss the granular consequences. However, there is one fascinating part (prompted below) where VDH accurately identifies conservative economic hero Milton Friedman as one of the early globalist villains.

VDH is correct when he says that Friedman was a rabid open borders advocate, who had no issue with lowered wages for U.S. workers and embraced the global system of manufacturing which led to a destroyed U.S industrial base creating the Rust Belt. Few people on the conservative side of politics will ever admit how Milton Friedman was the original Bush-class economist. It’s good to see VDH set the record straight. WATCH:

Keep in mind, Milton Friedman was vociferously against tariffs of any kind. Friedman believed once the entire world was connected, all prices and economies would equalize. The pain felt within the American economy was simply something that had to be endured until American wealth was distributed and the entire world was balanced.

What follows below was my review of what would happen with Donald Trump policies put into place. This is very deep and in the weeds. This was originally written in December of 2016.

Traditional economic principles have revolved around the Macro and Micro with interventionist influences driven by GDP (Gross Domestic Product, or total economic output), interest rates, inflation rates and federally controlled monetary policy designed to steer the broad economic outcomes.

Additionally, in large measure, the various data points which underline Macro principles are two dimensional. As the X-Axis goes thus, the Y-Axis responds accordingly… and so it goes…. and so it has historically gone.

Traditional monetary policy has centered upon a belief of cause and effect: (ex.1) If inflation grows, it can be reduced by rising interest rates. Or, (ex.2) as GDP shrinks, it too can be affected by decreases in interest rates to stimulate investment/production etc.

However, against the backdrop of economic Globalism -vs- economic Americanism, CTH is noting the two dimensional economic approach is no longer a relevant model. There is another economic dimension, a third dimension. An undiscovered depth or distance between the “X” and the “Y”.

I believe it is critical to understand this new dimension in order to understand Trump economic principles, and the subsequent “America-First” economy his policies build.

As the distance between the X and Y increases over time, the affect detaches – slowly and almost invisibly. I believe understanding this hidden distance perspective will reconcile many of the current economic contractions. I also predict this third dimension will soon be discovered and will be extremely consequential in the coming decade.

To understand the basic theory, allow me to introduce a visual image to assist comprehension. Think about the two economies, Wall Street (paper or false economy) and Main Street (real or traditional economy) as two parallel roads or tracks. Think of Wall Street as one train engine and Main Street as another.

The Metaphor – Several decades ago, 1980-ish, our two economic engines started out in South Florida with the Wall Street economy on I-95 the East Coast, and the Main Street economy on I-75 the West Coast. The distance between them less than 100 miles.

As each economy heads North, over time the distance between them grows. As they cross the Florida State line Wall Street’s engine (I-95) is now 200 miles from Main Street’s engine (traveling I-75).

As we have discussed – the legislative outcomes, along with the monetary policy therein, follows the economic engine carrying the greatest political influence. Our historic result is monetary policy followed the Wall Street engine.

[…] there had to be a point where the value of the second economy (Wall Street) surpassed the value of the first economy (Main Street).

Investments, and the bets therein, needed to expand outside of the USA. hence, globalist investing.

However, a second more consequential aspect happened simultaneously. The politicians became more valuable to the Wall Street team than the Main Street team; and Wall Street had deeper pockets because their economy was now larger.

As a consequence Wall Street started funding political candidates and asking for legislation that benefited their interests.

When Main Street was purchasing the legislative influence the outcomes were beneficial to Main Street, and by direct attachment those outcomes also benefited the average American inside the real economy.

When Wall Street began purchasing the legislative influence, the outcomes therein became beneficial to Wall Street. Those benefits are detached from improving the livelihoods of main street Americans because the benefits are “global” needs. Global financial interests, investment interests, are now the primary filter through which the DC legislative outcomes are considered.

Here is an example of the resulting impact as felt by consumers:

♦ TWO ECONOMIES – Time continues to pass as each economy heads North.

Economic Globalism expands. Wall Street’s false (paper) economy becomes the far greater economy. Federal fiscal policy follows and fuels the larger economy. In turn the Wall Street benefactors pay back the politicians.

Economic Nationalism shrinks. Main Street’s real (traditional) economy shrinks. Domestic manufacturing drops. Jobs are off-shored. Main Street companies try to offset the shrinking economy with increased productivity (the fuel). Wages stagnate.

Now it’s 1990 – The Wall Street economic engine (traveling I-95) reaches Northern North Carolina. However, it’s now 500 miles away from Main Street’s engine (traveling I-75). The Appalachian range is the geographic wedge creating the natural divide (a metaphor for ‘trickle down’). By the time the decade of 2000 arrives – Wall Street’s well fueled engine, and the accompanying DC legislative attention, influence and monetary policy, has reached Philadelphia.

However, Main Street’s engine is in Ohio (they’re now 700 miles apart) and almost out of fuel; there simply is no more productivity to squeeze. From that moment in time, and from that geographic location, all forward travel is now only going to push the two economies further apart. I-95 now heads Northeast, and I-75 heads due North through Michigan. The distance between these engines is going to grow much more significantly now with each passing mile/month….

However, and this is a key reference point, if you are judging their advancing progress from a globalist vessel (filled with traditional academic economists) in the mid-Atlantic, both economies (both engines) would seem to be essentially in the same place based on their latitude.

From a two-dimensional linear perspective you cannot tell the distance between them.

It is within this distance between the two economies, which grew over time, where a new economic dimension has been created and is not getting attention. It is critical to understand the detachment.

Within this three dimensional detachment you understand why Near-Zero interest rates no longer drive an expansion of the GDP. The Main Street economic engine is just too far away to gain any substantive benefit.

Despite their domestic origin in NY/DC, traditional fiscal policies (over time) have focused exclusively on the Wall Street, Globalist economy. The Wall Street Economic engine was simply seen as the only economy that would survive. The Main Street engine was viewed by DC, and those who assemble the legislative priorities therein, as a dying engine, lacking fuel, and destined to be service driven only….

Within the new 3rd economic dimension, the distance between Wall Street and Main Street economic engines, you will find the data to reconcile years of odd economic detachment.

Here’s where it gets really interesting. Understanding the distance between the real Main Street economic engine and the false Wall Street economic engine will help all of us to understand the scope of an upcoming economic lag, which, rather remarkably I would add, is a very interesting dynamic.

Think about these engines doing a turn about and beginning a rapid reverse. GDP can, and in my opinion, will, expand quickly. However, any interest rate hikes (fiscal policy) intended to cool down that expansion -fearful of inflation- will take a long time to traverse the divide.

Additionally, inflation on durable goods will be insignificant – even as international trade agreements are renegotiated. Why? Simply because the originating nations of those products are going to go through the same type of economic detachment described above.

Those global manufacturing economies will first respond to any increases in export costs (tariffs etc.), by driving their own productivity higher as an initial offset, in the same manner American workers went through in the past two decades. The manufacturing enterprise and the financial sector remain focused on the pricing.

♦ Inflation on imported durable goods sold in America, while necessary, will ultimately be minimal during this initial period; and expand more significantly as time progresses and offshored manufacturing finds less and less ways to be productive. Over time, durable goods prices will increase – but it will come much later.

♦ Inflation on domestic consumable goods ‘may‘ indeed rise at a faster pace. However, it can be expected that U.S. wage rates will respond faster, naturally faster, than any fiscal policy because inflation on fast-turn consumable goods become re-coupled to the ability of wage rates to afford them.

The fiscal policy impact lag, caused by the distance between federal fiscal action and the domestic Main Street economy, will now work in our favor. That is, in favor of the middle-class.

Within the aforementioned distance between “X” and “Y”, a result of three decades traveled by two divergent economic engines, is our new economic dimension, which, if successful, will be forever known as “MAGAnomics”….

“We support reinstating the Glass-Steagall Act of 1933 which prohibits commercial banks from engaging in high-risk investment,” said the platform released by the Republican National Committee. (link)

What you just read above was written in December of 2016, before President Trump’s economic policies were put into place.

Compare what was stated, what was predicted, a completely new paradigm in American economic perspective, to what happened.

It was the Fourth Quarter of 2019…..

Right before the pandemic would hit a few months later, despite two years of doomsayer predictions from Wall Street’s professional punditry, all of them said Trump’s 2017 steel and aluminum tariffs on China, Canada and the EU would create massive inflation – it just wasn’t happening!

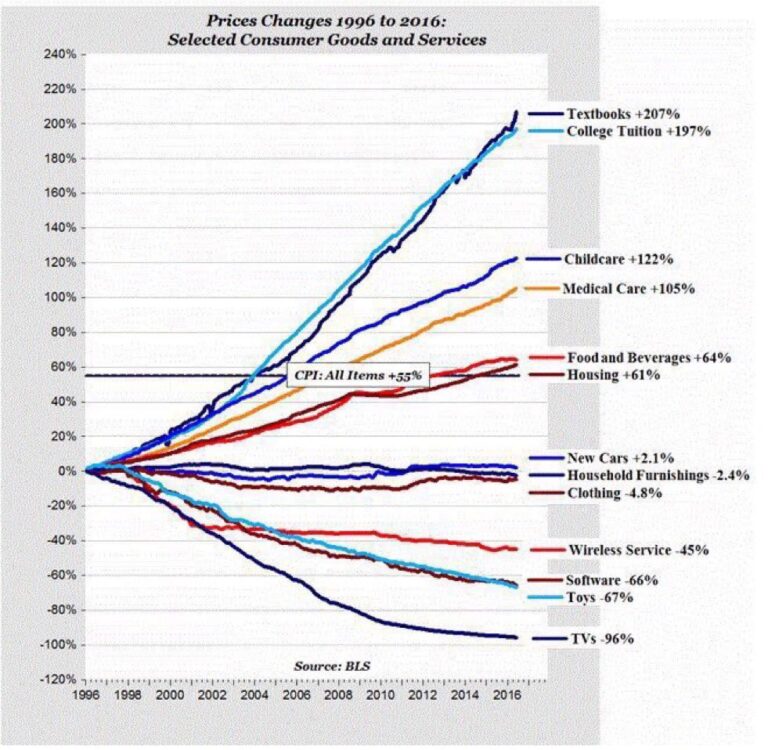

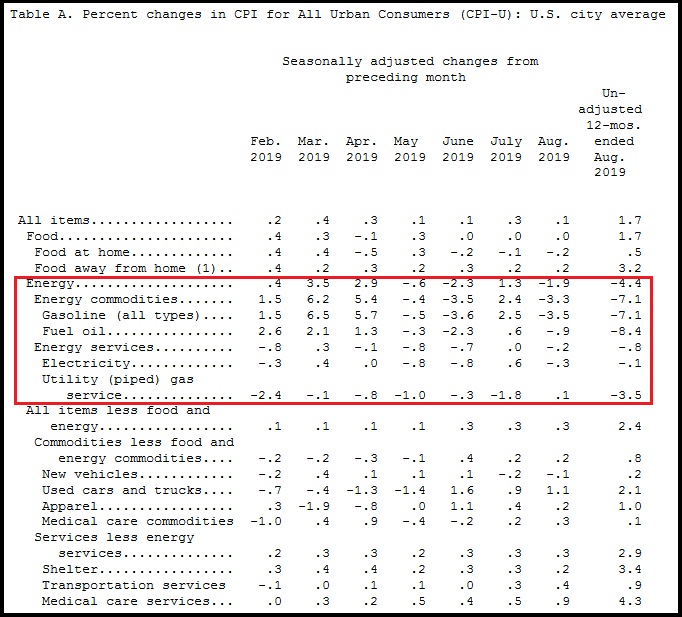

Overall, year-over-year inflation was hovering around 1.7 percent [Table-A BLS]; yup, that was our inflation rate. The rate in the latter half of 2019 was firmed up with less month-over-month fluctuation, and the rate basically remained consistent. [See Below] The U.S. economy was on a smooth glide path, strong, stable, and Main Street was growing with MAGAnomics at work.

A couple of important points. First, unleashing the energy sector to drive down overall costs to consumers, and industry outputs was a key part of President Trump’s America First MAGAnomic initiative. Lower energy prices help the worker economy, middle class and average American more than any other sector.

Which brings us to the second important point. Notice how food prices had very low year-over-year inflation – 0.5 percent. That is a combination of two key issues: low energy costs, and the fracturing of Big Ag’s hold on the farm production and the export dynamic:

(BLS) […] The index for food at home declined for the third month in a row, falling 0.2 percent. The index for meats, poultry, fish, and eggs decreased 0.7 percent in August as the index for eggs fell 2.6 percent. The index for fruits and vegetables, which rose in July, fell 0.5 percent in August; the index for fresh fruits declined 1.4 percent, but the index for fresh vegetables rose 0.4 percent. The index for cereals and bakery products fell 0.3 percent in August after rising 0.3 percent in July. (link)

For the previous twenty years, food prices had been increasingly controlled by Big Ag, and not by normal supply and demand. The commodity market became a ‘controlled market’. U.S. food outputs (farm production) was controlled and exported to keep the U.S. consumer paying optimal prices.

President Trump’s trade reset was disrupting this process. As farm products were less exported, the cost of the food in our supermarket became reconnected to a ‘more normal’ supply and demand cycle. Food prices dropped, and our pantry costs were lowered.

The Commerce Dept. then announced that retail sales climbed by 0.4 percent in August 2019, twice as high as the 0.2 percent analysts had predicted. The result highlighted retail sales strength of more than 4 percent year-over-year. These excellent results came on the heels of blowout data in July, when households boosted purchases of cars and clothing.

The better-than-expected number stemmed largely from a 1.8 percent jump in spending vehicles. Online sales, meanwhile, also continued to climb, rising 1.6 percent. That’s similar to July 2019, when Amazon held its two-day blowout Prime Day sale. (link)

Despite the efforts to remove and impeach President Trump, it did not look like middle class America was overly concerned about the noise coming from the pundits. Likely that’s because blue collar wages were higher, Main Street inflation was lower, and overall consumer confidence was strong. Yes, MAGAnomics was working.

Additionally, remember all those MSM hours and newspaper column inches where the professional financial pundits were claiming Trump’s tariffs were going to cause massive increases in prices of consumer goods?

Well, exactly the opposite happened [BLS report] Import prices were continuing to drop:

This was a really interesting dynamic that no one in the professional punditry would dare explain.

Donald Trump’s tariffs were targeted to specific sectors of imported products. [Steel, Aluminum, and a host of smaller sectors etc.] However, when the EU and China responded by devaluing their currency, that approach hit all products imported, not just the tariff goods.

Because the EU and China were driving up the value of the dollar, everything we were importing became cheaper. Not just imports from Europe and China, but actually imports from everywhere. All imports were entering the U.S. at substantially lower prices.

This meant when we imported products, we were also importing deflation.

This price result is exactly the opposite of what the economic experts and Wall Street pundits predicted back in 2017 and 2018 when they were pushing the rapid price increase narrative.

Because all the export dependent economies were reacting with such urgency to retain their access to the U.S. market, aggregate import prices were actually lower than they were when the Trump tariffs began:

[…] Prices for imports from China edged down 0.1 percent in August following decreases of 0.2 percent in both July and June. Import prices from China have not advanced on a monthly basis since ticking up 0.1 percent in May 2018. The price index for imports from China fell 1.6 percent for the year ended in August.

[…] Import prices from the European Union fell 0.2 percent in August and 0.3 percent over the past 12 months.

So yes, we know President Trump can save Social Security and Medicare by expanding the economy with his America First economic policy. We do not need to guess if it is possible or listen to pundits theorize about his approach being some random ‘catch phrase’ disconnected from reality. Yes folks, we have the receipts.

This was MAGAnomics at work, and this is entirely what created the middle class MAGA coalition. No other Republican candidate has this economic policy in their outlook, because all other candidates are purchased by the Wall Street multinationals.

America First MAGAnomics is unique to President Trump, because he is the only one independent enough to implement them.

That’s just the reality of the situation. They hate him for it…

Posted originally on Aug 29, 2024 By Martin Armstrong

When I was in high school history class, I had to read Galbraith’s The Great Crash. It was not until I came across a two-volume set of Herbert Hoover’s Memoirs that my eyes were pulled open. Nowhere in Galbraith’s book was there ever any mention of a 1931 Sovereign Debt Default because he was a Socialist, and the object of his book was to pin all the blame on corporations and the rich. He omitted everything that ever remotely pointed to the government as a cause. We should all own nothing, shut up, and be happy. Speak up, and today, you go to prison for Free Speech.

The conflict surfaced in my mind in high school. As I have said, in physics class they said nothing is random. Then in economics class, they said everything is random so government has the power to manipulate society and prevent recessions. That was a conflict to me that began my questioning of what I was being taught.

It is becoming painfully obvious schools are programming children for political agendas. This is very Stalinistic, for he, too, instructed children that the state was their parent and if their biological parents ever said anything against the state, they were to report them.

It has gotten far worse than when I was a kid. They were trying to brainwash us that the government is good and the corporate world is all evil. Today, that has gone into being gay, changing your gender, and not telling the parents like Stalin for the State is your parent. This is a movement to reduce the population to make Schwab, Gates, and Soros happy.

What does this all say? Today, if I had to start over, I would choose homeschooling.

“I named my computer model after Socrates because the oracle of Delphi had said that he was the smartest man in Greece. He tried to prove the oracle wrong and the process proved it to be correct. He was put on trial and sentenced to death because he knew too much. My computer has taught me a lot in geopolitics, we had a major bank in Lebanon in the 1980’s and they asked if I could create a model on the Lebanese pound. I put the data in the computer and it came out and said their country would fall apart in 8 days. I thought something was wrong with the data. When I told the client, they asked me what currency would be best, and I said the Swiss Franc. Eight days later the civil war begn. Obviously they saw the movement of money themselves and came to me for the timing. The same thing happened with a client in Saudi Arabia who was a big shipper. He called me asking me what gold would do tomorrow because Iran was going to begin attacking shipping in the gulf. So once again, there was advanced information about war. By 1998, I understood how the computer was forcasting such events. I warned in June at our London conference that Russia was about to collapse. The London financial Times had snuck into the back of the room and reported that forecast on the front of their newspaper on June 27th 1998. Russia collapsed about 6 weeks later.”

Posted originally on the CTH on January 1, 2024 | Sundance

In this outline I am going to expand on the details previously discussed {HERE}. You won’t find this in any financial media discussion, and there’s only a handful of people I know in the west who really understand the ramifications. Fortunately, one of them is running for President.

First some non-pretending context. If you are a Friedman-ite, finance major from any traditional academic institute – including Wharton, and/or a person who uses data models to frame analysis about economics and finance, without the capacity to put all of your traditional reference points in the trash heap of irrelevance, then just move along. We ain’t got time for that.

Consider Austan Goolsbee and Bill Ayers having dinner talking about what would happen if they successfully de-dollarized the globe. Austan comes at it from one perspective, Bill from another. Bernardine Dohrn smiles, because neither of the Chicago dinner guests has any idea what would really happen in this ideological landscape; no one really does.

I first sounded the alarm on this on March 2, 2022, almost two years ago {SEE HERE}.

In the ideological DoS/CIA/WEF/Western banking frenzy to punish the horrible Russia, I took a different approach. I overlaid the human factor with the geopolitical reality of financial control mechanisms. I predicted a cleaving outcome, because I carry no assumptions. That’s the context.

Additionally, I’m not coming at this situational analysis having relied on charts, graphs, trade analysis, Western finance systems or actuarial constructs of monetary manipulation by central bankers. Nope. I sat quietly inside small to medium-sized regional banks in Western Europe and listened to the reality of what businesspeople are doing, actually doing, in their operation of their enterprise as it relates to finance and Russia. {Go Deep}

This is where the razor’s edge outcome of the cleaving, the “yellow zone” -vs- “grey zone” construct, meets reality.

What we will witness this year will be one of the biggest stories of 2024 that will impact every American. However, few people will understand the information that will slowly trickle toward us, because too few people analyze information without historic assumptions.

When the “West” (yellow zone) triggered the sanction regime against Russia, almost no one took a big picture overlay and asked, “What about those nations who do not align with the Western intent; what will they do?”

Russia is not an enemy of the world; in fact, they have good relationships with China, Iran, India, multiple Middle East nations including Syria, Egypt and Saudi Arabia, and several Eastern European as well as African countries.

When the USA was walking away from the Arab Spring crisis Obama created, it was Russia who stepped in to help stop radicalization; just ask President Abdel Fattah al-Sisi.

Even NATO ally Turkey has an ongoing diplomatic and strategic friendship with Russia; that’s why Turkish Airlines operates as the best transportation company for travel into and out of Russia.

In fact, when the proverbial West triggered the sanctions against Russia, approximately one-third of the global GDP was not in alignment. A trade system that represents roughly 40% of all global production and trade (grey) can sustain a targeted enemy, while the 60% (yellow) allows complacency, hubris and delusions of grandeur to create an echo-chamber.

In essence, the “West” targeted Russia, but Russia had friends.

Those friendships expanded when the international fence-sitters saw how extreme and hateful the USA was going to be. How long before they, country xxxx might upset a USA administration? Who wants to be blackmailed by a similar targeted financial control system that the USA/EU and West triggered.

You might not think this Western sanction ‘shock value’ was a factor of importance, but two years later evidence suggests it was a much bigger deal than anyone was willing to admit.

De-dollarization is underway; failing to admit or accept this reality is akin to retaining a great pretense. The outcomes are only just now beginning to surface, and when we are trapped inside the Western zone, we cannot see, quantify or fully appreciate it.

India is trading with Russia in national currencies, not dollars. Iran and Russia are trading in national currencies, not dollars. China is trading with Russia in national currencies, not dollars. This process is expanding not shrinking, and it has huge outcomes.

If trades between nations are not contingent upon dollars, then less dollars need to be purchased. Less U.S. treasuries are purchased to back up the trade. Less dollar demand means lower dollar value. This process is only just beginning, and we cannot see it. The only way to see it is to step out of the yellow zone and look at the costs of goods and services in the grey zone.

Dollars are still in demand for anyone who wants access to the USA or EU market, so this de-dollarization process is limited in scale right now. But again, it’s expanding – meaning the demand for dollars is less.

Inside the Yellow Zone we cannot see the shift, but we can see the signs of a less demanded dollar in the prices of goods and services in the yellow zone. Inflation runs high in the Western zone as this devalued dollar begins to become more of an issue.

When we talk about “inflation” it is critical to keep in mind we are not ONLY talking about the price of goods. Yes, goods are one component to increased costs of living; however, financial service products like insurance costs (health, life, auto, homeowners etc.) are part of the equation where we see the inflationary impact of de-dollarization running amok. The financial services are closely related to the overall finance sector (think banking), so those skyrocketing costs hit first and become the precursor.

Next in the inflationary scale of impact comes the energy costs, which – as a direct and consequential outcome – transfer into the increased costs of goods, via packaging, processing, manufacturing, transportation, warehousing, etc. The overall business costs for insurance and financial services then aggregate with the energy cost impact and amplify the issue.

You can argue whether the current cost drivers or inflationary reality was a feature (intent) or a flaw (short-sighted outcome) of the western sanction regime, in combination with the intentional Build Back Better energy shift.

Austan Goolsbee might say it’s an accidental outcome, while a more radical communist like Bill Ayers says it was intended.

Personally, I think it was absolutely an intended feature, created to pave the way for a digital Western currency; that’s what it looked like in March 2022, and that’s what it still looks like today.

Regardless of intent, the reality is here…. barely visible right now, but here, and the de-dollarization is growing.

That opaque visibility is what I am talking about becoming much clearer in 2024. Eventually, people will start to ask questions about why the cost of products inside the yellow zone is so far out of sync with identical products and services inside the grey zone. {GO DEEP} The only way to see it, is to travel to both.

Now bring back the traditional Goolsbee economist thinking. If domestic prices continue rising (de-dollarization outcome), then domestic wage rates will need to rise in order for people inside the yellow zone to cope. Unfortunately, as Austan would lament, this dynamic becomes a self-fulfilling prophecy for even higher prices….

True… But why is Bernardine smiling?

“Maybe,” she says from the kitchen, as Austan squints and tilts his head with curiosity.

Bill smiles and replies, “I think she says ‘maybe’, because the surest way to avoid that dynamic is to import mass volumes of cheap low-skilled migrants as an offset.”

Austan looks even more curious as Bernardine says, “Yup, if ‘Western govt’ wants to align favorably with WEF corporate needs, then let the government give the corporations the means to avoid higher wages by allowing mass migration.”

Austan sits with jaw agape as Bill finishes the discussion and drops the mic. “If, for the sake of argument, that was indeed the plan, then specifically due to the nature of the USA dollar being the most severely impacted, it would be the borders of the USA that would need the highest rise in migrant crossings.”

Huh.

Go figure!

A.R ROBERTS …”I come here to the treehouse to get my morning dose of doom and gloom, lol. Everything I hear from SD and other alt-media people paints a very bleak picture. It’s like watching an 18-wheeler going down a steep grade with no brakes and no way to stop it. What you’re talking about SD is our imminent death at the hands of these insane inbred billionaire genocidal whackos. There seems to be no political solution to our situation. They will either terrorize us if we resist their death by a thousand cuts or drag us off to a Gulag or an extermination camp.

Tell me, please, what options do we have left? They have us boxed in and control an absolute police state. How about giving us some hope, some solutions?

I feel alone. Almost every “conservative” around me has their heads in the sand with bread and circuses. They think the stock market is doing great. They think everything is going back to normal. The libs in my family think anything is better than Trump in office. They are oblivious. They think I’m being a Chicken Little. It’s pretty damn depressing. Why should I stick my neck out to fight for any of these morons? It would almost be satisfying to watch them suffer from their ignorance if it wasn’t so tragic for the rest of us.”…

Instead of writing another article, I will show you the solution. At least what the solution should look like, albeit in a USA version. Let’s call it America First.

Economic nationalism. Make America Great Again, economically.

Stop the de-dollarization by Making Dollars Great Again!

Posted originally on Dec 21, 2023 By Martin Armstrong

QUESTION: Why do you seem to be the only analyst who understands central banking? My son got an internship at one of the major banks in New York during the summer. I won’t say which bank, but he asked a senior-level guy there about you and the interest rates, explaining I had been following you for years. He said you were the only one with international experience and who has ever advised multiple central banks. Is that the answer?

PK

ANSWER: Perhaps in part. But there is a massive gap between the experience of those of us who have dealt at high levels internationally and domestic analysts who always seem wrong calling the shots based on the headlines they read.

The number one problem is this fiction that the dollar is a fiat currency when, in fact, currency from the beginning of time has ALWAYS been valued NOT by its pure metal content but by who issued it. There has historically always been a premium to the currency of the dominant economy.

When Cyrus the Great conquered Lydia, he continued to strike coins of their design because they were highly regarded in international trade. We see the same with Roman coinage imitated in India when they, too, could have issued their own designs, but the Roman coinage carried a premium.

Even when the Barbarians were on the Northern frontier of Rome, they too took silver and struck imitations of Roman coins because they were worth more than the metal content. In 260AD, when emperor Valerian the Persians captured me, there was a Financial Panic of 260AD where bankers suddenly did not know if Roman coins would still be worth anything when there was no emperor.

While everyone claimed hyperinflation would engulf the world because of Quantitative Easing (QE), I warned there would be no such inflation. Indeed, with QE, there was no inflation, and people then developed the Modern Monetary Theory, claiming that they could increase the money supply and it would not result in inflation.

The entire problem rests with the fact that these people not only did not understand the role of money but also failed to grasp international capital flows and how they play into the world economy. Because you can now buy US TBills and place them as collateral to trade with at a brokerage house, the debt is simply money that pays interest. BEFORE 1971, it was illegal to borrow against government bonds. For you see, if you could borrow against the bonds, that meant the bonds were part of the REAL money supply.

Once debt became cash that paid interest, that changed economics forever. I have said over and over again the Fed is NOT the problem, and it can not stop inflation with interest rates. The REAL money supply if the national debt, so if the Fed buys-in 30-year bonds and creates cash to do so, it is NOT increasing the money supply; it is increasing the liquidity – that is all. Swapping cash for bonds does not change the balance sheet. If you buy a house for $100,000 and pay cash, then you have merely converted your cash into an asset.

Now, it all depends upon the buyer. If I have a building and sell it to a fellow American for $10 million, it does NOT alter the domestic money supply. However, if I sell it to Brit, he brings in cash to buy the property, and that DOES INCREASE the money supply BECAUSE he has imported $10 million that did not previously exist within the domestic system.

This is a very complex topic that only those of us in international finance ever encountered. I helped the Japanese reduce their trade surplus for political reasons. I had them buy gold in New York, export it to London, and sell it there. The trade statistics only count dollars in and dollars out – not the product. Buying gold and exporting it reduced the trade deficit, and nobody understood anything.

I handled a lot of the takeover boys during the 1980s when they made the move about Wall Street. They never understood what I was doing. The stocker was way undervalued when you could buy a company, sell its assets, and double your money. I took it to another level. I ran the model on currencies, and we would then buy like all the Courage Pubs in England but borrow in Swiss in a currency that would decline against the asset. We were making 20% on the currency moves besides the asset values. I was restructuring companies selling assets in one currency to buy assets in another to create balance hedge portfolios. That’s how I became friends with Maggie Thatcher. She wanted to know who this guy was sending companies into Britain.

Maggie was one of the few world leaders who grasped what I was doing. She kept Britain out of the EU because she understood what and how I was restructuring multinational companies. They staged a coup against here to take the pound into the Euro, then Soros attacked the overvalued pound in the ERM, and John Major had to reverse the entire mess, making Soros very rich in the process.

I will get around to doing my memoirs. I understand what I was doing set the stage for the world economy post-1971 Bretton Woods. That’s why Milton Friedman bothered to listen to my lecture about currencies in Chicago.

Posted originally on Dec 12, 2023 By Martin Armstrong

The Federal Reserve Bank of New York’s data shows that auto loans have surpassed student loans, becoming the second-largest debt burden for U.S. consumers. Auto loan debt has reached $1.582 trillion, exceeding the $1.569 trillion in student loan debt. This surge in auto loan debt is attributed to rising vehicle prices, leading consumers to take out larger loans at higher rates.

Lenders have responded to this trend by tightening restrictions on auto financing, with approximately 30% of lenders reporting significantly tighter lending standards. The pressure for companies to switch to EVs and inventory shortages have contributed to the increase in vehicle pricing, resulting in consumers financing more expensive vehicles.

At the same time, the government is moving full speed ahead to reach their target of 50%+ EVs by 2030. Thousands of auto dealers have penned the Biden Administration to explain how this policy is significantly hurting their business. The public is drowning in debt over mostly gas-powered purchases, and EVs are significantly more expensive to purchase and maintain. Car manufacturers are focused on producing cars of the future rather than autos that fit the budget and lifestyle of the middle class.

Bidenomics believes student debt should be waived for those who knowingly took on the debt. Will those supporting Bidenomics also push to forgive this mounting auto debt? Like diplomas, people may realize their EVs cost more than they’re worth and they cannot keep up the payments. Perhaps the public, including those who do not own cars, should subsidize these car purchases through taxes since that is the same premise as student loan forgiveness.

The World Economic Forum is in partnership with global governments to end private car ownership by 2050. Owning a car is becoming an increasing luxury. Insurance costs could be a topic for another time as most states have seen their premiums skyrocket. Major cities around the globe like London and New York City are implementing congestion and traffic taxes as well.

Decades ago, someone could purchase a nice car with less than a month’s pay. Kelly Blue Book states thatthe average price of a new car was $48,008 as of March 2023, which is 27.8% more than pre-COVID pricing. The average cost of a crossover or SUV now ranges between $30,353 and $74,502, with costs rising by over 6% every year since 2020. We will see car ownership become an increasing luxury.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America