Posted originally on Apr 24, 2024 By Martin Armstrong

This is what happens when Soros funds Bureaucrats to destroy the very country they grew up in. Soros is out to flood the USA to destroy our politics and culture.

This is what happens when Soros funds Bureaucrats to destroy the very country they grew up in. Soros is out to flood the USA to destroy our politics and culture.

While Turkey is a NATO ally, Recep Erdogan strategically refused to participate in the process to ostracize Russia. True to Erdogan’s strategic political interests of being an influence broker, Turkey is the only NATO country that does not participate in the sanctions regime against Russia. Next month Russian President Vladimir Putin will travel to Turkey for diplomatic discussions.

Turkey represents the literal gateway for most Western travel into and out of Russia. However, first things first. Despite the position of Turkey, notice how Hungary receives all the EU admonitions for not supporting the Ukraine side of the conflict, while NATO/EU never criticize Turkey who never even joined the EU/Western sanctions regime. Inside that hypocritical contrast there is a revealing story.

Turkey established themselves as the neutral entity for future brokering negotiations between Russia and Ukraine. Turkey has multiple geopolitical ties to Russia, including the purchase of Russian military equipment. Apparently, despite the severity of the original sanction demand, Western interests -specifically the U.S. government- had no issue with Turkey proactively taking their ‘neutral’ position. Always remember this.

Given all of the domestic headlines in the USA, there is a very good reason for Americans to keep paying attention to all things that happen in the orbit of Russia right now. Many people ponder the issue of a dollar-based central bank digital currency; however, only a few people have paid attention to the self-fulfilling prophecy of the CBDC that was created by the Russian sanctions regime.

Those who ask about the possibility/probability of a dollar-based CBDC, and the possibility of the timeframe therein, should always be referenced back to the Western financial sanctions against Russia. It was that triggering point that put the USA and Western alliance on the irreversible path to the U.S CBDC, and the process is no longer a matter of “if” because the determining issue is no longer (primarily) in U.S. control.

The de-dollarization of half the trade globe, the general cleaving of finance that followed the Russian sanctions (see the efforts of BRICS+), has essentially created a system where major economic nations are trading between themselves in non-dollar-based exchanges. India trades with Russia in Rupes to Rubles. China trades with Russia on old fashioned ledgers of value (due to proximity somewhat of a quasi-bartering system); Iran, Saudi Arabia, Egypt, South Africa and a host of non-Western nations are all in various stages of direct trade in national currency outside the dollar zone.

At the core of the issue behind the question of a U.S. or dollar-based Central Bank Digital Currency, you will find this global financial cleaving. Intra-Western trade (USA, Canada, Australia, New Zealand, Japan and the EU) is still done in dollars, and trade done into the Western system is still done in dollars. Ex. if China wants to trade into the USA, they must complete transactions in dollars. However, trade from grey zone to grey zone nation is no longer contingent upon dollars.

Very few people are talking about these new financial trade alternatives. Yet ultimately, this cleaving is likely what will result in a dollar-based U.S CBDC. Remember, the need for alternative trade currencies was triggered in time by the immediacy of the sanctions against Russia. I do not believe the Western financial alliance thought the Russian allies could assemble the alternative so quickly.

If the DoS and CIA truly believed the sanctions would cripple Russia, it’s then likely our institutions vastly underestimated the prior diplomatic talks that preceded those sanctions. As a big picture consequence, no geopolitical issue is as connected to your kitchen table as anything that connects with Russia. So, pay close attention to how Russia is engaged by the rest of the non-Western world (grey zone), and you will get a good idea about the speed and timing of a pending U.S. CBDC.

As soon as the grey zone trade is predicted to take place in non-dollar terms, the U.S CBDC will be fast-tracked. The only way for President Donald Trump to stop the CBDC process would be to immediately end the Russia-Ukraine conflict and subsequently remove the sanctions. [And that might not even work.] As long as there are financial trade blocks based on dollars and who we like, there will be an easy justification for the financial cleaving to continue.

RUSSIA – Russian President Vladimir Putin will visit Turkey next month in a rare foreign trip to a NATO nation, according to a Kremlin announcement on Monday.

Yuri Ushakov, a top adviser to Putin on foreign policy matters, told the Interfax news outlet that “a visit is being prepared.” As to the purpose of the visit, Ushakov added: “I can say that Ukrainian issues will probably be one of the main subjects of negotiations.”

Though a key NATO nation, Turkey and its president, Recep Tayyip Erdoğan, serve as a rare diplomatic bridge between the Kremlin and its Western rivals. Since Russia’s full-scale invasion of Ukraine on February 24, 2022, Ankara has supported Ukraine with military supplies while refusing to join Western sanctions on Moscow.

Turkey has positioned itself as a mediator between the two nations, hosting two rounds of peace talks in Antalya and Istanbul in 2022. Turkey was also key to the Black Sea Grain Initiative that temporarily facilitated the export of agricultural products from southern Ukrainian ports amid Russia’s naval blockade.

Following a phone call with Ukrainian President Volodymyr Zelensky at the beginning of this month, Erdoğan said Ankara remains ready to help “establish lasting peace, stability and prosperity in our region.”

“We have previously acted as a host country for direct talks between the parties to the conflict,” the president said. “We are, as before, ready to do our best in this matter and act as a mediator….Ukraine in order to take joint steps with Russia certainly needs to soften its position.”

Putin last visited a NATO nation in 2020 when he traveled to Germany to meet with then-Chancellor Angela Merkel. His Western travel options have been limited by his war on Ukraine and the arrest warrant issued for him in 2023 by the International Criminal Court over alleged related crimes. (read more)

I really do not like Turkish President Recep Erdogan. His political policy is full of dangerous self-interest (Muslim Brotherhood) and thirst for power (recreation of the Ottoman empire). However, on the issue of ending this Russia-Ukraine conflict, I will admit Erdogan has positioned himself very well.

If Trump wins in November, Erdogan will play a major role in the end of hostilities.

You might even say Erdogan holds the key to eliminating the self-fulfilling prophecy of a US CBDC that Obama/Biden created.

Collapse is never a sudden occurrence; it is an outcome of gradual erosion over time. A weakening that takes place almost invisible to those who pass through the construct, until eventually, at an uneventful time in the mechanics of history, the process gives way.

Fitch has joined with the prior position of Standard & Poors to downgrade the USA credit rating. The weight of debt, in combination with reverberations from the continued hammering deep inside the political fundamental change operation, has triggered another flare.

In the bigger picture, this is a self-fulfilling prophecy driven by the latest focus on unsustainable economic policy, aka The Green New Deal. The efforts of the fiscal, monetary and economic policy are all aligned to shrink the U.S. economy, thereby creating the era of “sustainable energy” a possibility. Unfortunately, this is akin to a household intentionally shrinking their income while at the same time taking on credit card debt. The process itself is not sustainable.

(Reuters) – Rating agency Fitch on Tuesday downgraded the U.S. government’s top credit rating, a move that drew an angry response from the White House and surprised investors, coming despite the resolution of the debt ceiling crisis two months ago.

Traders’ immediate response was to embark on a safe-haven push out of stocks and into government bonds and the dollar.

Fitch downgraded the United States to AA+ from AAA, citing fiscal deterioration over the next three years and repeated down-the-wire debt ceiling negotiations that threaten the government’s ability to pay its bills.

[…] “In Fitch’s view, there has been a steady deterioration in standards of governance over the last 20 years, including on fiscal and debt matters, notwithstanding the June bipartisan agreement to suspend the debt limit until January 2025,” the rating agency said in a statement.

U.S. Treasury Secretary Janet Yellen disagreed with Fitch’s downgrade, in a statement that called it “arbitrary and based on outdated data.”

[…] In a previous debt ceiling crisis in 2011, Standard & Poor’s cut the top “AAA” rating by one notch a few days after a debt ceiling deal, citing political polarization and insufficient steps to right the nation’s fiscal outlook. Its rating is still “AA-plus” – its second highest.

After that downgrade, U.S. stocks tumbled and the impact of the rating cut was felt across global stock markets, which were in the throes of the euro zone financial meltdown.

In May, Fitch had placed its “AAA” rating of U.S. sovereign debt on watch for a possible downgrade, citing downside risks, including political brinkmanship and a growing debt burden. (read More)

What do Barack Obama and Joe Biden have in common? They were both in office, executing an identical economic, fiscal and monetary policy, when the USA credit was downgraded.

Legendary financial and geopolitical cycle analyst Martin Armstrong was forecasting “chaos” in 2023, and that’s exactly what we got. His cycle work says don’t look for it to get better anytime soon. Armstrong explains, “We are in the midst of a coup. We have all these people who have been neocons for 30 years. Even Ron Paul said recently that the neocons have been waging war for 30 years and have not won a one single one. This is what they live for. Look at the clip of Lindsey Graham saying this is the best money we ever spent killing Russians. How can you take pleasure in that statement that this is the best money we ever spent killing Russians. This is not defense. These are the words of a psychopath in my mind. . . . They are not about to accept anybody who is going to be against war. The neocons are in full control of the government—period. We are living in the time of a coup. The United States is not the free country you thought it was. . . .”

Armstrong also predicts that the neocons will rig the 2024 election so Biden (or some other neocon) gets a second term. Is there any way to stop this election rigging and fraud in 2024? Armstrong says, “I don’t believe so. Our computers show that holy hell breaks loose starting in 2025. I think the problem will be the cheating will be in everybody’s face this time.”

Armstrong also says the neocons will try to start a war before the 2024 election so Biden will win because a wartime president has never lost an election. Armstrong says the cheating will be necessary because the real poll numbers for Biden are in the single digits and not the 40% approval ratings the Lying Legacy Media tells you. Armstrong contends Biden’s approval number is still stuck at 9.5% with his deadly accurate Socrates computer program, but the big reason for Biden and his crew to worry is the real inflation number. Armstrong says, “Inflation is subsiding a little bit, but it is basically still over 26%.”

Armstrong says Biden’s approval numbers are so low and inflation is so high that they have to have war with Russia. War is the reason they had to remove Trump out of the White House because Trump was against constant war. Armstrong adds, “No way they are going to allow a free election. It you think the CIA cannot rig the vote, I don’t know what planet you live on.”

Don’t expect Fed Head Jay Powell to lower interest rates. It will be just the opposite. Armstrong explains, “What is Powell looking at? War is the number one cause of inflation. He can’t say because you people are dumping all this money into Ukraine, inflation is only going to go higher because then he is criticizing the government. So, he just says he’s looking at ‘international considerations.’ Look what the Vietnam war did. It broke the back of Bretton Woods. War is always the number one problem. The neocons only care about winning, and they do not care about the country. The do not care about your 401-k or your retirement. They could care less.”

In closing, Armstrong warns, “Russia is like a wild animal, and if it is cornered, it will attack.” This means the whole thing in Ukraine could go nuclear if Russia is pushed into a corner. And what about all that debt the western world has built up? Armstrong says, “They intend to default on all the sovereign debt. . . .I don’t see this succeeding. I think it’s all going to collapse. The reason why they are doing this is they realize they are losing power. They feel it slipping out of their fingers. The more that happens, the more they become aggressive. That’s what this is all about.”

Despite the cheering from the Washington Post, CNN, NY Times, the rest of the anti-Democracy press, and all the Democrats who were brainwashed into thinking Trump really won only because of Putin in the Hillary version of conspiracy theory (misinformation), what they have unleashed is the international collapse in confidence of the United States. Ever since Trump’s arrest, my phone has been in meltdown mode. People who were even on the fence about my case suddenly called and said gee, they use the criminal law for political purposes in the United States. Once upon a time, they trusted the United States. It seems that Trump’s arrest is now a sea-change in realization.

People are starting to wake up. The list of people they go after criminally who are whistleblowers in some capacity like Snowden and Julian Assange is just the tip of the iceberg. Criminally charging Trump was crossing the Rubicon. Then the Democrats stated that Biden will not debate anyone – Democrat or Republican. That is in itself a confirmation that he is not competent to be president. Yet he is the perfect patsy for the Neocons to run the show. When Lindsey Graham holds up a sheet and quotes Biden as authority for him and his fellow Neocons to declare war on Russia, it confirms what I have been saying. The United States is no longer a free nation. We are living in a coup, but the press is silent as was the press in every such incident from Communist Russia to Venezuela when the state turns against its people.

So, the Democrats who do not care about the Constitution or our future as a nation can cheer that this is your time to utterly destroy the other 50% of Americans who you despise so deeply. You will win the 2024 election if Biden can make it that far, and every investigation into him and Hunter will be blocked by the Department of Justice, FBI, and the NSA because this is now about the power resting in the hands of the Neocons who just want war. So pack your toothbrush, you will get to fight Russians in Ukraine and put your political dreams on the line.

These leftist zealots are cheering the end times like the Romans who they said were still laughing when the barbarians stormed the gates. For EVERY phone call I have had from Asia to Europe, they are all expressing complete shock that the United States is collapsing in the midst of political corruption. Suddenly, our forecast that the 2024 election might not even take place or certainly will not be real is starting to hit home. They are now all seeing that our forecast about the 2024 Presidential Election would be the most corrupt in history and mark the END of democracy in the United States is not so far-fetched.

These leftist people just do not get it. They crossed the Rubicon and now the view of the United States from the outside looking in, nobody seems to believe that America is still the beacon of liberty to the world. It is becoming so obvious that our computer will be right once again.

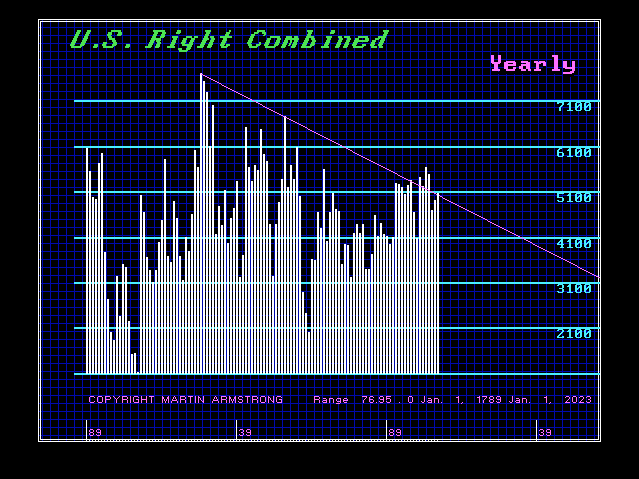

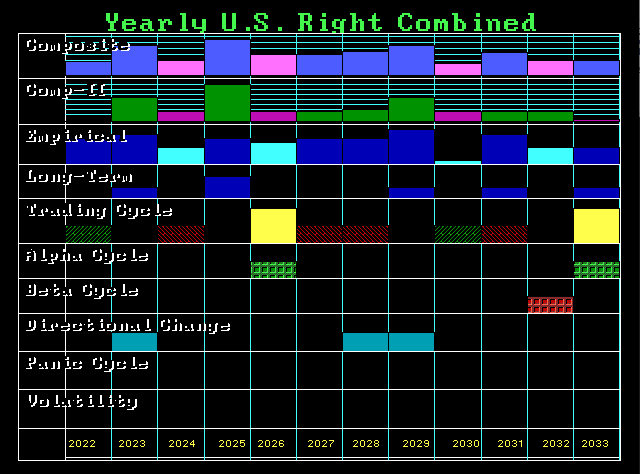

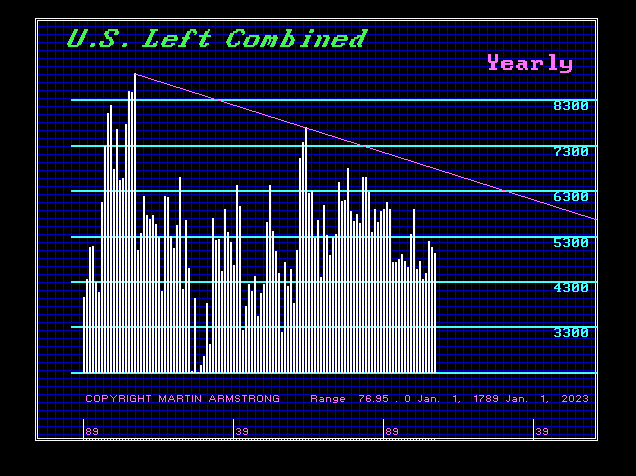

This year 2023 was a MAJOR turning point and an important Directional Change. You can see that 2025 is the biggest target for a decade. Announcing that Biden will not debate anyone is on par. I am warning you that the Neocons need to create war with Russia BEFORE the November 2024 election for in their mind, no president has ever lost an election during war. It will also allow them to create the excuse to suspend the election during a national crisis.

Desantis – PLEASE stay here in Florida. They will never let anyone win that office anyway. The Neocons are in charge. Stalin was correct. It does not matter who you vote for. Those who count the votes decide the election. Anyone who thinks the CIA cannot rig the election is an absolute fool.

As details begin to emerge, many of the House Republicans are furious at Kevin McCarthy for the deal to lift the debt ceiling he has brokered with Joe Biden.

Suddenly, the prior battle and construct of the House Rules Committee is becoming important. While Kevin McCarthy may have the 218 votes on the floor of the House to pass the deal, he first has to get it out of the House Rules Committee (HRC). If three Republicans oppose it in the HRC, McCarthy cannot get it to the floor. Chip Roy and Ralph Norman are on the HRC and oppose the bill. Thomas Massie is also on the HRC but appears to be supporting Kevin McCarthy (lol, because muh principles).

Byron Donalds also delivered a strong rebuke of the McCarthy deal, as outlined below:

WASHINGTON DC – […] The powerful House Rules Committee will spend Tuesday afternoon debating and — ultimately working to pass — the bipartisan debt deal, requiring a simple majority of at least seven votes on the panel to come to the floor. But some conservatives, including Rep. Chip Roy (R-Texas), a committee member, have signaled they may use their power on that panel to block the debt plan from receiving a full House vote.

“I’m going to do what’s in the best interest and this bill is not in the best interest of the country. That is why Democrats are voting for it,” said Rep. Ralph Norman (R-S.C.), another conservative who sits on the Rules panel and has suggested he will oppose the bill during the panel’s meeting.

[…] Under the panel’s current makeup, Rules Chair Tom Cole (R-Okla.) can lose two GOP votes — along with all four Democratic votes — and still advance the bill.

Senior Republicans believe that’s exactly what’s going to happen, according to three people familiar with the discussions. Norman and Roy haven’t explicitly said they will oppose, though Massie is expected to vote in support of the measure going to the floor.

GOP Whip Tom Emmer (R-Minn.) said that he is “confident” that the bill will hit the floor on Wednesday, noting that Rules would be considering amendments. Members submitted more than 55 amendments to the debt deal, most of them from Republicans but some from Democrats as well. (read more)

Rep Dan Bishop: The bill is bad

After the FOMC decision, Jerome Powell stated during his Q&A that the Federal Reserve does not have a plan to consolidate banks. “I personally felt that having small, medium, and large were a great part of our banking system,” Powell stated, noting that they all serve different customers. Powell said it could have been a good outcome had one of the regional banks bought failed First Republic instead of JPMorgan Chase. However, the chairman noted that the FDIC mandates that banks be acquired using the least costly resolution option.

The FDIC says it does not give preference to bidders. How can a bank qualify? According to the FDIC website: “Bid lists are created for each acquisition opportunity based on potential acquirer’s qualifications and interests and characteristics of the failing bank such as capital ratios, regulatory ratings, assets and core deposits as reported on the most recent Call Report and geographic location of the bank. Each bid list is developed using several criteria sets to identify approved potential bidders for an acquisition opportunity, while considering factors that match likely approved bidders to an acquisition opportunity.”

Due to the recent banking failures, the FDIC has also created guidelines specifically for failed bank acquisitions:

“The FDIC markets troubled institutions to healthy insured depository institutions. The FDIC is statutorily required to resolve failed institutions using the least costly resolution option minimizing losses to the Deposit Insurance Fund. The FDIC's primary objective is to maintain financial system stability and public confidence. Returning assets to the private sector in an orderly manner at the best price is another key objective. The FDIC also tries to reduce the impact on the community. Recapitalization before failure is the preferred method to resolve open troubled financial institutions. FDIC markets institutions in case a failing institution is not able to resolve its issues on its own. If an insured depository institution is unable to resolve its issues, the FDIC will implement its resolution process by which qualified bidders may seek to acquire the assets and assume the liabilities of the failing institution.”

Obviously, smaller banks will not have the ability to compete. All banks are struggling with liquidity issues, and mid-sized institutions will likely be unable to offer the “least costly resolution option.” Ideally, they want failing banks to be attained prior to failure, and only large institutions can provide that cushion. Nothing in the FDIC guidelines at the time of this writing currently limits what a large institution could acquire. The computer states that we will see more banking failures across the globe. Based on these guidelines in the US, it is reasonable to assume that large banks like JPMorgan Chase will benefit from future acquisitions and continue to grow. It is unclear whether banking monopolies are permitted under the 1890 Sherman Antitrust Act, but it remains to be seen what alternatives the system will have as more banks go under.

All we hear is the same claims that the dollar is dead and it will be totally worthless any day now. Over the last few weeks, all we hear from the majority now is that the dollar is finished. Virtually every page you turn or site you visit claims the death of the dollar. They are calling this the de-dollarization of the world economy and that the future of the US dollar as well as the American empire itself is now collapsing. The general claim is that the group of economically-aligned nations known collectively as BRICS is a major threat to the greenback. That was the same story we heard about the Euro back in 1997.

As their scenario goes, the BRICS [Brazil, Russia, India, China, and South Africa] have moved to form an anti-dollar colation and Saudi Arabia is considering jumping on board. They insist that once that happens, the “petrodollar” will die and cease to be a reserve currency.

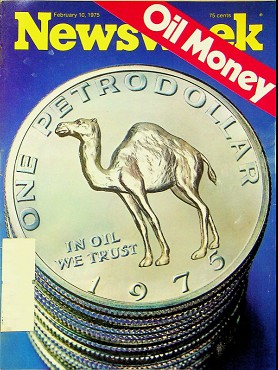

This is then followed by the forecast that the economy will suffer and that any bounce in exports will be short-lived simply because the dollar will be dead for the long term. Of course, this has been the favorite forecast that they keep putting out since Bretton Woods collapsed. They were wrong back then for the dollar rose between 1972 and 1976 against the British pound, with the collapse of Bretton Woods. To try to explain why the dollar did not collapse, that is when they claimed that the dollar was backed now by oil rather than gold. That was just an excuse as always to cover up their wrong forecast.

They sold that story to Newsweek and now the dollar rally was because of oil which replace gold. Suddenly the dollar became de facto backed by oil. They needed an explanation to explain why all the old theories were wrong. They sold this theory and it made the front cover of Newsweek. Everyone said YES! That must be the reason. OPEC priced oil in dollars! Naturally, everything was priced in dollars because, under the fixed exchange rate of Bretton Woods, everything from wheat and corn to copper and gold was all priced in dollars.

Now they are saying the American empire is threatened by the potential commercial real estate collapse and the BRICS anti-dollar venture. So they are forecasting a great depression-style crash is possible in the not-too-distant future. They spin this to forecast the end of the America Empire. The London FT, always anti-American/Pro WEF, reports that the dollar as a reserve currency has declined from 73% in 2001 to around 55% by 2021. Yet the FT did state an obvious fact:

“But if you are a reserve-rich central bank elsewhere that isn’t going to be a lot of comfort. Moreover, would you really feel more comfortable in, say, the renminbi? Even if it was fully convertible and liquid, would you honestly feel more sure that Beijing will behave lawfully than DC? The dollar still looks like the proverbial least dirty shirt in the closet.”

COVID actually has played a major role in shifting the world economy. In 2020, the US economy was 24.75% of the world’s GDP. By the start of 2022, it had fallen marginally to 24.15%. What these dollar-forecasting jockeys do not understand, is that if they were correct and the dollar collapsed, then the very BRICS would collapse even further. Economically speaking, when the United States gets a head cold, the rest of the world catches ammonia. You can’t have it both ways. The strength of the dollar is not gold or oil, it is the American consumer.

The risk to the entire world is runaway inflation thanks to Biden pouring untold amounts of money into the black hole known as Ukraine. The Neocons, who control Biden, are planning to launch a war against Russia and China before 2024. This will only continue to accelerate inflation. That reduces the spending power of the American consumer and in the process, the US economic growth declines in real terms and with it, the rest of the world plunges into recession.

While Macron has figured it out that the Neocons are in charge of US foreign policy and he is telling Europe to stop being the puppet of the USA, that all sounds nice but Europe is marching into war with Russia. NATO is firmly in control of the American Neocons and they need war or face losing power. With Trump in the lead, they must stop him at all costs for he is anti-war, would haul the Neocons out by the necks, and defund NATO, as well as stop the climate change agenda.

The US dollar in the global economy has been supported by the size and strength of the US consumer-based economy. Its stability and openness to trade and capital flows without restrictions and it has never been canceled, are the major foundation of the dollar in addition to strong property rights and the rule of law. That is why Russians and Chinese buy US property for they are secure in their ownership of US property which cannot always be guaranteed outside the US.

Consequently, the depth and liquidity of US financial markets remain unmatched. For institutions parking billions, the United States represents a large supply of extremely safe dollar-denominated assets. Are they really going to switch to China or buy debt from Brazil? Not a single institutional client will take that bait.

China has been divesting of dollar reserves because it KNOWS that the American Neocons want war. You do not fund your adversary who intends to wage war against you. China cannot shift reserve assets to Europe or Japan. They have been buying gold because it is geopolitically neutral territory. They are NOT buying gold as an investor thinking it will rally. That is irrelevant. If gold drops 25%, that does not translate into them becoming a seller.

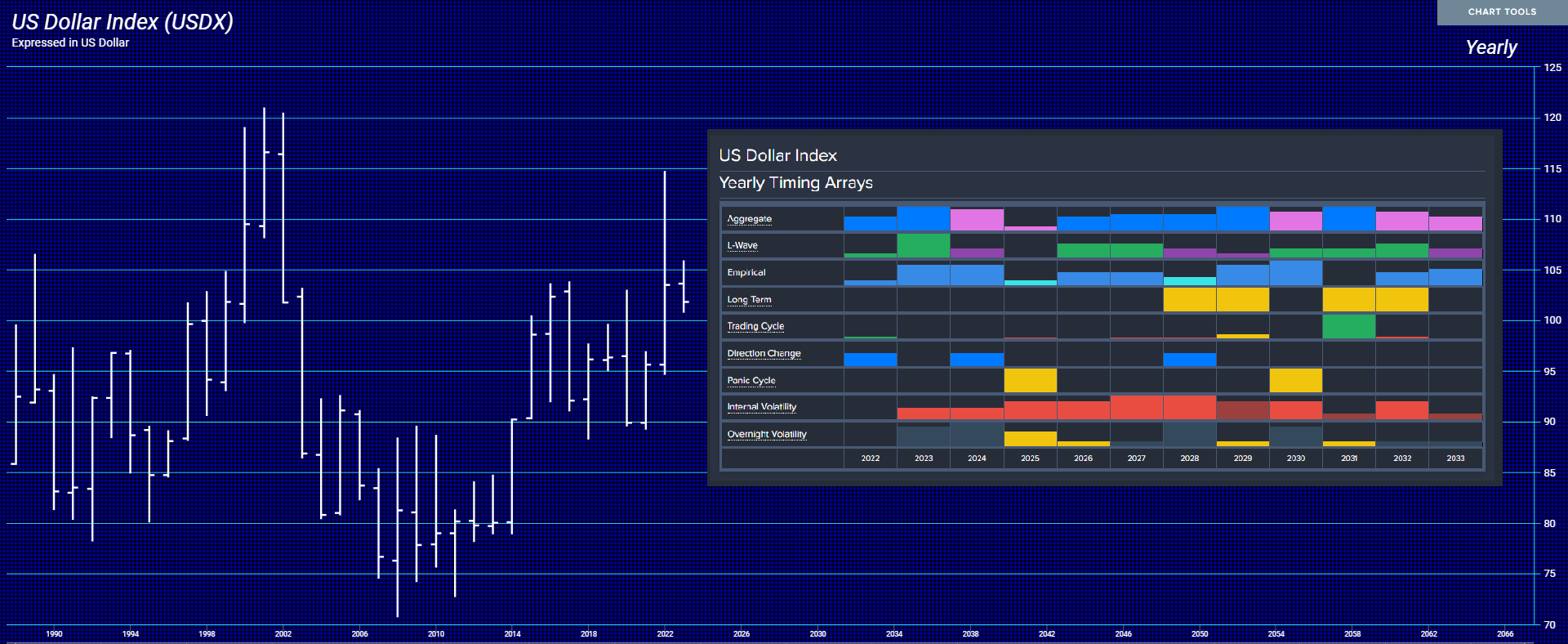

The dollar in international reserves stood at 60+% at the start of 2022 against the US share of GDP at 24.25%. This comparison belittles the argument that the dollar is finished. Eventually, the US will lose the wars it is starting and the dollar will be replaced perhaps as soon as 2028. The IMF is already licking its lips and rubbing its hands together eager to get control of the reserve currency. But they too will collapse. We have a Directional Change next year and a Panic Cycle in 2025. So buckle up.!

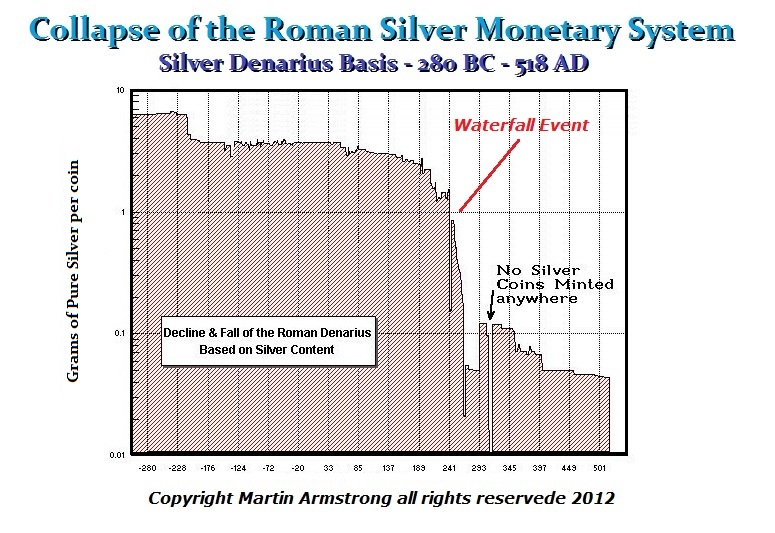

Remember one thing, even with the debasement and collapse of the Roman Denarius between 260AD and 268AD, it still took 224 years for Rome to completely collapse. When war breaks out, capital flight will still be to the dollar. It will not be to public assets, but private. The United States is still supporting the entire world economy. The BRICS need the US consumer to keep their economies functioning. All this talk of the dollar being finished is really nonsense. That day will come, but when the US consumer no longer buys.

Remember 1997? The Euro was going to dethrone the dollar. They claimed the new EU will be a bigger economy than the US. The problem was, they lacked a consumer economy, and low taxes, and they routinely canceled their currency to force people to pay taxes. It is always the same story over and over again.

COMMENT #1: Hi Martin, corn also turned nicely on the ECM:

JB

COMMENT #2: Hello Marty, I just want to point out that the Japanese yen broke really hard on the 10th. Not sure if this will prove to be a precursor of what is to come.

Thanks from Tokyo, your old home ground.

AS

COMMENT #3: Well the ECM also marked the reversal in trend in the 30-year bond. It peaked at 134 and fell to 130 by the end of the week. That was just remarkable.

Colin

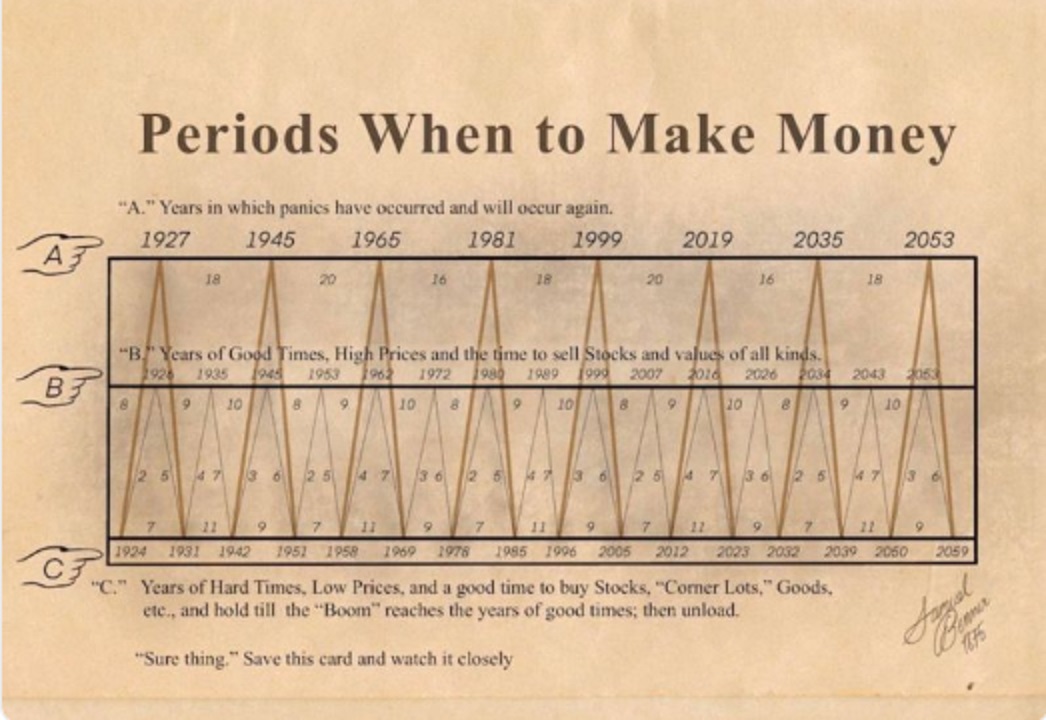

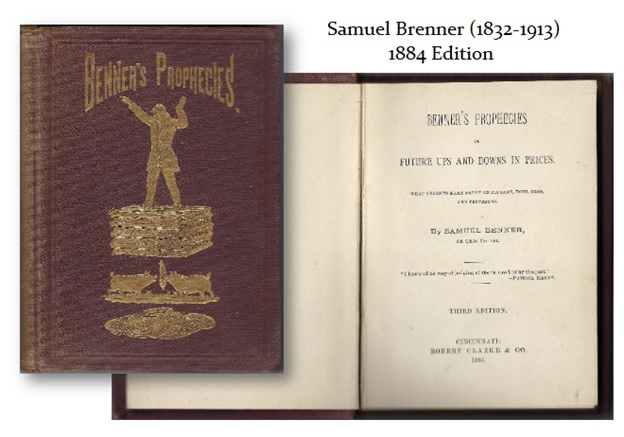

COMMENT #4: Martin; is this chart real that people are sending around claiming it was Benner’s work?

Mat

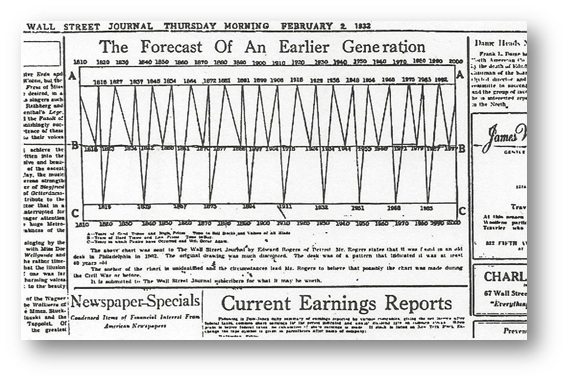

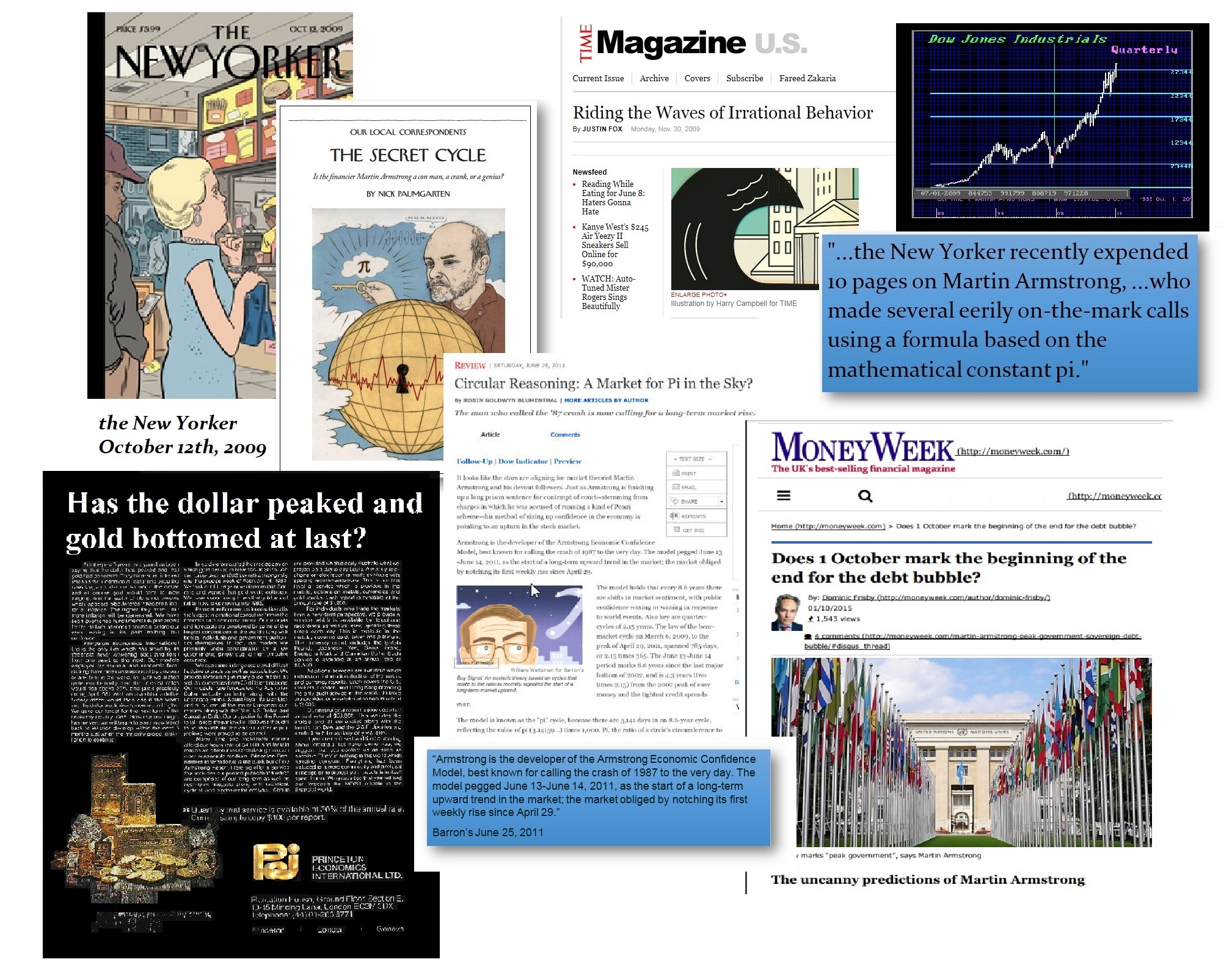

ANSWER: As far as this chart of Brenner’s Cycle being real, the answer is no Someone has made it up and signed his name. They have at least extended his cycle correctly. The last time someone tried that they skewed the cycle to make it look like it forecast the Depression 1932 low.

When the WSJ published it, it showed 1932 instead of 1931. Brenner did not extend this out in this manner. What is important to understand is that Brenner was a farmer and farmers understand the cycles in nature. Economists and governments pretend they can smooth out the cycle and eliminate the booms and busts.

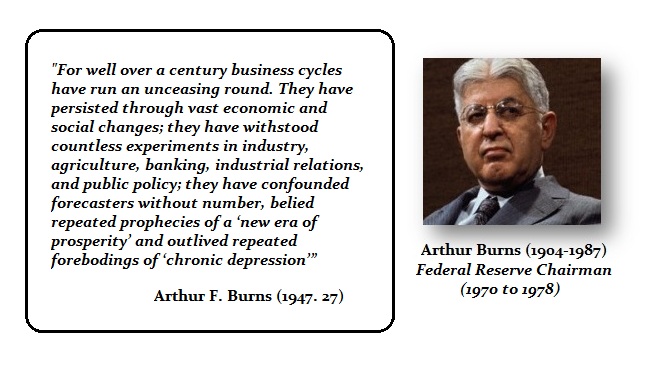

The business cycle always wins as both former chairmen of the Federal Reserve conceded – Arthur Burns and Paul Volcker.

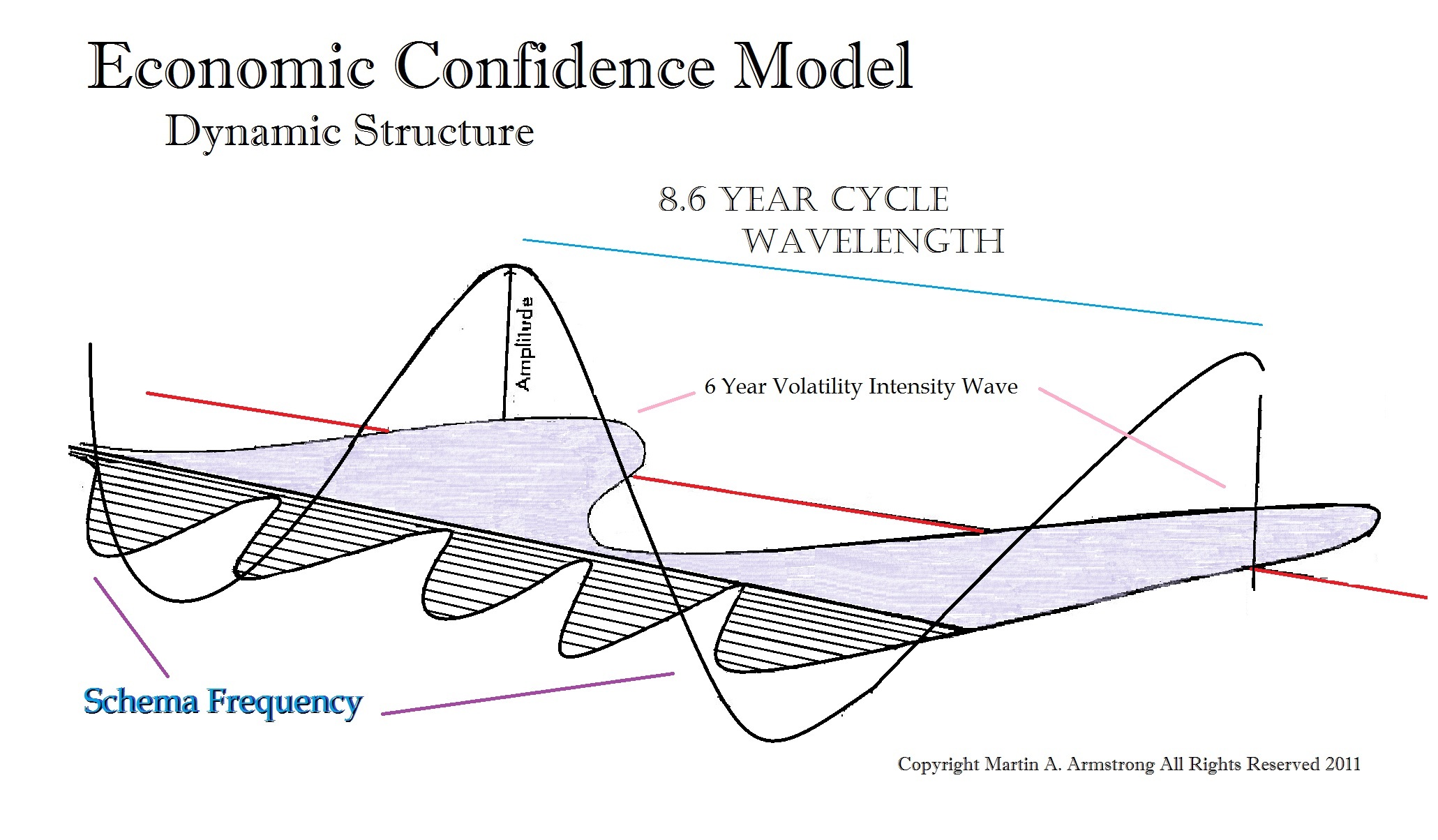

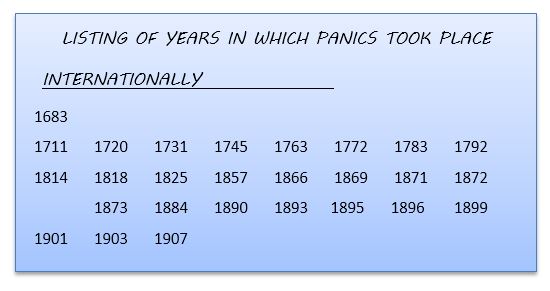

Back during the 19th century when Brenner was observing the business cycle, it was still based on commodities. Kondratieff took the same data. I believe the reason WHY the Economic Confidence Model has been so accurate is that it was based on a list of Panics – not one sector of the economy. Therefore, the ECM incorporates weather as Brenner and Kondratieff did by using the commodity sector. Yet just that the ECM was derived from financial panics, it was not based on any one specific type so it strangely seems to have incorporated the whole gambit.

Furthermore, all previous cyclical analysis was based on just a single market like stocks. They have failed because they could not account for the external influence of a contagion. The fact that this list began with the Turks’ siege of Vienna, means that the list was also influenced by war and from an international perspective.

This is a fascinating subject that I will explore in far more detail in my coming book.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

De Oppresso Liber

A group of Americans united by our commitment to Freedom, Constitutional Governance, and Civic Duty.

Share the truth at whatever cost.

De Oppresso Liber

Uncensored updates on world events, economics, the environment and medicine

De Oppresso Liber

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America

Australia's Front Line | Since 2011

See what War is like and how it affects our Warriors

Nwo News, End Time, Deep State, World News, No Fake News

De Oppresso Liber

Politics | Talk | Opinion - Contact Info: stellasplace@wowway.com

Exposition and Encouragement

The Physician Wellness Movement and Illegitimate Authority: The Need for Revolt and Reconstruction

Real Estate Lending