Posted originally on Dec 21, 2023 By Martin Armstrong

QUESTION: Why do you seem to be the only analyst who understands central banking? My son got an internship at one of the major banks in New York during the summer. I won’t say which bank, but he asked a senior-level guy there about you and the interest rates, explaining I had been following you for years. He said you were the only one with international experience and who has ever advised multiple central banks. Is that the answer?

PK

ANSWER: Perhaps in part. But there is a massive gap between the experience of those of us who have dealt at high levels internationally and domestic analysts who always seem wrong calling the shots based on the headlines they read.

The number one problem is this fiction that the dollar is a fiat currency when, in fact, currency from the beginning of time has ALWAYS been valued NOT by its pure metal content but by who issued it. There has historically always been a premium to the currency of the dominant economy.

When Cyrus the Great conquered Lydia, he continued to strike coins of their design because they were highly regarded in international trade. We see the same with Roman coinage imitated in India when they, too, could have issued their own designs, but the Roman coinage carried a premium.

Even when the Barbarians were on the Northern frontier of Rome, they too took silver and struck imitations of Roman coins because they were worth more than the metal content. In 260AD, when emperor Valerian the Persians captured me, there was a Financial Panic of 260AD where bankers suddenly did not know if Roman coins would still be worth anything when there was no emperor.

While everyone claimed hyperinflation would engulf the world because of Quantitative Easing (QE), I warned there would be no such inflation. Indeed, with QE, there was no inflation, and people then developed the Modern Monetary Theory, claiming that they could increase the money supply and it would not result in inflation.

The entire problem rests with the fact that these people not only did not understand the role of money but also failed to grasp international capital flows and how they play into the world economy. Because you can now buy US TBills and place them as collateral to trade with at a brokerage house, the debt is simply money that pays interest. BEFORE 1971, it was illegal to borrow against government bonds. For you see, if you could borrow against the bonds, that meant the bonds were part of the REAL money supply.

Once debt became cash that paid interest, that changed economics forever. I have said over and over again the Fed is NOT the problem, and it can not stop inflation with interest rates. The REAL money supply if the national debt, so if the Fed buys-in 30-year bonds and creates cash to do so, it is NOT increasing the money supply; it is increasing the liquidity – that is all. Swapping cash for bonds does not change the balance sheet. If you buy a house for $100,000 and pay cash, then you have merely converted your cash into an asset.

Now, it all depends upon the buyer. If I have a building and sell it to a fellow American for $10 million, it does NOT alter the domestic money supply. However, if I sell it to Brit, he brings in cash to buy the property, and that DOES INCREASE the money supply BECAUSE he has imported $10 million that did not previously exist within the domestic system.

This is a very complex topic that only those of us in international finance ever encountered. I helped the Japanese reduce their trade surplus for political reasons. I had them buy gold in New York, export it to London, and sell it there. The trade statistics only count dollars in and dollars out – not the product. Buying gold and exporting it reduced the trade deficit, and nobody understood anything.

I handled a lot of the takeover boys during the 1980s when they made the move about Wall Street. They never understood what I was doing. The stocker was way undervalued when you could buy a company, sell its assets, and double your money. I took it to another level. I ran the model on currencies, and we would then buy like all the Courage Pubs in England but borrow in Swiss in a currency that would decline against the asset. We were making 20% on the currency moves besides the asset values. I was restructuring companies selling assets in one currency to buy assets in another to create balance hedge portfolios. That’s how I became friends with Maggie Thatcher. She wanted to know who this guy was sending companies into Britain.

Maggie was one of the few world leaders who grasped what I was doing. She kept Britain out of the EU because she understood what and how I was restructuring multinational companies. They staged a coup against here to take the pound into the Euro, then Soros attacked the overvalued pound in the ERM, and John Major had to reverse the entire mess, making Soros very rich in the process.

I will get around to doing my memoirs. I understand what I was doing set the stage for the world economy post-1971 Bretton Woods. That’s why Milton Friedman bothered to listen to my lecture about currencies in Chicago.

Posted originally on Dec 12, 2023 By Martin Armstrong

The Federal Reserve Bank of New York’s data shows that auto loans have surpassed student loans, becoming the second-largest debt burden for U.S. consumers. Auto loan debt has reached $1.582 trillion, exceeding the $1.569 trillion in student loan debt. This surge in auto loan debt is attributed to rising vehicle prices, leading consumers to take out larger loans at higher rates.

Lenders have responded to this trend by tightening restrictions on auto financing, with approximately 30% of lenders reporting significantly tighter lending standards. The pressure for companies to switch to EVs and inventory shortages have contributed to the increase in vehicle pricing, resulting in consumers financing more expensive vehicles.

At the same time, the government is moving full speed ahead to reach their target of 50%+ EVs by 2030. Thousands of auto dealers have penned the Biden Administration to explain how this policy is significantly hurting their business. The public is drowning in debt over mostly gas-powered purchases, and EVs are significantly more expensive to purchase and maintain. Car manufacturers are focused on producing cars of the future rather than autos that fit the budget and lifestyle of the middle class.

Bidenomics believes student debt should be waived for those who knowingly took on the debt. Will those supporting Bidenomics also push to forgive this mounting auto debt? Like diplomas, people may realize their EVs cost more than they’re worth and they cannot keep up the payments. Perhaps the public, including those who do not own cars, should subsidize these car purchases through taxes since that is the same premise as student loan forgiveness.

The World Economic Forum is in partnership with global governments to end private car ownership by 2050. Owning a car is becoming an increasing luxury. Insurance costs could be a topic for another time as most states have seen their premiums skyrocket. Major cities around the globe like London and New York City are implementing congestion and traffic taxes as well.

Decades ago, someone could purchase a nice car with less than a month’s pay. Kelly Blue Book states thatthe average price of a new car was $48,008 as of March 2023, which is 27.8% more than pre-COVID pricing. The average cost of a crossover or SUV now ranges between $30,353 and $74,502, with costs rising by over 6% every year since 2020. We will see car ownership become an increasing luxury.

Posted originally on Nov 27, 2023 By Martin Armstrong

The US national debt has exceeded $33 trillion and counting. For decades, people have predicted that the dollar will crumble to dust and gold will rise to the moon. They have applied to the Austrian School of Economics to no avail. Then you have the opposite side pushed by economists like Nobel Prize-winning economist Paul Krugman, who wrote a piece for the New York Times that argues effectively the debt can never be too big. Krugman goes to extreme lengths to justify perpetual deficit spending pointing out that government deficits don’t work the same as personal household debt. He contends in his May 13 opinion piece that the big debt number isn’t as scary as it seems.

“Governments aren’t like people,” he wrote. “[They] must service their debts — pay interest and repay principal when bonds come due — but they don’t necessarily have to pay them off; they can issue new bonds to pay principal on old bonds, and even borrow to pay interest as long as overall debt doesn’t rise too much faster than revenue.”

“So for all those whose instinct is to assume that a responsible government would, like a responsible individual, pay off its debts as soon as it can, again: Governments aren’t like people. If death and taxes are the only sure things in life, well, death isn’t an issue for governments, and taxes are an asset — a growing asset — rather than a liability.”

Krugman admits that governments are NOT immortal. “Nothing is, and no doubt someday America will, as Rudyard Kipling put it, be “one with Nineveh and Tyre.” But individuals face a more or less predictable life cycle in which their earnings will eventually dwindle.”

Paul Krugman also wrote for the New York Times back on September 2nd, 2009 that the economists all got it wrong. He admitted that reality and wrong:

“When it comes to the all-too-human problem of recessions and depressions, economists need to abandon the neat but wrong solution of assuming that everyone is rational and markets work perfectly. The vision that emerges as the profession rethinks its foundations may not be all that clear; it certainly won’t be neat; but we can hope that it will have the virtue of being at least partly right.”

The Notorious Larry Summers even admitted that economists have NEVER been able to forecast any recession since World War II. They refuse to accept that there is a business cycle and sell their profession to governments as all-seeing. If they listen to them, they will instruct governments how to manipulate the great unwashed below and eliminate the business cycle forever.

It was John Maynard Keynes (1883-1946) who in 1926 pronounced “The end of Laissez-Faire” and that economists could eliminate the business cycle and governments should enlist their profession. Yet, before he died, he admitted that everything he fought against, the business cycle, was simply wrong.

Even Arthur Burns, who was the head of the Federal Reserve when Bretton Woods collapsed, concluded that Keynesian economics had failed. The business cycle always defeated every theory economists devised to try to eliminate it.

I had an interesting conversation with Paul Volcker back in 1999, where he admitted that the business cycle not only existed but was, in fact, about eight years in length. In 1978, the former Chairman of the Federal Reserve made it clear in a publication of the Charles C. Moskowitz Memorial Lectures stating:

“The Rediscovery of the Business Cycle – is a sign of the times. Not much more than a decade ago, in what now seems a more innocent age, the ‘New Economics’ had become orthodoxy. Its basic tenet, repeated in similar words in speech after speech, in article after article, was described by one of its leaders as ‘the conviction that business cycles were not inevitable, that government policy could and should keep the economy close to a path of steady real growth at a constant target rate of unemployment.’

“Of course, some minor fluctuations in economic activity were not ruled out. But the impression was conveyed that they were more the consequence of misguided political judgments, of practical men beguiled by the mythology of the old orthodoxy of balanced budgets, and of occasional errors in forecasting than of deficiency in our basic knowledge of how the economy worked, or in the adequacy of the tools of policy. The avant-garde of the profession began to look elsewhere – to problems of welfare economics and income distribution – for new challenges.

“Of course, the handling of the economic consequences of the Vietnam War was an obvious blot on the record – but that, after all, reflected more political than economic judgments. By the early 1970s, the persistence of inflationary pressures, even in the face of mild recession, began to flash some danger signals; the responses of the economy to the twisting of the dials of monetary and fiscal policy no longer seemed quite so predictable. But it was not until the events of 1974 and 1975, when a recession sprung on an unsuspecting world with an intensity unmatched in the post-World War II period, that the lessons of the ‘New Economics’ were seriously challenged.”

That was even Karl Marx’s goal of Communism. Seize all private assets, and that would terminate the business cycle. Well, even Communism failed, collapsing by its own weight. Only Adam Smith ever investigated the economy to discover how it functioned. Every major economist thereafter spent their lives trying to disprove Smith and nobody has ever succeeded.

Now we have our modern-day Marx, Klaus Schwab, who is trying to force the entire world to adopt his version of economics which is a rehash of communism all over again. “You will own nothing and be happy” he proudly declares following the footsteps of Marx and Lenin. Schwab has failed to understand that ALL social-economic advancement comes EXCLUSIVELY from human nature and curiosity. If people have no incentive to dream, they will never advance. That is why communism fell, and Schwab does not get it because academics, more often than not, are still pursuing this dream of ultimate power to defeat the business cycle.

Instead of investigating HOW the Business Cycle functions and WHY, they seek to eliminate it, and you cannot win a fight blindfolded. Krugman admits that governments are NOT immortal. However, if you have NEVER investigated how governments collapse, then you will certainly never see the collapse until it has unfolded.

It was the city of Mainz that provided a colorful example of the political decline caused by excessive debt and inadequate management of public finances that we face today. Financial difficulties had led to the trade guilds being involved in the government of the city from 1332 onwards, and taxation became the self-interest of those in power. A major political conflict was thus avoided until 1411, when the payment of debt annuities accounted for 48% of total expenditure.

In 1411, there was a popular uprising that forbade the sale of any more debt without the consent of the trade guilds. Yet, the financial conditions continued to worsen. By 1436-1437, about 75% of the total city expenditure was now consumed by interest. Interest rates began to rise as there were subtle fears that Mainz might be unable to pay its debts. The interest rates climbed as the city searched for buyers for its debt. The interest rates jumped from 3% to 5% during the 1430s.

In 1420, the citizens of Mainz drove the patricians out of the city in a tax revolt. A new city government emerged which forbade the sale of any more annuities without the consent of the trade guilds. Nevertheless, the city’s financial situation continued to decline as it effectively sent the “rich” fleeing and in the process, the tax revenues plunged. Clearly, with the “rich” gone, the city could not revive its economy, having effectively destroyed the foundation for investment. This led to the expelled “rich” families being recalled to Mainz in a desperate realization that without the “rich,” there is no economic growth – Atlas Shrugged.

The return of the patricians may have been predicated upon their buying debt of the city since, on January 16, 1430, Gutenberg’s mother arranged with the city of Mainz to purchase an annuity belonging to her son. This appears to be the reason for the recall of the expelled rich when the city cannot revive its economy without them.

Finally, in 1436-1437, 75% of the total expenditure of Mainz went to creditors, whose interest payments continued to increase crowding out all economic growth. The interest expenditures were draining the economic fortunes of Mainz and now there was an ever-increasing difficulty to find new subscribers to its loans. This escalated causing interest rates to rise further. During the 1430s, Mainz offered 5% for the perpetual annuities instead of the previous 3% or 4%. The total national debt of Mainz reached 373,184 gulden. It was in 1448, when the city of Mainz could find no buyer of its debt and was unable to raise 21,000 gulden that it declared itself bankrupt. Since 60% of the debt was purchased by foreign investors outside Mainz, the city was placed under an Imperial ban, and excommunicated by the Pope.

The default of the City of Mainz is a classic script for the decline and fall of any government. Taxing the rich is the nail in the coffin of every society that thinks they can just tax the rich without any economic impact. The unsound economics of the Silver Democrats, who inflated the economy by overvaluing silver at 16:1 and taking bribes from the silver miners, led to the Panic of 1893, and eventually, even the Call Money Rate touched 200% by 1899.

It was the Democratic President Grover Cleveland who broke with his own party over their reckless spending, as we see today under the Biden Administration. It was Cleveland who also recognized the flight of the “rich” during that period. He noted that during such periods of unsound finance, capital can be hoarded as people refuse to invest, and traders can profit from the volatility in the markets. However, he pointed out:

“but the wage earner – the first to be injured by a depreciated currency – is practically defenseless … for he can neither prey of the misfortunes of others nor hoard his labour.”

Just look at Argentina. It was once the richest nation, and when Marxism was introduced to get those evil “rich” people, the nation declined for 100 years, and the living standards collapsed. Like the City of Mainz, they defaulted on their national debt as well. When the people say enough is enough, the press calls them the evil and dangerous far right.

This is what Krugman and most economists never understand because they do NOT investigate HOW empires, nations, and city-states collapse. If we look at the US National Debt, the total accumulative interest expenditures in 2001 reached 90% of the total debt. In other words, just like in the City of Mainz, the interest was going to foreign investors, so it never stimulated the domestic economy. Only lowering interest rates brought that level down to about 50%. But this recent rise in interest rates has brought it back to 70%.

The US has the largest economy, so its serving of the debt is at the top of the food chain in economics. So it will be the last to fall. As we can see, this debt problem is NOT unique to the United States. Every country has been borrowing with no intention of paying back anything. They are all following the course of the City of Mainz, and we are looking at a major Sovereign Debt Default. The economists simply think this will never end, for their livelihood depends on that advice.

We will be releasing the timing for the Sovereign Debt Crisis next week

Posted originally on the CTH on November 3, 2023 | Sundance

I have not written as much about the economic analysis coming from the official institutions of government because, well, quite frankly, none of it has made sense for several months. In this era of great pretending, I am reminded of the official catchphrase which began in 2021, “managing the transition.”

When you contemplate that “managing the transition” can also equate to controlling public opinion, and when you overlap the dynamic of large U.S. institutions manipulating information in order to control that opinion, then suddenly the trust in the data evaporates. When the reality of the economic situation you can measure, gauge, and sense on Main Street is increasingly detached from the government data about what’s happening on Main Street, things get weird.

EXAMPLE TODAY – Bureau of Labor and Statistics: “Total nonfarm payroll employment increased by 150,000 in October, and the unemployment rate changed little at 3.9 percent.” That’s the topline as announced.

Then you drop to the adjustments on the same report: “The change in total nonfarm payroll employment for August was revised down by 62,000, from +227,000 to +165,000, and the change for September was revised down by 39,000, from +336,000 to +297,000. With these revisions, employment in August and September combined is 101,000 lower than previously reported.”

September and October are generally significant upticks in labor, as the process for holiday preparation (shipping, transport, etc.) are underway. However, that historic pattern is no longer applicable. We see consumer trends in a downward direction, general uneasiness of the economic situation is relayed by businesses and consumers who are the key to reality, and yet the official reporting reflects something entirely different. Thus, you must ask yourself if this is part of the aforementioned “managing the transition.”

Additionally, staying with the bigger (non-pretending) picture, the U.S. government intentionally imports 7.5 million illegal aliens. Where are they in the data of employment conditions? Is there a metric that can evaluate the impact of a non-skilled labor influx that takes place simultaneous to a negative economic reality of inflation and diminished wages felt by those traditionally measured.

When you look carefully at the data provided by the Bureau of Economic Analysis (BEA), the Dept of Labor (DoL) and the Bureau of Labor and Statistics (BLS), what you come away with is the data-driven impression of something that you cannot actually see in the reality of the economic world around you. Quite simply, none of it makes sense.

If you begin talking about the disconnect, you enter a sphere of sounding like a conspiracy theorist. Would the official institutions of economic analysis actually manipulate data as an outcome of the larger goal to “manage the transition”? For me the answer is an emphatic, yes. However, how do you quantify that disconnect when the people with a vested interest in hiding any conflict are the same people who control the release of the data?

It is a reality that 75% of the American people feel their economic situation has worsened and continues to be worse. Many people are increasingly incapable of staying ahead of increases in cost of living. Govt institutions say inflation has come under control, yet the prices continue skyrocketing and everyone can feel it. Financial insecurity is the new normal amid a growing population, while the managers of the transition say, ‘all is well.’

The only thing that brings a person back from the world of crazy speak, is a review of actual ground reports on Main Street from people who are living their daily lives and trying to cope with the costs of maintaining that standard. Almost everyone expresses having more difficulty keeping their financial head above water. Yet the data released by government paints a different picture. The distance between reality and ‘official data’ has never been wider than it is today.

Fewer goods are being manufactured. Fewer goods are being shipped. Fewer sales are taking place. In a naturally contracting cycle this would mean less jobs. However, the data shows job growth.

♦Health care added 58,000 jobs in October, in line with the average monthly gain of 53,000 over the prior 12 months. Over the month, employment continued to trend up in ambulatory health care services (+32,000), hospitals (+18,000), and nursing and residential care facilities (+8,000). ♦Employment in government increased by 51,000 in October and has returned to its pre-pandemic February 2020 level. Monthly job growth in government had averaged 50,000 in the prior 12 months. In October, employment continued to trend up in local government (+38,000). ♦Social assistance added 19,000 jobs in October, compared with the average monthly gain of 23,000 over the prior 12 months. ♦In October, construction employment continued to trend up (+23,000), about in line with the average monthly gain of 18,000 over the prior 12 months. Employment continued to trend up over the month in specialty trade contractors (+14,000) and construction of buildings (+6,000). ♦Employment in manufacturing decreased by 35,000 in October, reflecting a decline of 33,000 in motor vehicles and parts that was largely due to strike activity. ♦In October, employment in leisure and hospitality changed little (+19,000). The industry had added an average of 52,000 jobs per month over the prior 12 months. ♦Employment in professional and business services was little changed in October (+15,000) and has shown little net change since May. Employment in temporary help services changed little over the month (+7,000) but is 229,000 below its peak in March 2022. ♦In October, employment in transportation and warehousing was little changed (-12,000) and has shown little net change over the year. Over the month, warehousing and storage lost 11,000 jobs, while air transportation added 4,000 jobs. ♦Information employment changed little in October (-9,000). Employment in motion picture and sound recording continued to trend down (-5,000); the industry has lost 44,000 jobs since May, at least partially reflecting the impact of an ongoing labor dispute.

The world will become a more hostile place in the months ahead as we move toward 2024. Governments have identified their enemies that have embedded themselves within Western society. First, governments will ask businesses owned by unfriendly nations to leave, and next, they will target individuals.

Syngenta has owned 160 acres of farmland in Arkansas for three decades. Arkansas Gov. Sarah Huckabee Sanders raised concerns over the company’s ties to China and the CCP. “Seeds are technology. Chinese-owned state corporations filter that technology back to their homeland, stealing American research and telling our enemies to target American farms,” Huckabee explained. The company is now being forced to leave America due to fears of national security. Additionally, they must pay a $280,000 fine for failing to disclose foreign ownership.

The state is providing Syngenta with a 30-day evacuation notice before they attempt to confiscate their land. A spokesperson for the company stated that they have been in operation since 1988 with no issue. “Syngenta’s work in the US — including in Arkansas — continues to benefit American farmers, strengthens American agriculture and makes the US a more innovative and competitive participant in the global agricultural marketplace,” the spokesman said, calling the move “shortsighted.”

However, the government knew this was a Chinese-run business years ago, as the US Department of Defense compiled a watchlist of companies connected to China in 2017. The growing fear of global warfare has gifted government the power to deport businesses on short notice. Slowly but surely, these companies will be asked to leave the US.

As a reminder, China is America’s largest trading partner. China is not currently at war with America. The government is opening Pandora’s box as this will lead to an exodus of foreign-run businesses and China will retaliate. We remember the ongoing trade war with China during the Trump administration with sanctions matched with sanctions. The globalists scream “Inclusivity!” left and right but plan on removing businesses simply because they’re connected to a foreign nation deemed unfriendly without a thorough investigation.

There are already discussions of deporting individuals for their religious and/or political beliefs. This will not be limited to the US. France’s Macron is attempting to deport those with “extremist beliefs.” Other countries will follow, especially with violently charged protests growing throughout Western nations that opened the doors to countless refugees since 2015 when Syrians were fleeing. The issue here is that the government has the sole discretion to decide who can stay and who must leave. If only those in charge would use history, recent history, as an example.

COMMENT: I watched a pretend analyst who claimed the 1987 Crash was nothing. It is amazing how these people claim to be analysts yet do not understand the first thing about what took place behind the chart. I was there at your WEC in Princeton the weekend of the crash. I don’t remember if it was videoed. If so, you should post that.

Dan

See you in Orlando.

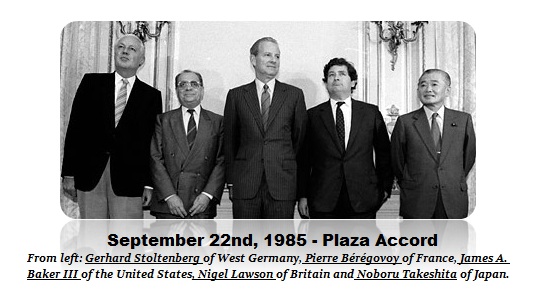

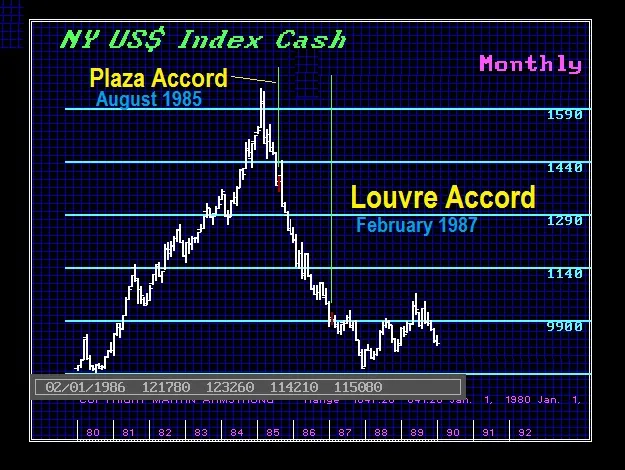

REPLY: Your statement is a sad epitaph on analysis these days. The “pretend analyst” is a Fed watcher who never looks beyond the shore. There is nothing you can do with these people. If they cannot look beyond a domestic economy, they are not analysts – plain & simple. Because I warned them back in 1985 that they would create a crash within 2 years by manipulating the dollar down 40%, when the Crash Came in 1987, that is when they were forced to call me.

When they began to realize that lowering the dollar by 40% also created a bear market in US assets for foreign investors, including US debt, they held the Louve Accord. Yet, look closely at the chart. The dollar had already bun its decline. It had nothing to do with the central banks. Those in charge know less than the average investor. They proceed, always assuming they have power – but over what they do not comprehend.

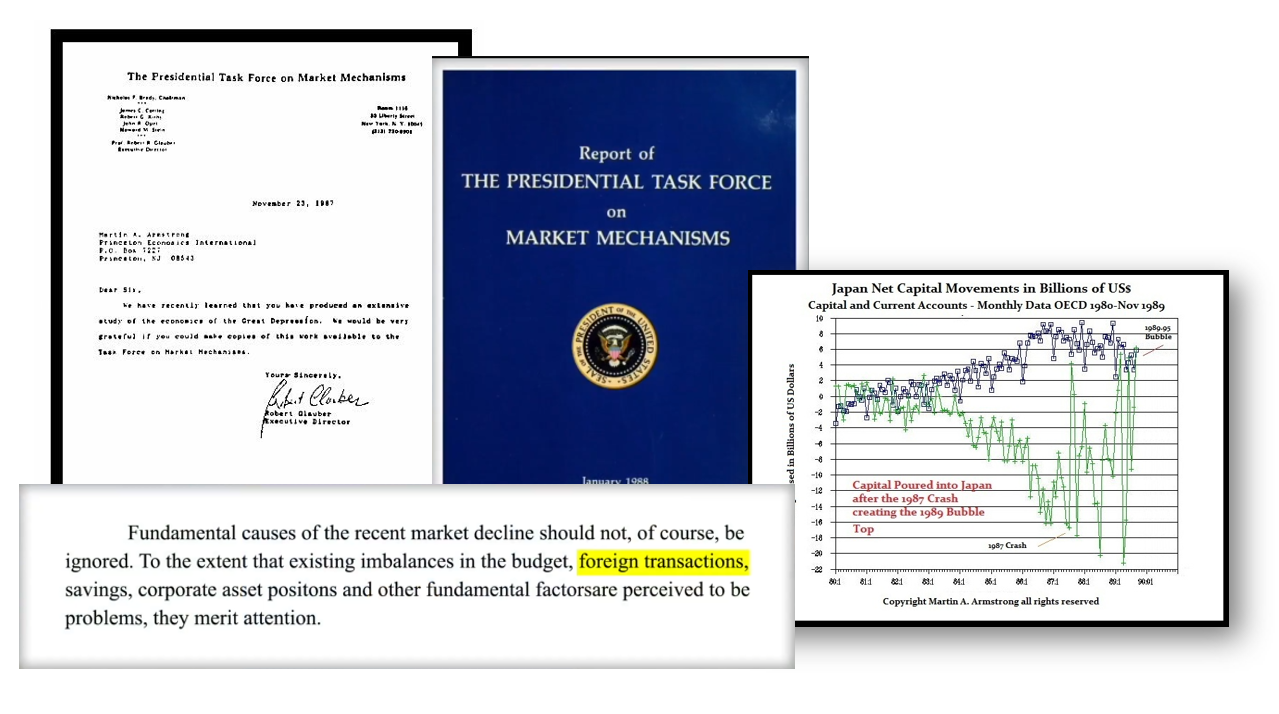

They then announced that the dollar had fallen far enough. When the dollar continued to decline, that is when the market realized that the CENTRAL BANKS COULD NOT CONTROL THE WORLD ECONOMY. Once that took place, that is what unfolded as the 1987 Crash. My biggest accomplishment was to persuade the Brady Commission not to impose restrictions on the market when the formation of the G5 created the crisis. But the government will NEVER blame itself. The most significant accomplishment I was able to do was to get the Brady Commission to at least imply that foreign exchange had something to do with it.

The lesson of 1987 is NOT in the chart. It is behind the chart. Once the public realized that the central banks were not actually in control, that is when the panic took place. Today, when interest rates rise without the Fed’s actions because of the Neocons constantly threatening the world and China over Taiwan, that is when panic will strike. It all goes nuts once people realize that the government is just a ship of fools with ZERO sailing experience. That is when gold will break out. It is that CRACK IN CONFIDENCE that will cause the panic.

This conference is rather unique. This is blending the manipulation of COVID tactics to control society and the financial backdrop behind the agenda that has been the motivation behind this authoritarian approach and the powers behind the headlines seek to drive us into their version of a Great Reset.

Martin Armstrong joins us today. We’ll talk about the real motivations behind the war in the Ukraine and the future of fiat (paper) currency and why tangible assets like gold and silver should be considered as part of your financial planning.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America