QUESTION: Mr. Armstrong; People are adamant that there is a move to return to the gold standard. They claim various scenarios. Is there any such plot by the IMF and it seems strange that the ECB gold reserves are minimal. Can you explain the truth in this matter?

Thank you

GS

ANSWER: The IMF has actually been jockeying positions for decades to remove gold as a monetary instrument quite to the contrary of these reports. IMF Special Drawing Rights (SDR) was first established with one SDR being equal to 0.888671 gram of fine gold, which was the par value of the US dollar on July 1, 1944. The IMF acquired its gold holdings through four main channels. First, 25% of initial quota subscriptions to join the IMF and subsequent quota increases were to be paid in gold. This represents the largest source of the IMF’s gold. Furthermore, all payments of charges (interest on member countries’ use of IMF credit) were also normally made in gold. The structure was established with Bretton Woods and then a member wishing to acquire the currency of another member could do so by selling gold to the IMF. The major use of this provision was sales of gold to the IMF by South Africa in 1970–1971. Thereafter, member countries could use gold to repay the IMF for credit previously extended.

The IMF has decided to either return gold to member countries or to sell some of its holdings. The reasons for this are varied; between 1957 and 1970, the IMF sold gold on several occasions to replenish its holdings of currencies. The IMF also sold gold to the United States and invested in U.S. government securities to offset operational deficits during this same period.

The Second Amendment was to make the SDR the principle reserve asset in the international monetary system, paving the way to remove gold as the ultimate reserve asset. The Second Amendment to the Articles of Agreement in April 1978 fundamentally changed the role of gold in the international monetary system by eliminating its use as the common denominator of the post-World War II exchange rate system. Gold ceased to be the basis of the value underlying the SDR. The Second Amendment, therefore, abolished the official price of gold and ended any obligatory use in transactions between the IMF and its member countries. Consequently, the Second Amendment of 1978 decreed that the IMF would no longer manage the price of gold or establish a fixed price. This, in part, helped the rally initially to $400 by 1979.

Under the Second Amendment to the Articles of Agreement, the use of gold in the IMF’s operations and transactions was very limited. Furthermore, the IMF may sell gold outright according to prevailing market prices under the 1978 Second Agreement. It may accept gold in the discharge of a member country’s obligations (loan repayment) at an agreed price based on market prices. This officially ended the idea of a gold standard set out at Bretton Woods. If the IMF were to sell gold, it would require Executive Board approval by an 85% majority vote. Therefore, the Second Agreement eliminated any IMF authority to engage in gold loans, gold leases, gold swaps, or use of gold as collateral. The IMF also no longer had the authority to buy gold under the Second Agreement formally ending the gold standard.

So in short, the IMF had been desperate to remove gold as a monetary instrument. From the mid-1960s, the total central bank gold reserved fell by about 25% by 2007. There is no evidence of any intent to return to a gold standard, and if anything, the hope is that the IMF will take on the role of making the SDR the new reserve currency that will replace the dollar when everything crashes and burns.

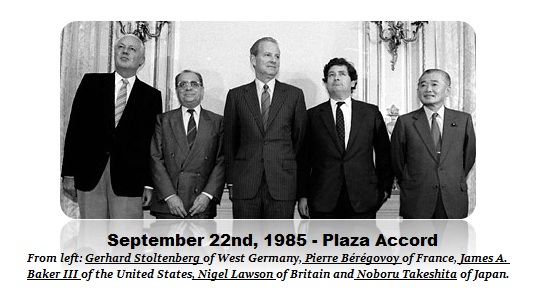

In the first six months of the year, the raw data has shown that several central banks have been selling US government bonds in an attempt to support their currencies against the dollar. This has come in part at the request of the United States, exactly as took place back in 1985 at the Plaza Accord. The United States has a strikingly different view as to currency value. You even hear Trump calling China a currency manipulator because they have seen a declining currency. He does not view that this has been a global trend. Nonetheless, European central banks see a weak current as a weakness politically and thus want a high valued currency.

In the first six months of the year, the raw data has shown that several central banks have been selling US government bonds in an attempt to support their currencies against the dollar. This has come in part at the request of the United States, exactly as took place back in 1985 at the Plaza Accord. The United States has a strikingly different view as to currency value. You even hear Trump calling China a currency manipulator because they have seen a declining currency. He does not view that this has been a global trend. Nonetheless, European central banks see a weak current as a weakness politically and thus want a high valued currency.

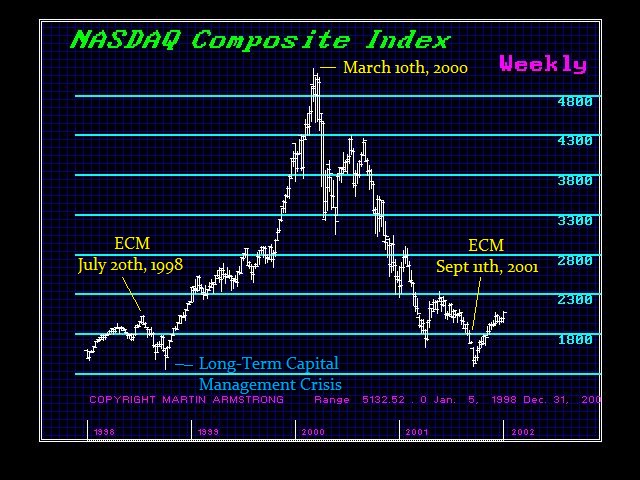

Finally, the Dow made new highs in the face of constant calls for a crash. This past week, in a horse race we would call it a trifecta where the Dow Jones Industrials, S&P 500,and the NASDAQ all made new record highs. This sent a bunch of analysts to look again and began to proclaim that this was the first time that all three major indices have reached new highs on the same day since 1999. They then look at the charts and pronounce that the 1999 rally lasted only until 2000 and then crashed. Of course that was the DOT.COM Bubble and there was a massive wave of retail investor in the market back then compared to today.

Finally, the Dow made new highs in the face of constant calls for a crash. This past week, in a horse race we would call it a trifecta where the Dow Jones Industrials, S&P 500,and the NASDAQ all made new record highs. This sent a bunch of analysts to look again and began to proclaim that this was the first time that all three major indices have reached new highs on the same day since 1999. They then look at the charts and pronounce that the 1999 rally lasted only until 2000 and then crashed. Of course that was the DOT.COM Bubble and there was a massive wave of retail investor in the market back then compared to today.