Posted Originally on May 16, 2024 By Martin Armstrong

The New York Federal Reserve reported that American households set a new record after plummeting into $17.69 trillion of debt, a 1.1% ($184 billion) increase from Q4 2023. Worse, the number of delinquencies is rising as households struggle to make ends meet amid the cost of living crisis. Inflation is not waning, taxes are rising, and America’s debt burden has become utterly unmanageable.

Mortgage balances rose by $190 billion and reached $12.44 trillion by March. People are paying far more in interest alone than they have in recent years. Those who bought in the hopes of refinancing are not in a good position. Auto loan debt rose by $9 billion, reaching $1.62 trillion.

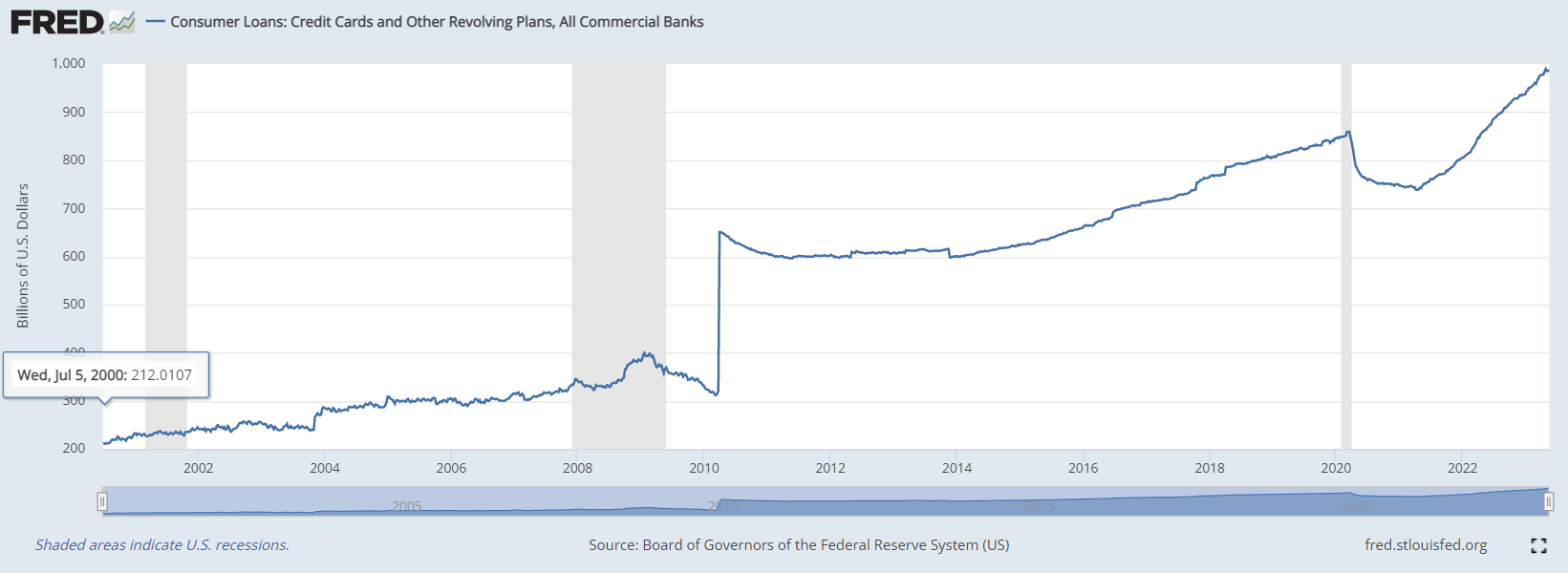

Americans have been attempting to pay off their credit card balances, with overall credit card debt declining by $14 billion to $1.12 trillion. Yet, that was close to a record-high for credit card debt and we tend to see balances lowered after the holiday retail spending spree ends. Consumers do not want to pay those 20%+ interest rates on cards but many are forced to do so simply to put food on the table.

Delinquencies are rising – this is a major issue. It is difficult to crawl out of debt once someone is deep within the cycle. “In the first quarter of 2024, credit card and auto loan transition rates into serious delinquency continued to rise across all age groups,” said Joelle Scally, regional economic principal within the Household and Public Policy Research Division at the New York Fed. “An increasing number of borrowers missed credit card payments, revealing worsening financial distress among some households.”

Credit card delinquencies have reached their highest levels since 2012 when America was recovering from the Great Recession. In fact, by the end of Q1 2024, around 3.2% of all outstanding debt was in delinquency. The New York Fed reported a rise in missed payments across all debts, including those 90 days past due.

No foreign nation is coming to offer America a bailout check. The Biden Administration has made it clear that American households are NOT Washington’s priority. We are to continue working and paying taxes in order to fund foreign wars and climate change packages. How else will we house those 7+ million illegal migrants and offer them free healthcare and shelter? How else will we pay off the student loans for millions? How else will we continue to grow the public sector and pay for countless new social programs? Americans are in serious debt, and Washington is all but ensuring this trend continues.