$64 billion of the current annual trade deficit with Mexico stems from the auto sector alone.

$64 billion of the current annual trade deficit with Mexico stems from the auto sector alone.

For over a decade auto manufacturers have moved to Mexico in order to import parts from Asia, assemble and install them, and then ship the completed cars into the U.S. through NAFTA without duties (tariffs).

The U.S. auto ancillary business groups (parts suppliers) have been pushed out of competition in the auto sector by this corporate profit strategy. Thousands of U.S. jobs have been lost in both the plant assembly and the ‘auto-parts’ manufacturing sector.

CTH has called attention to this bastardized supply chain for years. Foreign auto-parts, made by foreign workers, assembled into U.S. owned manufacturing, and sold as U.S. automobiles. The weird supply chain and assembly process is essentially a multinational corporate scheme (in the auto sector) which exploits one of the loopholes in the 25-year-old NAFTA agreement.

If the assembly plant was on U.S. soil the foreign (mostly Asian) parts would be taxed as imported parts. However, so long as the assembly is in Mexico (or Canada), the origin of the parts is currently irrelevant, and the finished automobile crosses the border into the U.S. avoiding the taxes using NAFTA.

Keep in mind, the auto manufacturing sector, not just U.S. assembly plants but also European auto-makers, have made capital investments into Mexico, based on this NAFTA loophole as part of their business model. They don’t want this cost/profit plan disrupted.

Along comes U.S. Trade Rep. Robert Lighthizer and U.S. Commerce Secretary Wilbur Ross and say: NO MORE.

Along comes U.S. Trade Rep. Robert Lighthizer and U.S. Commerce Secretary Wilbur Ross and say: NO MORE.

If you are going to consider it a North American Free Trade Agreement vehicle, then an established percentage of that vehicle should actually have to come from North America; just as importantly, that percentage should be high.

That’s the basic argument behind the “rules of origin” part of NAFTA. If you are going to call it a “North American vehicle”, then the parts should come from North America. Makes rational sense, no?

The U.S.A. position is that half of content for ‘American-built’ autos should be produced in the United States; and the regional (NAFTA) vehicle part content requirement should be increased to 85 percent from the current 62.5 percent.

Mexico and Canada do not want rules of origin because they want to use their workers to assemble vehicle parts from other nations and sell into the U.S. as “American Autos”. They correctly fear that if American cars must actually contain American content, and be assembled by actual Americans, then the American Auto-Manufacturers will move their auto plants to America.

The auto-industry, who have invested tens-of-millions in the current scheme, wants to keep the entire source of origination a hidden secret from the public. They are not too keen on American consumers finding out that Japanese, Chinese, Indonesian, Korean and Vietnamese parts are actually behind the American badges.

Additionally, the European Auto-Manufacturers who are also building in Mexico and Canada don’t want to lose the NAFTA loophole that lets them assemble outside the U.S. and get their vehicles into the American market.

The current system employs lots of Mexican and Canadian workers who assemble foreign parts into American vehicles that are then sold into the U.S. as “American Cars”.

If “rules of origin” are forced upon them, there’s no incentive -beyond labor- for the U.S. auto corporations to continue making cars in Mexico and/or Canada. Simultaneously, the vast majority of the assembly is now automated (with human assistance), so the labor costs are currently smaller as a percentage of the overall cost of manufacturing.

Automation and modern efficiencies in human assisted robotics mean the labor cost incentive is not as valuable as it once was for manufacturing. In the modern auto-era it’s the quest for cheaper parts that is now driving the business model; hence, the “rules of origin” exploitation.

MEXICO CITY (Reuters) – Canada and Mexico will rebuff the United States over its demand for tougher NAFTA automotive content rules, top officials said on Monday as negotiations to renew the treaty bogged down with only a few months to go.

[…] Canadian and Mexican negotiators will address the U.S. auto demands on Tuesday, the final day of the fifth round of talks to update the North American Free Trade Agreement, chief Mexican negotiator Ken Smith told reporters.

Although the talks are due to wrap up in March 2018 after a seventh and final round, they are deadlocked over a series of hard-line proposals the United States unveiled at the fourth round last month.

“It’s definitely slowed down from the previous round,” said a Canadian source with direct knowledge of the talks. “There has been no progress in the contentious chapters.”

Canadian and Mexican officials have complained repeatedly about what they see as U.S. inflexibility. A spokeswoman for the U.S. Trade Representative declined to comment.

Mexico and Canada fear Trump will follow through on a promise to pull out of NAFTA, causing disruption and economic damage. The Canadian dollar edged lower against its U.S. counterpart on Monday, in part because of concerns about the negotiations. (read more)

This is where we must fight the lobbyists.

You must remain engaged and understanding of the issues within these and other trade disputes. President Trump is wearing the bullet-proof vest, but you must engage your congressman to let him/her know you support the administration and their objectives in these Trade deals.

Your congressional representative is being lured with millions of millions of dollars from lobbyists who work for the multinational corporations. They will try to retain their financial position. YOU must educate yourself and your family on these issues.

Together we must engage and fight. This is the president we have been waiting for. Don’t expect he can do this on his own. Make your voice heard.

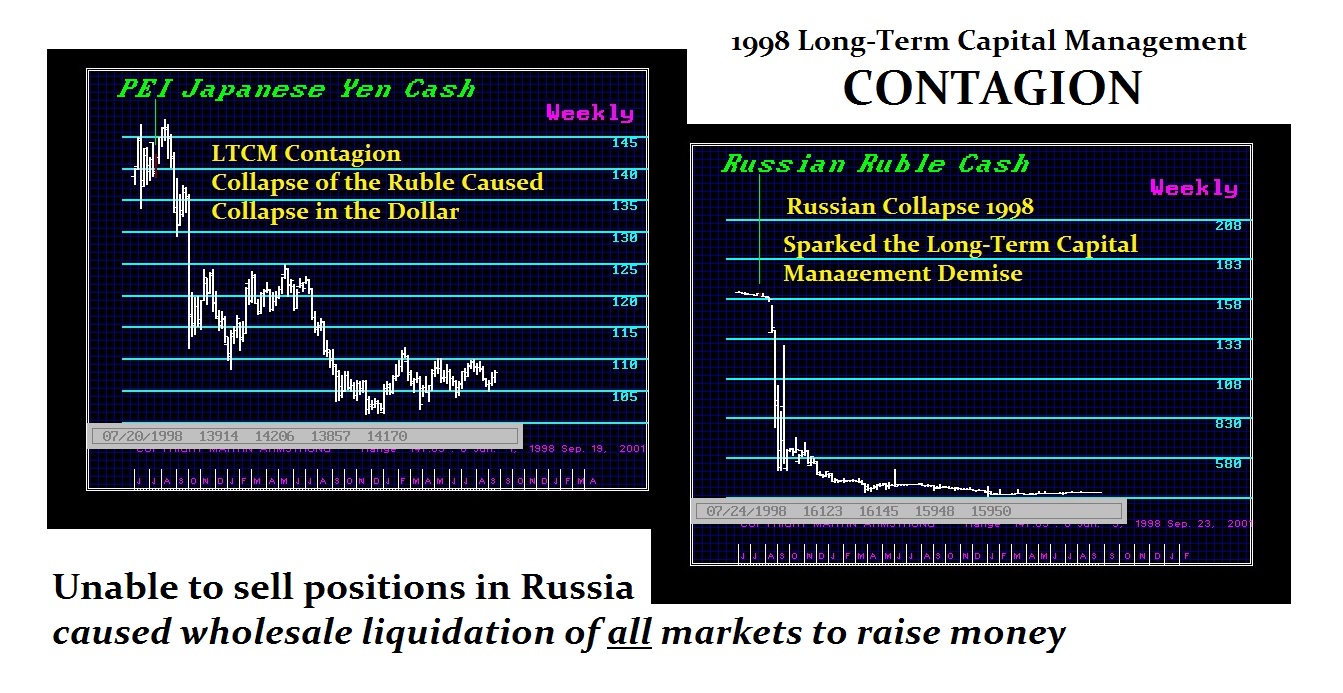

REPLY: No government that I am aware of has ANY plan for a contagion such as LTCM, S&L etc…. You must understand that the people who even dream up legislation have ZERO experience in markets. Absolutely everything is based upon a single failure of any institution. When the LTCM crisis hit, bids withdraw and institutions are unsure who to even trade with. This creates the NO BID crisis and volatility rises dramatically. The panic unfolds because of price moves without volume. When large gaps appear WITHOUT supporting news, even professionals sell because they cannot make a decision in a vacuum.

REPLY: No government that I am aware of has ANY plan for a contagion such as LTCM, S&L etc…. You must understand that the people who even dream up legislation have ZERO experience in markets. Absolutely everything is based upon a single failure of any institution. When the LTCM crisis hit, bids withdraw and institutions are unsure who to even trade with. This creates the NO BID crisis and volatility rises dramatically. The panic unfolds because of price moves without volume. When large gaps appear WITHOUT supporting news, even professionals sell because they cannot make a decision in a vacuum.