Posted originally on the conservative tree house May 7, 2021 | Sundance | 157 Comments

This obtuse explanation from Treasury Secretary Janet Yellen about the April jobs report is one for the record books. According to Yellen, the government handing people more free money than they would achieve with a working job is not a disincentive for employment.

To prove her case she cites the hospitality industry hiring people in April. However, what Yellen doesn’t figure into her bizarro logic is that all sectors in all states are not created equal. Yes, the statistics of “sector analysis” apply across the entire nation; however, the underlying economic activity is not equally distributed.

Blue states are more economically closed than red states. The job gains are in the states where the economic activity is strongest and the incentives for workers are the biggest. The lack of people working is disproportionately happening in the blue states where dependency models are strongest. WATCH this nonsense:

These bureaucrats don’t have a lick of common sense. According to Secretary Yellen’s logic, there are times when water is not lacking dryness.

Posted originally on the conservative tree house April 30, 2021 | Sundance | 116 Comments

The federal reserve has announced they will support the economic agenda of the Biden administration by allowing rapid inflation. The FED is trying to provide cover for JoeBama’s economic plan. The era when the FED could impact inflation is long past. However, the Joe Biden policy impact will be clear, immediate and concise. The U.S. middle-class and blue-collar worker are about to be crushed under rising prices for consumable products.

Increases in inflation hit the working class (Main St) much harder than the investment class (Wall St) and financial elites. Factually the multinationals benefit from U.S. inflation as it puts pressure on domestic companies to ship their manufacturing overseas. Wall Street likes that. This dynamic has been an issue not-discussed by the financial media for decades. First, the Reuters article (when you see “commodity prices” think about the term “consumables”):

REUTERS – The U.S. Federal Reserve has signaled it will tolerate faster inflation for a time to cement the post-pandemic recovery and boost employment, but the side effect is likely to be a faster rise in commodity prices.

[…] After its latest meeting on Wednesday, the Federal Open Market Committee confirmed it will seek to achieve the *twin objectives of maximum employment and inflation at the rate of 2% over the longer run.

[*NOTE: in the new era of global economics these two are mutually exclusive. The FED is intentionally ignoring this point.]

[…] The committee noted price rises have been running persistently below target, so it aims to achieve inflation moderately above 2% for some time to make up the shortfall and anchor expectations at around the 2% level.

[…] The plan is to run the economy hot to achieve faster job gains, especially among disadvantaged groups that are marginally attached to the labour force, before shifting back to inflation control later in the cycle.

But the resulting pressure on global supply chains while the Fed pursues employment increases is likely to generate significantly quicker price rises for raw materials and a range of manufactured items. (read more)

This perspective is fundamentally false and based on assumptions that are decades old economic arguments. The reality of what will happen is exactly the opposite on the employment front.

The JoeBama administration is attempting to hide their economic program behind the smokescreen of a COVID economic bound; but the reality of what will happen is exactly the opposite. Employment is going to drop far below pre-COVID numbers.

The problem that people do not understand, and the federal reserve will intentionally not consider, is that Macro Economic principles no longer apply in the era of global economics and multinational trade. I have outlined this dynamic for years. What did Trump see that politicians were intent on hiding?

WHAT WAS THE PROBLEM?

Traditional economic principles have revolved around the Macro and Micro with interventionist influences driven by GDP (Gross Domestic Product, or total economic output), interest rates, inflation rates and federally controlled monetary policy designed to steer the broad economic outcomes.

Additionally, in large measure, the various data points which underline macro principles are two dimensional. As the X-Axis goes thus, the Y-Axis responds accordingly… and so it goes…. and so it has historically gone.

Traditional monetary policy centered upon a belief of cause and effect: (ex.1) If inflation grows, it can be reduced by rising interest rates. Or, (ex.2) as GDP shrinks, it too can be affected by decreases in interest rates to stimulate investment/production etc. However, against the backdrop of economic Globalism -vs- economic Americanism, CTH is noting the two dimensional economic approach is no longer a relevant model. There is another economic dimension, a third dimension. An undiscovered depth or distance between the “X” and the “Y”.

I believe it is critical to understand this new dimension in order to understand Trump’s MAGAnomic principles, and the subsequent “America-First” economy he was building.

As the distance between the X and Y increases over time, the affect detaches – slowly and almost invisibly. I believe understanding this hidden distance perspective will reconcile many of the current economic contractions. I also predict this third dimension will eventually be discovered/admitted, and will be extremely consequential in the coming decade.

To understand the basic theory, allow me to introduce a visual image to assist comprehension. Think about the two economies, Wall Street (paper or false economy) and Main Street (real or traditional economy) as two parallel roads or tracks. Think of Wall Street as one train engine and Main Street as another.

The Metaphor – Several decades ago, 1980-ish, our two economic engines started out in South Florida with the Wall Street economy on I-95 the East Coast, and the Main Street economy on I-75 the West Coast. The distance between them less than 100 miles.

As each economy heads North, over time the distance between them grows. As they cross the Florida State line Wall Street’s engine (I-95) is now 200 miles from Main Street’s engine (traveling I-75).

As we have discussed – the legislative outcomes, along with the monetary policy therein, follows the economic engine carrying the greatest political influence. Our historic result is monetary policy followed the Wall Street engine. THIS PART IS CRITICAL:

[…] there had to be a point where the value of the second economy (Wall Street) surpassed the value of the first economy (Main Street). [This important acceptance is just common sense. The U.S. GDP is currently around $20 trillion, but the total valuation of the Wall Street stock market is much larger than our GDP. Wall Street is more valuable than Main Street. It is a simple albeit important reality to accept.]

Investments, and the bets therein, needed to expand outside of the USA. Hence, globalist investing.

However, a second more consequential aspect happened simultaneously. The politicians became more valuable to the Wall Street team than the Main Street team; and Wall Street had deeper pockets because their economy was now larger.

As a consequence Wall Street started funding political candidates and asking for legislation that benefited their interests.

When Main Street was purchasing the legislative influence the outcomes were beneficial to Main Street, and by direct attachment those outcomes also benefited the average American inside the real economy.

When Wall Street began purchasing the legislative influence, the outcomes therein became beneficial to Wall Street. Those benefits are detached from improving the livelihoods of main street Americans because the benefits are “global” needs. Global financial interests, investment interests, are now the primary filter through which the DC legislative outcomes are considered.

Here is an example of the resulting impact as felt by consumers:

♦ TWO ECONOMIES – Time continues to pass as each economy heads North.

Economic Globalism expands. Wall Street’s false (paper) economy becomes the far greater economy. Federal fiscal policy follows and fuels the larger economy. In turn the Wall Street benefactors pay back the politicians.

Economic Nationalism shrinks. Main Street’s real (traditional) economy shrinks. Domestic manufacturing drops. Jobs are off-shored. Main Street companies try to offset the shrinking economy with increased productivity (the fuel). Wages stagnate.

Now it’s 1990 – The Wall Street economic engine (traveling I-95) reaches Northern North Carolina. However, it’s now 500 miles away from Main Street’s engine (traveling I-75). The Appalachian range is the geographic wedge creating the natural divide (a metaphor for ‘trickle down’).

By the time the decade of 2000 arrives – Wall Street’s well fueled engine, and the accompanying DC legislative attention, influence and monetary policy, has reached Philadelphia.

However, Main Street’s engine is in Ohio (they’re now 700 miles apart) and almost out of fuel; there simply is no more productivity to squeeze.

From that moment in time, and from that geographic location, all forward travel is now only going to push the two economies further apart. I-95 now heads North East, and I-75 heads due North through Michigan. The distance between these engines is going to grow much more significantly now with each passing mile/month….

However, and this is a key reference point, if you are judging their advancing progress from a globalist vessel (filled with traditional academic economists) in the mid-Atlantic, both economies (both engines) would seem to be essentially in the same place based on their latitude.

From a two-dimensional linear perspective you cannot tell the distance between them.

It is within this distance between the two economies, which grew over time, where a new economic dimension has been created and is not getting attention. It is critical to understand the detachment.

Within this three dimensional detachment you understand why Near-Zero interest rates no longer drive an expansion of the GDP. The Main Street economic engine is just too far away to gain any substantive benefit.

Despite their domestic origin in NY/DC, traditional fiscal policies (over time) have focused exclusively on the Wall Street, Globalist economy. The Wall Street Economic engine was simply seen as the only economy that would survive. The Main Street engine was viewed by DC, and those who assemble the legislative priorities therein, as a dying engine, lacking fuel, and destined to be service driven only….

Within the new 3rd economic dimension, the distance between Wall Street and Main Street economic engines, you will find the data to reconcile years of odd economic detachment.

Here’s where it gets really interesting. Understanding the distance between the real Main Street economic engine and the false Wall Street economic engine will help all of us to understand the scope of the economic inflation lag during the Trump administration. Which, rather remarkably I would add, was a very interesting dynamic.

Trump was in charge… Now think about these engines doing a turn about and beginning a rapid reverse. GDP could, and as we saw did, expand quickly. However, any interest rate hikes (monetary policy) intended to cool down that expansion -fearful of inflation- would take a long time to traverse the divide. That is exactly what happened.

Jerome Powell attempted to block the America First program with interest hikes; however, his efforts were futile because of the distance between the two economic engines. President Trump was focused on assisting Main Street, and Powell’s attempts at impacting Main Street growth couldn’t impact Trump’s program.

During the Trump era we actually imported deflation because China and other nations were attempting to avoid tariff cost increases; so they devalued their currency. The problem for them was that devaluation of their currency not only made their tariffed goods cheaper, it made the non tariff goods cost less. As a result we were importing deflation from around the world.

Inflation on durable goods could not be significant until those nations stopped devaluing their currency. Simultaneously, as international trade agreements were renegotiated the originating nations of those products were forced into the same type of economic detachment described above.

The global manufacturing economies first responded to increases in export costs (tariffs etc.), by devaluing their currency; then they began driving their own productivity higher as an offset, in the same manner American workers went through in the past three decades. The manufacturing enterprise and the financial sector (connected to the consumer) remained focused on the pricing.

♦ Inflation on imported durable goods sold in America, while necessary, was -as we expected- ultimately minimal during this initial period of Trump policy. Predictably, if we stuck with the program inflation would have expanded significantly as time progressed and off-shored manufacturing found less and less ways to be productive. Over time, imported durable good prices would increase – but it was going to come much later; and by that time our own industrial base would be re-established.

♦ Inflation on domestic consumable goods ‘would’ likely rise at a faster pace. However, as we saw U.S. wage rates were respond faster, naturally faster, than any monetary policy because inflation on fast-turn consumable goods became re-coupled to the ability of wage rates to afford them…. and the labor market was on fire. Wages were factually growing faster than inflation during Trump’s term in office.

The economic policy impact lag, caused by the distance between federal monetary action and the domestic Main Street economy, was -under the Trump policy- now working in our favor. That is, in favor of the middle-class. Within the aforementioned distance between “X” and “Y”, a result of three decades traveled by two divergent economic engines, that was our new economic dimension….

What JoeBama 3.0 is proposing now, and what the Federal Reserve just announced they are going to support, is a return to the prior economic model where Wall Street multinationals benefit and the U.S. middle-class is pushed into their intentionally created “service driven economy”.

Inflation on domestic consumable goods (food, fuel, energy) hurts the U.S. middle-class, it does not hurt the multinationals, the elites and Wall Street investors. It takes a long time for inflation to push up wages when the workforce is experiencing lay-offs due to downsizing, outsourcing and expanded imports of multinational products.

But it doesn’t stop there…. If we get too granular, missing the larger picture, it is difficult to understand. However, if we stay at the elevated perspective, understanding leads to awakening. We start to see how the various JoeBama policies intersect.

In generally approximated terms 2020 has delivered a serious financial blow to Main Street businesses.

The COVID-19 lockdowns and shutdowns have led to business in your local community suffering massive losses of income while simultaneously taking on debt directly from lenders or indirectly from government relief efforts. Main Street has been hit hard, some analysts estimate 40 to 50 percent of those service businesses may not recover.

Conversely, the COVID-19 lockdowns and shutdowns have created a massive income benefit for multinationals, Wall Street corporations and big tech. Amazon, Walmart and massive tech companies had their highest earnings ever recorded.

According to most maco-analysis somewhere around forty percent of Main Street economic wealth was lost or suspended in 2020 due to COVID-19. Simultaneously the multinational firms have seen increases in stock evaluations of forty percent. These two almost identical numbers are not coincidental. The billionaire class (multinationals) have gained wealth in an almost identical amount the middle-class (Main Street) lost.

These empirical results are accepted. No-one is challenging the shift of financial resources was/is directly related to regional COVID policy. The math is the math.

Where things change from simple economic math to downstream consequences is where the story is really told.

This is where we are going…

This is where we have been going ever for decades, COVID-19 has (not coincidentally) just sped up the process.

If you take out a national map and: (1) put a green pin in the areas where the lock-downs are most severe (draw a 100 mile circle); then (2) put a red pin in the areas where the riots and local anxiety was highest in summer 2020; then (3) put a white pin in the seven counties where election fraud was prevalent; then (4) put a blue pin in the areas known as “Opportunity Zones“, what you will see is a direct correlation. This is not accidental.

There are more than 8,760 designated Qualified Opportunity Zones (PDF) located in all 50 States, the District of Columbia, and five United States territories. Investors can defer tax on any prior gains invested in a Qualified Opportunity Fund (QOF) until the earlier of the date on which the investment in a QOF is sold or exchanged or until December 31, 2026. (link)

If you are a member of ‘THE BIG CLUB’ with a massive influx in capital due to the benefits of the COVID-19 lockdowns, limits and regulations, the Opportunity Zones are now the perfect place to expand ownership and wealth. Take advantage of the Main Street weakness, make moves with government authorization, and do so without capital gains.

The regions where real property will be purchased at a low cost will, not coincidentally, be the “opportunity zones” where investment transactions without capital gains can be made. The areas where riots took/take place will sell cheap. “Opportunity zones” allow for mass investment moves from billionaire class without paying capital gains taxes.

The mass accumulation of wealth (multinationals) at the upper tier of Big Tech and the multinational billionaire class (technocrats) during COVID is approximately +40% since it began. 40% of Main Street businesses wiped out. Not coincidentally almost 40% of wealth has been transferred from Main Street to the Wall Street mega-corps and multinationals.

“Never let a crisis go to waste”…

Only in 2020 the “crisis” was (yet again) by design. The highest level of COVID mitigation control in the Blue states is not coincidentally in the same states with the largest number of Opportunity Zone regions. As a direct result of this mass transfer of wealth to the upper tier the “opportunity” is an unprecedented level of Main Street ownership by elite interests and foreign nationals.

It gets worse… Just like the banking and real-estate crisis of ’07/’08 the government steps in to back-fill the Main Street losses to the mass U.S. population. When an individual or family receives the relief money, they still cannot support Main Street because in many areas they remained forcibly closed. Paying down debt and making purchases in the same lock-down strata only ends up putting those relief funds into the hands of the banks and multinationals who were allowed to operate.

Continued consumer spending only feeds the beast that is -by policy via purchased politicians- designed to destroy us. In essence, we are paying the Technocrats, bankers and multinational corporations to fatten their bank accounts while the U.S. government re-opens the economy with a finger on the scale to benefit the multinationals.

This is by design….

This has always been the design…

CTH has been warning about this for well over a decade and we exhibited the (un)natural conclusion with this graphic:

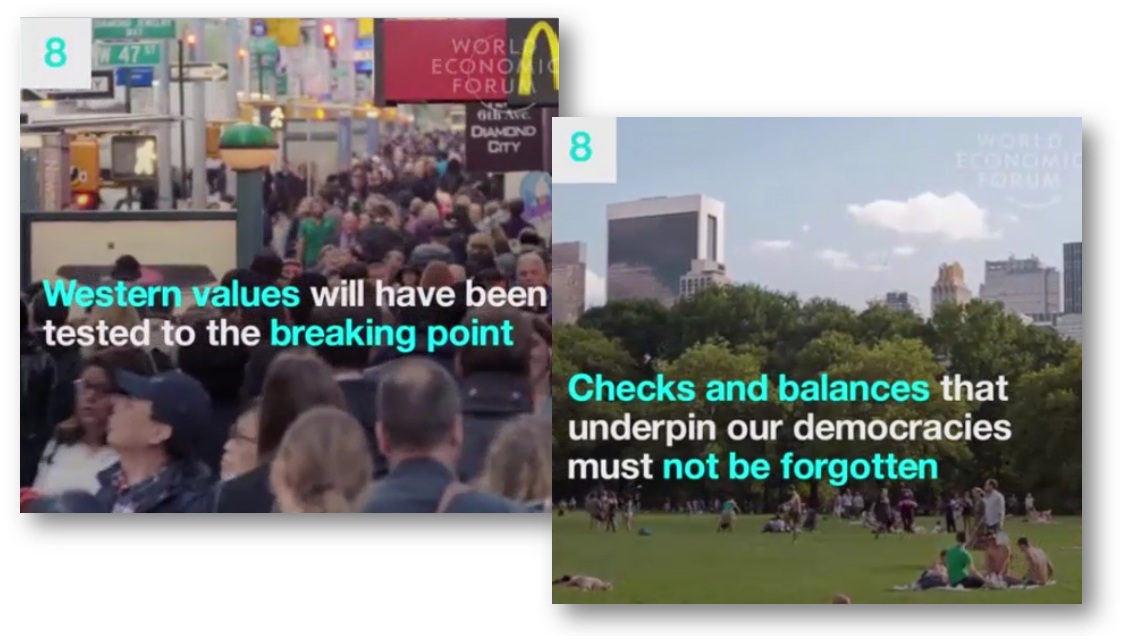

The proposal is to create a global tax rate as world leaders move to create a one-world government. The United Nations, behind the curtain, is preaching that ONLY they can solve the world crisis in climate change, for it requires a single government to control the world. On top of that, Bill Gates has taken over the funding for studies by Ivermectin & Fluvoxamine Clinical Trial Targeting COVID-19. We can bet that given his monopoly over vaccines, taking over the funding of studies to show an alternative to vaccines will by no means be legitimate. The conflicts of interest are vast.

As I have warned, they desperately needed to remove Trump from office because they viewed him as an outsider and someone elected by “populism,” which threatened the world establishment of political control by elite career politicians. They are now moving in high gear to eliminate democracy by 2022, but certainly, their goal is by 2024.

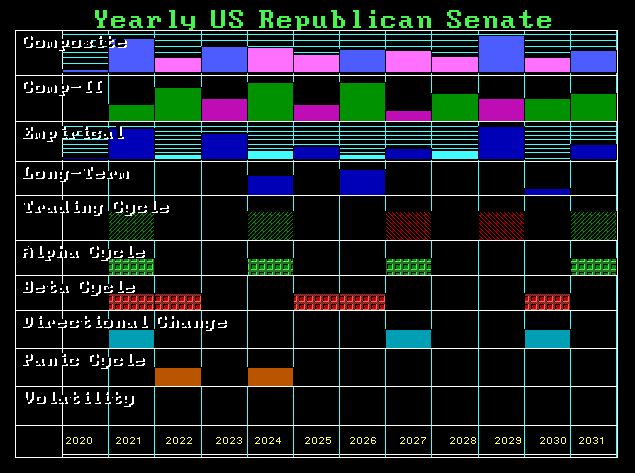

As I have warned, our models of politics have NEVER shown Panic Cycles since the 1930s. It appears that some states are trying to fight back where the Democrats want mail-in ballots that are not secure and same-day registration to vote to ensure there can be no verification of who the people even are. The Supreme Court has abandoned its role to protect our constitution by refusing to hear any of the cases, which may not have overturned the election but would have dealt with changing the rules as they went.

People have no idea what is at stake. These people in power want ABSOLUTE control, and they never want another popular person to run for office anywhere that would dare to threaten their goal of eliminating democracy. Then they want worldwide taxation, and this has been the goal of the United Nations. They argued that climate change could not be combated by a single country. It will take a one-world government, UNELECTED, of course, to rule the world and make regulations that dictate everything right down to what you can and cannot do in your home.

The Democrats are out to end saving and passing on something for your children. I am sure those who voted for Biden simply because they hated Trump will find out what the real agenda is fairly soon. It might simply be a good time to die right now because the Democrats tear up everything that made America the land of opportunity.

The one thing that I would have to agree with Karl Marx on was his version of the “rich” in England was all about preventing the lower classes from ever obtaining wealth. You would take a house and basically pay full value, but it was for a 100-year lease, the way the Brits did in Hong Kong. The 100 years pass, and the property reverts to the historical owners. It was known as a “long lease.” The term “freehold” meant that it was a property you and your family could actually own.

The Democrats are back to the same philosophy of the old aristocratic families of England. Instead of the aristocratic families retaining the title, the Democrats want whatever wealth you have earned and saved to make your family well established to revert to the state. People fled Europe and came to America so they could actually own the property outright. The Financial Panic of 1792 inspired Ben Franklin to say, “In this world nothing can be certain, except death and taxes.”

Many people have criticized my solution that the government should be prohibited from borrowing and it should simply create money to cover its expenses each year capped at 5% of GDP — all federal taxes should be abolished. State and local taxes would still exist since they cannot create money. But they too should be prohibited from borrowing.

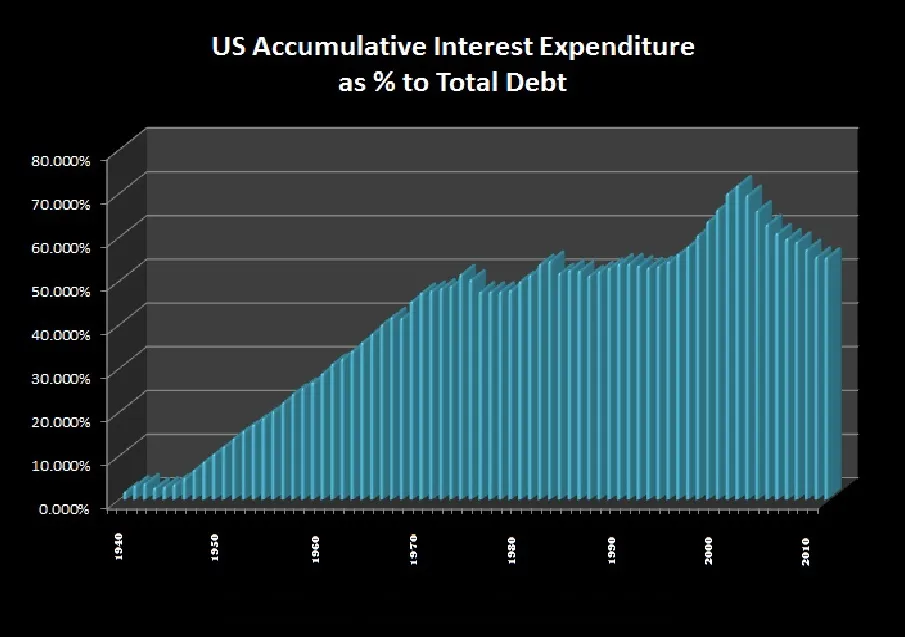

My critics will argue this will be inflationary. My point is that would be a dramatic improvement over the current system and eliminating federal debt means that the capital will be redirected into the private sector, creating far more economic growth. Politicians are incapable of managing the economy and should be prohibited from attempting anything. At times, up to 70% of the national debt is accumulated interest expenditures because they borrow year after year with NO intention of paying anything back.

Biden will not destroy the economy because he is spending recklessly, and then argues we must raise taxes to pay for this spending. Yet, the government will never pay for everything because they need to reduce the debt.

So, my solution would have kept your family and their future. Under the Democrats, they are wiping out the future of your family. We are returning to the days where private wealth is not something they will tolerate.

Remember one thing — 99% of all revolutions are created because of taxes! NO TAXATION WITHOUT REPRESENTATION!

COMMENT: Well it looks like the coronavirus is going to cause a major problem because everyone will be deducting their home offices.

HL

ANSWER: You better check with your accountant. It is my understanding that if you are a W2 employee, you cannot take a home office deduction. Currently, you need to have self-employment income to benefit from home office deduction. This is going to cause real problems now that so many people are forced to work remotely. I seriously doubt the Democrats will allow a deduction for working remotely.

Your post today on inflation(when people see it coming) reminds me how things have changed from the 1970s. Then, the inflation we saw came from oil rising(Opec raising prices), unions demanding wage increases, and currencies untethered to the abandoned Bretton Woods agreement. Governments then seemed clueless how to stem this rise, with interest rates rising relentlessly, pressuring bonds and eroding earnings of still largely manufacturing-based economies. Globalization was not an issue as half the world still lived under communism.

Today, it seems central banks have “learned” how to rig interest rates by flooding markets addicted to debt. What is different today is governments now, instead of fearing inflation, actually want it. In fact, desire it to bring about the Great Reset. They appear to want to drive oil prices higher to such levels that this makes Green Energy cheaper and helps to accelerate the conversion over to electric cars. All at the expense of the consumer. On top of this, taxing old tech, principally oil and gas, only helps to fuel shortages, since companies have cut back on oil exploration. When you force people to stay home, the demand for energy shifts from driving to people staying home, more demand for computers, more energy required to supply the grid, more companies delivering products to the home. What has been accomplished? People fleeing high tax states to ones that remain open, those with no state income taxes, those in the south. The burden shifts to northern states, the advantage gained by southern states.

Today, governments are deliberately fueling these shortages…encouraging them, to expedite the transition away from globalization to one centrally controlled. No longer do they need access to debt markets, they can supply guaranteed income without fear of inflation or failed bond auctions. This is truly diabolical. And with Big Tech doing their bidding, people too stupid to grasp what is happening, it appears today’s inflation is by design, intended to destroy a private business, which can’t compete with large companies, jobs destroyed, inflation today used as a weapon against private enterprise. This is pure evil, which stands out against the market-based inflation of the 1970s.

MS

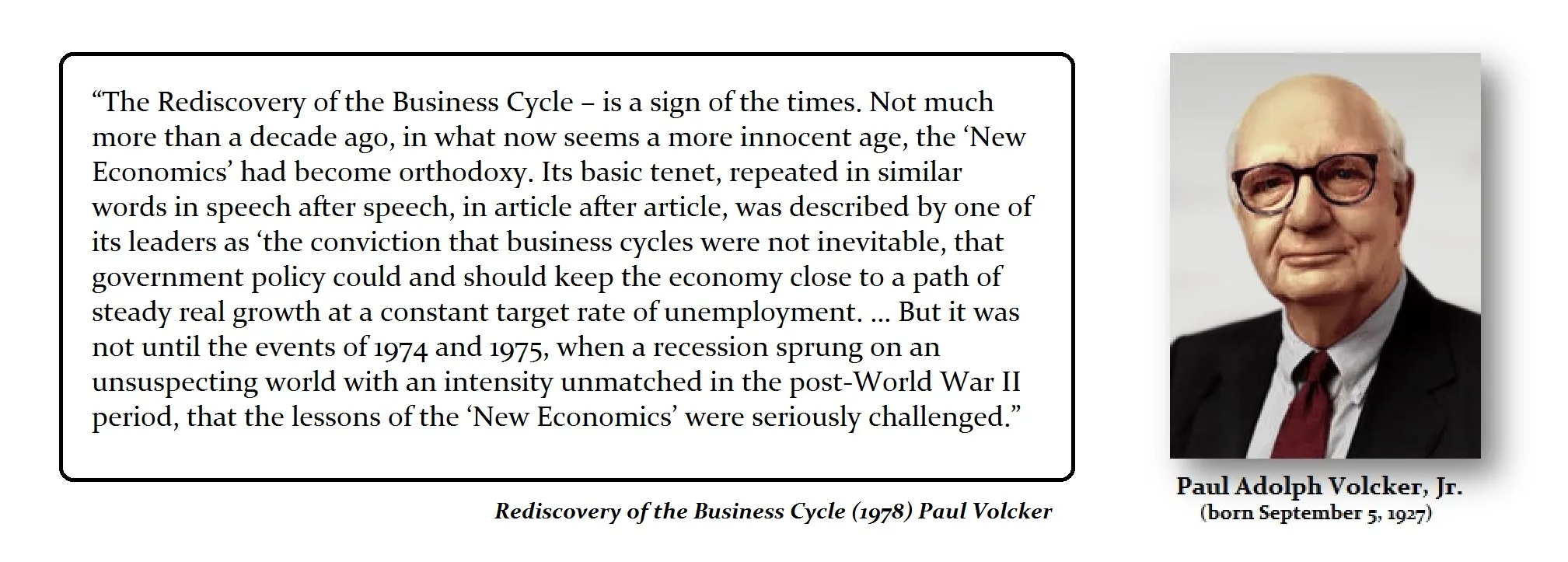

REPLY: You are correct that it was a period of unions demanding more, but it was more than just that aspect. There were two other major developments. First, there were rising prices with lower economic growth. This became known as STAGFLATION. This took place because COSTS were rising from an external price shock that rippled through the economy, which was created at the same time as an economic recession. That never took place before because previous recessions were entirely confined domestically, so prices declined with lower demand.

It was more than simply the collapse of Bretton Woods. It was the in-your-face collapse of Keynesian economics. Still, it was Paul Volcker who followed Keynesianism and raised interest rates into 1981 simply because he had no other theory available. I had a conversation with Volcker at the IMF Dinner in Washington. I did not bash him over his head with his mistake, he was so tall it would have been hard to do so, but we did have a frank discussion of the changes in the global economy.

Today, the central banks are still trapped by the same Keynesian economic theories. Now, they have painted themselves into a corner with artificially low interest rates that they cannot escape without a drastic alteration to the debt markets as a whole. Volcker could at least correct his mistake by lowering interest rates. Today, the central banks cannot raise rates without blowing up their own portfolios. It is a very different type of crisis they face today than what it was during the 1970s.

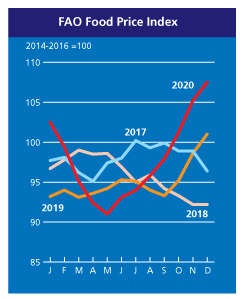

We are staring in the face of a serious food crisis in Europe as food prices rise continuously, and with further draconian COVID measures within the EU, they are bringing the food supply chains to a standstill. Our models have been warned that this 8.6-year cyclical wave into 2024 will be one of commodity inflation due to SHORTAGES rather than speculative demand. All the indications that the world is heading for a serious food price crisis are in play. The Food Price Index (FFPI) of the Food and Agriculture Organization of the United Nations (FAO) averaged 107.5 points in December 2020, an increase of 2.3 points (2.2%) compared to November 2020, which represents an increase for the seventh consecutive month.

With the exception of sugar, all sub-indices of the FFPI recorded slight gains in December, with the sub-index for vegetable oil again rising the most, followed by that for dairy products, meat, and cereals. For 2020 as a whole, the FFPI averaged 97.9 points, a three-year high, 2.9 points (3.1%) higher than in 2019, but still well below its 2011 high of 131.9 points. It is also interesting that the FFPI in 2002 was still 53.1 points. It only increased significantly from the financial crisis of 2007/08, only to then level off in the 90-point range. Since May 2020 it has increased by 18%.

Our models project that the upward trend in the FFPI will intensify going into 2024. With the coronavirus mutating, as we warned ALL viruses do, as such, we have these various strains from Africa, Brazil, UK, and even California, are inspiring politicians to use this as an opportunity to restrict the population even further. These corona measures have extended to the food supply chains, disrupting them just as we see in electronics. For example, the German Fruit Trade Association sees the supply of fruit and vegetables from abroad is at a substantial risk whereby imports are suspended. The reason is the tightening of the corona entry regulation by the federal government. The tightening of the lockdown in Europe is beginning to restrict the supply chains reducing the food supply

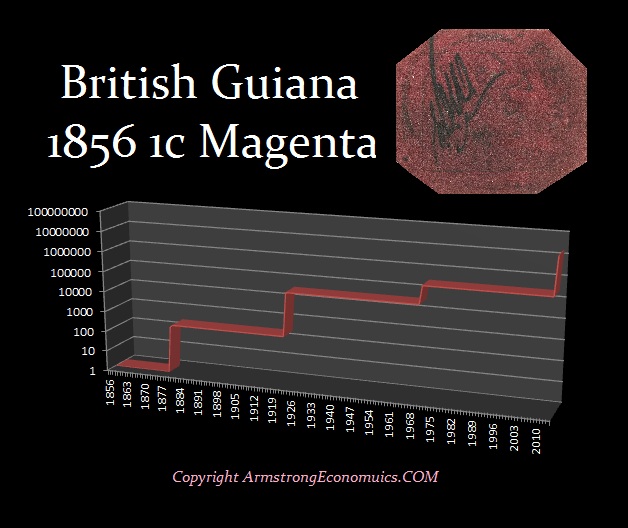

This June, Sotheby’s will be auctioning off three of the greatest rarities in the stamp and coin field. The 1933 Double Eagle $20 gold coin, the unique British Guiana One-Cent Black on Magenta, and the unique Inverted Jenny 1918 Plate Block. This is truly an incredible offering from a single collector to have captured three of the rarest and most unique collectibles in history.

It is a bit unusual that a unique stamp from a less than the mainstream region has emerged as the rarest and sole-surviving example of the British Guiana One-Cent Magenta from 1856. It was last sold in 2014 at Sotheby’s for $9.48 million. While it was rediscovered by a 12-year-old schoolboy living in South America in 1873, perhaps due to fantastic marketing, it has emerged as one of the most important stamps in famous collections that have ever assembled. In 1873 L. Vernon Vaughan, a 12-year-old schoolboy living with his family in British Guiana found the stamp among a group of family papers bearing many British Guiana issues. The young philatelist would later sell the stamp for several shillings to another local collector. The British Guiana then entered the UK in 1878, and shortly after, it was purchased in Paris by Count Philippe la Renotière von Ferrary who many considered to be perhaps the greatest stamp collector in history. Then following the war, France seized Ferrary’s collection, which had been donated to the Postmuseum in Berlin, as part of war reparations due from Germany following World War I. The stamp was then sold in 1922 at auction when it was purchased by Arthur Hind, a textile magnate from New York, for its first auction-record price of $35,000. The stamp changed hands moving from the collections of the Australian engineer Frederick T. Small; then a consortium headed by Irwin Weinberg; then by John du Pont of the famous chemical company. Du Pont paid $935,000 for the stamp in a 1980 auction, before it was last sold at auction to Weitzman for the record-setting price of $9.48 million.

Interestingly, a tradition emerged where previous owners of the British Guiana signed the back of the stamp. Weitzman added his own personal mark to the reverse of the stamp inscribing his initials “SW” along with a line drawing of a stiletto shoe as a nod to his legacy in fashion.

This 1933 Double Eagle ($20 gold coin) is the only example that may be legally owned by an individual. It was the coin acquired by King Farouk of Egypt. Stuart Weitzman purchased the coin at a Sotheby’s/Stack’s auction in 2002 for a world record price of US$7.59 million, nearly doubling the previous record. The Director of the United States Mint signed a Certificate of Monetization that, in return for twenty dollars, authorized the issuance of this single example.

In August 2005, the US Mint announced the recovery of ten additional stolen 1933 double eagle gold coins from the family of Philadelphia jeweler/coin dealer Israel Switt, who was the illicit coin dealer identified by the Secret Service as a party to the theft who admitted selling the first nine double eagles that were recovered. Israel Switt had many contacts and friends within the Philadelphia Mint. As the story goes, the Secret Service found that only one man, George McCann, had access to the coins at the time and served prison time for similar embezzlement in 1940. Israel Switt somehow obtained the stolen 1933 double eagles. One theory is that McCann swapped the previous year’s Double Eagles for the 1933 specimens prior to melting, thereby making sure the count was correct. The US mint began striking Double Eagles on March 15, 1933. Roosevelt’s executive order to ban gold was not finalized until April 5. Therefore, on March 6, 1933, the Secretary of the Treasury ordered the Director of the Mint to pay gold only under a license issued by the Secretary, and the United States Mint cashier’s daily statements do not reflect that any 1933 Double Eagles were paid out.

In September 2004, the claimed owner, Joan Switt Langbord, heir to Israel Swift, tried to sell the 10 coins and they had to be surrendered to the Secret Service. In July 2005, the coins were authenticated by the United States Mint after working with the Smithsonian Institution, as being genuine 1933 double eagles. Joan Switt Langbord claimed to have found them in a box and she went to court to have them returned. On October 28, 2010, US court ruled and the issue went to trial in July 2011. On July 20, 2011, after a ten-day trial, a jury ruled unanimously in favor of the United States government and Lanford appealed. At first, the Court of Appeals overruled the jury, but then it went En Banc and the Court of Appeals ruled in favor of the government. The Langbords appealed to the U.S. Supreme Court, which on April 17th, 2017 denied certiorari.

Hetty Green’s son, Edward Howland Robinson Green (1868-1936), was not so frugal and spent $3 million on coins and stamps. He was an avid collector and bought the famous sheet of 100 inverted airmail stamps in 1918, paying $20,000. The last time this Plate Block appeared on the market was 16 years ago when it sold at auction for $2.97 million.

Meanwhile, the classic Ferraris from the 1980s have nearly doubled in price over the past year.

COMMENT: Dear Mr Armstrong, I wanted to write in to affirm your observation of regular people buying now rather than waiting (The Bull v Bear in the US Markets). I had to buy a new dryer earlier in the year. It took 6 weeks to get the one I had ordered. I wanted to buy a new computer recently. Lenovo showed delivery in 12 weeks for the one I wanted! Another company I looked at was taking pre-orders for delivery beginning the end of May. I paid a little extra and went with a small manufacturer that could deliver within 10 business days. I bought an extra freezer so we can stock up. I actually tried to buy a freezer last year and couldn’t get one at all, so I snapped one up as soon as they were available back in January. My wife just asked me if I wanted to get a new grill for Father’s Day. I said, ‘Let’s buy that right now and put it aside. Who knows what will happen by Father’s Day.’

J

REPLY: I remember the 70s well. Because of OPEC, not just gasoline was rising, but suddenly everything made of plastic was rising. For those who do not know, plastics are made starting with raw materials, such as natural gas, oil, or plants, which are refined into ethane and propane. Ethane and propane are treated with high heat, in a process known as cracking. This is how they’re converted into monomers such as ethylene and propylene. The monomers ethylene and propylene are combined with a catalyst to create a polymer “fluff,” which looks like powdered laundry detergent. Then the polymer is fed into an extruder, where it is melted and fed into a pipe, and the plastic forms a long tube as it cools. So when oil rose in price, so did everything made of plastic. That was much of the inflationary boom between 1976 and 1980.

Everything was rising in price which led to the realization that it was cheap to buy today because it would only cost more tomorrow. I ordered a new refrigerator in December. It finally arrived in March. We are entering a period of shortages so prices will be moving higher as supply is constrained and demand will rise. The other side-effect of lockdowns and the destruction of offices with people working more remotely, everyone is out remodeling or expanding their homes. The construction industry is booming. Just look at the price of lumber.

Welcome to the inflation cycle our computer has been projecting would be built upon shortages

While the general overview of this market by most technicians has been bearish simply based upon how high the market has risen, we are also in an interesting position where the fiction of vaccines is providing some underlying support. Based upon RELIABLE sources, this entire Build Back Better motto and a scheme were developed BEFORE COVID took place. This virus has been one of convenience and I know people were warned to sell stocks and bonds because a virus was coming and that was Jan/Feb 2020. That leaves only two possibilities.

(1) This is really the Fauci virus since this was the precise research he was doing and was told to shut down so he sent it to Wuhan

(2) They knew a natural virus would appear seasonally and they would exploit it as extremely dangerous

While Europe is still trying to push the Great Reset and destroy as much of the economy as possible that is reliant upon fossil fuels, there is no question that this virus has been greatly exploited and exaggerated for political purposes. In the United States, because the power has resided with state governors, it has been more difficult to accomplish the economic contract that we see in Europe especially in Britain where Boris Johnson is in bed with Bill Gates.

Consequently, the US will not see the economic devastation that we are witnessing in Europe because Trump was in charge and made no effort to lockdown the entire country. Additionally, politics is so corrupt they rely on corporate donations and they have been getting a lot of resistance. On the private blog, I warned that the Biden Administration, according to reliable sources, was looking at putting a tax per mile that you drive in addition to the gasoline tax. That would create an army of new government employees and a nightmare of enforcement.

That all said, the real impact of all of this nonsense has been to seriously disrupt the supply chain in everything from food to electrical appliances. These shortages have already led to rising prices and consumers are starting to realize that it may be cheaper to buy today because whatever it is will be more expensive tomorrow. That is the REAL stimulus to inflation – not the increase in money supply which has been exponential since the 2007-2009 Financial Crisis with no inflationary impact. As long as the consumer does not trust the future, then they hoard their cash. Inflation emerges ONLY when they see that it is no longer beneficial to hoard their cash. That is the psychology we are now entering.

While our near-term target in the Dow Jones Industrials remains in the 36,000-37,000 range, we are still in a position to test the 40,000 number on a broader-term. What you must keep in mind are the capital flows. Because we had Trump, that one year of refusing to join this Build-Back-Better agenda was critical in keeping the US economy much stronger compared to Europe, yet neck & neck with China, which will put in a stronger growth pattern number in 2021. The Dow has been making new record highs which the NASDAQ peaked in February on target with our timing models. This disparity is reflecting the international capital flows for foreign money always go for the blue-chips.

To see the future, we must look at the entire world. Analyzing a single market based upon what comment the Fed will make tomorrow is for amateurs. We live in a global economy and it is time we open our eyes to the real world that surrounds us.

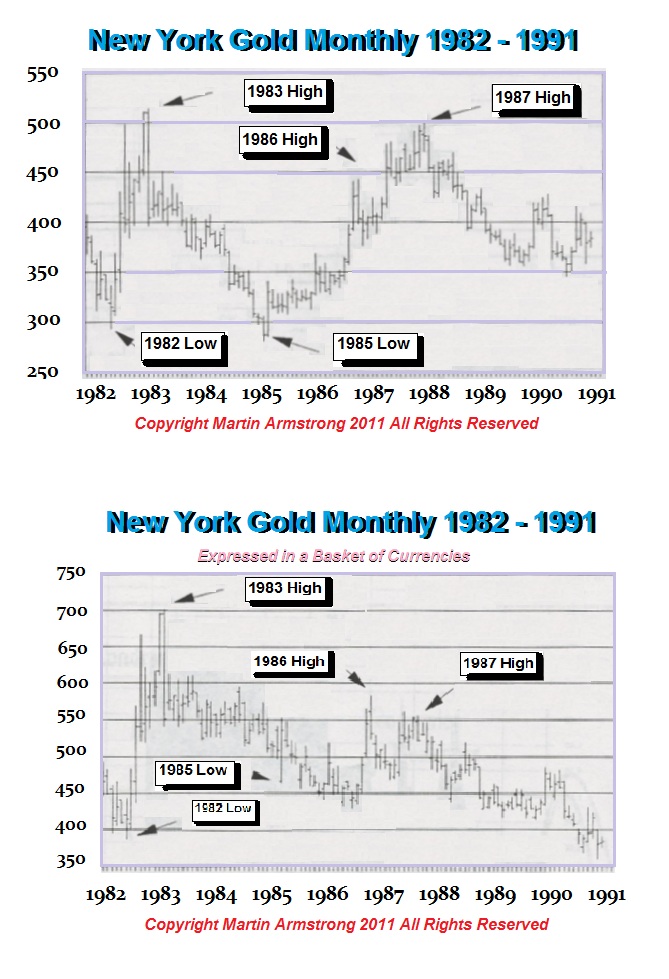

It has always been critical to look at everything from a global perspective. Gold declined for 19 years from 1980 into 1999 and the domestic analysis was always wrong. They looked at gold only in dollars. Yet when we looked at gold in a basket of currencies, what looked like a bull market in dollars was really a bear market in world currencies. This is why Socrates looks at everything in all currencies – not just domestic.

Those that keep calling to the collapse of the dollar because of debt have not bothered to look outside the United States. The US sovereign debt is about $28 trillion out of nearly $59 trillion globally. However, add in state and local government with private debt, as we are approaching $300 trillion. This is why US federal debt is still the golden parachute in the world and the fact that US long-term rates are not being manipulated as they are in Europe only offers a greater incentive for capital inflows. We are witnessing US rates rising and this will further attract international capital in the face of the US economy doing far better than Europe.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America