Armstrong Economics Blog/Understanding Cycles

Re-Posted Jan 12, 2018 by Martin Armstrong

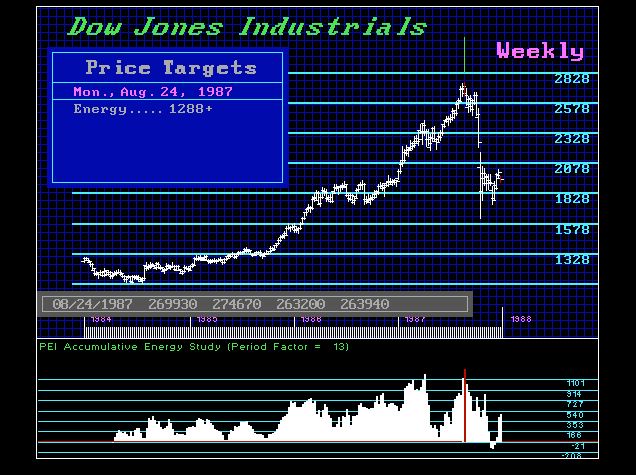

TIME is more than just money; it’s absolutely everything and then some! Personal opinion just utterly fails because we are all human. Markets routinely do what the majority never expects. That is their function. They mutate like a virus always changing its genetic code to defeat medicine, or in this case, traders. Back on November 30th, 2017, I explained on the private blog: “We must respect that exceeding the November high now in December on a sustained basis, points to a January high. If we pull back, then January will be a low and then watch out for a sharp rally into March.”

TIME is the very fabric of the universe and probably the most misunderstood element of all. In physics, the relativity of simultaneity is the concept that baffles many. The question becomes, do two distant events actually take place simultaneously? Therefore, the question whether two spatially separated events occur at the same TIME is recognized to be far from absolute. It is “relative” depending on the observer’s reference frame. This becomes incredibly important in terms of forecasting the world markets.

TIME is the very fabric of the universe and probably the most misunderstood element of all. In physics, the relativity of simultaneity is the concept that baffles many. The question becomes, do two distant events actually take place simultaneously? Therefore, the question whether two spatially separated events occur at the same TIME is recognized to be far from absolute. It is “relative” depending on the observer’s reference frame. This becomes incredibly important in terms of forecasting the world markets.

To grasp what our model is really doing one must look at TIME and EVENTS more in the perspective of turning points – not specific events. Once you understand we are forecasting turning points on the TIME horizon, not specific events, you will begin to make a leap forward into a new world of understanding TIME.

Specific events on the horizon become easy for forecast based upon the trend in motion relative to TIME. When trends reach that events horizon in time, then a specific high or low is easily ascertained. Right now, we are in the throes of a major breakout and a characteristic of Vertical Markets has been what we call the Cycle Inversion process. Normally, turning points unfold in opposite pairs. So a November high would traditionally be followed by a January low. Merely exceeding the November high on a closing basis during December identified the continued rally into the next target being January 2018 warning we were (1) dealing with a Cycle Inversion, and (2) a Vertical Market that is going to be very difficult to trade for most people.

It is paramount that we understand how Vertical Markets function.