Posted originally on Mar 29, 2024 By Martin Armstrong

The quoted banker does not specifically talk about the Central Bank Digital Currency that lays at the end of the promoted rainbow; the author does. However, the banker does outline a familiar step in the current process. As a result, it is worth drawing attention to the continuum.

MAINE – “According to Hannigan, the COVID-19 pandemic forced businesses to implement “paper-free and virtual processes” to handle their finances while “adapting to the new reality.

“For years, Americans had been slowly moving away from cash and paper checks, but the pandemic supercharged the trend,” Hannigan wrote. “By last year, 41% said they never use cash for purchases, up from 24% in 2015, according to the Pew Research Center. Only 14% still exclusively use cash and checks.” (Read More)

There is a BIG difference between electronic funds (current), and a digital dollar (future).

In 1996, the US government released a white paper entitled, “How to make a mint: the cryptography of anonymous electronic cash.” Released by the National Security Agency Office of Information Security Research and Technology, this document basically explains how a government agency could create something like Bitcoin or another cryptocurrency.

I encourage those interested to read the contents of the link above. This document was released during the dawn of the dot.com bubble before the technology existed to create such a currency. The NSA quickly realized that it could weaponize this technology to create a cashless society.

As explained in the introduction:

“Among the most important uses of this technology is electronic commerce: performing financial transactions via electronic information exchanged over telecommunications lines. A key requirement for electronic commerce is the development of secure and efficient electronic payment systems. The need for security is highlighted by the rise of the Internet, which promises to be a leading medium for future electronic commerce. Electronic payment systems come in many forms including digital checks, debit cards, credit cards, and stored value cards. The usual security features for such systems are privacy (protection from eavesdropping), authenticity (provides user identification and message integrity), and nonrepudiation (prevention of later denying having performed a transaction) . The type of electronic payment system focused on in this paper is electronic cash. As the name implies, electronic cash is an attempt to construct an electronic payment system modelled after our paper cash system. Paper cash has such features as being: portable (easily carried), recognizable (as legal tender) hence readily acceptable, transferable (without involvement of the financial network), untraceable (no record of where money is spent), anonymous (no record of who spent the money) and has the ability to make "change." The designers of electronic cash focused on preserving the features of untraceability and anonymity. Thus, electronic cash is defined to be an electronic payment system that provides, in addition to the above security features, the properties of user anonymity and payment untraceability.. In general, electronic cash schemes achieve these security goals via digital signatures. They can be considered the digital analog to a handwritten signature. Digital signatures are based on public key cryptography. In such a cryptosystem, each user has a secret key and a public key. The secret key is used to create a digital signature and the public key is needed to verify the digital signature. To tell who has signed the information (also called the message), one must be certain one knows who owns a given public key. This is the problem of key management, and its solution requires some kind of authentication infrastructure. In addition, the system must have adequate network and physical security to safeguard the secrecy of the secret keys.”

The introduction goes on to discuss the reasons they could present to the public to switch to a cashless society, including money laundering, convenience, and security. “The term electronic commerce refers to any financial transaction involving the electronic transmission of information. The packets of information being transmitted are commonly called electronic tokens,” the paper continues.

The NSA states that it would like to use “user identification” and “message integrity” to protect privacy in “nonrepudiation” transactions. “Eavesdropping” concerns appear numerous times throughout the document, which could be prevented by “not just privacy but anonymity” in the form of “payer anonymity” and “payment untraceability.” The government clearly states that hard currency, cash, provided these luxuries but could not be traced by the banks and, therefore, the government.

Again, this was released in 1996 before basic online banking. The document outlines basic online banking but takes it a step further by explaining how they could seemingly make payments seem “untraceable” to the public using “blind signatures” that allegedly cannot be seen by the bank. “This step is called “blinding” the coin, and the random quantity is called the blinding factor. The Bank signs this random-looking text, and the user removes the blinding factor.”

PROTOCOL 3: Untraceable On-line electronic payment.

Withdrawal:

Payment/Deposit:

“This makes remote transactions using electronic cash totally anonymous: no one knows where Alice spends her money and who pays her.” Full “payment anonymity” would be “too much to ask”, thus, “we are forced to settle for payer anonymity.” In other words, the illusion that no one knows who is making the transaction.

PROTOCOL 5: Off-line cash.

Withdrawal:

Payment:

Deposit:

Note that, in this protocol, Bob must verify the Bank’s signature before giving Alice the merchandise. In this way, Bob can be sure that either he will be paid or he will learn Alice’s identity as a multiple spender.

The government begins to explain basic blockchain concepts, or at least how they’d like them to occur.

“When Alice spends her coins with Bob, his challenge to her is a string of K random bits. For each bit, Alice sends the appropriate piece of the corresponding pair. For example, if the bit string starts 0110. . ., then Alice sends the first piece of the first pair, the second piece of the second pair, the second piece of the third pair, the first piece of the fourth pair, etc. When Bob deposits the coin at the Bank, he sends on these K pieces. If Alice re-spends her coin, she is challenged a second time. Since each challenge is a random bit string, the new challenge is bound to disagree with the old one in at least one bit. Thus Alice will have to reveal the other piece of the corresponding pair. When the Bank receives the coin a second time, it takes the two pieces and combines them to reveal Alice's identity… Zero-Knowledge Proofs. The term zero-knowledge proof refers to any protocol in public-key cryptography that proves knowledge of some quantity without revealing it (or making it any easier to find it). In this case, Alice creates a key pair such that the secret key points to her identity. (This is done in such a way the Bank can check via the public key that the secret key in fact reveals her identity, despite the blinding.) In the payment protocol, she gives Bob the public key as part of the electronic coin. She then proves to Bob via a zero-knowledge proof that she possesses the corresponding secret key. If she responds to two distinct challenges, the identifying information can be put together to reveal the secret key and so her identity.” The document then discusses ways to blind the signature, so that the payee may remain anonymous. Now, why would the government allow that to occur? “Even in anonymous, untraceable payment schemes, the identity of the multiple-spender can be revealed when the abuse is detected. Detection after the fact may be enough to discourage multiple spending in most cases, but it will not solve the problem. If someone were able to obtain an account under a false identity, or were willing to disappear after re-spending a large sum of money, they could successfully cheat the system.”

The document even discusses what we now would refer to as a crypto wallet. A seemingly safe offline method to store these electronic coins. They explain that at least one party must always reveal their hand. “When a coin is spent, the spender uses his secret to create a valid response to a challenge from the payee. The payee will verify the response before accepting the payment. In Brands’ scheme with wallet observers, this user secret is shared between the user and his observer. The combined secret is a modular sum of the two shares, so one share of the secret reveals no information about the combined secret.”

Who is the “observer” in this scenario? “An observer could also be used to trace the user’s transactions at a later time, since it can keep a record of all transactions in which it participates. However, this requires that the Bank (or whoever is doing the tracing) must be able to obtain the observer and analyze it. Also, not all types of observers can be used to trace transactions.”

In the event that a transaction was compromised, the bank would have to change its secret key and “INVALIDATE ALL COINS.”

The authors explain that tax evasion, per usual, is the key concern. They mention money laundering and “old crimes such as kidnapping and blackmail” as reasons to allow backdoor entry. Restoring traceability was a proposed solution, and if they could restore traceability in the first place, one must question if the payments were ever truly anonymous. Using Alice as their example, they explain that they could simply issue a warrant and track all her payment history. “Back~ard traceability is the ability to identify a withdrawal record (and hence the payer), given a deposit record (and hence the identity of the payee). Backward tracing will reveal who Alice has been receiving payments from.”

So, while the bank only sees the deposit in encrypted form, the public key must be used for withdrawal. “The ability to trace transactions in either direction can help law enforcement officials catch tax evaders and money launderers by revealing who has paid or has been paid by the suspected criminal. Electronic blackmailers can be caught because the deposit numbers of the victim’s ill-gotten coins could be decrypted, identifying the blackmailer when the money is deposited.”

“In conclusion, the potential risks in electronic commerce are magnified when anonymity is present. Anonymity creates the potential for large sums of counterfeit money to go undetected by preventing the identification of forged coins. Anonymity also provides an avenue for laundering money and evading taxes that is difficult to combat without resorting to escrow mechanisms. Anonymity can be provided at varying levels, but increasing the level of anonymity also increases the potential damages. It is necessary to weigh the need for anonymity with these concerns. It may well be concluded that these problems are best avoided by using a secure electronic payment system that provides privacy, but not anonymity.”

The US government released this document in 1996, 27 years ago. Bitcoin was allegedly anonymously created in 2009, and numerous other blockchain-based payment coins have followed. This, paired with the push for CBDC, where the government simply does not need to pretend payments are anonymous, should make one question the security and longevity of cryptocurrencies.

COMMENT: I have investigated what you have said about our Western leaders. From the US to Britain, the Balkans, France, Poland, and Germany, they all want war. I am 77 now. My whole life was about creating peace. I remember Richard Nixon opening China and dividing it from Russia. I believe you are correct. There is no explanation for everyone seeking war other than to hide their appalling government mismanagement.

Thank you for your analysis. It is always unmatched.

GKB

REPLY: History repeats, and human nature never changes. We have the model from Rome, the greatest empire ever created. The Pax Romana was achieved by everyone benefiting in their economic relations. Once these people removed Russia from the SWIFT system, they condemned the United States to its demise. The rise of the BRICS has nothing to do with fiat money. All money has always been fiat. From ancient times, we find imitation coinage of the dominant economy being created by other regions, showing that there was always a premium over the metal content if it was a coin of the dominant economy like the US dollar today. Here is an imitation of an Athenian Owl stuck by the Egyptians, who never had coins until they were conquered nearly 100 years later by Alexander the Great. They issued imitation Athenian Owls because they were the currency of international trade.

Even the Celts, when Julius Caesar conquered Europe, still imitated his coinage. The metal was virtually the same, so it was a counterfeit but an imitation. The Celts still used Roman coinage for their monetary system.

Even 300 years before Caesar, when the Macedonians were the dominant economic power of Phillip II and his son Alexander the Great, we find Celtic imitations of Macedonian gold where they at least tried to imitate the design.

Even after Caesar conquered Europe, we find Germanic imitations of Roman bronze coinage. Once more, they could have created their own coinage but imitated the coinage of Rome.

As trade expanded with India, we find a series of Indian imitations of Roman gold coinage running the course of 300 years. We see Celtic imitations of Roman coinage as well as Germanic coinage, which also ran for about 300 years.

The fact that we have hundreds of years of imitations of the dominant economy PROVES beyond a shadow of a doubt that the coinage was NOT based on the metal content; there was always a premium applied to the dominant currency in the world at that time.

This entire nonsense that the dollar is just a fiat currency is absurd. The value of ANY currency is the strength of its economy. The dollar has been the RESERVE currency BECAUSE everyone wanted to sell their products to American consumers.

The PAX Romana took place BECAUSE all the conquered lands found it was beneficial to be part of the empire, for they could sell their products. World Peace was created by allowing free trade as the Romans did. Then, the people would oppose any local politician preaching war, for it would cut off their income. We were on the verge of world peace before COVID-19, when everyone participated in the world economy. Today, that has all been destroyed. Peace is no longer fashionable – it is hatred and war that now define world leaders.

Gary Cohn appears on Face The Nation to discuss the finance, the economy and the pain felt by consumers. He won’t say it directly, for obvious reasons, but what Cohn describes in terms of political support boils down to Main Street business supporting Donald Trump and Wall Street Multinational Corporations supporting Joe Biden. That is ultimately what is obvious at a macro level.

I’m starting the video at 03:08 for the purposes of emphasizing inflation. What Cohn says about U.S. inflation is essentially accurate and I have a Cliff Notes, tldr, HERE. However, what Cohn says about tariffs creating inflation is not accurate, as outlined by the 2017 through 2020 results of Trump tariff policy. Cohn says, “No one absorbs tariffs, except the consumer,” this is false. As we saw in 2017, 2018, and 2019 China, Asia and the EU essentially dropped their export prices to retain access to the USA market and offset tariff costs. That’s just a statistical reality.

The transcript is HERE; however, I want to draw attention to a geopolitical aspect that is not getting enough attention. Specifically, the cost of FOOD PRODUCTS and the attached inflation.

Why is food inflation continuing to be a problem? Why is food inflation not just a USA problem? Why are the EU farmers protesting? These questions are easily answered, and yet no one in the Western financial press will explain.

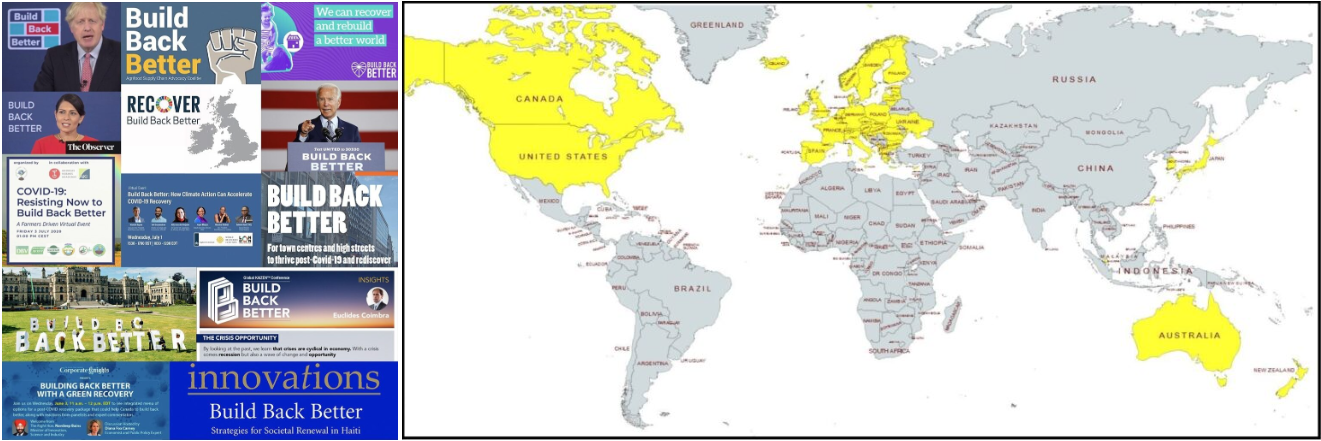

The Build Back Better agenda, known in the USA colloquially as the Green New Deal, carries with it massive increases in cost for energy products. Fertilizer, which needs natural gas, and farming, which needs large amounts of fuel, diesel and fuel oil, uses costly energy products. Packaging, plastics (petroleum derivatives) and cardboard also require large amounts of energy.

The manufacturing (heating, cooling, freezing) as well as storage and transportation of food products also use massive amounts of energy. Additionally, and specifically because of the nature of their consumption, the increased energy costs associated with generating food travels quickly through the supply chain.

Food inflation is always the first thing you notice when the prices of energy products skyrocket. This is well known and not subject to debate; everyone accepts this.

In the past 30 +/- years, large multinational corporations known as Big Ag have created a system where the USA generates a massive amount of the global food supply.

The advent of modern farming fertilizer, pesticides, seed genetics and other farming products/equipment that increase crop yield, has also been a big factor in the capacity of the USA and Western farming world to increase production. As the globe became more reliant on the production efficiencies of the Big Ag “Western world,” they simultaneously became dependent on the outcome. That dependency put them at risk of feeling the impact of inflation when you think about the farm products.

The result was that when Western Ag farming costs skyrocketed, the high cost of harvest outcomes were not just felt in the USA and/or Western nations. As food production costs increased, the higher costs of production transferred into all the exported products. Food inflation was exported globally.

The Western Build Back Better and Green New Deal energy policies subsequently meant the world was going to pay a higher price for food globally. That’s what happened.

The Yellow Zone was responsible for a higher percentage of global food production. The Yellow Zone is also the place where energy policy was changed in such a radical format that massive increases in energy costs were created.

The Yellow Zone (geopolitically the “West”) drove up the cost of farming, the Gray Zone pays a higher price. This was all by design and not accidental. The corporations who supported the BBB/GRD agenda all benefit. The citizens who need to eat, do not benefit.

So, when you see EU farmers protesting against the ridiculous ENERGY POLICY changes of the West, you must accept the USA bears a greater responsibility for creating and demanding the increased prices that farmers globally are having to deal with.

In Gray Zone areas, where domestic food production costs are not subject to the changed energy policy, there is little to no food inflation. However, the more dependent the country is to food imports (ingredients or final product) the more they are impacted by rising farming costs.

Grey Zone countries that can self-sustain on the production of food and have no energy agenda have little food inflation.

The more the country is strangling energy production and driving up energy prices, the higher the cost of farming and subsequently the higher index on food inflation. The two metrics are directly related.

Food inflation globally is a big problem. Western energy policy is exactly why!

Those who follow this blog already knew that the Federal Reserve would not drop rates in the future due to unsustainable fiscal policies paired with America’s increasing involvement in foreign wars. All of the talking heads were preaching that rates would significantly decline to pandemic levels, as if that were the historical norm. Every fiscal policy in recent years has exacerbated inflation and the Fed cannot keep up with government spending. QE FAILED. The artificially low interest rates of the recent past were completely unsustainable and relied on outdated theories.

The outdated understanding based on Keynesian Economics remains to increase the supply of money and it MUST be inflationary. The Fed raises rates to reduce consumption and lower rates to stimulate consumption. It’s a very nice theory, but when actually tested, it utterly fails. Lower rates will NEVER cause people to invest UNTIL they believe that there is an opportunity to invest. We are watching the big players withdraw from equities, let alone government debt. We are in a private wave where money is running off the grid at a rapid pace.

The peak in interest rates took place in 1899 at virtually 200%. Yet, 1929 was the real bubble top and it peaked with 20% interest rates in call money on the NYSE. In theory, the biggest boom should have been met with the highest interest rate. In truth, the “real interest rate” as I have defined it is when the interest rates exceed expectations. If you think the stock market will double, you will pay 25% interest.

As you can see, while interest rates hit nearly 200% in 1899, the share market did NOT crash percentage-wise anything as it did following 1929. Look, there is a lot more to this than meets the eye. Everything must be addressed on a global scale for it all depends also on the direction of capital flows. There is just a lot more to this than simply the money supply and interest rates.

Now, Powell continues to explain to the public that VOLATILITY and economic conditions are beyond the control of the Fed. “We believe that our policy rate is likely at its peak for this tightening cycle,” Powell said. “If the economy evolves broadly as expected, it will likely be appropriate to begin dialing back policy restraint at some point this year. But the economic outlook is uncertain, and ongoing progress toward our 2% inflation objective is not assured.”

All the news of inflation waning, including recent data, is inaccurate propaganda intended to calm recessionary fears. Even by the government’s data, inflation is up 3.1% compared to last year. It was an unprecedented moment when Powell broke with Washington and criticized the government for their unsustainable spending. The Fed NEVER criticizes the government, despite the two being separate.

Hence, I say to stop blaming the Fed. They are not the ones creating all the money but are working to match monetary policy with unsustainable fiscal policies. We are looking at trillions in deficits per year. There is no restraint when creating new massive spending packages. Then people blame the central bank with no concept that it’s only a fraction of “money;” the real issue is CONGRESS.

Listen, interest rates cannot decline in the face of war. The 2020 yearly array showed a turning point for a high in 2022 and a possible correction into 2024. I explain this in more detail on the Socrates private blog but buckle up for the year ahead.

The Biden Administration implemented a new rule that will cap credit card late fees at $8. The Consumer Financial Protection Bureau has praised the measure, estimating it will save Americans over $10 billion annually in late fees, or around $220 annually per person as 45 million Americans have experienced these fees within the last year, but this measure may be more harmful than helpful.

Credit card debt in America is at an all-time high of nearly $1.13 trillion and continues to rise as around 56 million Americans carry credit card debt. The typical late fee payment is around $32, but this is merely the fee for missing a payment and does not account for compounded interest. It seems like common sense, but one must realize that the average person is not financially literate. The concept of basic finance is not a mandatory requirement for the public education system, leading many people to live off debt, well beyond their means, with no chance of recuperating. America has the leading median level of credit card debt among all developed nations. There is a widespread belief that one can afford certain goods if they are approved for a line of credit, which only benefits the banks.

Now, the banks are certainly profiting on late fees, which account for about 15% of credit card profits based on the CFPB’s 2021 Consumer Credit Card Market Report. Do these fees deter reckless spending? A 2022 ABA-led survey found that 46% of respondents said they made it a priority to pay off their credit cards on time to avoid late fees. That particular study found that a fee of $10 was enough to redirect one’s attention to their financial obligations. Another study by the Harris Poll and NerdWallet found that Americans were more likely to make a payment of their cards if a $30 fee was implemented.

Again, one must understand that the average person cannot compute the cost of compounding interest. Borrowing money is not a legal right and should be done with the utmost caution. Simply forgetting or dismissing financial obligations has consequences.

The banks will find a way to profit off the people in other ways. It is the nature of banking. Rob Nichols, the president and CEO of the American Bankers Association, explained that other measures could be implemented that will hurt everyone. “The Bureau’s misguided decision to cap credit card late fees at a level far below banks’ actual costs will force card issuers to reduce credit lines, tighten standards for new accounts and raise APRs for all consumers – even those who pay on time,” Nichols said. This is yet another Biden Admin policy favoring the financially irresponsible at the expense of others.

So, what is the CFPB recommending as an alternative? CBDC. The agency is first suggesting digitizing banking so that consumers have instant access to their credit scores and spending habits. Again, these numbers are disregarded by a portion of the population. The agency is patronizing all Americans by stating we are not intelligent enough to know when to pay off our monthly debts without digital notifications and reminders.

Financial literacy is desperately needed in America. So, while the Biden Administration is breaking its arm patting itself on the back for this surface-level win for the everyday man, the ruling does nothing to combat the growing personal debt crisis.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

De Oppresso Liber

A group of Americans united by our commitment to Freedom, Constitutional Governance, and Civic Duty.

Share the truth at whatever cost.

De Oppresso Liber

Uncensored updates on world events, economics, the environment and medicine

De Oppresso Liber

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America

Australia's Front Line | Since 2011

See what War is like and how it affects our Warriors

Nwo News, End Time, Deep State, World News, No Fake News

De Oppresso Liber

Politics | Talk | Opinion - Contact Info: stellasplace@wowway.com

Exposition and Encouragement

The Physician Wellness Movement and Illegitimate Authority: The Need for Revolt and Reconstruction

Real Estate Lending