After the FOMC decision, Jerome Powell stated during his Q&A that the Federal Reserve does not have a plan to consolidate banks. “I personally felt that having small, medium, and large were a great part of our banking system,” Powell stated, noting that they all serve different customers. Powell said it could have been a good outcome had one of the regional banks bought failed First Republic instead of JPMorgan Chase. However, the chairman noted that the FDIC mandates that banks be acquired using the least costly resolution option.

The FDIC says it does not give preference to bidders. How can a bank qualify? According to the FDIC website: “Bid lists are created for each acquisition opportunity based on potential acquirer’s qualifications and interests and characteristics of the failing bank such as capital ratios, regulatory ratings, assets and core deposits as reported on the most recent Call Report and geographic location of the bank. Each bid list is developed using several criteria sets to identify approved potential bidders for an acquisition opportunity, while considering factors that match likely approved bidders to an acquisition opportunity.”

Due to the recent banking failures, the FDIC has also created guidelines specifically for failed bank acquisitions:

“The FDIC markets troubled institutions to healthy insured depository institutions. The FDIC is statutorily required to resolve failed institutions using the least costly resolution option minimizing losses to the Deposit Insurance Fund. The FDIC's primary objective is to maintain financial system stability and public confidence. Returning assets to the private sector in an orderly manner at the best price is another key objective. The FDIC also tries to reduce the impact on the community.

Recapitalization before failure is the preferred method to resolve open troubled financial institutions. FDIC markets institutions in case a failing institution is not able to resolve its issues on its own. If an insured depository institution is unable to resolve its issues, the FDIC will implement its resolution process by which qualified bidders may seek to acquire the assets and assume the liabilities of the failing institution.”

Obviously, smaller banks will not have the ability to compete. All banks are struggling with liquidity issues, and mid-sized institutions will likely be unable to offer the “least costly resolution option.” Ideally, they want failing banks to be attained prior to failure, and only large institutions can provide that cushion. Nothing in the FDIC guidelines at the time of this writing currently limits what a large institution could acquire. The computer states that we will see more banking failures across the globe. Based on these guidelines in the US, it is reasonable to assume that large banks like JPMorgan Chase will benefit from future acquisitions and continue to grow. It is unclear whether banking monopolies are permitted under the 1890 Sherman Antitrust Act, but it remains to be seen what alternatives the system will have as more banks go under.

A lot of people somehow think that the move to Digital Currency is a completely new monetary system, It is targeted to eliminate cash transactions so everything is taxable and nothing can be hidden from our overlords. If we look at commerce in the United States during 2022, 82% of all transactions were digital – Debit cards (20 percent), credit cards (30 percent), and digital wallets 32 percent. That was e-commerce.

They are hunting down what they believe is 30% of all commerce and cash and lick their lips at the thought of having their hand in your pocket. Make no mistake about it. They know major upheaval threatens their power. Like Trudeau seizing accounts of anyone who donated to the Truckers, that is the agenda. Control all transactions and turn off anyone who they see as a threat.

QUESTION: Just about every Bitcoin advocate says you are wrong and Bitcoin cannot be stopped. Yet, it seems they are dreaming. Here in Europe, we are already restrained by the maximum cash transaction is €1000. Do you maintain that cryptocurrency will be outlawed or seized?

HT

ANSWER: Yes. Here is Lagarde on digital currency. She states this object is “control” everything you do. Europe is a Marxist Paradise. Everyone is an economic slave and whatever they earn belongs to the state – not them. The state will decide how much you are allowed to keep. I really do not understand these Bitcoin people. They put out all of these theories as if Bitcoin is the savior. These people are out to control EVERYTHING. Do you really think they will allow any cryptocurrency to survive?

I don’t think these people read the memo. Government is broke. They will default on all their debts. And the new monetary system they are planning is total control. LaGarde says they are “considered” no controls on 300-400 euros. “CONSIDERING” means as it stands now, there is 100% proposed control – period! They will be able to restrict what you are allowed to spend money on or even donate if donations will even be allowed.

These people would NEVER be hedge fund managers. The first question you must ask yourself is: What if I am wrong?

They have made up their mind, refuse to consider any other scenario, and in the process, they will have a very rude awakening. We are entering a period of COMPLETE TOTALITARIANISM as we move toward 2032. Governments are losing control in this Private Wave and they then fight back to survive like a cornered animal that will fight to the death.

That is the agenda! What do they not understand? They will impose capital controls. They always do. That will mean that they will have no intention of allowing people to buy and sell cryptocurrencies. They will most likely do that as well when it comes to gold.

The entire purpose of the CBDC is to impose COMPLETE capital controls. So how will you buy and sell anything that they deem to be a threat to their totalitarian world? That is what is coming. All the fools who voted for Biden and will again deserve the world these people are creating. They intend to make RESISTANCE IS FUTILE. In the process, the right to vote will vanish.

Trump won in 2016 and John Kerry called it “populism” not Democracy. They WILL terminate our right to vote in the years ahead because it will no longer be defined as democracy – but populism, which is any movement against the establishment.

Schwab is telling you that Democracy will be terminated. Pay attention. Listen carefully to the report by the FT and how the election of Trump scared the hell out of career politicians. They will never allow Trump to win in 2024. They will assassinate him if there is no other way. The propaganda was that the 2020 vote was real- that was a joke. The Deep State was not going to let Trump win and they control the vote counts.

QUESTION #1: why no information on CBDC. Need help fast. Feds are suppose to call in the dollar in July. HELP mk

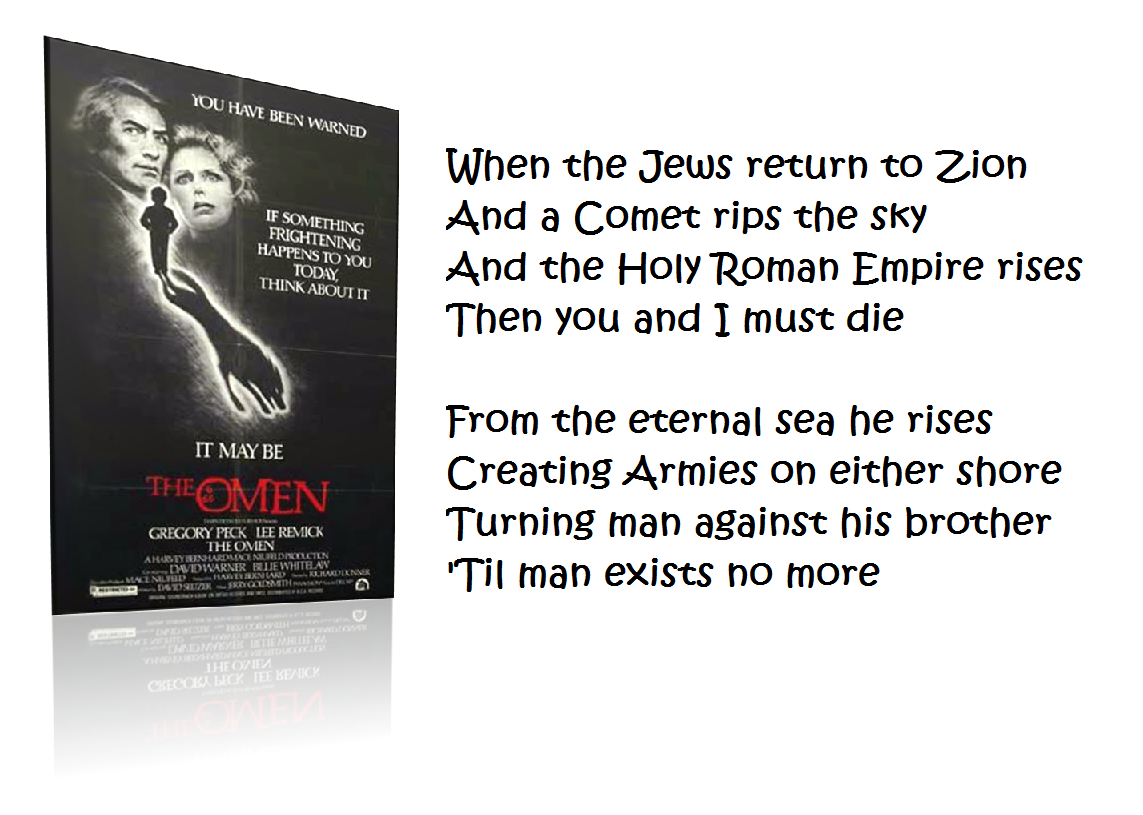

COMMENT #1: This whole thing reminds me of the movie The Omen and we will be accepting the number of the beast and without it we will not be allowed to buy or sell. I don’t know about a person being the infamous anti-Christ, but it sure looks like the government is trying hard to fulfill that role.

SC

ANSWER: The FedNow is the system that will be for CBDC and the elimination of all paper money. However, they will not cancel the dollars in July – not just yet. This is why they are rushing 5G before testing to see if the radiation is harmful. This is all about total control and 100% tax collection. They will be able to turn off the ability to buy and sell categories as well as individuals.

I will do a private post on the timing for the end of paper money. That is coming. It is part of their authoritarianism into 2032.

As for the governments of the world being the anti-Christ, who knows? Perhaps they saw that movie and said that’s a great idea! The “eternal sea” has always been used to refer to politics. This is certainly justification for term limits. Once career politicians were created, that ended any hope of an honest government. Those who are not crooks, look down on us as the scum – hence hiring 87,000 IRS agents with guns.

As far as the number everyone knows the “666” of the anti-Christ, but strikingly, most do not know the number of the name the Jews gave to God – “Jehovah.” If we use the old Hebrew system we can find the number of God. Yod =10 , He = 5, and Vau = 6. Therefore, the name of God in Hebrew – He Vau He Yod equals 5 + 6 + 5 + 10 = 26. The number of the name assigned to God by the Jews is 26. Perhaps they should apply this system to entities rather than individuals.

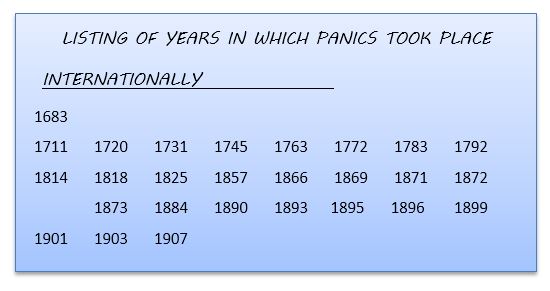

I have been often asked by students of history that the list from which I derived the Economic Confidence Model was 224 years divided by 26 events yielding 8.6153846 which was a derivative of Pi, and was it based on this calculation of 26? It was not. There just so happened to be 26 events in that 224 period. Beyond that, who knows?

Posted originally on the CTH on May 1, 2023 | Sundance

Everything about the process of cutting down energy exploitation, then driving supply side inflation, then raising interest rates to shrink demand (stem inflation) created by a desire to lower economic activity to the scale of diminished energy production, is a game of pretending.

The collateral damage from the rate hikes has been the banking destabilization, which shows the priority of the government officials and central banks to support the climate change agenda. Into the game of pretending comes the second unavoidable consequence with inflation continuing as a result of the energy policy.

They simply cannot cut energy demand enough to meet the diminished scale of production. There is no alternative ‘green’ energy system in place to make up the difference. That is the reality. Now, the fed is scheduled to raise rates again, then begin to debate the collateral damage as they continue the pretending game.

(Via Wall Street Journal) – […] Another quarter-percentage point increase would lift the benchmark federal-funds rate to a 16-year high. The Fed began raising rates from near zero in March 2022.

Fed officials increased rates by a quarter point on March 22 to a range between 4.75% and 5%. That increase occurred with officials just beginning to grapple with the potential fallout of two midsize bank failures in March.

The sale of First Republic Bank to JPMorgan Chase & Co. by the Federal Deposit Insurance Corp. announced early Monday is the latest reminder of how banking stress is clouding the economic outlook.

Fed officials are likely to keep an eye on how investors react to that deal ahead of Wednesday’s decision, just as they did before their rate increase six weeks ago when Swiss authorities merged investment banks UBS Group AG and Credit Suisse Group AG. (read more)

There is no other way to look at the combined policy without seeing a Central Bank Digital Currency (CBDC) in the future. All of these combined policies are creating a self-fulfilling prophecy.

Posted originally on the CTH on April 29, 2023 | Sundance

There’s something sketchy afoot in the world of high finance. Following the collapse of Silicon Valley Bank, the most likely first contagion bank would have been First Republic Bank; both California banks carried similar vulnerabilities. However, once the Treasury Dept agreed to cover all deposits, even those unsecured deposits over the $250k FDIC insurance protection, suddenly First Republic Bank survived.

After the FDIC announcement, a group of 11 larger banks lent First Republic a tranche of money ($30 billion) to secure its holdings and help stabilize it. Approximately six weeks passed, suspiciously perhaps the burn rate for the tranche in combination with risk averse exits says I, and suddenly First Republic starts destabilizing again. [Insert Suspicious Cat here]

The First Republic stock value collapsed further last week, and the FDIC is now trying to get a takeover bid secured before government regulators are forced into a position of receivership. I’m not dialed in to the banking industry, but it looks to me like the six-week interim phase was an agreement to give the illusion of stability and afford time for highly exposed, ¹likely well connected, stakeholders to exit.

With the Treasury taking the prior SVB position, thereby securing all deposits regardless of scope, the FDIC is now on the hook if the collapse includes a govt takeover. The FDIC seems to be playing hot potato and looking for a buyer. Additionally, the FDIC is asking JP Morgan-Chase if they are interested. JPMorgan holds more than 10% of all deposit funds in U.S. banking. From a regulatory position, JPM cannot legally take any more institutional deposits. So, what gives? It is all sketchy, all of it.

(Bloomberg) — The Federal Deposit Insurance Corp. has asked banks including JPMorgan Chase & Co., PNC Financial Services Group Inc., US Bancorp and Bank of America Corp. to submit final bids for First Republic Bank by Sunday after gauging initial interest earlier in the week, according to people with knowledge of the matter.

The regulator reached out to some banks late Thursday seeking indications of interest, including a proposed price and an estimated cost to the agency’s deposit insurance fund. Based on submissions received Friday, the regulator invited some of those firms and others to the next step in the bidding process, the people said, asking not to be named discussing the confidential talks.

Spokespeople for JPMorgan, PNC, US Bancorp, Bank of America and the FDIC declined to comment. Bank of America is considering whether to proceed with a formal offer, one of the people said. Citizens Financial Group Inc. is also involved in the bidding, Reuters reported, citing people with knowledge of the matter.

The bidding process kick-started by regulators — after weeks of fruitless talks among banks and their advisers — could pave the way for a tidier sale of First Republic than the drawn-out auctions that followed the failures of Silicon Valley Bank and Signature Bank last month. Authorities are stepping in after a particularly precipitous drop in the company’s stock over the past week, which is now down 97% this year.

Unclear to some involved in the process is whether regulators might use a bid for a so-called open-market solution that avoids formally declaring First Republic a failure and seizing it. The stock’s drop — leaving the company with a $650 million market value — has made such a takeover at least somewhat more feasible.

[…] A group of 11 banks that deposited $30 billion into First Republic last month — giving it time to find a private-sector solution — have proved reluctant to band together on making a joint investment. A few proposals that surfaced in recent days called for a consortium of stronger banks to buy assets from First Republic for more than their market value. But no agreement materialized.

Instead, some stronger firms have been waiting for the government to offer aid or put the bank in receivership, a resolution they view as cleaner — and potentially ending with a sale of the bank or its pieces at attractive prices.

But receivership is an outcome the FDIC would prefer to avoid in part because of the prospect it will inflict a multibillion-dollar hit to its own deposit insurance fund. The agency is already planning to impose a special assessment on the industry to cover the cost of SVB and Signature Bank’s failures last month. (more)

¹This is pure speculation on my part, but if you were a well-connected California big fish and you had exposure in FRB, after the SVB collapse you might ask the govt to construct an exit plan to assist you.

$11 billion flows in, you make your quiet withdrawals, and after exit the delayed outcome proceeds accordingly.

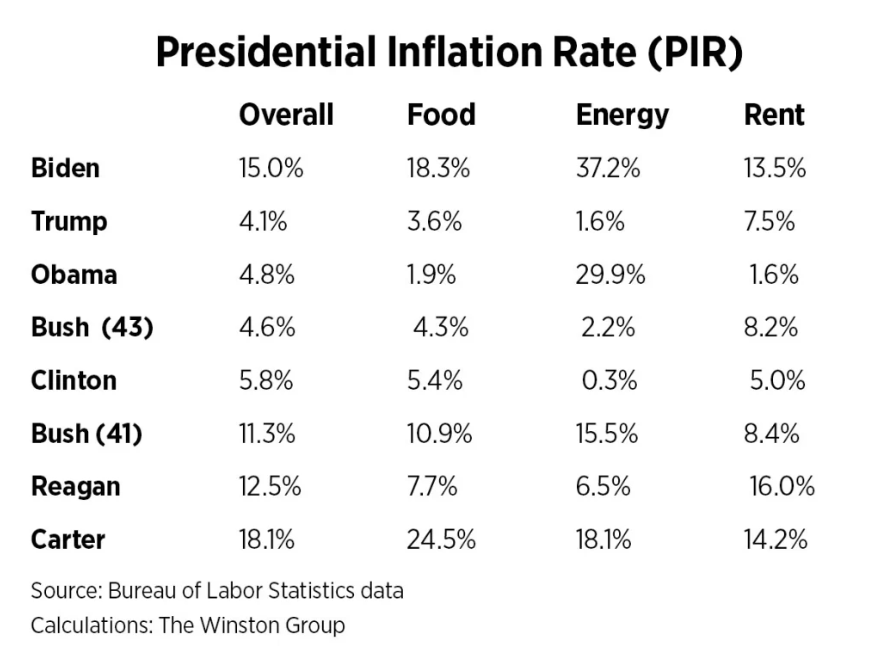

Inflation was only 1.4% when Biden took office. He began implementing policies on his first day that directly created the energy crisis in the US. He refused to reopen the economy under the pretense of COVID for as long as possible, disrupting the supply chain and damaging small businesses. Biden has created multi-trillion dollar spending programs that saddled the nation with more debt and increased price volatility. His team has been working to divide the people and create civil unrest. I could go on about his failures, but his worst move was involving America in the Russia-Ukraine war. Inflation has steadily risen to unsustainable levels nearly every month since Biden took office.

Biden’s team toys with the numbers to tout that inflation has gone down, but they are comparing the high and low both created under Biden. Wages cannot support the increase in costs and absolutely no one is better off under Biden. Considering the dire situation, it is infuriating that the US had a 1.4% inflation rate not long ago.

Inflation has soared by over 15% since Biden’s inauguration in January 2021. The “Presidential Inflation Rate,” (PIR) developed by the Winston Group, measures a president’s progress in handling inflation over time, from their inauguration month to the month of the most recent CPI report. As of March, inflation under Biden is 15%, which makes him the most inflationary president since Carter. Biden’s 24% “Presidential Inflation Rate” for rising electricity costs is higher than any of the previous seven presidents as it is now up 37.2%. The cost of food rose 18.3% under Biden, and eggs alone have soared by nearly 80%. Shelter costs are now at a 42-year high, and Biden’s PIR for rent has surpassed 13.5%.

Joe Biden takes no responsibility for the inflation caused by his policies and failures as a president. Inflation will continue to increase under Biden. He has absolutely no plans to address the issue, and the legislation he creates to address the problem only exacerbates it. Biden is a corrupt politician who lines his pockets with money from Ukraine and China. The investigation into his crime family that the media is sweeping under the rug reveals the truth. This man needs to be removed from office immediately, but the people alone must decide when they’ve had enough.

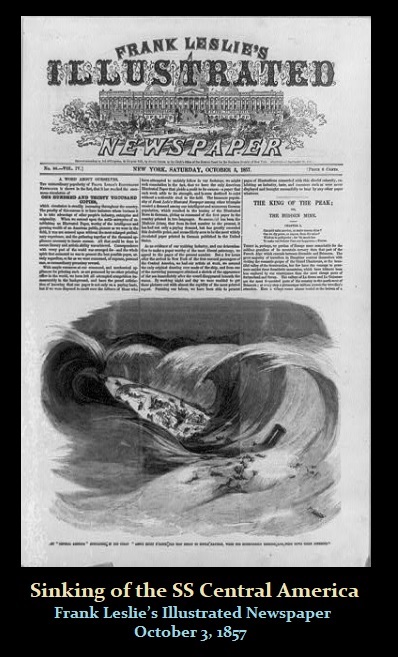

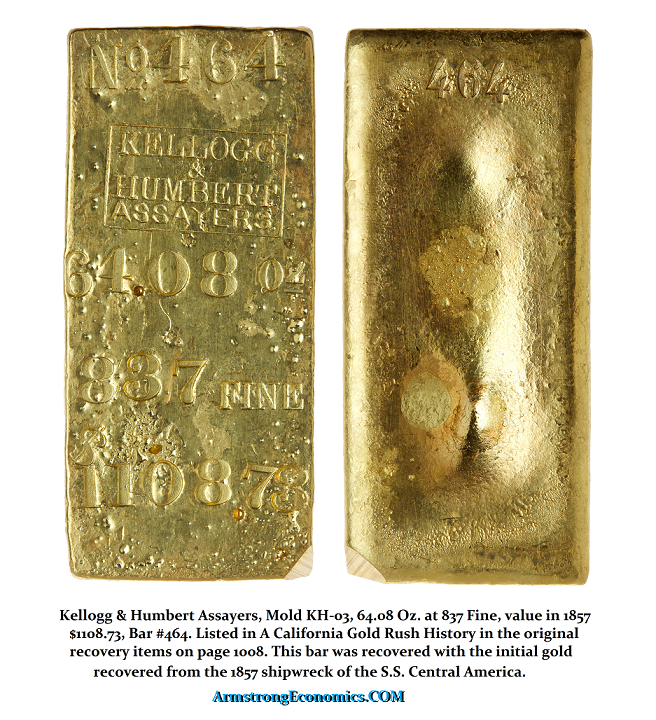

QUESTION: Didn’t you also buy gold bars from the SS Central America ship that was discovered? The gold bugs hate you and say you are bearish gold but you buy a lot of it.

All the best

JE

ANSWER: Oh yes. I tend to collect important relics from major economic events. The sinking of that ship set off a financial panic in NYC because the banks were counting on that gold shipment. I did buy bars. There were some 30,000 pounds (13,600 kg) of gold and about 15 tons were recovered.

They are a piece of history. I would not melt them down.

It is very interesting that I just purchased a hoard of $20 liberties, all uncirculated like the day they came from the mint and all dated 1904. The source was a foreign central bank. They were going through their reserves and came across this exciting hoard. It just goes to show that sometimes being disorganized results in new discoveries and excitement all the time. This batch was 500. The fact that every coin has the same date demonstrates that it was indeed a reserve asset directly from the Philadelphia Mint.

All we hear is the same claims that the dollar is dead and it will be totally worthless any day now. Over the last few weeks, all we hear from the majority now is that the dollar is finished. Virtually every page you turn or site you visit claims the death of the dollar. They are calling this the de-dollarization of the world economy and that the future of the US dollar as well as the American empire itself is now collapsing. The general claim is that the group of economically-aligned nations known collectively as BRICS is a major threat to the greenback. That was the same story we heard about the Euro back in 1997.

As their scenario goes, the BRICS [Brazil, Russia, India, China, and South Africa] have moved to form an anti-dollar colation and Saudi Arabia is considering jumping on board. They insist that once that happens, the “petrodollar” will die and cease to be a reserve currency.

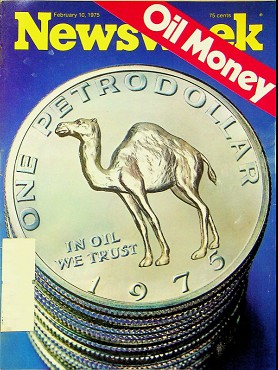

This is then followed by the forecast that the economy will suffer and that any bounce in exports will be short-lived simply because the dollar will be dead for the long term. Of course, this has been the favorite forecast that they keep putting out since Bretton Woods collapsed. They were wrong back then for the dollar rose between 1972 and 1976 against the British pound, with the collapse of Bretton Woods. To try to explain why the dollar did not collapse, that is when they claimed that the dollar was backed now by oil rather than gold. That was just an excuse as always to cover up their wrong forecast.

They sold that story to Newsweek and now the dollar rally was because of oil which replace gold. Suddenly the dollar became de facto backed by oil. They needed an explanation to explain why all the old theories were wrong. They sold this theory and it made the front cover of Newsweek. Everyone said YES! That must be the reason. OPEC priced oil in dollars! Naturally, everything was priced in dollars because, under the fixed exchange rate of Bretton Woods, everything from wheat and corn to copper and gold was all priced in dollars.

Now they are saying the American empire is threatened by the potential commercial real estate collapse and the BRICS anti-dollar venture. So they are forecasting a great depression-style crash is possible in the not-too-distant future. They spin this to forecast the end of the America Empire. The London FT, always anti-American/Pro WEF, reports that the dollar as a reserve currency has declined from 73% in 2001 to around 55% by 2021. Yet the FT did state an obvious fact:

“But if you are a reserve-rich central bank elsewhere that isn’t going to be a lot of comfort. Moreover, would you really feel more comfortable in, say, the renminbi? Even if it was fully convertible and liquid, would you honestly feel more sure that Beijing will behave lawfully than DC? The dollar still looks like the proverbial least dirty shirt in the closet.”

COVID actually has played a major role in shifting the world economy. In 2020, the US economy was 24.75% of the world’s GDP. By the start of 2022, it had fallen marginally to 24.15%. What these dollar-forecasting jockeys do not understand, is that if they were correct and the dollar collapsed, then the very BRICS would collapse even further. Economically speaking, when the United States gets a head cold, the rest of the world catches ammonia. You can’t have it both ways. The strength of the dollar is not gold or oil, it is the American consumer.

The risk to the entire world is runaway inflation thanks to Biden pouring untold amounts of money into the black hole known as Ukraine. The Neocons, who control Biden, are planning to launch a war against Russia and China before 2024. This will only continue to accelerate inflation. That reduces the spending power of the American consumer and in the process, the US economic growth declines in real terms and with it, the rest of the world plunges into recession.

While Macron has figured it out that the Neocons are in charge of US foreign policy and he is telling Europe to stop being the puppet of the USA, that all sounds nice but Europe is marching into war with Russia. NATO is firmly in control of the American Neocons and they need war or face losing power. With Trump in the lead, they must stop him at all costs for he is anti-war, would haul the Neocons out by the necks, and defund NATO, as well as stop the climate change agenda.

The US dollar in the global economy has been supported by the size and strength of the US consumer-based economy. Its stability and openness to trade and capital flows without restrictions and it has never been canceled, are the major foundation of the dollar in addition to strong property rights and the rule of law. That is why Russians and Chinese buy US property for they are secure in their ownership of US property which cannot always be guaranteed outside the US.

Consequently, the depth and liquidity of US financial markets remain unmatched. For institutions parking billions, the United States represents a large supply of extremely safe dollar-denominated assets. Are they really going to switch to China or buy debt from Brazil? Not a single institutional client will take that bait.

China has been divesting of dollar reserves because it KNOWS that the American Neocons want war. You do not fund your adversary who intends to wage war against you. China cannot shift reserve assets to Europe or Japan. They have been buying gold because it is geopolitically neutral territory. They are NOT buying gold as an investor thinking it will rally. That is irrelevant. If gold drops 25%, that does not translate into them becoming a seller.

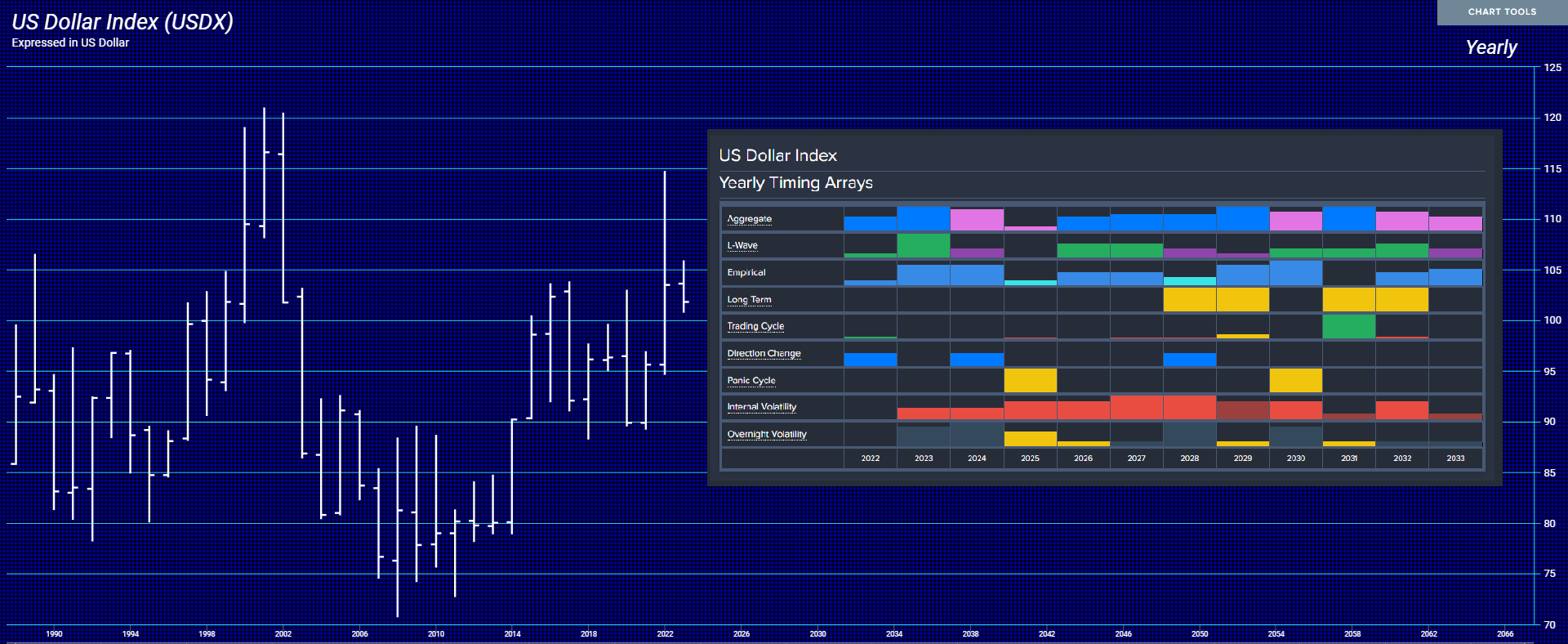

The dollar in international reserves stood at 60+% at the start of 2022 against the US share of GDP at 24.25%. This comparison belittles the argument that the dollar is finished. Eventually, the US will lose the wars it is starting and the dollar will be replaced perhaps as soon as 2028. The IMF is already licking its lips and rubbing its hands together eager to get control of the reserve currency. But they too will collapse. We have a Directional Change next year and a Panic Cycle in 2025. So buckle up.!

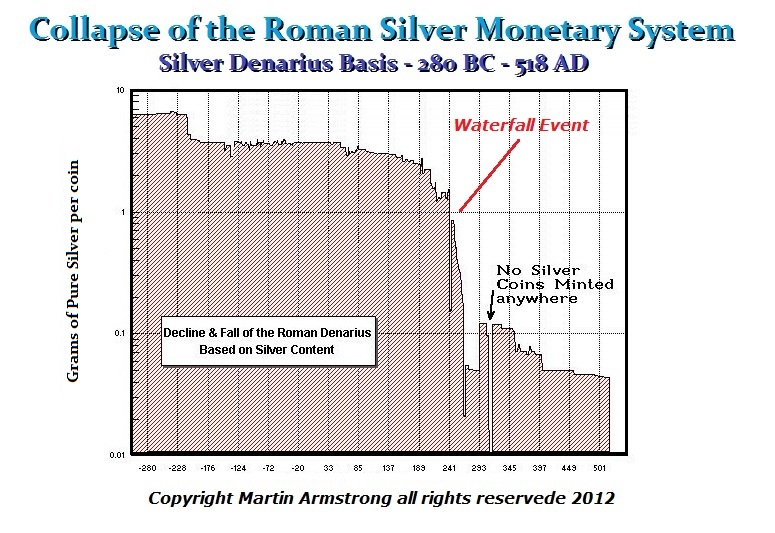

Remember one thing, even with the debasement and collapse of the Roman Denarius between 260AD and 268AD, it still took 224 years for Rome to completely collapse. When war breaks out, capital flight will still be to the dollar. It will not be to public assets, but private. The United States is still supporting the entire world economy. The BRICS need the US consumer to keep their economies functioning. All this talk of the dollar being finished is really nonsense. That day will come, but when the US consumer no longer buys.

Remember 1997? The Euro was going to dethrone the dollar. They claimed the new EU will be a bigger economy than the US. The problem was, they lacked a consumer economy, and low taxes, and they routinely canceled their currency to force people to pay taxes. It is always the same story over and over again.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America