Armstrong Economics Blog/Armstrong in the Media Re-Posted Mar 19, 2023 by Martin Armstrong

Click here to listen to my interview on 3/16/23 with World Affairs Monthly (also published on Monitoring Risk).

Click here to listen to my interview on 3/16/23 with World Affairs Monthly (also published on Monitoring Risk).

Small to medium sized banks along with credit unions are the best vehicle for Main Street USA small businesses. Somehow in all the conversations about banking customers, this little factoid is seemingly, perhaps purposefully, overlooked. WATCH:

During today’s Senate Finance Committee hearing, Sen. Bill Cassidy (R-LA) questioned Treasury Sec. Janet Yellen about Social Security and the immediate cuts that take place in nine years if the current plan goes bankrupt. The confrontation was professional, but also very focused. WATCH:

.

There once was a time when cash was the undisputed king. Merchants preferred cash payments over credit, and there were often incentives for paying with paper. I recall receiving lower gas prices when paying with cash, for example. It is increasingly common to see “no cash accepted” signs at establishments as the world moves toward a cashless society. At the Federal level, there are no laws protecting consumers who wish to pay in cash. The Federal Reserve stated on its website:

There is no federal statute mandating that a private business, a person, or an organization must accept currency or coins as payment for goods or services. Private businesses are free to develop their own policies on whether to accept cash unless there is a state law that says otherwise.

"Section 31 U.S.C. 5103, entitled "Legal tender," states: "United States coins and currency [including Federal Reserve notes and circulating notes of Federal Reserve Banks and national banks] are legal tender for all debts, public charges, taxes, and dues." This statute means that all U.S. money as identified above is a valid and legal offer of payment for debts when tendered to a creditor."

Yet, the Federal Reserve also recognizes that as of 2021, 4.5% of US households were “unbanked.” This means that 5.9 million households are unable to pay by card. This is the lowest unbanked rate since the Fed began keeping track in 2009. The most common reason for not having an account, reported by 21.7% of unbanked households, is that they do not meet minimum balance requirements. The second most reported reason (13.2%) is that people simply do not trust banks, while the third most cited reason (8.4%) was the desire for privacy.

If merchants refuse to accept cash, these people cannot participate in consumerism. Their legal tender is simply not accepted. Unbanked households are more likely to contain persons with lower levels of education, lower incomes, disabilities, single mothers, and minorities. As the Fed reported:

“Differences in unbanked rates between Black and White households and between Hispanic and White households in 2021 were present at every income level. For example, among households with income between $30,000 and $50,000, 8.0 percent of Black households and 8.4 percent of Hispanic households were unbanked, compared with 1.7 percent of White households.”

If cash is legal tender, then it should be accepted everywhere. Numerous merchants not only refuse cash but they charge an additional fee for using credit. Tennessee, Arizona, Delaware, District of Columbia, Idaho, Maine, Massachusetts, Michigan, Mississippi, New York, North Dakota, Oklahoma and Pennsylvania, New Jersey, Rhode, Colorado, and Connecticut have laws at the state level protecting cash payments. Some cities such as Washington D.C., Berkley, Chicago, New York City, Philadelphia, and San Francisco also have laws in place. However, I can assure you that many retailers in these areas still do not accept cash.

Washington wants to move us toward a cashless society to tax everyone, even those with the least to give, on every transaction we make.

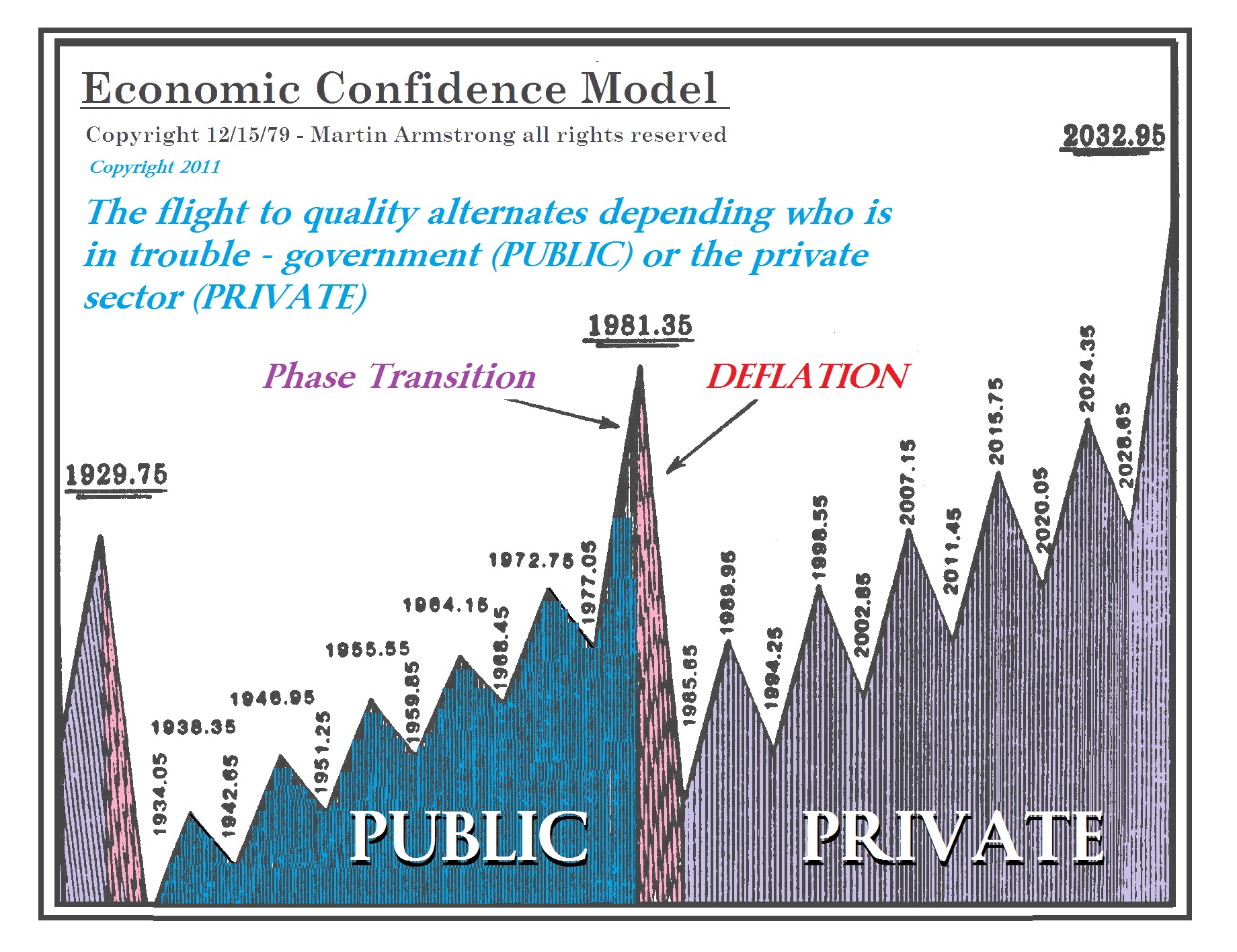

In an interview on May 11, 2014, I explained on USAWatchdog that confidence always outweighs reality. “It’s basically what you believe. There have been all sorts of studies on fundamentals that say if interest rates go up, stocks go down. It is simply not true. The stock market has never peaked with interest rates twice in history. If you think you are going to make 25% in the market, you’ll pay 10% interest; but if you really think the market is only going to go up 10%, you won’t pay 10%. So, it’s always the difference between what you believe and reality.”

The people have lost all confidence in government. We have heard rumors of a “soft landing” from the Fed for the past year, but the situation continues to worsen. Washington maintains that everything is stable as banks continue to fail and inflation rages on. There can be no price stability when war is at play. Biden just released his latest budget plan that no reasonable person would condone. I explained in 2014 that great empires all come crashing down after piling on massive debt. People believe hyperinflation would cause such a scenario, but debt is the major player. Once the government accumulates enormous debt, it targets its citizens aggressively. That is what we are seeing today.

So where should you put your money? I said in 2014: “One of the number one questions I get all the time is where do I put my money? If the banks can just take whatever they want now, there will be bail-ins rather than bail-outs. People are afraid. What do you do with the cash? So, people are buying things like real estate and stocks, just trying to get money out of the banking system.” That sentiment is continuing and the latest CPI report even showed that shelter costs are rising at the highest rate since June 1982. Smart money has been trying to escape the banks for years. There was no incentive until very recently to park money in the banks due to artificially low rates.

I also explained that the Fed would only bail out deposits and had been asking institutions to change their models. “Everybody knows I advise some of the big institutions around, and I can tell you that they have told me directly that the Fed went to them and told them they will not be bailed out for proprietary trading. It will be only on deposits. That’s it,” I stated. “The Fed has been going around telling them, ‘hey, you better change your models.’ They don’t think it will be a flight to quality as it was before. You buy the long term (Treasuries) and that saves you. They don’t think that’s going to happen. It’s quite interesting. . . . It looks like the long term (Treasury bonds) is going to end up starting to rise.”

Sound familiar to the current situation? People have moved from the public sector into the private sector. We are well into a private wave, and the public will not go back to the public sector for many years to come.

Before getting to the details of the Credit Suisse issue, it is worth taking a bigger geopolitical context to the dynamic. The initial backstop sought by Credit Suisse was from the Saudi National Bank; however, SNB Chairman Ammar Abdul Wahed Al Khudairy refused more lending {LINK}.

This is where we need to keep the BRICS -vs- WEF dynamic in mind and consider that ideologically there is a conflict between the current agenda of the ‘western financial system’ (climate change) and the traditional energy developers. This conflict has been playing out not only in the energy sector, but also the dynamic of support for Russia (an OPEC+ member) against the western sanction regime. Ultimately supporting Russia’s battle against NATO encroachments.

Russia, Saudi Arabia and China are geopolitically aligned in interest against the western financial system. As a consequence, when western banks find themselves in need of capital and cash, there is a layered geopolitical dynamic in the background to Saudi refusal that must be considered.

With multiple western banks now in trouble, Credit Suisse is also exposed, and, like U.S. Treasury/Fed intervention in America, the Swiss central bank has stepped in to backstop the looming collapse.

In the big picture we are seeing the ramifications of the ‘Build Back Better‘ agenda impacting the banking and finance sector which spearheaded it. I am not seeing this discussed anywhere, as the western governments of the collapsing banks are being forced to intervene.

(Reuters) – Credit Suisse on Thursday said it was taking “decisive action” to strengthen its liquidity by borrowing up to $54 billion from the Swiss central bank after a slump in its shares intensified fears about a broader bank deposit crisis.

The Swiss bank’s problems have shifted the focus for investors and regulators from the United States to Europe, where Credit Suisse led a selloff in bank shares after its largest investor said it could not provide more financial assistance because of regulatory constraints.

Regulators in the private banking hub on Wednesday had sought to ease investor fears around Credit Suisse, which added to broader worries sparked by last week’s collapse of Silicon Valley Bank and Signature Bank, two U.S. mid-size firms.

Asian stocks had extended Wall Street’s tumble on Thursday and investors bought gold, bonds and the dollar, leaving markets on edge ahead of a European Central Bank meeting later in the day. The bank’s announcement in the early European morning helped trim some of those losses though trade was volatile. (read more)

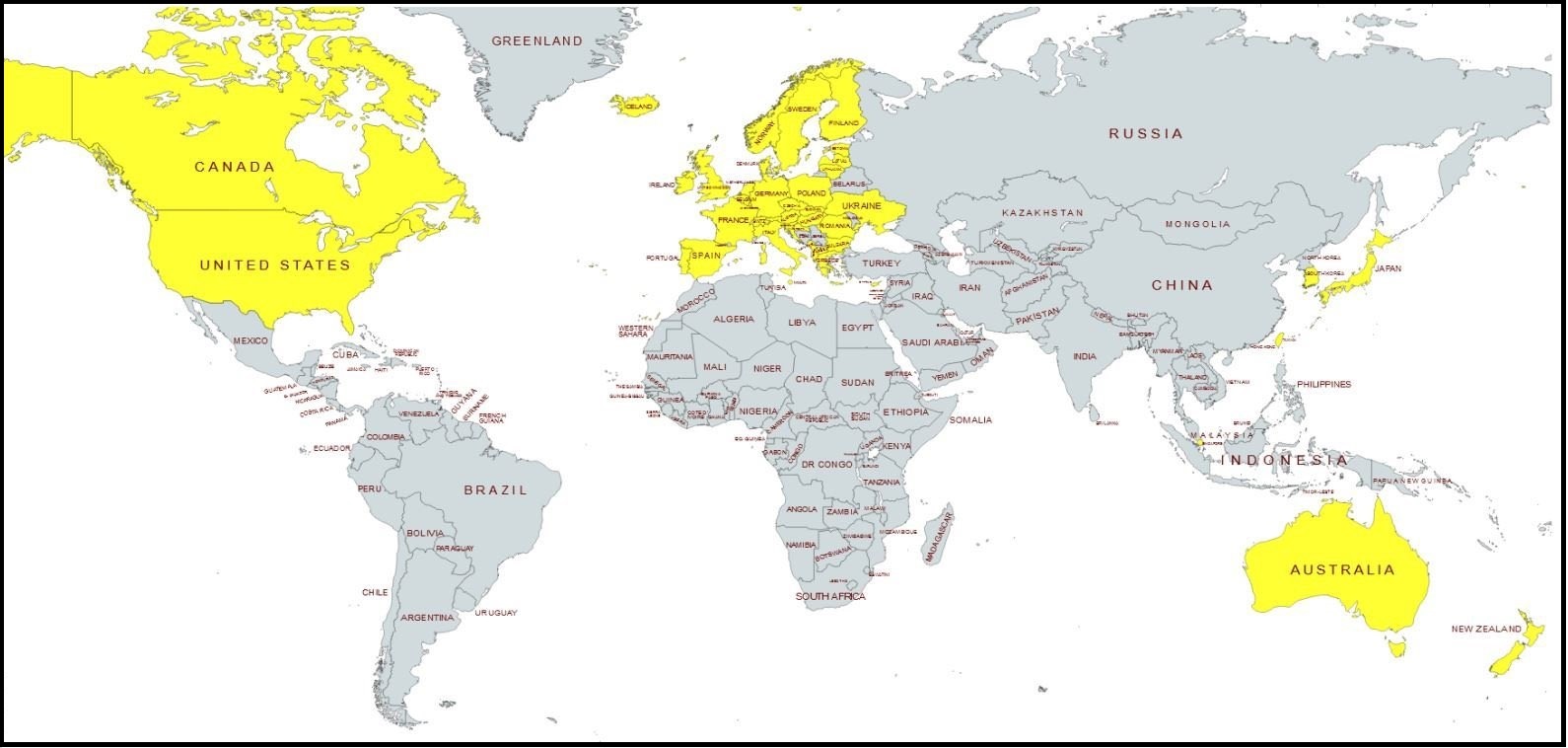

Again, I go back to the geopolitical map. The yellow nations with sanctions against Russia are also the yellow nations driving the ‘Build Back Better’ climate change energy policy. The grey nations are not in alignment with either dynamic. It is not a coincidence the banking issues are all within the yellow nations.

(Via Daily Mail) Wall Street’s main stock indexes opened lower on Wednesday, as turmoil at Credit Suisse renewed fears of a banking crisis and sent shares of major US banks lower.

At the opening bell, the Dow Jones Industrial Average fell 396 points, or 1.23 percent, while the S&P 500 opened 1.09 percent lower and the Nasdaq Composite dropped 1.20 percent.

Shares of First Republic, one of the regional banks swept up in contagion fears after the collapse of Silicon Valley Bank, dropped up to 11 percent after the bank’s bond rating was downgraded to junk status by S&P.

In Europe, shares of Credit Suisse plunged more than 25 percent, hitting a new record low for the second day in a row, after the Swiss bank’s largest investor said it could not provide more financial assistance to the lender.

The Big Four trillion-dollar US banks suffered in early trading after yesterday’s rally. Wells Fargo slid 3.9 percent, Citigroup dropped 4.3 percent, Bank of America was down 2.2 percent and JP Morgan saw a 3.5 percent dip.

After the collapse of SVB Financial and Signature Bank, emergency measures by US authorities had soothed some worries about the health of the other banks, helping regional lenders stage a rebound in Tuesday’s session.

However, regional banks were giving back their gains in early trading Wednesday, with shares of First Republic, PacWest and Western Alliance all down between 2.7 percent and 11 percent.

[…] Driving investor sentiment was turmoil at Credit Suisse, after its biggest shareholder – the Saudi National Bank – said that it would not inject more money into the ailing Swiss bank.

Saudi National Bank chairman Ammar Al Khudairy told Reuters: ‘We cannot [buy more shares] because we would go above 10 percent. It’s a regulatory issue.’

The Saudi bank holds a 9.88 percent stake in Credit Suisse, according to Refinitiv data. (read more)

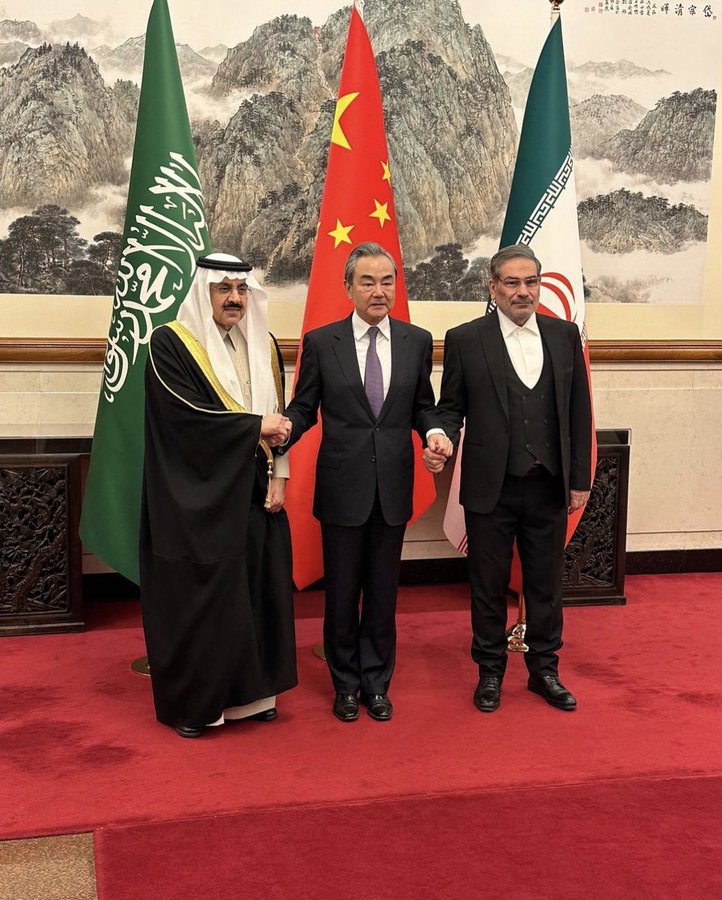

Yellow Team -vs- Gray Team: Remember, China just brokered a deal to lessen hostilities between Iran and Saudi Arabia. The fulcrum of that agreement was economics.

Meanwhile in North America, Mexican President Andres Manuel Lopez-Obrador has said he was not willing to join the energy suicide pact pushed by Joe Biden and Justin Trudeau…. A policy break in the trilateral relationship which suddenly, and not coincidentally, aligns with the timing to make Mexico a pariah to the U.S. vis-a-vis a renewed media push on the drug cartel narrative.

BIG PICTURE NOT BEING DISCUSSED – The western politicians followed the climate change instructions of the WEF multinational corporations and banks (Build Back Better) and post-pandemic immediately started reducing energy development. The central bankers then began raising interest rates to shrink the economies of the same western nations to the scale of the now diminished energy production.

The raising of interest rates is now hitting the national and multinational banks impacted by government policy that was following WEF orders. Now the western politicians are stepping in with the government controlled central banks to backstop the national banks and multinationals. Can you see the dynamic?

Team yellow is suffering the consequences of their own ideological policy as enacted. Team grey is not going to help team yellow get out of a crisis team yellow created, which was intended to hurt team grey.

…. And we continue watching.

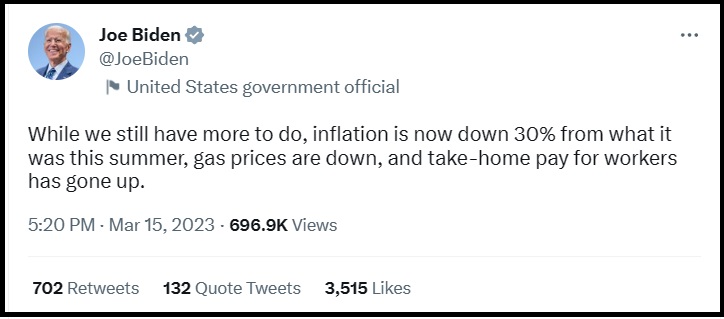

This is so far beyond hubris, the gaslight from where hubris emanates would take a year to reach it.

Joe Biden spikes the football on the Twitter claiming to have lessened inflation he created. [LINK]

I try not to hold negative sentiments, but I cannot help but loathe this man.

COMMENT: Marty, I really cannot thank you enough. Socrates called yesterday as the turning point and it was the strongest one of the week. We got the bounce when everyone was in a panic state claiming that the Fed would not have to lower rates. They really do not understand central banks as you alone have explained many timers. There was no way the Fed would lower rates and undermine its credibility by suspending its inflation fight now, That would blow all credibility and lead to panic for sure. The Fed will not change because of SVB for that would undermine financial stability completely.

I am not sure just how much Socrates helps traders and society.

Paul

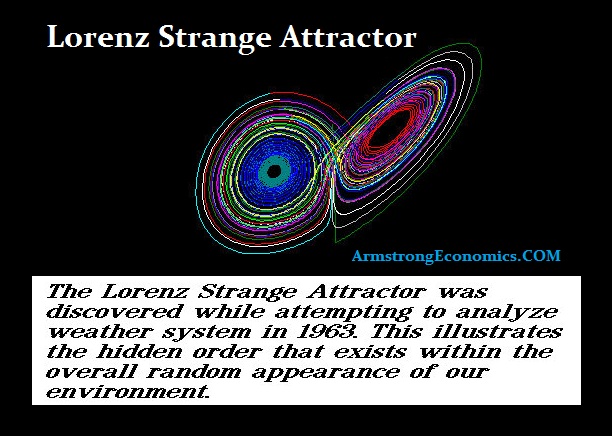

REPLY: I do realize that Socrates could run the economy far better than any human. It is my hope that it proves itself over the course of now and 2032 and that people will look back upon these forecasts and at last comprehend that there is truly a hidden order in what people think are just random walks.

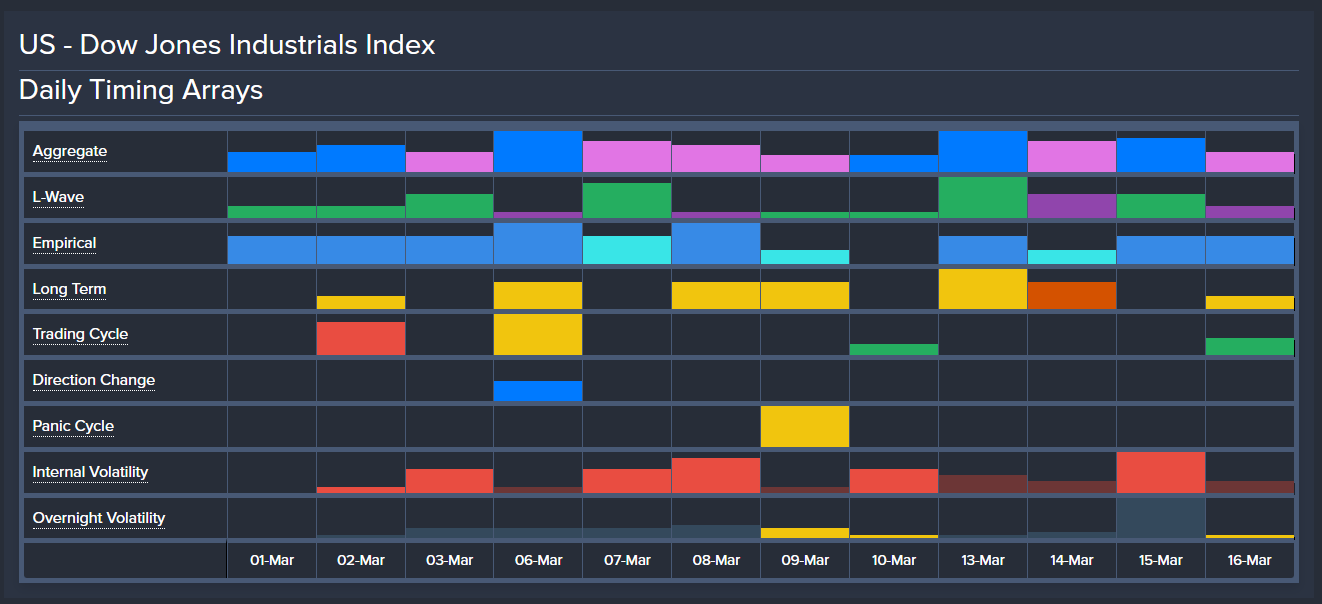

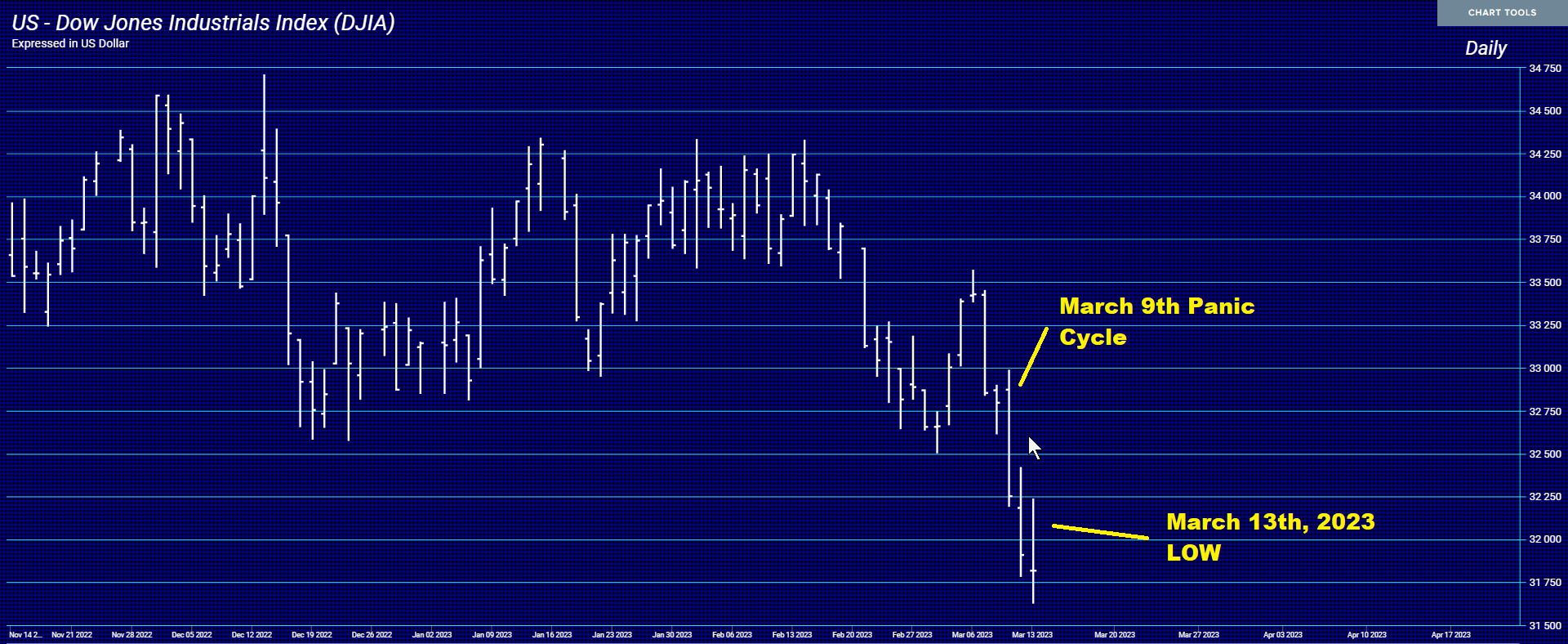

Here is the Array published on March 1st. It forecast the high for the 6th with a turning point, a Panic Cycle for the 9th, and then the turning point on the 13th for a low. This was clearly published in advance of the SVB failure. This raises the question, how can a computer possibly predict such a Panic would take place on the 9th long before anyone heard about SVB? This is NOT my personal opinion. You do not see me running ads saying this is the guy who had forecast whatever. Socrates has taught me a lot about market behavior.

Just as Edward Lorenz ran what appeared to be random weather data into a computer and out came the most perplexing image of a hidden order that existed in what the human eye could see only randomness. He became the father of Chaos Theory, which to this day, prevents us from seeing the future as part of a pattern that has been set in motion.

My real hope is that the world will come to recognize that there is a hidden order to everything that most are blinded by the appearance of randomness – chaos. We need to understand how everything worked if we are to reconstruct a new form of government after the great collapse of governments post-2032.

COMMENT: Pi Day history compliments —-

On March 14, 1883 KARL MARX MADE HIS MOST IMPORTANT CONTRIBUTION TO MANKIND . . .

HE DIED.

Happy Pi Day!

SR

REPLY: Also, Albert Einstein was born in Ulm, Germany, on March 14th, 1879.

The Chinese yuan has out-traded the US dollar by volume for one of the first times in recent Russian history. The dollar was king in 1991 when the Soviet Union collapsed, but that is no longer the case after Moscow branded the dollar a “toxic currency” along with the euro. Toxic currencies accounted for 87% of exports from Russia at the beginning of 2022, but this figure fell to 48% by the start of the new year. The Bank of Russia has reported that the proportion of USD/ruble pair in exchange fell to only 36% in February. The central bank is calling this a “broad structural transformation of the Russian economy.”

As “unfriendly countries” and their “toxic currencies” band together, those on the outskirts are winning. China has become the new go-to country for new trade partnerships as it bypasses Western-imposed sanctions. Toxic currencies represented 46% of imports in December 2022 but were at 65% in January 2022 before the war. In contrast, the yuan’s share rose from 4% to 23% during that time.

Those who were previously shunned from the big table are now pulling up a chair to discuss economic prospects with China. This will make it much easier to phase out toxic currencies because more people are willing to accept the yuan. The confidence in the yuan is growing. Everything occurring may seem odd, but it is precisely on target. As I mentioned in my report “China on the Rise,” China will dethrone the United States to become the world’s leading economic powerhouse by 2032. It’s just time.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

De Oppresso Liber

A group of Americans united by our commitment to Freedom, Constitutional Governance, and Civic Duty.

Share the truth at whatever cost.

De Oppresso Liber

Uncensored updates on world events, economics, the environment and medicine

De Oppresso Liber

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America

Australia's Front Line | Since 2011

See what War is like and how it affects our Warriors

Nwo News, End Time, Deep State, World News, No Fake News

De Oppresso Liber

Politics | Talk | Opinion - Contact Info: stellasplace@wowway.com

Exposition and Encouragement

The Physician Wellness Movement and Illegitimate Authority: The Need for Revolt and Reconstruction

Real Estate Lending