Armstrong Economics Blog/The Hunt for Taxes

Re-Posted Jan 17, 2019 by Martin Armstrong

COMMENT: Hi,

The Norwegian Data Protection Authority is now arguing that GPS based taxation, for the amount of kilometers driven by car, can be done within 5-6 years! Norwegians trust the government way too much, because they believe that this system will eliminate the need for road tax, fuel tax, toll roads and reduce the cost of car insurance.

No way will the tax be reduced! GPS based taxation is a governments dream! Who is to stop them from issuing parking fees or speeding tickets?

Norway also has a high number of electric cars, and an electric car is sold without any tax or VAT, has reduced road tax, free of reduced toll road passage and does not contribute to fuel taxation. With GPS active, the government can finally collect taxes from electric cars without the messy environmentalists meddling.

In the worst case, a corrupt government can use the system against its people to create implications, push the burden of proof over to a troublesome citizen, in court.

Norway may be a great country regards to statistics, but will be some kind of self-imposed totalitarianism if this nonsense continues. Stay away from Norway if you cherish your hard-earned cash!

And as always, thank you, Mr. Armstrong, for your service and enlightenment.

AA

Ex-social democrat

(see source #1)

REPLY: The political-economic system post-World War II has been a socialist driven agenda. “Vote for me and I will give you other people’s money.” This system cannot be sustained when those in power have promised themselves pensions. As government workers retire, they need to be replaced. The growth rate of government has started to explode. Instead of looking at the problem objectively, they are simply looking from paycheck to paycheck on how to meet the next payroll. This leads them to become more and more aggressive in hunting things to tax. Any rational person would look at this economic model and see it leads to massive civil unrest. They pretend that socialism is to help people, but they come first. As this gets far worse, nothing trickles down to the people.

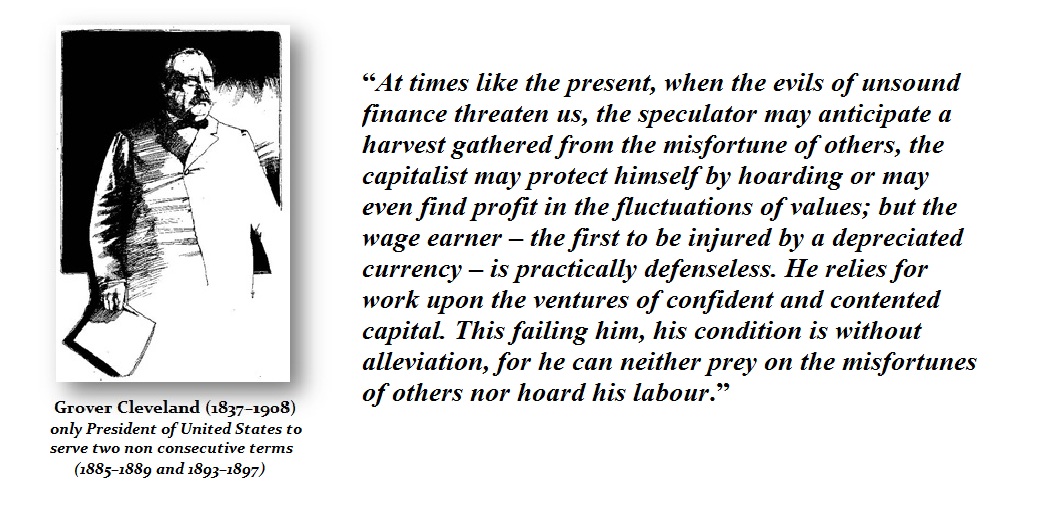

Even former President Grover Cleveland, who was a Democrat, saw the insanity his party unleashed with the Silver Democrats. Taxing the rich does not present a solution. They will simply leave. The rich, through their investments, create jobs. This proposal to use GPS to track movements for taxes will allow the government to end tolls, and thus reduce their own workforce and pension liabilities. This has been the very idea behind E-Z Pass in the USA where you drive through tolls and are automatically charged.

Then we have the legislative branches who spend whatever they need and look to the central banks to manage the inflation they themselves create. They take no responsibility for their own actions. This places the central bank between a rock and a hard place. Trump was bashing the Fed over its rate hike while he fails to understand the crisis we are in thanks to Larry Summers. The Fed has to choose between Fiscal Policy and its own monetary policy or Fed Policy. It raises rates to deal with the crisis of excessively low interest rates and then the budget deficit increases as the cost to keep rolling the debt grows exponentially.

Then we have the legislative branches who spend whatever they need and look to the central banks to manage the inflation they themselves create. They take no responsibility for their own actions. This places the central bank between a rock and a hard place. Trump was bashing the Fed over its rate hike while he fails to understand the crisis we are in thanks to Larry Summers. The Fed has to choose between Fiscal Policy and its own monetary policy or Fed Policy. It raises rates to deal with the crisis of excessively low interest rates and then the budget deficit increases as the cost to keep rolling the debt grows exponentially.