Amstrong Economics Blog/Cryptocurrency Re-Posted Jun 12, 2023 by Martin Armstrong

QUESTION: Dear Mr. Armstrong,

could you please explain what happens in technical terms from a capital flow perspective, when confidence is lost and hyperinflation starts to begin?

For example Turkey. When Erdogan was elected i think you wrote that ever since the lira started dropping. So confidence in politics is key. Do you think one day we will see hyperinflation in Turkey?

And another example, is Yugoslavia: what caused the hyperinflation (in technical terms/capital flow perspective)? Are foreign investors getting rid of the dinars? Too many dinars than suddenly rushed back into Yugoslavia causing hyperinflation?

Regards,

Magdalena Š.

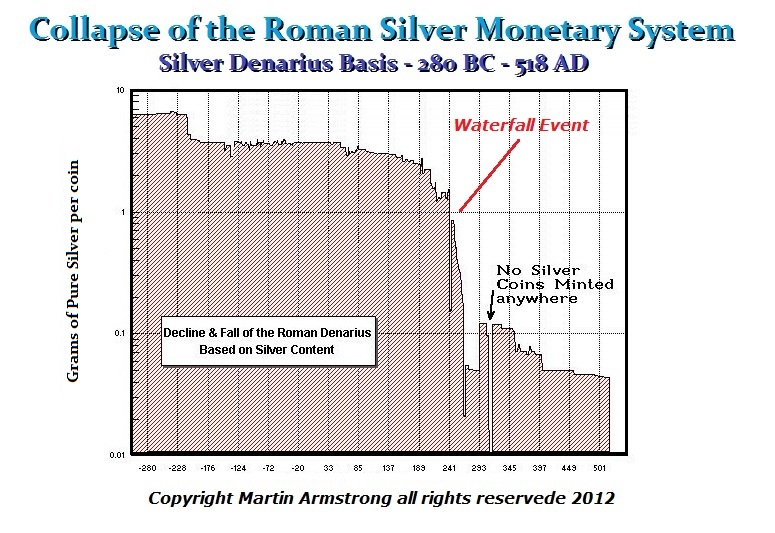

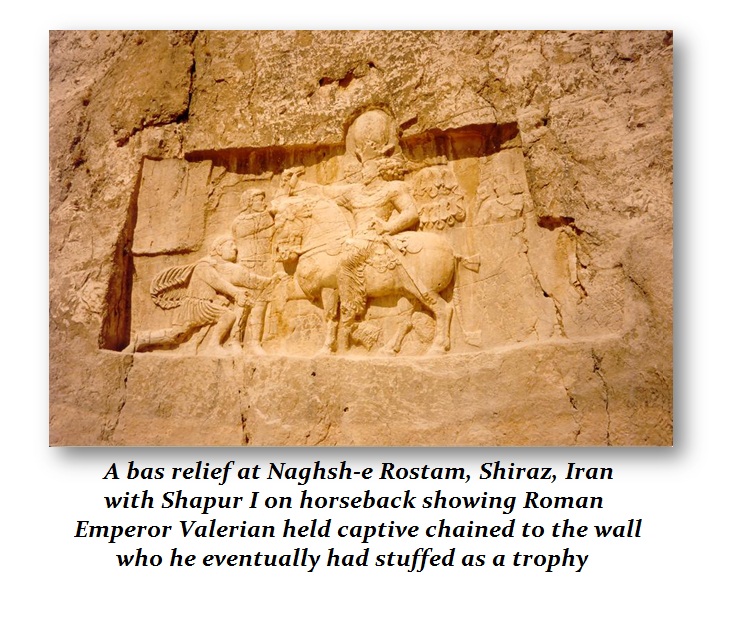

ANSWER: The misnomer about hyperinflation is that it is caused by printing money. It is a RESPONSE to the collapse in the confidence of the government. If we look at the 3rd century, this is where we find the greatest number of hoards of ancient coins. What began this was the capture of Valerian I by the Persians in 260AD.

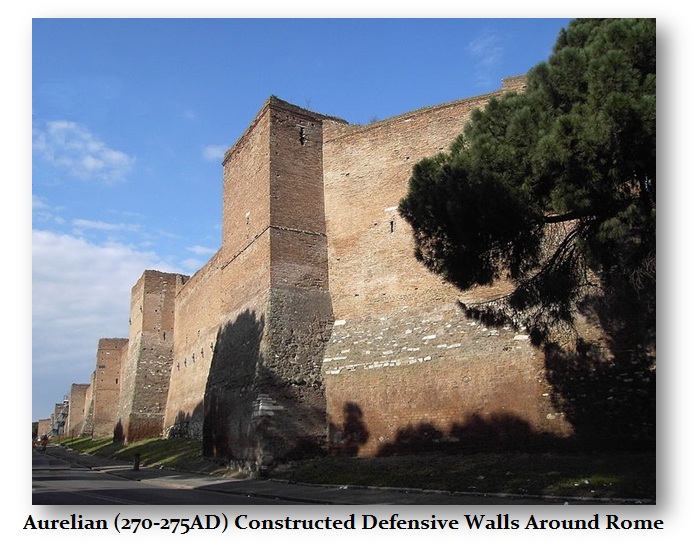

Valerian was the first Roman Emperor to be captured and Rome was unable to recuse him. That shook the confidence of the Roman people, but it also was a signal to the barbarian tribes in the North that if the Persians could do it, they could as well. Within 10 years, Emperor Aurelian constructed the great wall around Rome. Never before did Romans have such a defensive wall. That had a powerful army.

There was a trend toward debasing the silver coinage which began with Nero to try to fund the rebuilding of Rome after the Great Fire. But that did not undermine the confidence in the Roman Monetary System any more than our perpetual deficit spending since World War II.

However, a spark is ignited and suddenly that trend turns into what I have called a Waterfall event in the purchasing power of the currency. Such an event has taken various forms. However, the end result is the collapse in the confidence of the government and as a result, that is when you get that waterfall event.

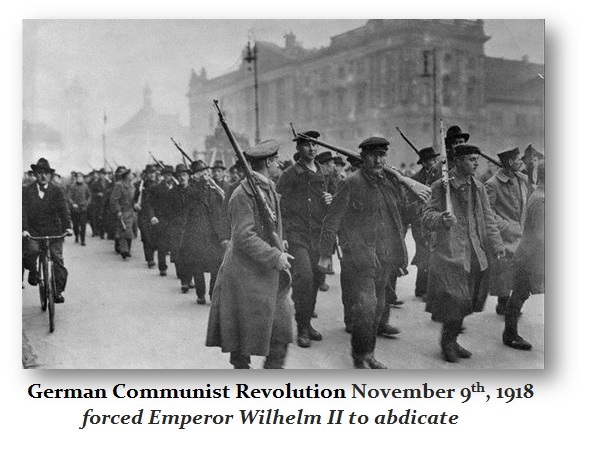

In the case of Germany, Yugoslavia, Hungary, etc, there was a 1918 Revolution where communists seized power and the emperor of Germany lost power. In that case, they actually asked Russia to take Germany after their revolution in 1917. This was the beginning of the Weimar Republic.

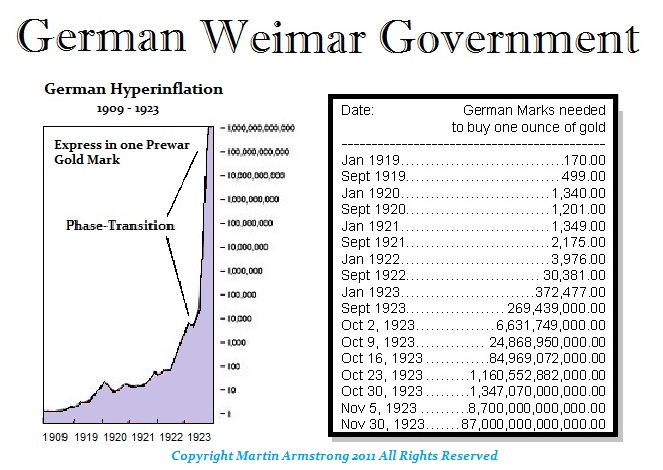

Germany was saddled with reparation payments demanded by France. First, you had a communist revolution and people with capital began to flee to other places in Europe or certainly move their money out of German banks. It was this drain of wealth that forced the Weimar Republic to print money to try to make their reparation payments. Then in December 1922, they seized 10% of everyone’s assets and handed them a bond.

Here you can see that after that December 1922 confiscation, hyperinflation simply took over. It was NOT the printing of money that caused the hyperinflation it was the collapse of confidence FIRST which then compels the government to expand the money supply lacking taxation revenues etc.

I suspect the spark this time may be the Digital Currency and the proposed cancellation of paper currency. This is why people are moving to anything tangible from real estate, gold, silver, ancient coins, and even equities. With DIGITAL CURRENCY they will have capital controls and prevent you from even moving money outside of your country.

The precise day of the ECM was the announcement of the IMF Digital Currency which they intend to replace the US dollar as the reserve currency. This may be timed with the turning point in 2024. It is unlikely that they would cancel paper currencies before the 2024 election. This is all being