Armstrong Economics Blog/Cryptocurrency Re-Posted Jul 28, 2023 by Martin Armstrong

QUESTION: You said that when Rome fell it took 700 years before gold coins reappeared. Are we facing something like that again?

PO

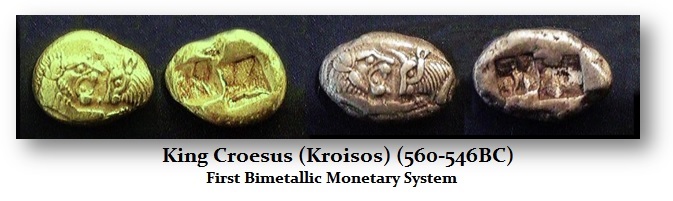

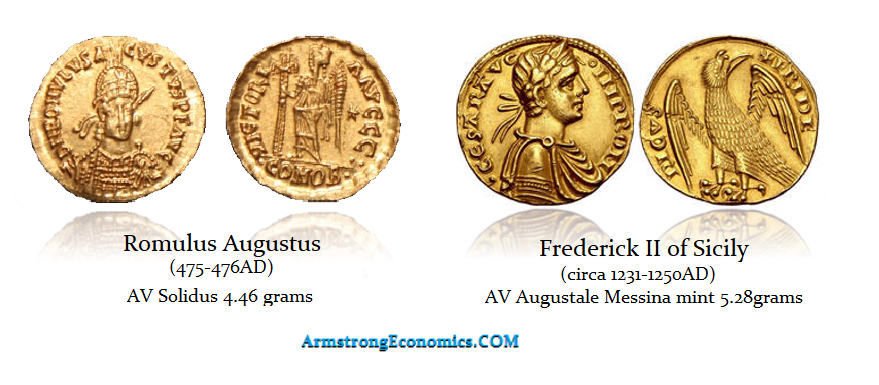

ANSWER: Yes, when Rome fell, gold continued in the East under the Byzantine and Islamic Empires. However, in Europe, the last Western emperor was Romulus Augustus (475-476AD) who was a puppet anyhow. He was a young son, whereas today, we have senile leaders who are puppets and incapable of independent rational thought. The first gold coin to reappear in Western Europe was that of Frederick II of Sicily (1231-1250AD). The Augustale was a gold denomination of about 5 and a half grams which Frederick II introduced to Sicily in 1231AD, and it was primarily issued for international trade.

Actually, Fibonacci (1170-1240 AD) published in 1202 his “Liber Abaci” (Book of Abacus). He introduced Hindu-Arabic numerals into Western culture. Suddenly, this allowed the calculation of numbers that were not taught in schools and was unknown in Christian circles. Only a very small group of intellectuals had access to translations of the Arab mathematician al-Khwarizmi (780-850 AD). The techniques that Fibonacci introduced were groundbreaking to re-establish a culture that lost its identity with the fall of Rome. Fibonacci illustrated practical problems on how to calculate profit margin, money changing, barter, conversion of weights and measures, partnerships, and, last but not least, interest. He also introduced some geometry and algebra.

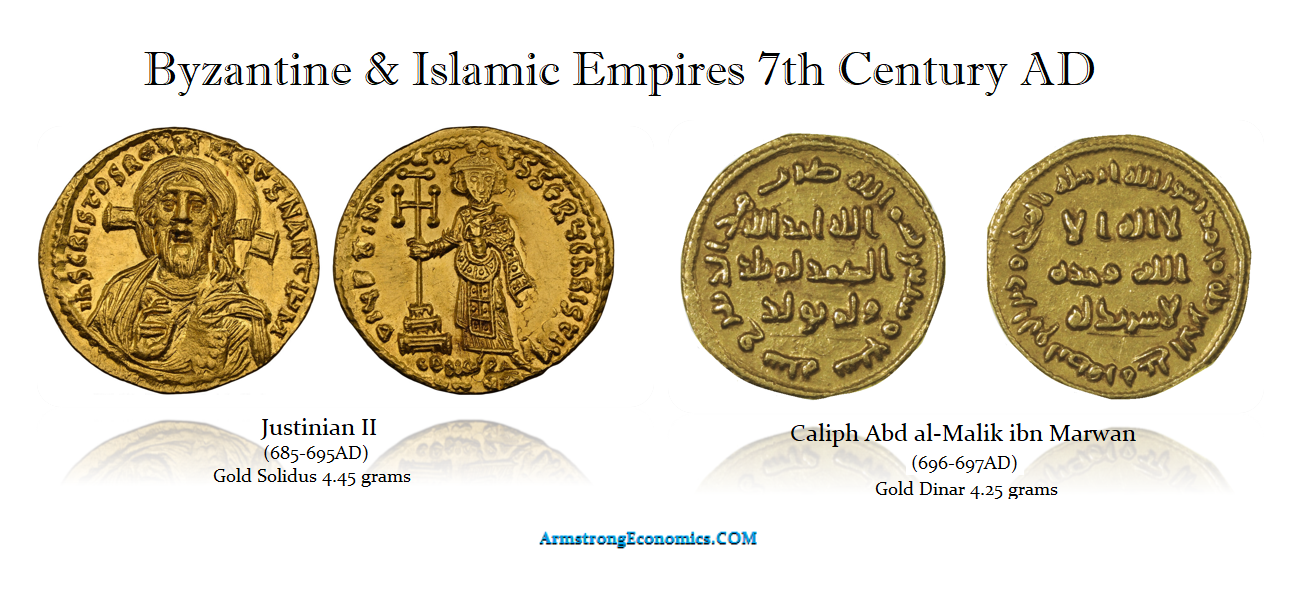

However, Fibonacci’s work was so earth-shattering it became the topic of discussion and caught the attention of King Frederick II of Sicily. I believe it was Fibonacci’s introduction to mathematics that also inspired Frederick II to even reintroduce gold coinage in order to trade with the outside world. At the time, that included the Arabs as well as the Byzantines. The gold dinar was the Islamic medieval gold coin first issued in 696–697AD by Caliph Abd al-Malik ibn Marwan with a weight of 4.25 grams. Frederick II made his coin about 1 gram heavier in order to project economic power.

The introduction of CBDC is highly dangerous in war; even a nuclear blast also sends out an EM pulse that will destroy electronics. If I were Russia or China, I would NOT move to any sort of digital currency and then use an EMP against the United States. The entire economy would collapse. People would not even be able to buy anything. We have idiots in power who are so greedy, looking at the power this will place in their hands, they are ignoring the risks. This could mark the collapse of Western society, sending us back to the days of Barter.

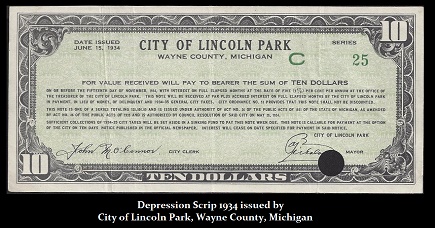

The Post-2032 era would most likely be fragmented rather than national states as we know them today. There will most likely emerge regional currencies, as we have witnessed throughout history many times. Even during the Great Depression, over 200 US cities resorted to issuing their own money.