Armstrong Economics Blog/Central Banks

Re-Posted Oct 5, 2017 by Martin Armstrong

QUESTION: Do you you really think Trump would let the Central Banks Default? He said we would write off PoteRicos debt maybe he plans to write everything off can he do that? If this really did happen wouldn’t the dollar be worthless?

S

ANSWER: It seems as though far too many people ASSUME that all central banks were created EQUAL. Sorry – that is just not the case. These people who do not really know what they are talking about assume that just because the Fed has the power to create elastic money, that therefore the ECB can do the same thing. SORRY – WRONG!!!!

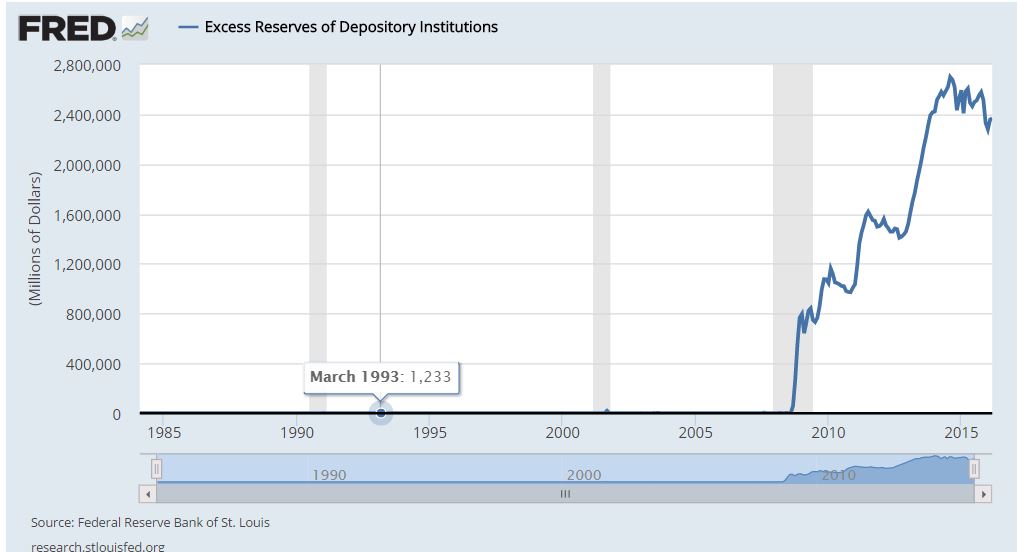

![]()

There is a substantial difference between the Federal Reserve and the European Central Bank (ECB).

The accounting at the Fed allows for it to CREATE money as needed. Now the fiat crowd will argue that the Fed can just create money in a very ELASTIC money supply. This is true and it was intended from the very outset that when economic declines appeared, the leverage within the system would implode and thus to ease that contraction in the supply of money. Hence, the shortage of money resulted in defaults and assets decline in value relative to the contraction in money supply. Therefore, the Fed was created with the power to create ELASTIC money based upon the system of Clearing House Certificates that had pre-existed during the 19th century. The Clearing House would issue its own money and then after the crisis, that money was retired – hence the term ELASTIC.

So how does this contrast with the ECB? Here in lies the problem. The ECB is NOT authorized to create

an ELASTIC MONEY SUPPLY. Germany would never allow that. Consequently, the ECB cannot continue to just buy-in sovereign debt of member states as the market forces come down upon them. The ECB, unlike the Fed, will run out of money and then there will be a very public crisis whereby the ECB will have to be recapitalized. I wrote about this before in Federal Reserve v ECB.

I warned back then that “Something will have to give in Europe.” The ECB was granted a ceiling to buy in government bonds. It cannot just print money with no end in sight. It must get approval, which the Fed does not require from Congress. The two are completely different animals.

On top of this, each member state retained its own central bank. Each member bank issues euros in their domestic economies. You can collect euro coins from each central bank – the ECB does not issue them.

On top of this, each member state retained its own central bank. Each member bank issues euros in their domestic economies. You can collect euro coins from each central bank – the ECB does not issue them.

Then the reserves of the European banking system had to be politically correct and the reserves were composed of all member bonds. Why? Germany opposed a single European debt issue.

Now, the Fed bought in $4 trillion against $20 trillion and the debt was only federal. The ECB bought the worst debt and now owns 40% of the total debt of the Eurozone members. Why is the ECB in danger of a default?

If there is a disagreement in Brussels, then the ECB runs out of cash. As interest rates rise, the value of its balance sheet will collapse. The ECB cannot sell the debt back to the market for there is no bid. To try to support the debt market, Brussels made it illegal to short government debt. Hence, there is no free market in European sovereign debt. If the ECB bought 40% of all debt, who is going to buy it when they stop?

This is a completely different perspective v the Federal Reserve which will just let its US federal debt holdings mature and expire. They too cannot sell the debt or interest rates would explode.

Welcome to the reality of the crisis. NOT all central banks were created equal. Those who paint them all with the same brush know nothing about what they are talking about. The ECB claims it cannot go bankrupt because it will just issue more money. The fact that they have even stated that demonstrates there is a huge problem. That depends upon one thing – approval from the politicians to issue more money.

I meet with central banks directly! This is comments about a field I only read about in the newspapers. I am not even sure the newspapers ever reported the actual differences between the central banks.

Governments are NOT a single entity. Central Banks are far too often on the opposite side of the table with the Political side of government. It is far more complicated than most people would ever guess