COMMENT: Mr. Armstrong, I just wanted to say thank you so much. I was listening to the perpetual gold analysts for years who never changed their tune. It was always buy, buy, buy, and the dollar would go to zero any day now. They always looked at the Fed and the balance sheet, and when they were wrong, they blamed the bankers for manipulating gold.

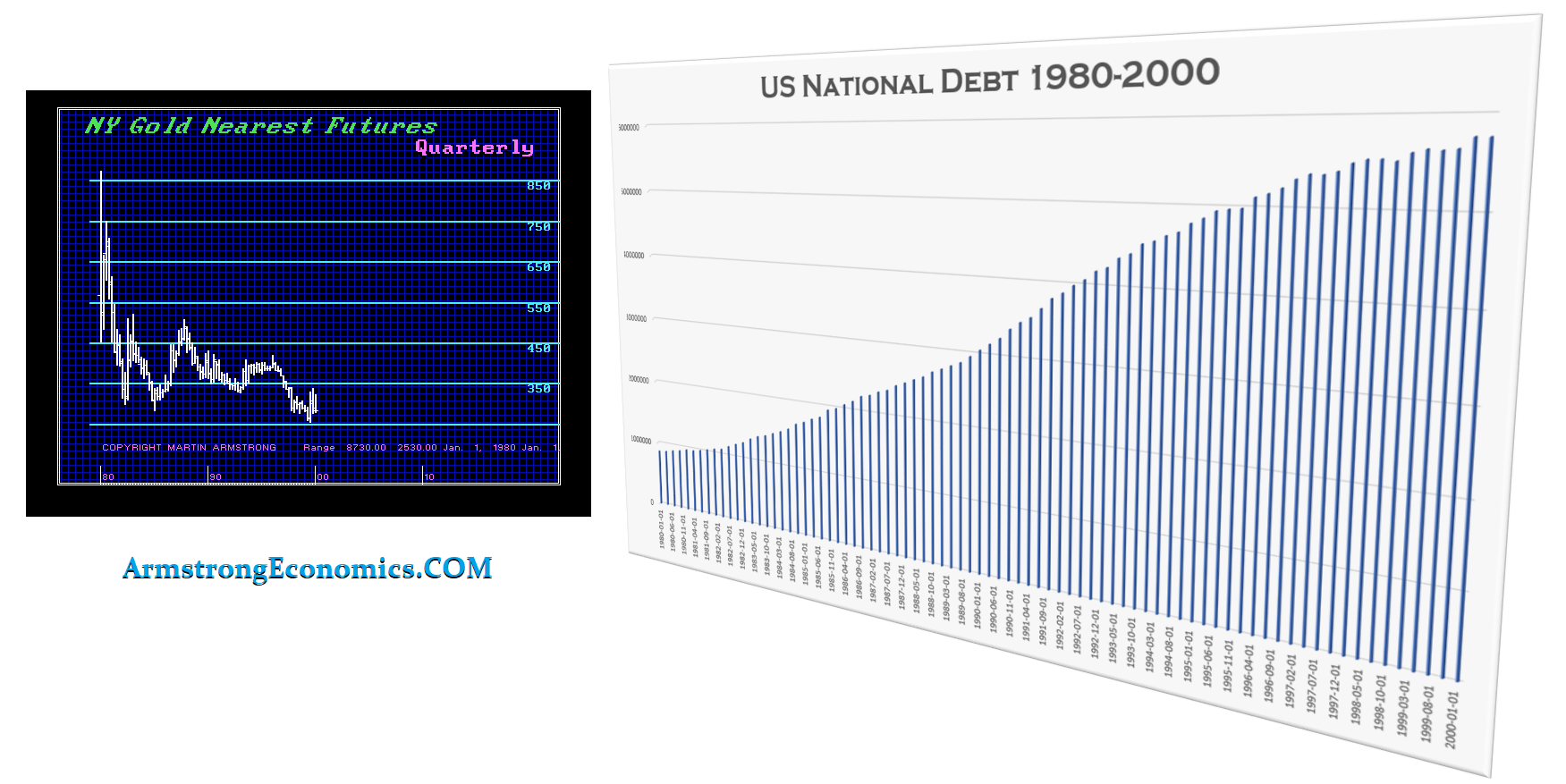

I sold out in 2013, and you said gold would decline for two years. It did not crack $1,000 as you hoped, but it elected two monthly bullish reversals within two months of that low, and you said it would rally to test $2,000. You also projected that the stock market would outperform gold, and contrary to all the gold bugs, you said they would rise together. Nobody made that forecast.

I had two friends who did not listen to you. They took home equity loans to buy more gold and did not sell in 2013. The gold bugs ruined the marriages of my former friends, and both lost their houses. We no longer talk because they lost everything when I followed you. The stock market did much better. People need to understand that when you forecast the world, you see things are all connected.

Thank you so much for the education.

ED

REPLY: I am glad you understand that you cannot forecast a single market to the exclusion of everything else. The world economy is all connected. As I have said, without World War I & II, the USA would still be an agrarian society. The capital shifted, transforming the USA into the world’s financial capital. The problems with the goldbugs’ view of the world is that:

They have broken rule #1 of investing – NEVER MARRY THE TRADE.

They are prejudiced by old economic theories that have not been updated since the 16th century.

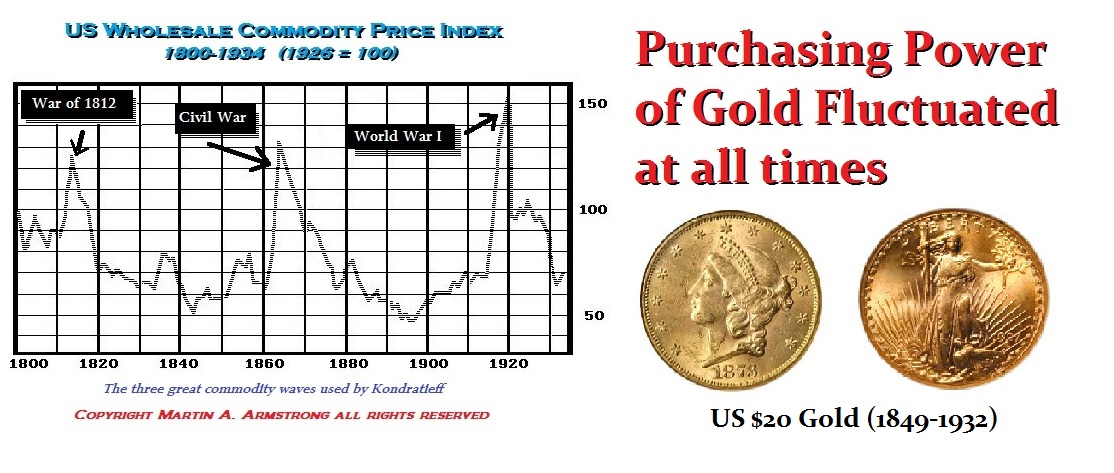

When Sir Thomas Gresham (c. 1519 – 1579) devised his Law that bad money drives out good, the metal content determined foreign exchange on the Amsterdam Exchange. Today, the backing of a currency has returned to the days of the Roman Empire. Rome was militarily superior, as is the case of the United States, when it became the #1 military power after WWII. Yet more importantly, Rome had a consumer-based economy, so everyone was proud to be Roman, for it gave them access to the largest consumer market in history. The Emperor Marcus Aurelius (161-180 AD) had even sent an ambassador to meet with the emperor of China. The United States currency is NOT backed by gold or any commodity. It is supported by a consumer-based economy, the same as Rome.

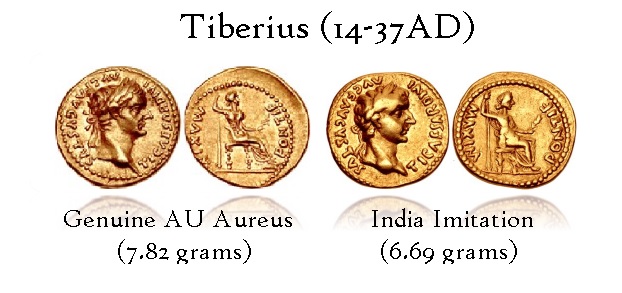

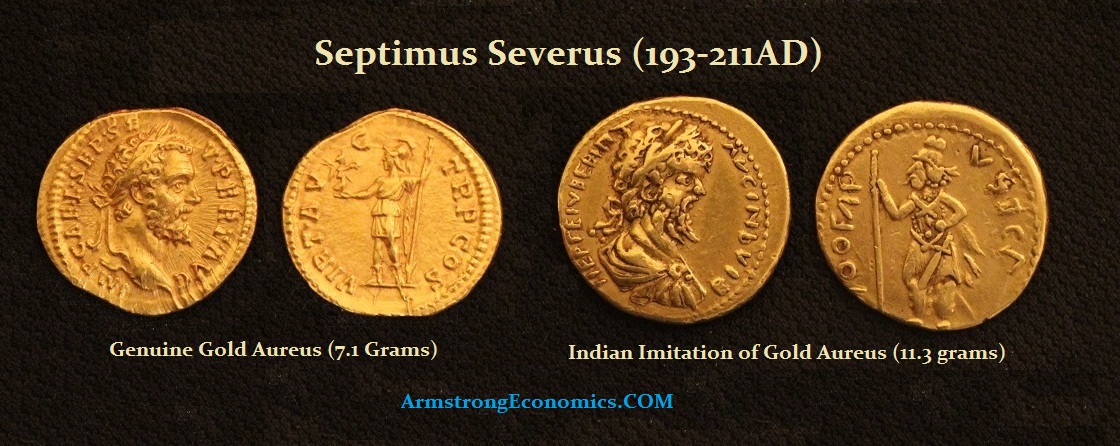

India traded with Rome. That is where the silk from China moved through India to Rome. However, India was also the supplier of dyes and spices. Rome’s coinage was worth more than the metal content of the time of Gresham during the 16th century, for there was no significant military power nor a consumer-based economy. For over 200 years, Southen India imitated Roman gold and silver coins; at times, they even weighed more in gold than genuine coins.

Here we have an imitation gold aureus of Septimus Severus (193-211AD), which weighs 11.3 grams compared to 7.1 grams for a genuine Roman aureus. That meant that the Indian imitation was nearly 60% heavier. The coinage had a premium because of the consumer-based economy in Rome, and that attributed a premium to the coinage that had NOTHING to do with the metal content. Southern India NEVER issued their own gold coinage. They imitated that of Rome. Today, many emerging markets use the US dollar and borrow in dollars.

The world has changed – I hate to tell them. The old theory of the Quantity of Money does not hold up under any correlation. The nonsense that gold rises with inflation has ruined many and bankrupted others. The central banks have used this theory supported by Keynesian Economics, and it has utterly failed. We have ballooning national debts thanks to Austrian Economics, which propagated the idea that borrowing rather than printing would be less inflationary because you were not creating more money – you were supposed to be draining the money supply. Everything is connected. If a foreign investor buys property in the United States, his money, be it in euro, yen, or yuan, is converted to dollars, and the domestic “real” money supply increases, for the seller, now has that cash to spend. This is not accounted for in any of these antiquated theories.

It is time we reassess how the modern economy of the 21st century truly works. Currency pegs, gold standards, and schemes like the G5 Plaza Accord, which tried to lower the value of the dollar to reduce the trade deficit being oblivious to the fact that they also lowered the value of foreign investment in the dollar, have done nothing but create confusion and economic chaos. Central banks have nothing other than the old-fashioned 16th-century theory of the quantity of money to play with.

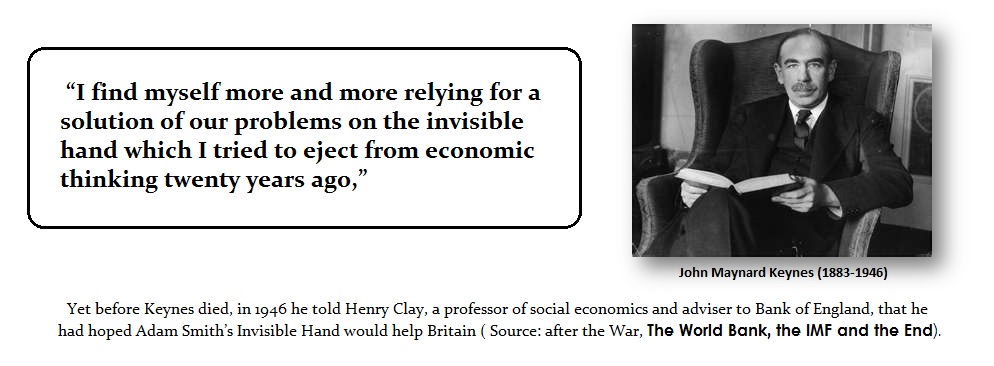

Keynes added to the chaos by advocating, like Marx, that the government had the power to control the economy. Keynes advocated the end of Laissez-Faire in 1926. Yet, before he died, Keynes admitted that he was wrong. Nobody paid attention because once the government seized that power, they refused to hand it back to the people.

Gold is NOT a hedge against inflation. It declined for 19 years after 1980 when inflation rose, as did the national debt. Gold is a hedge against the government. That will be why it will make new highs on the 4th run – not because of the Fed or the CPI.

I am finishing up a new book on this crisis in theory. Not only have the godbugs been wrong, but so have the central bankers and those in government. It is time we take a closer look at how things truly function that apparently, like Thomas Gresham, it takes someone to observe reality from a trader’s perspective.

The US housing market has not been this unaffordable since 1984, a new study finds. Analysts at Black Knightanalyzed home prices, income, and interest rates on a monthly basis going back to 1975 and found that the average mortgage today would cost $2,423 per month on a 30-year fixed with 20% down. This marks a 91% increase in housing costs over the past two years alone.

The $2,423 figure represents 38.3% of the median household income, despite home ownership costing only 24% of the median household income for the past 25 years. This study does not take into account that many do not put down the 20% downpayment due to rising closing costs, insurance costs, and taxes. The current 30-year fixed mortgage is around 7.23% at the time of this writing, marking a 20-year high. For housing affordability to reach 24% of the median income, the average household would need to earn 60% more or home prices would need to decline by 27%.

Home prices are at their highest level in 30 of the 50 largest metros. People are continuing to flee to more desirable areas for financial and political reasons, and with historically low inventory, prices will not decline any time soon in those areas.

Worse still, 344,000 US homeowners owe more than their home is worth, which is a 70% uptick from last year. In Florida, insurance rates alone are causing many longtime residents to flee. I will discuss that in more depth in another post. The housing crisis is in full swing, but this is by design. The globalists have said countless times that they want the world to become perpetual renters who own nothing. Never before has the average man had to go to battle with investment firms to own a piece of the American dream.

I reported previously that a dealer I knew suddenly had his credit line closed. I have warned that besides banks preparing for the coming CBCDs closing local branches in the USA as well as in Britain, I seriously question if they will allow people to buy precious metals and use cryptocurrencies post-CBDC. This is about control, and they want to shut down what they view as the underground economy, which they estimate is 20%-35%, and this is about increasing their taxation to automatic theft. This is the net result of Direct Taxation, which the Founding Fathers warned would happen, so they prohibited any form of Direct Taxation in the Constitution. The Socialists seized power and pushed for the income tax in 1913, and that has been a slow grinding process that led to eventually owning nothing and being very miserable – not happy.

Welcome to the Tyranny of Republics that NEVER Represent the People as History Warns

QUESTION: Marty, How the hell are you? It’s been too long. This case of charging manipulation of precious metals being “spoofing” is the end of the free markets. This eliminates the locals, and trading will never be the same. I remember when the lawyers over the insider trading cases with Michael Milken came to you, and you wrote about that back then and how they turned it upside down. Do you think turning spoofing into manipulation is the death knell of trading as we head into 2032?

Pat

ANSWER: Yes, it has been a long time. I don’t know how you trade size anymore. I would not want to trade a major fund in this atmosphere. I probably should explain why Milken and all those charged with insider trading were really innocent. During the Great Depression, insider trading was defined as a director who knew the company would go bankrupt, and he sold his shares BEFORE releasing that information. That is what REAL insider trading indeed was.

The problem with our law is that a prosecutor gets to create a new theory of the law and then charges you, and it can be precisely the opposite of what the law was intended to do. I saw them charge Muslims after 9/11 with money laundering because they paid off one credit card with another. That certainly was not the intent of money laundering. If you have cash now, they will consider it money laundering because you are trying to avoid taxes.

The theory they used against Milken was that, let’s say, you and I intend to take over General Motors. The legal theory was that we defrauded the person reading this from the same OPPORTUNITY to make money. They did not lose anything. They turned inside trading upside down. The various lawyers came to me because I had written about what real inside trading was back in 1986.

Trading has always been just a poker game. When I would call a bank for a quote, they would always try to read what I would do and move the spread in that direction. Sometimes, you have to pretend to be a buyer if you really have the size to sell. If “spoofing” is now manipulation, trading is finished. You cannot call Goldman Sachs and say, gee, I want to sell $1 billion. They will clip you.

John Maynard Keys wrote in 1926 “The End of Laizzez-Faire” which was the piece that argued that the government can MANIPULATE the economy by using interest rates to manage demand. It was the “New Economics” which completely failed. Before he died, he admitted he was wrong and that not even central banks could manipulate the trend of the economy, no less a single market. Paul Volcker, back in 1979, wrote about the failure of Keynesian Economics in his Rediscovery of the Business Cycle. I remember Paul and I had a conversation about that back in 1998.

Even Larry Summers, the father of NEGATIVE interest rates, admitted that economists cannot forecast the future trend of the economy. Absolutely NOBODY can manipulate any market that changes its direction. Yes, locals could gun for stops and move the quotes on the London Fix, so it kicks off the stops. But that does not change the trend. Those who have pushed this theory that the metals are manipulated have been wrong in their analysis. They push this theory that the metals rise with inflation when they have not done so for centuries.

Gold declined for 19 years, from 1980 to 1999, while the national debt kept rising so much for the debt and inflation theories. Gold does NOT rise with inflation – it rises with geopolitical uncertainty. And when we were on a gold standard, gold declined with inflation. Moving to some gold standard will NOT defeat the business cycle and prevent inflation. There is far more to inflation than just the nonsense of the quantity of money. Most of the theories these people push to sell their gold are false, and as a result, they then have to claim that gold has been manipulated to keep it suppressed to cover their ass, for their analysis is biased.

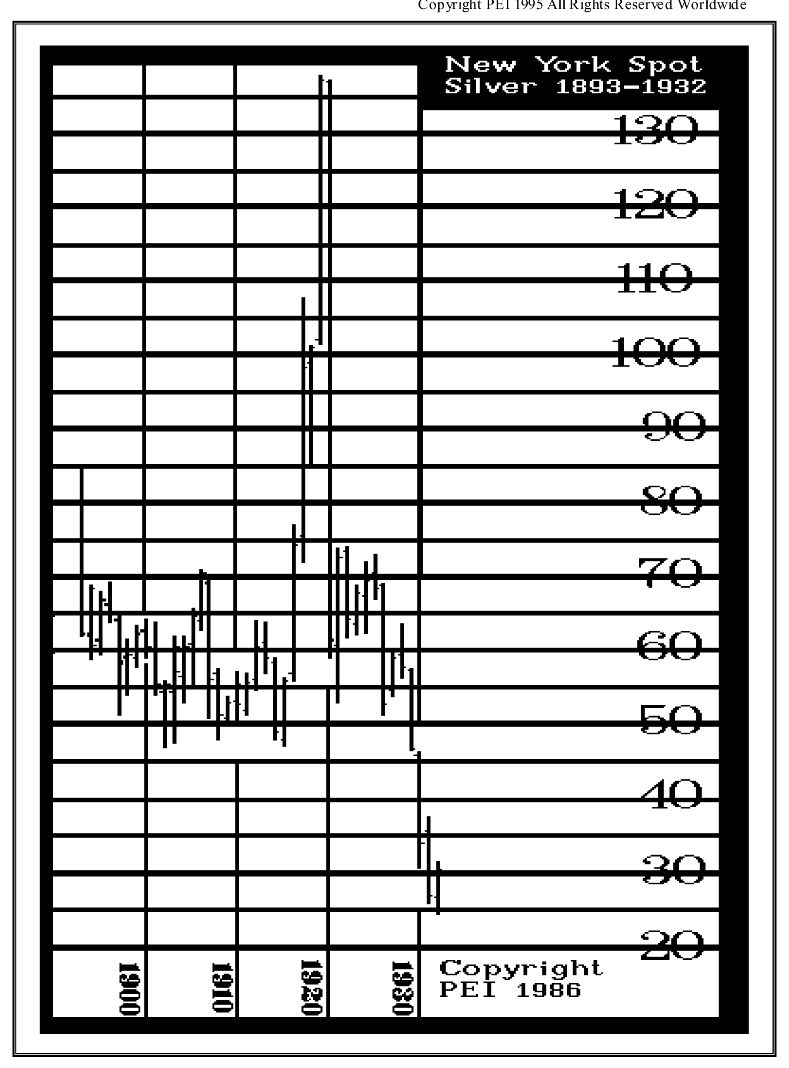

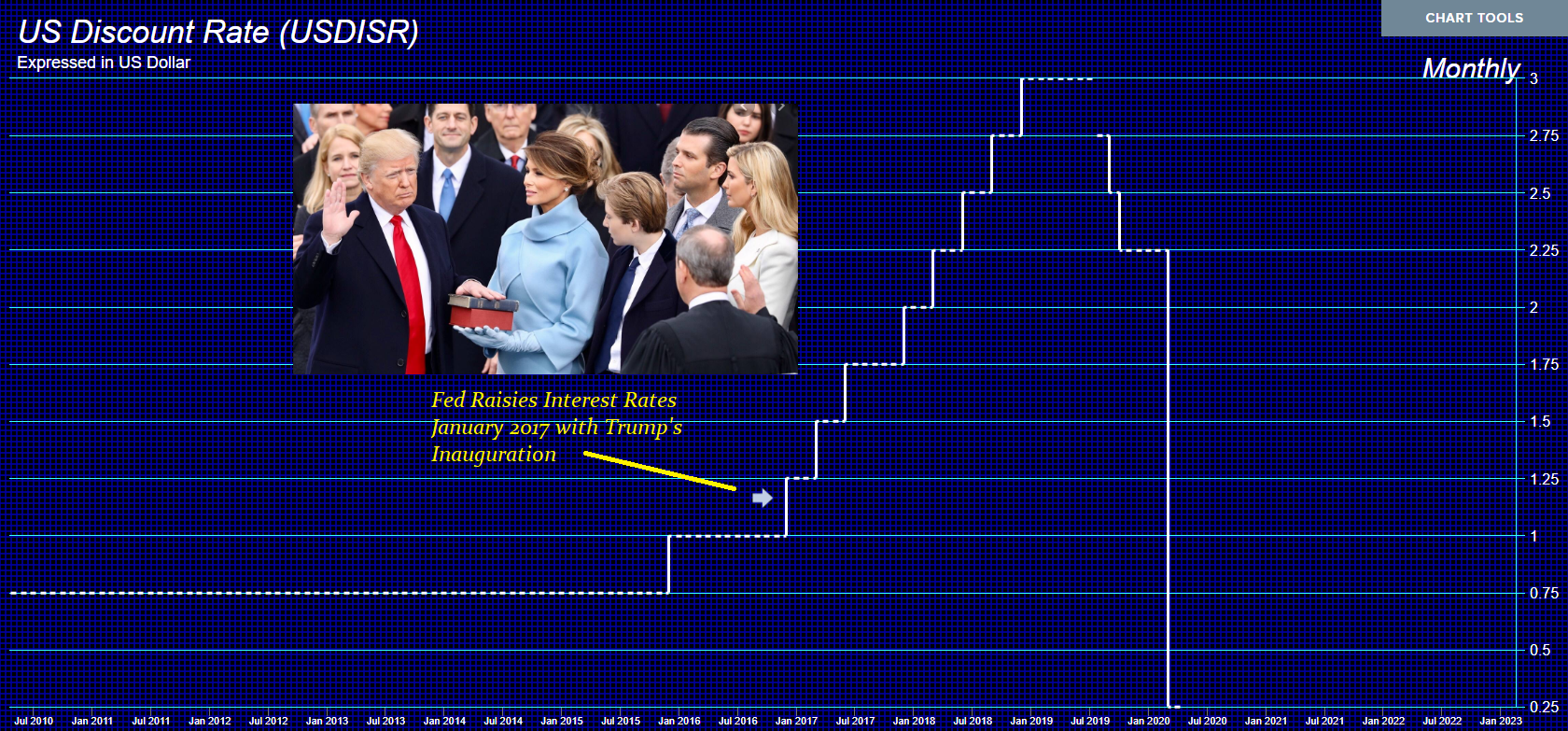

Even the propaganda they put out about the Great Depression is false. Commodities peaked in 1919 with the shortages thanks to World War I. Silver declined and made its low in 1932, with the stock market collapsing from its 1919 high. Then there is the propaganda that gold and the share market are supposed to decline because of Keynesian Economics raising interest rates. Sorry! That is also a myth and fake news, yet they preach that every time. The stocks soared, and they called it the Trump Rally while the Fed kept raising rates. Gold also rose with rising interest rates.

Welcome to the chaos and misinformation that has plagued investors since the Great Depression.

The public is not concerned about “Russian aggression,” the Trump inditement, or even the MSM wrench about aliens. No one cares — the average person is struggling to keep up with the rising cost of living. Homelessness is on the rise as people cannot afford shelter. The blank checks to Ukraine are a slap in the face of those begging for help at home. These politicians need to work for us. No one campaigning is going to make a dent in the polls unless they clearly detail how they plan to address INFLATION! And no, the problem is not limited to America. The solution cannot be a universal income, currency, or Great Reset. The economy was strong before they attempted to BUILD BACK BETTER.

Britain’s four largest banks have reported that clients have withdrawn £78 billion, marking the steepest bank run since 2018. NatWest, Barclays, Lloyds, and HSBC all reported significant withdrawals in the 12 months leading up to June 2023. Worsening matters, the House of Commons Treasury Committee accused the four banks of“blatant profiteering” and “squeezing higher profits from their loyal savings customers.” The people simply have lost confidence in the banks.

The Bank of England (BoE) all but admitted the UK was officially in a recession back in September 2022. Bank Governor Andrew Bailey stated there was nothing the central bank could do to prevent a recession at that stage. The central bank raised rates for the 14th time at its last meeting, bringing the borrowing rate to 5.25%, which marks the highest level since February 2008. Those with two-year mortgages have felt the pressure as the average fixed rate now sits at 6.85% compares to 3.95% last August. Bailey said “depending on what the evidence on the economy indicates, we might need to raise interest rates again but that’s not certain,” worsening confidence in the central bank.

The big four, as they are known, have passed their costs onto the consumers and then some. Unite analysis found in March 2023 that these institutions managed to profit an additional£7 billion due rising rates. Yet, the ONS found that households were spending 1.5 percentage points more on financial services, a cost that continues to rise. The financial sector is coming out as the winner in all of this as workers in the sector have seen their incomes nearly triple since 2021. Additionally, the big four have seen a 42% rise in profits since the pandemic and have been aided by government tax cuts.

Unite’s analysis concluded:

“Unite’s research shows how the banks have already made billions in extra profit from interest rate rises. If the MPC raises rates again they stand to gain even more. Banks treat these rises as a licence to pick the pockets of householders across Britain. “Unbridled profiteering is taking billions of pounds away from workers and communities and putting it into the hands of corporate Britain. Last year, the profits of the big four banks soared to an eye watering £33 billion. Politicians need to wake up. It’s only by taking on runaway profiteering that we can end the cost of living crisis.”

Smart money is simply moving out of the banks. People are shopping around at smaller institutions that offer a competitive advantage and/or placing their money where it will not continue to decline in value. It will only become more expensive for consumers to keep their money in these institutions as rates rise since inflation is far from under control. So far, the banks are not worried about liquidity, but watch out if this becomes a trend.

Credit card balances in the US have surpassed $1 trillion for the first time, with balances up almost 20% from a year ago. The Federal Reserve Bank of New York reported that total credit card debt stood at $986 billion in the first quarter of 2023, unchanged from the record hit at the end of 2022. The average credit card interest rate offered in the US over the last three months of 2022 stood at 21.6%, according to WalletHub, a jump from about 18% a year prior. Americans are now tapping into their retirement funds to make ends meet.

Hardship withdrawals allow employees to pull money out of their 401K for an “immediate and heavy financial need.” No one would recommend doing this unless the situation was dire. Bank of America reported that 15,950 employees enrolled in 401K programs made a hardship withdrawal during the first three months of 2023, a 36% rise from Q2 22. Individuals must show evidence that the money will be used for a major hardship in order to avoid the 10% early withdrawal fee imposed for those under 59.5.

It costs more money to borrow thanks to rising interest rates. The majority of Americans do not have money stashed away for a rainy day, and those who do are rapidly draining their accounts to keep up with Biden’s economy. The CPI report in June showed a rise of 3% YoY, but look around, absolutely everything is more expensive. Shelter costs have reached an all-time high and the price of food is on the rise, especially with wheat price manipulation going on using the war in Russia as a guise. Why are we sending hundreds of billions to a foreign nation when our own people cannot afford to live? The masses need to wakeup and get mad at their current predicament before the next election if we even have one.

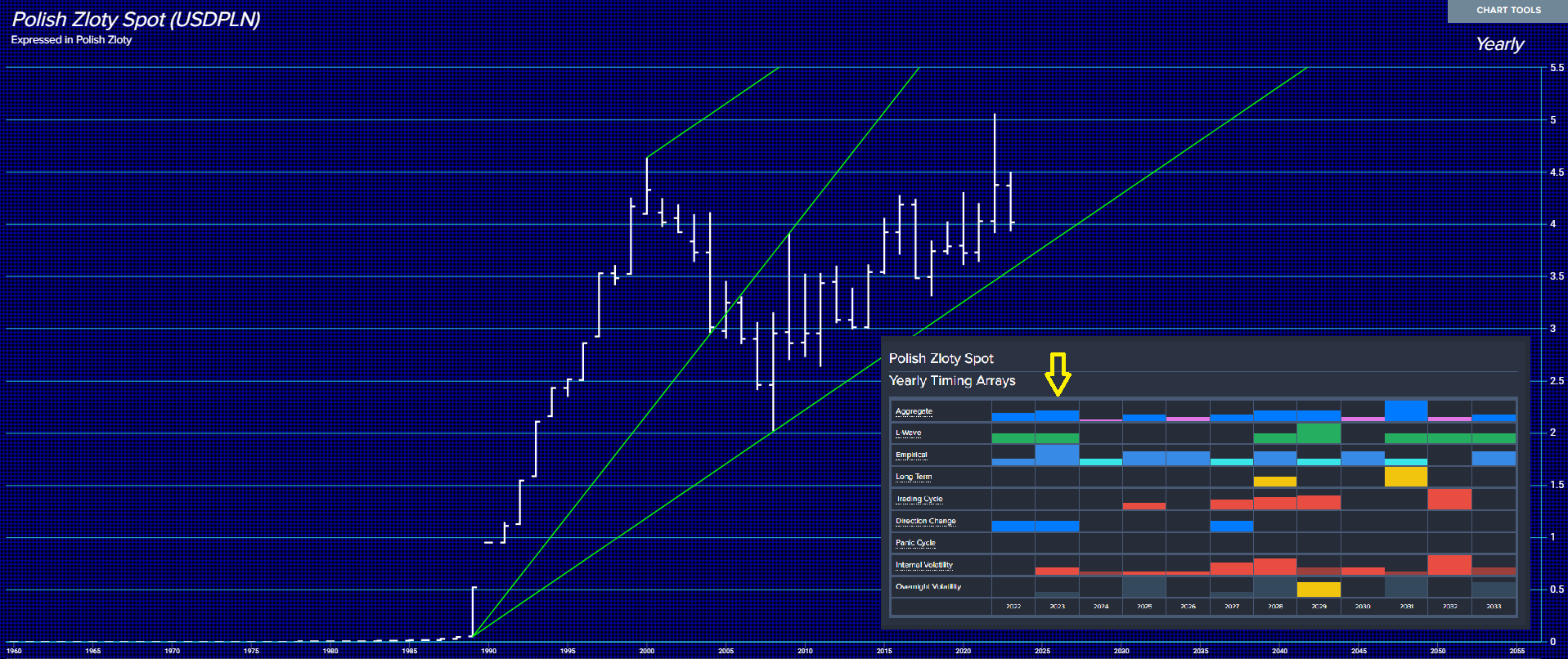

QUESTION: Mr. Armstrong, We met when you came to lecture here in Poland. Everything you warned about has unfolded right down to a dollar high in 2022, followed by a low in 2023. The majority now are against the government. We, too, fear that the election may be rigged later this year. Putting all these troops on the border with Ukraine, which includes 40,000 Americans, has raised grave concerns that our government will cross the border in hopes of getting Russia to attack our troops to justify NATO invoking Article V. Some are starting to wonder if our government needs to get Russia to attack us to suspend elections as Zelensky has done in Ukraine.

What do you see for Poland ahead?

Aleksy

ANSWER: Yes, it has been quite a while. Thank you for recommending Krakow. It was beautiful. Loved the architecture and vast square. I know the concerns there about the upcoming elections. We have a Panic Cycle in November. I am also aware of the idea of Polish troops crossing the border and taking the Western portion of Ukraine, which used to be their territory. Putin has warned about this, but the Western press calls it misinformation and Russian propaganda. Then you have Yevgeny Prigozhin in Belarus with his eyes on Poland. Your government is indeed pushing the envelope.

The risk remains that the greenback will rise into 2027, which seems to be more on the threat of war. You have Poland, Lithuania, and Estonia with severe concerns about Russia retaking the region. The Russian people are not really interested in that. Much of that propaganda has been spread by the ISW and NATO, which is desperate to remain relevant.

I think Zelensky’s days are numbered. If he is assassinated, it will be for what he has done to Ukraine. The social media in Ukraine shows funerals and images of the dead. The kill ratio is 5 Ukrainian soldiers to even one Russian and that comes from Ukraine – not Russia.

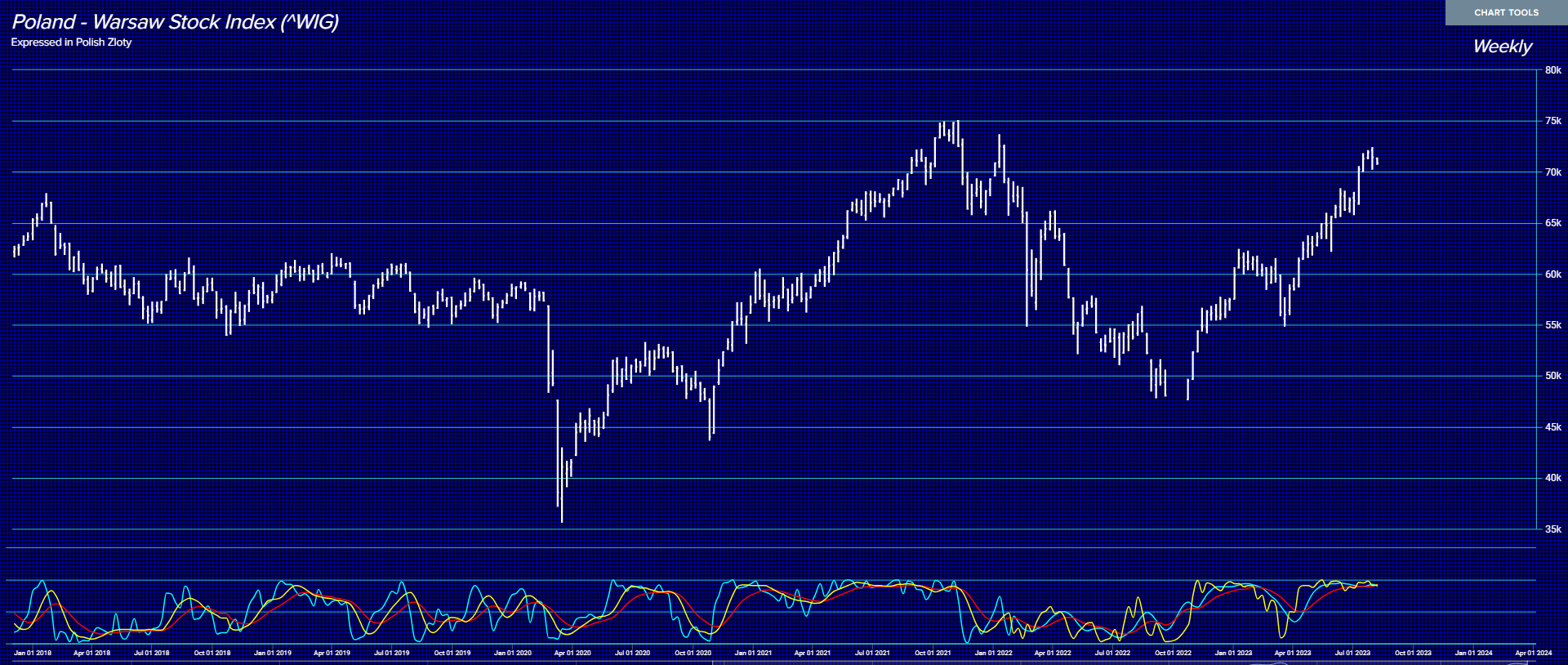

Ukraine is losing badly. That is my concern that the Polish/American Troops will cross the border begging for Russia to attack them so they can indeed invoke Article V. The share market is going to roll over. Closing below last week’s low should spark a correction, and the volatility should start next week.

Insofar as this election being rigged, I appreciate the concern. Poland will reach a critical turning point on October 26th, 2023, which is now 34 years from the overthrow of communism on June 4th, 1989. There should be a shift in politics; ideally, the present government should lose. That remains to be seen.

We seem to be begging to start another proxy war against Russia in the middle of Africa. There was a coup overthrowing the government, and you have people chanting chanting “Wagner” and raising Russian flags. The whole problem has been the Neocons and their private propaganda machine, the ISW, keep projecting that Russia is weak and they can take it down. Russia can manufacture all the weapons it needs, and it is one of the wealthiest countries on the planet regarding natural resources. These people are putting out fake news to encourage war, telling everyone the West can win.

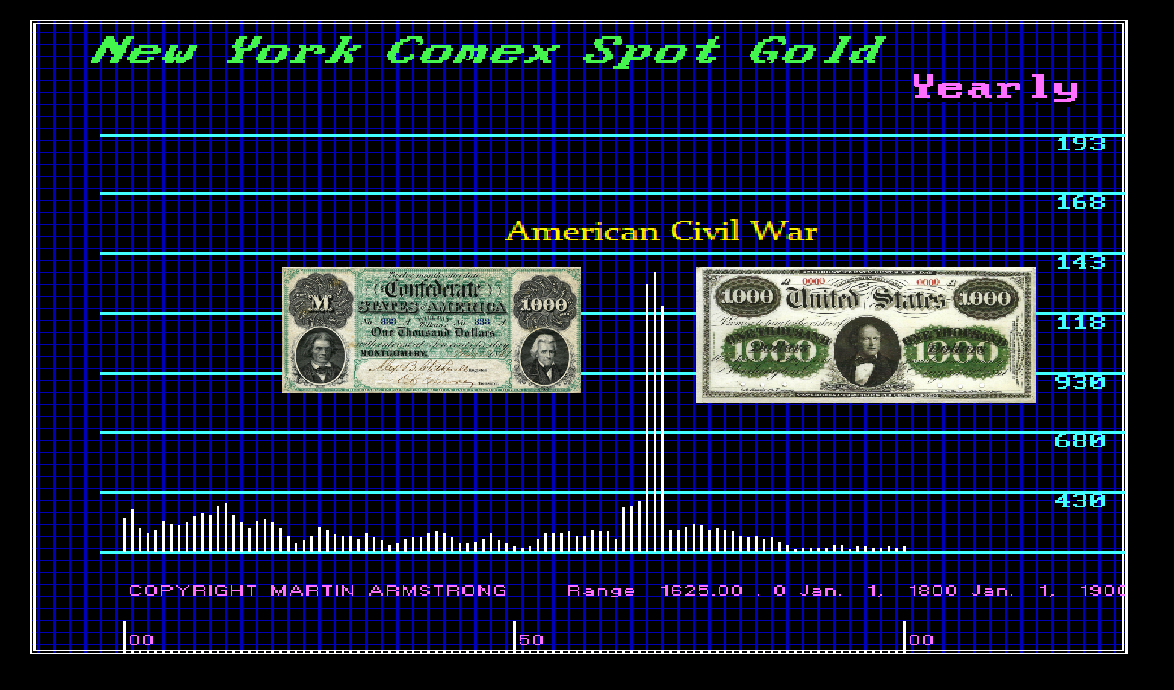

This is more akin to the US Civil War, where the North had all the capacity to manufacture weapons, and the South had been primarily an agrarian society. The South needed money and supplies from Europe.

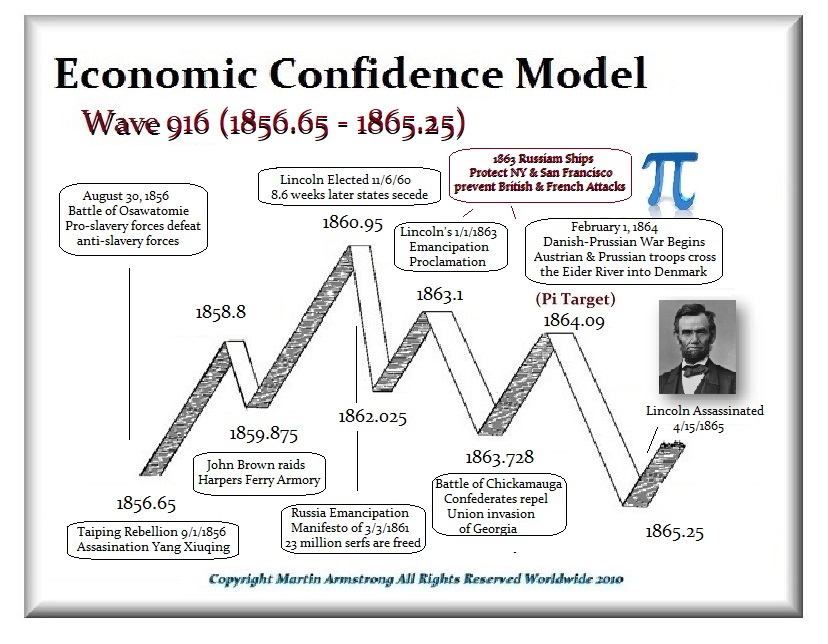

Secretary of State William Henry Seward (1801–1872) for the North was deeply concerned that no foreign nation would intervene in the conflict on behalf of the Confederacy. Russia came to Seward’s aid to protect the US from a European invasion. Russia sent its warships to protect New York City and San Francisco in 1863 against the British and French, who perhaps considered the American Civil War an opportunity to conquer the United States.

In contrast, the Confederate diplomats desperately attempted to convince the stronger European countries to come to their aid and intercede on their behalf. These diplomats were successful in helping to convince Great Britain and France, two European countries that had much at stake in the outcome of the American conflict, to legally confer belligerent status upon the Confederacy, which recognized it as a nation engaged in war. In other words, they recognized the South as independent. In contrast, today, the West refuses to grant that to the Donbas in Ukraine despite the Minsk Agreement and the fact that the people there are Russian, while Ukraine outlaws their language and their religion.

In fact, Abraham Lincoln drew his Emancipation Proclamation taking the actions of Tsar Alexander II (b: 1818; 1855–1881), who issued his own Emancipation Manifesto on March 3rd, 1861, emancipating 23 million Russian serfs. American abolitionists cheered his action and pushed for Lincoln to do the same, which he finally did on January 1st, 1863. Russians were actually shocked when the American states descended into armed conflict over the issue. In Russia, the serf owned nothing, and they were not happy. They embraced Marxism, and the first Russian Revolution followed in 1905, 43 years later (8.6/2).

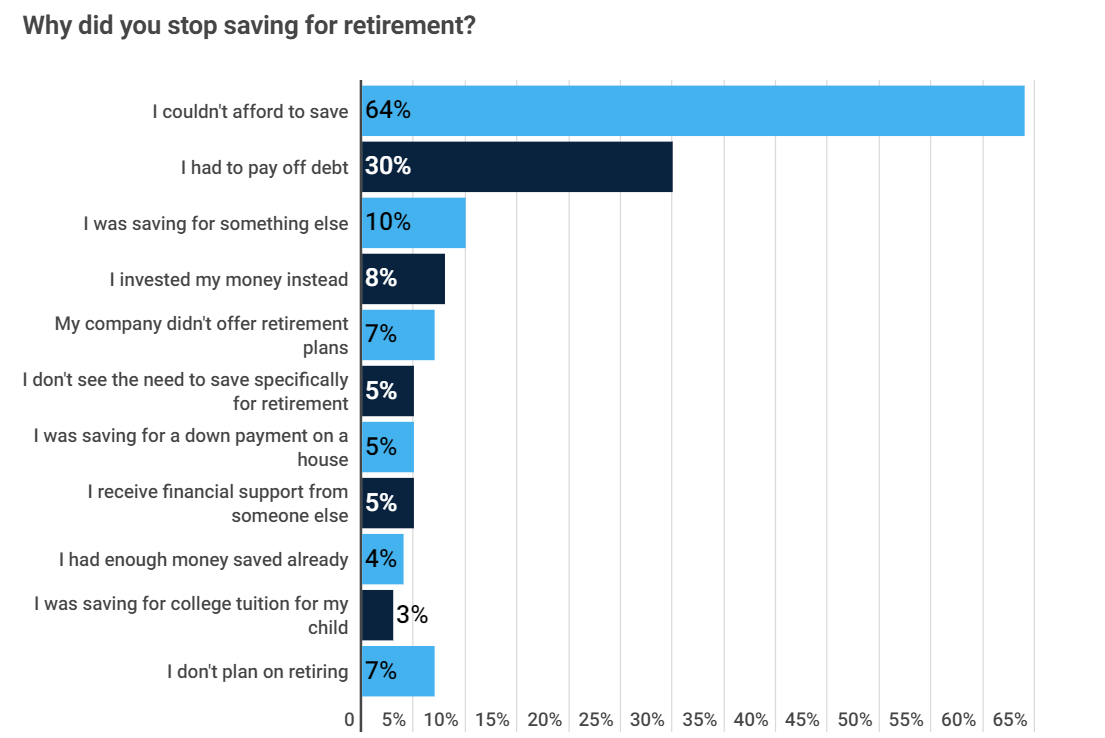

A new survey by Clever Real Estate shows that 64% of Gen Xers have stopped saving for retirement. These are the people born between 1965 and 1980. Retirement has become a luxury, and people are working well into their golden years out of necessity. The cost of living is so high that the majority cannot afford to save for the future. Social Security will not be there to soften the blow, pensions are failing for those lucky enough to secure one, and we soon will have a nation of elderly individuals with no financial means. This is a great premise to usher in the Great Reset, where the government usurps all power, as people may have no other option.

According to the survey, 56% of respondents have less than $100,000 in savings, while 22% have absolutely nothing saved for retirement. Most (69%) would like to retire before the age of 65, but only 37% believe that is a possibility. In fact, 19% do not believe they will retire before 80, and 11% believe they will be working until the day they die.

The average 401K match from employers is at an all-time high of 4.7%, but people are still unable to stow away funds. Of those who never saved for retirement, 73% said they simply could not afford to save, while 30% said they were focused on paying off debt. Over half (52%) said they have over $10,000 in non-mortgage outstanding payments. Around 44% blame the poor economic conditions of the US for their dilemma.

Americans are falling deeper into debt and have no plans for financial management. Americans raked in a record $17.05 trillion in debt during Q1 of 2023 alone. Credit card debt is at an all-time high, and the cost of borrowing continues to rise. Public schools do not educate people on the importance of saving for retirement, and we are all paying into Social Security with no guarantee that it will be paid back to us. America is heading toward a retirement crisis.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America