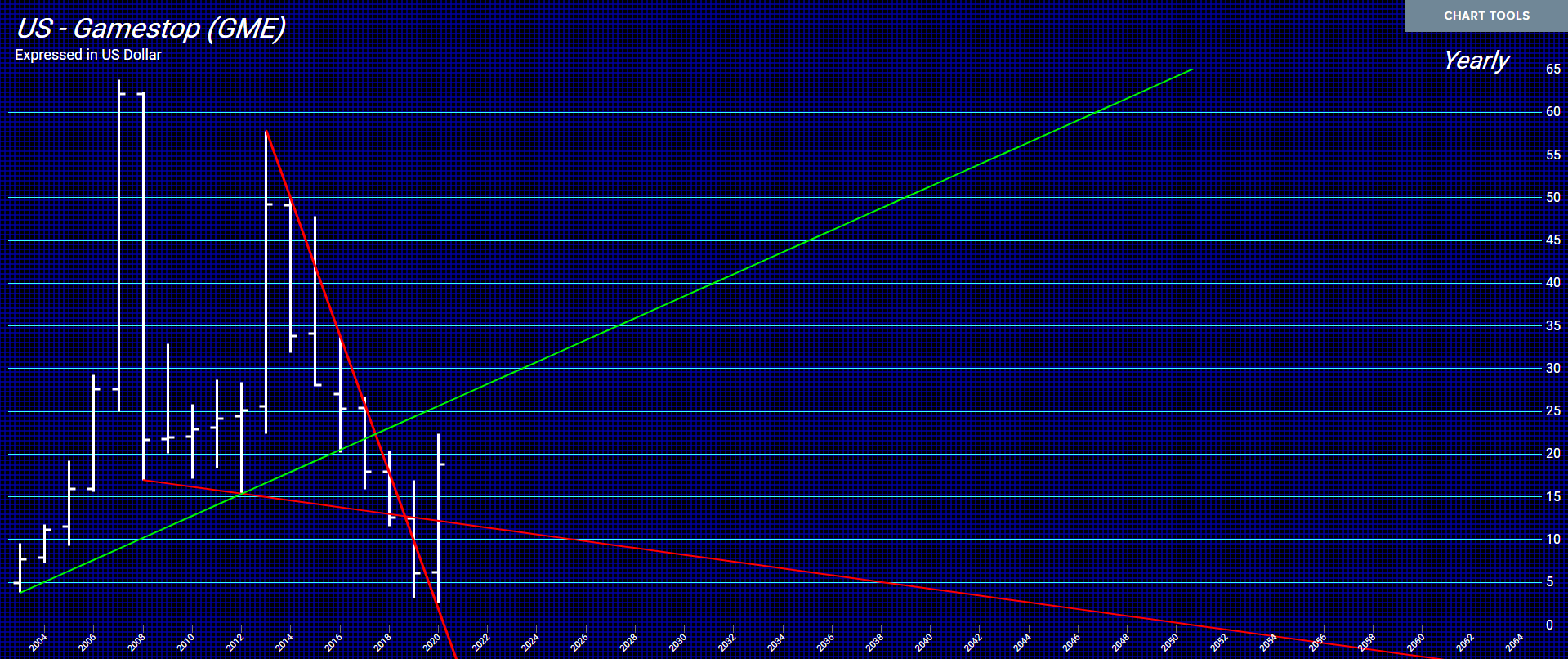

Gamestop has rallied back during the week of March 8th after all the hoopla. Cyclically, it was 13 years down and it was due for a bounce. Even our pattern recognition models picked up the rally starting in August 2020. Quite frankly, this has all the hallmarks of manipulation, but not what you may think. The classic manipulation is to pump up a market touting some player but the pros have already been in the market. This is how the Buffet manipulation of silver was done in 1998 and even the entire Hunt Brothers silver rally back in 1980.

I knew the Hunt Brothers were buying silver from the early 1970s. At the end, their name was attached to silver and the claim was they were taking it to $100. At that time, the exchange pulled the same maneuver and made it a fraction in margin to go short but 10x that to go long. The Hunts were trapped and could not sell anything without everyone jumping in front of them,

Melvin Capital, which was a small hedge fund lost 53% of its capital in January on GameStop. Not sure how that was possible unless the bet was purely a gut-trade rather than quantitative. The four largest asset managers in the world together own 39 percent of GameStop shares, according to regulatory filings. Those stakes, which are mostly held for years in passive index funds, have collectively gained roughly $1 billion in value since the beginning of this year. The hype of a huge short-squeeze seems to be exaggerated. One hedge fund, Senvest Management, recently boasted to clients that it made more than $700 million from a bet on GameStop in September, the Wall Street Journal reported. Certainly, our model was long, not short and I cannot see even a trend-following-model that would have been short. Melvin Capital to lose 53% does not seem to be very professional to lost that much on a single stock. The long-term is not over in this stock.

The assumption in governments has always been that WE ARE THE PROBLEM – not them! They have really believed that if they could tax the underground economy they would have balanced budgets. We all know that in reality, no matter how much money they collect, they will always spend more. This idea that digital currency will wipe out crime is rather absurd. I was talking to a young person who buys their weed, like so many these days. They make a phone call, it is dropped off in their mailbox, and they pay by some cash transfer application. So they never even see the person anymore. So the move toward digital transactions has not eliminated the underground economy, it has actually improved it making it more efficient.

Meanwhile, the criminals have to learn now how to code in order to hack into systems. It seems that this trend is forcing criminals to become much more professional in their endeavors.

COMMENT: Mr. Armstrong, I thought you were wrong on Bitcoin and that it was a store of value. I can see now that it is only a trading vehicle as you have said. But what made me write to you is I just read that Dorsey is opening up an online bank. You got that right too. It is interesting when I read you and compare to others, you are the one who comes out correct in the end.

My humble apology for being a doubting, Thomas.

GP

REPLY: I know for a fact they have allowed Bitcoin and other cryptocurrencies to exist in order to condition people into accepting the end of paper money. I cannot understand people who think I am wrong and somehow cryptocurrencies will overthrow the dollar and governments. Really? Does anyone really believe that governments will just relinquish power willingly?

We are headed into a wave of inflation, but one that is constructed on shortages. One need only look at the systemic problems behind the shortages created by a planned economy during the communist era. A goods shortage was the norm. Those under communism were confronted with chronically empty store shelves. When the shelves were replenished on rare occasions, there were long lines that would form outside the stores for blocks. I had a Russian girl who worked for me as a programmer. She said the number one problem coming to America was having to make decisions in the store. She said they had only one type of toilet paper. There are so many here. She didn’t know how to buy anything for each purchase involved a choice and decision.

Even in China, there were ration coupons that became the norm. Just about everything was rationed. This is what takes place when the government is in control of production be it directly, or through what we are beginning to see, outrageous regulations – lockdowns which are hailed by Schwab’s World Economic Forum.

This is NOT really a question of I TOLD YOU SO. This is not a contest of my opinion v someone else. I really have to wonder if some of those mouthing these absurd forecasts are not being made as deliberate misinformation to move people toward a digital currency on behalf of the powers behind the curtain. They defy all reason and show either sublime stupidity or cunning devious misinformation to manipulate society to pull off this Great Reset.

I warned back on January 21, 2021, that BigTech sees the power to overthrow the banks. These powers have declared that they want everyone in the banking system worldwide to end paper money, which is over 1 billion people (just read the IMF). This is why Dorsey, Facebook, YouTube, and Google along with Microsoft were blocking Trump and funneling money to the Democrats who bribed them with the dream of controlling international banking. If governments take Schwab’s solution and default on all its debt, then they NO LONGER NEED THE BANKERS to sell their bonds. Branch banking will come to an end and these people think they will move to a controlled economy with no private debt. They are out of their minds!

I know what I am talking about. I have shaken the hand of Schwab. Have any of these people claiming Bitcoin will overthrow the dollar ever talked to anyone in authority? I have met with board members of the IMF. There are those who are so desperate to convince people not to listen to me because they are part of the entire scam against We the People. I have been approached many times to join these globalists. They preach the Fourth Industrial Revolution is coming, but post comments on YouTube to try to prevent people from looking at Socrates because it forecasts their demise. Sorry Schwab, but Socrates says you fail!

Schwab and his cohorts think locking us all down and destroying the economy and production is a good thing. I cannot see how ANYONE takes a position against me who is not really working against our freedom and human rights. They are so desperate to stop people looking at Socrates or the media to ever cover what Socrates is doing, all in their quest to conquer the world.

So it is not I TOLD YOU SO, this is not a matter of opinion. This is a serious global effort to redesign the world economy and Socrates stands in their way.

The outage of the National Settlement Service and the Fedwire Securities Service, which provides issuance, settlement, and transfer services for Treasuries and other government securities, was down and this has caused some concern and then conspiracy theories mixed in. The Fed made progress reversing the shutdown within a couple of hours, however, this has illustrated that a long-term outage of the Fed’s online services could cause intense chaos across the world financial system, preventing banks and businesses from finalizing transactions and impeding basic banking functions.

The Federal Reserve said an outage of its key financial services on Wednesday was caused by a maintenance mistake and it is taking steps to prevent a recurrence. The official statement read:

“The incident was caused by an operational error involving an automated data center maintenance process that was inadvertently triggered during business hours,” a Fed spokeswoman said. Such tasks are normally performed after-hours, she said, adding, “This was human error.”

“Our technical teams have determined that the cause is a Federal Reserve operational error,” the Fed said on Wednesday on its website. “The Federal Reserve Banks have taken steps to help ensure the resilience of the Fedwire and NSS applications, including recovery to the point of failure.”

There was no power-outage so it does appear that the Federal Reserve was honestly calling it a disruption due to an ‘operational error’. This raises the issue of concern surrounding digital currency. Indeed, solar flares and other solar–mass ejections that travel through space can overwhelm Earth’s atmosphere and generate powerful electricand magnetic fields. These magnetic storms can occasionally be intense enough to disrupt the operation of high-voltageelectricity lines. A digital currency system could be brought to its knees with an EM attack.

We do have an EMP Task Force on National and Homeland Security whichissued a reporton China’s ability to conduct an Electromagnetic Pulse attack on the United States. China now has super-EMP weapons and could engage in a first-strike attack that could blackout the entire country. China could actually launch a surprise “Pearl Harbor” type attack that could produce a deadly blackout of the entire country. Indeed, China has built a network of satellites, high-speed missiles, and super-electromagnetic pulse weapons that could meltdown the electric power grid, fry critical communications, and even takeout the ability of our aircraft carrier groups to respond. All of this is possible today using EMP weapons rather than nuclear.

The outage at the Federal Reserve was not an attack, loss of power, or anything nefarious. It was indeed a human error. Nonetheless, this outage even for a few hours brought the economy to a halt. This is the system used by U.S. banks to execute some $3 trillion in transactions daily and the outage began around 11.15 am Eastern time on Wednesday, and remained down for more than three hours. Most of the key systems, including the backbone settlement services Fedwire and FedACH, were back online by 3 pm. Fedwire is the system for large transfers between banks which last year handled 184 million transactions totaling more than $840 trillion, or more than $3.3 trillion daily, according to Fed data.

Other affected systems included FedACH, the clearinghouse which generally handles smaller transactions such as paychecks, tax refunds, and utility bill payments. The National Settlement Service (NSS), used by depository institutions with Federal Reserve Bank master accounts, was also shutdown offline. Every other transaction service maintained by the Fed was also affected by the disruptions.

Fedwire Funds is the premier electronic funds-transfer service that banks, businesses, and government agencies rely on for mission-critical, same-day transactions. On a monthly basis, Fedwire handles more than 835,000 transactions a day on average, with a daily average dollar volume of $3.4 trillion.

CHIPS, a private-sector alternative to Fedwire run by The Clearing House, continued to operate normally. ET. CHIPS handles about $1.5 trillion a day, according to its website.

QUESTION: Marty, do you agree with other analysts who claim debt defaults create revolutions? From reading your work for decades now, I think you would say it was taxes. Am I correct?

Hopefully, see you at the next WEC again

KL

ANSWER: You are correct. Rome never had a national debt nor a central bank. State debt is really a post-Dark Age phenomenon and there have been plenty of sovereign defaults and the vast majority never involved revolution. The Spanish sovereign defaults took place, turning the country into a serial defaulter beginning in 1557 followed by 1570, 1575, 1596, 1607, and 1647 ending in a 3rd world status. Greece defaulted on its external sovereign debt obligations at least five previous times in the modern era (1826, 1843, 1860, 1894 and 1932). Even Magna Carta cut off the king’s ability to use the courts to raise money, which was before taxing the average person.

Anyone who claims that a sovereign default will unleash a revolution has not actually done the research. It is probably more of a sales pitch to get business with scare tactics. Both the American and French Revolutions were over taxes – not sovereign defaults.

We are headed into a revolutionary period, but it is being caused by this global hunt for taxation which is undermining the entire world economy. The sovereign default comes because of the collapse in commerce which is set in motion by raising taxes.

Yes, we are trying to pick a date for the next WEC. I am trying to be optimistic that our international clients can fly in. Of course, it all depends if Biden does not try to put a blockade around Florida because we have become the best state in America by preserving our freedom and it is at least far enough south to avoid the dip in the Jet Stream.

AOC “Thinks” More Wind Turbines Will Solve ALl Our Problems

In Texas, the cold snap and power outages have finally abated. For nearly a week millions of Texans suffered power blackouts during severely cold weather. Water was out as well. For awhile, Texas was plunged into the Dark Ages.

Part of the problem is America’s crumbling infrastructure. It is something President Trump addressed. He wanted to build new power plants, airports, bridges, and highways. Instead we have Biden carrying on Obama’s work of destroying America for the benefit of socialism and our enemy, China.

Biden’s regime did not want Texans to resort to emergency measures and burn more fossil fuels. Instead they had to rely on malfunctioning wind and solar farms, which proved ineffectual. It’s a bitter cold irony that Texas is rich in oil, yet the power still went out and for those who did get power, their electric bills skyrocketed.

Alexandria Ocasio Cortez said her new Green New Deal would have helped to prevent the blackouts in Texas. It’s illogical for her to believe that climate change, global warming, and white supremacy are causing blackouts, but logic isn’t illuminating the socialist mind of AOC.

My wife and I are trying to buy a second home. We live in Wisconsin and want a place somewhere warm. We are trying to buy in Florida, but we are financing it and we bid at the asking. However, on all of the properties, someone comes in with cash and ABOVE asking.

Are we buying into a bubble? Is it best to wait? I will only consider Florida because that is where you are based off of your computer.

Any guidance would be appreciated.

Best,

P

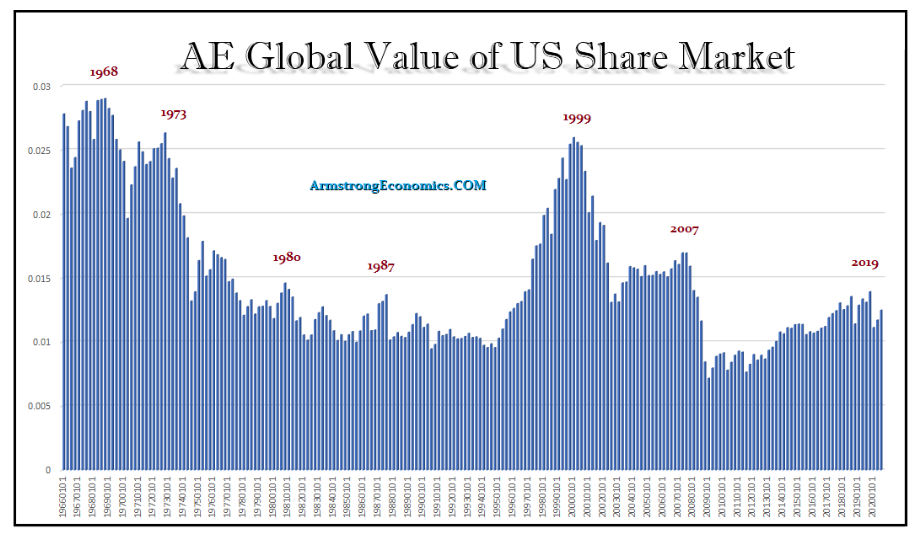

ANSWER: It does not appear to be a bubble. It is not just the real estate going up in Florida. The problem is limited supply and a mad dash out of New England, Illinois, and California. But this is taking place across the board. I was looking for a classic 328 Fararri of 1985 vintage. I use to have one in London. They were going for $50,000 on average. They are now running $100-$150,000 in 3 months. The same is happening in collectibles and art. It simply appears that we are entering the phase of a massive shift from Public to Private assets. This is our Index we have provided to our Institutional clients over the decades. The historic low was 2009 post-1968. This trend appears to be in motion overall into 2032.

In real estate, very few places up for sale and they are selling very fast. The draconian measures in the Democratic states like New York and California have accelerated the migration out of those regions. More than 1 million people have fled New York City to Florida already. You have major chains shutting down in New York City. New Yorkers are fleeing to Florida and so are the restaurants from New York. New Yorkers are realizing that even when vaccinated, it will not return to normal. New Yorkers are even migrating to Texas. But with the Ice Storms there, they are already shifting to Florida. Places like New York City are just no longer safe as is the case now in many cities in California. Gun permits are soaring in New York because of the sharp rise in crime. Politicians do not understand anything. If you are in business and sales decline, you run sales to try to boost activity. In New York, you impose lockdowns, revenue declines, so the solution is tax taxes and fees like tolls. You can’t make up this sort of brain-dead mismanagement. On top of all of that, the lockdowns have resulted in alcohol abuse, kids committing suicide for they cannot learn remotely, the very fabric of society is being torn apart.

I personally am not thrilled about this. Traffic has increased noticeably. Please go to the east coast! Even my house has doubled in value in four years. Florida is the safe-haven in the United States with no state income tax and no ice storms and a governor who has rejected the Democrat’s lockdown agenda that destroys society and business. It reminds me of my favorite movie, Brave Heart, being of Scottish heritage. They may take our lives, but they will never take our freedom. Just sometimes, you have to stand up against tyranny or you and your posterity will lose everything.

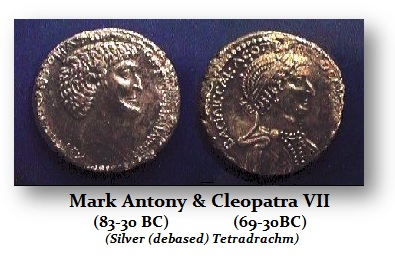

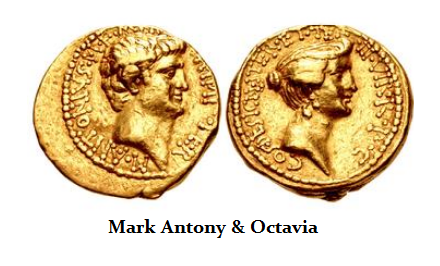

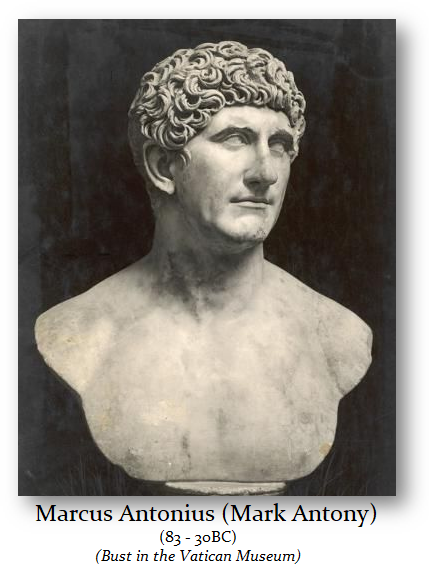

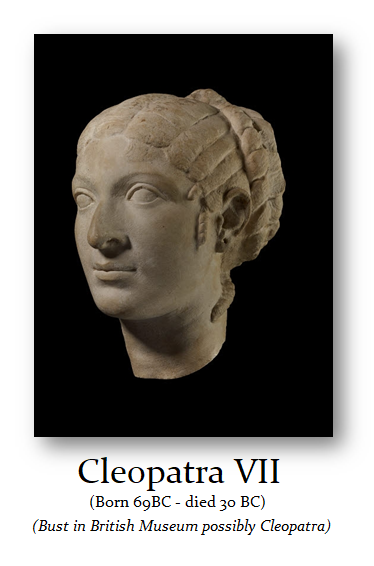

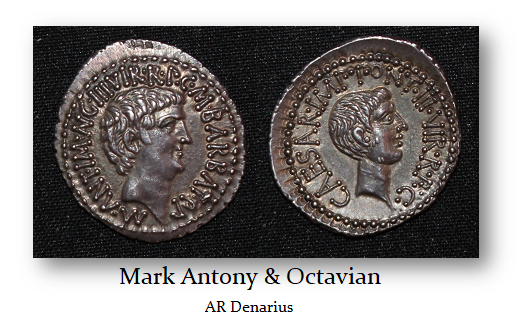

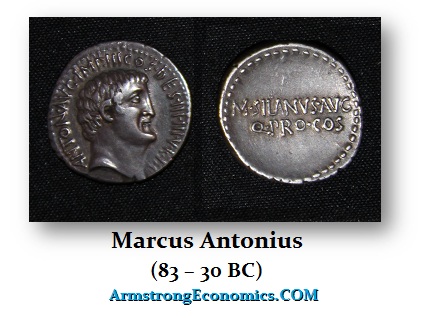

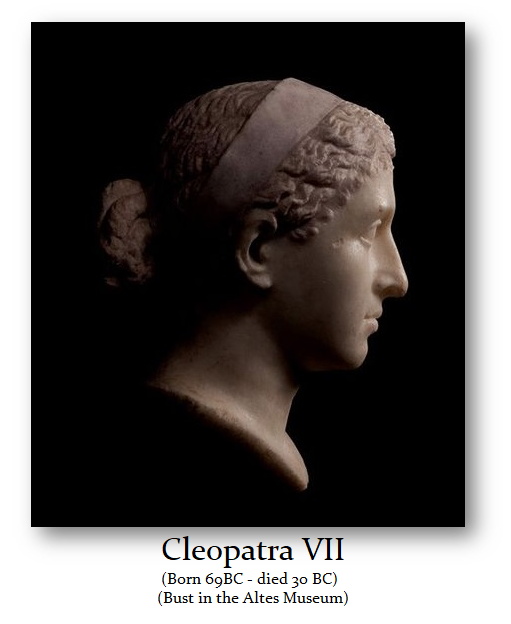

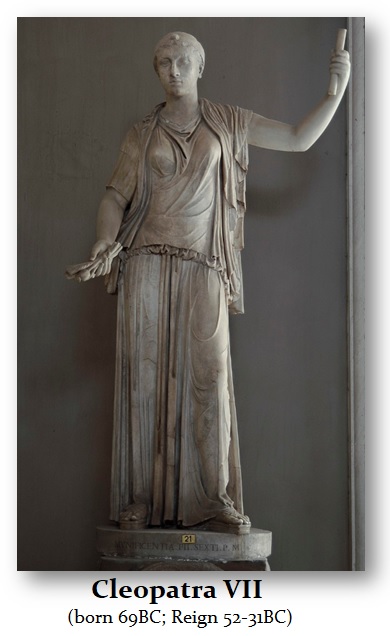

QUESTION: Marty, I watched a documentary on Cleopatra. Strange how she was married to her younger brothers. They said nobody knows what she really looked like but I thought if anyone would really know, it must be you. Was she the most beautiful woman of antiquity or was that legend?

FR

ANSWER: Plutarch does remark that the Romans pitied Antony for having callously evicted his dutiful wife Octavia from their house, “especially those who had seen Cleopatra and knew that neither in youthfulness nor beauty was she superior to Octavia” (LVII.3). It was said that her seductive abilities were superior, not necessarily her looks.

When we look at the coinage, that is how we are often able to identify the bust. They had created models for the coin engravers to follow for their images. Therefore, we can refer to the coins to get a real sense of who someone really was.

In the case of Cleopatra, coins clearly support what Plutarch wrote and he tends to be more historically accurate in general. The Romans I believe claimed she was so beautiful because Octavia was said to have been stunning. However, claiming Cleopatra was beautiful may be more of a rationale for her seducing both Caesar and Antony.

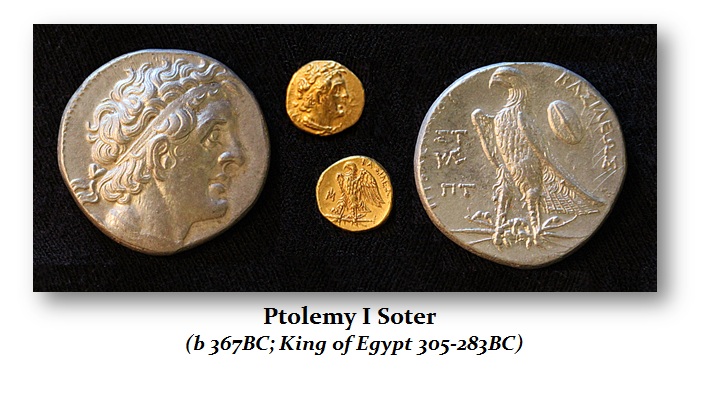

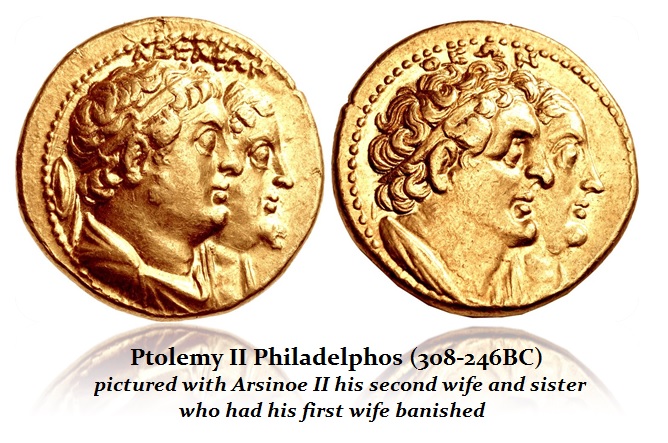

As for marrying her brother, there were two trends that gave rise to that practice. In ancient Egypt at that period in time, one was considered very lucky to have married their sister. Perhaps it was just keeping the property in family hands. In the case of Cleopatra, her family from Ptolemy I who was a general of Alexander the Great, were Greeks – not Egyptian. So some of the claims that Cleopatra was African were really absurd.

The son of Ptolemy I became Ptolemy II Philadelphos which meant “brotherly love” but not in the Christian sense, in terms of incest. Therefore, the entire family line of the Prolemy I were Greeks and nobody intermarried with an Egyptian.

The Ancient Egyptians were not a black race but were Phoenicians in origin. The question of the race of ancient Egyptians was always a hotly debated topic but the art does not support an African heritage. They appear to be more of the white race of Greeks which was the same for the Carthaginians. The dispute was really settled with DNA taken from mummies which revealed they were not of African origin.

The fall of the Bronze Age civilizations throughout the Middle East and Northern Africa, with the single exception of the Egyptians barely holding on, was the result of the invasion from up north of what was called the Sea People. There was most likely a pole migration which caused the temperature to drop sharply up north and inspired the migration south.

The freezing of the Whooly Mamouths in Siberia is estimated to have been about 10,000 years ago which may also account for why recorded history really beings about 6,000 BC. Dwarf woolly mammoths survived until about 4,000 years ago on Wrangel’s Island, north of Russia), and now their remains are disappearing fast.

It certainly appears that there was a dramatic shift in climate around 2,000 BC which impacted the migration out of Africa reversing the trend backward.

QUESTION: Marty, I found your passing comment on cash-like coupons by private stores becoming cash in the digital world. Could you elaborate?

thank you as always

BK

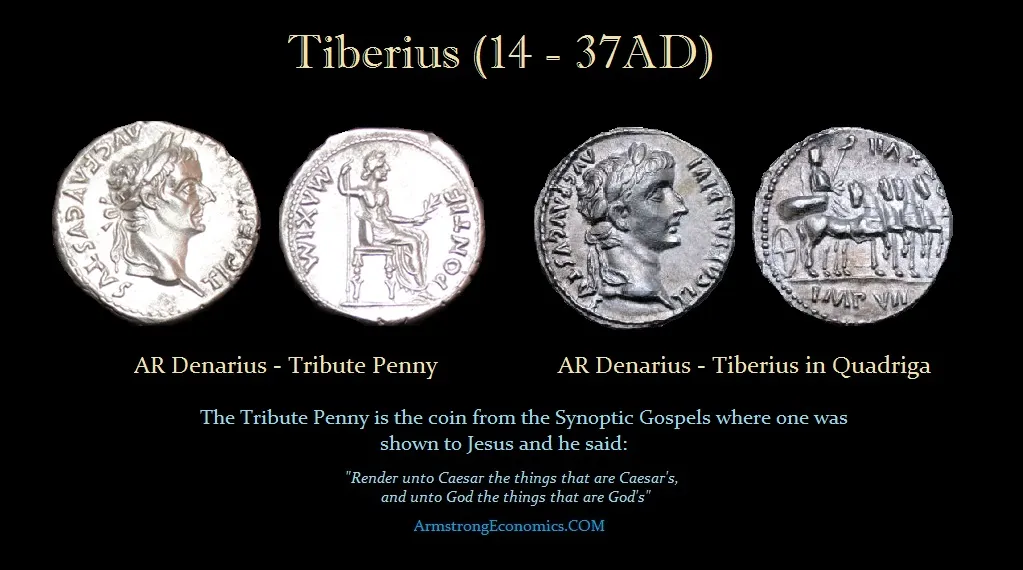

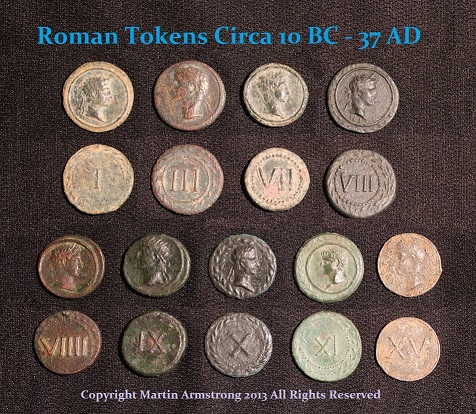

ANSWER: Aside from the ancient Roman prostitute token, we have often found private tokens emerge as money during periods of shortages in physical money. The Roman Emperor Tiberius (14-37AD) was notoriously frugal. Where his predecessor Augustus (27BC-14AD) minted coins like no other emperor with so many varieties well over a 100, Tiberius reduced everything to two designs and cut the money supply. He ended up creating a Financial Panic of 33AD which was also a shortage of cash like during the Great Depression.

Hence, we find not only the prostitute tokens but a full range of tokens with different numerals on the reverse expressing value. One theory argued that they were tickets for entrance to the theater or the games, and the numerals represented sections in the stands, or that they were brothel tokens, with the obverse representing a chosen “product” and the reverse the price. However, this theory seems unlikely when one considers that the two seemingly divergent themes are joined by the same die links to the numeral reverses.

Alberto Campana (“Le Spintriae: Tessere Romane con Raffigurazioni Erotiche,” in La Donna Romana Imagini e Vita Quotidiana [2009], pp. 43-96) has published a new die study of the erotic pieces, recording eight specimens with at least basic find spot information, most notably a sealed tomb in Modena, firmly dated to the mid-late Julio-Claudian period, as well as other examples found around the Roman world in Palestine, Gaul, Germany, and Britain, often in areas of military interest. He notes that these tokens (tesserae) are primarily struck in orichalcum, a metal more valuable than regular copper or bronze. He thought they might be game pieces from a now-forgotten board game, possibly a variant of duodecim scripta, a game resembling modern backgammon (“Les spintriae et leur possible fonction ludique,” in Archeothema 31 [2013], p. 66).

These theories that have tried to come up with an explanation for these tokens, or tesserae, fail to consider the economics of the time. When we look at such periods of austerity such as the American Civil War were there was a shortage of metal coins and the Great Depression where hundreds of cities were forced to print their own currency, then these tesserae from the time of Tiberius are more in line with the financial crisis of 33AD and the fact that Tiberius reduced the coinage dramatically and disapproved of real estate speculation at the time.

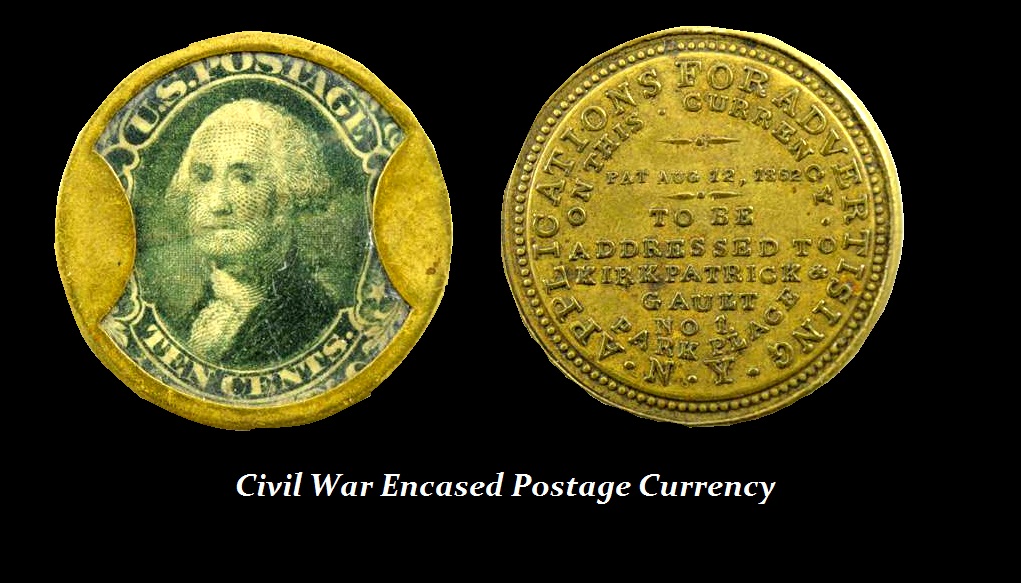

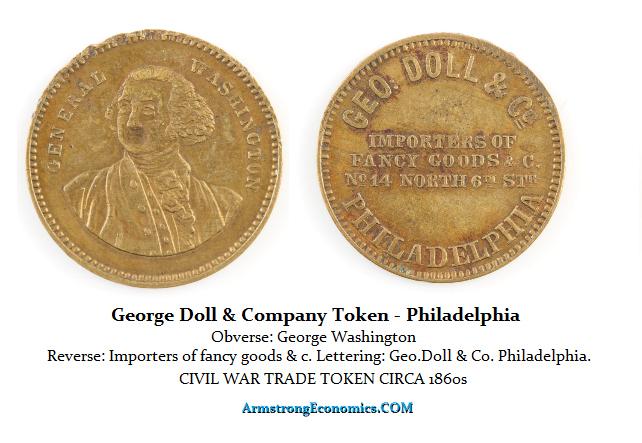

During the American Civil War, the shortage of coins led to private companies striking their own coinage, The reverse would often advertise the store but these tokens were generally accepted universally. They were treated as regular pennies.

We find also higher denominations where they used postage stamps as the backing. They were encased and again on the reverse, you will find the store advertising that they were the originator. Once more, these were universally accepted in common day to day commerce.

From the Panic of 1873, once again there was a shortage of coinage developing. Here we find an 1876 token issued by R. H. Macy & Company. The US demonetized silver in 1873 and stopped producing the silver half-dime. They also changed the design of much of the coinage. In 1874 they minted 14.1 million pennies but in 1876 it dropped to 7.9 million and in 1877 production collapsed to just 852,500. Indeed, the 1877 Indian Head pennies are rare due to the economic slump that began in 1873 continued with full force. Demand for United States coinage was at an all-time low, and families struggled to make ends meet. Saving even a penny for a coin collection was not an option for most Americans so these coins in uncirculated condition will often bring over $100,000.

The first large issue of Notgeld (Emergency money)started at the outbreak of World War I as coins were hoarded and metals were diverted for wartime uses. These notes were issued in small denominations. This currency was not legal tender — but was used and accepted on a voluntary basis within local areas. The advantage of issuing Notgeld (Emergency money) was that it stabilized local government and local markets, so people could buy and sell what they needed while government services kept functioning, plus it helped concentrate the official currency in the hands of the government, where it could be used for non-local transactions. This very same trend emerged in the United States during the Great Depression. The central bank in Germany could not produce enough notes to keep up with inflation, so new Notgeld was issued in denominations of thousands, millions and billions of marks. Private Notgeld was also issued in the form of commodities or other currencies for backing: wheat, rye, sugar, coal, wood, natural gas, electricity, gold, or U.S. dollars, known as “Wertbeständige” or notes of “fixed value.”

There was no “helicopter money” during the Great Depression for it was exactly the opposite – massive DEFLATION. There was a shortage of money to the point that hundreds of cities began to issue their own “Depression scrip.” You have to understand the dynamics of economic decline. People naturally hoard their money when they fear the future. The Great Depression was the very age of AUSTERITY where the assumption was that the collapse was due to a lack of confidence in government so they increased tax collection and cut spending, which unleashed both deflation and a dwindling money supply. This led many cities to create their own money due to the lack of money in circulation that was impacted by hoarding.

In Austria, there was an experiment to try to prevent people from hoarding cash during periods of economic crisis. This experiment was hailed as the “Miracle of Wörgl” which also took place during the Great Depression. The Wörgl Experiment began on July 31, 1932, the very month that the Dow Jones bottomed. The experiment involved issuing “Certified Compensation Bills” that were was a form of local currency known as Scrip or Freigeld. The monetary theories of the economist Silvio Gesell were applied by the town’s then-mayor, Michael Unterguggenberger. What differed from Gesell’s idea was that the currency would expire. Believe it or not, there are some governments looking into a currency that expires. Since World War II, Europe has issued currency that expired roughly every 10 years. This forced people to bring out the old currency to be swapped and thus prevented hoarding.

The central part of Gesell’s idea was how to stop the HOARDING of money. This is why FDR confiscated gold. He too saw the problem of people hoarding money and not spending it. This is part of every economic decline. If there is no CONFIDENCE in the future, people save more. This is simply human.

Nevertheless, the Wörgl Experiment resulted in a growth in employment largely because they had to use the money. This allowed the local government projects to all be completed, which many called a miracle, for it appeared to defy the depression in the rest of the country. Inflation and deflation are also reputed to have been non-existent for the duration of the experiment. But this was simply the result of money expiring so there was no purpose in hoarding “money” or shifting it back to “asset” appreciation as in hyperinflation. Despite the appearance of success, the Wörgl Experiment was terminated by the Austrian National Bank on September 1, 1933.

This time, they are seeking to use digital currency to just totally eliminate physical money. No matter how politicians try to eliminate the underground economy, as we have witnessed since ancient times when there is a shortage of money that is when the private sector will respond. As I mentioned they will reestablish a rise to the reestablishment of barter and private tokens. In prison, cigarettes were money. Then packs of mackerel. Who knows what will emerge? USB sticks? Perhaps private paper money issued by companies that are a hybrid-coupon perhaps from stores like Macy’s. Big chain stores could easily issue coupons redeemable by the bare which will function as money.

The Seatle government has directed that people who are “essential” workers during this pandemic are to be now paid $4 per hour extra for hazard pay. Kroger grocery has decided to close its stores. There is simply no proof of a pandemic and far more people die from cancer than COVID and grocery stores do high volume with a very low markup, but politicians do not understand how businesses operate. The press touts 500,000 have now died from COVID to scare the hell out of everyone, yet the total number of deaths 606,520 deaths are expected in the US in 2020 from Cancer, and of 1,806,590 new cancer cases were reported. The government does not outlaw cigarettes nor do they lock down the country. 1.35 million people die in road accidents worldwide every year, but we do not outlaw cars.

Both Fauci and the World Health Organization are touting the Great Reset. Both are supposed to be confined to health. Yet both are supporting Klaus Schwab’s attempt to take over the world and install his vision of economic precisely as Karl Marx. When will the world wake up and smell the poison in the air?

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America