Posted originally on Mar 7, 2024 By Martin Armstrong

Those who follow this blog already knew that the Federal Reserve would not drop rates in the future due to unsustainable fiscal policies paired with America’s increasing involvement in foreign wars. All of the talking heads were preaching that rates would significantly decline to pandemic levels, as if that were the historical norm. Every fiscal policy in recent years has exacerbated inflation and the Fed cannot keep up with government spending. QE FAILED. The artificially low interest rates of the recent past were completely unsustainable and relied on outdated theories.

The outdated understanding based on Keynesian Economics remains to increase the supply of money and it MUST be inflationary. The Fed raises rates to reduce consumption and lower rates to stimulate consumption. It’s a very nice theory, but when actually tested, it utterly fails. Lower rates will NEVER cause people to invest UNTIL they believe that there is an opportunity to invest. We are watching the big players withdraw from equities, let alone government debt. We are in a private wave where money is running off the grid at a rapid pace.

The peak in interest rates took place in 1899 at virtually 200%. Yet, 1929 was the real bubble top and it peaked with 20% interest rates in call money on the NYSE. In theory, the biggest boom should have been met with the highest interest rate. In truth, the “real interest rate” as I have defined it is when the interest rates exceed expectations. If you think the stock market will double, you will pay 25% interest.

As you can see, while interest rates hit nearly 200% in 1899, the share market did NOT crash percentage-wise anything as it did following 1929. Look, there is a lot more to this than meets the eye. Everything must be addressed on a global scale for it all depends also on the direction of capital flows. There is just a lot more to this than simply the money supply and interest rates.

Now, Powell continues to explain to the public that VOLATILITY and economic conditions are beyond the control of the Fed. “We believe that our policy rate is likely at its peak for this tightening cycle,” Powell said. “If the economy evolves broadly as expected, it will likely be appropriate to begin dialing back policy restraint at some point this year. But the economic outlook is uncertain, and ongoing progress toward our 2% inflation objective is not assured.”

All the news ofinflation waning, including recent data, is inaccurate propaganda intended to calm recessionary fears. Even by the government’s data, inflation is up 3.1% compared to last year. It was an unprecedented moment when Powell broke with Washington and criticized the government for their unsustainable spending. The Fed NEVER criticizes the government, despite the two being separate.

Hence, I say to stop blaming the Fed. They are not the ones creating all the money but are working to match monetary policy with unsustainable fiscal policies. We are looking at trillions in deficits per year. There is no restraint when creating new massive spending packages. Then people blame the central bank with no concept that it’s only a fraction of “money;” the real issue is CONGRESS.

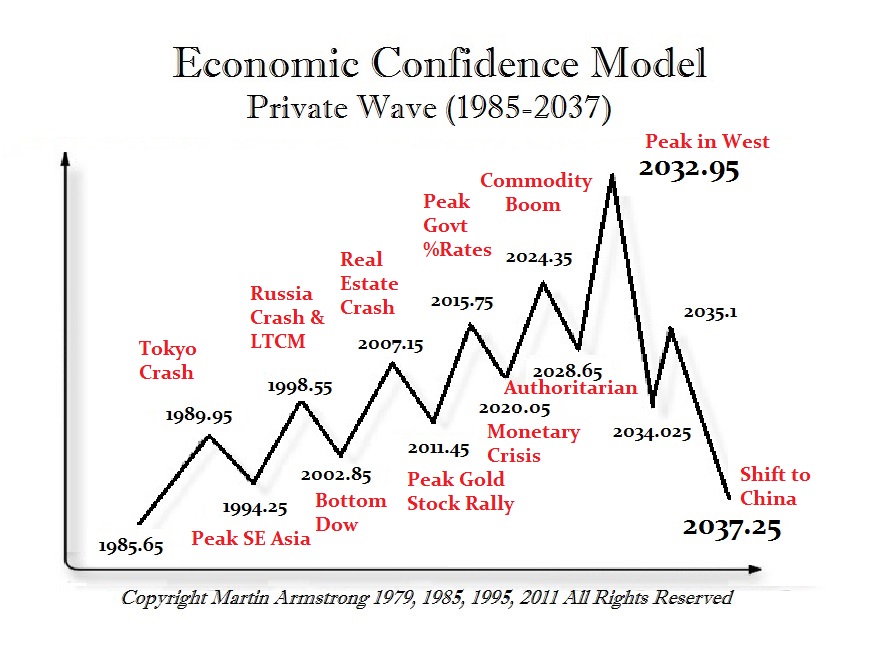

Listen, interest rates cannot decline in the face of war. The 2020 yearly array showed a turning point for a high in 2022 and a possible correction into 2024. I explain this in more detail on the Socrates private blog but buckle up for the year ahead.

In 2019, New York hosted 72 billionaires. That figure has declined to 62 in 2023, with smart money fleeing the state due to high taxes and crime. The state of New York depends on the top 1% of earners to pay 42% of its tax burden. New York is already operating in a deficit and has the added burden of hosting tens of thousands of migrants with tax funds.

The top 1% of Americans have an average net worth of $10,815,000. While billionaires earn on investments and not income, states like New York expect top earners to pay 14.8% in income tax. “If you had someone who was earning $100 million [a year] in New York suddenly move to Florida, that’s something like a $11 million-a-year hit per year recurring to the state,” said Ken Girardin, the research director for the Albany-based think tank, Empire Center for Public Policy. The 62 billionaires that remain in New York have a collective net worth of $562.3. Only the top 5% of Americans have a net worth of over a million dollars.

Inflation is hurting those at every class level and people do not want to downgrade their lifestyles. Policymakers want to scream “Eat the rich!” to appease voters who do not understand that the money held by those at the top is needed for a healthy economy. In 2020 alone, when the pandemic struck, New York lost $19.5 billion in taxes from people fleeing the state. California lost $17.8 in tax revenue that year and counting.

We are seeing a wealth migration in the US. This is why I say that markets like real estate cannot be looked at on the national level, as prices in red states continue to rise as blue states have become uninhabitable. This is only taking into consideration individuals as moneymakers are also taking their businesses to states where they do not need to support the welfare system. Around 160 firms have fled Wall Street since 2019, displacing $1 trillion.

Hence, people are saying Miami is the new Wall Street. Lawmakers do not comprehend the impact that this will have on state budgets.

This is precisely what happened prior to the collapse of the Roman Empire. The top 1% half 16% of the empire’s wealth. Wealthy Romans were the first to leave cities when public confidence collapsed. We can see the migration from archaeological finds that saw villas built far from city centers. And even in those days, people felt that the wealthy were selfish for acting in accordance to the invisible hand. As noted in “The Decline and Fall of the Roman Empire” by James William Ermatinger: “Their disinclination to leave may have been caused by forced exactions, confiscations, business concerns, tax pressured, or general economic fears, which made protecting one’s own interests seem more prudent than looking out for the interests of others.”

Rome’s Sovereign Debt Crisisis what ultimately led to its collapse. Yet one of the first signs of major trouble was the mass exodus of wealth from the cities.

QUESTION: Looking at Socrates, do you think that these people who were constantly calling for a recession because there were two quarters that declined with covid really need revision? Socrates was correct, no recession. But it is showing major turning points in 2024 which seem to align with your old ECM forecast calling for commodity inflation into 2024. How would you define a recession?

EJ

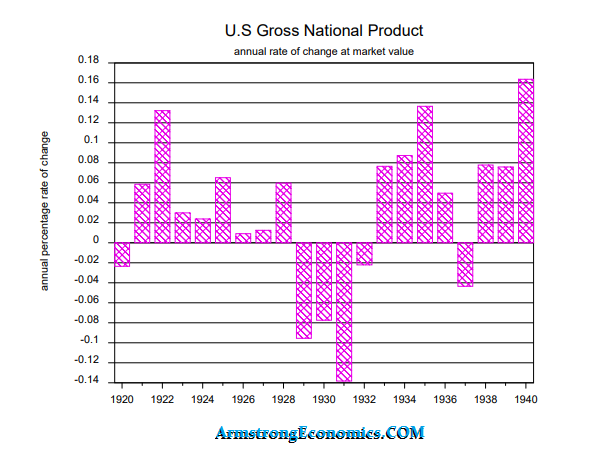

ANSWER: In trading, reactions are 1 to 3 time units. I believe that the same definition should be used for classifying a recession. They define a recession as two consecutive quarterly declines. If you look at the “Great Recession” of 2008-2009, you will see three consecutive quarterly declines and a rebound. If we look at the COVID recession caused by locking everyone down, that was just two consecutive quarterly declines.

I personally would argue that a true economic recession MUST exceed three consecutive declines. Here is the chart of GNP from 1929 to 1940. There were three years of negative growth. I simply think that this definition of two quarters is wrong. You can have a slight decline of 1 to even 5%, but that does not suggest a recession. In the case of 1929, that was a decline of 9.5% in 1930 – the first year. Now look at the COVID Crash, which was also a decline of 9.53%. But the difference is that the COVID decline was forced and not natural. That is why it rebounded so quickly. Now the so-called “Great Recession” of 2008-2009 only saw a decline in GDP of 3.47%.

The “Great Recession” was not really so great. It wiped out real estate and bankers but did not fundamentally alter the economy. So who is right and who is wrong will always depend upon the definition. Yes, the AI Timing Arrays point to a recession starting Next Year by their definition. This will most likely be caused by the decline in confidence that will lead to UNCERTAINTY, and as such, the consumer will contract. Up to now, the continued expansion of the economy into 2024 has also been fueled by the shift in assets from public to private.

As originally forecast, we should have seen a commodity boom into 2023,

and we should expect a highly authoritarian attempt by 2028.

Posted originally on the CTH on July 3, 2023 | Sundance

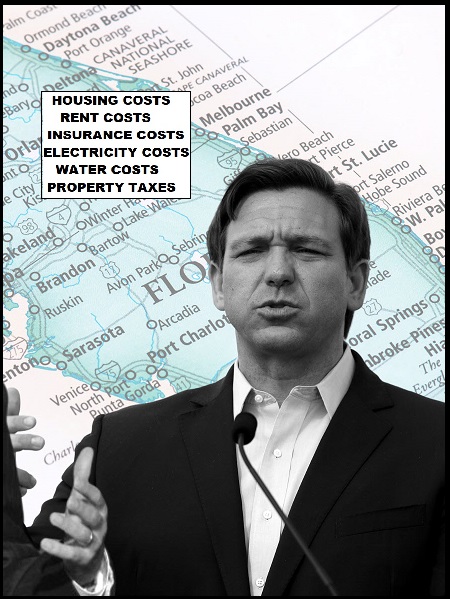

As if carrying Homeowners insurance in California and Florida wasn’t already subject to ridiculous increases in premiums, things are about to get a lot worse.

Effective with the July 1st notification, Reinsurance rates, these are companies who insure the insurance companies, are telling their clients there will be up to a 50% increase in cost for underwriting catastrophic coverage. Perhaps claims in the past few years have been higher; however, I suspect the issue amid the reinsurers is partly connected to the issue that surrounds banks and bond rates.

Back when interest rates were near zero, banks and reinsurers likely scooped up lots of Treasuries and bonds. As the Federal Reserve hikes rates those bonds have declined in value. When interest rates rise, newly issued bonds start paying higher returns to investors, which makes the older bonds with lower rates less attractive/valuable. The result is that most banks, and I suspect big reinsurance houses, have some amount of unrealized losses on their books.

Whatever the reason, the big reinsurance companies are now telling the insurance carriers their catastrophe rates are going up as high as 50%. Those insurance companies will then pass those rate hikes to the individual policy holders for commercial buildings, residential homes, cars, RV’s etc. Bottom line, homeowner insurance rates are about to go up again with policy renewals, especially in Florida and California.

LONDON, July 3 (Reuters) – U.S. property catastrophe reinsurance rates rose by as much as 50% at a key July 1 renewal date, broker Gallagher Re said in a report on Monday, with states such as California and Florida increasingly hit by wildfires and hurricanes.

Reinsurers insure insurance companies, and have been raising rates in recent years because of steepening losses, which industry players put down in part to the impact of climate change. Higher reinsurance rates can affect the premiums which insurers charge to their customers.

U.S. reinsurance rates for policies which previously faced claims for natural catastrophes rose 30-50%, Gallagher Re said.

Reinsurance rates for similar policies in Florida rose 30-40%, the broker added.

Some insurance firms have pulled out because of the risk of heavy losses. State Farm said in May it would stop selling new insurance policies to homeowners in California.

In Florida, “all the major carriers (insurers) left and so you ended up with this market which is populated by a large number of very small, very thinly capitalised insurers which is exactly what you don’t want,” James Vickers, chairman international, reinsurance, at Gallagher Re told Reuters. (keep reading)

In Florida specifically, homeowners insurance costs have now generally risen higher than the mortgage payment for a middle-class family. This is not sustainable.

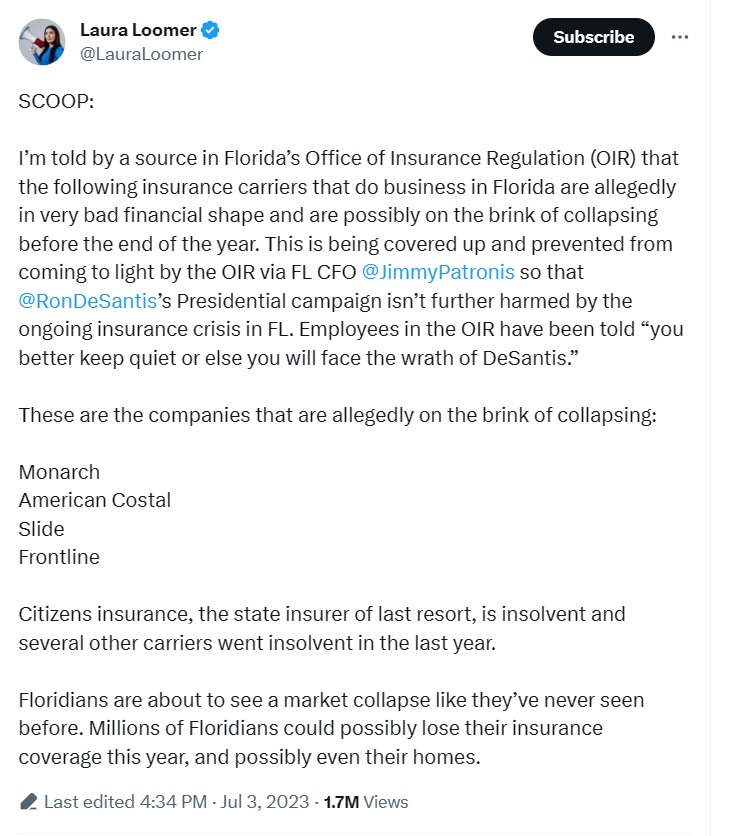

SCOOP:

I’m told by a source in Florida’s Office of Insurance Regulation (OIR) that the following insurance carriers that do business in Florida are allegedly in very bad financial shape and are possibly on the brink of collapsing before the end of the year. This is being covered…

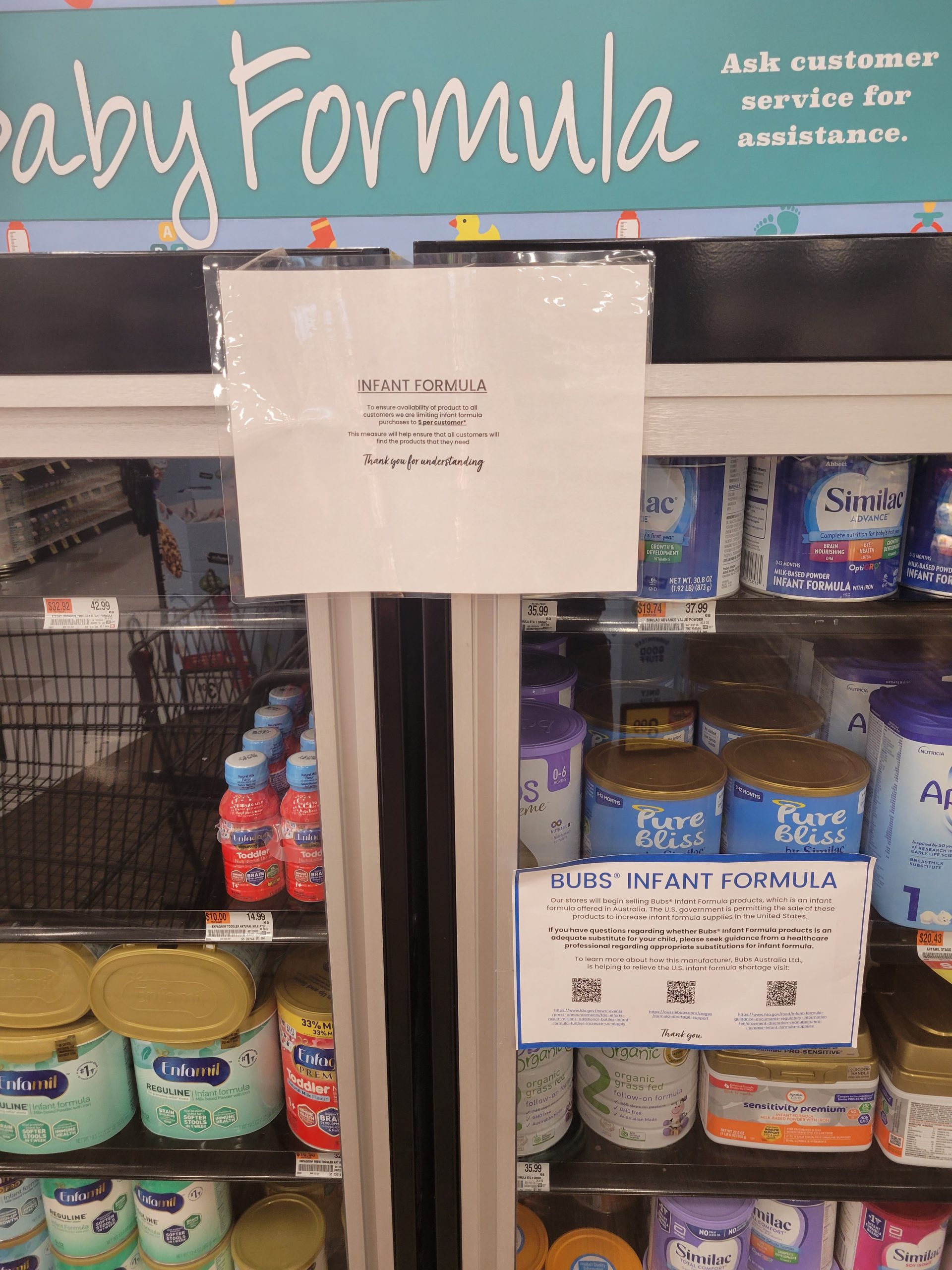

COMMENT: Hello Mr. Armstrong. Thank you for my daily dose of reality. Your blog is one of the last sources of untainted news. I would like to show these pictures my daughter sent me last week. We live in an affluent neighborhood in New Jersey where petty theft does not occur. The news outlets have not mentioned baby formula shortages. I do not believe they are locking up the baby formula to prevent crime. What is going on here?

Thanks — C.G.

REPLY: The supply chain issue has never been resolved. It improved from the days of bare shelves in the grocery stores, but many essentials are stuck in the pipeline. Products that expire will see additional shortages naturally. The supply shortage is fueling inflation and raising rates will not solve the problem.

The Fed thinks that raising rates will curb inflation by raising the cost of borrowing. That is not the problem here. Part of the inflationary crisis we are witnessing is due to demand outweighing available supply across industries. The Fed cannot control government spending nor the money supply. People are viewing the crisis today from the perspective of the ‘60s when it was NOT possible to borrow on T bills. After the collapse of Bretton Woods in ’71, you COULD trade off government debt and that eliminated the idea that it was less inflationary to borrow rather than spend. Artificially low rates that created a borrowing addiction among institutions who believed it was safe to do so.

Powell cannot come out and criticize Congress for their spending. These rate hikes are not good for the supply chain shortages. Inflation went up two years before the Fed even addressed rates due to the supply chain crisis. The central bank only began to hike rates after the war in Ukraine began. Notice how at the last meeting, the FOMC incorporated that they will monitor “international events.” WAR is the primary driver of inflation and there is nothing that the central bank can do to prevent the destruction caused by government and years of poor monetary policy.

(image above represents shrinkflation — an additional burden to consumers)

Italy’s Industry Minister Adolfo Urso called for an emergency meeting to discuss the sharp uptick in food prices. Pasta alone is up nearly 20%, and this is a major problem in a country where 60% of residents report eating this item daily. Some provinces are seeing a 58% increase in this staple item. Siena, Tuscany, reported pasta rising from $1.50 a kilo to $2.37 a kilo within in a year. The European Central Bank stated that inflation reached 8.1% in March, so what is driving these food prices?

Some may point to wheat, the main ingredient, as the recent usurping of farmland and the Ukraine war had an impact on prices. However, wheat prices have actually declined in recent months. Durum wheat is down 30% since May of last year. The only other ingredient required to make pasta is water.

Coldiretti, Italy’s biggest farmers association, said that farmers are not seeing an uptick in revenue and are struggling to make ends meet. “There is no justification for the increases other than pure speculation on the part of the large food groups who also want to supplement their budgets with extra profits,” Assoutenti president Furio Truzzi told the Washington Post. Yet, food manufacturers are claiming that this spike in pasta costs in temporary and a result of pasta produced during the beginning of the Ukraine war and energy crisis.

This is not the first time that Italy has seen a rise in food prices. Italian authorities raised 26 pasta manufacturers in 2009 and fined the industry 12.5 million euros for creating what Reuters described as a “pasta cartel.”Around 90% of pasta makers in the country were in on the price gouging scheme that operated from May 2006 until May 2008, during which pasta prices rose 51.8% for retailers and 26% for consumers. Barilla, the largest pasta producer at the time, received the largest fine of 5.7 million euros.

Food inflation is a major problem across the world. In Italy, overall food prices rose 12.6% in April 2023, marking a slight decline from March’s 13.2% reading. This is unsustainably high. The overall inflation numbers put forth by government agencies are always the best-case scenario as they do not want us to see the true damage of inflation.

Posted originally on the CTH on May 1, 2023 | Sundance

Everything about the process of cutting down energy exploitation, then driving supply side inflation, then raising interest rates to shrink demand (stem inflation) created by a desire to lower economic activity to the scale of diminished energy production, is a game of pretending.

The collateral damage from the rate hikes has been the banking destabilization, which shows the priority of the government officials and central banks to support the climate change agenda. Into the game of pretending comes the second unavoidable consequence with inflation continuing as a result of the energy policy.

They simply cannot cut energy demand enough to meet the diminished scale of production. There is no alternative ‘green’ energy system in place to make up the difference. That is the reality. Now, the fed is scheduled to raise rates again, then begin to debate the collateral damage as they continue the pretending game.

(Via Wall Street Journal) – […] Another quarter-percentage point increase would lift the benchmark federal-funds rate to a 16-year high. The Fed began raising rates from near zero in March 2022.

Fed officials increased rates by a quarter point on March 22 to a range between 4.75% and 5%. That increase occurred with officials just beginning to grapple with the potential fallout of two midsize bank failures in March.

The sale of First Republic Bank to JPMorgan Chase & Co. by the Federal Deposit Insurance Corp. announced early Monday is the latest reminder of how banking stress is clouding the economic outlook.

Fed officials are likely to keep an eye on how investors react to that deal ahead of Wednesday’s decision, just as they did before their rate increase six weeks ago when Swiss authorities merged investment banks UBS Group AG and Credit Suisse Group AG. (read more)

There is no other way to look at the combined policy without seeing a Central Bank Digital Currency (CBDC) in the future. All of these combined policies are creating a self-fulfilling prophecy.

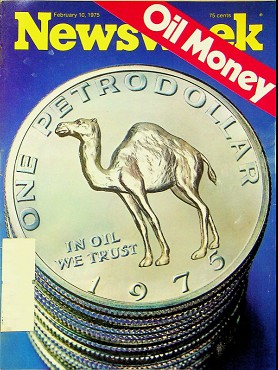

All we hear is the same claims that the dollar is dead and it will be totally worthless any day now. Over the last few weeks, all we hear from the majority now is that the dollar is finished. Virtually every page you turn or site you visit claims the death of the dollar. They are calling this the de-dollarization of the world economy and that the future of the US dollar as well as the American empire itself is now collapsing. The general claim is that the group of economically-aligned nations known collectively as BRICS is a major threat to the greenback. That was the same story we heard about the Euro back in 1997.

As their scenario goes, the BRICS [Brazil, Russia, India, China, and South Africa] have moved to form an anti-dollar colation and Saudi Arabia is considering jumping on board. They insist that once that happens, the “petrodollar” will die and cease to be a reserve currency.

This is then followed by the forecast that the economy will suffer and that any bounce in exports will be short-lived simply because the dollar will be dead for the long term. Of course, this has been the favorite forecast that they keep putting out since Bretton Woods collapsed. They were wrong back then for the dollar rose between 1972 and 1976 against the British pound, with the collapse of Bretton Woods. To try to explain why the dollar did not collapse, that is when they claimed that the dollar was backed now by oil rather than gold. That was just an excuse as always to cover up their wrong forecast.

They sold that story to Newsweek and now the dollar rally was because of oil which replace gold. Suddenly the dollar became de facto backed by oil. They needed an explanation to explain why all the old theories were wrong. They sold this theory and it made the front cover of Newsweek. Everyone said YES! That must be the reason. OPEC priced oil in dollars! Naturally, everything was priced in dollars because, under the fixed exchange rate of Bretton Woods, everything from wheat and corn to copper and gold was all priced in dollars.

Now they are saying the American empire is threatened by the potential commercial real estate collapse and the BRICS anti-dollar venture. So they are forecasting a great depression-style crash is possible in the not-too-distant future. They spin this to forecast the end of the America Empire. The London FT, always anti-American/Pro WEF, reports that the dollar as a reserve currency has declined from 73% in 2001 to around 55% by 2021. Yet the FT did state an obvious fact:

“But if you are a reserve-rich central bank elsewhere that isn’t going to be a lot of comfort. Moreover, would you really feel more comfortable in, say, the renminbi? Even if it was fully convertible and liquid, would you honestly feel more sure that Beijing will behave lawfully than DC? The dollar still looks like the proverbial least dirty shirt in the closet.”

COVID actually has played a major role in shifting the world economy. In 2020, the US economy was 24.75% of the world’s GDP. By the start of 2022, it had fallen marginally to 24.15%. What these dollar-forecasting jockeys do not understand, is that if they were correct and the dollar collapsed, then the very BRICS would collapse even further. Economically speaking, when the United States gets a head cold, the rest of the world catches ammonia. You can’t have it both ways. The strength of the dollar is not gold or oil, it is the American consumer.

The risk to the entire world is runaway inflation thanks to Biden pouring untold amounts of money into the black hole known as Ukraine. The Neocons, who control Biden, are planning to launch a war against Russia and China before 2024. This will only continue to accelerate inflation. That reduces the spending power of the American consumer and in the process, the US economic growth declines in real terms and with it, the rest of the world plunges into recession.

While Macron has figured it out that the Neocons are in charge of US foreign policy and he is telling Europe to stop being the puppet of the USA, that all sounds nice but Europe is marching into war with Russia. NATO is firmly in control of the American Neocons and they need war or face losing power. With Trump in the lead, they must stop him at all costs for he is anti-war, would haul the Neocons out by the necks, and defund NATO, as well as stop the climate change agenda.

The US dollar in the global economy has been supported by the size and strength of the US consumer-based economy. Its stability and openness to trade and capital flows without restrictions and it has never been canceled, are the major foundation of the dollar in addition to strong property rights and the rule of law. That is why Russians and Chinese buy US property for they are secure in their ownership of US property which cannot always be guaranteed outside the US.

Consequently, the depth and liquidity of US financial markets remain unmatched. For institutions parking billions, the United States represents a large supply of extremely safe dollar-denominated assets. Are they really going to switch to China or buy debt from Brazil? Not a single institutional client will take that bait.

China has been divesting of dollar reserves because it KNOWS that the American Neocons want war. You do not fund your adversary who intends to wage war against you. China cannot shift reserve assets to Europe or Japan. They have been buying gold because it is geopolitically neutral territory. They are NOT buying gold as an investor thinking it will rally. That is irrelevant. If gold drops 25%, that does not translate into them becoming a seller.

The dollar in international reserves stood at 60+% at the start of 2022 against the US share of GDP at 24.25%. This comparison belittles the argument that the dollar is finished. Eventually, the US will lose the wars it is starting and the dollar will be replaced perhaps as soon as 2028. The IMF is already licking its lips and rubbing its hands together eager to get control of the reserve currency. But they too will collapse. We have a Directional Change next year and a Panic Cycle in 2025. So buckle up.!

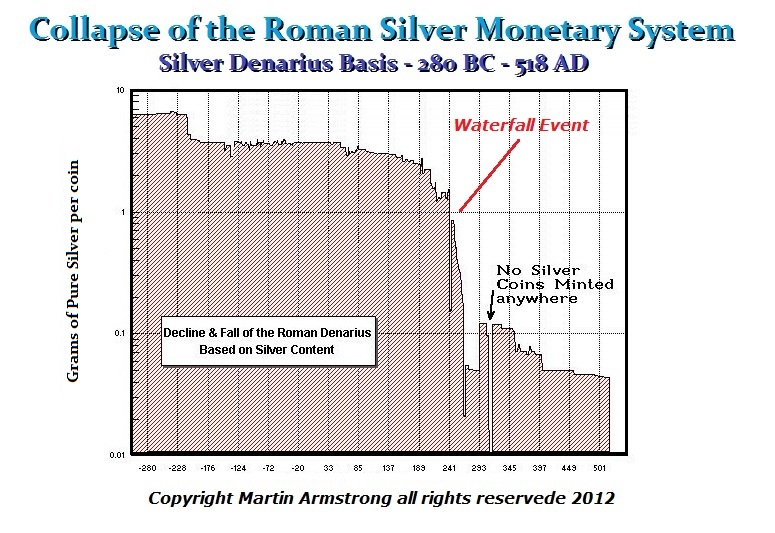

Remember one thing, even with the debasement and collapse of the Roman Denarius between 260AD and 268AD, it still took 224 years for Rome to completely collapse. When war breaks out, capital flight will still be to the dollar. It will not be to public assets, but private. The United States is still supporting the entire world economy. The BRICS need the US consumer to keep their economies functioning. All this talk of the dollar being finished is really nonsense. That day will come, but when the US consumer no longer buys.

Remember 1997? The Euro was going to dethrone the dollar. They claimed the new EU will be a bigger economy than the US. The problem was, they lacked a consumer economy, and low taxes, and they routinely canceled their currency to force people to pay taxes. It is always the same story over and over again.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America