Armstrong Economics Blog/Socrates

Re-Posted Feb 23, 2019 by Martin Armstrong

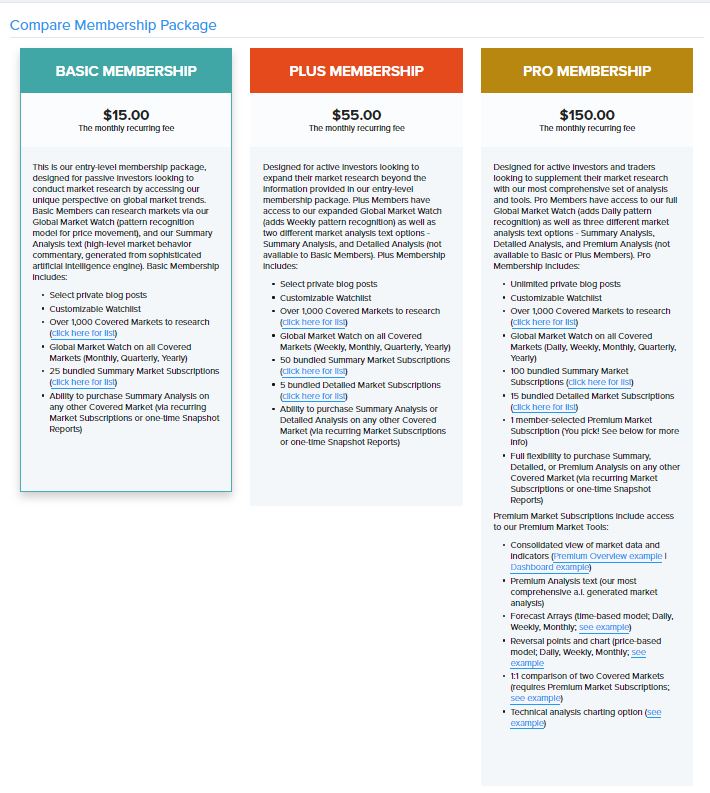

We have created three separate membership options for the Socrates Platform(www.Ask-Socrates.com) which are intended for three separate audiences. First, we have the BASIC Membership service at $15 per month which is intended for the average person who is interested in the broader term with respect to trends and not interested in short-term trading back and forth. Then we have the Plus Membership which provides short-term forecasting for the investor. The third level is the Pro Membership where reversals and arrays are available to access on over 1,000 markets worldwide (requires Premium Market Subscription or Snapshot Report). This is intended for active traders rather than investors who tend to be more position oriented (see comparison).

Then on top of all of this, we have our Institutional Level of service which includes hedging models among other information. While we try to target a version for everyone, it is difficult. The main goal has been to bring the ONLY FULLY FUNCTIONING Artificial Intelligence computer in the world focused on financial markets and global economy, proven over time, to the general public. This is free of personal bias. All of the market analysis (with exception of private blog post commentary) is written by the computer – not analysts. This inspires confidence for everyone knows there is no hidden agenda and there is no conflict of interest. The computer does not own property, mines, manufacture, and beside the fact that it cannot be bribed, it has not national patronage either.

I personally apologize for doing just one blog on Friday for the Pro Version. It is just that there are specific Reversals given so it is not designed to a general investor – we will create a broader view version over the weekend after closings. This is the difference between the three versions of the Socrates Platform, and corresponding private blog posts that are tailored to the three different groups of people we are servicing.

WE HAVE NOT YET COMPLETED THE NEW RELEASE OF SOCRATES

We are still working to finalize various aspects, including adding some additional features and forecasting modules over time. When we are finished with this initial rollout, we will make the formal announcement. Thank you.

Why 50 Million Chinese Homes are Empty

Published on Dec 14, 2018

How 10% of the People Can Make a Difference & Real Estate’s Role

Armstrong Economics Blog/Politics

Re-Posted Feb 20, 2019 by Martin Armstrong

QUESTION: Dear Marty,

First I would like to thank you for all the help you provide especially for us little guys.

I’m from Barcelona, and happily attended the release of “The forecaster” when you were there a few years ago.

I’m under 30 and working my butt off trying to save what I can while paying rent with my partner on a smallish 50m flat (which has become prohibitevely expensive for young local people as rents are at all time highs).

Following your recomendations I’ve put my small savings into movable assets (US and European equities).

With regards to the chart you posted on Spanish Real Estate I was surprised to see the price still so near the bottom of the Housing Crisis. I live in Barcelona and prices are in most cases near or at all time highs for most of the city neighborhoods (of course in € nominal prices wich have dropped quite a bit in $ terms) but as you move away from the city the recovery has been more modest to say the least.

In Barcelona price increses are mostly due to foregneirs moving in and maybe also because people here don’t ussually invest in the stock market but instead put savings into RE (despite the housing bubble people have a big chunk of retirement savings into real estate).

RE is not cheap to say the least but I’m wondering wether I should contract a 30y fixed mortgage and buy a house. My biggest fears are two:

– If long term mortgages dry up I may find out in mkt to mkt loss positions on the house as prices might collapse.

– If the economy declines I have the risk of maybe being fired but still chained to a mortgage.

I fear the later specially since my father has been recently notified that he is going to get fired. The company he works for has decided to fire all employees who are up to 13y!!! close to retirement age (and will probably replace 1/4 of the workforce with cheaper labor).

Given the above do you think it’s still a good time to buy in the big Spanish cities like Barcelona using a fixed mortgage or that you might be better off renting and waiting for the collapse.

Thank you

A.

ANSWER: Barcelona is one of the most beautiful cities in Europe. It is even one of the best places to live. In terms of local earning power, yes, rent in Barcelona is high. In terms of international value, they are cheap, which is why you have so many foreign investors who have poured into your city. Even economically, Barcelona is extremely productive and this was in part behind the reason for the separatist movement. It also had its own history of separatist movements from the Roman Empire (see Maximus 409 AD).

You have noticed the foreign buyers. As the euro drops, the value of property will look cheaper to a foreign investor than domestic. If you stay in the city proper region, this will have an international bid based on currency. In real terms, of course, the property will decline in value. However, this is more of a short-term trend. We all need a place to live. If you can buy with a FIXED rate mortgage, then you will be better off and certainly do not do floating rates. The risk with banks remains that they will stop lending on property as loans turn bad and political turmoil unfolds. Soon it will be an issue of whether Spain will stay in the euro, or whether the euro even exists. The property in the rural area will always be cheaper. So it depends upon what your personal goals might be. Rural property where you have a bit of land and can grow some food is not a bad hedge. But it has been getting cold even in Spain, a country that normally supplies Europe with food during the winter.

We will be heading into a currency crisis. Tangible assets are the way to survive. The biggest problem with real estate is that you cannot take it with you. So keep that in mind. We need a place to live so that is the bottom line. You do not want all your wealth in one asset. You are young enough to survive the major government reset. That will happen. I remain hopeful that if enough people understand the causes behind this crash, then we can make a difference and push back against tyranny.

Make no mistake about it. Government will ALWAYS act in its own self-interest to survive. There has NEVER been a single government that has EVER admitted it is wrong. They must always suppress the people to survive. Remember one thing: even in the USA, there were only three presidents who ever won slightly more than 60% of the popular vote. So, about 10% of the people really decide the fate of nations. We do not have to convince 100% or even 50%. We just need that 10% to make a difference.

Farmers going Bankrupt – A Prelude to a Boom?

Armstrong Economics Blog/Agriculture

RE-Posted Feb 13, 2019 by Martin Armstrong

Part of the cycle for a commodity boom is typically preceded by a commodity depression in which the productive capacity is reduced. We are witnessing that in the agricultural sector. Additionally, extremely cold weather continues. Bankruptcies in the farming sector have been on the rise since 2014. These are the pre-staged events that are required to create a commodity boom for the next cycle — the reduction in supply.

Student Loans – The Economic Time Bomb

Armstrong Economics Blog/Education

Re-Posted Feb 6, 2019 by Martin Armstrong

Trump should reverse what the Clintons did to student loans. He should RESTORE the right to go bankrupt. This huge problem was created by the Democrats who exempted student loans from normal protection for consumers. In addition, the bankers then exploited the entire issue by getting parents to co-sign. The entire argument for eliminating the right to go bankrupt was that they had no collateral. The FRAUD here is the bankers managed to get the Democrats to hand students to them on a silver platter. Then they then pulled a fast one by demanding parents co-sign. That way, they can take their parents’ house.

Trump should reverse what the Clintons did to student loans. He should RESTORE the right to go bankrupt. This huge problem was created by the Democrats who exempted student loans from normal protection for consumers. In addition, the bankers then exploited the entire issue by getting parents to co-sign. The entire argument for eliminating the right to go bankrupt was that they had no collateral. The FRAUD here is the bankers managed to get the Democrats to hand students to them on a silver platter. Then they then pulled a fast one by demanding parents co-sign. That way, they can take their parents’ house.

The scary thing is that the generation of Americans over 60 years of age is on the hook for worthless degrees, owing $86 billion in student loan debt. True, some of these people owe for degrees they themselves obtained in hope of getting a better job. They have discovered that the degrees mean nothing and their age tends to scare companies because of pensions. The bulk of these people in the 60+ group had their kids late in life and co-signed for their children of which 40% are still living at home. Interest rates are not cheap and run from 5.05% to 7% annually. Compound that out and you will nearly double the cost of a degree by interest in 10 years.

A number of major companies NO LONGER require a degree. Here are just a few. BTW – neither do we.

- Ernst and Young (EY)

- Penguin Random House

- Costco Wholesale

- Whole Foods

- Hilton

- Publix

- Apple

LIBOR v SOFR Interest Rates

Armstrong Economics Blog/Interest Rates

Re-Posted Feb 6, 2019 by Martin Armstrong

QUESTION:Dear Martin:

Do you have any concerns for the equity markets from the upcoming conversion from Libor to SOFR (the secured overnight financing rate). A recent article from Business Insider highlighted the following:

“Libor, linked to about $350 trillion worth of financial products, will be replaced by an alternate pricing benchmark for everything from mortgages to credit cards.”

“Replacing Libor will be lengthy and problematic, and is one of the key themes to look out for in 2019 as financial services and asset managers start transferring to new systems.”

“Thousands of existing contracts will need to be renegotiated causing a huge operational and financial burden that will consume legal teams for months.”

“Market structure experts cite the need to amend existing contracts to include “fallback” clauses which which specify what happens when Libor disappears. This is comparatively easy for loans, but for derivatives, swaps, and options, amending existing contracts could potentially lead to legal battles.”

This conversion seems like it could get awful messy.

Regards,

ML

ANSWER: Ever since the London Interbank Offered Rate (LIBOR) scandal, there has been one faction that has sought to eliminate the powers of banks to manipulate the LIBOR rate. This is similar to ending floor tradings in financial markets. Yes, LIBOR has been used to price trillions of dollars’ worth of loans, derivatives, and a lot more. The Federal Reserve moved to actually intervene and prevent a handful of banks to fix the interest rates. The Fed created a group in response, known as the Alternative Rate Reference Committee (ARRC), which has created a new benchmark dollar interest rate. This new rate is known as the Secured Overnight Financing Rate (SOFR). Actually, since April 2018, SOFR has been used for a growing number of bond offerings by large institutions including the World Bank, MetLife, and Fannie Mae. Europe is also moving to create a new benchmark rate that includes the Bank of England, Central banks in Europe with the ECB, Japan, and even Switzerland. This new group is also constructing new benchmark rates. However, there is another reason the Eurozone is taking this giant step. This is a major effort to take the dominance of trading away from Britain in light of BREXIT.

Now as for a crisis, no, that is about as likely as Y2K Millennium bug. Borrowing will take place under SOFR without a problem. The issue will be more with past contracts. That will tend to be a court issue if rates rise under SOFR or old contracts are converted involuntarily. The real issue will be concerning the manipulation of SOFR by governments as they have done with Quantitative Easing. The banks were never able to manipulate LIBOR to the extent of changing the trend. Front-running to elect stops etc. were the “manipulation” tactics. With governments involved, then we can see false trends and real manipulation. The banks could never manipulate LIBOR, suppress the rate, or increase it out of competition.

Italy Falls into Recession

Armstrong Economics Blog/ECM

Re-Posted Feb 1, 2019 by Martin Armstrong

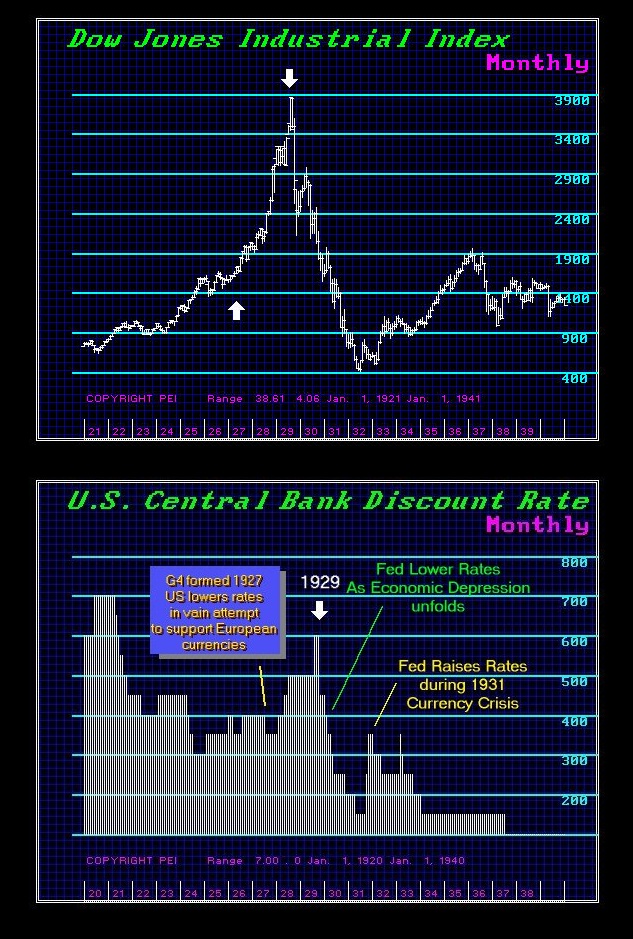

QUESTION: It is official. Italy is now in recession. Obviously, the Fed is looking outside its own economy. Your Economic Confidence Model is remarkable. I have been following you now for more than 10 years. It has always been correct. Why does the economic community and governments pretend you cannot forecast the economy? You have proven the economy can be accurately forecast.

PV, Rome

ANSWER: Yes, Italy has turned down. The Fed knew what is coming. All these pundits who claim the stock market forced the Fed to change policy have only shown their total ignorance of the true factors upon which central banks will act.

I have probably met with more central banks than anyone. They all know the Economic Confidence Model. That is one of the primary questions I am asked by them – where does it stand now. They cannot publicly come out an say the economy will turn down now for fear that they will be blamed. Just look at the Russia-Trump nonsense. They want to pretend that Hillary would have been elected BUT FOR the release of the emails which showed he true colors. Our computer was forecasting she would lose BEFORE any emails were released. The trend was already set in motion – anti-career politicians. Just look around the world and you see the same trend. But it is easy to always blame someone else for your failure. Thus, central banks cannot forecast a decline because if it happens, they would be blamed just like the Russians right now for Hillary’s loss. The central banks can only forecast economic growth, not recessions.

As for the academic community maintaining that the business cycle cannot be forecast, this “opinion” is self-serving. To announce that the business cycle is regular means you cannot control the economy and the entire theory of Marx and Keynes is completely wrong. They kill Kondratieff because he warned the business cycle would kill communism. The economic community would not be able to put out theories to manage the economy and they would have no importance if they admitted they cannot control the business cycle. It is just self-interest.

I have been talking with central bankers for months and it has been about the decline into 2020. That is the backdrop to the Fed’s actions – not the stock market. And as for gold, it rallies because interest rates will decline when the Fed said there is less of a risk of inflation? It just seems the reasoning is never consistent.

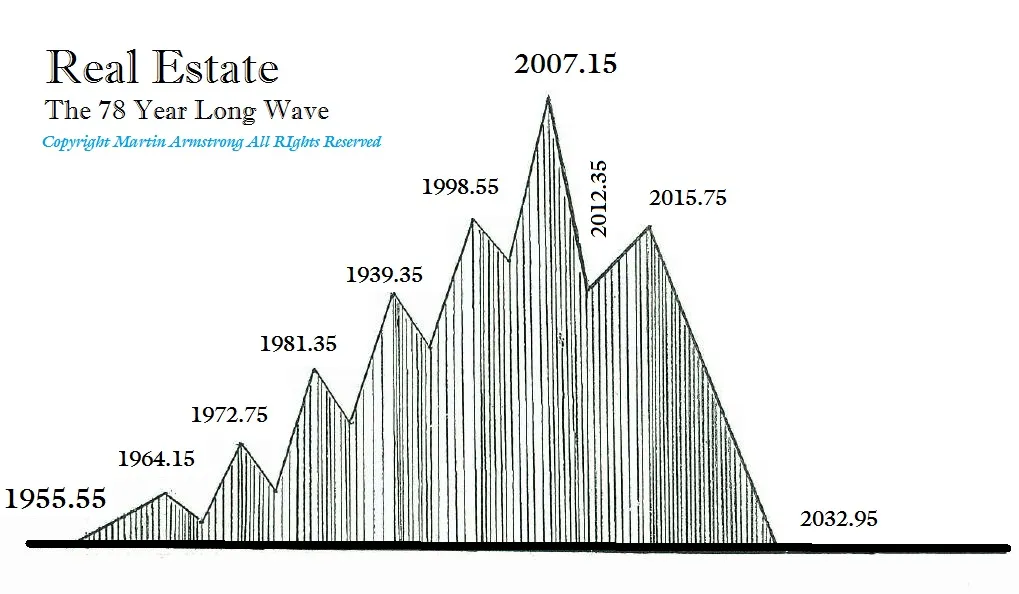

Economic & Real Estate Bubbles

Armstrong Economics Blog/Real Estate

Re-Posted Jan 31, 2019 by Martin Armstrong

QUESTION: I work in the construction industry in Phoenix Arizona and there has been a boom in new construction for apartments, condos massive housing tracts and all of the retail that follows this.

When I read about your worldwide property crash forecast the economic forecast for growth in our market is that that there is no end in sight for the next 6-8 years.

Are these guys whistling past the graveyard??

Thanks and keep up the good work!

JW

ANSWER: There are 8 states without an income tax (Alaska, Florida, Nevada, South Dakota, Texas, Washington, Wyoming, and Tennessee). You are in one of them that is receiving NETpopulation growth. There are herds migrating there from California. Now that said, the real estate market will have an undying bid in those states, but that will be specific to particular regions within the state. However, the trend that will cap the real estate is clearly interest rates and banks. The greater the decline in confidence in government, the less likely it will be to find long-term mortgages. The 30-year fixed rates mortgage will eventually vanish.

During the Great Depression, real estate collapsed to 10% for there was no money available for loans whatsoever. On June 13, 1933, President Roosevelt signed the Home Owners’ Loan Act into law thereby creating the 30-year mortgage to try to give people time to buy a home that they otherwise could not afford without having the cash. This is the 86-year cycle due here in 2019. This really implies that we may see a Directional Change whereby the confidence in the future will start to decline because of political instability. Of course, we can now count on Alexandria Ocasio-Cortez to scream about taxing the rich and their property. The Democrats WILL look into creating a major tax increases and this will seriously harm the economy. We will see a collapse in capital investment resulting in money for 30-year mortgages drying up.

Hence, they always say there is no end in sight to all booms. We should still see 2019 provide a peak in new construction as capital becomes scarce to fund such projects.

Markets Cheer a Recession?

Armstrong Economics Blog/Central Banks

Re-Posted Jan 31, 2019 by Martin Armstrong

The rally in gold and the stock market together is demonstrating that eventually, we will see the alignment as it transforms from Public to Private assets. The most deranged reaction to the Federal Reserve saying they will be “patient” on any further rate moves, is just beyond all reason. But markets are not always rational – they tend to trade emotionally much of the time.

The Fed also said that it would be flexible on the path for reducing its balance sheet. The Federal Open Market Committee’s statement twice refers to “financial developments.” The actual passages Powell read the first one verbatim in his press conference

“In light of global economic and financial developments and muted inflation pressures, the Committee will be patient as it determines what future adjustments to the target range for the federal funds rate may be appropriate to support these outcomes.”

“This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.”

The talking heads have so distorted reason that the markets interpreted it as complete capitulation. The two-year Treasury yield, the most sensitive coupon-bearing maturity to Fed policy, dropped like a stone 4 basis points to 2.53% percent. The yield curve steepened, as everyone expected the Fed would stop raising short-term rates. Of course, you have the pundits claiming that Powell has yielded to the correction in the stock market. They argue that Powell and other officials made their new posture clear. Additionally, Powell disclosed that the FOMC is evaluating the appropriate timing for the end of the central bank’s balance-sheet reduction and that they would be looking to finalize their plans on that issue going forward.

The pundits seem to ignore history completely. They are touting that the Fed was backed into a corner by financial-market volatility. It is just totally amazing how ignorant these people are when it comes to the global economy and the business cycle.

The Fed ALWAYS lower interest rates NOT because of the stock market, but because of an economic decline. A stock market decline by itself is no big deal. We did not even elect a single Monthly Bearish Reversal. There was no significant damage from that respect. The real issue being ignored here is the entire world is declining sharply into 2020 on an economic level. Lowering interest rates NEVERsupports a collapse in the stock market. The Fed even raised interest rates as the market was falling in 1931 because the dollar was under pressure during the Sovereign Debt Crisis.

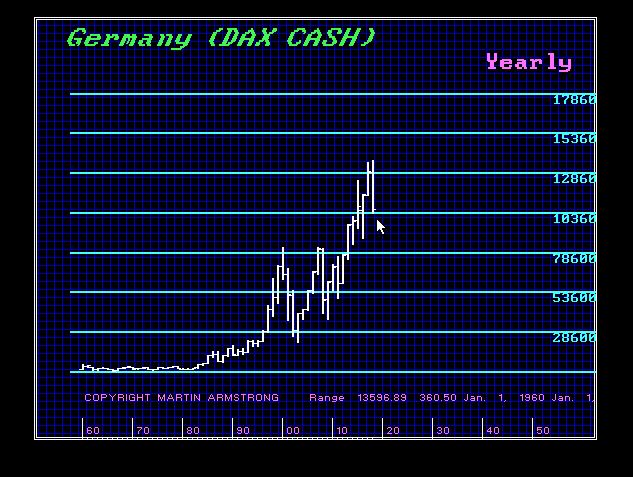

It is so amazing how oblivious pundits are to what is unfolding around the world. Trump is correct. The USA has been the strongest economy. However, the US is starting to slow and overseas is having a very bad dream. Just look at the DAX which not only was a major crash, it closed BELOW the low of 2017. The US market has been the BEST performer. The Fed is NOT taking action based on the stock market. That is absurd.

The US share market has outperformed everything in terms of currency from the international perspective. While the pundits had forecast Europe as a great buy two years ago, people simply lost tons of money on that forecast and their buy of Emerging Markets.

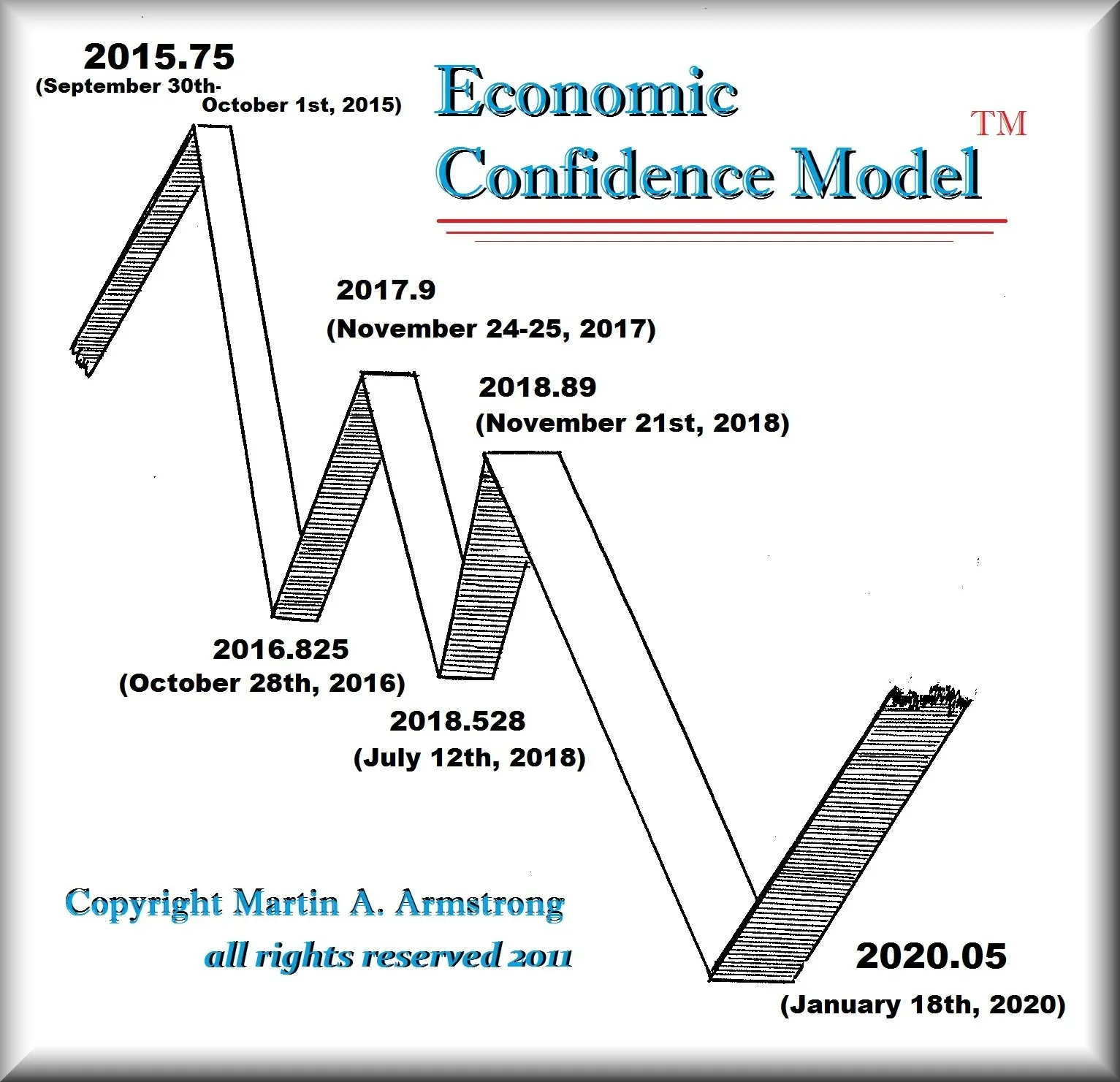

We are now going to go down very hard economically into 2020. The Fed is under a lot of pressure from other central banks pleading with it to stop raising rates for they cannot raise rates. The ECM is in no position to stop Quantitative Easing. The Fed’s actions here have ZERO to do with the stock market. This is the culmination of the economic decline into 2020 that began in 2015.

The Fed is not going to lower rates dramatically. While rates closed at 2.5% for 2018, resistance still stands at 2.67% here in 2019 so rates have not broken out just yet. It is unlikely that the Fed will lower rates of more than 1%. That could unfold after May if the election in Europe create havoc over the future. So far everything is on target. Last year was a Directional Change and 2019 is a turning point with 2020 coming in as another Directional Change and 2021 in a Panic Cycle. So hang on tight. We are in for some really confusing good times as we conclude this business cycle into 2020. Sorry – the Fed did not lower rates to help the stock market. It lowered rates because we are in a global economic recession into 2020. All I have been hearing is complaints from central banks around the world. They can see what is unfolding.

Thanks to Bankers – Student Loans Are Suppressing our Future & Destroying the Real Estate Market

Armstrong Economics Blog/Interest Rates

RE-Posted Jan 30, 2019 by Martin Armstrong

I have warned that the entire Student Loan Crisis has significantly altered the economy thanks to the Clintons courting the New York bankers making Student Loans the exception to bankruptcy. In Florida, like many other states, if you are in default on your student loans, the medical license to obtained is suspended. The Florida State Board of health has stated that some 900 healthcare workers were in danger of losing their license over the past two years because they were in default of their student loans. The board clarified it worked out repayment plans with most of those workers. It estimates the actual number of health care license suspensions is between 90 and 120 since November 2016. We may yet see the Yellow Vest Movement erupt in the United States over Student Loans.

The situation with student loans has gone from bad to worse. Bankers will try to get the parents to still co-sign for their child – DO NOT DO SUCH A THING!!!!! The degrees are worthless in most fields except health and law. The bankers have circumvented all your legal rights because the student loan is the exception to bankruptcy so they can take your house and you cannot even argue fraud.

Then there is the fact that even death does not relieve a parent of a student loan. Marcia DeOliveira-Longinetti’s son was killed, and after death, the remaining balance of his federal student loans were written off, but not by the state of New Jersey. The state told his mother, “Your request does not meet the threshold for loan forgiveness.” What the Clintons did to students is really horrible. Even Zillow’s research, the big realtor, has reported that student debt has impacted the real estate market in many ways reducing future buyers.

![]() FOX News reported that the U.S. Marshals Service in Houston was arresting people for failing to pay their outstanding federal student loans. Actually, Paul Aker, the subject of the Fox News report, failed to appear in court so the court sent U.S. Marshals to his home where he was arrested for a $1500 federal student loan he received in 1987. Of course, when they arrest anyone, the reason is irrelevant. Everyone is treated the same. If he ran, they would have shot him in the back and killed him on the spot and they would NEVER be prosecuted.

FOX News reported that the U.S. Marshals Service in Houston was arresting people for failing to pay their outstanding federal student loans. Actually, Paul Aker, the subject of the Fox News report, failed to appear in court so the court sent U.S. Marshals to his home where he was arrested for a $1500 federal student loan he received in 1987. Of course, when they arrest anyone, the reason is irrelevant. Everyone is treated the same. If he ran, they would have shot him in the back and killed him on the spot and they would NEVER be prosecuted.

After seven U.S. Marshals burst into Aker’s home with guns drawn, they took him to federal court where he had to sign a payment plan for the 29-year-old school loan. Thank you, Hillary. I honestly do not know how anyone could have possibly voted for her. This is totally insane. The judge could just as easily thrown him in prison on contempt of court and not release him until he pays the $1500. It’s all about a judge’s power to act as if he still represents a king.

The Student Loan Crisis is serious. The US census showed that one-third of children over 30 were still living with their parents. This is also taking place in Britain thanks to rising taxes which lower disposable income. There are greater odds of your children living with you until they are 35. The real shocking number is that 40% of millennials are still dependent on mom and dad. The excuses seem endless. Student Loan debt can make buying a home IMPOSSIBLE! This is part of the reason real estate has been in a bear market since 2007 when we look at the average home.

The entire Student Loan Crisis has altered the real estate market significantly. While the High-End rallied into 2015 as capital was trying to get off the grid, as one friend in the real estate business put it, if prices ever got back to 2007, 50% of the State of New Jersey would go up for sale. The average market for homes has been declining overall. There are pockets where houses have risen, but these upon close inspection are the destinations where people are fleeing to from states like California, Illinois, New Jersey, New York, and Connecticut among others.

The real estate profile has another weight dragging it down – TAXES. Real Estate is IMMOVABLEand as states go broke, they keep raising property taxes. The states with NET declines in population because the smart people have been fleeing, leaving behind people who are not paying attention and become trapped because there are no buyers. One friend here in Florida moved from New Jersey and rents out his home back there because he cannot sell it. He rents it at this stage just to pay the taxes.

The states with no income taxes are a net migration seeking refuge from other places. Florida seems to get New Jersey, New York, and Connecticut. Nevada and Texas are getting those fleeing Illinois and California. Nonetheless, the overall view of real estate looks rather grim into 2032 insofar as scoring REAL gains over the depreciation in the purchasing power of a currency. Then add the rising interest rates and you will discover that bankers are no longer willing to lend money at fixed rates for 30 years.