QUESTION: Allison Schrager at Bloomberg claimed that AI does a great job finding solutions based on existing rules and information. But it’s less suited for finding novel solutions to new problems. Somehow, this does not seem to apply to Socrates for there are no new problems anyway. Am I correct that Socrates will find new solutions?

GU

ANSWER: Yes, you are correct. However, Socrates has a database that is unprecedented and cost tens of millions of dollars to assemble. It can find solutions that are certainly not mainstream and may appear to be revolutionary but in fact, may have taken place even 2,000 years ago.

Socrates is NOT a Neutral Net. This is something I created from scratch. I put myself into this system. I had to teach Socrates how to analyze. I did not create some open AI and let it develop in some unknown manner. This is not Chat GPT where it is searching the net to come up with answers to what is the name of Lady GaGa’s dog.

Socrates has the largest financial database in the world. It has a money supply recreated from the coinage of thousands of years. It has correlated that with wars and plagues and it makes the connections. It has a database of 6,000 years which is unsurpassable. If I even tried to recreate this at today’s prices, it would be more than $1 billion.

Just on Forex Exchange, I had staff recording all the currencies back hundreds of years taking down quotes for all the world newspapers stored at the Royal Newspaper Library in London for years. Without that, we would never have been able to forecast that the pound would drop to par in 1985 when it was trading at $2.40.

What Socrates will do is it will test what attempts were made to solve crises in the past and what worked and what failed. Diocletian (284-305AD) imposed wage and price controls to try to stop inflation the same as Richard Nixon.

There was a major earthquake in Turkey that devastated the region. Emperor Tiberius issued coins to provide relief and suspended all taxes in the region to help rebuild. There have been so many different solutions that people today would never consider, but Socrates will.

Posted originally on the CTH on May 4, 2023 | Sundance

According to those who relish the Cloward-Piven strategy, things are proceeding swimmingly.

…”As long as the decisionmakers continue doing the things that are creating the crisis, the crisis will continue.”

Federal Reserve Chairman Jerome Powell said yesterday the “U.S banking system is sound and resilient,” insert uncomfortable snicker here. However, uncertainty is continuing to pummel the banking industry, despite assurances from the Fed, Treasury, FDIC financial regulators and bankers such as Jamie Dimon who are all saying there is no crisis in the banking industry.

If you want to know the big picture source of the uncertainty, it’s the great pretending. The average person can sense something is wrong, and the person who pays attention has the experience of institutional lying over the past several years. The last ten years of lying and pretending has created the biggest collapse in institutional trust in U.S. history.

Russians interfered with the election – trust us. Stick this needle in your arm, it’s safe – trust us. The FBI are the good guys – trust us. Biden won more votes – trust us. This inflation is merely transitory – trust us.

See the problem?

So, when the same voices shout, “the banking industry is sound, trust us,” well,… yeah, that suspicious cat sense that’s on high alert isn’t buying the chorus.

Reasonably intelligent people who accept things as they are, not as they would have us pretend them to be, can see the core connection to the World Economic Forum, Central Banks, and western globalist policy to change the entire dynamic of economics and finance around the “Climate Change” agenda, or Build Back Better, or Green New Deal.

Overlay that commonsense and pragmatic outlook with the logical consequences of the activity, and this banking collapse issue is a self-fulfilling prophecy. As long as the decision makers continue doing the things that are creating the crisis, the crisis will continue.

(Via Wall Street Journal) – Regional-bank stocks tumbled Thursday despite assurances from the Federal Reserve that the banking system is on solid footing.

PacWest Bancorp PACW -47.04%decrease; red down pointing triangle, which has been hit hard since the collapses of several banks, dropped by about 40%. The stock started falling in after-hours trading Wednesday evening, after a report that it was considering selling itself.

PacWest said in a statement after midnight Eastern Time Thursday that its core customer deposits were up since the end of the first quarter, and that it hadn’t experienced any unusual deposit flows since the collapse of First Republic.

[…] Investors have been wondering how much further the problems in regional-banking could spread, and whether they will spill over to the broader economy. Some analysts said the decline in PacWest and others reflected the market’s tendency to view news as categorically good or bad, rather than worries about PacWest specifically. Western Alliance, another bank whose stock has been hit hard, fell by about 35%.

[…] Regional banks, as major lenders to businesses and families across the U.S., also tend to fall when investors are expecting a recession. The 10-year Treasury yield slipped this week, and Brent crude hit a 52-week low on Wednesday.

[…] On Wednesday afternoon, the Fed said the U.S. banking system “is sound and resilient,” echoing language from its March statement. Fed Chair Jerome Powell added then that deposit flows at banks had eased and that this week’s seizure and sale of First Republic should further stabilize the industry.

[…] PacWest shares were recently trading around $3.70, putting them on track for their lowest close on record. The stock has now lost some 85% of its value since March 8, the day that SVB spooked bank investors by announcing a loss and a planned capital raise.

Many of PacWest’s customers are tied to technology startups—a tightknit clientele that pulled from high-balance accounts en masse at Silicon Valley Bank before it failed. (more)

Posted originally on the CTH on May 3, 2023 | Sundance |

If you think about Joe Biden’s 4-year term in office as an intentionally constructed single term with no limits or consequences to the cascading damage inflicted; and if you think about the ideologues behind the plan to use cognitively challenged Biden as a tool to achieve their agenda; then everything from the way he was selected in 2020, to the disconnected and fragmented policy and Biden’s interpretation of them, just makes sense.

As our friend Lee Smith summed up in early 2021, “Joe Biden is an avatar for Barack Obama’s third term.” That is what we have been witnessing. A term in office where every policy wish list and far-left agenda item could be triggered without any care or consequence of political damage.

The people behind Biden are ideologues using this unique opportunity to further the “fundamental change.” From that perspective every single granular move during the Biden term makes sense. However, this also means there’s no term two in the design. The damage will be so great, there’s no way for a second term.

Again, if you accept that background, and ignore the puppet presentations, everything currently underway that seemingly makes Biden look vulnerable and disposable makes sense. It’s not Republicans trying to take him down, it’s Democrats – who will use republicans to assist them.

Into this landscape comes the second leverage point for the removal. The vulnerability represented by Hunter Biden. This approach also explains why the Hunter Biden investigation was completed long ago, and the Deputy Attorney General Lisa Monaco/Obama-minds were simply waiting for the timing of the election calendar. Earlier today a Main Justice whistleblower provided the triggering mechanism for one removal approach. Here is another:

WASHINGTON DC – Prosecutors are nearing a decision on whether to charge President Biden’s son Hunter with tax– and gun-related violations, according to people familiar with the matter, the culmination of a four-year investigation that Republicans have sought to portray as evidence the Biden family is corrupt.

Biden’s attorneys met at Justice Department headquarters in downtown Washington last week to discuss the case with U.S. Attorney David Weiss of Delaware, according to the people familiar with the matter, who spoke on the condition of anonymity to discuss an ongoing criminal investigation. Typically, that sort of meeting — in which defense lawyers urge prosecutors not to seek an indictment of their client, or to seek reduced charges —comes toward the end of an investigation.

The people familiar with the matter said Weiss is nearing the end of his decision-making process, although they offered no specific timetable. They cautioned that the probe has taken longer than some officials thought it would, frustrating some law enforcement officials, and conceivably could slow down again before a decision has been reached. (read more)

Every single conflicting point reconciles, if you accept the Biden program was a one-term disposable effort.

The timing is up, now the removal leverage is deployed with enough time to present the branding needed for the Biden replacement.

Assets like Susan Rice are pulled from the White House. The Obama embeds position to avoid damage, and the circumstances for Biden’s removal are created by the same people who control the collection of the evidence against him.

There isn’t going to be a Joe Biden DNC nominating convention in Chicago. There isn’t going to be another presidential race by Biden; it was never the intention from the outset in the 2020 plan to use him. Biden is in the process of being excommunicated from the party. His usefulness exhausted, this is the disposal phase.

The only thing left to negotiate are the terms of the exit.

Posted originally on the conservative tree house on April 27, 2023 | Sundance

The Bureau of Economic Analysis (BEA) released their first quarter estimate of economic growth [DATA HERE] and the result of 1.1% growth shows how the U.S. economy has become dependent on government spending money we don’t have. The Gross Domestic Product (GDP) calculation is a valuation of all goods and services created within the U.S. economy, minus the value of goods and services imported.

Keep in mind that all calculations are in dollar terms. Personal consumption expenditure (PCE) prices increased 4.2% in the first quarter after increasing 3.7% in the fourth quarter. Excluding food and energy, the PCE “core” price index increased 4.9% after increasing 4.4%. Two-thirds of the increased spending on goods was driven by higher prices, only one third by consumers purchasing more stuff.

Looking at Table 2 (the percentage change by sector) the increase in prices provided 2.48% lift to the GDP but the actual purchasing of goods only delivered 1.45%. Meanwhile the decline in inventories subtracted 2.26% from the GDP, a major factor, and domestic investment has dropped subtracting 2.34%.

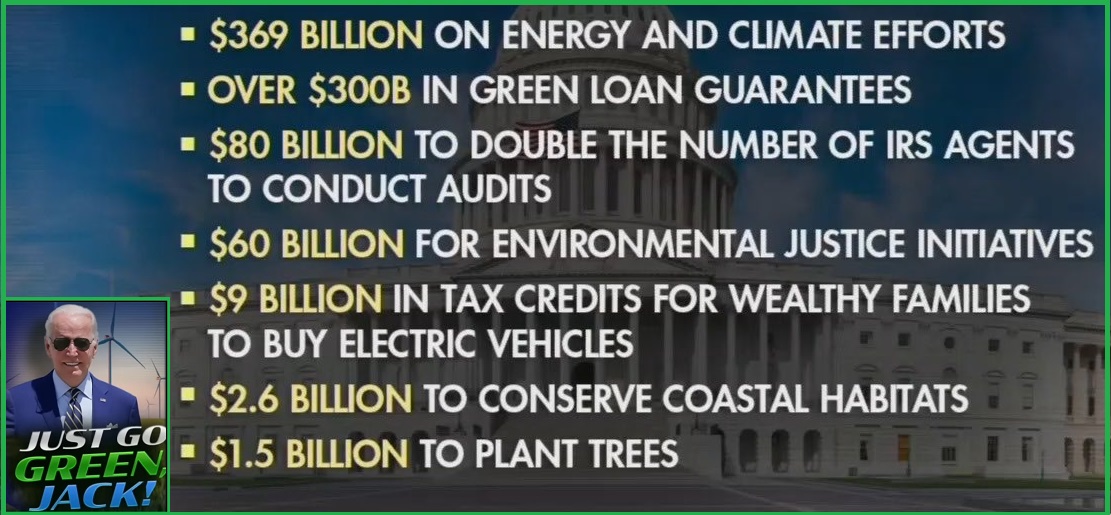

Government expenditures (+0.81) drove more than 70% of the total GDP growth as national defense spending (Ukraine War) was a major federal component. The local and state government spending increase was driven by higher wage rates. Don’t forget there’s $2.2 trillion in Inflation Reduction Act (Green New Deal) spending that is also within the economy.

Overall, this is a dark picture. Inflation is still raging. Inventories are dropping as consumer purchasing is squeezed, and replacements goods are not being manufactured. Companies are tightening their belts. The federal government is spending to try and assist the economy, but the private sector is contracting economic activity.

When households evaluate their checkbooks, a Biden administration claim of a growing economy falls flat – because the only part of the economy that is growing is the part that fuels the energy and security needs of Europe. Main Street USA is suffering through the massive inflation that Joe Biden has created, and purchases of anything other than necessities have come to a near halt.

Earlier GM cut 5,000 salaried workers and several hundred hourly jobs. Ford previously announced it would cut a total of 3,000 salaried and contract jobs, mostly in North America and India. Now, today, Chrysler parent company Stellantis announces 3,500 auto sector job cuts.

Stellantis owns the Jeep, Ram, Chrysler, Dodge and Fiat brands. Apparently, there is something in the U.S. economy that’s happening despite the great pretending….

Biden in Michigan, speaking to auto-workers, 2020

WASHINGTON, April 25 (Reuters) – Chrysler-parent Stellantis NV (STLAM.MI) wants to cut approximately 3,500 hourly U.S. jobs and is offering voluntary exit packages, according to a United Auto Workers union letter made public Tuesday.

The automaker is looking to reduce its hourly workforce offering incentive packages that include $50,000 payments for workers hired before 2007, UAW Local 1264 said in a letter dated Monday posted on its Facebook page.

Stellantis spokeswoman Jodi Tinson declined to comment. A person briefed on the matter said the figure might be lower than the figure cited in the UAW letter.

In late February, Stellantis indefinitely halted operations at an assembly plant in Illinois, citing rising costs of electric vehicle production.

The action impacted about 1,350 workers at the Belvidere, Illinois, plant that built the Jeep Cherokee SUV and resulted in indefinite layoffs. The automaker has warned it may not resume operations as it considers other options. (read more)

The Investment Recovery Act (IRA), aka “the green new deal” multitrillion spending bill, was supposed to enhance autoworkers. Funny how the exact opposite happens.

Incentive Package for Retirement: $50,000 for seniority members hired prior to the 2007 agreement.

Voluntary Termination of Employment Program: guaranteed lumpsum benefit payment and is applicable to employees with at least 1 year seniority.

.

Overall govt spending and regulatory controls drove inflation for these past two years. The ‘demand side’ was blamed, despite the lack of demand. I will be proven right when history is concluded with this. Interest rates were raised by central banks in an effort to support the policies that are driving ‘supply side’ inflation, not demand side.

Energy policy was/is crushing the consumer by driving up the cost of all goods and services. To support the overall goal of changing global energy resource and development (a false and controlled global operation), central banks raised interest rates. Various western economies, including our own, have been pushed deeper into a state of contraction by central banks crushing consumer demand, and eliminating investment via increased borrowing costs.

In short, the goal was/is to lower energy consumption by shrinking the economic activity. This, according to the BBB plan, was needed at the same time as energy development was reduced.

These economic outcomes are not organic, they are all being controlled by collective western government agreement.

Armstrong Economics Blog/USD $ Re-Posted Apr 24, 2023 by Martin Armstrong

COMMENT: Marty; I was in a board meeting and I just wanted to let you know one guy who is there simply because his family had a stake in the company with zero worldly experience, started ranting about the end of the dollar he probably read on that biased _____________________. I asked this fool, should we then move all our company funds to Russia or China since Brazil is too small of an economy? Should we stop dealing with Americans? He had no response.

Separating a fool from his money seems to be a never-ending fact about humanity.

Cheers

You are the only sane one out there these days

PY

REPLY: I know what you mean. The people promoting this BRICS nonsense have no understanding of the real world. Institutions cannot park billions in Brazil, China, or Russia. Especially in the face of war. The reason the Euro has failed as a serious reserve currency is that there is NO NATIONAL EURO DEBT! Institutions have to still jockey between the various risks of each country and all the Euro did was transfer the foreign exchange risk to the bond market. Sorry, I just do not see where the dollar is in some state of collapse.

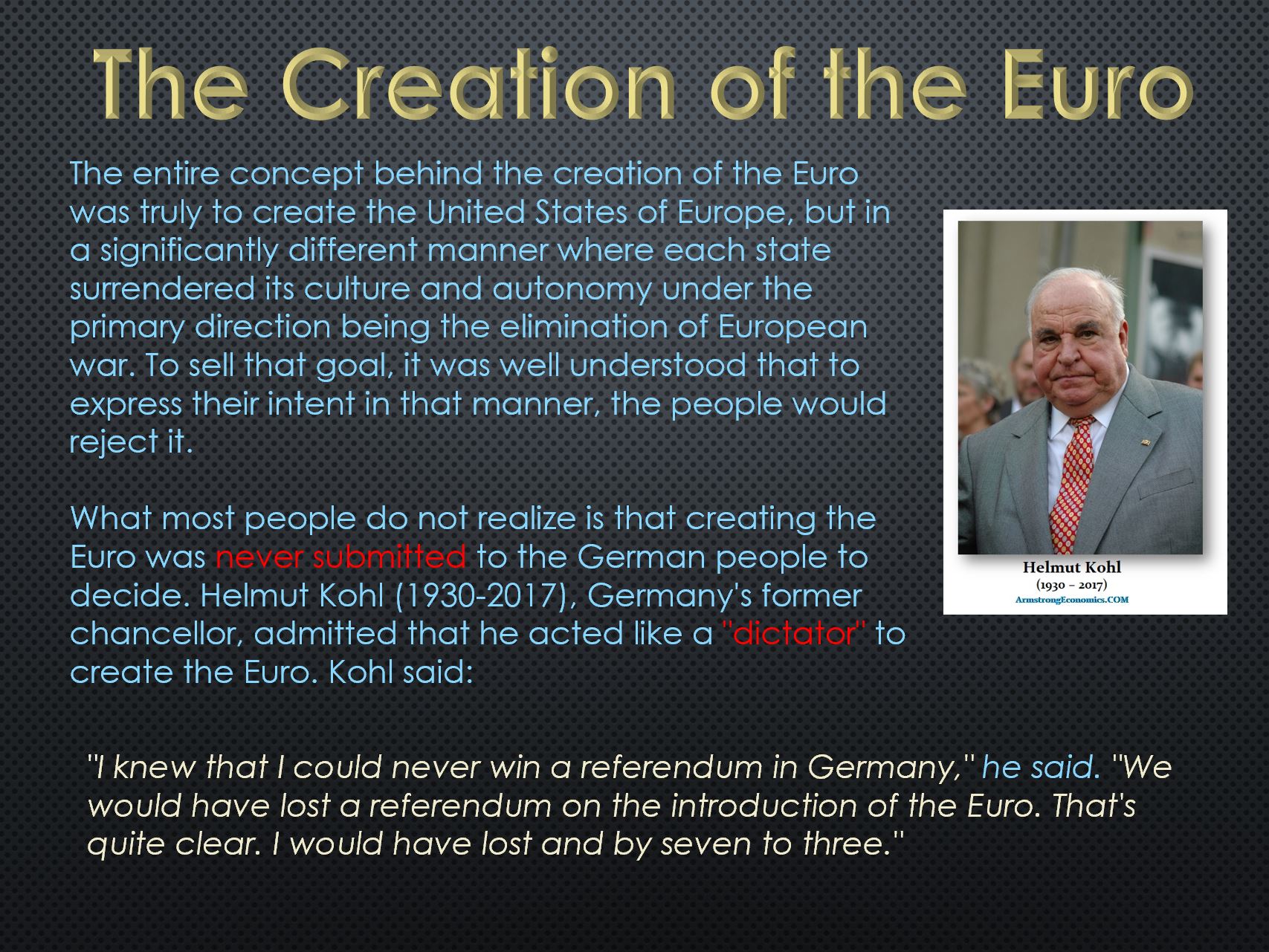

When they came to me to create the Euro, I warned them that there would be no single interest rate without the consolidation of the debt. But Kohl never allowed the German people to vote on joining the Euro, so he would not allow the consolidation of the debt. I was told then that they just had to get the Euro started and they would worry about consolidating the debts later. Of course, that never came. Hence, the volatility in FX simply moved to the debt market. The bottom line – the US dollar is still the ONLY place for major institutions to park money – PERIOD! They are not buying Brazil, China, or Russia.

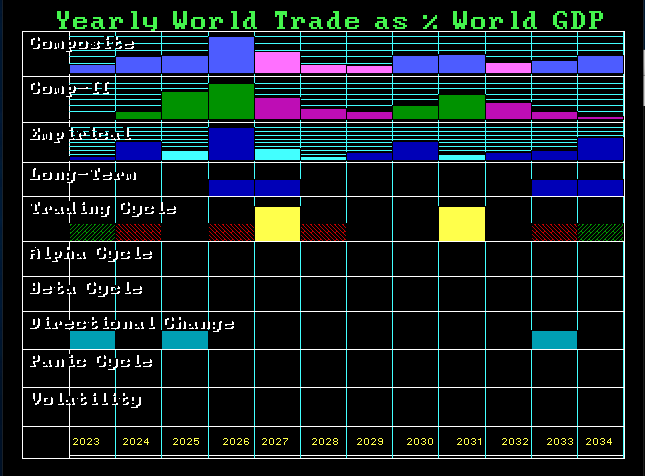

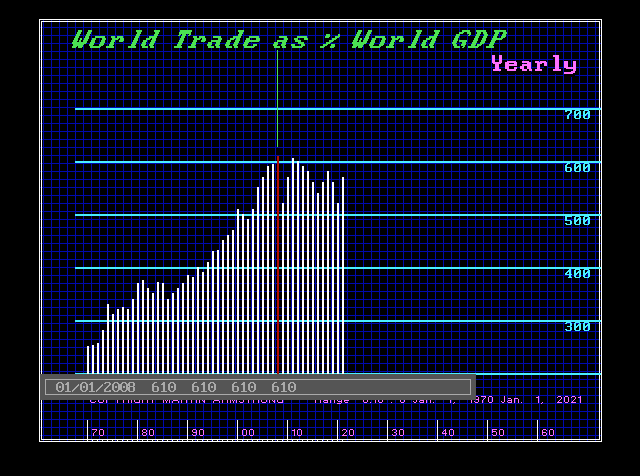

World Trade as a percent of total world GDP PEAKED in 2008 at 61%. It has been in a bear market that will not bottom before 31.4 years taking us into 2040. The sanctions on Russia have divided the world economy and killed SWIFT but it has also ended globalization. To think that the BRICS can replace the dollar with ZERO capacity for international capital to park in such markets is the delusion of absolute fools. China will surpass the USA, but only after 2032.

So here we go again. This nonsense is leading unsuspecting people to follow the piper to divest of dollars and move into what exactly? Most of this is propagated by the gold bugs who will NEVER listen. They hate the dollar because they think gold will rise then. What kind of a world will exist if their doom and gloom were a reality? You might not have any place to spend your wealth. I own gold NOT as an investment, but because of its neutrality.

There is such a major fraud going on with digital currencies with people reporting that the latest scam is using social media to tell people to transfer all their cash to a digital wallet, and BTW – here is the link! If you believe that one, perhaps you would like to buy the Brooklyn Bridge. NYC has a deficit and they will sell it for all the money in your savings. Wake up!

These people remind me of the famous drawing of a fool and his cat.

Reposed from Armstrong Economics Blog Posted Apr 25, 2023 by Martin Armstrong

QUESTION: Mr. Armstrong, Your knowledge and database on financial crises is really unprecedented. I googled the first banking crisis and it brought up only the Crisis of 1763, which started in Amsterdam. Yet that list published in the WSJ which showed 1683 as the first panic and the siege of Vienna was most interesting. I know you have written about the sovereign defaults on the ancient central bank in Delos. My question is, was there any major financial banking crisis between antiquity and 1683? I figured if anyone would know, he had to be you.

PF

ANSWER: As the 13th century unfolded, the cost of endless Crusades burdened both the crowns of England and France. Throughout the remainder of the 13th century, a variety of Crusades were aimed not so much at toppling Muslim forces in the Holy Land but to combat any and all groups seen as enemies of the Christian faith. Edward began his reign in 1275 with heavy debts incurred from the Crusades.

These endless wars resulted in the time of major sovereign defaults by Edward I of England and Philip IV of France. In 1275, Edward secured a financial monopoly and negotiated a grant of export duties on wool, woolfells, and hides that brought in an average of £10,000 a year. He then used this as collateral to borrow substantially from Italian bankers granting them the security of these customs revenues to fund his endless wars of aggression.

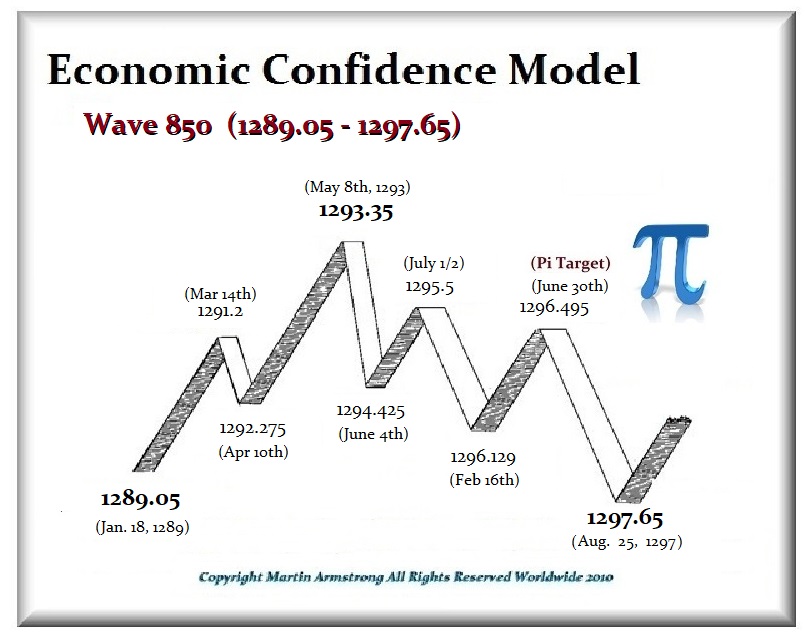

Edward imposed heavy taxes on the value of movable goods. At the beginning of this Wave 850, Edward defaulted on his loans from the English Jewish bankers, and then as 1290 began, to cover that default he expelled all of the Jews from England and confiscate all their property.

Moreover, this was the Edward Langshakes of the movie “Brave Heart” when in 1291 he attacked Scotland. As this 8.6-year Wave 850 peaked, Edward launched his very costly war against Philip IV (1295-1314) of France which lasted until the end of this 8.6-year wave came to an end in 1297.

The Riccardi of Lucca was perhaps one of the major international merchant banking houses to emerge during the 13th century. The Riccardi established branches in Rome, Bordeaux, Paris, Flanders, London, York, and Dublin, Ireland. They engaged in trade with Edward I of England. Prior to 1272, the English kings were customers of the Italian merchant who had exotic imports as they were purchasing luxury goods and would use them to transfer money to Rome. With the outbreak of war against Philip IV in 1294, a major credit crunch and inflation erupted which impacted the entire international money markets throughout Europe at the time. The value of gold rose against silver from 10:1 to virtually 15:1, which was a monumental distortion of the European monetary system as a consequence of these endless wars.

Cash-strapped, Edward sought financial support from the Riccardi establishment but they refused to lend him any funds. In response, Edward seized all of Riccardi’s assets in England, effectively bankrupting them. The Riccardi had derived significant benefits in dealing with the English monarchy. They held contracts with special access to the English wool market. The Riccardi banking establishment was involved in about 50% of all the forward contracts with English wool producers, which were in effect futures contracts in the cash market. When Edward confiscated all the assets of the Riccardi, his action backfired. Nobody else would then deal with England in international money markets. This led Edward I to impose heavy levels of domestic taxation, which led to civil unrest. This led to a constitutional crisis of 1297.

We all may know that Magna Carta established rights that were forced on King John on June 15th, 1215. After John’s death, the regency government of his young son, Henry III, reissued the document in 1216, but it removed some of its more radical content. This led to civil unrest and at the end of the war in 1217, it became part of the peace treaty when it acquired the name “Magna Carta.” Henry III was compelled to reissue the charter again in 1225 in exchange for a grant of new taxes. Edward I was his son who was then once more compelled to reaffirm the Magna Carta in 1297 at the end of the 8.6-year Wave 850. That is when Edward I was forced to confirm that the Magna Carta was England’s statute law. That is when it actually became England’s rule of law.

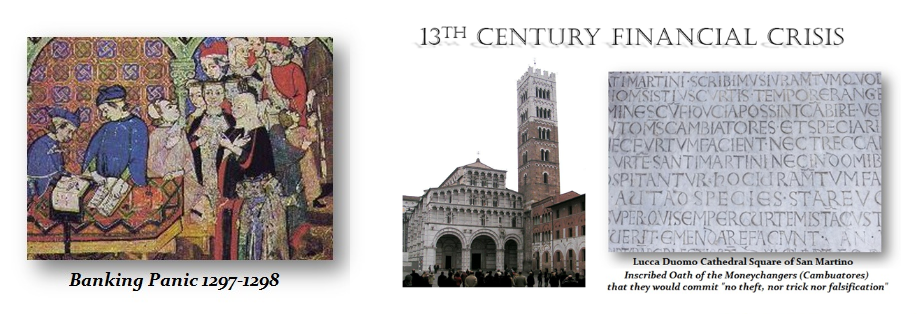

The Bonsignori bank was known as the Gran Tavola, which had become the most powerful of the Italian merchant banking firms throughout Europe between 1255 and 1298. The Gran Tavola was indeed the greatest bank of the 13th century with branches in Paris, Marseille, Genoa, Bologna, and Pisa in addition to the main office in Siena.

Philip IV of France was also strapped for funds. He chose the debasement of the coinage which was massive. Philip had no other course of action to meet the expenses of the war. He began as a massive debasement of the coinage. Silver began to migrate out of France. This debasement only accelerated after 1298 when Philip IV confiscated all the assets Italian bank known as the Gran Tavola in France on claims that they owed him money, without netting anything with respect to his loans owed to them. This caused a major banking crisis in 1298 with the collapse of the institution which also held funds for the Papacy resulting in their loss of 80,000 gold florins. This was the first Banking Panic post-Dark Age. This confiscation of assets wiped out Siena and the city never again rose to the forefront of European commerce. By 1320, Siena was no longer a significant city in international commerce whatsoever which was a direct attack on the Papacy by Philip IV. This resulted in shifting the banking power to Florence.

A full-blown financial panic unfolded as silver migrated overseas. People hoarded the old currency and by 1301 there was virtually no silver remaining in the open market in France. Currency depreciation let Philip cover the cost of the war but it destroyed the credit of France and that ultimately led to France seizing the Papacy and strip-mining all its assets moving the Church to Avignon where a French Pope was installed. They then seized all the assets of the Knights Templar and burned all resistance alive. The Knights Templar were effectively an international transfer agent. If you were in France and needed to pay someone in Italy, you gave the money to the local office in France and they instructed the brank in Italy to pay. It was a 13th-century version of a wire transfer service. That is why the French crown seized the Knights and strip-mined all their wealth as well.

Obviously, this banking crisis of 1298 was far beyond anything most people would have read about in a financial crisis. This is what I mean when I warn that those in power will do WHATEVER it takes to retain power, and religion never means anything at the end of the day.

People often ask if their money is safe in a regional bank. Yes—if you keep it under $250,000 to guarantee the FDIC insures those funds. Some clueless minds brainwashed into fighting the class warfare thought, “Oh well!” for people who had more than them in the bank and did not care if the Silicon Valley Bank or Signature Bank failed.

My phone did not stop ringing and the bankers wanted to know if they should cover ALL the deposits. I actually lost my voice, screaming, “YES YOU MUST COVER ALL THE DEPOSITS! ALL OF THEM!!!” Aside from the fact that no one deserves to lose their hard-earned money, the primary issue here is that failing to cover the deposits would have completely wiped out small businesses.

Small businesses comprise 70% of GDP and must be protected at all costs. They must park large sums in the bank to cover payroll to pay their employees and operational costs. Small businesses would come to a standstill and banks would fall like dominoes. Unemployment would spike and the entire economy would plummet. We would see a massive banking crisis if all small businesses went under. More banks will go broke, it is only a matter of time, but it is crucial that deposits are covered

Posted originally on the CTH on April 20, 2023 | Sundance

Stop looking at the Washington DC Potemkin village; start looking at the financial system behind it that controls it.

You may recently have seen this story:

WASHINGTON DC – Homebuyers with good credit scores will soon encounter a costly surprise: a new federal rule forcing them to pay higher mortgage rates and fees to subsidize people with riskier credit ratings who are also in the market to buy houses.

The fee changes will go into effect May 1 as part of the Federal Housing Finance Agency’s push for affordable housing, and they will affect mortgages originating at private banks across the country. The federally backed home mortgage companies Fannie Mae and Freddie Mac will enact the loan-level price adjustments, or LLPAs.

Mortgage industry specialists say homebuyers with credit scores of 680 or higher will pay, for example, about $40 per month more on a home loan of $400,000. Homebuyers who make down payments of 15% to 20% will get socked with the largest fees. (read more)

If you focus on the DC Potemkin Village, you view this move through the prism of Biden’s FHFA creating a policy to favor low-income (nonwhite) voters by punishing stable credit worthy borrowers. That’s what the powers who control the levers, and create policy, want us to focus on. That’s not what is going on.

Biden doesn’t control anything. Biden is a puppet to the multinationals that control DC policy. When Biden was installed, the people who control the money and wealth (Blackrock, WEF assembly etc.), the people behind the Potemkin Village, knew what the larger economic agenda would create.

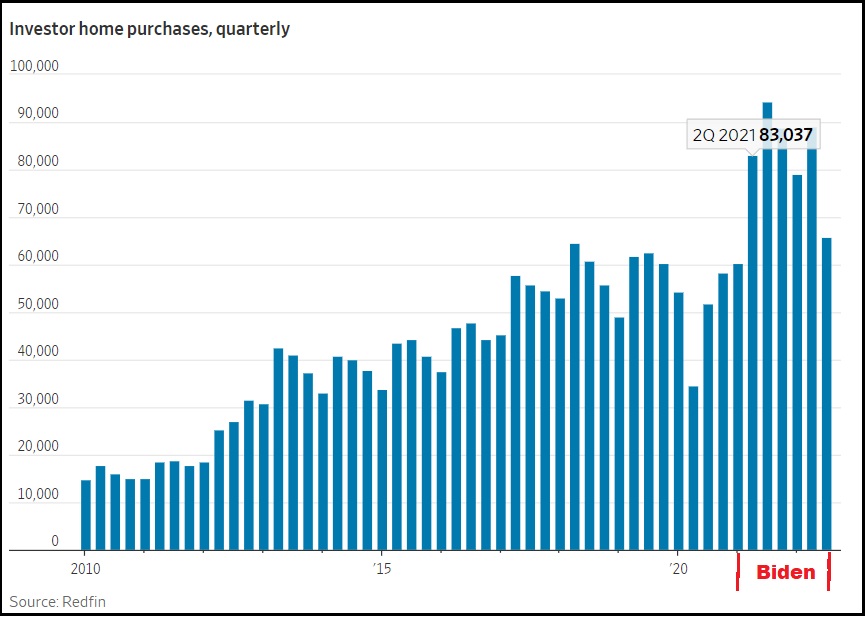

They knew BBB, or Green New Deal policy, combined with excessive govt spending would generate inflation. They moved their money from inflation sensitive liquid and paper assets, into real estate. Inflation raged, liquid assets depreciated, real assets (real estate) surged. 25% of housing was bought with investment dollars by institutional investors, housing prices skyrocketed – their investments increased accordingly.

The financial control operators avoided the consequences of the government policy they controlled.

Now, those same institutions need to turn those appreciated real estate assets into capital outcomes. They need to sell the real estate. However, the assets are now at maximum appreciation and dropping as a result of the central banking moves to raise borrowing rates.

How do they exit the investment? They need a mechanism – a new policy to create the financial instrument that transfers the increased investment wealth back into their hands.

They need buyers.

How do they get buyers? They create new policy.

That’s what is behind this new FHFA rule. Fannie Mae and Freddie Mac will create a new category of buyers that allows the investors to sell the real estate assets at higher appreciated values and exit their investment. They will transfer the depreciating loss of the asset to the new buyers, like a game of hot potato.

Learn to look behind the Potemkin Village to the institutional financial operators who control the laws, rules and regulations. This is all a continual game of wealth transfer and redistribution. There are trillions at stake.

Look at who moves the money around and how they position govt policy for the shifts into and out of the financial system they control. All of this is being controlled, and Joe Biden has no idea what is happening beyond the talking points that are put in front of him.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America