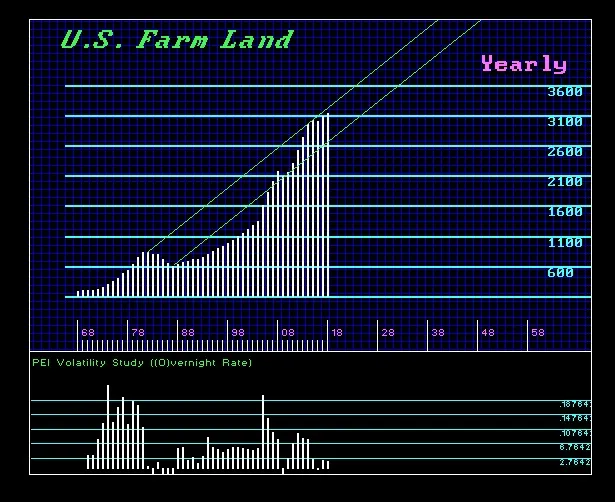

Most people have little idea WHY big money was targeting buying farmland in Canada, USA, and Australia. It was more than just Chinese investment. With interest rates down to negative, capital has been looking for returns. They were buying farmland and then renting it out generally for 5%. This created what many call the farmland bubble which has now begun to burst in some Corn Belt states, such as Iowa, as interest rates begin to rise. In 2015, the average increase of 2.4% percent on the low end and up to 8% in some states where the crop yields were best. This has not been a small investor or spec market. This was driven by the big boys seeking yield thanks to particularly the European Central Bank (ECB).

The nominal high came in 1982 and the commodity boom peaked in 1980 and interest rates peaked in 1981. The rising dollar caused the correction in nominal terms declining into its low in 1987. The market began to recover while the days of inflation and goldbugs faded forging the final low in gold during 1999. As is often the case, people just never look at assets in terms of international value. The surge in prices of latter that domestic analysts have called a “bubble” truly reveal more of a Phase Transition type rally more than doubling in price when plotted in Euros. The key to any market lies hidden within the depths of international capital flows which are driven foremost by currency values.

The lack of individual investors infiltrating this market leaving the big agricultural bets being placed not on expectations of global food demand will increase over time, but looking simply for yield, has led most analysis astray. Institutions, like the pension fund TIAA-CREF, have been the big buyers throughout 2017. They have been looking for bargains as farm real estate values have started to decline. Small farmers are finding it difficult to borrow from the banks for a crop season which can involve loans into several millions of dollars. If crops are wiped out, then they have a real problem.

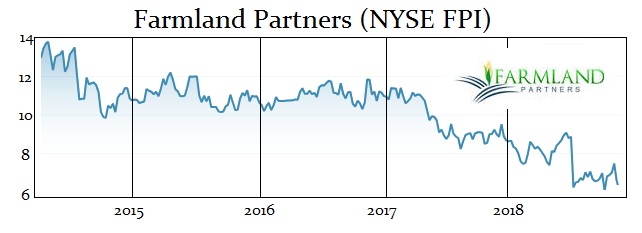

There have been stocks issued seeking to capitalize on the boom. Farmland Partners (FPI, NYSE) has been down about 20% since it was floated in 2014. It is a REIT which is a company that owns, operates or finances income-producing real estate. REITs were modeled after mutual funds to gather investors to collectively own valuable real estate and provide the opportunity to access dividend-based income and total returns. On its website, it states: “Farmland Partners Inc. is an internally managed, publicly traded (NYSE: FPI) real estate company that owns and seeks to acquire high-quality farmland throughout North America addressing the global demand for food, feed, fiber and fuel.” However, the play has NOT been the boom in commodities, but the yield from renting out the land.

Investors should be very careful with REITs because they tend to be illiquid and volatile.

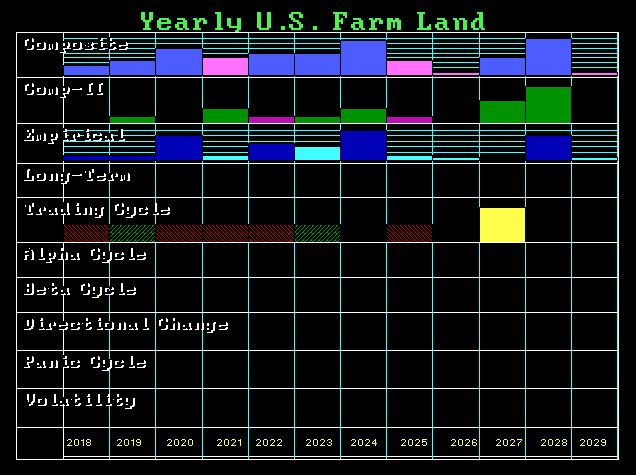

When we look at the Array, we see turning points lining up for 2020/2021 and 2024 followed by 2026 and then 2028. The commodity cycle appears to be pointing to 2024. That is when we should see farmland values peak in real terms but keep in mind that it will all depend upon the particular region. The weather is going to kick in and that will reduce crop yields. Keep in mind that most of these REITs have entered this sector of the market for the wrong reason. It was not truly a commodity boom expectation as it was simply to get a 5% yield when interest rates were below that level. As interest rates rise above that 5% threshold, we will begin to see the big players bailout and begin to dump farmland at losses. Anyone looking to borrow against their land should use FIXED RATES only. If you decide to sell your land to the big boys while rates are still below 5%, the include a right of first refusal to buy it back at a reduced price when they decide to cut and run – which they will inevitably always do at the precise wrong time.

QUESTION: Mr. Armstrong; You mentioned that we should expect a further decline in the economy. Do you have a target for that decline?

Thank you

KT

ANSWER: The world economy has been in a prolonged economic decline as taxes have risen and regulation has expanded. As government hunts money everywhere, they are bringing the world economy into a major decline since the 1970s. The bottom in nominal terms appears to be 2025. However, in REAL TERMS, we are looking for a decline into 2035.8

QUESTION: You mentioned that Goldman Sachs can take down the entire banking sector. Do you see this correlating in the future?

JF

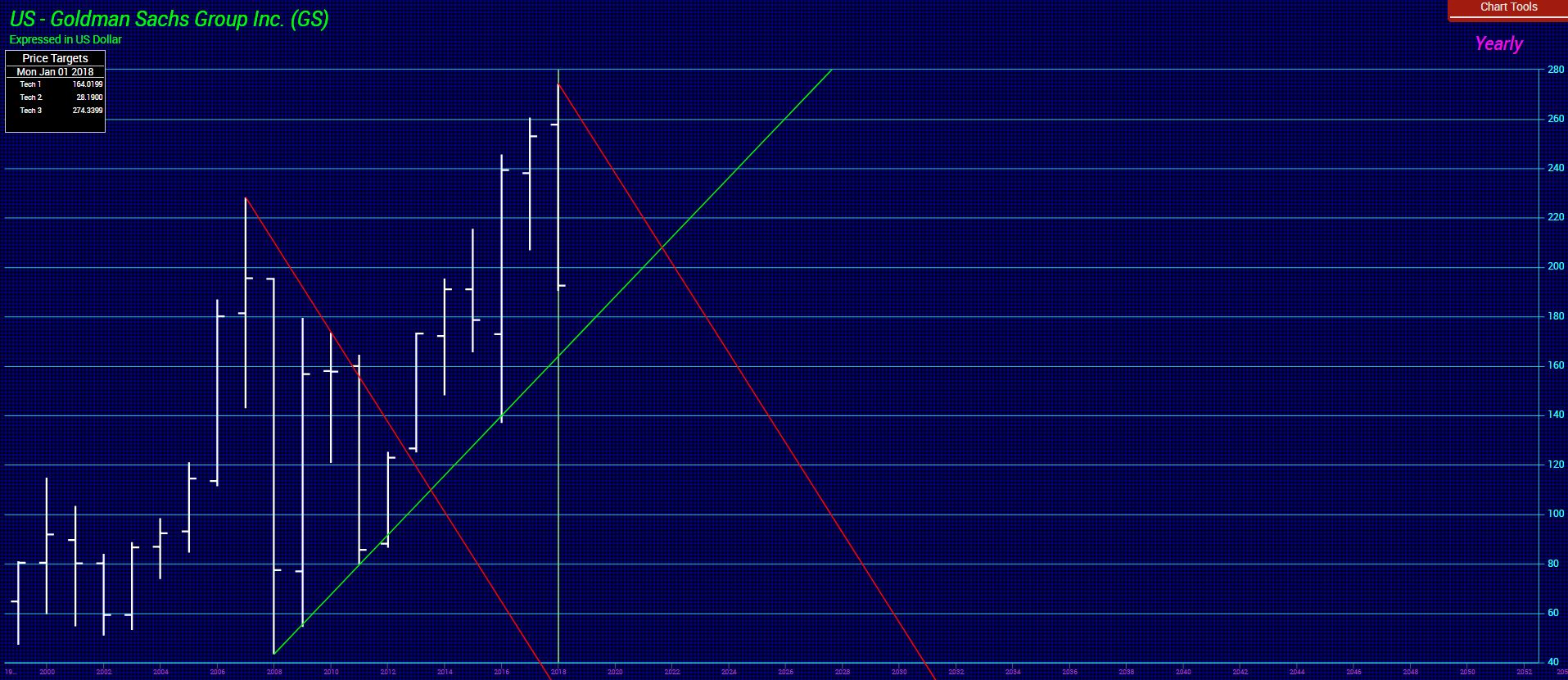

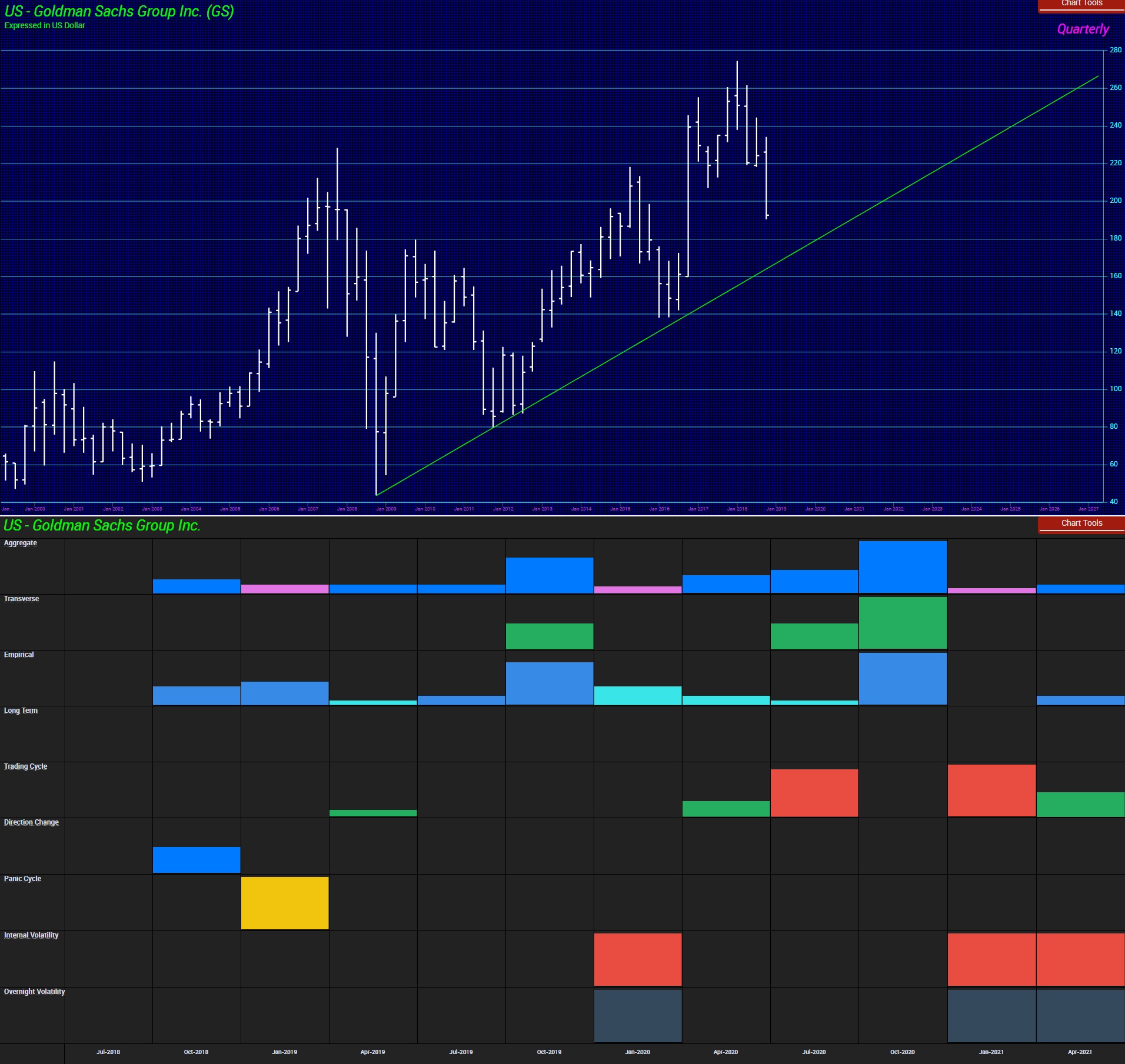

ANSWER: Here is Goldman Sachs and JP Morgan. The first thing you will notice is that JP Morgan has been in a REAL bull market. Goldman has not. I am a firm believer that the markets instinctively forecast major future trends if you know how to read them. Now, look at the arrays. They both are showing the major target as the 4th quarter of 2020. JP Morgan shows the 2nd quarter of 2019 as a turning point. Look at the pattern difference with Goldman Sachs. There is no question that Goldman will do whatever it takes to try to survive calling in every political marker possible. However, because of this Malaysia scandal is worldwide involving four countries, pulling this off is not going to be easy. Its huge fees that were 10x that of any other firm to do this deal smells of something wrong. I know brokers who were denied the right to even bid on this project.

The bottom line is clear. Just go by the Reversals. Not even Goldman Sachs can overcome them.

The Abu Dhabi sovereign wealth fund sued Goldman Sachs on the Pi Target, Wednesday, November 21st, 2018, for allegedly conspiring against the Middle Eastern fund to further a criminal scheme by Malaysia’s scandal-plagued 1MDB. The suit, filed in a New York court on behalf of Abu Dhabi’s International Petroleum Investment Company (IPIC), names Goldman Sachs as well as former Goldman officials who were charged by the US Justice Department in indictments unsealed earlier this month. “This action seeks redress for a massive global conspiracy on the part of the defendants to defraud and injure plaintiffs,” said the lawsuit, which also named former executives from IPIC and its subsidiary Aabar Investments.

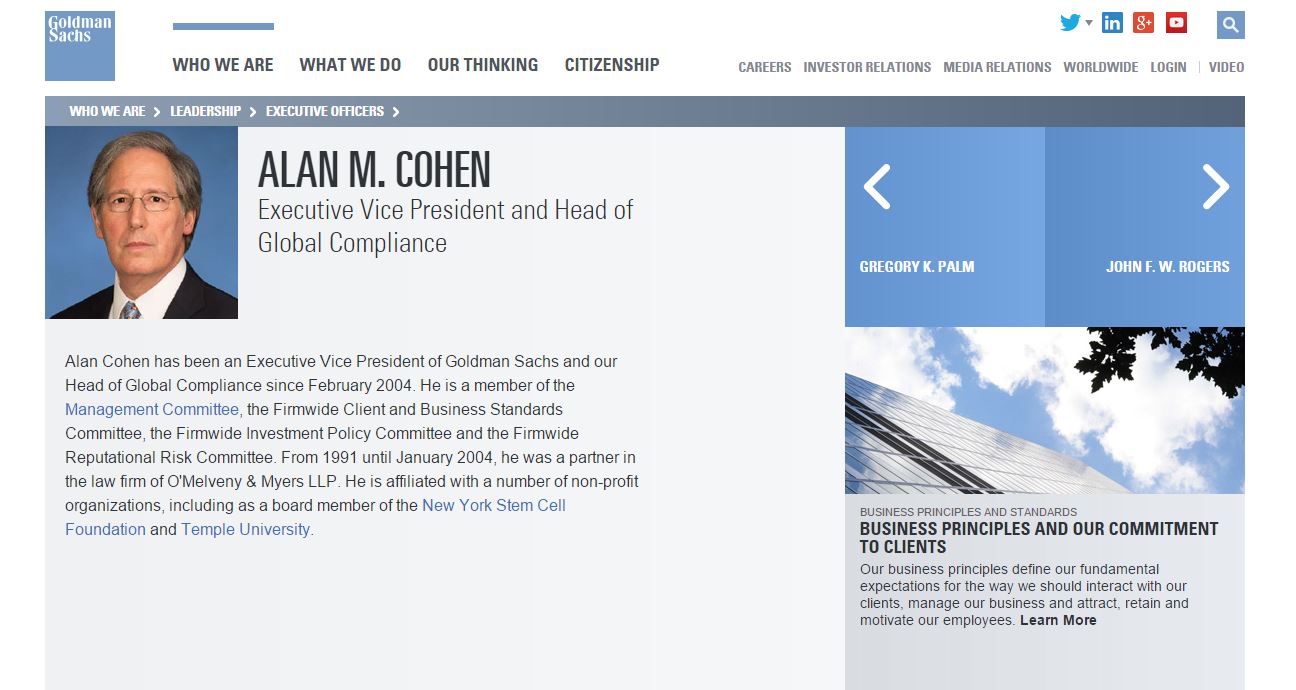

It was Alan Cohen who I believe was in charge of reviewing all deals as head of Global Compliance at Goldman Sachs and now he is at the top of the SEC. I believe he was given the job at Goldman Sachs because he threatened my lawyers to turn over all tapes I had of conversations with the various bankers including Goldman Sachs’ metal desk. It is now only logical that the Abu Dhabi sovereign wealth fund should also name Alan Cohen given he was the head of Global Compliance.

Here are just a few tapes that I found copies of. The bulk the SEC claimed were all destroyed in the 911 attack. There have continually been questions of the ethics inside Goldman Sachs. The entire crash in the world economy due to the Mortgage Back Securities were designed by Goldman Sachs. The major product they sold the day of the high of the ECM back in 2007 was widely touted as “Abacus 2007-AC1: Built to fail.”

As the Financial Post wrote: “Goldman has often been criticized for selling billions of dollars of debt securities, called credit default obligations (CDOs), filled with mortgages that the bank itself allegedly thought were overvalued.”

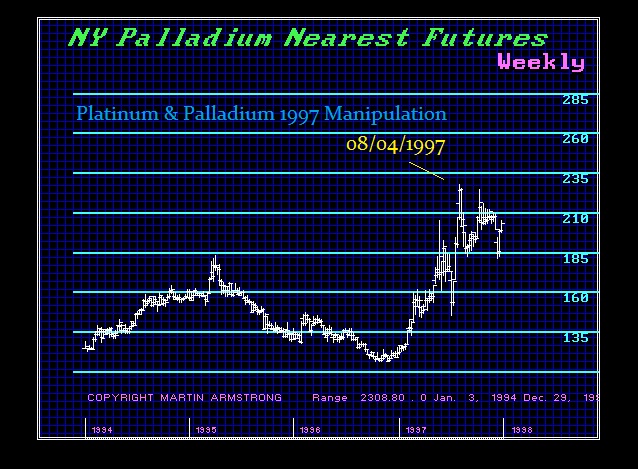

I believe it was Goldman Sachs who paid bribes to Russian politicians to recall Platinum from the market and temporarily stop sales to allegedly take an “inventory” of their stockpile. This sent prices soaring back in 1997. Russia stopped all shipments of Platinum and Palladium in December, was expected to resume exports. The hedge fund Tiger Management, a New York hedge fund back then, announced it sell some of its palladium holdings which it was believed held about one-fifth of the annual world supply of palladium (1.5 million ounces). This was followed by the silver manipulation in 1998 with most of the same firms involved.

The charging documents, unsealed in federal court on November 1st, 2018 refer to an unidentified Goldman executive as an unindicted co-conspirator who approved of the alleged bribery. The street rumor is that happens to be the executive Andrea Vella, who was Goldman’s co-head of Asian investment banking. Interestingly, Goldman Sachs suspended him the very same day that prosecutors unsealed the criminal complaints. It was also Andrea Vella was had to respond to cross-examination from Philip Edey QC, who was a lawyer acting on behalf of yet another government accusing Goldman Sachs of questionable dealings. That was the Libyan Investment Authority, which claims the investment bank took advantage of its financial illiteracy back in July 2008.

Let us not forget Goldman Sachs’ role in blowing up Greece and instigating the beginning of the Euro crisis. The crisis was created by a deal Greece struck with Goldman Sachs, that was engineered by Goldman’s CEO, Lloyd Blankfein. Blankfein and his Goldman team helped Greece hide the true extent of its debt, and in the process almost doubled it. The speculation back in 2015 was that Greece would file a lawsuit against Goldman Sachs for creating that debt crisis. There were the personal meetings between Greece and Gary Cohn to do that deal. When the client is a government, it ALWAYS involved the top people.

In 2001, Greece was looking for ways to disguise its mounting financial debt in order to just get into the Eurozone. The Maastricht Treaty required all Eurozone member states to show improvement in their public finances. Greece was heading in the wrong direction and Goldman Sachs came to the rescue. They arranged a secret loan of €2.8 billion and disguised it as an off-the-books “cross-currency swap” that was a complicated transaction in which Greece’s foreign-currency debt was converted into a domestic-currency obligation using a fictitious market exchange rate. They made 2% of Greece’s debt magically vanish from its national accounts. Goldman Sachs charged €600 million euros which was about 12% of Goldman’s revenue for 2001 giving them a record sales year.

Then the deal turned sour in the aftermath of 9/11 attacks when bond yields plunged. They resulted in a huge loss for Greece because of the formula Goldman had crafted to their benefit dictating the country’s debt repayments under the swap. By 2005, Greece owed almost double what it had put into the deal and thus we see the European debt crisis unfold.

Until 2008, European Union accounting rules allowed member nations to manage their debt with these so-called off-market rates in swaps. In the late 1990s, JPMorgan enabled Italy to hide its debt by swapping currency at a favorable exchange rate, thereby committing Italy to future payments that didn’t appear on its national accounts as future liabilities. However, what Goldman did to Greece made Italy look like child’s play.

Goldman Sachs’ share price is going down hard into 2019. The 159 level will be critical on a closing basis for the year. If that is breached, then we could see very major implications for the firm whereby it may no longer survive. There is technical support between 174 and 164. From a cyclical perspective, Goldman Sachs has peaked as an institution as of 2017. It was founded in 1869 and 17.2 x 8.6 = 147.92. That means, in fact, the 2017 closing was the all-time high for Goldman Sachs and this incident is its Death knell. Goldman Sachs may be going down for the count.

August 2003 – Goldman Sachs creates Mortgage Back Securities & AIG Insures them

February 2006 – AIG Stops writing CDS on subprime mortgages

December 2006 – Goldman turns bearish on mortgage/real estate market

July 2007 – Goldman Sachs demands $1.8 billion in insurance from AIG

August 2007 – AIG posts $450 million as collateral

November 2007 – AIG posts $2 billion with Goldman on $3 billion demand

March 2008 – Goldman Sachs demands $6.6 billion from AIG

March 2008 – Bear Stearns collapses on 13th

August 2008 – Goldman Sachs takes a bearish view on AIG on 18th

September 2008 – Gov’t Bails out Fannie Mae on 7th

September 2008 – Lehman Brothers files for bankruptcy on 15th

September 2008 – Treasury Hank Paulson bails out AIG to save Goldman 16th

September 2008 – Paulson emails Congress with TARP 20th

September 2008 – Goldman Sachs & Morgan Stanley become banks 21st

October 2008 – Congress passes TARP on 3rd

October 2008 – Goldman Sachs demand another $1.3 billion from AIG

November 2008 – Federal Reserve creates Maiden III for Toxic Assets

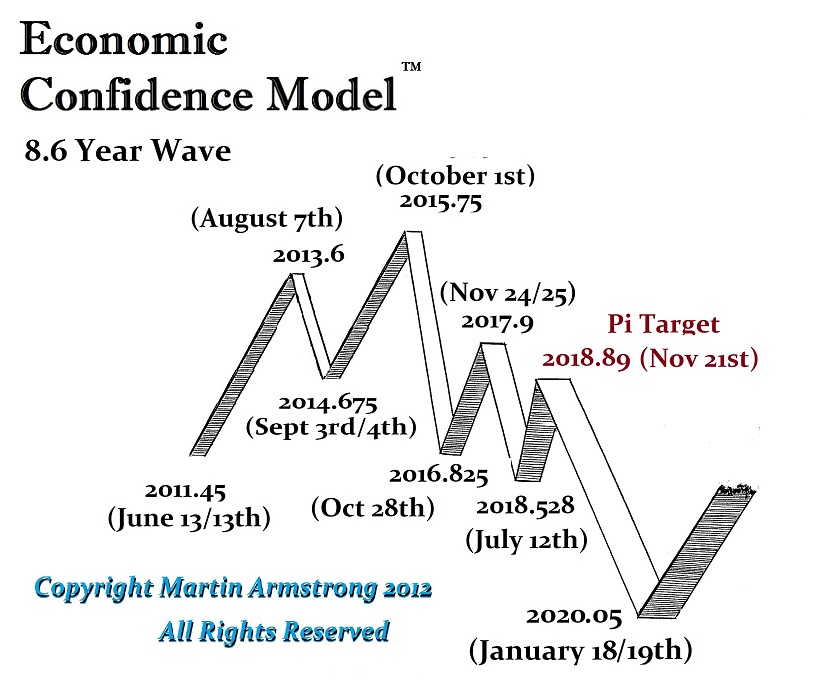

Here we have 2007.15 when Goldman Sachs sells precisely at the top of the ECM back in 2007 ABACUS2007-ACI which was a $2 Billion Synthetic CDO. It was then on the Pi Target when the SEC charged Goldman Sachs with fraud back on April 16, 2010, for that very transaction. Any small firm is imprisoned and stripped of its license. But Goldman Sachs has the SEC and the DOJ in its back pocket along with the judges and politicians. Now again on the precise Pi Target Abu Dhabi filed a lawsuit against Goldman Sachs Wednesday (Nov 21) for allegedly conspiring against the Middle Eastern fund to further a criminal scheme by Malaysia’s scandal-plagued 1MDB.

Because we have 3 countries now bringing charges and/or suits against Goldman Sachs, it appears that this will mark the beginning of the end for the firm. When the Euro cracks, they will also be blamed for their role in Greece and the rest of Europe. Don’t forget that Mario Draghi is also ex-Goldman Sachs. When the Euro cracks, there will be a microscope applied to every communication that was ever carried out between Draghi and Goldman Sachs. Every trade they have pulled off will be inspected with its tentacles into the European bond market.

After the government took down Solomon Brothers back in 1991 for manipulating the US Treasury Auctions, Goldman Sachs began a program of buying protection. They allegedly began aggressively funding politicians and then began stuffing their people in key places of government. They have been known as “Government Sachs” among dealers and they have held a power-house political hand in their back pocket. Our model, at least, warns that day is NOW OVER!!!!!!

The computer would have shorted Goldman Sachs if it could. The Global Market Watch has pinpointed a high and it warned this stock was moving into a Waterfall on the Monthly Level. This is one stock to get out of. We will see major new lows next year.

CTH has pointed, repeatedly, toward a very specific economic and financial dynamic because President Trump is uniquely focused on Main Street’s “real economy“.

Everything happening in/around the financial markets is very predictable when you focus on understanding the principles of Main Street MAGAnomics and how those basic principles diverge from Wall Street’s “paper economy” (currently weighted by tech stocks).

Everything is happening in a very predictable sequence. Few understand the MAGAnomic reset and what was predicted to happen in the space between disconnecting a Wall Street economic engine (globalism and multinationals) and restarting a Main Street economic engine (nationalism/America-First). In 2016 CTH explained where we would be today. With current Wall Street events, perhaps it is worthwhile remembering the CTH forecast.

President Trump’s MAGAnomic trade and foreign policy agenda is jaw-dropping in scale, scope and consequence. There are multiple simultaneous aspects to each policy objective; however, many have been visible for a long time – some even before the election victory in November ’16. What is happening within the financial markets should not be a surprise.

If we get too far in the weeds the larger picture is lost. Our CTH objective is to continue pointing focus toward the larger horizon, and then at specific inflection points to dive into the topic and explain how each moment is connected to the larger strategy.

Today, as a specific result of a very predictable stock market contraction, we repost an earlier dive into how MAGAnomic policy interacts with multinational Wall Street, the stock market, the U.S. financial system and perhaps your personal financial value. Again, reference and source material is included at the end of the outline.

If you understand the basic elements behind the new dimension in American economics, you already understand how three decades of DC legislative and regulatory policy was structured to benefit Wall Street, Multinational corporate interests, and not Main Street USA.

The intentional shift in economic policy is what created distance between two entirely divergent economic engines to the detriment of the American middle-class.

REMEMBER […] there had to be a point where the value of the second economy (Wall Street) surpassed the value of the first economy (Main Street).

Investments, and the bets therein, needed to expand outside of the USA. hence, globalist investing.

However, a second more consequential aspect happened simultaneously. The politicians became more valuable to the Wall Street team than the Main Street team; and Wall Street had deeper pockets because their economy was now larger.

As a consequence Wall Street started funding political candidates and asking for legislation that benefited their multinational interests.

When Main Street was purchasing the legislative influence the outcomes were -generally speaking- beneficial to Main Street, and by direct attachment those outcomes also benefited the average American inside the real economy.

When Wall Street began purchasing the legislative influence, the outcomes therein became beneficial to Wall Street. Those benefits are detached from improving the livelihoods of main street Americans because the benefits are “global”. Global financial interests, multinational investment interests -and corporations therein- became the primary filter through which the DC legislative outcomes were considered.

As an outcome of national financial policy blending commercial banking with institutional investment banking something happened on Wall Street that few understand. If we take the time to understand what happened we can understand why the Stock Market grew and what risks exist today as the financial policy is reversed to benefit Main Street.

Instead of attempting to put Glass-Stegal regulations back into massive banking systems, the Trump administration is creating a parallel financial system of less-regulated small commercial banks, credit unions and traditional lenders who can operate to the benefit of Main Street without the burdensome regulation of the mega-banks and multinationals. This really is one of the more brilliant solutions to work around a uniquely American economic problem.

♦ When U.S. banks were allowed to merge their investment divisions with their commercial banking operations (the removal of Glass Stegal) something changed on Wall Street.

Companies who are evaluated based on their financial results, profits and losses, remained in their traditional role as traded stocks on the U.S. Stock Market and were evaluated accordingly. However, over time investment instruments -which are secondary to actual company results- created a sub-set within Wall Street that detached from actual bottom line company results.

The resulting secondary financial market system was essentially ‘investment markets’. Both ordinary company stocks and the investment market stocks operate on the same stock exchanges. But the underlying valuation is tied to entirely different metrics.

Financial products were developed (as investment instruments) that are essentially wagers or bets on the outcomes of actual companies traded on Wall Street. Those bets/wagers form the hedge markets and are [essentially] people trading on expectations of performance. The “derivatives market” is the ‘betting system’.

♦Ford Motor Company (only chosen as a commonly known entity) has a stock valuation based on their actual company performance in the market of manufacturing and consumer purchasing of their product. However, there can be thousands of financial instruments wagering on the actual outcome of their performance.

There are two initial bets on these outcomes that form the basis for Hedge-fund activity. Bet ‘A’ that Ford hits a profit number, or bet ‘B’ that they don’t. There are financial instruments created to place each wager. [The wagers form the derivatives] But it doesn’t stop there.

Additionally, more financial products are created that bet on the outcomes of the A/B bets. A secondary financial product might find two sides betting on both A outcome and B outcome.

Party C bets the “A” bet is accurate, and party D bets against the A bet. Party E bets the “B” bet is accurate, and party F bets against the B. If it stopped there we would only have six total participants. But it doesn’t stop there, it goes on and on and on…

The outcome of the bets forms the basis for the tenuous investment markets. The important part to understand is that the investment funds are not necessarily attached to the original company stock, they are now attached to the outcome of bet(s). Hence an inherent disconnect is created.

Subsequently, if the actual stock doesn’t meet it’s expected P-n-L outcome (if the company actually doesn’t do well), and if the financial investment was betting against the outcome, the value of the investment actually goes up. The company performance and the investment bets on the outcome of that performance are two entirely different aspects of the stock market. [Hence two metrics.]

♦Understanding the disconnect between an actual company on the stock market, and the bets for and against that company stock, helps to understand what can happen when fiscal policy is geared toward the underlying company (Main Street MAGAnomics), and not toward the bets therein (Investment Class).

The U.S. stock markets’ overall value can increase with Main Street policy, and yet the investment class can simultaneously decrease in value even though the company(ies) in the stock market is/are doing better. This detachment is critical to understand because the ‘real economy’ is based on the company, the ‘paper economy’ is based on the financial investment instruments betting on the company.

Trillions can be lost in investment instruments, and yet the overall stock market -as valued by company operations/profits- can increase.

Here’s the critical part – Conversely, there are now classes of companies on the U.S. stock exchange that never make a dime in profit, yet the value of the company increases.

This dynamic is possible because the financial investment bets are not connected to the bottom line profit. (Examples include Tesla Motors, Amazon and a host of internet stocks like Facebook and Twitter.) It is this investment group of companies, primarily driven by technology stocks in the “tech sector” that stands to lose the most if/when the underlying system of betting on them stops or slows.

Specifically due to most recent U.S. fiscal policy, modern multinational banks, including all of the investment products therein, are more closely attached to this investment system on Wall Street. It stands to reason they are at greater risk of financial losses overall with a shift in economic policy.

That financial and economic risk is the basic reason behind Trump and Mnuchin putting a protective, secondary and parallel, banking system in place for Main Street.

Big multinational banks can suffer big losses from their investments, and yet the Main Street economy can continue growing, and have access to capital, uninterrupted.

Bottom Line: U.S. companies who have actual connection to a growing U.S. economy can succeed; based on the advantages of the new economic environment and MAGA policy, specifically in the areas of manufacturing, trade and the ancillary benefactors.

Meanwhile U.S. investment assets (multinational investment portfolios) that are disconnected from the actual results of those benefiting U.S. companies, highly weighted within the tech sector, and as a consequence also disconnected from the U.S. economic expansion, can simultaneously drop in value even though the U.S. economy is thriving. THIS IS EXACTLY what is happening!

There are so many things happening in the political world it is next to impossible to figure out what is going to be the focal point for the Pi target since perhaps it could be a combination. The lastest hat being thrown into the ring is the European Commission is planning to enter their sanctions against Italy. As it stands currently, they have proposed disciplining Italy under EU fiscal rules on November 21st, 2018, unless the country’s government agrees to change its draft budget plan according to EU dictates. This could set in motion a drop in Italian debt which may force the ECB to buy more Italian debt or stand back and watch rates go crazy. This may also be the starting point of sending Italy into an exit position from the EU. In the weeks and months from now, we will be able to see that this was the turning point if this takes place.

COMMENT: Mr. Armstrong, I have to say that Bitcoin has crashed again because the IMF says each country should create its own cryptocurrency. That would kill all the cryptocurrencies and you were right again. Governments will never surrender their power to Bitcoin.

Thank you for your realistic perspective

DT

REPLY: I really do not get these people. They are dreamers. Of course, governments will not surrender. Their own pensions are at stake. The majority of transactions are already electronic. You just take a picture of your check and deposit it electronically without having to go to the bank. Separate the technology from power

Since the beginning of the year, the Turkish currency has lost more than a third of its value against the dollar. As the currency declines, imports rise in cost since they are denominated in foreign currency. This adds to the inflation problem domestically. Among other things, the sharp criticism of Erdoğan in the markets has cast doubt on the independence of the central bank. In September, it raised its key interest rate from 17.75 to 24 percent in the fight against inflation without success. This too adds to inflation.

There are people starting to look at tax cuts in selected areas to compensate for the crisis in hyperinflation. It is an interesting proposal but Erdoğan is worried about a real coup this time.

I bought ‘The World Real Estate Report’ at the end of 2016. It stated that Australian real estate was going to fall after the first quarter (March) in 2016. The property prices in Melbourne (where I live) continued to rise in April 2016 so I sent an email to Socrates Support asking them when real estate should peak. I received the reply below, which stated that the peak was either in for global real estate or the latest by the end of the first quarter 2017.

Anyway, since I owned a tiny house in Melbourne, I was facing a difficult decision if I should sell or not since it would be impossible to buy back in if the prices continued to go up.

I have been reading your blog daily since 2012, and I have read all of your forecasts being correct (eg. the Dow continuing to go up, US Index going up, Brexit, Trump winning). I also bought your Gold report in 2014 and watched gold bottom (Dec 2015) correctly for the date and price on the first benchmark, truly an unbelievable forecast.

Based on your track record I decided to sell my property at the end of the first quarter (March 2017), for which I received a fantastic price.

I’m happy to inform you that prices have been falling since the 3rd quarter of 2017.

I just wanted to congratulate you on another correct forecast.

REPLY: We all need a place to live. Governments are attacking real estate thinking it is too high and they need to make it more affordable for others to buy. They fail to understand that when they do that, the wipe out the savings dor retirement for others. Raising taxes to support government pensions is morally wrong and economically a disaster. There really should be some qualification to be a politician who them plays with people’s lives

QUESTION: Mr. Armstrong; When you were here last giving lectures in Poland, you said that we should leave the EU, retain our currency, and focus of your ties to the United States and Asia. You said if we did that, Poland would be one of the most imp[ortant economies in Europe. Have you updated that forecast at all?

Thank you

It was a tremendous honor to shake your hand in Warsaw.

JF

ANSWER: Poland is and will remain at the center of economic growth within Europe and it will still experience increasing political influence. Poland’s population won’t decline as much as those of the other major European economies and that is critical moving forward economically. Poland is also the most prosperous European state on Russia’s western border. That will mean that it will expand its position as a regional leader with political and economic prestige.

The Zloty has strengthened against the dollar and the Euro. The critical time where Poland may see this break with the EU could come in 2020.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America

The lack of individual investors infiltrating this market leaving the big agricultural bets being placed not on expectations of global food demand will increase over time, but looking simply for yield, has led most analysis astray. Institutions, like the pension fund TIAA-CREF, have been the big buyers throughout 2017. They have been looking for bargains as farm real estate values have started to decline. Small farmers are finding it difficult to borrow from the banks for a crop season which can involve loans into several millions of dollars. If crops are wiped out, then they have a real problem.

The lack of individual investors infiltrating this market leaving the big agricultural bets being placed not on expectations of global food demand will increase over time, but looking simply for yield, has led most analysis astray. Institutions, like the pension fund TIAA-CREF, have been the big buyers throughout 2017. They have been looking for bargains as farm real estate values have started to decline. Small farmers are finding it difficult to borrow from the banks for a crop season which can involve loans into several millions of dollars. If crops are wiped out, then they have a real problem.

I believe it was Goldman Sachs who paid bribes to Russian politicians to recall Platinum from the market and temporarily stop sales to allegedly take an “inventory” of their stockpile. This sent prices

I believe it was Goldman Sachs who paid bribes to Russian politicians to recall Platinum from the market and temporarily stop sales to allegedly take an “inventory” of their stockpile. This sent prices