Following Mondays near 3k point drop in the DOW, today’s attention is brought back to the Repo market and the demand for US Dollars is off the charts! In the FX market, there has been significant demand for dollars with aggressive bids seen against the Euro -9, GBP -7 and CHF -10 for T/N (Tomorrow Next). This has also been reflected in the spot market, as people’s attention turned back to a month and quarter-end.

The banning of short selling in the Euro government bond market only increases the fear of the unknown. If you can’t sell the bonds, you sell what you can and that this morning it has been the currency in Europe. Back in the late 1980’s, when the Nikkei had peaked, we saw corporate spreads actually trade through government paper. Interesting that the FED is now providing assistance in the Commercial Paper market, offering support at 3M +200bp. Good quality paper will find bids in dollars, it just takes time. However, when panic selling hits – the time is the one commodity that is never on offer!

The Fed offering at least $1.5 trillion worth of short-term loans to banks did not save the day. The market still plunged showing the Fed is now powerless as is the case with all central banks. We are facing the collapse of Keynesian Economics where manipulating interest rates no longer works to stimulate the economy.

The government’s economic stimulus is set to quickly balloon into a trillion-dollar bailout in the coming days, which will be the largest rescue in modern American history. Instead of banks, this time we are dealing with major industries as they are screaming loudly to the Trump administration and Capitol Hill for aid. Vasts portions of the economy have been undermined by this coronavirus scare which the press has turned into a financial pandemic when the number of deaths are under 8,000 compared to 1 million annually between smoking and the flu. The press has unleashed an unprecedented economic crisis and they really should be haled in to account for what they have done.

In Britain, they are asking those 70 years or older to self-quarantine for 4 months! Borris Johnson’s father was on the radio and was asked if he will comply with that and he said no way. He would still go down to the pub.

Because Europe has been in the austerity philosophy and negative interest rates since 2014, there is a panic unfolding for dollars. We see this building from clients making markets even in the Middle East. Right now, the dollar is by no means “trash” but KING! The number of institutions now clamoring for help is skyrocketing. All the Relative Value Desks and Correlation Desks have been blown out of the water in the last week.

QUESTION: Gold & the younger generation

Regarding the article ‘Gold & the Future ‘

‘…Will they then look to gold and history? ‘

I think the following article about the younger generation putting their savings into, less durable, sneakers, is interesting:

DH

ANSWER: Yes, when I ask certain people in their 20s about investment, I find it very interesting that they never seem to mention gold. The article you highlight mentions how they are selling their sneaker collections to pay for weddings, car repairs, or bail money. Even consumer reports note the disadvantages of buying gold.

Millennials (ages 23 to 38) will become the largest generation, surpassing the Baby Boomers, in 2020. But Millennials do not have the same passion for gold. Even their fathers and mothers may not remember the gold standard and Bretton Woods. Some view that Millennials are just looking for a quick buck. They tend to be more short-term speculators is the general view. When I was making money as a trader in my teens, my father was very disappointed for he remembered an uncle who lost a lot of money in the Great Depression. Being a trader was not cool then whereas the mantra was to buy and hold bonds for the long haul.

Millennials seem to have a higher risk tolerance than the previous two generations. This means they have been less interested in owning property, fixed income, or even buying and holding stocks. They are much more concentrated in higher risks and high returns. In the last two years, only 37% of those younger than 35 invested in the stock market directly or through mutual funds, exchange-traded funds, or retirement plans such as 401(k)s at any given time, according to Gallup Polls. This has increased in 2019 to perhaps as highs as 43%. The ownership of property among Millennials is at a record low, and only about 48% even consider property as an investment. When it comes to gold, that interest drops to about 34%.

The sales pitch that had you bought Polaroid or Apple as an IPO you would be the next Warren Buffet falls on closed ears. Things do change with each generation. What was once the belief of a majority becomes the rantings of a minority. You cannot judge everyone else based upon your own beliefs. That not only applies to religion but economics as well.

Israel has come out and stated that it is only weeks away from developing a vaccine against the novel coronavirus, according to its science and technology minister. Meanwhile, the coronavirus has evolved into two major lineages and it is possible to be infected with both, a new study shows.

In 1918, the world was a very different place. Doctors knew viruses existed but had never seen one. There was no testing so people really did not know if they should be quarantined. While the Spanish flu killed 50 million people, the mortality rate was 2.5%. Some say that many died from taking excessive doses of aspirin. Others say the flu actually began in China. However, that flu killed more people in their 20s to 40s. Researchers believe the 1918 flu spared older people because they had some immunity to it.

The theory as to why the elderly were spared was predicated on the idea that decades before, there had been a version of that virus that was not as lethal and spread like the ordinary flu. Therefore, older people living in 1918 may have been exposed to that less lethal version of the flu and developed antibodies. With respect to children, most viral illnesses such as measles and chickenpox are far more deadly in young adults. This may also be the reason the children were spared leaving the most vulnerable being the young adults during the 1918 epidemic.

If this version of the coronavirus subsides with the normal flu season, then a more lethal version could evolve for the 2021/2022 flu season or at least one that spreads faster more like the 1918 Spanish flu. We will not know until the next flu season.

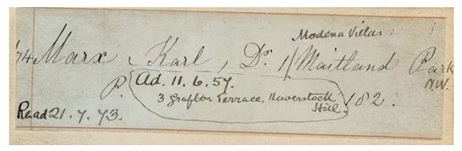

QUESTION: Mr. Armstrong, you said that Marx was influenced by Aristotle. I have never heard that before. Would you care to explain?

HF

ANSWER: Aristotle recognized that the economy evolves, and to some degree, this also takes place with the generational shift in thinking. Aristotle’s writings actually influenced Karl Marx, for he was complaining about the evolution of Athens’ economy. Aristotle saw that Athens was emerging as the Financial Capital of the World. Athens was experiencing a Market Economy and this altered what I call the Villa Economy.

Traders emerged in Athens and were offering farmers to produce more crops than they needed so they could export them to other regions. This altered society by transforming it into a Market Economy compared to the self-sufficient Villa Economy. Aristotle called these people those who made money from money. Aristotle also wrote:

The life of money-making is one undertaken under compulsion, and wealth is evidently not the good we are seeking; for it is merely useful and for the sake of something else.

Book I, 1096.a5

Marx was influenced by this observation which led to his eventual ideas of communism (Villa Economy) against capitalists (Market Economy). Marx was studying Aristotle’s works at the British Library in London.

COMMENT: Marty, you are correct about this panic. Our local school said they would remain open unless there was even one case of the virus in town. We then received an email that said they were closing for 5 weeks because they were ordered by the state board of health. Nobody realizes what they are doing to people and the economy. There are over 600,000 deaths from the flu each year. This is less than 8,000. Cigarette smoking they claim is responsible for more than 480,000 deaths per year in the United States, including more than 41,000 deaths resulting from secondhand smoke exposure. This is insanity.

ZT

REPLY: I understand if nobody is social and you remain in your house without any contact with the outside world, it is true you will not get the flu or the Coronavirus. However, the people in the medical field have no idea that this recommendation is destroying the economy and disrupting everyone. This really is insane.

What is the world going to look like Post-Coronavirus? How much damage has been caused by this panic? Reduced mobility, the tourism crisis, drastic contraction of the economy, small business that cannot afford to pay salaries with everything shut down for 5 weeks. Will advertising collapse in newspapers forcing journalists to lose their jobs? Will governments seize pension funds to bailout government failures? What about the digitalization of central bank currencies? We are looking at radical reform of the international financial system and the likely bankruptcy of many businesses caused by this panic. The post-Coronavirus world is going to be very different.

White House trade adviser Peter Navarro outlines some of the ongoing supply chain initiatives to meet ongoing demands of the corovirus effort. Navarro highlights the cooperation between US government and private enterprise. WATCH:

As an outcome of short-sighted coronavirus issues, the Philadelphia police department has announced they will no longer be arresting suspects for retail theft, auto theft, burglary, narcotics or other “non violent” offenses. Instead they will write tickets, release the suspects and address the criminality later on. Now watch what happens.

CTH saw the instructions earlier today (see below) but we did not want to immediately distribute the information. It should be remembered the current Philadelphia police commissioner, Danielle Outlaw (pictured left), is a social justice activist from Portland, Oregon.

Unfortunately, there is a predictive element to this. Perhaps some are familiar with the post Hurricane Andrew experience in Homestead and Miami-Dade.

The only thing standing between law-abiding citizens and those who would take their possessions is an ability to defend your own property. This is now the Philadelphia reality.

PHILADELPHIA – In response to the COVID-19 outbreak, Philadelphia police officers have been instructed to stop making arrests for certain non-violent crimes.

The department said individuals who would normally be arrested and processed at a detective division, will be temporarily detained to confirm identification and complete necessary paperwork. The individual will then be a arrested at a later date on an arrest warrant. (read more)

Beware, the law of unintended consequences.

Here’s the leaked guidance. You can easily predict the problem with this policy:

From the instructions above…. Non-violent offenses include: All narcotics offenses. Theft from persons. Retail theft. Theft from auto. Burglary. Vandalism. All bench warrants. Stolen auto. “Economic crimes” (ie. looting, bad checks, fraud) and finally Prostitution.

Those offenders will be immediately released after documentation.

This is the exact issue that drives the need for law-abiding citizens to the second amendment for protection when the police openly admit they will not protect people or property.

Steve Keeley

✔@KeeleyFox29

·

BREAKING: @phillypolice officers instructed to stop making arrests for following list of what are consider non-violent crimes. Here is the email sent to city police officers telling them to just obtain arrest warrants for now. @FOX29philly

Steve Keeley

✔@KeeleyFox29

Full Philadelphia Police Commissioner’s directive here @FOX29philly

Tonight Florida, Illinois and Arizona are holding their 2020 democrat presidential primary. Ohio Governor Mike DeWine cancelled/postponed the Ohio primary due to Wuhan virus fears.

The polls began to close in Florida at 7pm ET/ panhandle polls will be closed in FL at 8pm ET.

Polls also close in in Illinois at 8pm ET, and in Arizona at 10pm ET.

Bernie Sanders is expected to get crushed in Florida as a result of his supportive politics toward Fidel Castro and Cuba, the only question will be the size of the Biden win. However, Illinois and Arizona might fare better for Bernie depending on turnout.

Earlier today President Trump met with executives from the U.S. tourism industry to discuss how their operation are impacted by the various COVID-19 mitigation efforts.

Participants included: Roger Dow, President & CEO, Travel Association; Chip Rogers, President & CEO, American Hotel & Lodging Association (AHLA); Jon Bortz, President and CEO, Pebblebrook Hotel Trust and AHLA Chairman; Elie Maalouf, President, The Americas, Intercontinental Hotels Group (IHG); Christopher Nassetta, President & CEO, Hilton; Arne Sorenson, President & CEO, Marriott International; Richard Bates, EVP, Disney; Mark Hoplamazian, President & CEO, Hyatt Hotels Corporation; John Sprouls, Chief Administrative Officer, Universal Parks and Resorts; Patrick Pacious, President and CEO, Choice Hotels International; David Kong, CEO, Best Western Hotels and Resorts; Jim Murren, President & CEO, MGM [Video and Transcript Below]

.

[Transcript] – THE PRESIDENT: Well, thank you very much. We have the tourism industry executives, the biggest anywhere in the world. These are the great ones, and they’re going to say a couple of little words pretty soon, I think. We’ll talk about their company quickly and the number of employees and what’s happened since the Chinese virus came about. And they’ll be discussing that.

So we’re joined this afternoon by the true leaders of our nation’s travel, hospitality, and tourism industries. And I want to thank you all for being here. I’ve known many of you for a long time. Great people.

I want to thank Vice President Pence for his tremendous leadership on the task force. He’s done a great job. And thanks also to Secretary Mnuchin over at the Hill. They’ve been working — and Wilbur Ross and everybody, basically. They’re all working. We’re all working very hard.

We’re profoundly grateful to all of the companies and organizations here today representing tens of thousands of American workers and really representing something so important. It’s the place to stay when they come to our country. Such a big business. One of the biggest businesses. And thank you for adopting additional protocols to keep Americans healthy, including enhanced cleaning processes throughout your hotels and buildings.

We know that your industry is among the hardest hit by the economic impact of the virus. Our goal is to beat the virus, and we will — we call it the hidden virus, the hidden enemy — with aggressive action now so that we can rebound stronger than ever before, and that’s what we’re doing. And everyone is cooperating. We’re really getting tremendous spirit. Republicans are getting along with Democrats, and a lot of good things are happening.

Yesterday, we issued new guidelines for how all Americans can minimize their risk of exposure and stop the transmission of the virus.

My administration has taken decisive action to support American workers and businesses. We love our workers. We love those workers. They’re incredible. And we’re going to come out stronger than ever before. And it’s not going to be so long.

The IRS will defer tax payments for affected individuals and businesses.

Today, the Senate is taking up legislation to provide for free testing — and that will happen — paid, sick, and family medical leave and nutritional assistance for the vulnerable.

We’re announcing — and we will be announcing again later on — that we’re working with Congress to provide rapid relief for affected workers and industries. And this will allow us to emerge from the strongest economy on Earth because we had, literally, the strongest economy on Earth. And now this is in, as of last count, over 124 countries, I understand. A hundred and twenty-four countries. Unbelievable. But we’ll emerge — I really believe we’ll emerge stronger because we’ll be doing things differently than this country has done them in the past for many, many decades.

And we’re deeply committed to ensuring that small businesses have the support they require. The Small Business Administration announced disaster loans, which provide impacted businesses with up to $2 million. And we’ve asked Congress to increase the SB lending authority. We’re going to be going up to $50 billion and, actually, much more than that for small businesses. So they’ll be helped. In your cases, they’re very big businesses, but it’s a lot of employees. And so we appreciate it very much.

We appreciate your being here. And maybe, in front of the media, you could say a couple of words about your companies and the number of people you employ. And I pretty much know every one of you in that respect. It’s a lot of people and great companies.

Please.

MR. NASSETTA: Hi. I’m Chris Nassetta. I am CEO of Hilton. And we have 6,000 hotels around the world, about 4,500 hotels in the great United States of America. We employ, globally, about 450,000 people, about 260,000 people here in America.

Mr. President, on behalf of everybody — I’m sure you’ll hear this from others — we appreciate you having us here. We appreciate all that you’re doing today to keep all of us safe and secure first, and working on trying to secure a good future for the economy, as you point out, that was quite strong but obviously being impacted by this.

THE PRESIDENT: Right.

MR. NASSETTA: Vice President Pence, to you and all others that are working on this day and night, we appreciate it.

As the President pointed out, we’re, you know, one of the biggest industries in the country. We’re one of the biggest employers in the country. And our industry, as you will hear from others, has been impacted in a devastating way.

I personally lived through many crisis, starting with the S&L, the 9/11 crisis, the Great Recession. I’ve been doing this for 35 years. Never seen anything like it. And so, you know, we’re hoping to have a constructive dialogue about, you know, how we protect the small businesses that make up the bulk of this industry and how we protect the people on the frontlines of this industry — that number, 5 million people — that, at this point, given what’s going on in our industry, are in harm’s way.

So —

THE PRESIDENT: And tell me: So you’re in many countries. And how are you doing in other countries? Some are in very, very bad shape, I know.

MR. NASSETTA: I would — you know, I was looking at our numbers last night; it is strikingly similar everywhere in the world.

If you look at the — you know, around the world, we — within, you know, I would say, just a few — you know, a few days or maybe a week, we will probably be running 10 to 15 percent occupancy in the world.

THE PRESIDENT: And that’s pretty much all over the world.

MR. NASSETTA: That’s everywhere in the world. It’s a little bit better here, but — but catching up. If you look at the major cities around the United States, they’re running in the single digits, which means, for the first time in 100 years — Hilton has been around 100 years — we’ve never closed a hotel that wasn’t going to be demolished for rebuilding. The bulk of our hotels in the major cities are closing, as we speak.

THE PRESIDENT: Well, we’ll get it open soon and we’re going to — we’re doing a — we’re doing a yeoman’s effort. I think it’s — we’re going to be very successful. You’ll be back in business soon. But we have to keep your employees going —

MR. NASSETTA: We do.

THE PRESIDENT: — and the businesses going. And we —

MR. NASSETTA: Yeah. That’s our first priority.

THE PRESIDENT: And we will be able to do that, Chris. Thank you. But all over the world, it’s a disaster.

MR. NASSETTA: All over the world, it’s a disaster. There’s not one part of the world that’s not being —

THE PRESIDENT: Yeah. It’s all over.

MR. NASSETTA: — severely impacted.

THE PRESIDENT: Yep. Thank you very much. Please.

MR. KONG: Mr. President, Mr. Vice President, Secretary Ross, thank you for taking the time to see us, and thank you for everything that you’re doing.

THE PRESIDENT: Thank you very much.

MR. KONG: We very much appreciate it. I’m the President and CEO of Best Western and also WorldHotels. We have about 5,000 hotels around the world; half the hotels are in the United States. We employ tens of thousands of employees in our company.

As Chris has already alluded to, this is a very difficult time and very challenging times for us. Just today, I had a call with one of our franchisees. He was lamenting that, although he owns about 10 different hotels and different brands, and some with us and some with other brands, he was lamenting having to lay off tens of hundreds of people in his company. Some of them have been with him for 20, 30 years. And he was really concerned about their livelihood and their safety net.

And the other thing that he mentioned was, if the government can help with liquidity and access to capital, that would be of great assistance.

THE PRESIDENT: Yeah.

MR. KONG: And he specifically mentioned that his loans were — swap loans and therefore there are severe penalties to refinance. And so if there’s any way to alleviate that burden, they would be —

THE PRESIDENT: With the banks.

MR. KONG: — most grateful.

THE PRESIDENT: Yeah. We’re dealing with the banks too, and the banks have been very accommodating. They will be. I think they will be.

MR. KONG: Thank you.

THE PRESIDENT: Thank you, David. I appreciate it.

Please.

MR. SORENSON: Thank you, Mr. President. Arne Sorenson, CEO of Marriott. Thanks for giving us your time this afternoon, and —

THE PRESIDENT: Thank you.

MR. SORENSON: — appreciate the leadership of all of you as we go through —

THE PRESIDENT: Great job. Good job.

MR. SORENSON: — this crisis.

The — I don’t need to repeat much of what’s been said. We think we have about 750,000 people that wear our name badge around the world every day.

THE PRESIDENT: Right.

MR. SORENSON: Probably about two-thirds of those in the United States.

THE PRESIDENT: How many hotel rooms now, worldwide?

MR. SORENSON: 1.4 million. Just shy of 1.4 million hotel rooms. And, as you know, the business is made up of hotels we run. Often, the hotels are owned by other investors, but we will operate them, and then also by franchise operators. And they are typically owner-operators. They might range from a Fairfield Inn in suburban or rural market, all the way up to a Ritz Carlton or a St. Regis someplace.

And you asked about the globe. You know, in January — of course, this all starts in China — business falls by 90 percent.

THE PRESIDENT: And this all started in China.

MR. SORENSON: All started in China.

THE PRESIDENT: That’s where you first saw the problem and it’s where you first got hit.

MR. SORENSON: Absolutely. Third week in January, and within a week, business —

THE PRESIDENT: I hope you all heard that.

MR. SORENSON: — business is down about 90 percent. And you’ve been living this just the way we have. About three weeks ago, we had that horrible weekend where it shows up in Korea and in Italy. They are, sort of, a clarion call, if you will, that it has left China and it —

THE PRESIDENT: Right.

MR. SORENSON: — and it is moving to the rest of the world. And while we didn’t know exactly how it would show up in the United States, it was fairly clear that it was now a broader spread. And, from that —

THE PRESIDENT: Is China doing better now?

MR. SORENSON: China, there are starting to be some green shoots. So, Macau, for example, we think we bottomed at about 2 percent occupancy. We think we —

THE PRESIDENT: Two percent?

MR. SORENSON: Two percent.

THE PRESIDENT: In Macau?

MR. SORENSON: Yeah.

THE PRESIDENT: Wow.

MR. SORENSEON: And we think we might be approaching 30 [percent], as of last night. Now, that’s probably one of the stronger markets in China.

THE PRESIDENT: Well, that means it’s coming. It’s (inaudible).

MR. NASSETTA: It’s coming back.

MR. SORENSON: And so they’re trying to get things going again, but we’re still, in the rest of the world, including the United States — I get dailies, of course, of new reservations and cancellations — in every other market, the numbers are continuing to go down. So we — I don’t think we’ve bottomed anywhere else yet.

In the U.S., in the last couple of days anyway, when you look at decline in reservations and in cancellations, the total is negative.

THE PRESIDENT: Right.

MR. SORENSON: So we’re losing business every day, (inaudible).

THE PRESIDENT: No, we’re in that process. We haven’t hit that top yet. We’re in the process.

MR. SORENSON: Yeah, I think that’s right. And, of course, we’ll have some time with you today. But employees, first, and I think —

THE PRESIDENT: Right.

MR. SORENSON: — liquidity, second, is the two things that are on our list.

THE PRESIDENT: Thank you very much. Thank you.

MR. MAALOUF: Thank you, Mr. President. Elie Maalouf with InterContinental Hotels Group, Chief Executive of the Americas. Thank you, Mr. Vice President.

We have nearly 6,000 hotels around the world, over 3,800 hotels in the United States, over 530,000 rooms. Eighty percent of those are owned by small business people across 50 states, across every county, across every community. So we’re experiencing the same impacts similar to what the industry, the HLA, and our colleagues here have been talking about.

But I want to turn our attention to those small business owners in 50 states across the communities because they’re the bedrock of those communities. And as they’re getting impacted, it’s not just their employees that begin to see an impact in job losses, but it’s an entire ecosystem of their suppliers, their vendors. And so I think — I’m very pleased that we can work together with you and the administration to find a solution to preserve that —

THE PRESIDENT: We will.

MR. MAALOUF: — network of entrepreneurs across the country.

THE PRESIDENT: Yep, we will.

MR. MAALOUF: Thank you, Mr. President.

MR. PACIOUS: Thank you, Mr. President, Mr. Vice President. Patrick Pacious, CEO of Choice Hotels International. We have 6,000 hotels in the U.S. That’s 1 out of every 10 hotels flies our flag.

As others have talked about, we’re in secondary and tertiary markets. We may be the only hotel in a small town. Those owners have two key concerns: one, what do they do with their employees when they’ve got zero occupancy? And two, how do they pay their mortgage? So it is this question of employee retention and liquidity so that you get through this period.

Ninety percent of our hotels are SBA eligible, so we’re very familiar with the SBA loan program and the disaster relief. There’s some red tape there that we have some suggestions that we think the SBA could —

THE PRESIDENT: Okay, give us those suggestions.

MR. PACIOUS: You want them right now?

THE PRESIDENT: Yeah, go ahead.

MR. PACIOUS: I’ll give them to you right now. The first is the disaster relief cap. It’s only 2 million, and if you’ve taken out the full 5, you can’t get access to the — to the additional 2.

THE PRESIDENT: I see.

MR. PACIOUS: So we need the cap raised.

THE PRESIDENT: To what?

MR. PACIOUS: We need it to — at least raised to 10 — 10 million on a per — per-individual basis.

THE PRESIDENT: Okay.

MR. PACIOUS: Secondly is the personal liquidity test, which just got put in place. That could be rolled back.

And the final one is figuring out the affiliation. So an individual may own a partnership in multiple hotels.

THE PRESIDENT: Right.

MR. PACIOUS: So that again restricts the amount of capital available to them. So we’d really like the opportunity to speak to the SBA about lifting some of those requirements to really help inject more liquidity.

THE PRESIDENT: So it’s individual properties, instead of — instead of accumulated properties?

MR. PACIOUS: Absolutely.

THE PRESIDENT: Okay. I got it. Thank you very much. Thank you, Patrick.

MR. HOPLAMAZIAN: Thank you. Mark Hoplamazian, CEO of Hyatt Hotels.

THE PRESIDENT: Right.

MR. HOPLAMAZIAN: We have 950 hotels around the world and we have 600 in the United States, over 70,000 employees. And I’m not going to repeat a lot of the things that were said.

We’ve been tracking — we have a large base of group business in the United States. Big convenings and conventions. And we’ve been tracking major cancellations. We now have tracked, in the U.S. alone, canceled events — and I’m not talking about major sport leagues that have — the sports leagues that have shut down or universities and those kinds of things — but actual convenings, conventions, big meetings.

THE PRESIDENT: You have some of the sports leagues, right?

MR. HOPLAMAZIAN: As customers.

THE PRESIDENT: You have quite a few? Yeah, I would think so.

MR. HOPLAMAZIAN: Yeah, but when we look at just the other meetings that have been canceled, they involve attendees of over one and a half million people. So when you think about the ecosystem impact — it’s major convention markets where those attendees are not showing up. So they’re not traveling on airplanes, but they’re not staying in our hotels. They’re also not going out to restaurants. And so the collective impact is quite significant.

I think the key issue that I would leave you with is that the urgency is very high because, day by day, the occupancy rates have dropped precipitously. So now we are seeing occupancies below 10 percent, in the single digits, for the vast majority of our hotels — whereas a week ago, they were 20, 30 points higher than that. It’s happened very rapidly.

THE PRESIDENT: When this ends, do you see a quick build up?

MR. HOPLAMAZIAN: I think that all depends on how — how confident people are to get back on planes and start traveling again.

THE PRESIDENT: Right.

MR. HOPLAMAZIAN: So I think that’s really the key issue. We’ve got to also position ourselves to get people back into their jobs. Either retain them or rehire them: One of those two things are critical. Because we all are proud of the people that we employ and we want to retain them. So whether we can retain them or have some assistance in getting them rehired early so that we can spool back up.

THE PRESIDENT: Hopefully you can retain them.

MR. HOPLAMAZIAN: Hopefully. Hopefully, we can retain them.

THE PRESIDENT: So that’s what we’re shooting for. You want to retain them.

MR. NASSETTA: I think the issue of that — sorry to interrupt, Mark — Mr. President, is that when our owners are running 8, 9 percent —

THE PRESIDENT: Yeah?

MR. NASSETTA: They said, “We’re shutting hotels.” So all of those employees are being furloughed or laid off right now, day by day.

THE PRESIDENT: Right.

PARTICIPANT: (Inaudible.)

MR. NASSETTA: You know, Jim Murren is here somewhere –-80,000 people this week. We’re tens of thousands, because our owners can’t pay it.

MR. HOPLAMAZIAN: Well, that’s the key. The key issue that I was really making is the timing. It’s really — it’s happening instantaneously.

THE PRESIDENT: Okay.

MR. NASSETTA: One of the things we could — yeah, we want to talk about is trying to, you know, create a fund for those people in order to stop that from happening, because it —

THE PRESIDENT: What kind of a fund would that be?

MR. NASSETTA: I think that would have to — you know, in lieu of sort of the unemployment insurance, it would be —

THE PRESIDENT: In terms of dollars.

MR. NASSETTA: I think the fund for that, probably our — our quarterly payroll for the industry is $45 billion in total. So that would be sort of —

THE PRESIDENT: Forty. Okay.

MR. NASSETTA: You can sort of scale it there.

THE PRESIDENT: I got it. Yep.

MR. NASSETTA: Yeah.

THE PRESIDENT: I got it.

MR. BROWN: Mr. President and Mr. Vice President, thank you for your time. I’m the CEO of Wyndham Destinations and we’re in the vacation ownership and exchange business, the world’s largest company in that space. We employ 23,000 associates and take care of over 5 million households on vacation every year.

Largely in the industry, it’s about a $80 billion impact to the overall economy. And we employ, directly, 250,000 and another 250,000 through other small businesses that work well with our industry.

To your point about a quick recovery, we purely serve a leisure customer, which means — just like after 9/11, just after that ’08, ’09 — our customers will be back really quick, as soon as we’re on the other side. And they — we really believe our industry will recover quickly and be an accelerant —

THE PRESIDENT: I think so, too.

MR. BROWN: — an accelerant back to the economy once we get on the other side.

THE PRESIDENT: Right. I think so, too. Thank you very much. Great job. Thank you.

MR. MURREN: Thank you, Mr. President, Mr. Vice President. It’s Jim Murren —

THE PRESIDENT: Hi, Jim.

MR. MURREN: — the chairman and CEO of MGM resorts. It’s good to see you all again. Mr. Secretary.

THE PRESIDENT: We couldn’t get you a chair? What happened? (Laughter.)

MR. MURREN: Well, we’re in the spatial recognition world. But I just wanted to say, on behalf of MGM, we have made a decision around the country to close our resorts. And tomorrow night, we will close all of the resorts in Las Vegas. That’s 70,000 people we are now putting on a furlough. I want to retain those employees. I want to bring them back as soon as possible.

Las Vegas, as you know, will come back rapidly once the –you give us the green light.

THE PRESIDENT: I think so.

MR. MURREN: But it’s very important that we keep these people on our payrolls as soon as possible.

I also represent the 2 million jobs of the gaming industry in the United States. And, as you know, many of those casinos are in cities that rely upon them for their tax revenue. So I appreciate your efforts, and I stand by to help you in any way I can.

THE PRESIDENT: Okay. We’ll get it done, Jim.

MR. MURREN: Thank you.

THE PRESIDENT: We’ll get it done.

MR. BATES: I’m Richard Bates. I’m with the Walt Disney Company. And today I’m here for the theme park and hotel/motel business.

THE PRESIDENT: Good.

MR. BATES: So, thank you, Mr. President, Mr. Vice President, Mr. Secretary. We have about 220,000 employees. We think our company is great because of our employees. So employee retention is the single most important issue for me.

Second would be liquidity. So I, frankly, support some kind of employee/employer payroll tax holiday. I don’t know if you’re still —

THE PRESIDENT: Is that what you like the best of the various scenarios?

MR. BATES: I like them all. (Laughter.) But that one I like a lot.

THE PRESIDENT: Most direct. Not as quick, but most direct.

MR. BATES: I think so.

THE PRESIDENT: Thank you very much.

MR. MURREN: Especially, Mr. President, because a lot of us who have — like Disney voluntarily closed their parks, so they have people out of work today. And as has MGM — we have voluntarily closed these resorts. And if we can get some relief on that, we will absolutely want to keep these people employed.

THE PRESIDENT: Let me ask you, the parks outside of the United States —

MR. BATES: They’re closed.

THE PRESIDENT: Closed? You closed all of — all of your parks? Everything closed? That’s a real worldwide problem isn’t it?

MR. BATES: Absolutely.

THE PRESIDENT: That’s incredible.

MR. MURREN: And I’m sorry, one last point, Mr. President.

THE PRESIDENT: Yes?

MR. MURREN: And, on Macau, because Arne Sorenson was talking about it.

THE PRESIDENT: Right.

MR. MURREN: Of course, we own two resorts there. The government shut those casinos down, as you know, for two weeks. We’re starting to slowly see a recovery there, but it is absolutely single-digit occupancy right now. So we’re not seeing any better results there currently.

THE PRESIDENT: Okay. Good.

You guys okay? Yes, please.

MR. ROGERS: Chip Rogers, President and CEO of the American Hotel and Lodging Association. I’ll be quick. Industry wide, last year, occupancy was 67 percent. That helped support 8.3 million jobs. Right now, as these gentlemen have indicated, we’re probably under 20 percent nationwide and headed south.

If, by the end of the year, we get up to 35 percent and if nothing else happens, that’ll be about 4 million jobs lost. That’s if we can get back up to 35 percent.

THE PRESIDENT: But they’ll come back as we age a little bit, right?

MR. ROGERS: Yes. The quicker the better.

THE PRESIDENT: I hope so. I think so. It may come back fast. Thank you very much. Thanks, Jim.

Okay, thank you all very much. Thank you. Please.

Q How much money are you talking if you have to send checks to everybody? How much money are you talking about?

THE PRESIDENT: That’s all being figured now. And we’re also helping industries like Boeing. We have to help Boeing. We have to help the airline industry. It wasn’t their fault. This wasn’t their fault. And we will do that. We’ll be doing that. So we’re adding it up. It’ll be fine. It’ll come back very quickly once we’re finished with our war with the virus. Okay?

Q Mr. President, this idea of a payroll tax holiday — nothing as big as 12.4 percent has ever been tried. They did 2 percent in 2010.

THE PRESIDENT: They’ve done it in smaller amounts. Yes.

Q They’ve done it in smaller amounts.

THE PRESIDENT: But we have a lot of other —

Q But can the country afford something that big?

THE PRESIDENT: Right, we’re — well, it can definitely afford it. The question is, do we want to go through payroll, or do we want to do — you know, there are four other ways of doing it. And that’s what we’re determining, along with the Senate, right now. The Senate and House — we’re all working on this together, John.

Thank you all very much.

Q Mr. President, what’s your message to the tens of thousands — the tens of thousands of employees of all of these companies who have been furloughed? They live paycheck to paycheck, in many cases. What is your message to them, Mr. President?

THE PRESIDENT: Well, the message is that this was something that happened. It’s nobody’s fault. It happened and we’re going to take care of it. We’ll be bigger, stronger, better than ever before and it won’t take that long.

Thank you very much.

MR. DOW: Mr. President? Mr. President? One?

THE PRESIDENT: Yes. Please.

MR. DOW: Roger Dow, U.S. Travel. I would like to put together what everyone has said here. The numbers are $355 billion is what we’re going to lose, 4.6 million employees will be out of work, and we’re predicting unemployment will go to 6.3 percent. So, it’s now — it’s serious.

CTH is spending time on this issue because the food distribution sector is the most important sector in all commerce. Having some familiarity with the supply chain might help people to understand the challenges; and possibly help you locate product.

The Inversion – Big chain markets; those who spent millions developing their own proprietary ‘just-in-time’ distribution networks and automated ordering systems; are currently the least equipped to deal with the level of demand. Meanwhile smaller chains, or mom-and-pops, who rely on third-party brokered distribution are faster to respond.

Several factors have increased retail market demand for food products and non-perishables. People stocking up, kids out of school, some panic shopping (example toilet paper) and now curfews/quarantines have people purchasing more for ‘meals prepared at home’. Add in a level of closed restaurants and the demand on retail food markets is severely stressed.

In major urban areas the larger retailers are unable to keep up with demand. This is creating an outward spread as people drive further and further distances to find their needs. Those who travel a distance ultimately stock-up more; thus the outward spider web-cycle is created. Based on ground reports Atlanta Georgia is a prime example.

Depending on the distance from the distribution center [SEE HERE] large regional chain outlets are now in a downward inventory spiral without escape. That is: compared to their needs they are not getting near enough product. So long as demand continues at a level beyond distribution capacity this will only get worse; especially for those stores more than 50 miles from their distribution hub.

Costco announced Wednesday that it will start to limit certain items members can purchase in response to the surge in business from the coronavirus, though specific items were not outlined. The membership wholesaler also stated it will start limiting the number of members in stores at one time and asked customers to practice social distancing when shopping. (more)

Part of the reason the larger chains like: Safeway, Kroger, Albertsons, Publix, Mejers, etc are in such bad shape is their reliance on thin ‘just-in-time‘ supply chains. While the proprietary distribution process and JIT is more profitable, it collapses when that distribution needs to triple overnight. Once a point of extreme diminished inventory is reached, it takes a long time to recover. That issue is now crossing into Club stores.

If the consumer demand keeps up at the current pace, these larger regional food retailers will not recover; the outflow will always exceed the ability of the inflow to catch up. They will further reduce operating hours and shoppers will remain frustrated. Until the demand slows down, they simply cannot catch up. They are operating beyond capacity.

Meanwhile the smaller area supermarkets (1 to 10 stores), who use much more costly brokerage distribution, are able to get replenished much faster. Right now they are benefiting from a much more responsive supply chain. In the long term that will change, but in the current phase those outlets are the best option for a better in-stock position.

A limited number of fixed assets are also a choke-point for larger chains blocking their ability to ship product. Proprietary tractors, trailers and truck drivers are exhausted and the demand on leased haulers and independents to fill the distribution gap is no-where near enough. The entire country is currently looking for trucks, trailers (refer and dry), and drivers to handle the increased logistical demand.

As a direct result, during this phase of extreme demand, the big regional chain stores, who are usually the most efficient, are now the least dependable; particularly if they are far away from their distribution warehouse. Smaller retail operations are doing much better.

So if you are looking for product and have the time to travel (gas is cheap now too), you might consider these options: (A) travel to the retail stores closest to the distribution centers for regional/national outlets (should be less than 100 miles). (B) travel to smaller retailers that don’t have as many stores. Don’t forget to bring a cooler for perishables.

[However, a note of caution on the “B” option… over time (less than 10 days) they too will lose their ability because the broker distribution network (for independents) will end up in the same position as the larger corporate and regional retailers.]

Hopefully this panic shopping will stop soon. There is no need for many of these shortages other than the psychology of worry and fear. The fear is made worse when someone goes to their favorite store and sees aisles of empty shelves… that then creates a psychology to purchase even more… and so it goes.

Hopefully all restaurants will adapt soon, there will be more food options available, and people will settle down from the panic shopping. The seemingly endless quest for toilet paper is really one of the weirdest shortages.

This too shall pass….

Try to avoid this (crazy video):

Jameson Lopp

✔@lopp

When you didn’t prep because prepping is for the paranoid.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America