I have explained that we know nothing about who created blockchain, but it allows every transaction to be traced. With a credit card, they can tell if you bought something. With Bitcoin, they can tell I gave you money first, and then you bought something. Central banks are moving to cryptocurrency because this will ensure 100% tax collection. The Bank of England was saying that parents will be able to control what their children spend money on. The problem is that the government will control what we too can spend on. Here is the BIS telling you the reality of the future. They want 100% of all transactions taxed. I suppose the girl next door will have to watch your kids for payment in kind — chocolate bars or clothes.

Posted originally on the conservative tree house on July 2, 2021 | Sundance | 106 Comments

CTH has said repeatedly the road to serfdom is cemented with the catch-phrase “a service driven economy.” The June jobs report from the Bureau of Labor statistics [BLS LINK] highlights the JoeBama economic policy exactly that way.

Approximately 850,000 jobs were gained in June; however, simultaneously the number of long-term unemployed increased by 233,000 to the current state of four million.

While we should expect to see the leisure and hospitality industries as well as education rebounding from the various COVID-19 shutdowns, and indeed they did ( +343,000 and +155,000 respectively), manufacturing was flat (+11,000), and construction was down -7,000. The details inside the data are not as great as the top-line would presume.

CTH looks at alternative data connected to the overall economy; empirical data and sector specific trends inside industry. The biggest domestic issue is inflation, stunningly large increases in prices for fast-turn consumer goods like food and fuel. Inflation is one of the primary reasons we have stated home values and home sales have peaked on a MACRO level despite the massive amount of real estate investment purchasing underway by financial institutions.

When we look at durable good production, we focus on the primary drivers of higher cost middle-class or working class products. Seeing construction jobs decline by 7,000 at the same time real-estate values are increasing only points to the problem of working class not being able to afford new home purchases. In the real estate sector this is unsustainable; it is simply a matter of math, income stability and wages.

The same issue applies within the auto-manufacturing sector. Auto jobs were down -12,000 in June. Automotive manufacturing companies operate their production forecasts on short-term (6 month) and longer term (up to 5 year) analysis. The auto industry gets immediate (in real time) feedback throughout the supply chain, distribution and sales. They modify their employment quickly.

There are now 7,000 less construction workers and 12,000 less auto workers in June than May. This directly aligns with inflation and the substantial decline in real wages.

Additional confirmation of a weak blue-collar jobs situation shows up in work hours. In June “the average workweek for production and nonsupervisory employees on private nonfarm payrolls declined by 0.2 hour to 34.1 hours. (See tables B-2 and B-7.) This is not a sign of a healthy, broad-based expanding economy.

25,000 day-care workers went back to work; that’s good. That reflects the service workers going back to work in leisure, hospitality, hotels, restaurants, bars, venues and other service driven sectors. However, even that gain of 25k is soft when you consider the scale of U.S. unemployment which was unmoved at 5.9%.

The top-line data looks good with 850,000 jobs created, but when you look at the “good jobs“, those jobs with higher blue-collar wage rates, the outlook is a little more concerning. Everyone is paying more for gasoline & food, and that hits the checkbook quickly. It’s not a matter of random statistics, look at the people around you, your family, friends and community…. what do you see?

We hear almost nothing about corporate investment expanding inside the U.S. economy from either foreign or domestic corporations. Wall Street earnings are being enhanced by the return to a ‘service driven economy‘, unfortunately that creates a bigger wealth gap between the working class and the investment class.

A while back you made mention that there was fear that the dollar would split. I believe this was in the 1970’s, soon after the anchor to gold was lost. If that is the case then it looks like gold reflected that lack of confidence and I wonder whether it really was oil or the lack of confidence that sent interest rates higher?

If the above is true, how can we determine lost confidence today with floating currencies and central banks buying so much sovereign debt? Is there something that will “give way” in your opinion that will be the tell tale sign?

E

ANSWER: Yes, the increased buying of debt by central banks will demonstrate that the appetite for sovereign debt has declined. This is a reflection of the shift from public to private investment. The collapse in confidence came when Jimmy Carter was elected president. Although a nice guy, he was seen as just incompetent. When Russia invaded Afghanistan, that shot gold up dramatically for fear of geopolitical events.

The OPEC price shock created inflation for everything that relied on cheap oil from car production to plastics. This set in motion a systemic wave of inflation as we are witnessing today thanks to the lockdowns which cut off supply routes. Volcker was fixated on inflation and the gold standard so he rose rates excessively to stop inflation but he failed to account for the fact that it would more than double the national debt due to higher interest expenditure. We are witnessing once again a systemic increase in inflation which is once more broad-based.

Posted originally on the conservative tree house June 26, 2021 | Sundance | 133 Comments

Several people have written to CTH for an economic review of our current status. Below this post are two primary precursor articles [Primary One and Primary Two] which outline the economic dynamic in play and how we can look forward with accuracy to what is likely to happen. Despite the deflective talking points by the professional financial pundits this massive spike in inflation is entirely predictable due to Biden economic policy and Biden monetary policy.

Keep in mind the FED has already said in April they would “support inflation” but that’s because while they will not say it openly they know there’s no way to stop it. The massive inflation is a direct result of the multinational agenda of the Biden administration; it’s a feature not a flaw, and it has nothing whatsoever to do with COVID. Also keep in mind the first group to admit what is to come are banks, specifically Bank of America, because the monetary policy is the cause.

There’s no way around this. Despite the pundit and financial class selling a counter-narrative, home prices will crash and unemployment will go up. I know this is directly against the current talking points, but the statistical reality is clear. CTH was the first place who said two months ago that home sales will plummet, that is starting to happen right now. There’s no way for it not to happen, the big picture tells us why.

You might remember when President Trump initiated tariffs against China (steel, aluminum and more), Southeast Asia (product specific), Europe (steel, aluminum and direct products), Canada (steel, aluminum, lumber and dairy specifics), the financial pundits screamed at the top of their lungs that consumer prices were going to skyrocket. They didn’t. CTH knew they wouldn’t because essentially those trading partners responded in the exact same way the U.S. did decades ago when the import/export dynamic was reversed.

Trump’s massive, and in some instances targeted, import tariffs against China, SE Asia, Canada and the EU not only did not increase prices, the prices of the goods in the U.S. actually dropped. Trump’s policies led the largest deflation in consumer prices in decades. At the same time Trump’s domestic economic policies drove employment and wages higher than any time in the past forty years. With Trump’s policies we were in an era where job growth was strong, wages were rising and consumer prices were falling… The net result was more disposable income for the middle class, more demand for stuff, and ultimately that’s why the U.S. economy was so strong.

♦Going Deep – To retain their position China and the EU responded to U.S. tariffs by devaluing their currency as an offset to higher prices. It started with China because their economy is so dependent on exports to the U.S.

China first started subsidizing the targeted sectors hit by tariffs. However, as the Chinese economy was under pressure they stopped purchasing industrial products from the EU, that slowed the EU economy and made the impact of U.S. tariffs, later targeted in the EU direction, more impactful.

When China (total communist control over their banking system) devalued their currency to avoid Tariff price increase, it had an unusual effect. The cost of all Chinese imports dropped, not just on the tariff goods. Imported stuff from China dropped in price at the same time the U.S. dollar was strong. This meant it took less dollars to import the same amount of Chinese goods; and those goods were at a lower price. As a result we were importing deflation…. the exact opposite of what the financial pundits claimed would happen.

In response to a lessening of overall economic activity, the EU then followed the same approach as China. The EU was already facing pressure from the exit of the U.K. from the EU system; so when the EU central banks started pumping money into their economy and offsetting with subsidies they essentially devalued the euro. The outcome for U.S. importers was the same as the outcome for U.S-China importers. We began importing deflation from the EU side.

In the middle of this there was a downside for U.S. exporters. With China and the EU devaluing their currency the value of the dollar increased. This made purchases from the U.S. more expensive. U.S. companies who relied on exports (lots of agricultural industries and raw materials) took a hit from higher export prices. However, and this part is really interesting, it only made those companies more dependent on domestic sales for income. With less being exported there was more product available in the U.S for domestic purchase…. this dynamic led to another predictable outcome, even lower prices for U.S. consumers.

From 2017 through early 2020 U.S. consumer prices were dropping. We were in a rare place where deflation was happening. Combine lower prices with higher wages and you can easily see the strength within the U.S. economy. For the rest of the world this seemed unfair, and indeed they cried foul – especially Canada.

However, this was America First in action. Middle-class Americans were benefiting from a Trump reversal of 40 years of economic policies like those that created the rust belt.

Industries were investing in the U.S. and that provided leverage for Trump’s trade policies to have stronger influence. If you wanted access to this expanding market those foreign companies needed to put their investment money into the U.S. and create even more U.S. jobs. This was an expanding economic spiral where Trump was creating more and more economic pies. Every sector of the U.S. economy was benefiting more, but the blue-collar working class was gaining the most benefit of all.

♦ REVERSE THIS… and you now understand where we are with inflation. The Joebama economic policies are exactly the reverse. The monetary policy that pumps money into into the U.S. economy via COVID bailouts and federal spending drops the value of the dollar and makes the dependency state worse.

With the FED pumping money into the U.S. system the dollar value plummets. At the same time JoeBama dropped tariff enforcement to please the Wall Street multinational corporations and banks that funded his campaign. Now the value of the Chinese and EU currency increases. This means it costs more to import products and that is the primary driver of price increases in consumer goods.

Simultaneously a lower dollar means cheaper exports for the multinationals (Big AG and raw materials). China, SE Asia and even the EU purchase U.S. raw materials at a lower price. That means less raw material in the U.S. which drives up prices for U.S. consumers. It is a perfect storm… Higher costs for imported goods and higher costs for domestic goods (food). Combine this dynamic with massive increases in energy costs from ideological policy and that’s fuel on a fire of inflation.

Annualized inflation is now estimated to be around 8 percent, and it will likely keep increasing. This is terrible for wage earners in the U.S. who are now seeing no wage growth and higher prices. Real wages are decreasing by the fastest rate in decades. We are now in a downward spiral where your paycheck buys less. As a result consumer middle-class spending contracts. Eventually this means housing prices drop because people cannot afford higher mortgage payments.

Gasoline costs more (+50%), food costs more (+10% at a minimum) and as a result real wages drop; disposable income is lost. Ultimately this is the cause of Stagflation. A stagnant economy and inflation. None of this is caused by COVID-19. All of this is caused by economic policy and monetary policy sold under the guise of COVID-19.

This inflationary period will not stall out until the U.S. economy can recover from the massive amount of federal spending. If the spending continues, the dollar continues to be weak, as a result the inflationary period continues. It is a spiral that can only be stopped if the policies are reversed…. and the only way to stop these insane policies is to get rid of the Wall Street democrats and republicans who are constructing them.

Hope that makes sense, and love to all.

~ Sundance

.

Be patient, be respectful, be kind and caring toward all. Don’t look for trouble. However, when the time comes to get in the fight, drop the moral approach and fight for your family with insane ferocity. Fight like you are the third monkey on the ramp to Noah’s arc…. and damned if it ain’t starting to rain.

Posted originally on the conservative tree house on June 26, 2021 | Sundance | 12 Comments

Reposting an earlier article by request as more people are starting to understand why CTH has focused on the financial motivations behind the political ideology for over a decade. It is critical that people understand the landscape. Underline it. Study it. Research the issues and teach everyone about it.

Consider if you will, the backdrop of current U.S. politics; the influence of Wall Street and the multinationals who align with globalism; the reality of K-Street lobbyists writing the physical legislation that politicians sell to Americans; and then overlay what you are witnessing as those same multinationals now attack the foundation of our constitutional republic. All of this is CORPORATISM, a continuum that people were ignoring for decades… Now, thankfully, there is a new awakening.

.

Positive debate on solutions and constructive criticism of approach is always appropriate for our elected officials; heck, that is the essence of our discussion. However, recently there have been many critics of President Trump; many people only just now understanding the problem and proclaiming that President Trump specifically did not do enough to block, impede, stop and counteract the globalist forces that were/are aligned against his effort to Make America Great Again.

Hindsight is 20/20, but there are people who proclaim that Donald J Trump should have been more wise in his counsel; more selective in his cabinet; more forceful in his confrontation of corporate globalists. Let me be clear….

I will never join that crew of Trump critics because I have understood his adversary for decades. CTH did not just come around to the understanding of the enemy. CTH has been outlining the scope of the enemy, the scale of the specific war and the financial and economic power of the opposition for over a decade. We understand the totality of the effort it will take to stop decades of willful blindness amid the American people. We also see with clear eyes exactly what they are doing now, even with President Trump forcefully removed from office, to destroy the threat he still represents.

Donald J Trump was/is a walking red-pill; a “touchstone”: a visible, empirical test or criterion for determining the quality or genuineness of anything political. I have been deep enough into the network of the Deep State to understand the scale and scope of this enemy. To think that President Trump alone could carry the burden of correcting four decades of severe corruption of all things political, without simultaneously considering the scale of the financial opposition, is naive in the extreme.

♦ POTUS Trump was disrupting the global order of things in order to protect and preserve the shrinking interests of the U.S. He was fighting, almost single-handed, at the threshold of the abyss. Our American interests, our MAGAnomic position, was/is essentially zero-sum. His DC and Wall-Street aligned opposition (writ large) needed to repel and retain the status-quo. They desperately wanted him removed so they could return to full economic control over the U.S, because it is the foundation of their power.

You want to criticize him for fighting harder against those interests than any single man has ever done before him? If so, do it without me.

I am thankful for the awakening Donald J Trump has provided.

I am thankful now for the opportunity to fight with people who finally understand the scale of our opposition.

Without Donald J Trump these entities would still be operating in the shadows. With Donald J Trump we can clearly see who the real enemy is.

In these economic endeavors President Trump was disrupting decades of financial schemes established to use the U.S. as a host for their endeavors. President Trump was confronting multinational corporations and the global constructs of economic systems that were put in place to the detriment of the host (USA) ie YOU. There are trillions at stake; it is all about the economics; everything else is chaff and countermeasures.

The road to a “service-driven economy” is paved with a great disparity between financial classes. The wealth gap is directly related to the inability of the middle-class to thrive.

Elite financial interests, including those within Washington DC, gain wealth and power, the U.S. workforce is reduced to servitude, “service”, of their affluent needs.

The destruction of the U.S. industrial and manufacturing base is EXACTLY WHY the middle class has struggled, and exactly why the wealth gap exploded in the past 30 years.

Behind this dynamic we find the international corporate and financial interests who are inherently at risk from President Trump’s “America-First” economic and trade platform. Believe it or not, President Trump is up against an entire world economic establishment.

When we understand how trade works in the modern era we understand why the agents within the system are so adamantly opposed to U.S. President Trump.

♦The biggest lie in modern economics, willingly spread and maintained by corporate media, is that a system of global markets still exists.

It doesn’t.

Every element of global economic trade is controlled and exploited by massive institutions, multinational banks and multinational corporations. Institutions like the World Trade Organization (WTO) and World Bank control trillions of dollars in economic activity.

Underneath that economic activity there are people who hold the reigns of power over the outcomes. These individuals and groups are the stakeholders in direct opposition to principles of America-First national economics. Collectively known as “The Big Club”.

The modern financial constructs of these entities have been established over the course of the past three decades. When you understand how they manipulate the economic system of individual nations you begin to understand why they are so fundamentally opposed to President Trump.

In the Western World, separate from communist control perspectives (ie. China), “Global markets” are a modern myth; nothing more than a talking point meant to keep people satiated with sound bites they might find familiar. Global markets have been destroyed over the past three decades by multinational corporations who control the products formerly contained within global markets.

The same is true for “Commodities Markets”. The multinational trade and economic system, run by corporations and multinational banks, now controls the product outputs of independent nations. The free market economic system has been usurped by entities who create what is best described as ‘controlled markets’.

U.S. President Trump understood what had taken place. He used economic leverage as part of a broader national security policy; and to understand who opposes President Trump specifically because of the economic leverage he creates, it becomes important to understand the objectives of the global and financial elite who run and operate the institutions. The Big Club.

Understanding how trillions of trade dollars influence geopolitical policy we begin to understand the three-decade global financial construct they seek to retain and protect.

That is, global financial exploitation of national markets.

FOUR BASIC ELEMENTS:

♦Multinational corporations purchase controlling interests in various national outputs (harvests and raw materials), and ancillary industries, of developed industrial western nations. {example}

♦The Multinational Corporations making the purchases are underwritten by massive global financial institutions, multinational banks. (*note* in China it is the communist government underwriting the purchase)

♦The Multinational Banks and the Multinational Corporations then utilize lobbying interests to manipulate the internal political policy of the targeted nation state(s).

♦With control over the targeted national industry or interest, the multinationals then leverage export of the national asset (exfiltration) through trade agreements structured to the benefit of lesser developed nation states – where they have previously established a proactive financial footprint.

Against the backdrop of President Trump confronting China; and against the backdrop of NAFTA renegotiated; and against the necessary need to support the key U.S. steel and aluminum industries; revisiting the economic influences within the modern import/export dynamic will help conceptualize the issues at the heart of the matter.

There are a myriad of interests within each trade sector that make specific explanation very challenging; however, here’s the basic outline.

For three decades economic “globalism” has advanced, quickly. Everyone accepts this statement, yet few actually stop to ask who and what are behind this – and why?

Influential people with vested financial interests in the process have sold a narrative that global manufacturing, global sourcing, and global production was the inherent way of the future. The same voices claimed the American economy was consigned to become a “service-driven economy.”

What was always missed in these discussions is that advocates selling this global-economy message have a vested financial and ideological interest in convincing the information consumer it is all just a natural outcome of economic progress.

It’s not.

It’s not natural at all. It is a process that is entirely controlled, promoted and utilized by large conglomerates, lobbyists, purchased politicians and massive financial corporations.

Again, I’ll try to retain the larger altitude perspective without falling into the traps of the esoteric weeds. I freely admit this is tough to explain and I may not be successful.

Bulletpoint #1:♦ Multinational corporations purchase controlling interests in various national elements of developed industrial western nations.

This is perhaps the most challenging to understand. In essence, thanks specifically to the way the World Trade Organization (WTO) was established in 1995, national companies expanded their influence into multiple nations, across a myriad of industries and economic sectors (energy, agriculture, raw earth minerals, etc.). This is the basic underpinning of national companies becoming multinational corporations.

Think of these multinational corporations as global entities now powerful enough to reach into multiple nations -simultaneously- and purchase controlling interests in a single economic commodity.

A historic reference point might be the original multinational enterprise, energy via oil production. (Exxon, Mobil, BP, etc.)

However, in the modern global world, it’s not just oil; the resource and product procurement extends to virtually every possible commodity and industry. From the very visible (wheat/corn) to the obscure (small minerals, and even flowers).

Bulletpoint #2 ♦ The Multinational Corporations making the purchases are underwritten by massive global financial institutions, multinational banks.

During the past several decades national companies merged. The largest lemon producer company in Brazil, merges with the largest lemon company in Mexico, merges with the largest lemon company in Argentina, merges with the largest lemon company in the U.S., etc. etc. National companies, formerly of one nation, become “continental” companies with control over an entire continent of nations.

…. or it could be over several continents or even the entire world market of Lemon/Widget production. These are now multinational corporations. They hold interests in specific segments (this example lemons) across a broad variety of individual nations.

National laws on Monopoly building are not the same in all nations. Most are not as structured as the U.S.A or other more developed nations (with more laws). During the acquisition phase, when encountering a highly developed nation with monopoly laws, the process of an umbrella corporation might be needed to purchase the targeted interests within a specific nation. The example of Monsanto applies here.

Bulletpoint #3 ♦The Multinational Banks and the Multinational Corporations then utilize lobbying interests to manipulate the internal political policy of the targeted nation state(s).

With control of the majority of actual lemons the multinational corporation now holds a different set of financial values than a local farmer or national market. This is why commodities exchanges are essentially dead.

In the aggregate the mercantile exchange is no longer a free or supply-based market; it is now a controlled market exploited by mega-sized multinational corporations.

Instead of the traditional ‘supply/demand’ equation determining prices, the corporations look to see what nations can afford what prices. The supply of the controlled product is then distributed to the country according to their ability to afford the price. This is essentially the bastardized and politicized function of the World Trade Organization (WTO). This is also how the corporations controlling WTO policy maximize profits.

Back to the lemons. A multinational corporation might hold the rights to the majority of the lemon production in Brazil, Argentina and California/Florida. The price the U.S. consumer pays for the lemons is directed by the amount of inventory (distribution) the controlling corporation allows in the U.S.

If the U.S. lemon harvest is abundant, the controlling interests will export the product to keep the U.S. consumer spending at peak or optimal price. A U.S. customer might pay $2 for a lemon, a Mexican customer might pay .50¢, and a Canadian $1.25.

The bottom line issue is the national supply (in this example ‘harvest/yield’) is not driving the national price because the supply is now controlled by massive multinational corporations.

The mistake people often make is calling this a “global commodity” process. In the modern era this “global commodity” phrase is particularly nonsense.

A true global commodity is a process of individual nations harvesting/creating a similar product and bringing that product to a global market. Individual nations each independently engaged in creating a similar product.

Under modern globalism this process no longer takes place. It’s a complete fraud. Massive multinational corporations control the majority of production inside each nation and therefore control the global product market and price. It is a controlled system.

EXAMPLE: Part of the lobbying in the food industry is to advocate for the expansion of U.S. taxpayer benefits to underwrite the costs of the domestic food products they control. By lobbying DC these multinational corporations get congress and policy-makers to expand the basis of who can use Food Stamps, EBT and SNAP benefits (state reimbursement rates).

Expanding the federal subsidy for food purchases is part of the corporate profit dynamic.

With increased taxpayer subsidies, the food price controllers can charge more domestically and export more of the product internationally. Taxes, via subsidies, go into their profit margins. The corporations then use a portion of those enhanced profits in contributions to the politicians. It’s a circle of money.

In highly developed nations this multinational corporate process requires the corporation to purchase the domestic political process (as above) with individual nations allowing the exploitation in varying degrees. As such, the corporate lobbyists pay hundreds of millions to politicians for changes in policies and regulations; one sector, one product, or one industry at a time. These are specialized lobbyists.

It is ironic when we discuss corporate financial payments to government officials in foreign countries we call them corrupt. However, in the United States we call it lobbying, the process is exactly the same.

EXAMPLE: The Committee on Foreign Investment in the United States (CFIUS)

CFIUS is an inter-agency committee authorized to review transactions that could result in control of a U.S. business by a foreign person (“covered transactions”), in order to determine the effect of such transactions on the national security of the United States.

CFIUS operates pursuant to section 721 of the Defense Production Act of 1950, as amended by the Foreign Investment and National Security Act of 2007 (FINSA) (section 721) and as implemented by Executive Order 11858, as amended, and regulations at 31 C.F.R. Part 800.

The CFIUS process has been the subject of significant reforms over the past several years. These include numerous improvements in internal CFIUS procedures, enactment of FINSA in July 2007, amendment of Executive Order 11858 in January 2008, revision of the CFIUS regulations in November 2008, and publication of guidance on CFIUS’s national security considerations in December 2008 (more)

Bulletpoint #4 ♦ With control over the targeted national industry or interest, the multinationals then leverage export of the national asset (exfiltration) through trade agreements structured to the benefit of lesser developed nation states – where they have previously established a proactive financial footprint.

The process of charging the U.S. consumer more for a product, that under normal national market conditions would cost less, is a process called exfiltration of wealth. This is the basic premise, the cornerstone, behind the catch-phrase ‘globalism’.

It is never discussed.

To control the market price some contracted product may even be secured and shipped with the intent to allow it to sit idle (or rot). It’s all about controlling the price and maximizing the profit equation. To gain the same $1 profit a widget multinational might have to sell 20 widgets in El-Salvador (.25¢ each), or two widgets in the U.S. ($2.50/each).

Think of the process like the historic reference of OPEC (Oil Producing Economic Countries). Only in the modern era massive corporations are playing the role of OPEC and it’s not oil being controlled, thanks to the WTO it’s almost everything.

Again, this is highlighted in the example of taxpayers subsidizing the food sector (EBT, SNAP etc.), the corporations can charge U.S. consumers more. Ex. more beef is exported, red meat prices remain high at the grocery store, but subsidized U.S. consumers can better afford the high prices.

Of course, if you are not receiving food payment assistance (middle-class) you can’t eat the steaks because you can’t afford them. (Not accidentally, it’s the same scheme in the ObamaCare healthcare system)

Agriculturally, multinational corporate Monsanto says: ‘all your harvests are belong to us‘. Contract with us, or you lose because we can control the market price of your end product. Downside is that once you sign that contract, you agree to terms that are entirely created by the financial interests of the larger corporation; not your farm.

The multinational agriculture lobby is massive. We willingly feed the world as part of the system; but you as a grocery customer pay more per unit at the grocery store because domestic supply no longer determines domestic price.

Within the agriculture community the (feed-the-world) production export factor also drives the need for labor. Labor is a cost. The multinational corps have a vested interest in low labor costs. Ergo, open border policies. (ie. willingly purchased republicans not supporting border wall etc.).

This corrupt economic manipulation/exploitation applies over multiple sectors, and even in the sub-sector of an industry like steel. China/India purchases the raw material, coking coal, then sells the finished good (rolled steel) back to the global market at a discount. Or it could be rubber, or concrete, or plastic, or frozen chicken parts etc.

The ‘America First’ Trump-Trade Doctrine upset the entire construct of this multinational export/control dynamic. Team Trump focused exclusively on bilateral trade deals, with specific trade agreements targeted toward individual nations (not national corporations).

‘America-First’ is also specific policy at a granular product level looking out for the national interests of the United States, U.S. workers, U.S. companies and U.S. consumers.

Under President Trump’s Trade positions, balanced and fair trade with strong regulatory control over national assets, exfiltration of U.S. national wealth is essentially stopped.

This puts many current multinational corporations, globalists who previously took a stake-hold in the U.S. economy with intention to export the wealth, in a position of holding contracted interest of an asset they can no longer exploit.

Perhaps now we understand better how massive multi-billion multinational corporations, and the political institutions they pay for, were/are aligned against President Trump; and they will never relent in their need to see the risk he/we represents destroyed.

I will never relent in my support for anyone who fights this enemy.

I will align with and encourage anyone who joins this fight.

If you are looking for criticism against the only person I have ever witnessed who actually fought our correct enemy, look elsewhere.

Posted originally on the conservative tree house on June 26, 2021 | Sundance | 5 Comments

In April of this year the federal reserve announced they will support the economic agenda of the Biden administration by allowing rapid inflation. The FED was trying to provide cover for JoeBama’s economic plan. The era when the FED could impact inflation is long past. However, the Joe Biden policy impact will be clear, immediate and concise. The U.S. middle-class and blue-collar worker are about to be crushed under rising prices for consumable products.

Increases in inflation hit the working class (Main St) much harder than the investment class (Wall St) and financial elites. Factually the multinationals benefit from U.S. inflation as it puts pressure on domestic companies to ship their manufacturing overseas. Wall Street likes that. This dynamic has been an issue not-discussed by the financial media for decades. First, the Reuters article (when you see “commodity prices” think about the term “consumables”):

REUTERS – The U.S. Federal Reserve has signaled it will tolerate faster inflation for a time to cement the post-pandemic recovery and boost employment, but the side effect is likely to be a faster rise in commodity prices.

[…] After its latest meeting on Wednesday, the Federal Open Market Committee confirmed it will seek to achieve the *twin objectives of maximum employment and inflation at the rate of 2% over the longer run.

[*NOTE: in the new era of global economics these two are mutually exclusive. The FED is intentionally ignoring this point.]

[…] The committee noted price rises have been running persistently below target, so it aims to achieve inflation moderately above 2% for some time to make up the shortfall and anchor expectations at around the 2% level.

[…] The plan is to run the economy hot to achieve faster job gains, especially among disadvantaged groups that are marginally attached to the labour force, before shifting back to inflation control later in the cycle.

But the resulting pressure on global supply chains while the Fed pursues employment increases is likely to generate significantly quicker price rises for raw materials and a range of manufactured items. (read more)

This perspective is fundamentally false and based on assumptions that are decades old economic arguments. The reality of what will happen is exactly the opposite on the employment front.

The JoeBama administration is attempting to hide their economic program behind the smokescreen of a COVID economic bound; but the reality of what will happen is exactly the opposite. Employment is going to drop far below pre-COVID numbers.

The problem that people do not understand, and the federal reserve will intentionally not consider, is that Macro Economic principles no longer apply in the era of global economics and multinational trade. I have outlined this dynamic for years. What did Trump see that politicians were intent on hiding?

WHAT WAS THE PROBLEM?

Traditional economic principles have revolved around the Macro and Micro with interventionist influences driven by GDP (Gross Domestic Product, or total economic output), interest rates, inflation rates and federally controlled monetary policy designed to steer the broad economic outcomes.

Additionally, in large measure, the various data points which underline macro principles are two dimensional. As the X-Axis goes thus, the Y-Axis responds accordingly… and so it goes…. and so it has historically gone.

Traditional monetary policy centered upon a belief of cause and effect: (ex.1) If inflation grows, it can be reduced by rising interest rates. Or, (ex.2) as GDP shrinks, it too can be affected by decreases in interest rates to stimulate investment/production etc. However, against the backdrop of economic Globalism -vs- economic Americanism, CTH is noting the two dimensional economic approach is no longer a relevant model. There is another economic dimension, a third dimension. An undiscovered depth or distance between the “X” and the “Y”.

I believe it is critical to understand this new dimension in order to understand Trump’s MAGAnomic principles, and the subsequent “America-First” economy he was building.

As the distance between the X and Y increases over time, the affect detaches – slowly and almost invisibly. I believe understanding this hidden distance perspective will reconcile many of the current economic contractions. I also predict this third dimension will eventually be discovered/admitted, and will be extremely consequential in the coming decade.

To understand the basic theory, allow me to introduce a visual image to assist comprehension. Think about the two economies, Wall Street (paper or false economy) and Main Street (real or traditional economy) as two parallel roads or tracks. Think of Wall Street as one train engine and Main Street as another.

The Metaphor – Several decades ago, 1980-ish, our two economic engines started out in South Florida with the Wall Street economy on I-95 the East Coast, and the Main Street economy on I-75 the West Coast. The distance between them less than 100 miles.

As each economy heads North, over time the distance between them grows. As they cross the Florida State line Wall Street’s engine (I-95) is now 200 miles from Main Street’s engine (traveling I-75).

As we have discussed – the legislative outcomes, along with the monetary policy therein, follows the economic engine carrying the greatest political influence. Our historic result is monetary policy followed the Wall Street engine. THIS PART IS CRITICAL:

[…] there had to be a point where the value of the second economy (Wall Street) surpassed the value of the first economy (Main Street). [This important acceptance is just common sense. The U.S. GDP is currently around $20 trillion, but the total valuation of the Wall Street stock market is much larger than our GDP. Wall Street is more valuable than Main Street. It is a simple albeit important reality to accept.]

Investments, and the bets therein, needed to expand outside of the USA. Hence, globalist investing.

However, a second more consequential aspect happened simultaneously. The politicians became more valuable to the Wall Street team than the Main Street team; and Wall Street had deeper pockets because their economy was now larger.

As a consequence Wall Street started funding political candidates and asking for legislation that benefited their interests.

When Main Street was purchasing the legislative influence the outcomes were beneficial to Main Street, and by direct attachment those outcomes also benefited the average American inside the real economy.

When Wall Street began purchasing the legislative influence, the outcomes therein became beneficial to Wall Street. Those benefits are detached from improving the livelihoods of main street Americans because the benefits are “global” needs. Global financial interests, investment interests, are now the primary filter through which the DC legislative outcomes are considered.

Here is an example of the resulting impact as felt by consumers:

♦ TWO ECONOMIES – Time continues to pass as each economy heads North.

Economic Globalism expands. Wall Street’s false (paper) economy becomes the far greater economy. Federal fiscal policy follows and fuels the larger economy. In turn the Wall Street benefactors pay back the politicians.

Economic Nationalism shrinks. Main Street’s real (traditional) economy shrinks. Domestic manufacturing drops. Jobs are off-shored. Main Street companies try to offset the shrinking economy with increased productivity (the fuel). Wages stagnate.

Now it’s 1990 – The Wall Street economic engine (traveling I-95) reaches Northern North Carolina. However, it’s now 500 miles away from Main Street’s engine (traveling I-75). The Appalachian range is the geographic wedge creating the natural divide (a metaphor for ‘trickle down’).

By the time the decade of 2000 arrives – Wall Street’s well fueled engine, and the accompanying DC legislative attention, influence and monetary policy, has reached Philadelphia.

However, Main Street’s engine is in Ohio (they’re now 700 miles apart) and almost out of fuel; there simply is no more productivity to squeeze.

From that moment in time, and from that geographic location, all forward travel is now only going to push the two economies further apart. I-95 now heads North East, and I-75 heads due North through Michigan. The distance between these engines is going to grow much more significantly now with each passing mile/month….

However, and this is a key reference point, if you are judging their advancing progress from a globalist vessel (filled with traditional academic economists) in the mid-Atlantic, both economies (both engines) would seem to be essentially in the same place based on their latitude.

From a two-dimensional linear perspective you cannot tell the distance between them.

It is within this distance between the two economies, which grew over time, where a new economic dimension has been created and is not getting attention. It is critical to understand the detachment.

Within this three dimensional detachment you understand why Near-Zero interest rates no longer drive an expansion of the GDP. The Main Street economic engine is just too far away to gain any substantive benefit.

Despite their domestic origin in NY/DC, traditional fiscal policies (over time) have focused exclusively on the Wall Street, Globalist economy. The Wall Street Economic engine was simply seen as the only economy that would survive. The Main Street engine was viewed by DC, and those who assemble the legislative priorities therein, as a dying engine, lacking fuel, and destined to be service driven only….

Within the new 3rd economic dimension, the distance between Wall Street and Main Street economic engines, you will find the data to reconcile years of odd economic detachment.

Here’s where it gets really interesting. Understanding the distance between the real Main Street economic engine and the false Wall Street economic engine will help all of us to understand the scope of the economic inflation lag during the Trump administration. Which, rather remarkably I would add, was a very interesting dynamic.

Trump was in charge… Now think about these engines doing a turn about and beginning a rapid reverse. GDP could, and as we saw did, expand quickly. However, any interest rate hikes (monetary policy) intended to cool down that expansion -fearful of inflation- would take a long time to traverse the divide. That is exactly what happened.

Jerome Powell attempted to block the America First program with interest hikes; however, his efforts were futile because of the distance between the two economic engines. President Trump was focused on assisting Main Street, and Powell’s attempts at impacting Main Street growth couldn’t impact Trump’s program.

During the Trump era we actually imported deflation because China and other nations were attempting to avoid tariff cost increases; so they devalued their currency. The problem for them was that devaluation of their currency not only made their tariffed goods cheaper, it made the non tariff goods cost less. As a result we were importing deflation from around the world.

Inflation on durable goods could not be significant until those nations stopped devaluing their currency. Simultaneously, as international trade agreements were renegotiated the originating nations of those products were forced into the same type of economic detachment described above.

The global manufacturing economies first responded to increases in export costs (tariffs etc.), by devaluing their currency; then they began driving their own productivity higher as an offset, in the same manner American workers went through in the past three decades. The manufacturing enterprise and the financial sector (connected to the consumer) remained focused on the pricing.

♦ Inflation on imported durable goods sold in America, while necessary, was -as we expected- ultimately minimal during this initial period of Trump policy. Predictably, if we stuck with the program inflation would have expanded significantly as time progressed and off-shored manufacturing found less and less ways to be productive. Over time, imported durable good prices would increase – but it was going to come much later; and by that time our own industrial base would be re-established.

♦ Inflation on domestic consumable goods ‘would’ likely rise at a faster pace. However, as we saw U.S. wage rates were respond faster, naturally faster, than any monetary policy because inflation on fast-turn consumable goods became re-coupled to the ability of wage rates to afford them…. and the labor market was on fire. Wages were factually growing faster than inflation during Trump’s term in office.

The economic policy impact lag, caused by the distance between federal monetary action and the domestic Main Street economy, was -under the Trump policy- now working in our favor. That is, in favor of the middle-class. Within the aforementioned distance between “X” and “Y”, a result of three decades traveled by two divergent economic engines, that was our new economic dimension….

What JoeBama 3.0 is proposing now, and what the Federal Reserve just announced they are going to support, is a return to the prior economic model where Wall Street multinationals benefit and the U.S. middle-class is pushed into their intentionally created “service driven economy”.

Inflation on domestic consumable goods (food, fuel, energy) hurts the U.S. middle-class, it does not hurt the multinationals, the elites and Wall Street investors. It takes a long time for inflation to push up wages when the workforce is experiencing lay-offs due to downsizing, outsourcing and expanded imports of multinational products.

But it doesn’t stop there…. If we get too granular, missing the larger picture, it is difficult to understand. However, if we stay at the elevated perspective, understanding leads to awakening. We start to see how the various JoeBama policies intersect.

In generally approximated terms 2020 has delivered a serious financial blow to Main Street businesses.

The COVID-19 lockdowns and shutdowns have led to business in your local community suffering massive losses of income while simultaneously taking on debt directly from lenders or indirectly from government relief efforts. Main Street has been hit hard, some analysts estimate 40 to 50 percent of those service businesses may not recover.

Conversely, the COVID-19 lockdowns and shutdowns have created a massive income benefit for multinationals, Wall Street corporations and big tech. Amazon, Walmart and massive tech companies had their highest earnings ever recorded.

According to most maco-analysis somewhere around forty percent of Main Street economic wealth was lost or suspended in 2020 due to COVID-19. Simultaneously the multinational firms have seen increases in stock evaluations of forty percent. These two almost identical numbers are not coincidental. The billionaire class (multinationals) have gained wealth in an almost identical amount the middle-class (Main Street) lost.

These empirical results are accepted. No-one is challenging the shift of financial resources was/is directly related to regional COVID policy. The math is the math.

Where things change from simple economic math to downstream consequences is where the story is really told.

This is where we are going…

This is where we have been going ever for decades, COVID-19 has (not coincidentally) just sped up the process.

If you take out a national map and: (1) put a green pin in the areas where the lock-downs are most severe (draw a 100 mile circle); then (2) put a red pin in the areas where the riots and local anxiety was highest in summer 2020; then (3) put a white pin in the seven counties where election fraud was prevalent; then (4) put a blue pin in the areas known as “Opportunity Zones“, what you will see is a direct correlation. This is not accidental.

There are more than 8,760 designated Qualified Opportunity Zones (PDF) located in all 50 States, the District of Columbia, and five United States territories. Investors can defer tax on any prior gains invested in a Qualified Opportunity Fund (QOF) until the earlier of the date on which the investment in a QOF is sold or exchanged or until December 31, 2026. (link)

If you are a member of ‘THE BIG CLUB’ with a massive influx in capital due to the benefits of the COVID-19 lockdowns, limits and regulations, the Opportunity Zones are now the perfect place to expand ownership and wealth. Take advantage of the Main Street weakness, make moves with government authorization, and do so without capital gains.

The regions where real property will be purchased at a low cost will, not coincidentally, be the “opportunity zones” where investment transactions without capital gains can be made. The areas where riots took/take place will sell cheap. “Opportunity zones” allow for mass investment moves from billionaire class without paying capital gains taxes.

The mass accumulation of wealth (multinationals) at the upper tier of Big Tech and the multinational billionaire class (technocrats) during COVID is approximately +40% since it began. 40% of Main Street businesses wiped out. Not coincidentally almost 40% of wealth has been transferred from Main Street to the Wall Street mega-corps and multinationals.

“Never let a crisis go to waste”…

Only in 2020 the “crisis” was (yet again) by design. The highest level of COVID mitigation control in the Blue states is not coincidentally in the same states with the largest number of Opportunity Zone regions. As a direct result of this mass transfer of wealth to the upper tier the “opportunity” is an unprecedented level of Main Street ownership by elite interests and foreign nationals.

It gets worse… Just like the banking and real-estate crisis of ’07/’08 the government steps in to back-fill the Main Street losses to the mass U.S. population. When an individual or family receives the relief money, they still cannot support Main Street because in many areas they remained forcibly closed. Paying down debt and making purchases in the same lock-down strata only ends up putting those relief funds into the hands of the banks and multinationals who were allowed to operate.

Continued consumer spending only feeds the beast that is -by policy via purchased politicians- designed to destroy us. In essence, we are paying the Technocrats, bankers and multinational corporations to fatten their bank accounts while the U.S. government re-opens the economy with a finger on the scale to benefit the multinationals.

This is by design….

This has always been the design…

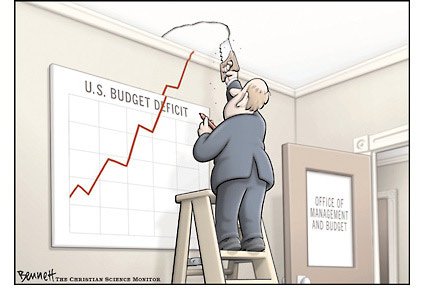

CTH has been warning about this for well over a decade and we exhibited the (un)natural conclusion with this graphic:

I find it interesting how nobody seems to distinguish between a digital currency and blockchain cryptocurrency. The former is not traceable other than that transaction. To eliminate cybercriminals, the World Economic Forum is pushing ending paper money and moving to cryptocurrencies – not digital. With blockchain, the government would be able to trace the money to the criminal. The side benefit will be to ensure everyone pays taxes on everything they ever dreamed of. This is the REAL purpose of cyberattacks that are private decisions and outside the jurisdiction of government to trace and prosecute.

This is why Klaus Schwab is warning of cyberattacks. This is to end commerce globally without government-trackable cryptocurrencies. In 1934 when Roosevelt confiscated gold if you had money on deposit in a bank, which had been in gold coin, Roosevelt seized it all. The difference between a digital currency you use today with a debt or credit card is that is not traceable beyond a single transaction. Bitcoin using blockchain allows the government to trace every person who had that Bitcoin in the flow of money. Crypto is far more than digital and they never want to talk about that either. They will tell you no more credit card theft. Everything will be 100% secure. You will no longer be able to find a $5 bill in the parking lot.

I have written before how the Romans tried to outlaw prostitution declaring you could not pay a prostitute with a coin that had the image of the emperor which they all did. So they created these tokens you would buy from a money changer, you would pay the prostitute and she accepted them because she knew she could go to the money changer and he would convert them to coin.

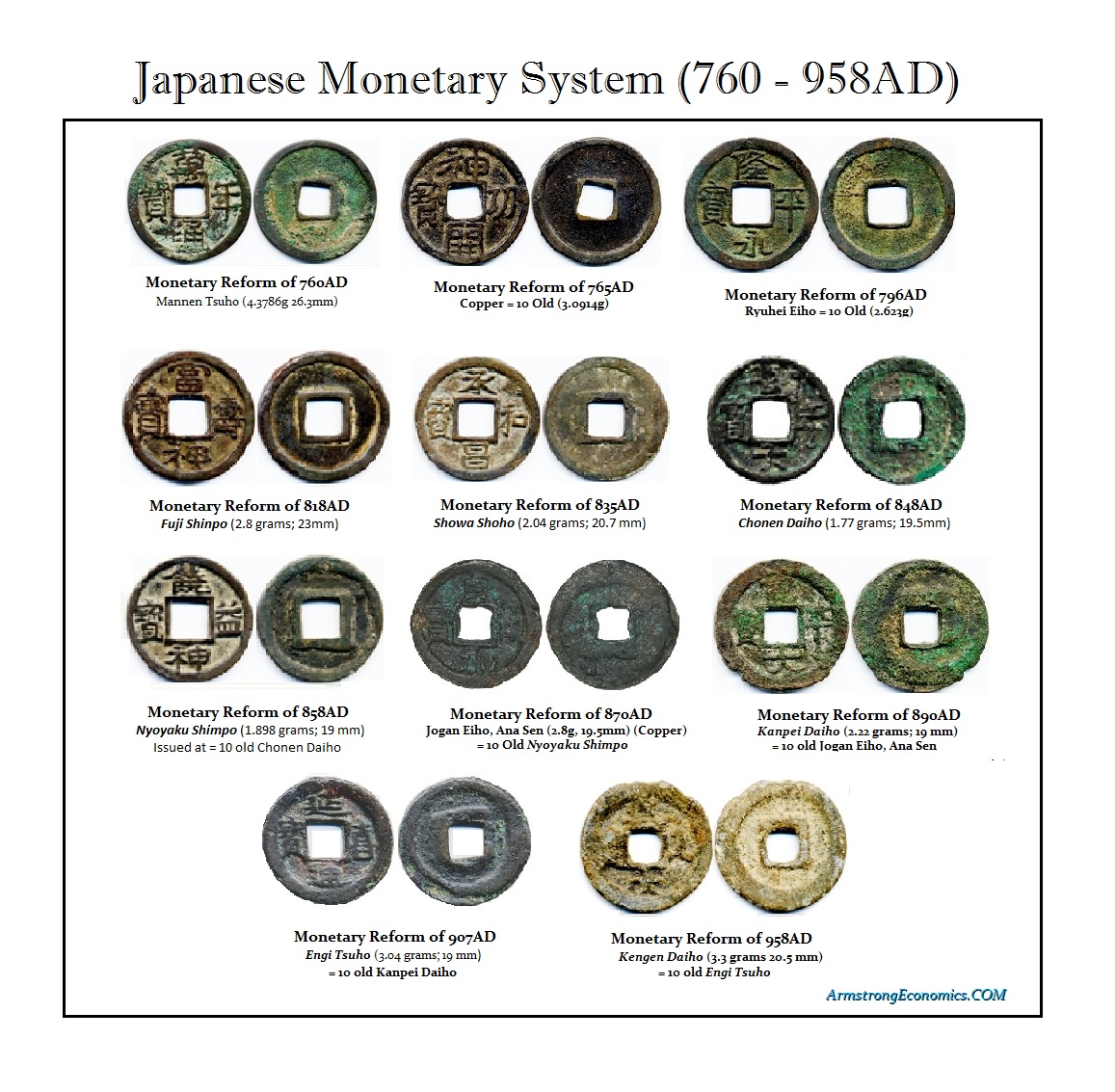

Human nature is resilient. There are already counterfeit COVID cards. In Japan, every new emperor would devalue the outstanding money supply to 10% of his new coins, which also had no metal value. Soon, the Japanese refused to accept Japanese coins. They used Chinese coins and bags of rice. The Japanese government LOST the confidence of its people and was UNABLE to issue coins for 600 years.

They are desperate to get China and Russia into their Great Reset because just as the US dollar is the world currency with 70% of paper dollars circulating outside the United States, that could be replaced by the Chinese currency as was the case back in Japan. Will history repeat? Will we be using Chinese currency because Schwab succeeds in 2023 to end paper money in the West? My advice to China – start printing and imitate the stability of the dollar and never cancel your currency.

Even when Rome fell in 476AD, the barbarians still imitated the Eastern Roman coinage issuing the coins in the name of the Eastern Emperor. This only illustrates my point, that often the currency commonly used is that of another country.

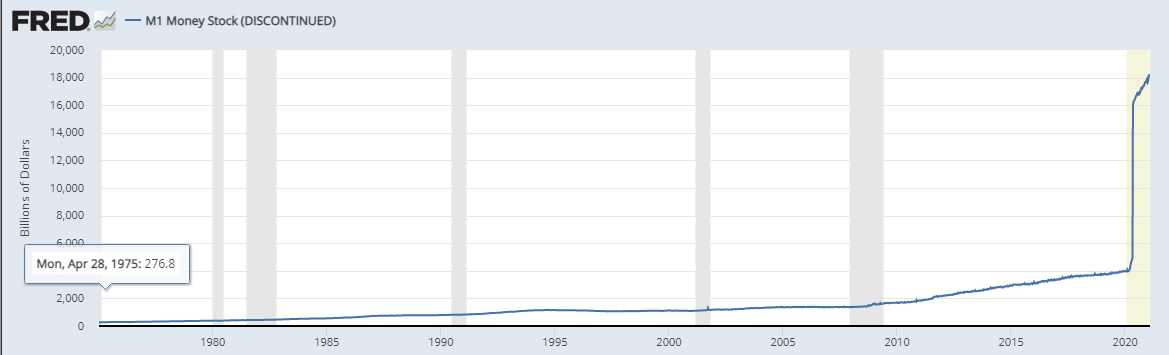

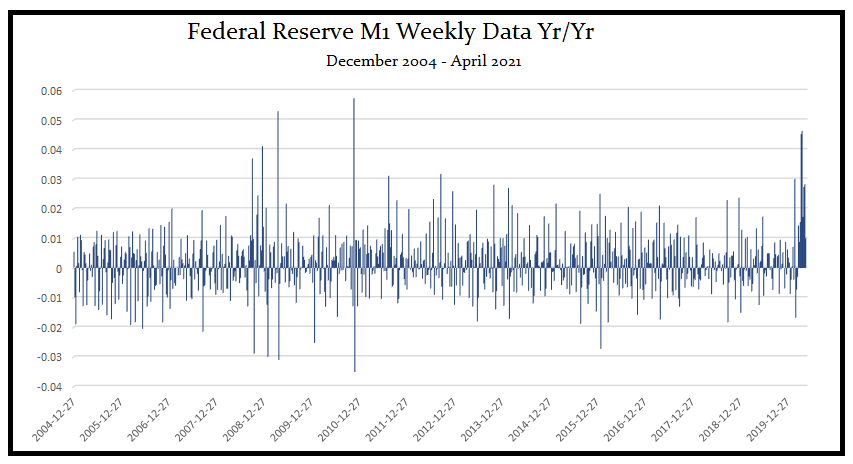

The Federal Reserve has discontinued updating the M1 and M2 weekly money supply series and is instead now updating the series monthly. What is really going on is what I have been talking about and was one of the key subjects behind the book I published – Manipulating the World Economy (5th edition to be released in a few weeks). This change reflects a profound change in economics whereby Keynesian Economics is collapsing. The view at the Fed has been stating what I have been warning was unfolding. Chairman Powell has stated that he no longer regards that the quantity of money is relevant. Powell has stated that the practice of measuring money no longer matters because it’s unrelated to inflation. The Fed now realizes what I have been saying all along – it is a matter of CONFIDENCE.

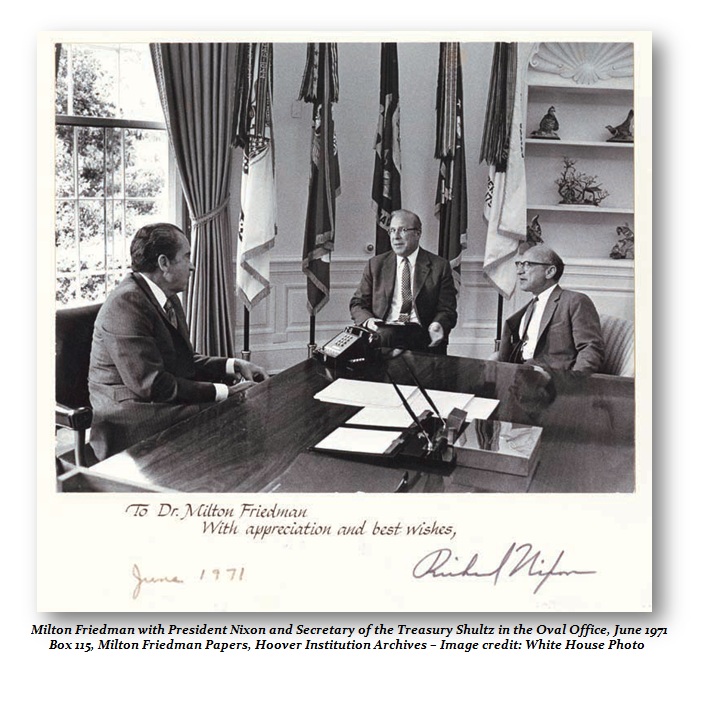

This money supply has been published since the 1970s when the idea of Milton Friedman first took hold as monetarism. It was Milton who convinced President Nixon that the value of money was no longer calculated by the amount of gold in your vault. The Fed has changed the publishing frequency on M1 and M2 money supply from weekly to monthly which is a direct result of the collapse in economic theory, although no economist will explain it that way.

The entire idea behind QE was you increase the supply of money and inflation would follow. They have poured money into the system since 2008 dramatically increasing the money supply which has had ZERO impact on inflation.

The Federal Reserve has realized what I have been saying turns out to be true. In principle, they realize that inflation is not tied to the money supply. Not only has the Keynesian economic theory failed, but so has Monetarism. Now the goldbugs have to realize that inflation is not tied to the money supply and that has nothing to do with hyperinflation and just maybe we can see that the emperor has no clothes after all.

Thank you for all the letters and emails congratulating me on the book and its impact on changing the central banks. The war has not been won. Now they move to the digital world.

FED Notes:

Starting on February 23, 2021, the H.6 statistical release is now published at a monthly frequency and contains only monthly average data needed to construct the monetary aggregates. Weekly average, non-seasonally adjusted data will continue to be made available, while weekly average, seasonally adjusted data will no longer be provided. For further information about the changes to the H.6 Statistical Release, see the announcements provided by the source.

Before May 2020, M1 consists of (1) currency outside the U.S. Treasury, Federal Reserve Banks, and the vaults of depository institutions; (2) demand deposits at commercial banks (excluding those amounts held by depository institutions, the U.S. government, and foreign banks and official institutions) less cash items in the process of collection and Federal Reserve float; and (3) other checkable deposits (OCDs), consisting of negotiable order of withdrawal, or NOW, and automatic transfer service, or ATS, accounts at depository institutions, share draft accounts at credit unions, and demand deposits at thrift institutions.

Beginning May 2020, M1 consists of (1) currency outside the U.S. Treasury, Federal Reserve Banks, and the vaults of depository institutions; (2) demand deposits at commercial banks (excluding those amounts held by depository institutions, the U.S. government, and foreign banks and official institutions) less cash items in the process of collection and Federal Reserve float; and (3) other liquid deposits, consisting of OCDs and savings deposits (including money market deposit accounts). Seasonally adjusted M1 is constructed by summing currency, demand deposits, and OCDs (before May 2020) or other liquid deposits (beginning May 2020), each seasonally adjusted separately.

QUESTION: Hello. I know financial gurus are like noses; but I would like to share something I heard. I heard its’ possible the money in our accounts could be exchanged for – lack of better term – Pelosi dollars. The value of these credits could be changed at will. Buying bitcoin will stop this and put our money out of their reach. I believe they can always get our money. Please explain how bitcoin is vulnerable. Thank you. BS

ANSWER: Look, any cryptocurrency can be seized and outlawed at any moment. They can seize all places that store precious metals for clients. Herbert Hoover admitted in his “Memoirs” that the entire investigation that led to the creation of the SEC was on the back of a phone call where he was told it was a conspiracy against his administration to create the stock market crash. When he realized that there was no such plot, he apologized in his “Memoirs” writing:

“But when representative government becomes angered, it will burn down the barn to get a rat out of it.”

There is ABSOLUTELY nothing the government cannot do. They rigged the election with mail-in ballots and you will never be able to truly verify anything. The medical profession has been converted into a prosecution and political manipulation tool. They have bribed BigTech to do their bidding and they own all the major mainstream media with few exceptions that make little difference. Do you really think they would EVER allow Bitcoin to defeat their agenda?

Drug dealers are not using and cryptocurrency because blockchain can be used to track money. There are programmers working right now on trying to devise a completely new form of cryptocurrency without blockchain to restore privacy. Blockchain technology can be traced! With the propaganda about Bitcoin and blockchain, it offers NO security in any transaction which is deemed illegal. Tax evasion is also a crime. I can CONFIRM that Bitcoin has been allowed to prosper because the government can trace the transactions and that is far better for them than paper money.

There are programmers now fully aware that Bitcoin offers no protection whatsoever and they are trying to create a new system that obliterates the blockchain to make it untraceable

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America