Posted originally on the CTH on May 18, 2024 | Sundance

On the issue of crypto currency, watch the DC voices very closely.

They are about to take up legislation on the topic of crypto currency, regulation and overall ramifications therein. Keeping in mind that a dollar-based Central Bank Digital Currency (CBDC) cannot and will not coexist within a financial system that permits the transition (the exchange) of dollars into crypto and vice-versa.

Put simply, in the Western financial system, crypto currency cannot exist with a CBDC. Duality of currency is possible outside the West, but not feasible, viable or possible given the political motivations behind the creation of the dollar-based CBDC.

First things first….. Remember just before Super Tuesday 2020 when all the Democrat candidates for the Dem nomination dropped out and fell in line behind China Joe? Do you remember Warren staying in to support Joe by splitting the Bernie vote and everyone wondered what her payment was going to be? Here’s your answer.

The holy grail for the progressive movement was formerly known as a “carbon trading” process or platform, where you would have to pay a fee for your specific life choices and human existence. That objective or goal never went away; it just modified into a process that would create the mechanism for the payment system – that’s the dollar-based CBDC.

Just like Obamacare, there is going to be a myriad of “If you like your doctor, you can keep your doctor” promises with CBDC. And there will be some “You have to pass the bill to see what is in the bill” later espousals to convolute the former promises as they conflict with the CBDC legislative outcomes that start to gain attention.

From the perspective of DC, control over us is the upside; however, their CBDC aspiration comes with a downside – direct bribery and money laundering for political benefit becomes harder. So, what we know they will try to achieve is something like they just did with FISA 702 renewal. Whereby everyone outside DC will be banned from crypto ownership, but everyone inside DC is exempt from the rule. [Remember, under their very specific FISA- 702 extension, DHS is not permitted to use electronic surveillance on federal politicians (without knowledge), only the proles.]

With the crypto currency issue, the ideological communists in DC (both Republican and Democrats alike) will demand legislation to block, ban and regulate the crypto exchange. The UniParty will not want a competing process for the exchange of value that subverts the control mechanism of the federal government.

(Washington DC) – Sen. Elizabeth Warren’s anti-cryptocurrency crusade is facing pressure from her own party.

Dozens of Democrats, including Senate Majority Leader Chuck Schumer, have broken with her in recent days and supported an effort to undo SEC guidelines that critics say discourage banks from holding digital assets. The Democrats defied not only Warren, but also President Joe Biden, who is threatening to veto the rollback. The rift may grow further next week when the House takes up sweeping, industry-backed legislation to incorporate crypto trading into federal financial regulations.

[…] The party’s Capitol Hill clash over crypto policy comes as the issue is becoming more prominent in the 2024 campaign. Former President Donald Trump is courting crypto fans, though they may represent a small minority of the electorate, and signaling that he’d rein in the SEC’s crackdown on the industry. Crypto super PACs are poised to spend more than $80 million to influence control of Congress and secure friendlier policy. It’s leaving Democrats at odds over whether to follow Warren’s push to clamp down on crypto firms or to take a friendlier approach. (read more)

The communists who are organizing the financial control system want to use the justification of war, North Korea, and a variety of foreign adversary arguments as well as drugs, criminal and human trafficking, as the manufactured crisis (scary shiny thing) not to be wasted. I mean if you like BitCoin, DC will claim you are a deviant predator of children who abuses drugs and loves some Kim Jong-Un dontchaknow.

The five major banks, all of whom gain maximum benefit from the CBDC as transfer brokers, will join Jamie Dimon (JPMorgan) and decry crypto as the planet harming, energy intense, earth polluting system that is currently melting the ice caps. Meanwhile Greta Thunberg and Taylor Swift will assemble their perpetually depressed Gen-Z forces against BitCoin et al.

Just watch, the seeds of the nonsense are already planted.

The Yellow Zone is specifically constructed to begin using a dollar-based CBDC likely sometime after the 2024 election, with open tests in 2025 depending on the election outcome. Even if Trump wins the ’24 U.S election, the bankers who control the rest of the yellow zone will continue implementation of the Dollar-Based Central Bank Digital Currency (DBCBDC) without direct USA participation (they will wait out Trump’s term).

Investors’ curiosity has peaked as central banks are increasing their gold purchases. We are not going back to a Bretton Woods type situation and that is not the issue. You must understand that gold is neutral. Central banks are buying gold because the Neocons have weaponized the dollar.

Russia was removed from the SWIFT system, and private citizens’ assets were confiscated. When Russian assets were removed from SWIFT, a threat to the world was issued to say, “Hey, if you don’t do what we tell you to do, we will take you out of SWIFT.”

This is not the end of the dollar. Money continues to pour into US equities, particularly the Dow. Why? When the drum of war is beating, major institutions rush to move their money into a safe haven, which happens to be the US at this point in time. The big money is not purchasing start-up equities on the Nasdaq, for example, as they will not take that risk. Our computer model indicates the Dow will continue rising into 2032 as it remains one of the last safe havens.

The West has become extremely aggressive in its geopolitics. You simply do not buy the debt of your enemy. Central banks are buying gold because the USD is political.

There is a stark difference between short-term and long-term bonds. The central banks have zero control over the short-term and that is how this whole QE fiasco began as central banks began purchasing long-term debt in an attempt to reduce long-term interest. Why would you buy long-term when war, the primary driver of inflation, is looming? This is a serious situation that the neocons who have weaponized the dollar simply do not understand.

The quoted banker does not specifically talk about the Central Bank Digital Currency that lays at the end of the promoted rainbow; the author does. However, the banker does outline a familiar step in the current process. As a result, it is worth drawing attention to the continuum.

MAINE – “According to Hannigan, the COVID-19 pandemic forced businesses to implement “paper-free and virtual processes” to handle their finances while “adapting to the new reality.

“For years, Americans had been slowly moving away from cash and paper checks, but the pandemic supercharged the trend,” Hannigan wrote. “By last year, 41% said they never use cash for purchases, up from 24% in 2015, according to the Pew Research Center. Only 14% still exclusively use cash and checks.” (Read More)

There is a BIG difference between electronic funds (current), and a digital dollar (future).

Posted originally on Mar 27, 2024 By Martin Armstrong

In 1996, the US government released a white paper entitled, “How to make a mint: the cryptography of anonymous electronic cash.” Released by the National Security Agency Office of Information Security Research and Technology, this document basically explains how a government agency could create something like Bitcoin or another cryptocurrency.

I encourage those interested to read the contents of the link above. This document was released during the dawn of the dot.com bubble before the technology existed to create such a currency. The NSA quickly realized that it could weaponize this technology to create a cashless society.

As explained in the introduction:

“Among the most important uses of this technology is electronic commerce: performing financial transactions via electronic information exchanged over telecommunications lines. A key requirement for electronic commerce is the development of secure and efficient electronic payment systems. The need for security is highlighted by the rise of the Internet, which promises to be a leading medium for future electronic commerce.

Electronic payment systems come in many forms including digital checks, debit cards, credit cards, and stored value cards. The usual security features for such systems are privacy (protection from eavesdropping), authenticity (provides user identification and message integrity), and nonrepudiation (prevention of later denying having performed a transaction) .

The type of electronic payment system focused on in this paper is electronic cash. As the name implies, electronic cash is an attempt to construct an electronic payment system modelled after our paper cash system. Paper cash has such features as being: portable (easily carried), recognizable (as legal tender) hence readily acceptable, transferable (without involvement of the financial network), untraceable (no record of where money is spent), anonymous (no record of who spent the money) and has the ability to make "change." The designers of electronic cash focused on preserving the features of untraceability and anonymity. Thus, electronic cash is defined to be an electronic payment system that provides, in addition to the above security features, the properties of user anonymity and payment untraceability..

In general, electronic cash schemes achieve these security goals via digital signatures. They can be considered the digital analog to a handwritten signature. Digital signatures are based on public key cryptography. In such a cryptosystem, each user has a secret key and a public key. The secret key is used to create a digital signature and the public key is needed to verify the digital signature. To tell who has signed the information (also called the message), one must be certain one knows who owns a given public key. This is the problem of key management, and its solution requires some kind of authentication infrastructure. In addition, the system must have adequate network and physical security to safeguard the secrecy of the secret keys.”

The introduction goes on to discuss the reasons they could present to the public to switch to a cashless society, including money laundering, convenience, and security. “The term electronic commerce refers to any financial transaction involving the electronic transmission of information. The packets of information being transmitted are commonly called electronic tokens,” the paper continues.

The NSA states that it would like to use “user identification” and “message integrity” to protect privacy in “nonrepudiation” transactions. “Eavesdropping” concerns appear numerous times throughout the document, which could be prevented by “not just privacy but anonymity” in the form of “payer anonymity” and “payment untraceability.” The government clearly states that hard currency, cash, provided these luxuries but could not be traced by the banks and, therefore, the government.

Again, this was released in 1996 before basic online banking. The document outlines basic online banking but takes it a step further by explaining how they could seemingly make payments seem “untraceable” to the public using “blind signatures” that allegedly cannot be seen by the bank. “This step is called “blinding” the coin, and the random quantity is called the blinding factor. The Bank signs this random-looking text, and the user removes the blinding factor.”

Alice sends the blinded coin to the Bank with a withdrawal request.

Bank digitally signs the blinded coin.

Bank sends the signed blinded coin to Alice and debits her account.

Alice unblinds the signed coin.

Payment/Deposit:

Alice gives Bob the coin.

Bob contacts Bank and sends coin.

Bank verifies the Bank’s digital signature.

Bank verifies that coin has not already been spent.

Bank enters coin in spent-coin database.

Bank credits Bob’s account and informs Bob.

Bob gives Alice the merchandise.

“This makes remote transactions using electronic cash totally anonymous: no one knows where Alice spends her money and who pays her.” Full “payment anonymity” would be “too much to ask”, thus, “we are forced to settle for payer anonymity.” In other words, the illusion that no one knows who is making the transaction.

PROTOCOL 5:Off-line cash.

Withdrawal:

Alice creates an electronic coin, including identifying information.

Alice blinds the coin.

Alice sends the blinded coin to the Bank with a withdrawal request.

Bank verifies that the identifying information is present.

Bank digitally signs the blinded coin.

Bank sends the signed blinded coin to Alice and debits her account.

Alice unblinds the signed coin.

Payment:

Alice gives Bob the coin.

Bob verifies the Bank’s digital signature.

Bob sends Alice a challenge.

Alice sends Bob a response (revealing one piece of identifying info).

Bob verifies the response.

Bob gives Alice the merchandise.

Deposit:

Bob sends coin, challenge, and response to the Bank.

Bank verifies the Bank’s digital signature.

Bank verifies that coin has not already been spent.

Bank enters coin, challenge, and response in spent-coin database.

Bank credits Bob’s account.

Note that, in this protocol, Bob must verify the Bank’s signature before giving Alice the merchandise. In this way, Bob can be sure that either he will be paid or he will learn Alice’s identity as a multiple spender.

The government begins to explain basic blockchain concepts, or at least how they’d like them to occur.

“When Alice spends her coins with Bob, his challenge to her is a string of K random bits. For each bit, Alice sends the appropriate piece of the corresponding pair. For example, if the bit string starts 0110. . ., then Alice sends the first piece of the first pair, the second piece of the second pair, the second piece of the third pair, the first piece of the fourth pair, etc. When Bob deposits the coin at the Bank, he sends on these K pieces.

If Alice re-spends her coin, she is challenged a second time. Since each challenge is a random bit string, the new challenge is bound to disagree with the old one in at least one bit. Thus Alice will have to reveal the other piece of the corresponding pair. When the Bank receives the coin a second time, it takes the two pieces and combines them to reveal Alice's identity…

Zero-Knowledge Proofs. The term zero-knowledge proof refers to any protocol in public-key cryptography that proves knowledge of some quantity without revealing it (or making it any easier to find it). In this case, Alice creates a key pair such that the secret key points to her identity. (This is done in such a way the Bank can check via the public key that the secret key in fact reveals her identity, despite the blinding.) In the payment protocol, she gives Bob the public key as part of the electronic coin. She then proves to Bob via a zero-knowledge proof that she possesses the corresponding secret key. If she responds to two distinct challenges, the identifying information can be put together to reveal the secret key and so her identity.”

The document then discusses ways to blind the signature, so that the payee may remain anonymous. Now, why would the government allow that to occur? “Even in anonymous, untraceable payment schemes, the identity of the multiple-spender can be revealed when the abuse is detected. Detection after the fact may be enough to discourage multiple spending in most cases, but it will not solve the problem. If someone were able to obtain an account under a false identity, or were willing to disappear after re-spending a large sum of money, they could successfully cheat the system.”

The document even discusses what we now would refer to as a crypto wallet. A seemingly safe offline method to store these electronic coins. They explain that at least one party must always reveal their hand. “When a coin is spent, the spender uses his secret to create a valid response to a challenge from the payee. The payee will verify the response before accepting the payment. In Brands’ scheme with wallet observers, this user secret is shared between the user and his observer. The combined secret is a modular sum of the two shares, so one share of the secret reveals no information about the combined secret.”

Who is the “observer” in this scenario? “An observer could also be used to trace the user’s transactions at a later time, since it can keep a record of all transactions in which it participates. However, this requires that the Bank (or whoever is doing the tracing) must be able to obtain the observer and analyze it. Also, not all types of observers can be used to trace transactions.”

In the event that a transaction was compromised, the bank would have to change its secret key and “INVALIDATE ALL COINS.”

The authors explain that tax evasion, per usual, is the key concern. They mention money laundering and “old crimes such as kidnapping and blackmail” as reasons to allow backdoor entry. Restoring traceability was a proposed solution, and if they could restore traceability in the first place, one must question if the payments were ever truly anonymous. Using Alice as their example, they explain that they could simply issue a warrant and track all her payment history. “Back~ard traceability is the ability to identify a withdrawal record (and hence the payer), given a deposit record (and hence the identity of the payee). Backward tracing will reveal who Alice has been receiving payments from.”

So, while the bank only sees the deposit in encrypted form, the public key must be used for withdrawal. “The ability to trace transactions in either direction can help law enforcement officials catch tax evaders and money launderers by revealing who has paid or has been paid by the suspected criminal. Electronic blackmailers can be caught because the deposit numbers of the victim’s ill-gotten coins could be decrypted, identifying the blackmailer when the money is deposited.”

“In conclusion, the potential risks in electronic commerce are magnified when anonymity is present. Anonymity creates the potential for large sums of counterfeit money to go undetected by preventing the identification of forged coins. Anonymity also provides an avenue for laundering money and evading taxes that is difficult to combat without resorting to escrow mechanisms. Anonymity can be provided at varying levels, but increasing the level of anonymity also increases the potential damages. It is necessary to weigh the need for anonymity with these concerns. It may well be concluded that these problems are best avoided by using a secure electronic payment system that provides privacy, but not anonymity.”

The US government released this document in 1996, 27 years ago. Bitcoin was allegedly anonymously created in 2009, and numerous other blockchain-based payment coins have followed. This, paired with the push for CBDC, where the government simply does not need to pretend payments are anonymous, should make one question the security and longevity of cryptocurrencies.

Posted originally on the CTH on March 25, 2024 | Sundance

If you followed my research on banking and the reality of the Russian sanction regime, this report from Reuters today takes on an entirely new dimension.

ME: …”The same way the Patriot Act was not designed to stop terrorism but rather to create a domestic surveillance system. So too were the “Russian Sanctions” not designed to sanction Russia, but rather to create the financial control system that will lead to a USA digital currency. The Western sanctions created a financial wall around the USA (dollar-based west), not to keep Russia out, but to keep us in. The Western sanction regime, the financial mechanisms they created and authorized, created the control gate that leads to a U.S. digital currency.” (more)

REUTERS TODAY: …”The firm [SWIFT] has gone from being virtually unknown outside banking circles to a household name since 2022 when it cut most of Russia’s banks off from its network as part of the West’s sanctions for the invasion of Ukraine. (more)

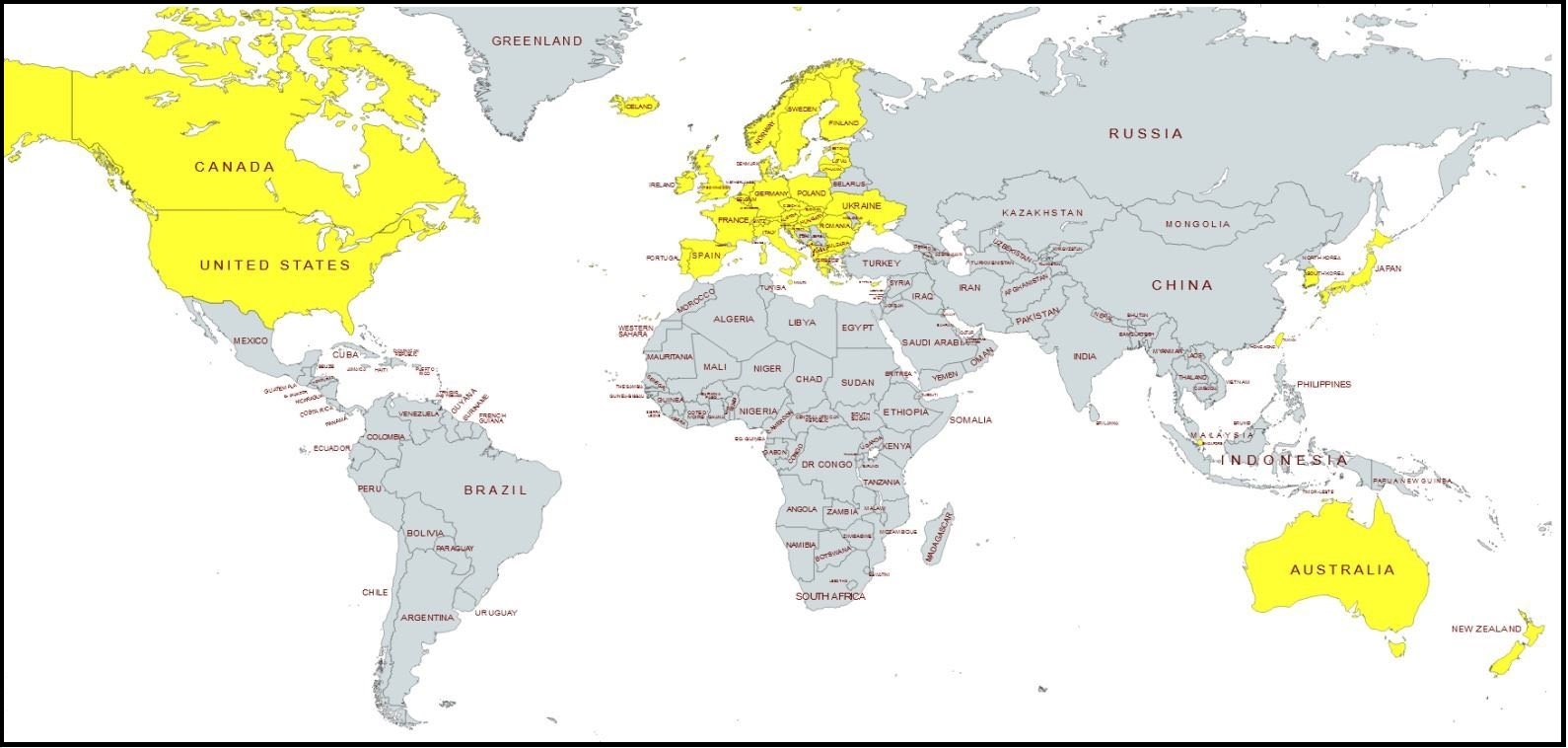

[The map shows the global financial cleaving, an outcome of sanctions against Russia]

I first started to deep dive research into these CBDC datapoints when the Russian sanctions were triggered.

You see, nothing about the sanctions really made sense from the way they were structured. Never before, not with Iran, North Korea, Venezuela or Cuba was the dollar weaponized against any entity who did not conform to the sanctions. Additionally, the intensity of the drive to make the sanctions the tip of the Western spear was just too pointed; something about it didn’t make sense. That’s what took me to dig deep into the sanction impact and realize nothing said about these financial sanctions made sense when compared against their actual outcome. {Go Deep}.

So, let’s start with the latest development:

(Reuters) – Global bank messaging network SWIFT is planning a new platform in the next one to two years to connect the wave of central bank digital currencies now in development to the existing finance system, it has told Reuters.

The move, which would be one of the most significant yet for the nascent CBDC ecosystem given SWIFT’s key role in global banking, is likely to be fine-tuned to when the first major ones are launched.

Around 90% of the world’s central banks are now exploring digital versions of their currencies. Most don’t want to be left behind by bitcoin and other cryptocurrencies, but are grappling with technological complexities.

SWIFT’s head of innovation, Nick Kerigan, said its latest trial, which took 6 months and involved a 38-member group of central banks, commercial banks and settlement platforms, had been one of the largest global collaborations on CBDCs and “tokenised” assets to date.

“We are looking at a roadmap to productize (launch as a product) in the next 12-24 months,” Kerigan said in an interview. “It’s moving out of experimental stage towards something that is becoming a reality.”

Although the timeframe could still shift if major economy CBDC launches get delayed, getting out the blocks for when they do would be a major boost for maintaining SWIFT’s incumbent dominance in the bank-to-bank plumbing network.

[…] A raft of heavyweight commercial banks including HSBC, Citibank, Deutsche Bank, Societe Generale, Standard Chartered and the CLS FX settlement platform all took part too, as did at least two banks from China.

The idea is that once the interlink solution is scaled-up, banks would have one main global connection point able to handle digital asset payments, rather than thousands if they were to set up an individual one with every counterparty. (read more)

The sanction regime against Russia was always intended to generate this outcome. This is the feature of the sanctions, not a flaw.

This dollar based CBDC was the intended destination of the people who constructed the Russian sanction plan (ex. BlackRock/WEF types). The Western politicians then were recruited and given instructions to support. Their cover story was “Build Back Better,” ie climate change, which was the predicate to the Russian sanctions.

I know at first blush a lot of this CBDC discussion seems esoteric, difficult to understand, and there are a lot of other issues happening simultaneously in the background. However, if you contemplate the biggest threat on this overarching power arc of Western government, you arrive to understand how serious this seemingly opaque issue really is.

2022 – NEW YORK, March 24 (Reuters) – BlackRock Inc’s (BLK.N) chief executive, Larry Fink, said on Thursday that the Russia-Ukraine war could end up accelerating digital currencies as a tool to settle international transactions, as the conflict upends the globalization drive of the last three decades.

In a letter to the shareholders of the world’s largest asset manager, Fink said the war will push countries to reassess currency dependencies, and that BlackRock was studying digital currencies and stablecoins due to increased client interest.

“A global digital payment system, thoughtfully designed, can enhance the settlement of international transactions while reducing the risk of money laundering and corruption”, he said.

[…] In the letter on Thursday, the chairman and CEO of the $10 trillion asset manager said the Russia-Ukraine crisis had put an end to the globalization forces at work over the past 30 years.

[…] “While companies’ and consumers’ balance sheets are strong today, giving them more of a cushion to weather these difficulties, a large-scale reorientation of supply chains will inherently be inflationary,” said Fink.

He said central banks were dealing with a dilemma they had not faced in decades, having to choose between living with high inflation or slowing economic activity to contain price pressures. (read more)

When the White House first started openly saying the Biden administration was reviewing how to implement CBDC’s, yes THAT Announcement ACTUALLY HAPPENED, September 2022, things from a research perspective really started to get serious. “While the U.S. has not yet decided whether it will pursue a CBDC, the U.S. has been closely examining the implications of, and options for, issuing a CBDC.” Whenever the U.S. govt says they’re “undecided,” pay close attention.

First things first with the Western financial sanctions- specifically the SWIFT exchange. It is true you cannot use VISA, Mastercard or any mainstream Western financial tools to conduct business in Russia; however, the number of workarounds for this issue are numerous. One of those tools is the use of a cryptocurrency like Bitcoin; and within that reality, you find something very ominous about the USA motive against crypto.

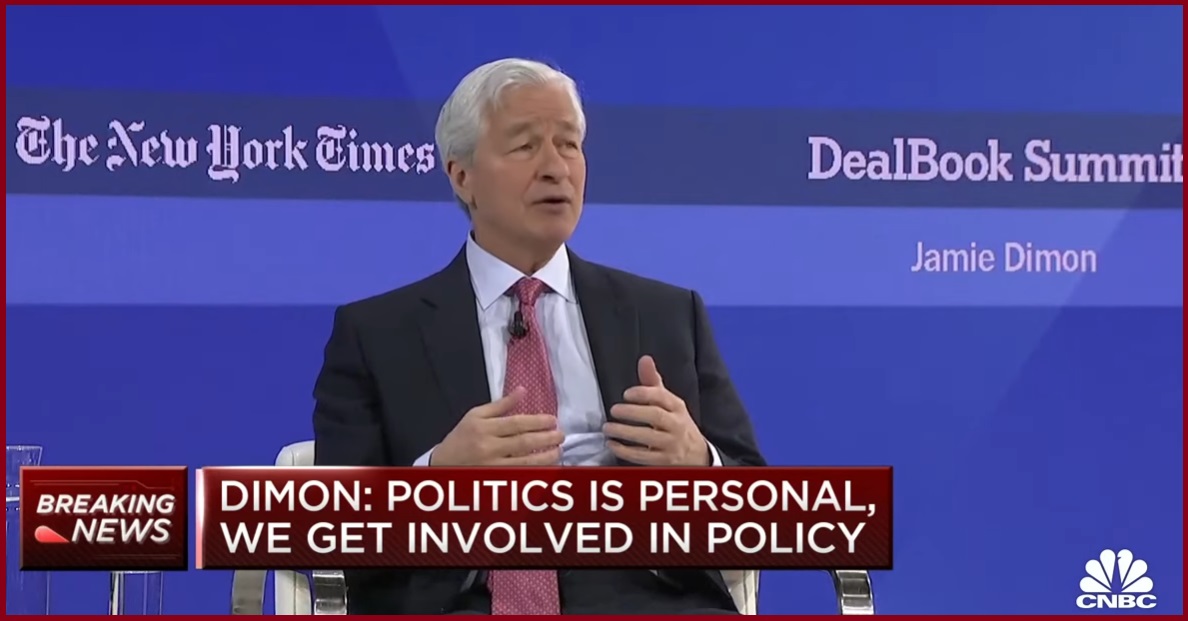

“I’ve always been deeply opposed to crypto, bitcoin, etc.,” Dimon said in response to a question from Sen. Elizabeth Warren, D-Mass. “The only true use case for it is criminals, drug traffickers … money laundering, tax avoidance because it is somewhat anonymous, not fully, and because you can move money instantaneously. “If I was the government, I would close it down.” (read more)

Dimon was/is positioning JPMorgan to be one of the facilitating beneficiaries of the financial control system evident within any CBDC process.

The US Treasury has set the financial system on an almost irreversible path to a U.S. Central Bank Digital Currency. As direct consequence, crypto currency alternatives are a threat to the establishment of that Western objective. This reality also pulls in the explanation around why the USA is so all-in for the banker-driven World War Reddit – the Russia-Ukraine conflict.

Conflict with Russia created the opportunity for the USA to create a sanctions regime that doesn’t truly sanction Russia; instead it controls the world of USA dollar-based finance. At the end of that control mechanism is a digital dollar, a Central Bank Digital Currency…. and by extension full control over U.S. citizen activity. The Marxist holy grail.

Take those reference points as an overlay, and now consider this little discussed 2022 announcement from the Biden administration:

[White House] – President Biden often summarizes his vision for America in one word: Possibilities. A “digital dollar” may seem far-fetched, but modern technology could make it a real possibility.

A United States central bank digital currency (CBDC) would be a digital form of the U.S. dollar. While the U.S. has not yet decided whether it will pursue a CBDC, the U.S. has been closely examining the implications of, and options for, issuing a CBDC. If the U.S. pursued a CBDC, there could be many possible benefits, such as facilitating efficient and low-cost transactions, fostering greater access to the financial system, boosting economic growth, and supporting the continued centrality of the U.S. within the international financial system. However, a U.S. CBDC could also introduce a variety of risks, as it might affect everything ranging from the stability of the financial system to the protection of sensitive data.

Notably, these benefits and risks might vary significantly based on how the CBDC system is designed and deployed. That is why Executive Order 14067, Ensuring Responsible Development of Digital Assets, placed the highest urgency on research and development efforts into the potential design and deployment options of a U.S. CBDC. The Executive Order directed the Office of Science and Technology Policy (OSTP), in consultation with other Federal departments and agencies, to submit to the President a technical evaluation for a potential U.S. CBDC system.

Today, OSTP is publishing its report, Technical Evaluation for a U.S. Central Bank Digital Currency System, which lays out policy objectives for a potential U.S. CBDC system and analyzes key technical design choices for a U.S. CBDC system. The report also estimates the technical feasibility of building a CBDC minimum viable product and describes how a U.S. CBDC system might affect Federal operations. The report makes recommendations on how to prepare the Federal Government for a U.S. CBDC system. Importantly, the report does not make any assessments or recommendations about whether the U.S. should pursue a CBDC, nor does it make any decisions regarding particular design choices for a potential U.S. CBDC system. (read more)

When you read that full announcement, you realize they have already built the system.

If the system is built, and they are now making policy recommendations for implementation, the question becomes, ‘What’s the goal’?

We do not have to look far for the explanation.

Prior to the White House announcement, the World Government Summit 2022 took place on March 29 and 30 in Dubai, hosting more than 4,000 individuals from 190 countries including senior government officials, heads of international organizations, and global “experts.” The invited participants presented ideas and worldviews from within their various fields of specialty.

One presentation was from Dr. Pippa Malmgren, an American economist who served as special adviser on Economic Policy to President George W. Bush.

Her father, Harald Malmgren, served as a senior aide to US Presidents John F. Kennedy, Lyndon B. Johnson, Richard Nixon, and Gerald Ford. In this segment, Mrs. Malmgren says the quiet part out loud. Yes, they are no longer hiding the construct; indeed, as you will hear, they are saying quite openly what the future will look like. WATCH (2 minutes):

Transcript – Dr. Malmgren: “What underpins a world order is always the financial system. I was very privileged. My father was an adviser to Nixon when they came off the gold standard in 71. And so, I was brought up with a kind of inside view of how very important the financial structure is to absolutely everything else.

And what we’re seeing in the world today, I think, is we are on the brink of a dramatic change where we are about to, and I’ll say this boldly, we’re about to abandon the traditional system of money and accounting and introduce a new one. And the new one. The new accounting is what we call blockchain.

It means digital, it means having a almost perfect record of every single transaction that happens in the economy, which will give us far greater clarity over what’s going on. It also raises huge dangers in terms of the balance of power between states and citizens.

In my opinion, we’re going to need a digital constitution of human rights if we’re going to have digital money. But also this new money will be sovereign in nature. Most people think that digital money is crypto, and private. But what I see our superpowers introducing digital currency, the Chinese were the first the US is on the brink, I think of moving in the same direction the Europeans have committed to that as well.

And the question is, will that new system of digital money and digital accounting accommodate the competing needs of the citizens of all these locations, so that every human being has a chance to have a better life? Because that’s the only measure of whether a world order really serves!”

The entry into a digital currency, needs a digital identity.

The end goal of a digital currency is why Western political leaders have not been worried about following the COVID-19 spending demands from the World Economic Forum. {Go Deep}

When the global trade currency does not need to be pegged, it is completely fiat. This is the current problem with global trade and transactions taking place in U.S. dollars, which arbitrarily lifts the standard of life for Americans while providing no similar benefit to other nations. That view became the underlying motive for Osama Bin Laden to target the World Trade Center, Twin Towers. That view was/is also the perspective carried by Barack Obama, that lay behind his “fundamental change” statement.

A digital currency allows ultimate control, on a global basis, by a one world government, or Western system of collective governments, that can assign value. No other mechanism will have as much control over the life of a person than a digital currency that will create a system of transactional credits and debits, perhaps also influenced by your social credit score.

Can it be stopped? I struggle with that question. I look in the mirror, think about the reality of how many people think this is an absurd conspiracy theory, and respond with…. How many people even know about the thing you are asking them to oppose?

How many people would believe the Western sanctions against Russia were really the USG building a cage to keep us in? Information, we need to start there. That’s my answer.

During remarks in New Hampshire, President Trump announced he would never allow the creation of a central bank digital currency. WATCH:

.

Of course, it should be noted….. as if the entire global system didn’t already oppose Donald Trump, this position against CBDC’s just puts an exclamation point on how the multinational financial systems will hate/oppose him even more.

This 2024 election is critical for a variety of reasons. However, high atop that list is this issue of how a dollar based CBDC is a threat to every liberty we cherish.

We will win this battle and eventually this war, or I’ll die fighting it.

They are trying to move fast, because people are catching on now.

We are on the right side of every issue; we cherish liberty and individual freedom. Our opposition is built upon a foundation of fraud and lies. The politicians are corrupt, and their arguments collapse when put in the sunlight; but they are not the root of the problem – they are vessels. That’s why the multinationals like BlackRock need the rules and referees (politicians) slanted in their favor. That’s why they need censorship, deplatforming, and beyond everything else…. they must control information.

…The key battle right now is an information war.

Tell your family, friends, neighbors. At first, they may think you are crazy, don’t quit. Share the information. Use the internal citations to help you bolster your arguments. Don’t quit planting seeds of information, and then update with additional information as it surfaces. Keep driving the awakening.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America