The goldbugs are cheering that there has been a central bank buying of gold. They think somehow that this is because they are bullish on gold. What seems to be going over their heads is what I warned before – when China starts to sell US debt, war is coming. I have made it very clear that the precursor to war is always capital flows. That will be on steroids this year.

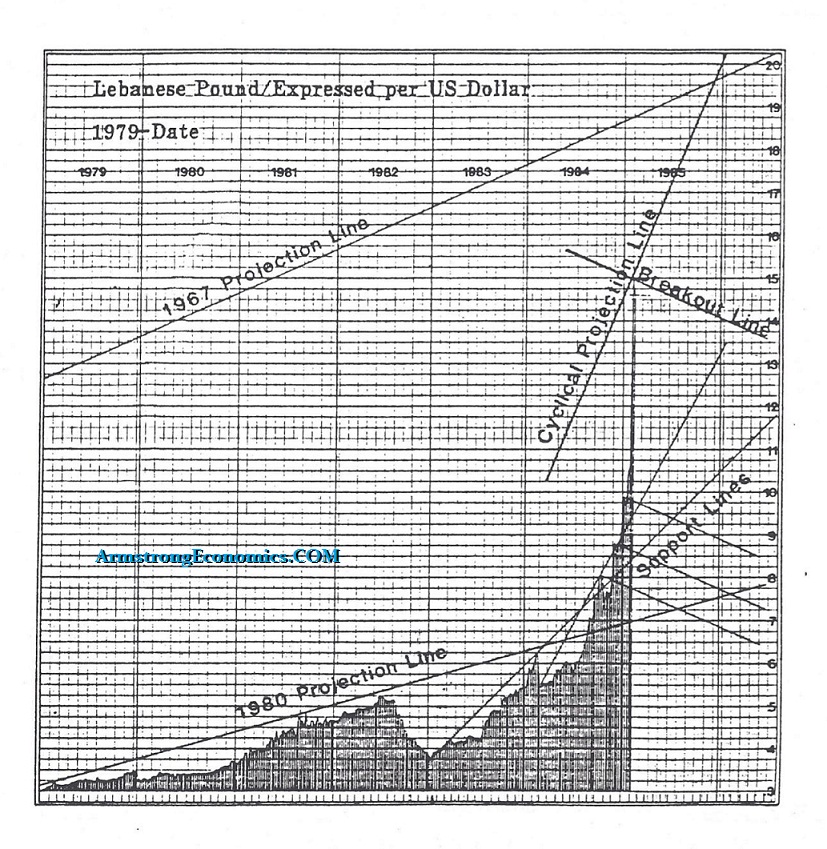

My clients taught me how capital and war move. At conferences, I stated that we were advising the Universal Bank of Lebanon. They found a ledger in the basement where someone wrote down the price of the Lebanese pound every day into the 19th century. They asked if we could build a model. I said sure! Here is a chart from back then. Our model warned that their currency would drop dramatically in 8 days. I thought there was something wrong with the data. Needless to say, I formed the client what the computer said and I commented that something had to be wrong. Very calmly, they asked what currency would be best. I said the Swiss franc. 8 days later the civil war began. The computer was correct. Then the same thing happened with the Iraq-Iran war.

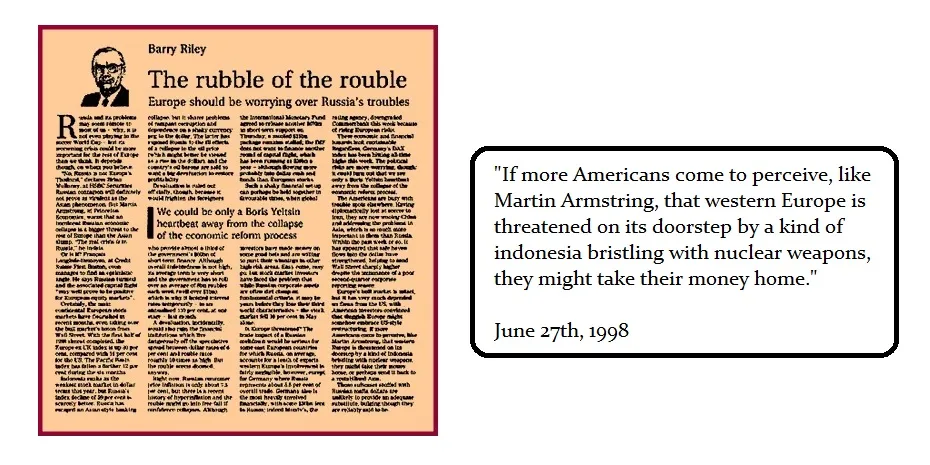

By 1998, I understood the model’s ability to forecast war. I have never created a model to do that. It figured it out all on its lonesome. I stood up in June 1998 in our London WEC and warned that Russia would collapse in about 30 days. The London Financial Times reported that forecast and that became the collapse of the Russian debt market and Long-Term Capital Management debacle.

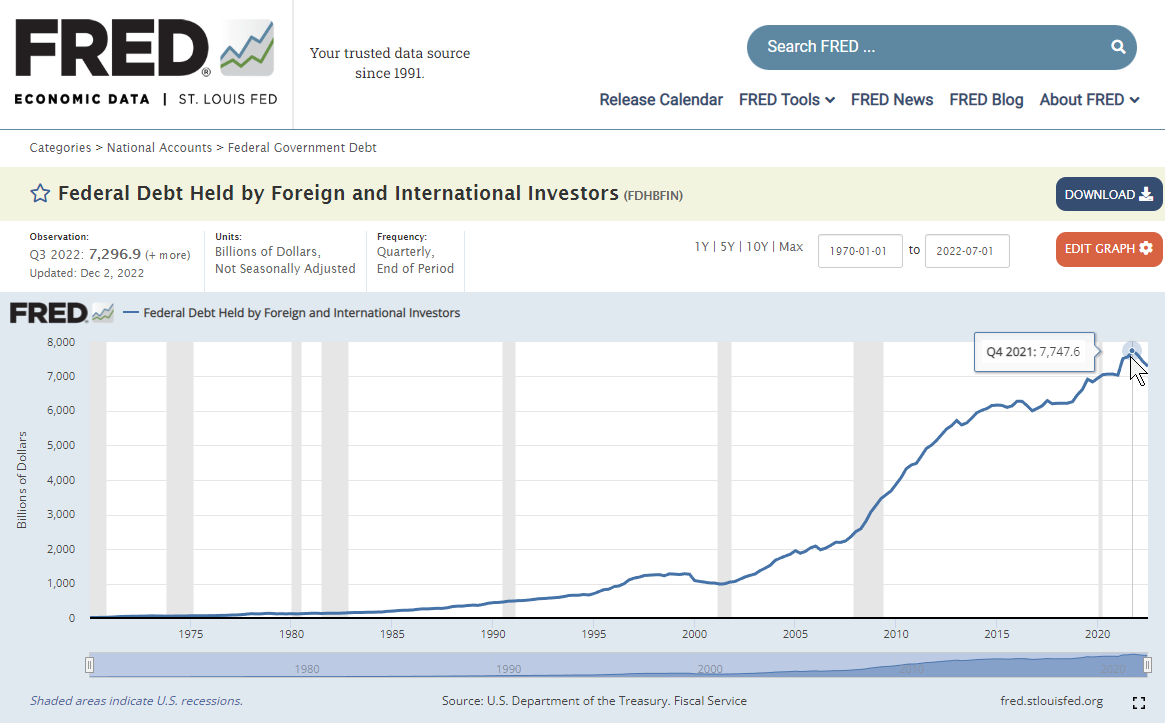

I have warned that if China was preparing to invade Taiwan, then they would start to sell off all US government debt. They would not risk owning US government bonds and watch Biden freeze it all and then claim it will be used to rebuild Taiwan as they are doing to Russia. So China began selling off US debt at the end of 2021. They have been buying gold because they cannot hold US or EU debt in time of war. It is as simple as that. The gold is simply neutrality, for it also does not pay interest. – So much for the inflation nonsense.

During the reign of King George III (1760–1820) the first issue of halfpennies actually was not issued until 10 years after his accession to the throne in 1770. Consequently, the vast number of halfpennies in circulation were actually all counterfeits. Indeed, counterfeiting became rampant at first because there was a coin shortage. In 1771, it was declared that counterfeiting copper coins were to be a serious crime. Nevertheless, this really made no difference. Over the course of the next twenty years, the majority of copper coins in circulation were forgeries. Even in the American Colonies, a favorite pastime was to counterfeit British halfpennies.

Coppers of this type are thought to have been minted from mid-1787 through 1788 and probably into 1789. Interestingly, it appears Thomas Machin first produced halfpence dated to the contemporary year as well as examples backdated to 1778. As the mints in Connecticut, New Jersey, and Vermont failed, their equipment ended up at Machin’s Mills. Along with imitation British halfpence, Machin’s Mills also produced illegal Connecticut coppers and some legal Vermont Coppers, with most of their Vermont coins being struck over counterfeit Irish halfpence. The illegal coining operation continued at Machin’s Mills until around early 1790, which was longer than any of the legal mints in New England.

“There is a vast sum in Circulation here of base Copper: to the amount of Several hundreds of thousands of Pounds. very lately these half Pence are refused every where: I suppose in Consequence of some Concerted Scheme. and it is supposed that they will be all purchased for a trifle and Sent to the United States where they will pass for good metal, and consequently our Simple Country men be cheated of an immense sum.2 The Board of Treasury, may be ordered with out the avowed Interposition of Congress, to give the alarm to our Citizens. and the seperate States would do well to prohibit this false Money from being paid or received.3

There was religious tension in Britain that still lingers to this day against Catholics. The Gordon Riots of 1780 took place over several days instigated by the anti-Catholic sentiment that again erupted with the passage of the Papists Act of 1778. That was an attempt to reduce official discrimination against British Catholics with the first legislation of the Popery Act of 1698. At the time, Lord George Gordon was the head of the Protestant Association. He argued that the law would enable Catholics to join the British Army and once in they would then use the army to plot treason. The protest became the excuse to burn people’s possessions, engaged in widespread rioting and looting, and they even used the opportunity to attack both Newgate Prison and the Bank of England. This was by far the most destructive riot in the history of London.

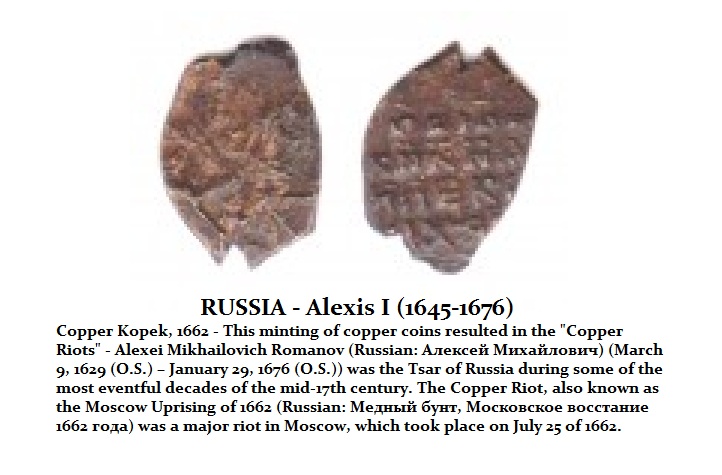

From the mid-1600s, the world money supply was increased largely with copper coins. Russia, in particular, began to overvalue the copper coins. Money is always fiat for its value is typically dictated by the government. Overvaluing copper as in the 17th and 18th centuries, led to the same trend of overvaluing silver during the 19th century. The result of this monetary manipulation by the Russian government led to what became known as the Copper Riots of 1662.

The Russian government began producing copper coins and monetizing them to be of equal value to silver Kopek currency with an average weight of about half of a gram to meet expenses during the mini-Ice Age. The effort failed and silver vanished from circulation as people began hoarding them causing the entire economy to collapse. The copper money was naturally devalued in purchasing power and then there were widespread counterfeiting operations since the official value of the copper coinage became far in excess of the cost of production. The economy collapsed into a deflationary black hole as businesses shut down and unemployment rose dramatically. This erupted into what has become known as the Copper Riots of 1662.

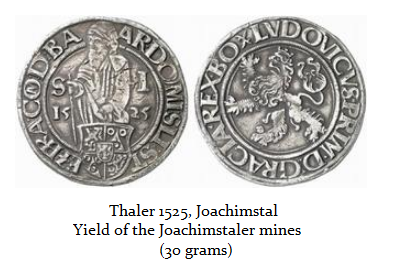

The German bankers, the Fuggers, emerged as the leading Augsburg merchant-banker, who then provided loans to local rulers secured with the silver produce of their mines. The discovery of vast silver mines eventually led to the development in 1525 of the one-ounce silver coin that was the thaler from which we derive the name “dollar” as the alternative to the British pound after the American Revolution. The Joachimsthaler of the Kingdom of Bohemia was therefore the first thaler ideally with a weight of 31 grams or one troy ounce.

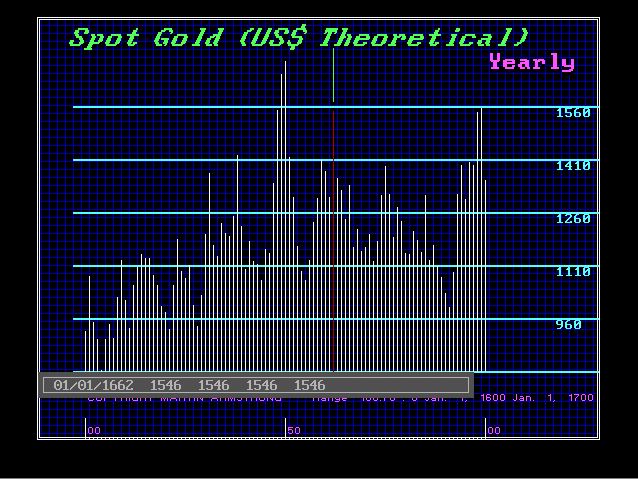

As the silver mines were declining, the decline in the supply of silver led to the rise of copper coinage during the next century. This was not an isolated incident confined to Russia. There was a shortage of precious metals going into 1662. It was most profound in Russia. Nevertheless, the price of gold rose sharply from the low of 1655 in a 7-year bull market. This also reflected the deflationary atmosphere that was emerging thanks also to the mini-Ice Age which was peaking during the 17th century yet would last well into the mid-19th century.

It was Spain’s silver mine known as the great red Cerro Rico or ‘Rich Hill’ that towered over the city of Potosí in Bolivia. It had been mined since 1545 by drafted armies of natives. The great silver boom of c1575-1635 was when Potosí alone produced nearly half the world’s silver. But the mine’s yield was starting to decline. By 1678, native workers became scarce and the output of the mines began to dwindle. This was the royal mint that produced vast amounts of ‘pieces of eight’, which became the precursor of the American dollar. The shortage of labor ended up being augmented by purchasing African slaves from the Dutch who were buying them under the pretense that they were the spoils of war, which had been the justification for slaves from ancient times.

As the quantity of new silver in the world monetary system was declining, we begin to see the rise of copper coinage make its first appearance under James I of England (1603-1625). Due to a shortage of small coins, James I authorized John Harrington to issue tin-coated bronze farthings in 1613, and three main types were minted – the last being a slightly larger copper farthing without the tin coating. The first halfpenny was introduced in 1672 by Charles II (1660-1685). Charles II issued some copper halfpennies and farthings in 1672 for a single year but issued farthings again in 1873. The next issue of a farthing was struck in a tin but during 1684 and 1685.

However, in 1694 the Bank of England was established to raise money for King William III’s war against France. The Bank started to issue notes in return for deposits. Therefore, the money supply for the first time began to include paper currency. By 1695 the first fraud took place. The authorities prosecuted Daniel Perrismore for forging sixty £100 notes. This incident caused the Bank of England to introduce a watermark in the paper to prevent such fraud. This was further enhanced by making counterfeiting subjected to the death penalty as a felony resulting in the confiscation of all your wealth and throwing your family out of the street as well. Pictured here, is a protest imitation note. The law was being prosecuted on the mere possession of a forged note. The complaint here was that these one-pound notes were easily forged and innocent people were duped, thereby committing a felony by mere possession. They were being hanged with no proof that they created the forgery – merely that they possessed one. This was creating an incentive not to even accept the notes in transactions.

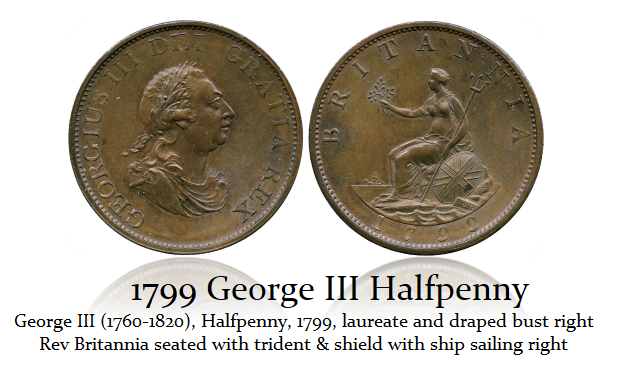

George I, II, and III all issued copper halfpennies. George III’s halfpennies were dated 1770 to 1772. The economic hard times no doubt contributed to the riots of 1780. After those events, at Newgate Prison in March 1782 a female alleged counterfeiter of halfpennies was hanged. She was then fixed to a stake and burned before the debtor’s door at Newgate prison in London as a further example of not to counterfeit.

In a letter to Lord Hawkesbury on April 14th, 1789, Matthew Boulton, who is considered the Grandfather of modern coinage, commented

“In the course of my journeys, I observe that I receive upon average two-thirds counterfeit halfpence for change at toll-gates, etc., and I believe the evil is daily increasing, as the spurious money is carried into circulation by the lowest class of manufacturers, who pay with it the principal part of the wages of the poor people they employ”.

Boulton’s contract in 1797 to produce the Cartwheel pennies and twopences, thwarting the counterfeiters, did not extend to producing the halfpenny, though Boulton had expected that it would, and had prepared patterns of the appropriate size and weight in accordance with his ideas on the intrinsic value of copper coins. The reason the government gave for the omission of the denomination from the contract was that a large number of de facto halfpennies (including tokens and fakes) would be driven out of circulation and Boulton would be unable to produce enough coins to meet the demand that would ensue.

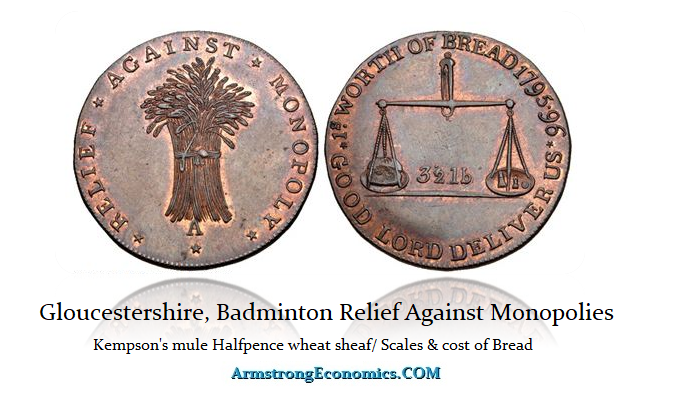

To avoid being hung for counterfeiting and burned at the stake, there was a multitude of halfpenny tokens. Many were of a political nature as this one complaining about the cost of bread. The government yielded to the private halfpenny tokens which became the majority of the small change. The overall public demand for legal halfpennies soon forced the government to change its mind, and in 1798 a contract was issued to Boulton for him to produce halfpennies and farthings dated 1799.

Interestingly, it was also at this time when inflation sent the price of copper rising, and consequently, the weight of the coins was reduced slightly, which resulted in them not being as popular as expected. In 1806 a further 427.5 tons of copper was struck into halfpennies by Boulton, but the price of copper had risen again and the weight was even less than the 1799 issue. This time, however, there was no unfavorable reaction from the public, so perhaps the national obsession with “intrinsic value” had run its course.

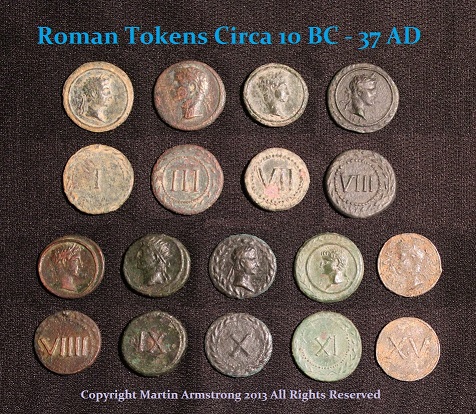

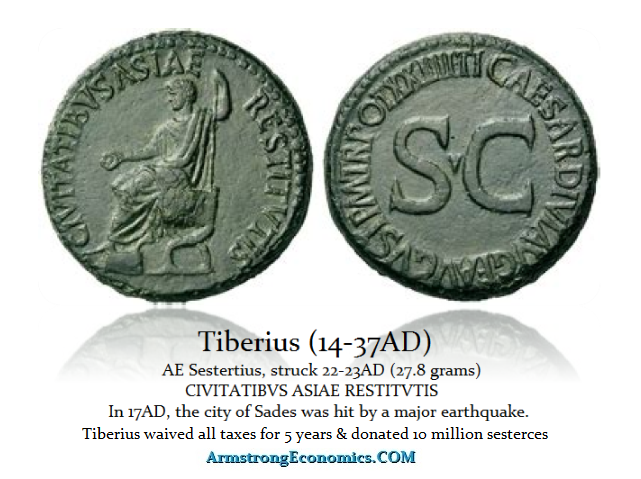

This was a very curious period where private money dominated the money supply for halfpennies. There are other periods where this has emerged in history primarily due to the shortage of real official money. One of the earliest such periods was during the reign of the Roman Emperor Tiberius (14-37AD).

Tiberius was legendary to be a frugal emperor. His deliberate contraction in creating new money led to the Financial Panic of 33AD. As far as Quantitative Easing, that too was nothing new. Tiberius offered loans INTEREST-FREE, but they had a limitation of three years. This was to prevent people from being forced to sell their estates further depressing land values.

There was a major earthquake in Asia, modern Turkey, and this was so devastating, he issued coins stating they were for the relief of Asia. He also waived all taxes in the region for 5 years – something our modern-day politicians would never dream of.

The lesson from history reveals that at times there emerges the acceptance of private money. During the 1870s, we also see private tokens circulating as money in the United States. Collectors call them the Hard Times Tokens. The very same thing took place during the American Civil War.

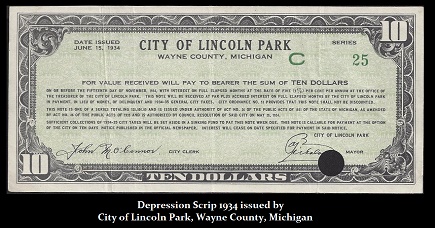

During the Great Depression, the shortage of money led to more than 200 cities issuing their own paper currency. As long as everyone in town accepted it, these Depressions Scrips enable people to work and to be paid locally when there was simply not enough federal money to go around.

During the Hyperinflation in Germany of the 1920s, there again we see private currency being printed known as NOTGELD. Therefore, in the end, when the confidence in government declines, society is compelled to return to a barter-based society and that is when we begin to see private forms of money take hold.

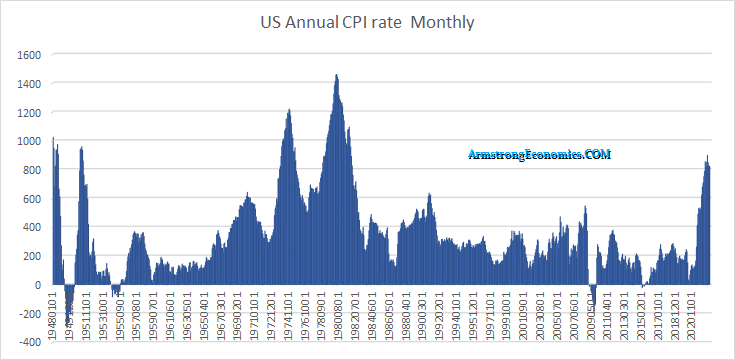

Our inflation models came in at 32% for 2022. This does not include things like paper clips to bring down the entire average. This number is the basic core inflation that consists of food, energy, and transportation. We do not include housing values which rose about 11% in 2022, but because that is the national average, it understands places such as Texas and Flordia and over states California and areas such as Chicago.

Our index attempts to reflect the national core inflation of things that most people use. The largest increase was obvious fuel between gasoline and diesel used in trucking and homes averaging 65%+, eggs were up nearly 50%, flour rose by 25%, cooking oil 23%, Butter was up 35%, Chicken by 14%, and Rice by 18%.

The more things you throw in, the lower the inflation rate. The national average rise in rental rates was 7.8%, in Florida it was 8.5%, and in NYC 1.5% when controlled.

If we broaden the list to include rents and coffee, which was up 15%, we can bring it down to about 27%. The Fed broaden the scope so widely that the rate come down to about 7%. The more you include, the lower the inflation rate. The object is to reduce government spending which is indexed to the CPI.

For those who have asked for the original 1995/1996 Tax Proposal that was on Capitol Hill in a single file, here it is. For those who just want the sections in a more manageable manner, click on this like here.

There is an onslaught of misinformation about the Federal Reserve from everything that it can go bankrupt, and the Treasury will become a second central bank, and of course, the Fed is really the cause of inflation and its balance sheet. The proposal by Janey Yellen to buy in long-term debt and swap it with short-term is not “creating” money for the Treasury has no such power. It was a proposal for a debt swap to shorten the yield curve. The first proposition that the Fed can go bankrupt only suggests that people do not comprehend that the Fed is different entirely from the European Central Bank.

The Fed has the authority to create elastic money for it followed the very idea of J.P. Morgan and how he saved the economy during the Panic of 1907. The Fed can create money when there is a shortage due to economic contractions, and it can then reduce its balance sheet reducing the money supply. When the Fed was created, it was established with branches around the country because the Panic of 1907 exposed that there were regional capital flow problems. The 1906 San Francisco Earthquake drained the cash from the East where all the insurance companies were.

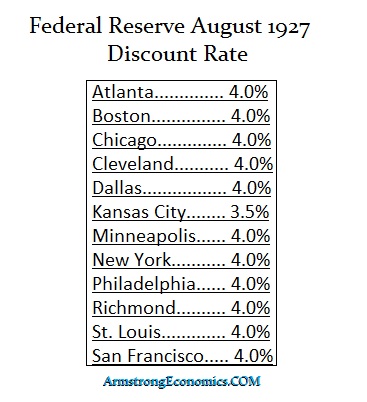

As we can see from this clip of rates in 1927, each branch was independent. There was an excess case in Kansas City so they lowered the interest rates there in hopes that capital would migrate to the other districts to earn more interest. All of that was eliminated by Franklin D. Roosevelt who wanted (1) to stack the Supreme Court to approve his Marxist agenda, which failed, and then he usurped all the power of the Federal Reserve and created the Washington headquarters and the President then was to appoint the head of the Federal Reserve and to illegally lobby him to ensure that his presidential agenda was to be the policy at the Federal Reserve. There was no more independence of the branches.

When Biden was running in 2020, he actually proposed requiring the Federal Reserve to regularly report on what they are doing to close economic gaps that exist along racial lines in the United States. Biden has viewed the Fed as a social tool and he has been making efforts to manipulate the Federal Reserve which will be extremely dangerous if they are carried out. Now, the Biden Administration is talking about closing branches of the Federal Reserve and replacing those board members with his hand-picked political cronies. In January 2022, he was pushing for black economists to be appointed to the Federal Reserve Board. My concern is that academics have ZERO experience and do not really understand the global economy trapped by domestic Keynesian Economics.

It was Paul Volcker who Chaired the Fed into the high in the interest rates back in 1981 who concluded in his Rediscovery of the Business Cycle that “it was not until the events of 1974 and 1975, when a recession sprung on an unsuspecting world with an intensity unmatched in the post-World War II period, that the lessons of the ‘New Economics’ were seriously challenged.” However, former Fed Chair Ben Bernanke has suggested that the Fed’s failure to contain inflation during the 1970s traced back to the political forces that shaped the Fed chairs in charge that he expressed in his book “21st Century Monetary Policy.” He wrote that the inflation of the ’70s puzzled economists relying on the 1958-ventage Phillips Curve, which would have predicted high inflation only in combination with extremely low unemployment rates. Bernanke admitted that the Phillips curve had “broken down” during the 1970s.

The critical problem with the entire way we view inflation rests on the QTM (Quantity Theory of Money) and the assumption that a mere increase in supply must produce inflation. There is absolutely nothing in the economic data that supports these old theories that were based upon (1) fixed exchange rates, and (2) the supply & demand theory dates back to the days of coinage. It was John Law who came up with the supply/demand theory that everyone else plagiarized, including Adam Smith. John Law’s writings influenced many, although they would never admit it. He was clearly the FIRST to use the term DEMAND and he was certainly the FIRST to join it with the word SUPPLY, for only a trader could have seen this connection in the price movements of anything.

The greatest fallacy of Keynesian Economics, Supply v Demand, and the Phillips Curve is that they have ALL failed because the US dollar is the reserve currency of the world and by default, the Federal Reserve has become the central bank of the world. With Biden desperate to get his hands around the neck of the Federal Reserve and force it to yield to his political agenda, threatens more than merely the US economy – but the entire world. Bernanke acknowledges in his book:

“Martin, my boys are dying in Vietnam, and you won’t print the money I need,” President Lyndon B. Johnson reportedly told then-Fed Chair William McChesney Martin Jr. at his Texas ranch after the central bank announced a half-point increase to its key discount rate over inflation fears, Bernanke writes. White House tapes, meanwhile, reveal President Richard Nixon frequently appealing to Fed Chair Arthur Burns’ Republican-party ties to clear the runway for more easy-money policies, with one call going as far as urging the Fed chair not to make any policy decisions that could “hurt us” in the November 1972 election.

I warned the Fed back then that buying in 30-year bonds during the 2007-2009 Financial Crisis, would NOT stimulate the domestic economy for one simple reason and this is why both the goldbugs and central bankers have been wrong. The domestic money supply DID NOT increase to stimulate when China was saying thank you very much and swapping their 30-year holdings for 10-year or less. The assumption that any central bank can control the domestic economy is absurd. The holdings of debt are global. Therefore, buying in 30-year bonds to reduce the supply in hopes of reducing the mortgage rates failed because the money did not stay in the USA. That is why the Fed then began to buy the mortgaged-backed securities because that was a more direct impact domestically.

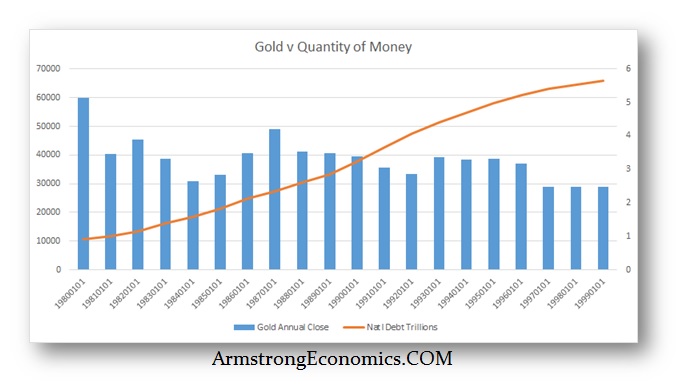

As the money supply increased and the national debt rose consistently, gold declined from 1980 into 1999 for 19 years. All the theories of inflation driving gold higher were simply wrong just as the central bankers relied on the very same theories.

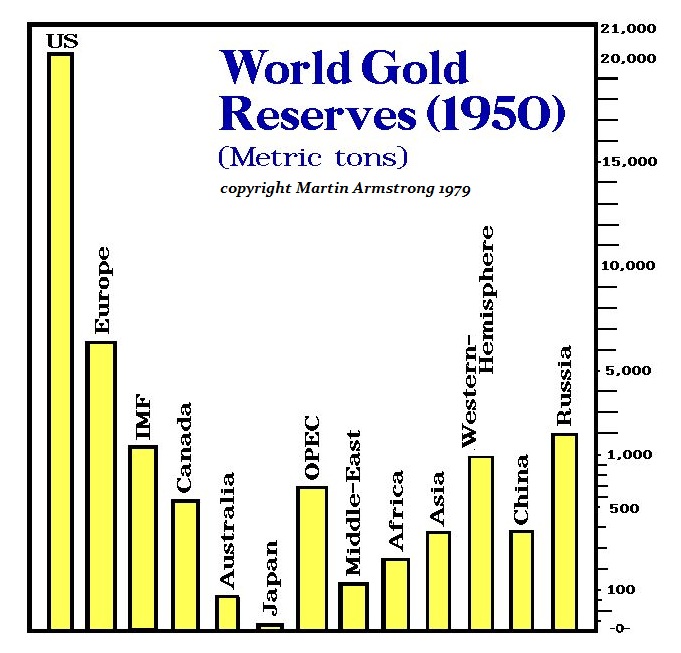

It was World War I and II that drove the gold to flee to the United States so by 1950, there was no choice but to make the dollar the reserve currency. Yet more significant was the realization that the factor which produced that result was ENTIRELY external to the domestic economy. Therefore, all the economic theories were bogus because they were all focused on domestic policy thanks to Karl Marx whose central theory was the government possessed the power to eliminate the business cycle by confiscating all private assets. That altered human nature and created economic stagnation. Nevertheless, Keynes and everyone else have sought to accomplish the very same authority that Marx maintained existed.

This focus on GDP (Gross Domestic Product) has reversed the GNP (Gross National Product), which was more global in its scope. If we attributed world trade to the flag the company flies rather than where it sets up a plant, then you would see that the United States has a trade surplus and not a trade deficit. This is also a backdrop to the reserve status of the dollar. Perhaps the greatest of all the wild proposals is that somehow Bitcoin will rise from the ashes and become the new Reserve Currency of the world. So all governments will issue debt in Bitcoin? Politicians will never be able to run for office and Socialism must collapse.

Rather than betting on the power grid to survive if governments collapse, I think we will see the pre-1965 silver coins return for a medium of exchange and gold for larger transactions. I have said plenty of times, GOLD will NOT rise as a hedge against inflation, it is a hedge against the collapse in confidence of the government.

As I have written before, when the Japanese government lost the confidence of the people, they lost the ability to produce any money for 600 years. The people used the coins of China and bags of rice – no Japanese coins were ever acceptable for 600 years which was the same time interval it took to reestablish gold in Europe following the fall of the Roman Empire.

Armstrong Economics Blog/Interest Rates Re-Posted Dec 14, 2022 by Martin Armstrongpread the love

The Central Bank Dilemma has become a major crisis in and of itself. I have been warning these past years that the ONLY tool a central bank has is manipulating the interest rates. Quantitative Easing was primarily to influence long-term rates indirectly since the Fed can only set short-term rates. During the past nine months, Fed Chairman Jerome Powell has raised interest rates at the fastest pace of any Federal Reserve chair since the 1980s. While some complain that this has triggered a stock market rout, and caused the housing market to come to a standstill, others argue that he has increased the fears of an imminent recession.

That was the domestic part. The Fed’s raising of interest rates has impacted the emerging markets including contributing to the chaos in the financial markets in China since many banks and provinces borrowed in dollars to save interest rates – or so they thought. It has forced the European Central Bank to raise interest rates and the net result was to unleash a crisis in long-term debt where life companies and pension funds cannot continue to buy the long-term with rates rising and bonds declining the day after you just bought a traunch.

Janet Yellen, who wants to hunt down everyone who sold a used bike on eBay for $600, understands the crisis we have erupting in debt because of rising interest rates and investors are afraid of the long end. Her proposal to buy in the long-term and swap it for the short-term recognizes the fact that we have a major debt crisis unfolding and she has come up with another scheme to keep kicking the can down the road.

Consequently, with inflation hitting 40-year highs, the warning signs are there that the central banks cannot do anything to address the economic crisis. Hence, initially, Fed officials were unanimous that rates needed to rise aggressively. Now, however, there are cracks in that view. These cracks will become fissures over how this type of inflation is NOT speculative but shortages set in motion by COVID and then accelerated by this drive for war with Russia and the insane sanctions they imposed on even private citizens.

While some expect inflation to cool steadily next year and want to stop raising rates soon, the problem is that inflation driven by shortages will not subside with a reduction in demand. Even real estate replacement costs have risen despite the fact that the market has started to pause. The cost to build a home in many areas is already higher than existing homes, which tends to create a floor before prices. Others worry inflation won’t ease enough next year in the face of a war that is escalating, and they defer to the old standard of raising interest rates to temper inflation.

That leaves Chairman Powell struggling in the eternal seas of politics lost in the middle as the arguments get louder on both sides. Powell will be challenged trying to chart a course through war, stagflations, and complete fiscal mismanagement by our politicians. The next stage of interest-rate policy presents very difficult questions concerning how high to raise rates from here, and how long to hold them at that level in this Pyhric War against Inflation.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America