Posted originally on the CTH on May 13, 2023 | Sundance

Recently I went to the supermarket to pick up some general provisions. Given the nature of previously predicted food price increases, and proactive measures to mitigate the predictable prices, I haven’t needed to purchase basic foodstuffs in a while. Yikes! The prices… Wow.

Since we originally warned in ’21 about the waves of food price inflation that were coming, the prices have more than tripled on many food commodities. That part is not as surprising in current review; however, the prices of processed foodstuffs is, well, quite frankly astounding.

I am left to wonder how working-class people are able to afford the jaw dropping price increases in highly processed food products like condiments (mayo, ketchup, mustard, etc), and even coffee and milk. I knew the processing costs would drive those prices, but the scale is just astounding.

Beyond the foodstuff, what was truly stunning was the current price of non-food items at the store. Items like chemical cleaners, soaps, aluminum foil, trash bags, Styrofoam products, ziploc bags, paper goods, etc. I mean seriously, $8 for a box of trash bags, good grief.

After a review of the non-food item prices, I went back to the recent BLS report [DATA HERE] to look at the producer price index to see if the data reflected the scale of the processing cost that I was reviewing across a broad spectrum of goods.

Are consumers getting gouged by manufacturers who are taking advantage of the price shock inside the ongoing inflation?

Or are the processing costs, mostly driven by energy price increases, really that big a factor in the end product as it is generated?

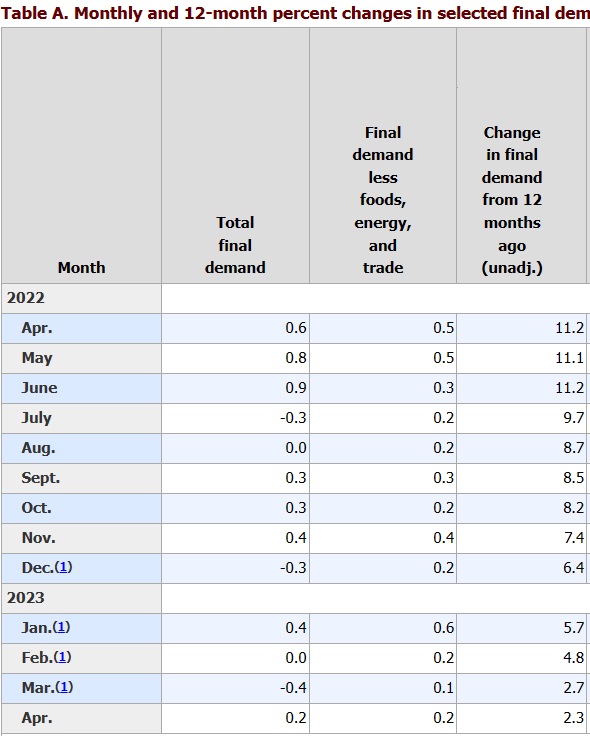

In the topline final demand Producer Price Index [Table A above] you can see how we are cycling through the second wave of inflation that hit in the spring of 2022. The rate of price increase is lower, but the prices are still rising. That means the prior massive price increase is now baked into the product, and the current price will never decline. Instead, it will just increase at a slower rate than before.

However, that’s not the full story… and that is not the data I was most curious about.

The intermediate product costs are really where the story is found.

Raw materials (unprocessed goods) are essentially in a deflationary status [-19.2% in April]. Meaning demand for the raw material has dropped well below the available supply. However, look at how much of the deflationary price is consumed in the processing of the raw materials.

A full 16% is consumed by processing cost increases [energy, physical plant, transit, production costs etc]. That is remarkable.

A random example might be citric acid. The price of the citrus base drops 19.2%, but the processing of the base into the intermediate good phase chews up 16% of the drop in raw material price and exits processing only 3.2% lower in price than a year prior.

Another example might be found in plastics. The petroleum base, and/or a combination of each material additive, might be 19.2% lower than prior year, but processing negates the lower raw material price, and exits into intermediate essentially even -.04, and then toward the ending +2.3% final demand change in the rate of price increase.

The PPI data is essentially showing the flow of costs of production as reflected in the impact during processing. We can assume mostly increases in energy, transport and distribution costs to bring the raw material forward to final good status.

Key takeaway, the demand side of the raw material is diminished. There is less raw material demand. However, processing costs are continuing to drive the final production price of goods that head into the hands of wholesalers who then bring the product to market.

The outcome of this are the prices of processed goods as noted in the products on the shelves.

QUESTION: Are you noticing rather remarkable price increases in non-food goods during your store visits?

As far as the 12 Caesars are concerned, I am doing my best to assemble a few sets. These are not easy to put together. Nevertheless, I am giving it a shot to see what I can do that would be reasonably priced, under that $100k people ask on the market. I believe reasonably excellent VF/XF sets for around $50,000. But this is not something that quantity exists. This is very hard to assemble. I’m still trying to fill in some gaps. They will be presented in a nice wooden case.

Posted originally on the conservative tree house on November 24, 2022 | sundance

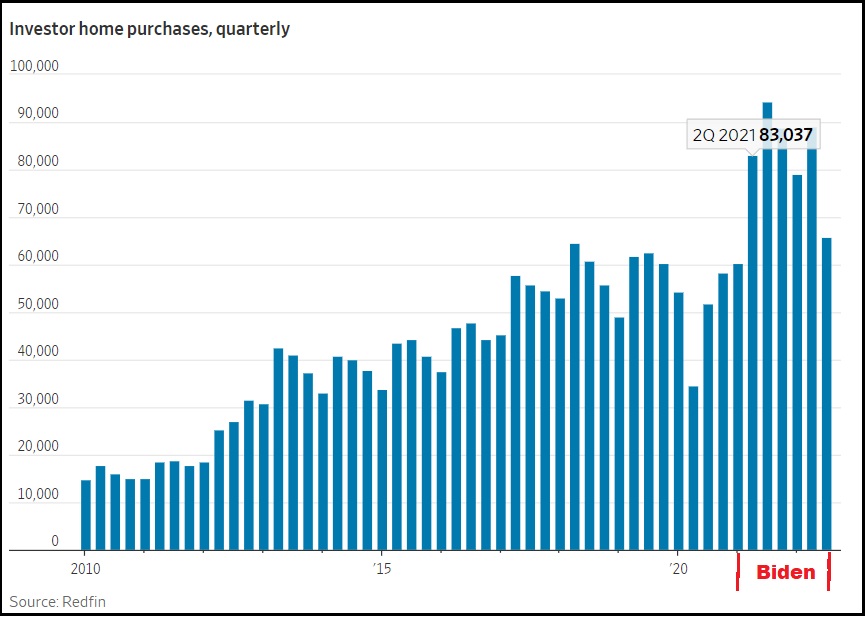

There is a significant lag in all data within the housing market. That said, the third quarter (July, Aug, Sept) data reflects a significant drop in institutional investment within the housing market.

If you look closely at the timing (keep in mind the data reporting lag) what you will notice is that financial institutions began a big surge in purchasing hard assets, specifically real estate, as soon as Joe Biden took office (Jan ’21), and the economic policy became evident. Intangible financial instruments became an immediate risk as the professional financial control groups recognized energy policy would drive inflation (supply side) and devalued money would fuel it (demand side).

As an offset to predictable inflationary policy (the insiders’ game), institutional money (Blackrock, Vanguard etc) was moved into hard assets with tangible value. This shift in asset allocation, institutional sales, helped fuel a false surge in home prices and their valuations. CTH was writing about this in 2021, and sounding alarms as it took place. 25% of all real estate purchases were being made by institutional investors.

The dynamic was predictable. The Biden administration economic policy, energy policy and monetary policy, was going to cause massive inflation. CTH was shouting about it in early 2021 and warning everyone to prepare for waves of price increases that would naturally surface first on high-turn consumable goods, and then embed into longer-term durable goods.

Despite claims to the contrary, this 2021 inflationary explosion had nothing to do with the pandemic or supply chain shortages. It is entirely self-created by western governmental policy; the collective ‘Build Back Better’ agenda. You can see now from the background moves within the financial sectors, they too knew the reality and their money shifts reflected that despite their ‘transitory’ pretending they were mitigating their own exposure.

We the People were yet again going to be victims of specifically intended monetary, regulatory, energy and economic policy.

The investment class rulers of the WEF assembly shifted assets to avoid the pain that we would feel. We “would own nothing and be happy,” and their shifts would position them to own everything and be in control.

Overall govt spending and regulatory controls drove inflation for these past two years. The ‘demand side’ was blamed, despite the lack of demand. I will be proven right when history is concluded with this. Interest rates were raised by central banks in an effort to support the policies that are driving ‘supply side’ inflation, not demand side.

Energy policy was/is crushing the consumer by driving up the cost of all goods and services. To support the overall goal of changing global energy resource and development (a false and controlled global operation), central banks raised interest rates. Various western economies, including our own, have been pushed deeper into a state of contraction by central banks crushing consumer demand, and eliminating investment via increased borrowing costs.

In short, the goal was/is to lower energy consumption by shrinking the economic activity. This, according to the BBB plan, was needed at the same time as energy development was reduced. These economic outcomes are not organic, they are all being controlled by collective western government agreement.

Within this control dynamic, there was always going to be a point where the reaction of the people to their economic reality means the financial control elements need to shift direction. They will always maximize profit and minimized risk, while knowing what the larger objective remains.

Just like every other durable good, housing demand contracts as prices and costs become unaffordable. The loss of equity within your home is damaging to your own value or ability to borrow against it. From the perspective of an institutional asset, that same equity drop is an investment loss. Thus, just as a consumer would exit the housing market, so too will institutional investment groups now control the slow dumping of the asset to remove the equity they pumped into it.

Much of the investment housing will be retained as rental housing, with the monthly rents being part of the returns on the investments. However, as this dynamic unfolds further purchases of houses stop, because the asset overall is declining in value.

(Via Wall Street Journal) – Investor buying of homes tumbled 30% in the third quarter, a sign that the rise in borrowing rates and high home prices that pushed traditional buyers to the sidelines are causing these firms to pull back, too.

Companies bought around 66,000 homes in the 40 markets tracked by real-estate brokerage Redfin during the third quarter, compared with 94,000 homes during the same quarter a year ago. The percentage decline in investor purchases was the largest in a quarter since the subprime crisis, save for the second quarter of 2020 when the pandemic shut down most home buying.

The investor pullback represents a turnaround from months ago when their purchases were still rising fast. These firms bought homes in record numbers last year and earlier this year, helping to supercharge the housing market.

Now, investors are reducing their buying activity in line with the decline in overall home sales, which have slumped with mortgage rates rising fast. (more)

At a macro level, if you bought a home in the last 18 months, or refinanced your home to pull out equity, you still have significant downside exposure. Home prices will continue dropping until they plateau on the downside at the price that existed in roughly June of 2021.

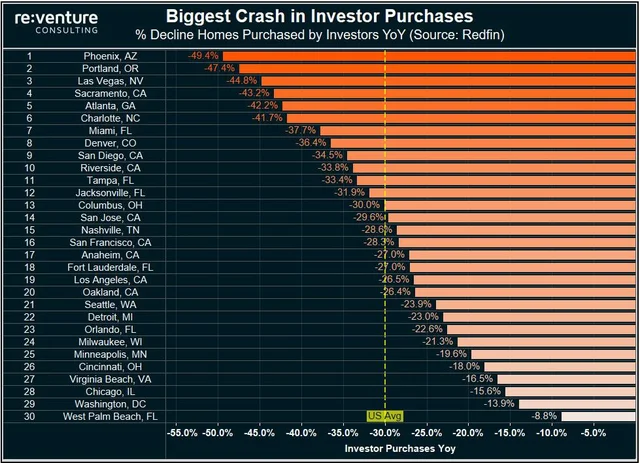

The drop in value is directly related to the regional purchases by the institutions. In areas where higher percentages of overall home sales were made by institutional investors, the subsequent drop in value will be larger (see chart above). In areas where actual people purchased homes to live in, the drop in value will be less significant.

I keep getting this buying question, so with the above in mind I will answer it in the most brutally honest way I can present…..

At a macro level, if you are going to purchase a home on this downslope, look at the historic valuation of that property (or a comparable property) in/around approximately the spring of 2021. Start there, and put your offer in that vicinity, then hold firm without any emotional attachment to it. Do not purchase another groups loss.

Posted originally on the conservative three house on April 13, 2022 | Sundance

Fed Governor Christopher Waller appeared on CNBC to announce we have reached peak inflation, and things will moderate from here. All of these fed moves are political moves, not monetary policy-based moves. Here’s the thing they will never admit to the non-institutional investor.

The fed has been painfully slow to raise interest rates on purpose. They did not make a mistake. The reason for their delay is they needed to wait for the beginning of the first 2021 inflation wave to cycle through before they raised interest rates. It’s a game of mirrors that almost no one sees. WATCH:

The rate of inflation will drop once the statistical year-over-year comparisons reach the same moment in the prior year. The fed will raise interest rates in May and then use the June inflation rate decline as a false talking point to highlight how their policy is working. They wait for May, because they need to wait for the calendar, nothing else. Inflation is measured as the percentage of change from the prior year. By waiting until the inflation is measured against the first wave of rising prices, it will give the illusion of a decline in inflation.

So that’s why they waited. But here’s the worse part….

All of these U.S. Fed monetary policymakers are in full ideological alignment with the global and central bankers. They are all following the same Build Back Better agenda and policy instructions.

All of bankers know the shift from ‘dirty energy’, coal, oil, natural gas, will create inflation. All of the bankers know there is no economic bridge within the plan to shift from oil to their unicorn dust. All of the bankers know that shutting down oil exploration as a matter of western unified policy will, as a factual matter, destroy the economic systems that rely on energy….. which is to say everything.

All of these bankers know the severity of the inflation crisis this energy shift creates. None of them do not know.

Everything they are doing is coordinated to assist the climate change agenda.

Posted originally on the conservative tree house on April 13, 2022 | Sundance

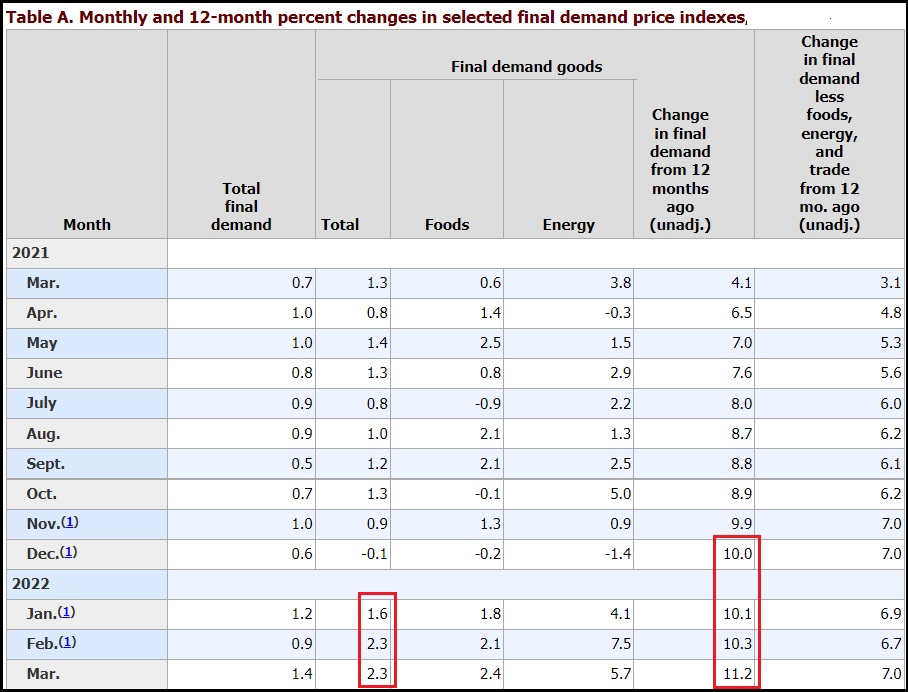

he “Producer Price Index” (PPI) is essentially the tracking of wholesale prices at three stages: Origination (commodity), Intermediate (processing), and then Final (to wholesale). Today, the Bureau of Labor and Statistics (BLS) released March price data [Available Here] showing a dramatic 11.2% increase year-over-year in Final Demand products at the wholesale level. This is the fifth consecutive month with the highest rate of inflation the PPI ever recorded.

The single month increase in wholesale prices of 2.3% was driven by inflation built into the supply chain at every level that shows up in the final wholesale price. Those price increases then get passed along to consumers along with the additional costs for warehousing, transportation and delivery. I modified Table-A (FINAL DEMAND) to take out some of the noise.

Wholesale prices of goods jumped 2.3 percent in March, and the wholesale price of food products jumped 2.4 percent. The total demand inflation compared to last year is 11.2 percent, the highest rate ever recorded since the PPI tracking was first started.

The total final demand monthly calculation (1.4%) is lower than the final demand goods (2.3%), because final demand services are offsetting. You may remember the discussion/analysis about prices beginning to stabilize after this month due to a contraction in demand for goods and services. I see support for that thesis within this data.

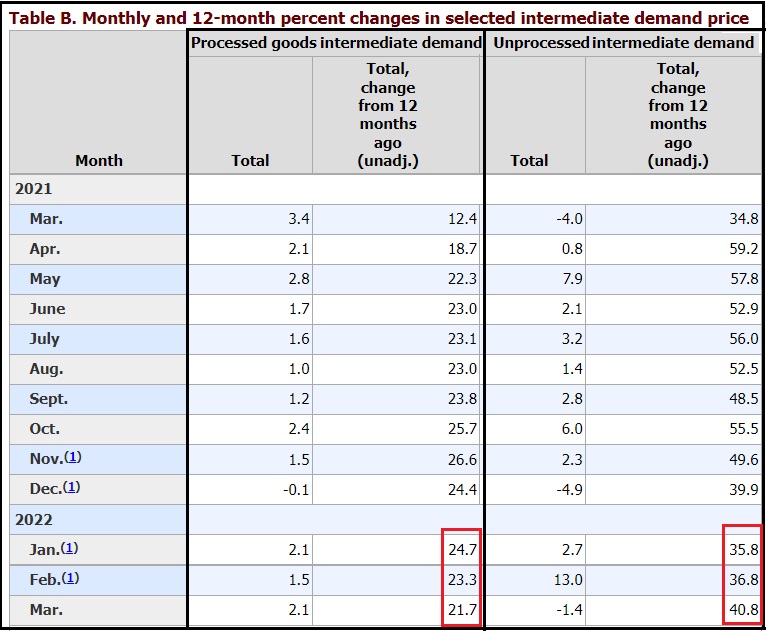

The three phases of wholesale product creation: (1) origination, (2) intermediate, and (3) final, cycle through the economic analysis in reverse chronological order. Roughly speaking, the flow of goods quantified is done in 30-day sequences. Final demand this month is comparing to final demand in March 2021. The intermediate demand goods this month will become final demand goods next month (April).

The rate of inflation behind this set of final demand goods is beginning to soften. See Table B, Intermediate goods. Again, modified to take out the noise:

While the yearly comparison for both processed and unprocessed intermedia goods is eye dropping, in the unprocessed intermediate demand goods, we are starting to see a lessening of monthly price increases.

In essence, prices have been rising so fast and for such an extended period of time, that we are now cycling through the rate of increase and starting to compare it to last year when the rate of increase was originally going high. As a consequence, the rate of price increase will likely lessen, even though the actual price may still keep climbing within the manufacturing process.

The price of raw materials, and the wholesale energy costs to process those materials into finished goods, are still rising. In addition to the consumer prices reported yesterday, this wholesale price data is showing the most recent increases (March) in fuel and transportation costs. For the next report these figures should now plateau.

♦ BOTTOM LINE – We have not yet reached PEAK INFLATION – However, the price increases from wholesalers to retailers are now at parity. The increased price of things coming into the supply chain are now at similar rates of increase when compared to the stuff on the shelves.

Inflation from field to fork is now fully matriculated and embedded in the total economy as a result of two massive price waves (July to October 2021 and November to March 2022). Those prices will never fall.

Highly consumable goods like food, fuel and energy will remain at approximately the price today for a period of around five months, then we will see the third wave kick in as the new higher harvest prices hit the processors in late summer.

The prices for non-essential durable goods, like cars, electronics, appliances etc. from this moment forth will now be determined by demand. Highly sought after goods will increase in price as more customers chase fewer products. However, ordinary or widely available durable goods will likely start to come down in price very soon as inventories climb because consumer spending has prioritized and dropped non essential goods from their shopping lists.

To put it more succinctly: The stuff we need will cost more. The stuff we don’t need will cost less.

COMMENT #1: Well, at least I got the decline accelerating in the Ruble correct and thanks to your models knew the war and commodity cycles were turning up. Getting the fundamentals correct ahead of time is a work in progress and definitely not easy.

But while watching the Ruble crashing into weakness going into the ECM, one could not reverse position and go long the RUB. Heck, nobody could even open new positions and definitely not buy the RUB. All that was allowed was closing already existing positions. And now the RUB was even removed from the trading platform altogether.

So my original trading strategy of shorting and then going long RUB got cut short and max profits throw out the window. So much for free markets.

EM

COMMENT #2: Marty you have proven your model and computer is the key to running governments for the future living with the cycle. It is easy to see why the CIA wanted your model pinpointing Ukraine almost 10 years in advance as the key spot for war. It is also interesting how others prefer not to ever mention you for your work is not opinion like everyone else. I really hope you succeed in securing Socrates for the world long-term. We all can learn so much.

All the best from Poland

and thanks for the conference that you did here in Warsaw

VA

REPLY: The free markets are not so free. During the Civil War, even President Lincoln went after trading gold and argued those people were making money off of every battle. The EU wanted to take trading the Euro away from London because of BREXIT. The people running these governments will NEVER honor the free markets when they go against them.

Yes, it was very nice to meet everyone in Warsaw. I had not been there before. I am doing my best to make sure Socrates continues beyond my shelf life. The problem is that the world is run by the seat of its pants and it is always based upon bias, prejudice, and power-plays driven by ego. I think some people just need to have an enemy and no matter what changes, they ignore that to keep the hatred ongoing.

There are people who still call China Communist even though there is private ownership which is the opposite of communism. They will continue to hate China no matter what and that in turn only invokes a response to counter that trend. Biases like that prevent us from ever moving forward and society is at times like a scratched record playing the same track over and over again.

The Federal Open Market Committee plans to taper its asset purchasing program by $30 billion per month. Starting in January, the central bank will begin buying $60 billion in bonds monthly, citing “inflation developments and the further improvement in the labor market.”

As for interest rates, the Fed is considering as many as three rate hikes in 2020, followed by two additional hikes in 2024. This comes after the Fed artificially lowered rates to near zero for the longest amount of time in the history of the Federal Reserve.

“With inflation having exceeded 2 percent for some time, the committee expects it will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the committee’s assessments of maximum employment,” the central bank stated. Unemployment reached a post-pandemic low of 4.2% last month, but nearly 7 million Americans are still unemployed. “Supply and demand imbalances related to the pandemic and the reopening of the economy have continued to contribute to elevated levels of inflation,” the statement continued. Now, the central bank believes inflation will somehow reach 2.6% in 2020, with core inflation dropping to 2.7%.

The central bank sees reduced GDP growth this year, dropping the forecast to 5.5% from 5.9%. GDP in 2022 is now estimated to reach 4%, and 2.2% in 2023.

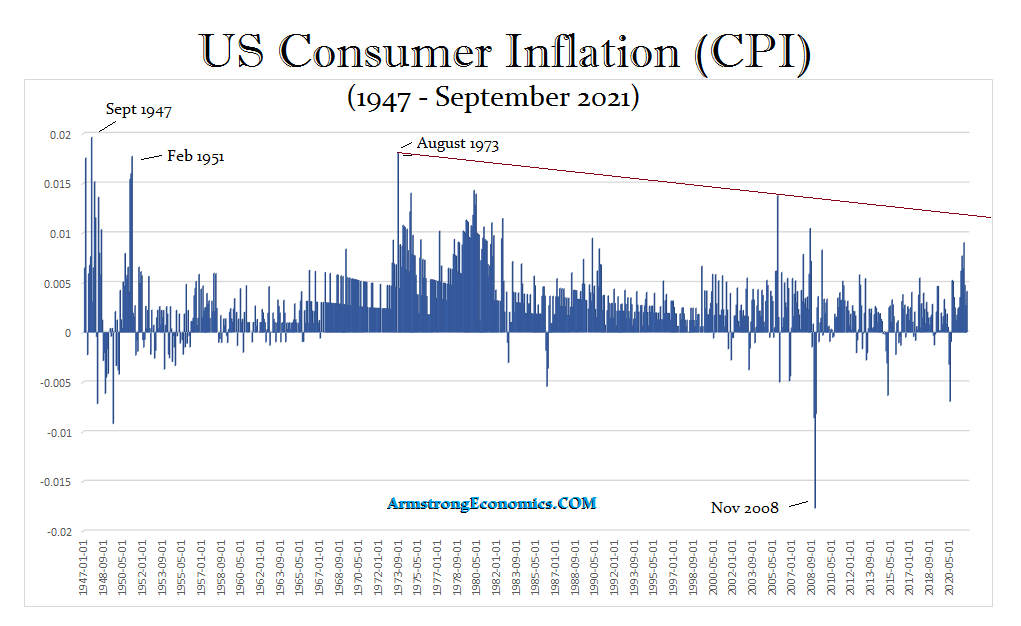

Inflation continued to surge, reaching 5.4% in September. Janet Yellen has never been right about anything and keeps calling this “transitory,” as if it will vanish in a few weeks. The Labor Department’s Consumer Price Index, which is supposed to measure a basket of goods and services as well as energy and food costs, came in at 5.4% in September from a year earlier, well beyond expectations. However, our model was projecting a rise in inflation into 2021 which is 13 years up from the November 2008 low. It is interesting how the COVID restrictions with lockdowns came in on target with our computer’s forecast. Curious how events seem to fulfill the forecast when it is done by a computer rather than human judgment.

Nevertheless, as you can see from the chart, inflation has bounced on a month/month basis, but it has not yet reached the Downtrend Line. The long-term forecast beyond a mere decade projects the historical high will be due in 2034, which should exceed all previous highs. A month/month number above 1.05% will signal that inflation is breaking out, and we will indeed make all-time record highs going into 2034.

The numbers are out — 4.3 million people in the US quit their jobs in August. This is the largest number since 2000. The leading sector is hotels and restaurants. I have a friend who has a daughter who had two jobs. She worked as a waitress/bartender at night and at a health food store during the day. She was very industrious, to say the least, and quite impressive. However, she quit the health food job because they demanded a vaccine. She said the bar owner was going to impose a vaccine rule and more than 50% of the staff said they would quit.

Meanwhile, New York’s bars and restaurants are hurting for business because of the vaccine mandates. Our most honorable leaders, who are most likely taking money from Pfizer lobbyists worldwide, are realizing that resistance is not futile. You can mandate vaccines and pretend they are 100% safe, but the truth always surfaces. The people can bring down the entire system if they simply refuse to participate.

Many journalists are too busy selling Biden’s propaganda about the vaccines. The FDA admits there are risks, but they, in their sole discretion, announced they “believe” the benefits outweigh the risk without any explanation of the analysis or a single word of caution (e.g., if you have certain conditions, you should not take the vaccine) despite doing so for other vaccines. So while the press and the Biden Administration are ignoring the facts and the trend, this only raises the question: How much has Pfizer and Moderna paid you?

Posted originally on the conservative tree house on October 13, 2021 | Sundance | 249 Comments

I do not expect White House Spokesperson Jennifer Psaki to understand how her bosses policies are driving massive price increases; nor do I expect Psaki to understand economics and inflationary impacts. However, the scale of her false statements surrounding inflation are not just false, they are now dangerous.

Following the release of the consumer price index [SEE table 2], in her press briefing today, Jen Psaki outlined the White House perspective on inflation, and specifically the Fed claims surrounding “transitory inflation.”

In her statements today, Psaki referenced people comparing the prices of 2021 consumable goods to 2020 and 2019. [Video prompted below] Within the statements, the scale of falsity is off the charts. WATCH [Video at 19:00 to 22:42, prompted]

There is not one single thing about that three minute verbal exchange that is accurate. Fast turn consumable goods, groceries etc., did not drop in 2020 during the first year of the pandemic. Factually, all goods but especially consumable goods increased in price throughout the pandemic, because demand actually increased and the supply chains were unable to keep up.

Example. A loaf of bread at $2.50 in 2019, climbed to $3.00 in 2020. That price jumped again to $3.75 this year (2021) and will likely continue rising as monetary policy driven inflation continues devaluing our currency.

Even if, as Psaki claims, inflation slows down (not likely) – “decelerating inflation” does not mean declining prices; it means a slower rate of price increase. Stuff still costs more, it just costs more at a slower rate. Consumable goods will cost more in 2022 than they do this year. The 2022 loaf of bread likely to climb to $4.00; it will never return to the 2019 price of $2.50 because the dollar is worth less.

This massive inflation is a direct result of the multinational agenda of the Biden administration in combination with the spending spree. Inflation is a feature not a flaw, and it has nothing whatsoever to do with COVID. The first group to admit what was obvious were banks, specifically Bank of America, because the monetary policy is the primary cause.

You might remember, when President Trump initiated tariffs against China (steel, aluminum and more), Southeast Asia (product specific), Europe (steel, aluminum and direct products), Canada (steel, aluminum, lumber and dairy specifics), the financial pundits screamed at the top of their lungs that consumer prices were going to skyrocket. They didn’t. CTH knew they wouldn’t because essentially those trading partners responded in the exact same way the U.S. did decades ago when the import/export dynamic was reversed.

Trump’s massive, and in some instances targeted, import tariffs against China, SE Asia, Canada and the EU not only did not increase prices, the prices of the goods in the U.S. actually dropped. Trump’s policies led the largest deflation in consumer prices in decades. At the same time, Trump’s domestic economic policies drove employment and wages higher than any time in the past forty years.

With Donald Trump’s policies, we were in an era where job growth was strong, wages were rising and consumer prices were falling. The net result was more disposable income for the middle class, more demand for stuff, and ultimately that’s why the U.S. economy was so strong.

♦Going Deep – To retain their position, China and the EU responded to U.S. tariffs by devaluing their currency as an offset to higher prices. It started with China, because their economy is so dependent on exports to the U.S.

China first started subsidizing the targeted sectors hit by tariffs. However, as the Chinese economy was under pressure, they stopped purchasing industrial products from the EU, that slowed the EU economy and made the impact of U.S. tariffs, later targeted in the EU direction, more impactful.

When China (total communist control over their banking system) devalued their currency to avoid Tariff price increase, it had an unusual effect. The cost of all Chinese imports dropped, not just on the tariff goods.

Imported stuff from China dropped in price at the same time the U.S. dollar was strong. This meant it took less dollars to import the same amount of Chinese goods; and those goods were at a lower price. As a result, we were importing deflation…. the exact opposite of what the financial pundits claimed would happen.

In response to a lessening of overall economic activity, the EU then followed the same approach as China. The EU was already facing pressure from the exit of the U.K. from the EU system; so, when the EU central banks started pumping money into their economy and offsetting with subsidies, they essentially devalued the euro. The outcome for U.S.-EU importers was the same as the outcome for U.S.-China importers. We began importing deflation from the EU side.

In the middle of this, there was a downside for U.S. exporters. With China and the EU devaluing their currency, the value of the dollar increased. This made purchases from the U.S. more expensive. U.S. companies who relied on exports (lots of agricultural industries and raw materials) took a hit from higher export prices. However, and this part is really interesting, it only made those companies more dependent on domestic sales for income. With less being exported, there was more product available in the U.S for domestic purchase…. this dynamic led to another predictable outcome, even lower prices for U.S. consumers.

From 2017 through early 2020, U.S. consumer prices were dropping. We were in a rare place where actual deflation was happening. Combine lower prices with higher wages, and you can easily see the strength within the U.S. economy.

For the rest of the world this seemed unfair, and indeed they cried foul – especially Canada. However, this was America First in action. Middle-class Americans were benefiting from a Trump reversal of 40 years of economic policies like those that created the rust belt.

Industries were investing in the U.S., and that provided leverage for Trump’s trade policies to have stronger influence. If you wanted access to this expanding market, those foreign companies needed to put their investment money into the U.S. and create even more U.S. jobs. This was an expanding economic spiral where Trump was creating more and more economic pies. Every sector of the U.S. economy was benefiting more, but the blue-collar working class was gaining the most benefit of all.

♦ REVERSE THIS… and you now understand where we are with inflation.

The JoeBama economic policies are exactly the reverse. The monetary policy that pumps money into into the U.S. economy, via COVID bailouts and ever-increasing federal spending, drops the value of the dollar and makes the dependency state worse.

With the FED pumping money into the U.S. system, the dollar value plummets. Now the value of the Chinese and EU currency increases. This means it costs more to import products, and that is the primary driver of price increases in consumer goods.

Simultaneously, a lower dollar value means cheaper exports for the massive multinational conglomerates who now control our farms and farming resources (Big AG and raw materials). China, SE Asia and even the EU purchase U.S. food and raw material at a lower price. That means less food and raw material in the U.S. which drives up prices for U.S. consumers.

It is a perfect storm. Higher costs for imported goods (durable goods) and higher costs for domestic consumable goods (food). Combine this dynamic with massive increases in energy costs from ideological Green New Deal policy, and that’s fuel on a fire of inflation.

Annualized inflation is now around 8 percent, and it will likely keep increasing in the short term. This is terrible for wage earners in the U.S. who are now seeing no wage growth and higher prices. Real wages are decreasing by the fastest rate in decades. We are now in a downward spiral where your paycheck buys less. As a result, consumer middle-class spending contracts. Eventually, this means household purchasing of durable goods drop because people have less disposable income.

Gasoline costs more (+50%), food costs more (+10% at a minimum) and as a result, real wages drop; disposable income is lost. Ultimately this is the cause of Stagflation. A stagnant economy and inflation. None of this is caused by COVID-19. All of this is caused by economic policy and monetary policy sold under the guise of COVID-19.

This inflationary period will not stall out until the U.S. economy can recover from the massive amount of federal spending.

If the spending continues, the Fed keeps printing money. The dollar continues to be weakened. As a result the inflationary period continues. It is a spiral that can only be stopped if the policies are reversed…. and the only way to stop these insane policies is to get rid of the Wall Street democrats and republicans who are constructing them.

Tucker Carlson hit this point very well last night:

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America

{kind=link}