Posted originally on the conservative tree house on July 10, 2022 | Sundance

Barrons has an interesting article on an increase in bank auto repossession rates connected to defaults [see here]. Essentially, used car prices have surged significantly and the timeline seems to indicate the temporary covid-19 stimulus spending had a lot to do with the increase in demand.

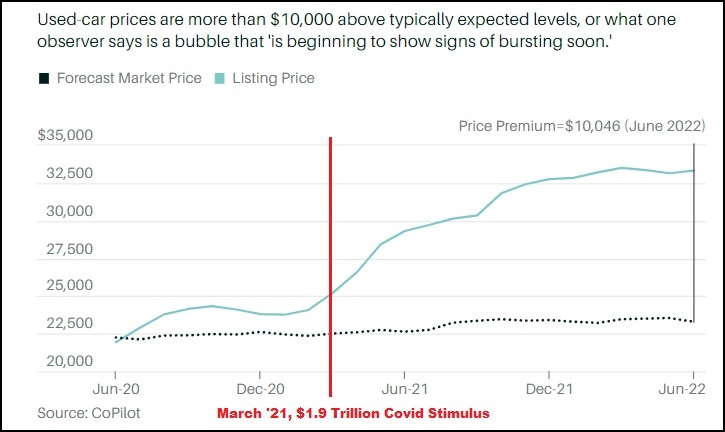

According to data assembled by CoPilot, used cars are currently priced approximately 10,000 higher than they would be without any pandemic related influence, supply side or demand side. Banks and financial institutions loaned money into the climbing market price. However, the artificially inflated car prices now create a bubble where the liability on the books is significantly higher than the repossessed asset is worth.

A higher rate of auto loans are now defaulting for both sub-prime and prime borrowers (double for both), indicating the former buyers are under financial pressure and can no longer make their car payments. The loan to value ratio was as high as 140% when the banks made the loans, a more traditional or normal ratio is 80%.

The banks have a vested financial interest in limiting the number of repossessed vehicles they allow into the used car auction market in order to keep the book value of the cars as high as possible. Those banks and financial institutions have recently rented more storage space for the vehicles being repossessed.

Barrons – […] Lucky Lopez is a car dealer who has been in the business for about 20 years. In recent meetings with bankers, where he bids on repossessed vehicles before they go to auction, he has noticed some common characteristics of the defaulted loans. Most of the loans on recently repossessed cars originated during 2020 and 2021, whereas origination dates are normally scattered because people fall on hard times at different times; loan-to-value ratios, or the amount financed relative to the value of the vehicle, are around 140%, versus a more normal 80%; and many of the loans were extended to buyers who had temporary pops in income during the pandemic. Those monthly incomes fell—sometimes by half—as pandemic stimulus programs stopped, and now they look even worse on an inflation-adjusted basis and as the prices of basics in particular are climbing. (read more)

Somehow, I would hazzard a guess, if we are to follow recent precedent, that taxpayers are going to end up backstopping the financial institutions when the bubble in this asset class pops. However, that said… the scale of these loan defaults could also foretell a significant slipping in the housing market.