Posted originally on Jun 5, 2024 By Martin Armstrong

Federal Reserve Bank of Minneapolis President Neel Kashkari has advised against anticipating near-term rate cuts. While speaking to the Financial Times, the Fed president stated that people would simply prefer a recession to continued inflation.

“I have learned that the American people—and maybe people in Europe equally—really hate high inflation. I mean, really viscerally hate high inflation,” he told the Financial Times’ The Economics Show podcast. Kashkari is speaking as if we are not already in a recession. It is not difficult to understand the “visceral” hatred people around the world feel toward rising prices. The effects of inflation are felt with every purchase, causing the average person to adjust their entire lifestyle.

Vague issues such as rising unemployment or declining wages do not impact everyone. “I lose my job, I lean on my sister or my parents or my friends, and they help me through it. But high inflation affects everybody. There’s no one I can lean on for help because everyone in my network is experiencing the same thing I’m experiencing,” Kashkari explained. Mass layoffs, for example, would only impact a fragment of the overall population, and people would feel lucky simply to keep their jobs.

“In the US, GDP has been remarkably strong, very strong,” he noted. “The labor market has been resilient. Wage growth has been mostly resilient. And we’re seeing even the housing market has shown signs of resilience. So if I look at this resilience and economic activity, that does not look like an economy that is under pressure of very high, very tight monetary policy.” Yet, inflation is outpacing wage increases and people are watching their savings dwindle while spending less. The average person cares not of the health of the overall economy as they simply want to be able to continue maintaining or improving their standard of living. Most Americans, for example, do not invest and live paycheck to paycheck.

Real prices have far surpassed anything they calculate in CPI. Everyone understands that prices have risen far more than the arbitrary number the Fed provides us. Taxes are continually increasing for everyone in every tax bracket. The government not only adds to inflationary issues with their spending but then expects their citizens to foot a portion of the bill with taxes, which will simply never be enough.

Then we have Washington telling the masses to blame corporations for price gouging while raising their taxes and making it increasingly difficult to conduct business and maintain a large workforce. It is not that the people would prefer to be in a recession, the real issue is that countless people are entering survival mode. People everywhere want to hold onto whatever they may have out of fear for the future, but they are unable even to hoard as real prices now demand they hand over whatever they have to maintain their lives.

Posted originally on May 29, 2024 By Martin Armstrong

The old idea that inflation is created by an increase in money supply has distorted the minds of many people. Inflation is caused by numerous factors for it is not a one-dimensional aspect. For example, say a bird flu has rendered half of the egg production to be worthless, which would send egg prices soaring. This would have nothing to do with the quantity of money. So, obviously, a decline in the supply of some service or commodity can also lead to rising prices. Supply and demand.

Then there can be cost-push inflation as we saw during the 1970s due to OPEC. The first OPEC price shock was October 1973 from where we should see the next low in 2016 (43 years later). The sudden rise in oil sent a shockwave through the economy, driving up prices because the entire economy had to readjust to higher energy. This was not the result of an increase in demand nor an increase in the money supply.

When gold was used for money during the 19th century, it fell sharply in value with each new discovery from California, Australia, and Alaska. Inflation rose because of a dramatic increase in the money supply, which is exactly what took place in Europe when Spain brought back ship after ship of gold from the New World. The sudden dramatic rise in the supply of money unleashed inflation, and during both periods, money (gold) failed to provide a store of value.

Steady, slow growth in the supply of money does not lead to inflationary waves. We find that major waves of inflation are often tied to waves of speculation, which differ with each wave moving from real estate, commodities, stocks, or bonds, constantly rotating over decades within a domestic economy and then this movement of capital takes place internationally.

Inflation is not a single one-dimensional aspect. It moves up and down between the rise and fall in the demand for private assets vs. hoarding and uncertainty.

QUESTION: Dear Mr. Armstrong, could you please explain what happens in technical terms from a capital flow perspective, when confidence is lost and hyperinflation starts to begin? For example Turkey. When Erdogan was elected i think you wrote that ever since the lira started dropping. So confidence in politics is key. Do you think one day we will see hyperinflation in Turkey? And another example, is Yugoslavia: what caused the hyperinflation (in technical terms/capital flow perspective)? Are foreign investors getting rid of the dinars? Too many dinars than suddenly rushed back into Yugoslavia causing hyperinflation? Regards, Magdalena Š.

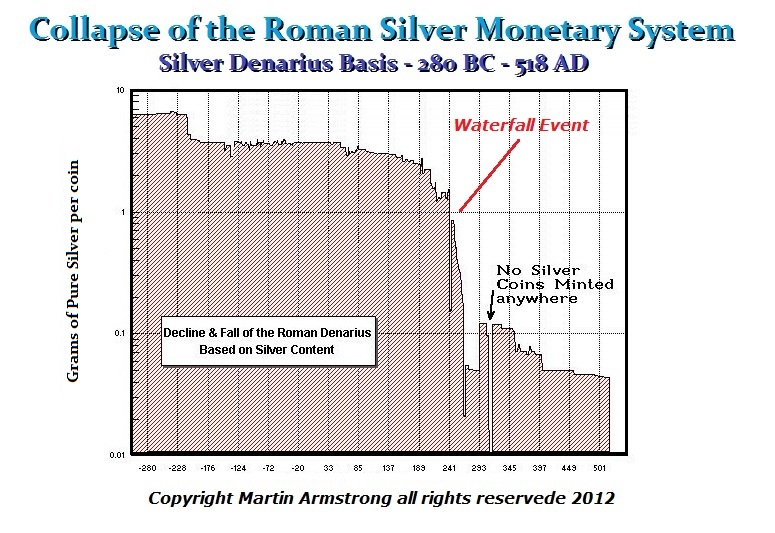

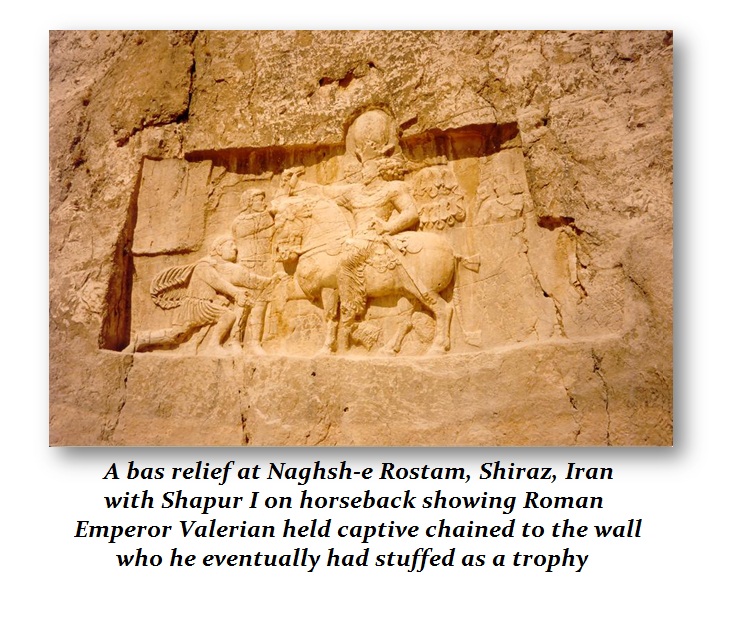

ANSWER: The misnomer about hyperinflation is that it is caused by printing money. It is a RESPONSE to the collapse in the confidence of the government. If we look at the 3rd century, this is where we find the greatest number of hoards of ancient coins. What began this was the capture of Valerian I by the Persians in 260AD.

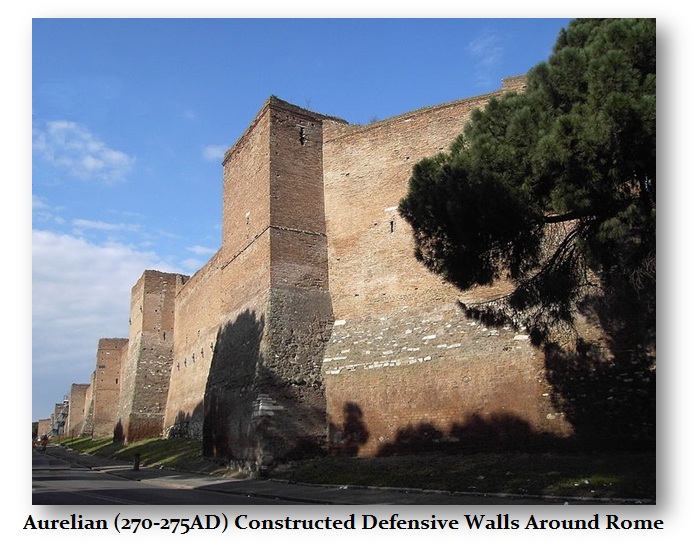

Valerian was the first Roman Emperor to be captured and Rome was unable to recuse him. That shook the confidence of the Roman people, but it also was a signal to the barbarian tribes in the North that if the Persians could do it, they could as well. Within 10 years, Emperor Aurelian constructed the great wall around Rome. Never before did Romans have such a defensive wall. That had a powerful army.

There was a trend toward debasing the silver coinage which began with Nero to try to fund the rebuilding of Rome after the Great Fire. But that did not undermine the confidence in the Roman Monetary System any more than our perpetual deficit spending since World War II.

However, a spark is ignited and suddenly that trend turns into what I have called a Waterfall event in the purchasing power of the currency. Such an event has taken various forms. However, the end result is the collapse in the confidence of the government and as a result, that is when you get that waterfall event.

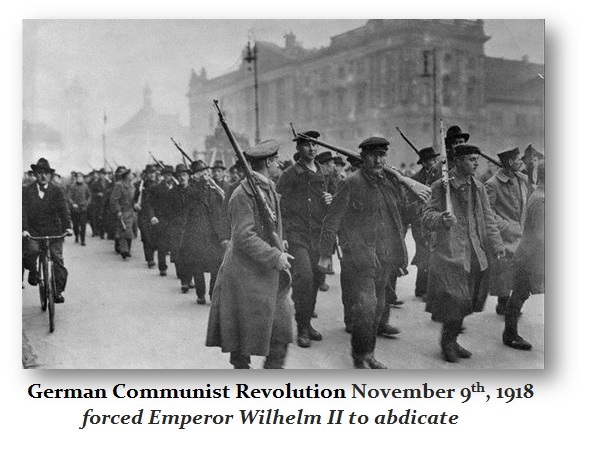

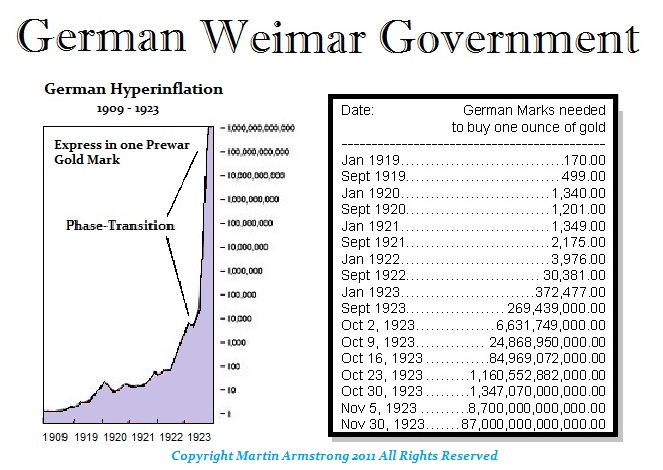

In the case of Germany, Yugoslavia, Hungary, etc, there was a 1918 Revolution where communists seized power and the emperor of Germany lost power. In that case, they actually asked Russia to take Germany after their revolution in 1917. This was the beginning of the Weimar Republic.

Germany was saddled with reparation payments demanded by France. First, you had a communist revolution and people with capital began to flee to other places in Europe or certainly move their money out of German banks. It was this drain of wealth that forced the Weimar Republic to print money to try to make their reparation payments. Then in December 1922, they seized 10% of everyone’s assets and handed them a bond.

Here you can see that after that December 1922 confiscation, hyperinflation simply took over. It was NOT the printing of money that caused the hyperinflation it was the collapse of confidence FIRST which then compels the government to expand the money supply lacking taxation revenues etc.

I suspect the spark this time may be the Digital Currency and the proposed cancellation of paper currency. This is why people are moving to anything tangible from real estate, gold, silver, ancient coins, and even equities. With DIGITAL CURRENCY they will have capital controls and prevent you from even moving money outside of your country.

The precise day of the ECM was the announcement of the IMF Digital Currency which they intend to replace the US dollar as the reserve currency. This may be timed with the turning point in 2024. It is unlikely that they would cancel paper currencies before the 2024 election. This is all being

Posted originally on the CTH on May 13, 2023 | Sundance

Recently I went to the supermarket to pick up some general provisions. Given the nature of previously predicted food price increases, and proactive measures to mitigate the predictable prices, I haven’t needed to purchase basic foodstuffs in a while. Yikes! The prices… Wow.

Since we originally warned in ’21 about the waves of food price inflation that were coming, the prices have more than tripled on many food commodities. That part is not as surprising in current review; however, the prices of processed foodstuffs is, well, quite frankly astounding.

I am left to wonder how working-class people are able to afford the jaw dropping price increases in highly processed food products like condiments (mayo, ketchup, mustard, etc), and even coffee and milk. I knew the processing costs would drive those prices, but the scale is just astounding.

Beyond the foodstuff, what was truly stunning was the current price of non-food items at the store. Items like chemical cleaners, soaps, aluminum foil, trash bags, Styrofoam products, ziploc bags, paper goods, etc. I mean seriously, $8 for a box of trash bags, good grief.

After a review of the non-food item prices, I went back to the recent BLS report [DATA HERE] to look at the producer price index to see if the data reflected the scale of the processing cost that I was reviewing across a broad spectrum of goods.

Are consumers getting gouged by manufacturers who are taking advantage of the price shock inside the ongoing inflation?

Or are the processing costs, mostly driven by energy price increases, really that big a factor in the end product as it is generated?

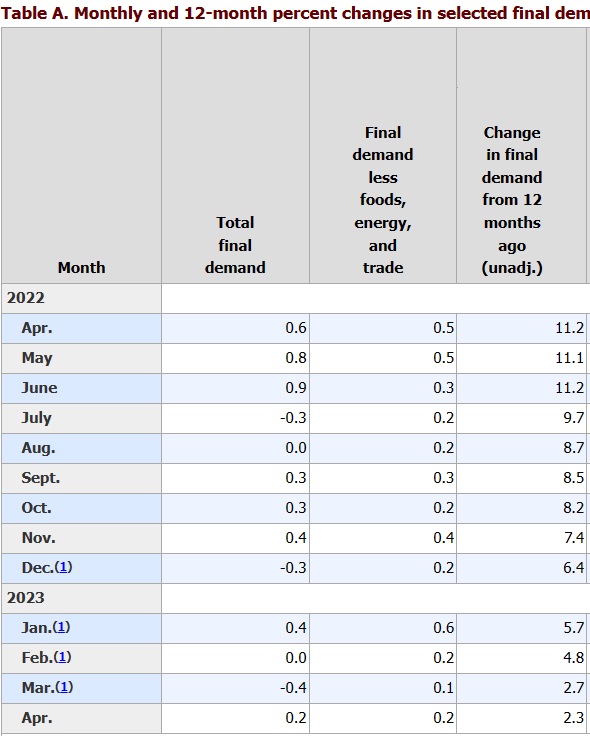

In the topline final demand Producer Price Index [Table A above] you can see how we are cycling through the second wave of inflation that hit in the spring of 2022. The rate of price increase is lower, but the prices are still rising. That means the prior massive price increase is now baked into the product, and the current price will never decline. Instead, it will just increase at a slower rate than before.

However, that’s not the full story… and that is not the data I was most curious about.

The intermediate product costs are really where the story is found.

Raw materials (unprocessed goods) are essentially in a deflationary status [-19.2% in April]. Meaning demand for the raw material has dropped well below the available supply. However, look at how much of the deflationary price is consumed in the processing of the raw materials.

A full 16% is consumed by processing cost increases [energy, physical plant, transit, production costs etc]. That is remarkable.

A random example might be citric acid. The price of the citrus base drops 19.2%, but the processing of the base into the intermediate good phase chews up 16% of the drop in raw material price and exits processing only 3.2% lower in price than a year prior.

Another example might be found in plastics. The petroleum base, and/or a combination of each material additive, might be 19.2% lower than prior year, but processing negates the lower raw material price, and exits into intermediate essentially even -.04, and then toward the ending +2.3% final demand change in the rate of price increase.

The PPI data is essentially showing the flow of costs of production as reflected in the impact during processing. We can assume mostly increases in energy, transport and distribution costs to bring the raw material forward to final good status.

Key takeaway, the demand side of the raw material is diminished. There is less raw material demand. However, processing costs are continuing to drive the final production price of goods that head into the hands of wholesalers who then bring the product to market.

The outcome of this are the prices of processed goods as noted in the products on the shelves.

QUESTION: Are you noticing rather remarkable price increases in non-food goods during your store visits?

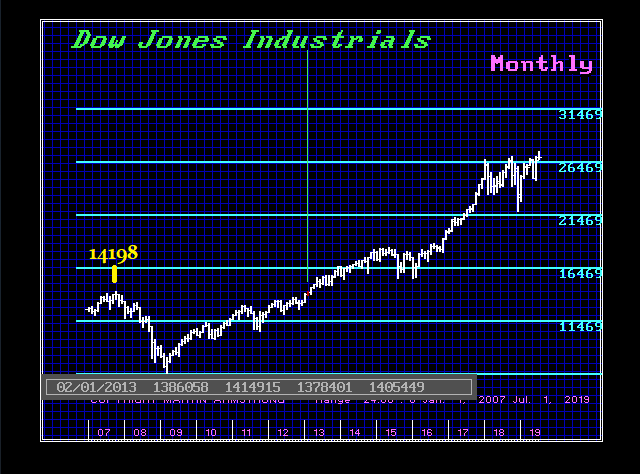

In 2010, Barron’s wrote a piece on me effectively laughing at my forecast that the share market would rally to new highs. What seems to inevitably unfold is this notion that whatever the event might be in motion, the mere thought of a reversal in trend appears impossible. When the press disagrees with Socrates, I know it will be the press who is wrong. And because they end up being wrong, of course, they cannot print a retraction so they will just pretend you do not exist rather than admit – Sorry, we were wrong. The Dow made that new high above 2007 by February 2013. That was 64 months from the October 2007 high.

I have been in the game for many years. With each event, it appears to be like Groundhog Day. They pop their heads out and declare they do not see their shadow, so the entire world will disintegrate and that is always based upon opinion. It is never backed by real analysis. Just the standard human trait of assuming whatever trend is in motion, will remain in motion.

Being an institutional adviser, I have never had that luxury. We have had to deal with some of the biggest portfolios in the world. They want accurate forecasting, and it has to be long-term – not day trading. They are not interested in the typical headlines of doom and gloom that the press love to print with every financial event simply to get readership. That is all they care about. It has been the financial version of the fake news.

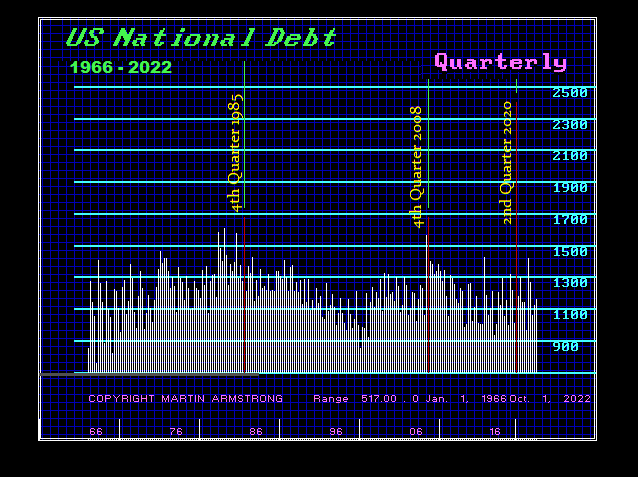

When we step back and look at this favorite fundamental that people beat to death to predict the end of the world, the national debt, and the collapse of the dollar. Little did they know that the increase in National Debt during the 2007-2009 Financial Crisis was supposed to bring down the sky and end the existence of the dollar. We can see the sharp rise in debt simply made a double top with the Financial Crisis of 1985.

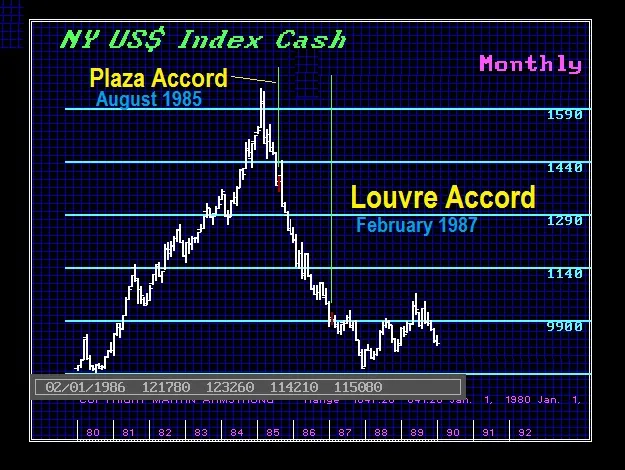

It was that previous 1985 Financial Crisis that set in motion the Plaza Accord which brought together the central banks creating what was then the G5 – now G20. Of course, like every government intervention, the side effect was the 1987 Crash and their attempt to reverse their directive at the Plaza Accord became the Louve Accord. When the traders saw that failed, the collapse in confidence led to the 1987 Crash.

It has always been a CONFIDENCE game as I pointed out with the 1933 Banking Holiday previously. In this case, the failure of the Louvre Accord which came out and said the dollar had fallen enough, once new lows in the dollar unfolded and the central banks could not stop the decline, led to financial panic by 1987 which manifested in the 1987 Crash.

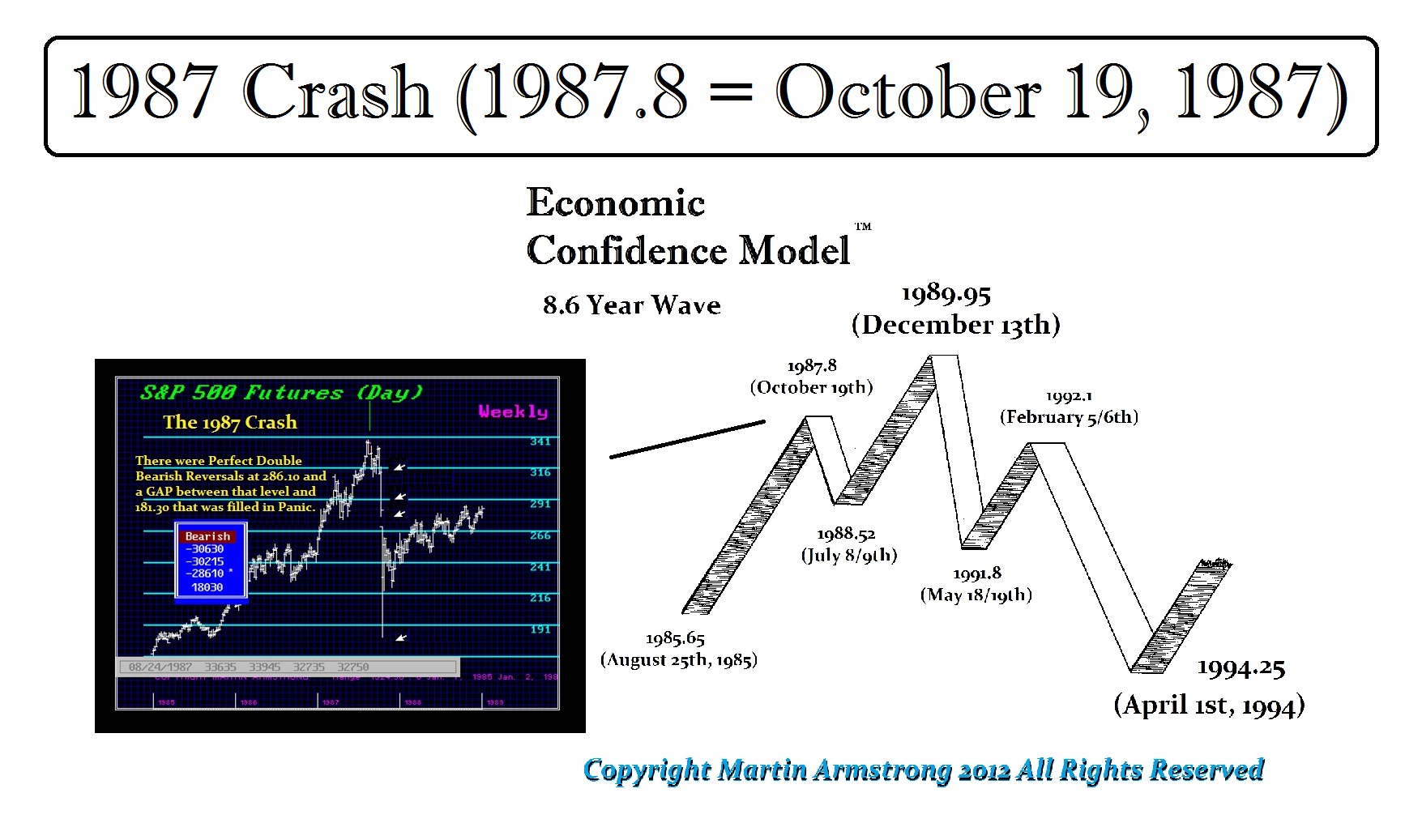

This chart shows the quarterly change in the National Debt since 1966, Here you can see the 1985 and 2008 Financial Crises were on par. Neither one ended the dollar no less the world economy. So when I warned the share market would rally and make new highs and Barron’s laughed in 2010, I said the same thing after the 1987 Crash and people laughed.

In fact, on the very day of the low, I said this was it and that we would rally back to new highs by 1989. That was perfect and the market responded to the Economic Confidence Model (ECM) which has been published back in 1979. This was more than simply forecasting the 1987 Crash and the very day of the low. It clearly established that the ECM had revealed that there was a secret cycle behind the appearance of chaos even in economics.

Larry Edelson was actually a competitor at the time. But Larry respected that the forecast from the model was far beyond what people would ever expect. If we are ever going to advance as a society, we have to stop the bullshit and understand HOW markets trade and WHY. Larry did that. He understood that the model was something larger than just personal opinion.

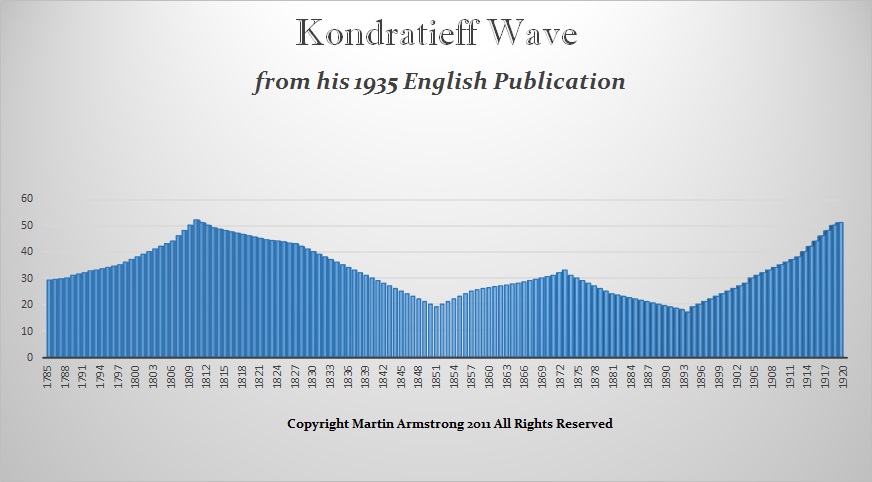

Even those claiming to be using the K-Wave cannot make real forecasts. The basis of Kondratieff’s argument came from his empirical study of the economic performance of the USA, England, France, and Germany between 1790 and 1920. Kondratieff took the wholesale price levels, interest rates, and production and consumption of coal, pig iron, and lead for each economy. He then sought to smooth the data using an averaging mathematical approach of nine years to eliminate the trend as well as shorter waves. Kondratieff thus arrived at his long-wave theory suggesting that the economic process was a process of continuous waves of boom and bust.

Kondratieff’s work was compelling and contributed greatly to the Austrian School of Economics that first began to develop the concept of a Business Cycle. The general central principle of the Austrian Business Cycle Theory is concerned with a period of sustained low-interest rates and excessive credit creation resulting in a volatile and unstable imbalance between saving and investment. Within this context, the theory supposes that the Business Cycle unfolds whereby low rates of interest tend to stimulate borrowing from the banking sector and thus then result in the expansion of the money supply that causes an unsustainable credit source boom which leads to a diminished opportunity for investment by competition.

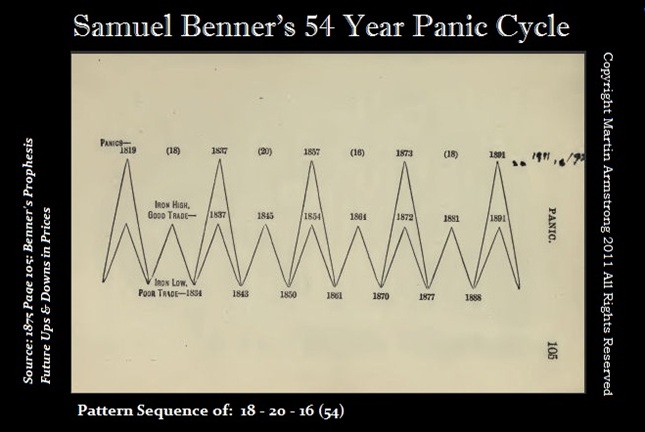

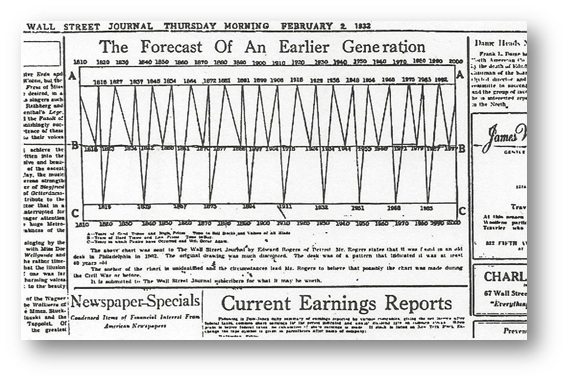

Here is a chart of the business cycle that was created by a farmer named Samuel Benner. Benner based his work on Sunspots, which actually incorporated solar maximum and minimum that today’s Climate Change zealots refuse to consider. Nevertheless, someone manipulated Brenner’s work and created a chart to try to influence society handing it in with a wild story to the Wall Street Journal published this cycle on February 2nd, 1932, when the market bottomed in July 1932. Still, nobody knew who had investigated this phenomenon in 1932.

When I was doing my own research reading all the newspapers to understand how events unfolded, I came across this chart. I found it interesting that during the Great Depression people were reaching out and some began to embrace cyclical ideas. The problem with both Kondratiff and Brenner was that the period they used to develop their cycles was the 19th century because the real Industrial Revolution was unfolding and in the 1850s, 70% of the civil workforce were all in agriculture. Consequently, if you constructed a model based entirely upon one sector, it would work only as long as that sector was the top dog.

Being a historian buff, it quickly hit me that NOTHING remains constant and that the economy will ALWAYS evolve, mature, and then crash and burn. Where agriculture was 70% of the workforce in 18590, it fell to 40% by 1900, and then down to 3% by 1980.

Just look at energy. The earliest lamps, dating to the Upper Paleolithic, were stones with depressions in which animal fats were burned as a source of light. In cultures closer to the sea, they began to use shells as lamps which they would burn at first animal fat. Clay lamps began to appear during the Bronze Age around the 16th century BC and the invention quickly spread throughout the Roman Empire. Initially, they took the form of a saucer with a floating wick.

We even find Roman oil lamps as luxury items crafted out of bronze. There are collectors of terracotta oil lamps for there is a vast variety of motifs. There is everything from dolphins, and various entities, to erotic oil lamps, which may have been used in brothels. The point is, if you constructed a model on oil, you would have surely accomplished similar results to Kondratief and Brenner.

Then of course, just as the energy moved from animal fats to vegetable oils, by the 19th century it returned to whale oil which was extracted from the blubber. Emerging industrial societies used whale oil in oil lamps and to make soap. However, during the 20th century, whale oil was even made into margarine.

Then the discovery of petroleum and the use of whale oils declined considerably from their peak in the 19th century into the 20th century. Ironically, it was fossil fuels that probably saved whales from extinction. Hence, now we are entering a period where they deliberately want to end fossil fuels and move to solar and wind power. Obviously, just a cursory review of energy reveals the problem of basing a model on the current energy source or major economic industry. Things change with time.

QUESTION: Marty there are a lot of people who seem to be trying to create a panic. Some are claiming the stock market will plunge by 50%. Others are saying nothing will survive other than gold. It seems like none of these people have any sense of what is really unfolding. They were saying the same thing for different reasons before the banking crisis. Can you offer any historical perspective?

Thank you. You seem to be the only real source these days.

Pete

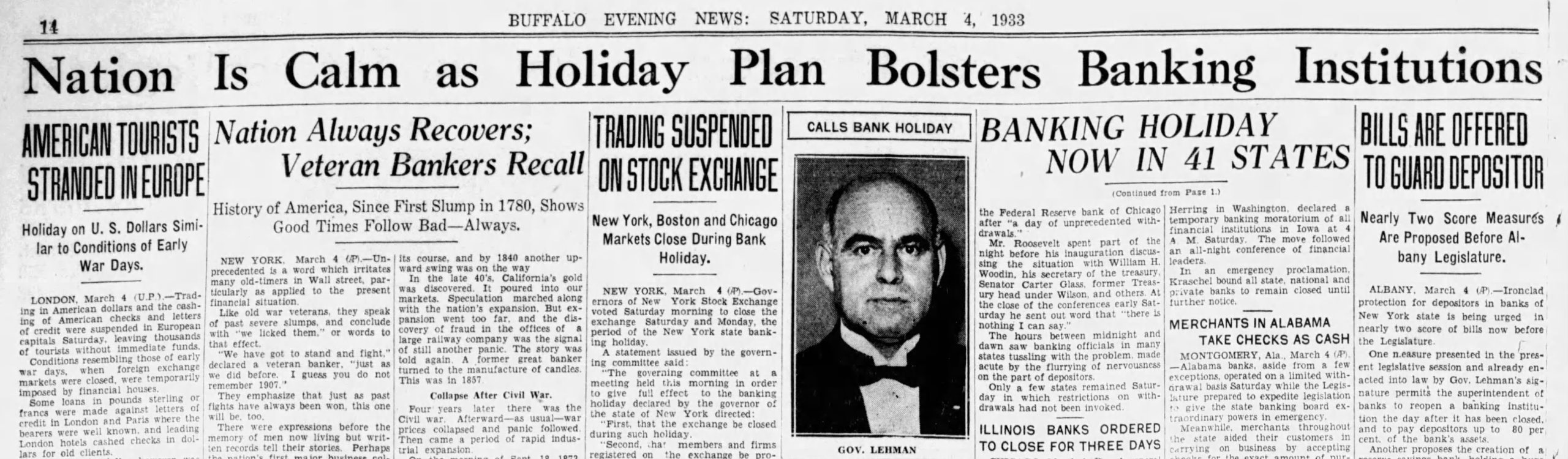

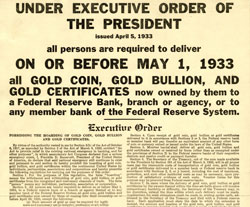

ANSWER: The Bank Holiday took place the first week of March 1933. It began with governors closing down the banks in their states. Once one began, like COVID rules, they quickly jumped on the bandwagon. As reported by March 4th, 1933, some 41 states had already declared a banking holiday. Back then, the president took office in March – not January. Thus, Roosevelt was sworn in on March 4th, 1933. As the new president, FDR delivered what is arguably his best-known speech.

“So, first of all, let me assert my firm belief that the only thing we have to fear is…fear itself — nameless, unreasoning, unjustified terror which paralyzes needed efforts to convert retreat into advance. In every dark hour of our national life a leadership of frankness and of vigor has met with that understanding and support of the people themselves which is essential to victory. And I am convinced that you will again give that support to leadership in these critical days.”

The following day, Roosevelt declared a national banking holiday on March 5th, 1933. Then Congress responded by passing the Emergency Banking Actof 1933 on March 9th, 1933. This action was combined with the Federal Reserve’s commitment to supply unlimited amounts of currency to reopened banks. Back then, they effectively created a de facto 100% deposit insurance and this was before the FDIC was created.

However, what the history books have omitted because it revealed the real reason for the major banking crisis, was the confiscation of gold precisely as Germany did in December 1922 seizing 10% of all assets which unleashed hyperinflation in 1923.

In Herbert Hoover’s memoirs (1951), he documents the fact that Franklin D. Roosevelt (FDR) played a very dirty game of politics. There were rumors that FDR would confiscate gold in 1932 BEFORE the election. These rumors spread and people ran to banks to withdraw their funds. The night before the election in 1932, FDR denied that he would do such a thing. After FDR won the election, the real bank panic began. FDR would not take office until March 1933.

The run on banks began as the Great Depression started. In 1929 alone, 659 banks closed their doors due to mismanagement and speculation. Ironically, to save money on paper, it was also in 1929 when the currency was reduced in size to save money. This time, they want to move to digital and save 100% on printing money. Here in 2023, the failures are due to the WOKE agenda which has deprived the banks of risk management rather than speculation.

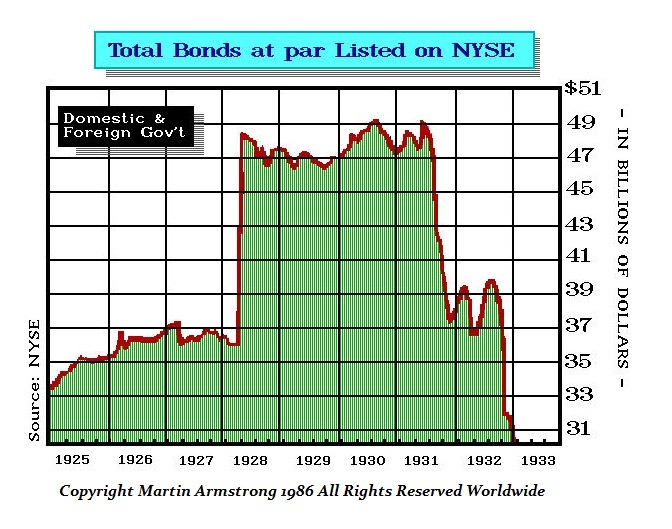

However, as the 1931 Sovereign Debt Crisis hit, the number of bank failures skyrocketed. Goldman Sacks and others were selling foreign bonds to Americans in small denominations., As Europe began to default, US banks holding foreign debt and individuals in need of cash led to a banking panic for external reasons. Here is a chart showing the listing of bonds on the NYSE. We can easily see the collapse in the bond market thanks to the 1931 Sovereign Debt Crisis.

By 1932, an additional 5,102 banks went out of business. Families lost their life savings overnight. Thirty-eight states had adopted restrictions on withdrawals in an effort to forestall the panic. By March 4th, 41 states had declared a bank holiday shutting down banks. Bank failures increased in 1933, and Franklin Roosevelt deemed remedying these failing financial institutions his first priority after being inaugurated.

However, it was actually the election of FDR that started the banking crisis post-1931. Hoover pleaded with FDR to please come out and address the gold confiscation rumors. People had been hoarding their gold coins fearing the rumored confiscation. Despite Hoover’s plea for FDR to come out and deny the rumors after the election, he remained silent. Given FDR’s manipulation of Japan and the attack on Pearl Harbor which he appeared to instigate with sanctions confiscating Japanese assets in the USA, denying the sale of any energy to Japan, and then threatening to use the fleet to block them from buying fuel from anywhere else, They Japanese attacked Pearl Harbor. There were Senate investigations afterward about FDR’s role because the US had already broken the Japanese code and knew in advance about the attack on Pearl Harbor. He did that to force the US into World War II.

It was in his character to remain silent and create the worst banking crisis in history before he was sworn in as president. FDR was a radical socialist and many viewed that he admired Lenin. If it were not for Mr. Jones exposing the truth behind Stalin, even the corrupt New York Times journalist promoting Stalinism was meeting with FDR. The run on the banks became massive when FDR won the election on November 8th, 1932. FDR allowed the banking system to implode with people rushing to withdraw the money in gold coins.

At 1:00 a.m. on Monday, March 6th, 1933, President Roosevelt issued Proclamation 2039 ordering the suspension of all banking transactions, effective immediately. Roosevelt had taken the oath of office only thirty-six hours earlier.

The terms of the presidential proclamation specified:

[N]o such banking institution or branch shall pay out, export, earmark, or permit the withdrawal or transfer in any manner or by any device whatsoever, of any gold or silver coin or bullion or currency or take any other action which might facilitate the hoarding thereof; nor shall any such banking institution or branch pay out deposits, make loans or discounts, deal in foreign exchange, transfer credits from the United States to any place abroad, or transact any other banking business whatsoever.

For an entire week, Americans would not have access to banks or banking services. They could not withdraw or transfer their money, nor could they make deposits. The entire economy ran simply on cash in your pocket.

While the first phase of the banking crisis unfolded after 1929 due to speculation losses (hence Glass–Steagall Act), then the second phase was the 1931 Sovereign Debt Crisis, it was the third phase with the election of FDR that led to thousands of banks failing as there was a mad rush to withdraw your gold coin. But a new round of problems that began in early 1933 placed a severe strain on New York banks, many of which held balances for banks in other parts of the country. About 4,000 banks failed during this period alone bringing the total to over 9,000.

Much to everyone’s relief, when the institutions that could reopen for business on March 13th, 1933 saw depositors standing in line to return their stashed cash to neighborhood banks. Within two weeks, Americans had redeposited more than half of the currency that they had withdrawn post-FDR’s election on November 8th, 1932. This would prove to be a sneaky trick of FDR to get people to redeposit all the gold coins they had withdrawn – as we are about to explore.

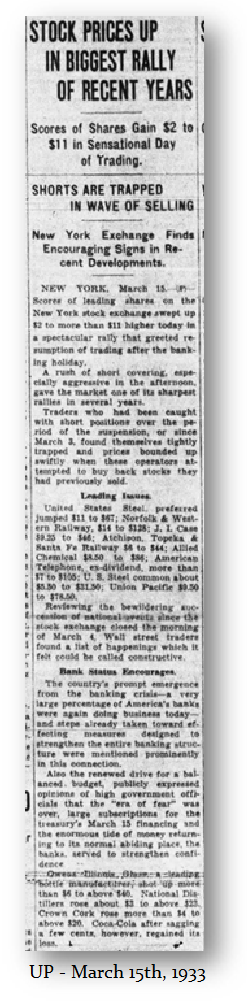

The stock market was also ordered closed when FDR came to power. With the cleverness of a real con artist operating a Ponzi Scheme to gain the confidence of the people, FDR needed the gold coin to be deposited for Phase 4 of the banking crisis. On March 15th, 1933, (The Ides of March), the stock market was allowed to reopen. On the first day of trading, the New York Stock Exchange recorded the largest one-day percentage price increase ever.

The week before the closure, the Dow Jones Industrials fell to 49.68. The week following the closure, the Dow rallied to 64.56 – a percentage gain of virtually 30% over the banking holiday. The shorts who were better on the collapse of the market once it reopened were devastated. It was a major short-covering rally.

With the benefit of hindsight, the nationwide Bank Holiday and the Emergency Banking Act of March 1933, ended the bank runs that had plagued the Great Depression, but it also set the stage for the confiscation of gold. What you have to understand is that Franklin Delano Roosevelt’s (FDR) actions in 1933 were not directed simply at gold. He was embarking on what he called the New Deal, which was a Marxist Agenda that was very popular at the time. His New Deal would end austerity, whereby they were maintaining a balanced budget in the belief that they needed to inspire confidence in the currency.

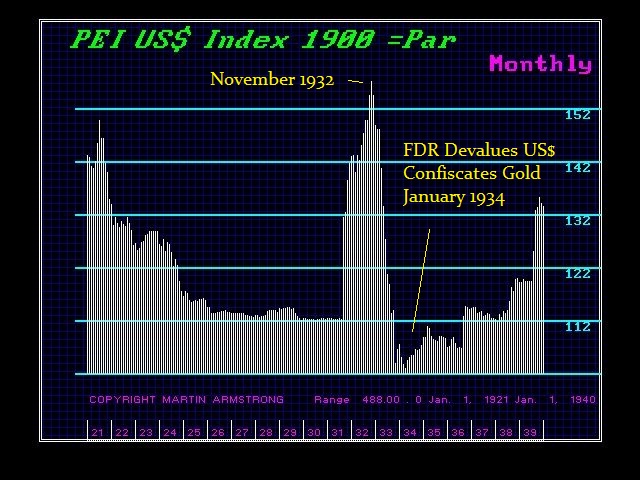

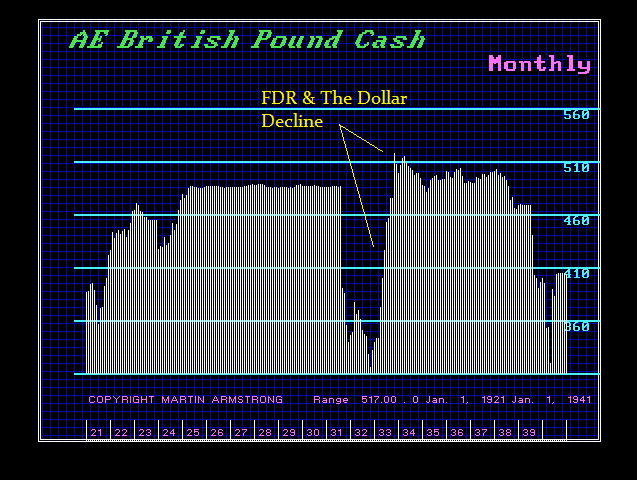

It was this balanced budget philosophy that also inspired John Maynard Keynes who argued that in times of economic distress when the demand has collapsed, that is when the state needs to run a deficit and increase the money supply. There was a simultaneous international flight of capital from Europe to the United States in the face of European sovereign debt defaults. That capital flight lasted for nearly two years until FDR won the election in 1932. There was much concern that Roosevelt would do what Germany did in 1922 in confiscating assets. That was the rumor about the possible confiscation of gold.

Milton Friedman criticized the Fed because the capital flows poured into the US but they refused to monetize it. We can see that as Europe defaulted on its debts in 1931, the capital rushed head-first into the dollar. Then we see that the dollar peaked in November 1932 with the election of FDR fearing that would weaken the dollar and exploit the economy. All this gold came to the USA pushing the dollar higher, but the Fed refused to monetize it, was Milton’s criticism. The backing of gold behind the dollar doubled in supply between 1929 and 1931.

So, you must separate gold and the devaluation of the dollar to comprehend what the issue was all about. FDR could have simply abandoned the gold standard, as did Britain, and not confiscated gold. However, that would have also been sufficient to end austerity. But the bankers would have profited and sold the gold overseas at higher prices. Roosevelt in his confiscation of gold was intended to deprive the private sector of profiting from his devaluation of the dollar which was rising the price of gold from $20 to $35. You must keep in mind that he even degraded Pierre du Pont (1870-1954) and called him the “Merchant of Death” because he produced arms for World War I and made a profit off of that war demand. Many saw Roosevelt as a traitor to his own class.

The confiscation of the gold was for two reasons. First, FDR was changing the monetary system from one where there was no distinction domestically from internationally to a two-tier system. Gold would freely circulate without restriction only internationally. Therefore, the confiscation of gold was altering the monetary system moving to a two-tier monetary system with gold only used in international transactions.

Consequently, FDR confiscated gold to move to a two-tier system and to deprive Americans of any profit from his devaluation. What FDR then did was confiscate gold from all institutions ordering them to turn over whatever they had. Ironically, this move was intended to target bankers rather than the public. FDR did not have people knocking on every door demanding all their gold. That is why there are plenty of US gold coins that have survived. If individuals possessed them rather than an institution, then they kept what they owned

Therefore, Roosevelt was able to seize whatever gold existed in banks. He declared all contracts void that had gold provisions for payment. It was in Perry v. United States – 294 U.S. 330 (1935) that the US Supreme Court ruled that Congress, by virtue of its power to deal with gold coin as a medium of exchange, was authorized to prohibit its export and limit its use in foreign exchange. Hence, the restraint thus imposed upon holders of gold coins was incidental to their ownership of it, and gave them no cause of action. id/P. 294 U. S. 356.

The Supreme Court held that it could not say that the exercise of this power by Congress was arbitrary or capricious. id/P. 294 U. S. 356. They held that even if the Government’s repudiation of the gold clause in the government bonds was unconstitutional, it did not entitle the plaintiff to recover more than the loss he has actually suffered, and of which he may rightfully complain. id/P. 294 U. S. 354. Therefore, the Joint Resolution of June 5, 1933, held:

“insofar as it undertakes to nullify such gold clauses in obligations of the United States and provides that such obligations shall be discharged by payment, dollar for dollar, in any coin or currency which at the time of payment is legal tender for public and private debts, is unconstitutional.” id/P. 294 U. S. 349.

Yet, swapping gold for dollars created no loss that was cognizable even though the taking of gold was unconstitutional. Clearly, the Supreme Court did not consider the loss in terms of foreign exchange. The Court reasoned:

“Plaintiff has not attempted to show that, in relation to buying power, he has sustained any loss; on the contrary, in view of the adjustment of the internal economy to the single measure of value as established by the legislation of the Congress, and the universal availability and use throughout the country of the legal tender currency in meeting all engagements, the payment to the plaintiff of the amount which he demands would appear to constitute not a recoupment of loss in any proper sense, but an unjustified enrichment.”

In my understanding of the law, those who argued before the Court made purely a domestic argument. A dollar was still a dollar in domestic terms so there was no cognizable loss and the Court did not reach the constitutional question. Had they argued that their loss was with respect to some debt owed in British pounds, they there was a loss. Purely domestically, the only loss would have been to inflation and the Court would never rule against the government on such an issue.

All of that said, there does not appear to be any historical precedent for the stock market to collapse by 50%, all tangible assets to turn to dust, and only gold will survive given a banking crisis where Biden and Yellen sit on each other’s hands and do nothing. Trust me. Every major Democratic donor will be screaming. And as for those claiming the Fed will reverse its position, say inflation is suddenly no longer a problem, and monetize everything in sight, this is even too big for the Fed. have to create QE and absorb all the debt, there to things have changed. If the Fed does that, it will also lose all credibility. It squarely understands that inflation comes from handing Ukraine a black check to the most corrupt government in the world. The Fed raised rates yesterday for it cannot back down. It is choreographing the best it can but the bankers do not listen.

If they simply stand behind all the deposits, then there will be no panic. That is what they did in 1933 and the market rallied in confidence thereafter.

COMMENT: Marty, it’s refreshing to have Socrates that is totally unbiased. It projected continued rising rates into next year and the Fed just proved its point. It is not backing down.

Thank you. Socrates is very enlightening.

GS

ANSWER: I know there were a lot of talks that surely the Fed had to lower rates and start QE all over again. Most of those sorts of comments have no real experience in markets. They just mouth a lot of hot air. Perhaps instead of putting masks on cows, we should do that on the shills. The Federal Reserve had no choice but to raise interest rates although it was just by a quarter point. Not to do so and the Fed would lose all credibility and the market would then not take them seriously.

You MUST understand that this crisis has unfolded because too many banks were wrapped up in WOKE culture and hired people who were UNQUALIFIED to run risk management. Some were more excited about cross-dressing as a woman and winning the Rainbow award in banking than actually protecting the bank from the risk of rising interest rates.

In a statement released at the conclusion of the meeting, Fed officials acknowledged that recent financial market turmoil is weighing on inflation and the economy, though they expressed confidence in the overall system. “The US banking system is sound and resilient.” They had no choice but to make this statement.

“Recent developments are likely to result in tighter credit conditions for households and businesses and to weigh on economic activity, hiring and inflation. The extent of these effects is uncertain.”

The Fed is saying that their rise in rates will in fact reduce inflation and economic activity. The banks have this yield curve risk and that is different from the 2007-2009 crisis where the debt was based on fraud. Here, the debt is US Treasuries so they are not going bankrupt from that aspect, but it is a liquidity crisis.

If these people who scream loudly but know nothing really about finance keep up the nonsense, they will only add to the uncertainly. This inflation is accelerating thanks to the war.

The banking crisis continues and it is impacting funds that have been buying bonds. Allianz, a subsidiary of Pimco, is writing off countless millions with Credit Suisse bonds. The banking crisis has been the result of artificially low-interest rates for far too long and banks were used to free money and buy long-term bonds all because they were making their money on the spread. Now that rates are rising, their risk management was effectively nonexistent, and thus the losses and widespread.

The Allianz subsidiary Pimco is one of the largest asset managers in the world. They have to now write off a loss in Credit Suisse bonds and it’s ain’t over yet as we head into April 10th.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America