Published on Mar 19, 2017

This video gives you everything you need to know about how Donald Trump was surveilled by Barack Obama.

This video gives you everything you need to know about how Donald Trump was surveilled by Barack Obama.

Following the Trump administration’s recent federal illegal immigration crackdowns, organizers have canceled El Carnaval de Puebla, a major Cinco De Mayo celebration in Philadelphia.

This week, ICE announced that 248 people in Pennsylvania, Delaware and West Virginia are now in federal custody awaiting deportation after a two-week sweep.

And now, NBC reports that the annual parade through South Philadelphia has taken place in late April or early May for the last decade and is the city’s largest Cinco de Mayo celebration. Organizer Edgar Ramirez said as many as 15,000 gather from as far as New England and Chicago.

“The group of six organizers decided to cancel unanimously,” Ramirez said. “Everyone is offended by the actions of ICE. They did not feel comfortable holding the event.”

The decision to cancel El Carnaval, Ramirez said in an interview Friday, was “sad but responsible” in light of the immigration crackdown by federal authorities.

“We have people who travel all the way from Chicago, Connecticut and New York. We don’t want anything to happen to them,” he said.

ICE Officer Khaalid Walls of the agency’s Philadelphia office said in an email that “ICE’s enforcement actions are targeted and lead driven. ICE does not conduct sweeps or raids that target aliens indiscriminately.”

As for a return of Carnaval, organizers will decide sometime in the future if the parade once again dances its way through the heavily Latino Pennsport neighborhood, Ramirez said. “Let’s see how things are next year,” he said.

I’ve been very surprised with the amount of vocal support for a Bitcoin Hard Fork – especially from many Bitcoin supporters who believe it is either inevitable or “not a bad thing”. I get it, but you’re wrong. I know everyone is tired of the scaling debate. I’m not going to go into the technical details around this debate for this post, but instead, I’m going to focus this post on debunking the non-technical arguments for a Hard Fork and highlighting the ensuing confusion and market impact that a contentious Bitcoin Hard Fork will have, if we indeed have a split between Bitcoin Core and Bitcoin Unlimited.

Exchanges today have just confirmed they will be listing BTU as an altcoin if there is a Hard Fork?—?this scares me because although the industry person knows what an altcoin is?—?the average person outside the industry doesn’t. This was the catalyst for my post today.

I have predicted that Bitcoin should hit $3,000 by end of this year?—?but not if there is a contentious Hard Fork.

Keep in mind that the hope of this post is that it changes the mindset around support for a contentious Hard Fork, which creates another Bitcoin, because I believe this needs to be avoided at all costs. In fact, if any of the scenarios below begin to play out, we’re already in trouble… If you agree with the logic below, translate this post into Mandarin and any other language and let’s convince miners and the community to not consider even doing a Bitcoin Unlimited Hard Fork.

Also, even after the big bug in Bitcoin Unlimited yesterday, more nodes are back up and running signalling it. I know many people don’t believe it will happen and they may be right, but we cannot ignore a persistent and growing threat to the ecosystem and so I’m speaking out about it now.

For more background on the Bitcoin Unlimited vs Segwit debate, check the bottom of this post for links, including a number of technical reasons why a Hard Fork is a risky proposition for Bitcoin. I’m also not delving into the technical debate as that has been done ad nauseam elsewhere.

It’s inarguable that Bitcoin is the single strongest brand in the crypto space. I believe it probably received $2–5bn in free media exposure over the years. A Hard Fork would create 2 brands of Bitcoin?—?essentially handing over some brand value to Bitcoin Unlimited. I wrote a post about Bitcoin’s power and network effect over 2 years ago?—?it’s worth reading if you haven’t.

The moment there is a hard fork, we are going to allow brand confusion to step in. This is a HORRIBLE idea.

The security of the Bitcoin network comes from the computational hash power that the miners bring. This is driven by the price of Bitcoin?—?higher the price, more hashing power. High prices are in turn driven by market demand. Market demand is driven by PR & media and the long term narrative that Bitcoin is the first and only true cryptocurrency which is a long term store of value. If we mess with this, I believe we can expect negative consequences…

When the media declared Bitcoin was dead in 2014, it took us a long time to recover, price wise.

Bitcoin Unlimited will just become an altcoin if it doesn’t have majority support?—?why does it matter?

In the event that 35–50% of miners broke away and created an altcoin, in this case?—?Bitcoin Unlimited, we would essentially then have 2 coins. Bitcoin (BTC) & Bitcoin Unlimited (BTU). One could argue that BTU is not Bitcoin, but it may still be called Bitcoin by the man on the street. For instance, if he buys what he thinks is Bitcoin, to buy some gift cards at Gyft, only to discover that he bought the wrong Bitcoin?—?can you imagine the issues that merchants are going to have now in dealing with the customer support fallout. In all or many cases, they may even remove Bitcoin as a payment method, unless the business is Bitcoin only, in order to avoid customer confusion or the risk of the individual coins fluctuating in price between purchase and usage.

As much as the crypto world is smart enough to understand the differences, the average person barely understands Bitcoin today and forcing them to tell the difference between BTU & BTC is going to be a big challenge.

Let’s not forget some other important points: Roger Ver (the force behind Bitcoin Unlimited aka Bitcoin Jesus) also owns Bitcoin.com (and a number of other strong domain names) and he also owns a couple of hundred thousand Bitcoins (apparently around 300k BTC).

When Bitcoin forks, everyone who is holding BTC, would receive an equal amount of BTU?—?so Roger would have presumably 600k coins (300BTC +300 BTU) according to industry rumours.

The moment Bitcoin splits, he is able to legitimize Bitcoin Unlimited using Bitcoin.com?—?which for the uninitiated would actually be a legitimate source of information, and is highly ranked on search engines like Google. Bitcoin Unlimited would effectively become Bitcoin.com. My first company was in search engine marketing?—?I know this world all too well.

If there was a fork and Roger wanted to pump Bitcoin Unlimited, he could literally dump all his Bitcoin (BTC) holdings into the market. I don’t want to even guess what 300,000+ coins being moved in a short space of time would do to prices, especially after a contentious hard fork where new money investors would already be on the sidelines. This happened to Ether Classic after the Ether Fork?—?the Ether Foundation sold off 90% of their coins and depressed the price. Just the threat of this alone will cause the market to tank for BTC, just for starters. If Roger wants to kill Bitcoin’s price and legitimacy, there is no reason to not fear this and the market will start pricing in this risk.

Roger would not be the only person to sell down BTC. Other BTU loyalists who have two sets of coins would do the same, initially in order to drive down BTC. Conversely, all the long term BTC holders would now receive equal amounts of BTU. Even the most hard core BTC Hodlers would probably sell down BTU with all their BTU coins in order to try and crush it. Given the importance of BTC as a reserve asset in altcoins, many traders could use weakness in price to short BTC and drive their altcoin prices up.

Long story short?—?none of these scenarios (or any others I can think of) play out well for Bitcoin, either in the markets or the media and this fundamental divide means that you’re going to have increased volatility from both sides, as more coins will pour into the market?—?crushing any demand side driven rally.

The whole point about Bitcoin being a long term store of value is that there are only 21m coins, ever. Stability, security and scarcity are the differentiation properties of Bitcoin, a contentious Hard Fork attacks these properties and will be strongly reflected in the price. After a Hard Fork, we will be sitting with 33m “Bitcoins”, on track for 42m and we’ll be having arguments about which one is the legitimate Bitcoin for years to come. You can expect legal cases to arise around the use of the brand, as the Ethereum Classic Investment Trust has shown.

Imagine someone says: I want to buy Bitcoin. Next question is: Which one?! After that, the very next question will be :

“What if one of these coins fork again?—?then we will have 63m coins, and so on and so forth.”

But, aren’t two coins are better than one! The market will adjust!

Let’s say the price of Bitcoin today is $1,000?—?if doing a 75%/25% split would now mean that you have have 2 coins, this should mean they are worth $1,000 ($750+$250). So, I did a simplified calc based on Metcalfe’s law, and it estimated the new coins combined could be worth more than 33% less almost immediately after a Hard Fork due to reduced network effects, and that’s assuming everything went well… With the ensuing FUD and negative press/media?—?you can expect this to drop even further! Bitcoin’s enemies can’t wait for an opportunity like this.

Creating two networks destroys network effects (payment providers, merchants, etc) and the Bitcoin price is non-linear to size of network, so the two coins combined will not equal the same price. You can compare this to the Ether split, as Bitcoin is at scale ($20bn) and Ether wasn’t at the time and it definitely set them back.

Bitcoin has died many times, it can survive a Hard Fork! Even Ethereum did.

Let’s start over. Ethereum is a B2B facing platform?—?consumers & media don’t know or really care about it. Bitcoin is a $20bn asset class. And yes, after the media declared Bitcoin dead after the last “bubble”, it took us 2+ years to rebuild the price by generating demand organically. The media attention this time during the recovery and cross the price of gold does not even come close to last time when it was taking off like a rocket. If a split is portrayed badly in the media and creates confusion, we will possibly go into another 2 years of sideways and down. Do we have that much time again with other competitors on the heels? And let’s be frank, a Hard Fork is not Bitcoin dying. It’s Bitcoin duplicating. Now we have two Bitcoins, both won’t die, maybe one will. Which one is the real Bitcoin? Do not underestimate how many enemies Bitcoin has?—?a fork will just give them all the ammunition they need to confuse the market.

Who cares if 30% of the miners fork off?

Bitcoin’s price is a function of faith and network security, given the large amount of computing power that goes into it. Metcalfe’s law dictates that the value of the network is the square of the network. By splitting the network even 70/30, it’s inarguable that it’s less secure. Yes, it could rebuild but, depending on the price of each coin after the split, hash power may move from one coin to the other. These are highly specialized machines and one coin surges in price, you can expect hash power to follow suit.

Remember that one of the biggest mining companies, Bitmain, is now signaling support for Bitcoin Unlimited. It’s very clear that the current difficulty of Bitcoin makes it harder and harder to compete in this market, but after a Hard Fork, there would need to be a difficulty adjustment on both new forks, given the reduced hash power?—?this opens up the opportunity for Bitcoin mining companies to sell more hardware to miners on both sides of each coin.

The sales of mining equipment are a huge economic disincentive to maintain the status quo without a block size increase, unless the Bitcoin price surges which I don’t believe will happen unless Segwit is adopted and then this debate is over. I called 1300 as a key resistance level and it’s proving to be.

Bitcoin was largely built on the premise that economic forces and self interest would help govern the security of the network. We talk a lot about decentralization but the reality is that the hardware that powers Bitcoin is produced by a handful of companies who also control mining pools which can be used against the network.

The real issue, I believe is two-fold. The community wants Bitcoin to be all things to all people?—?Roger wants cheap coffee transactions, Core wants to ensure its sufficiently decentralized and secure, Vinny wants a store of value, etc.

We have a governance problem in Bitcoin and we have no way to resolve conflict except to fight about it, publicly and given that it’s quasi-democratic, unless we all agree on something, nothing gets done. This has burned a lot of people and I can see why we have so many altcoins out there trying to replace Bitcoin.

Bitcoin cannot be all things to all people, at least, not a for a long time. Right now, it needs to be stable, secure and unchallenged. We can continue to argue amongst ourselves as a community, but for now I am against any contentious Hard Fork that would see us creating two separate code bases with two different brands of Bitcoin.

Companies like Coinbase, BitPay, Gyft, BitPesa, Bitgo and many others have invested years to build consumer adoption and understanding of Bitcoin and create outlets for people to use it. A fork now would undermine all these efforts, investments and limit adoption of Bitcoin in general. Unlike in the Ethereum Hard Fork, 100s of companies use Bitcoin and this would lead to a lot of counterproductivity. Companies should be focused on advancing adoption of their products, not in protocol fights. This debate has already been a strain on the community.

I understand and appreciate many of the different perspectives?—?some which I have not had the time to mention in this post, but given a balance of risks to the Bitcoin ecosystem, I believe that the adoption of Segwit right now is imperative in order for us to get to the next stage in the evolution of Bitcoin and remove the risks of a contentious Hard Fork. The Core Dev team has had a lot of criticism leveled at them and clearly they are not good at community relations, managing perceived conflicts of interests (like Blockstream’s involvement), which has resulted in emotions flaring up against them which is causing an uprising of sorts as we are now seeing. Technically, however, it’s inarguable that they are the best technical team in Bitcoin today.

If we all just breathe out, and put aside our differences and emotions (even just for a while), let’s accept that doing a Hard Fork right now is NOT in the best interest of Bitcoin and let’s please just adopt Segwit.

This post is not trying to be an endorsement or critique of either BU or Core. This post is asking the community to put aside their differences and come together to prevent an irreparable splinter.

I’ll keep posting more links below, but here one for starters:

Via Global Macro Monitor blog,

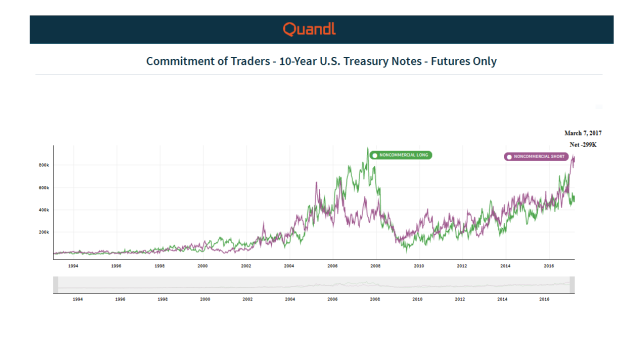

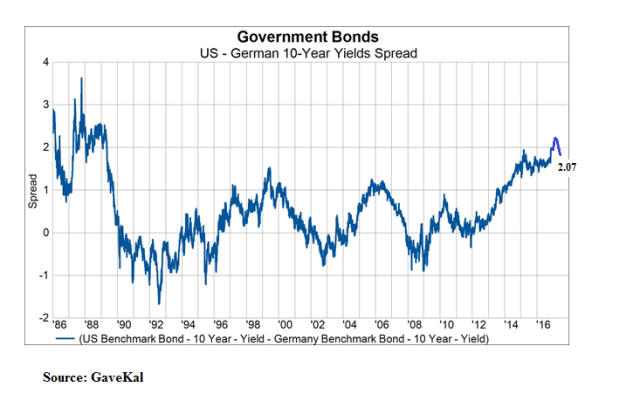

The Fed tightens on Wednesday and bonds rally. What the hay?

GaveKal, Jeff Gundlach, and Jim Bianco nailed it in that every spec and their mother are/were short 10-year Treasuries.

Source: Quandl (see here for interactive chart)

But this is only a small part of the story: The global bond markets are broken.

There are no signals, there is no noise. Trying to infer any sense of economic or financial information from bond yields is futile.

The intervention into the bond markets by central banks through quantitative easing (QE) in the big four sovereign bond markets – U.S., Japan, Eurozone, and UK – has created a structural shortage of risk-free instruments and distorted the most important price in the world — the yield on 10-year hard currency sovereign bonds.

Furthermore, past QE in the U.S, coupled with the recycling of foreign capital flows back into the U.S. bond market, has, in particular, created an acute structural shortage of longer-term Treasury securities. The totality of short positions of the fast money in both the cash and derivatives market are probably a much larger proportion of the effective float of longer-term marketable Treasury securities than what the market currently perceives. Hence the stickiness of U.S. bond yields.

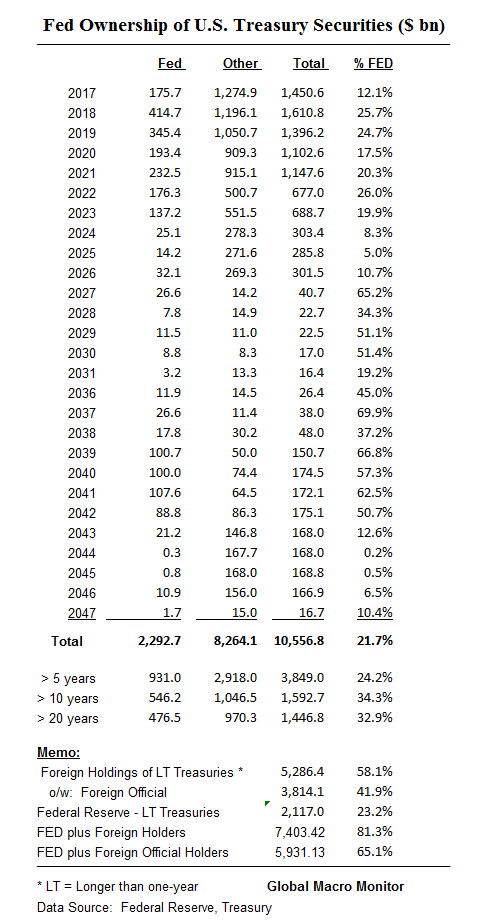

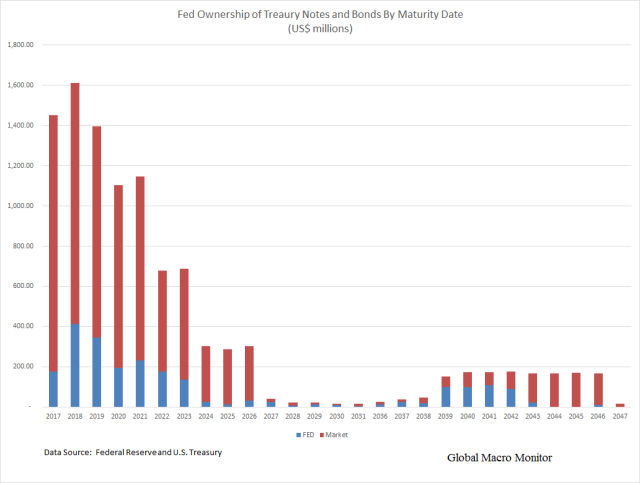

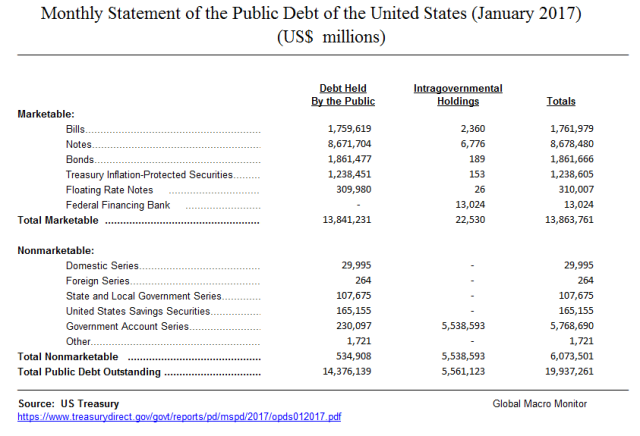

The table and chart below illustrate just how small the actual float of longer-term marketable U.S. Treasury securities is available to traders and investors. The data show the Fed owns about 35 percent of Treasury securities with maturities 10-years or longer. Note the data only include notes and bonds and excludes T-Bills.

The Fed’s holdings combined with foreign ownership of longer maturities — more than 1-year — exceeds 80 percent of marketable Treasuries outstanding. The Fed combined with just foreign official holdings, mainly, foreign central banks, is 65 percent of maturities longer than 1-year. Thus, almost 2/3rds of tradeable Treasuries longer than 1-year are held by entities with no sensitivity to market forces.

Note, the Treasury International Capital (TIC) data does not break down foreign holdings by year of maturity, only by short-term and long-term – that is, greater than 1-year.

.

.

.

.

We hear a lot these days about a 1994 bond market debacle. We lived through that bond bear and it wasn’t fun. However, the microstructure of the Treasury market is entirely different today than it was back then.

First, the Fed did not hold long-term Treasuries. Second, foreign holdings of Treasuries were only about 15 percent of the outstanding debt versus around 50 percent today and everybody, including, Ross Perot, who said the trade was “a no brainer”, were levered long riding the yield curve – short short-term, long long-term.

Foreign inflows, mainly the result of the recycling of U.S. current account deficits, resulted in Alan Greenspan’s bond market conundrum and the Fed losing control of the yield curve just prior to the 2007-08 financial crisis.

In this environment, long-term interest rates have trended lower in recent months even as the Federal Reserve has raised the level of the target federal funds rate by 150 basis points. This development contrasts with most experience, which suggests that, other things being equal, increasing short-term interest rates are normally accompanied by a rise in longer-term yields.

…In the current episode, however, the more-distant forward rates declined at the same time that short-term rates were rising. Indeed, the tenth-year tranche, which yielded 6-1/2 percent last June, is now at about 5-1/4 percent. During the same period, comparable real forward rates derived from quotes on Treasury inflation-indexed debt fell significantly as well, suggesting that only a portion of the decline in nominal forward rates in distant tranches is attributable to a drop in long-term inflation expectations.

A paper published by the Federal Reserve Board (FRB) in 2012 estimated the impact on interest rates of the capital flow recycling into the U.S. bond market,

We find that a $100 billion increase in foreign official inflows into U.S. Treasury notes and bonds lowers the 5-year yield by roughly 40 to 60 basis points in the short run. However, our VAR analysis shows that in the long-run, when we allow foreign private investors to react to the effects induced by a shock to foreign official holdings, the estimated effect is roughly -20 basis points per $100 billion. Putting these results into context, between 1995 and 2010 China acquired roughly $1.1 trillion in U.S. Treasury notes and bonds. A literal interpretation of our long-run estimates suggests that if China had not accumulated any foreign exchange reserves during this period, and therefore not acquired these $1.1 trillion in Treasuries, all else equal, the 5-year Treasury yield would have been roughly 2 percentage points higher by 2010. This effect is large enough to have implications for the effectiveness of monetary policy. – FRB

Extrapolating the above analysis to the current stock of foreign official Treasury holdings of around $4 trillion leads to nonsensical results, such as the 5-year yield should be 800 basis points higher than it is today. Obviously, the analysis should truncate the dependent variable – 5-year note yield — and ceteris paribus (other things being equal) does not hold in the real world.

But we should not miss the article’s main point that market interest rates would be much higher if not for foreign central bank interventions into their FX markets and the recycling of those reserves back into the Treasury market. We take the above analysis seriously but not literally and wonder if the Trump Administration considers it when they rail on “so-called” currency manipulators.

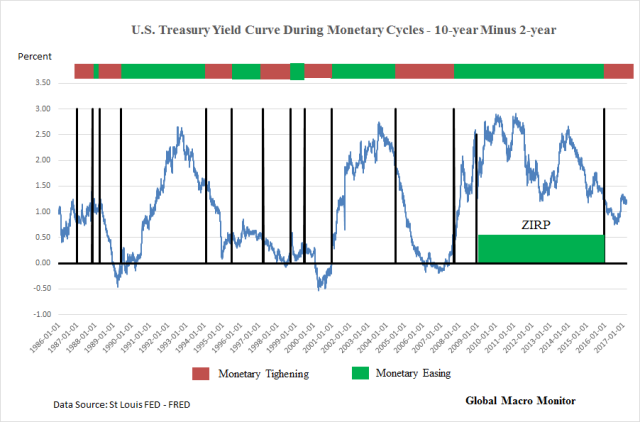

We have looked at the data and constructed some charts that show that in monetary tightening cycles in the U.S. the yield curve (10-2 years) usually flattens.

.

.

In only two of the past six prior tightenings did the 10-year bond rise in yield from the day of the first tightening to the day of the first easing. This is entirely possible due to the fact the Fed often “tightens until something breaks” and the bond market front runs the expected easing cycle.

During the 2004-07 tightening cycle, the era of the Greenspan bond market conundrum, for example, the 10-year yield managed to rise only a maximum of 64 bps during the entire cycle from a beginning yield of 4.62 percent to a cycle high yield of 5.26 percent. This as Greenspan raised the fed funds rate by 4.25 percent, from 1.0 percent to 5.25 percent.

Was the market forecasting the coming financial crisis? Hardly.

Alan Greenspan blames the Fed’s loss of control of the yield curve, mainly due to the recycling of capital flows by foreign central banks, as a major cause of the housing bubble. Notice the importance of the 10-year yield on the allocation of resources and on how its distortion can be at the root of financial and economic bubbles.

Those dreaded words, “this time is different.” We should warn readers that this time is truly different, however. When the Fed first raised interest rates in December 2015, for example, the 10-year yield was at 2.24 percent and more than 50-75 percent lower than at the beginning of any other monetary tightening cycle over the past 30 years. There are many “unprecedents” in this cycle and therefore more uncertainty.

.

.

Given the technical distortion of the bond market, we find it kind of silly with statements such as “what is the bond market telling us?” Nothing!

There is no price discovery. Given the intervention and distortion to bond yields caused by the Fed and foreign central banks, who knows what the right interest rate is for longer-term Treasury securities.

We will never forget the words of a prominent market strategist when rates were super depressed.

“ We’re in a depression. That is what the bond market is telling us.”

Even at the Friday close, we hear equity traders are worried about why the 10-year yield is so low and fell after Wednesday’s Fed tightening.

One of just many dangers of the lack of price discovery in the bond market is the potential formation of positive feedback loops, where other markets fail to discount these distortions and act accordingly. That is, for example, the equity markets sell off because they freak out interest rates are declining when they should be rising. Or the private sector fails to invest in CapX as they wrongly anticipate an economic downturn because of falling or excessively low bond yields. Their actions thus become a self-fulfilling prophecy.

A flatter than normal yield curve could also adversely affect bank lending. Look at how financial stocks have been underperforming recently as the yield curve has flattened about 7 bps this year.

Welcome to Bond Market Conundrum 2.0.

Asset prices are artificially elevated and foreign exchange rates are distorted due to the repression of the risk-free interest rates because of lack of supply. Capital has been misallocated and the Fed has once again lost control of the yield curve simply by the very fact it owns the yield curve.

Monetary policymakers probably won’t regain control of the yield curve until they begin to reduce their balance sheets and the supply/demand balance moves closer to equilibrium.

That’s when we suspect everybody and their mother will front run the central bank selling and we will have the real bond market debacle some in the market have been expecting. Will or can that day ever come? We don’t know.

Of course, governments could go on a tax cut/spending binge and increase the primary supply of government bonds. Possible but doubtful and a longer term story, if any.

Until then? We still believe bonds are in a slow bleed bear market, which will see fits of massive nutcracking short covering, as interest rates slowly drift higher.

Remember, there are no signals, there is no noise. Here’s to hoping the markets understand that.

The data points presented above should be taken as rough, but good, approximations. The dates of each source of data may differ and the same is true for the different data sources.

Furthermore, we may be entirely wrong in our conclusions.

Abraham Lincoln used to tell a story as a young Illinois circuit court lawyer when trying to convince the jury to render a verdict in his favor.

The story goes that Lawyer Lincoln was worried he had not convinced the jury during the closing argument of a civil case against a railroad. The jurors had gone to lunch to deliberate. Lincoln followed them and interrupted their dessert with a story about a farmer’s son gripped by panic,

“Pa, Pa, the hired man and sis are in the hay mow and she’s lifting up her skirt and he’s letting down his pants and they’re afixin’ to pee on the hay.” “Son, you got your facts absolutely right, but you’re drawing the wrong conclusion.”

The jury ruled in Lincoln’s favor.

Similarly, when looking at data and charts — the facts — we often draw the wrong conclusion about future direction.

Stay tuned.

Last week, we presented readers with the latest note from SocGen strategist. Albert Edwards, who explained why after so many years of false rate hike starts, the market not only responded to last week’s hike in a dovish manner – interpreting last Wednesday’s 0.25% hike as a 0.25% rate cut- but as Goldman Sachs showed previously, the dovish reaction was one of the strongest ones since the financial crisis, in other words: “the market no longer believes the Fed.” This is what Edwards said, citing his FX colleague Kit Juckes:

[T]he Fed’s reluctance to send an aggressive tightening signal, instead preferring to again shuffle upwards its dots just slightly, has disappointed markets. But to be fair, the problem isn’t really with the famous dots. It’s with the market, which just doesn’t believe the Fed will tighten as fast as they say they plan to (see left-hand chart below). If the market took the FOMC at their word and discounted a 3% Fed Funds rate at the end of 2019 and beyond, then we’d probably have a 3% nominal 10-year Treasury yield by now.”

That said, a 3% Fed Funds rate would also lead to steep selloff in risk assets as the dividend yield on the S&P, currently at about 2%, would be about 1% below the risk free rate, leading to a wholesale “great rotation” out of stocks.

And while the market may not believe the Fed is ready – and willing – to push rates that high, the relationship also cuts both ways.

As RBC also noted last week, explaining that while the Yellen put is alive and well, the market will simply not tighten financial conditions on its own, forcing Yellen to aggressively hike further… which the Fed may be reluctant to do.

That is the argument in a note released late last week by Morgan Stanley’s credit strategists, who note that while the party is still going strong, some 93 months into the current cycle, it may not continue should the Fed engage in an aggressive rate hike scenario. This is what they say:

At 93 months, the current cycle is already longer than all but two post-war recoveries (out of 12 total). We could certainly debate why this expansion is already longer than normal, but strong growth is clearly not the reason. In fact, quite the opposite – a lackluster economic backdrop for years, leading to massive central bank support,has likely kept the cycle going more than anything else. Last year is a good example. As we show below, early in the year, with oil collapsing and the economic data rolling over, recession risks were seemingly rising. As Exhibit 3 shows, central banks across the globe responded. Even the Fed provided stimulus (verbally) by allowing the market to go from pricing in almost three rate hikes at the end of 2015 to almost zero rate hikes in summer 2016. Markets recovered, and the economic data followed.

What is Morgan Stanley’s conclusion? Simple: for the party to continue, not only must the Fed revert back to its quasi-dovish mode, but for that to happen the recent economic “rebound” has to end (the sooner the better), extinguishing any reflationary impulse, removing the impetus for Yellen to hike aggressively further, and allowing the Fed to remain on hold for an indefinite period of time. In short: “In our view, for the cycle to last another several years, we want to see more of the same – a continued environment of ‘ok’ growth and low inflation, which allows central banks to keep the party going.”

Hopefully Trump, whose policies threaten to upstage this delicate balance benefitting the 1%, has read the memo.

This is going to be a tough battle to fix the mess the Democrats have made and who refuse to help fix that disaster.

Fear, hope and deportations

Rosa Maria Ortega near her home in Grand Prairie, Tex., outside Fort Worth. “I voted like a U.S. citizen,” she said. “The only thing is, I didn’t know I couldn’t vote.”

A Texas woman ‘voted like a U.S. citizen.’…

This is a joke – this women is playing dumb – why didn’t she ask at the voting table?

It is time to have a cut off date for “anchor” babies.

The Washington Post

Mary Jordan, Kevin Sullivan

VALLEY VIEW, Tex. — At 4:30 a.m. on a windy Monday, Tamara Estes swallows vitamin B12 for energy and krill oil for her arthritic fingers. Even with her nightly Ambien, she is always up before the sun, getting ready for a job that reminds her of what infuriates her about America.

She drives a school bus on a route that winds through a North Texas neighborhood filled with undocumented…

View original post 2,828 more words

Kommonsentsjane is 100% right

http://www.bibliotecapleyades.net/sumer_anunnaki/reptiles/reptiles115.htm Not an anyone can join membership. They pull new members from around the globe. Global is a popular word for the Illuminati; it’s what they are about; and achieving one ruling class globalization is their goal. They really love celebrities, The Madonnas, Beyoncé, Clooney, Gaga Yes they go gaga over Hollywood […]

via The ILLUMINATI: REVISITED — Arlin Report

Reblogged on kommonsentsjane/blogkommonsents.

It is time for America to put them in their place – they are not elected for any position. It is of their own making in which they consider themselves so important. The money they are using for this globalization has been stolen somewhere down the line – one hint is they cheated on their taxes or if they worked for the government – it was through corruption and money gained illegally.

We have to learn to dismiss them, especially the Hollyweeds!

kommonsentsjane

Its going to be hard but the budget does need to be cut down.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

De Oppresso Liber

A group of Americans united by our commitment to Freedom, Constitutional Governance, and Civic Duty.

Share the truth at whatever cost.

De Oppresso Liber

Uncensored updates on world events, economics, the environment and medicine

De Oppresso Liber

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America

Australia's Front Line | Since 2011

See what War is like and how it affects our Warriors

Nwo News, End Time, Deep State, World News, No Fake News

De Oppresso Liber

Politics | Talk | Opinion - Contact Info: stellasplace@wowway.com

Exposition and Encouragement

The Physician Wellness Movement and Illegitimate Authority: The Need for Revolt and Reconstruction

Real Estate Lending