Posted originally on Jun 13, 2024 By Martin Armstrong

The Federal Open Market Committee unsurprisingly voted to maintain rates at 5.25% to 5.5%. The numerous cuts others were anticipating are completely off the table, as the central bank said there might be one reduction for the year compared with their optimistic tone forecast made in March of three rate reductions in 2024.

“In recent months, there has been modest further progress toward the Committee’s 2 percent inflation objective,” the voting members of the Fed said in their statement. They changed their forecast on inflation from “a lack of” to “modest” progress toward the 2% inflation objective.

Four voting members do not believe the central bank should raise rates at all this year. The central bank continues to exclude food and energy, two of the primary drivers of inflation when creating their summaries and dot plots. They certainly would never include taxation in those figures. The Fed claims there will be multiple rate cuts come next year, but they would never cut rates in the face of war which is completely inflationary and produces nothing.

Raising interest rates can have no impact on demand, as the government will simply borrow more, and the central banks simply have no say. Fed Chair Powell has repeatedly said that government spending is completely unsustainable and the Biden Administration is borrowing against future generations.

I explained in an earlier post why Keynesian Economics is collapsing. That theory was created when the US had a balanced budget and the government was actually expected to repay what they borrow. They still mistakenly believe that the business cycle can be manipulated. There is not much that the Federal Reserve can do at this point in time besides hope and pray for a miracle before that $10 trillion in debt is due to expire this year.

Posted Originally on May 16, 2024 By Martin Armstrong

Powell reiterated this week that he does not see any short-term need to lower interest rates. The Fed remains delicate in its speech to the public. They knew that inflation would continue rising due to various factors but had to say they were awaiting incoming data. The data is in for Q1 and nothing indicates that inflation is easing, therefore, expect rates to hold.

The Labor Department noted that the PPI rose to 0.5% in April from May, up 2.2% since the year prior. PCE, the Fed’s primary inflation indicator, rose 2.7% in Match from 2.5% in February. The US economy overall advanced 2.7% from October to December. We are looking at inflation beginning to rise faster than economic growth, which will lead to stagflation.

I have pointed out numerous times that the various measures provided to the public drastically downplay the dollar’s loss in purchasing power. Americans can feel it daily every time they make a purchase or check their bank accounts.

I explained that we already began experiencing stagflation in 2021. Normally, the standard definition of “stagflation” has been explained as slow economic growth with relatively high unemployment/or economic stagnation that takes place with rising prices. Some have also defined it as a period of inflation combined with a decline in the gross domestic product (GDP).

Stagflation became a term that defined the 1970s because economic growth was still positive, but the rate of inflation was far greater due to the price shock of the OPEC embargo. The Democrats are constantly pushing to raise taxes, and sent corporations fleeing offshore, and it was NOT merely because of the tax rate. Back then, I testified before the House Ways & Means Committee on taxation, and they wanted to know why NO American company got a contract from China to construct the Yellow River Dam. I explained that German companies were NOT taxed on worldwide income, and as such, they were already 40% less than an American company because Americans pay taxes on worldwide income, and the ONLY other country to that was Japan. Thus, American companies moved offshore, NOT because labor was cheaper, but so they could complete.

Now, we have additional regulations that are making it increasingly difficult for American businesses to prosper. The capital gains tax will be a nail in the coffin. The recent tariff slap on Chinawill also cause the price of goods to rise and harm the supply chain.

Remember, inflation was only 1.4% when Joe Biden took office – far beneath the Fed’s target. Inflation has risen as a direct result of fiscal policies under Bidenomics. The government has completely ignored the Fed’s warning that it must curtail spending. We are sacrificing our economy for the interests of the globalists.

Posted originally on May 1, 2024 By Martin Armstrong

I do not agree with Donald Trump’s view of the Federal Reserve. I speak on behalf of sound economic policies that benefit the people. I do not blindly support a political candidate for the sake of being on the right side. Now, I criticized Trump during his presidency for constantly pressuring the central bank to lower interest rates. There are rumorsswirling that Trump, if elected, would set the price of interest rates himself without the advice of the Federal Reserve. While this may be an extreme side of the rumor, Trump and every other president would like more power over the Federal Reserve — BAD IDEA!

What we must keep in mind is that the Federal Reserve’s original design, which lasted for about one year, was brilliant. The classic banking model involved borrowing from depositors on a demand basis and lending long-term, making a profit on the spread in interest rates, such as for business loans and mortgages. This was relationship banking, not today’s transactional banking model.

This was fractional banking insofar as about 8% of the money needed to remain free to service demand requirements. The crisis comes during an economic contraction when people run to the bank for a loss of confidence and demand to withdraw their funds. This results in the value of cash rising in purchasing power compared to assets, so asset values collapse.

The idea of “elastic money” was to increase the supply of cash during such a crisis to meet the demand for withdrawals and that would offset the need to sell assets by calling in long-term debts. By increasing the money supply on a temporary basis, the Fed could offset the contraction in theory smoothing out the business cycle.

This was a brilliant scheme. However, it has been Congress, and not the Fed, that corrupted that mechanism. The banks technically owned the Fed as this was supposed to save the taxpayer money. The banks should contribute to their own bailout fund. Furthermore, the Fed’s design was also about buying in corporate paper when banks would not lend money. This was a mechanism used to offset rising unemployment if corporations could not fund their operations. They supplemented this by the management of regional interest rates to balance the domestic economy. Each branch of the Fed could raise or lower their local interest rate autonomously to attract capital when there was a local shortage or deflect capital when there was too much.

Congress began to manipulate the Federal Reserve for their own self-interest when World War I broke out on April 6, 1917. The alteration to the design of the Fed was to direct it to buy government bonds, not corporate. In this first step, they never reverse this decree after the war. They removed the brilliant design to stimulate the economy directly by purchasing corporate paper during a recession. In the last 2007-2009 crisis, the government wrote a check to TARP and hoped that the banks would lend money, but they did not. Removing this first pillar of the independent Fed distorted the entire system. It then made little sense for bankers to own shares in an entity that was no longer privately controlled.

Banks became traders during the 1929 Boom-Bust Cycle. Goldman Sachs became deeply involved in the bull market, establishing numerous trusts and mergers. Goldman Sachs expanded the leverage going right into the eye of the storm that was about to hit starting on September 3, 1929. The crash wipes our 70% of Goldman’s entire market.

The Glass-Steagall Act, also known as the Banking Act of 1933 (48 Stat. 162), was passed by Congress in 1933 and prohibited commercial banks from engaging in the investment business. Around 5,000 banks failed during the Great Depression largely because banks sold trusts and foreign sovereign government bonds to the public in small denominations. Bill Clinton later repealed Glass-Steagall and handed the power back over to the bankers. Disaster strikes every time the government tries to manipulate the free market.

People believe the Fed has the power to create money out of thin air, yet never explain why the Fed was given that power. You cannot have a fixed money supply as the population increases, then you end up with DEFLATION, which is the rise in the value of money. You can double the money supply, but if the people hoard it, as they tend to do during private waves when the public loses all trust in government, you will never create inflation. There was a huge contraction in the velocity of money during the Great Depression for this very reason.

The Biden Administration, as has the Trump Administration, has come after the Fed. Politicians merely want the economy to appear strong under their reign and fail to see the long-term impact of policies. Politicians have no knowledge of economics or the insight to run the Fed. Not to mention that law does not permit Washington to bark orders at the Fed, although Washington does oversee the Fed and can force the central bank to change its policies to align with government spending or repel debt buyers.

Trump is a borrower, not a lender. His bankruptcies were the result of the business cycle and he leverages himself to the hilt so when the recession comes, he gets in trouble and when it is booming he claims to be a fantastic investor. But he is no trader. He could have hedged the business cycle but did not.

Chairman Jerome Powell and Trump clashed repeatedly. Not so coincidentally, Powell and numerous Fed bank presidents have their terms expiring in 2028 – a key year, as indicated by our models. The Biden Administration has already driven the economy off a cliff. The central bank is merely trying to heal an already injured economy with a limited medical kit.

The Fed is INDEPENDENT and will not be bullied by Biden or Trump. The Fed understands that it has become the world’s central bank and its actions in raising rates have had a far greater impact externally particularly in emerging markets because so many other nations issue their debt in US dollars.

Posted originally on Mar 7, 2024 By Martin Armstrong

Those who follow this blog already knew that the Federal Reserve would not drop rates in the future due to unsustainable fiscal policies paired with America’s increasing involvement in foreign wars. All of the talking heads were preaching that rates would significantly decline to pandemic levels, as if that were the historical norm. Every fiscal policy in recent years has exacerbated inflation and the Fed cannot keep up with government spending. QE FAILED. The artificially low interest rates of the recent past were completely unsustainable and relied on outdated theories.

The outdated understanding based on Keynesian Economics remains to increase the supply of money and it MUST be inflationary. The Fed raises rates to reduce consumption and lower rates to stimulate consumption. It’s a very nice theory, but when actually tested, it utterly fails. Lower rates will NEVER cause people to invest UNTIL they believe that there is an opportunity to invest. We are watching the big players withdraw from equities, let alone government debt. We are in a private wave where money is running off the grid at a rapid pace.

The peak in interest rates took place in 1899 at virtually 200%. Yet, 1929 was the real bubble top and it peaked with 20% interest rates in call money on the NYSE. In theory, the biggest boom should have been met with the highest interest rate. In truth, the “real interest rate” as I have defined it is when the interest rates exceed expectations. If you think the stock market will double, you will pay 25% interest.

As you can see, while interest rates hit nearly 200% in 1899, the share market did NOT crash percentage-wise anything as it did following 1929. Look, there is a lot more to this than meets the eye. Everything must be addressed on a global scale for it all depends also on the direction of capital flows. There is just a lot more to this than simply the money supply and interest rates.

Now, Powell continues to explain to the public that VOLATILITY and economic conditions are beyond the control of the Fed. “We believe that our policy rate is likely at its peak for this tightening cycle,” Powell said. “If the economy evolves broadly as expected, it will likely be appropriate to begin dialing back policy restraint at some point this year. But the economic outlook is uncertain, and ongoing progress toward our 2% inflation objective is not assured.”

All the news ofinflation waning, including recent data, is inaccurate propaganda intended to calm recessionary fears. Even by the government’s data, inflation is up 3.1% compared to last year. It was an unprecedented moment when Powell broke with Washington and criticized the government for their unsustainable spending. The Fed NEVER criticizes the government, despite the two being separate.

Hence, I say to stop blaming the Fed. They are not the ones creating all the money but are working to match monetary policy with unsustainable fiscal policies. We are looking at trillions in deficits per year. There is no restraint when creating new massive spending packages. Then people blame the central bank with no concept that it’s only a fraction of “money;” the real issue is CONGRESS.

Listen, interest rates cannot decline in the face of war. The 2020 yearly array showed a turning point for a high in 2022 and a possible correction into 2024. I explain this in more detail on the Socrates private blog but buckle up for the year ahead.

Posted originally on Jan 10, 2024 By Martin Armstrong

One piece of analysis commonly misconstrued is the Federal Reserve’s role in the nation’s economic health. Even those who have the ability to piece together other variables that often go unnoticed commonly point their finger at the Federal Reserve. No one is factoring in the largest driver of inflation – WAR – nor are they factoring in the three main pillars of government debauchery (war, taxation, government spending) that the Fed cannot control.

They never look at the history of central banks and how Congress has been manipulating the law to alter the Fed’s purpose. If there was a single interest rate and one policy set in Washington, why do we even have branches of the Fed if they no longer act independently? When the Fed was created, the branches managed internal domestic capital flows. Each branch was independent, and they would lower or raise the interest rate in their jurisdiction depending on the flow of money. Too much cash? They lowered the rate. Not enough cash? They raised it. This was all before Keynesian Economics when the interest rate became the tool to manipulate our demand.

The San Francisco earthquake of 1906 created the Panic of 1907, which caused capital to rush from East to West. This created a shortage of cash in New York and led to bank failures. Hence, the Federal Reserve was created with branches to manipulate the internal capital flows – not the Quantity of Money Theory or the demand of the people.

Roosevelt usurped all the independence of the Fed and created a Washington monopoly to push his socialist agenda into place. We are hearing the same pitch of equality once again from Biden. The government is supposed to be separate from the Federal Reserve, but the president appoints the chair. The formerly independent central bank that was owned by the bankers to prevent the misuse of taxpayer funds is now under control by the banks only in theory; the reins of power are political.

The Federal Reserve failed to produce inflation while engaging in QE between 2008 and 2019. Most analysts ignore that entirely. If the Fed issued $1 trillion and buys in US Treasuries, I hate to tell you, but it would have ZERO impact. Why? Because debt today is simply cash that pays interest. Once upon a time, you could not borrow against government debt. Thus, it was deemed non-inflationary as long as it could not be used as money. Today, you post bills as collateral to trade futures. The old theories no longer exist in this new, strange world we live in. Hence, all the QE was merely swapping the debt for cash.

Also, consider where the Fed purchases its debt and who purchases US debt. China, for example, is no longer buying US debt due to US-China government relations that the Fed has absolutely no control over. Then, say China sold its debt for cash. The dollar would go offshore, and the domestic money supply would NOT increase. There is a lot more to this game than the simplistic analysis that leads to brainwashing the financial community and investors.

Jerome Powell has no power over fiscal spending or the deficit. Central banks everywhere are trapped. The central banks in Europe are in FAR worse shape right now. When Powell stood before Congress and subtly criticized the Biden Administration by calling their constant spending “unsustainable,” he was attempting to explain that the central bank could not overpower the government here. The central bank can create elastic money, and it will return to doing so. Private capital is fleeing government debt on a global level.

In the end, the globalist agenda is to default on all national debts, and they will no longer need to bail out the bankers. Welcome to the Decline & Fall of Western Civilization.

Posted originally on Jan 3, 2024 By Martin Armstrong

Everyone wants to know what the Federal Reserve will do in 2024. Of course, people want to believe that the Fed will slash interest rates in the New Year. The pundits cling to every word except when, at the start of the month of December, Powell boldly criticized the Biden Administration, saying that his outrageous spending is “unsustainable” and central banks do not criticize their governments. They certainly do not criticize each other. I have met with the boards of central banks worldwide because I understand their predicament. Unless you have been behind those closed doors, you will never comprehend the intricacies that are taking place.

The Federal Open Market Committee (FOMC) held rates at the 5.25% to 5.5% range at their last meeting in December 2023. Additionally, the committee indicated the possibility of at least three rate cuts in 2024, as their favored gauges for inflation appear to be easing. The “dot plot,” which reflects individual members’ expectations, suggests the potential for four rate cuts in 2025 and three more in 2026, bringing the rate down to between 2% and 2.25%. Now, that is simply what the public has been led to believe.

The Fed’s last decision reflects a cautious approach to policy tightening, considering multiple factors unknown to the public before any further adjustments. The committee’s PUBLIC decision and future outlook are based on the evolving economic conditions in relation to inflation and the labor market.

The Federal Open Market Committee will meet in 2024 as follows:

Jan. 30-31

Mar. 19-20

Apr. 30 – May 1

Jun. 11-12

Jul. 30-31

Sept. 17-18

Nov. 6-7

Dec. 17-18

There are simply things I cannot publish on the public blog. I have posted articles on the Socrates private blog that explain the Fed’s direction for 2024 in further detail. Now, consider the dates above and consider what events align with them. Further details will be provided in the Year-End Report, which should be out by the end of this week.

The Federal Reserve cannot criticize the federal government. The most significant issues facing our economy are simply out of the Fed’s hands: war, taxation, and government spending. Chairman Jerome Powell surprised everyone when he called current government spending “unsustainable.” While not a direct criticism, Powell issued a stark warning that aligns with our Revolution Cycle of 72 years. In 1951, the central bank defied the US government by refusing to purchase debt to prevent rate hikes amid the Korean War.

So, there is bad news for the perpetual bulls who insist rates must decline. There is a HUGE divergence unfolding between short and long-term rates. Institutions are buying up government debt without considering the potential that rates may not fall. Absolutely no one is factoring in the largest driver of inflation – WAR – nor are they factoring in the three main pillars of government debauchery (war, taxation, government spending) that the Fed cannot control.

Posted originally on Dec 21, 2023 By Martin Armstrong

QUESTION: Why do you seem to be the only analyst who understands central banking? My son got an internship at one of the major banks in New York during the summer. I won’t say which bank, but he asked a senior-level guy there about you and the interest rates, explaining I had been following you for years. He said you were the only one with international experience and who has ever advised multiple central banks. Is that the answer?

PK

ANSWER: Perhaps in part. But there is a massive gap between the experience of those of us who have dealt at high levels internationally and domestic analysts who always seem wrong calling the shots based on the headlines they read.

The number one problem is this fiction that the dollar is a fiat currency when, in fact, currency from the beginning of time has ALWAYS been valued NOT by its pure metal content but by who issued it. There has historically always been a premium to the currency of the dominant economy.

When Cyrus the Great conquered Lydia, he continued to strike coins of their design because they were highly regarded in international trade. We see the same with Roman coinage imitated in India when they, too, could have issued their own designs, but the Roman coinage carried a premium.

Even when the Barbarians were on the Northern frontier of Rome, they too took silver and struck imitations of Roman coins because they were worth more than the metal content. In 260AD, when emperor Valerian the Persians captured me, there was a Financial Panic of 260AD where bankers suddenly did not know if Roman coins would still be worth anything when there was no emperor.

While everyone claimed hyperinflation would engulf the world because of Quantitative Easing (QE), I warned there would be no such inflation. Indeed, with QE, there was no inflation, and people then developed the Modern Monetary Theory, claiming that they could increase the money supply and it would not result in inflation.

The entire problem rests with the fact that these people not only did not understand the role of money but also failed to grasp international capital flows and how they play into the world economy. Because you can now buy US TBills and place them as collateral to trade with at a brokerage house, the debt is simply money that pays interest. BEFORE 1971, it was illegal to borrow against government bonds. For you see, if you could borrow against the bonds, that meant the bonds were part of the REAL money supply.

Once debt became cash that paid interest, that changed economics forever. I have said over and over again the Fed is NOT the problem, and it can not stop inflation with interest rates. The REAL money supply if the national debt, so if the Fed buys-in 30-year bonds and creates cash to do so, it is NOT increasing the money supply; it is increasing the liquidity – that is all. Swapping cash for bonds does not change the balance sheet. If you buy a house for $100,000 and pay cash, then you have merely converted your cash into an asset.

Now, it all depends upon the buyer. If I have a building and sell it to a fellow American for $10 million, it does NOT alter the domestic money supply. However, if I sell it to Brit, he brings in cash to buy the property, and that DOES INCREASE the money supply BECAUSE he has imported $10 million that did not previously exist within the domestic system.

This is a very complex topic that only those of us in international finance ever encountered. I helped the Japanese reduce their trade surplus for political reasons. I had them buy gold in New York, export it to London, and sell it there. The trade statistics only count dollars in and dollars out – not the product. Buying gold and exporting it reduced the trade deficit, and nobody understood anything.

I handled a lot of the takeover boys during the 1980s when they made the move about Wall Street. They never understood what I was doing. The stocker was way undervalued when you could buy a company, sell its assets, and double your money. I took it to another level. I ran the model on currencies, and we would then buy like all the Courage Pubs in England but borrow in Swiss in a currency that would decline against the asset. We were making 20% on the currency moves besides the asset values. I was restructuring companies selling assets in one currency to buy assets in another to create balance hedge portfolios. That’s how I became friends with Maggie Thatcher. She wanted to know who this guy was sending companies into Britain.

Maggie was one of the few world leaders who grasped what I was doing. She kept Britain out of the EU because she understood what and how I was restructuring multinational companies. They staged a coup against here to take the pound into the Euro, then Soros attacked the overvalued pound in the ERM, and John Major had to reverse the entire mess, making Soros very rich in the process.

I will get around to doing my memoirs. I understand what I was doing set the stage for the world economy post-1971 Bretton Woods. That’s why Milton Friedman bothered to listen to my lecture about currencies in Chicago.

Posted originally on the CTH on July 3, 2023 | Sundance

As if carrying Homeowners insurance in California and Florida wasn’t already subject to ridiculous increases in premiums, things are about to get a lot worse.

Effective with the July 1st notification, Reinsurance rates, these are companies who insure the insurance companies, are telling their clients there will be up to a 50% increase in cost for underwriting catastrophic coverage. Perhaps claims in the past few years have been higher; however, I suspect the issue amid the reinsurers is partly connected to the issue that surrounds banks and bond rates.

Back when interest rates were near zero, banks and reinsurers likely scooped up lots of Treasuries and bonds. As the Federal Reserve hikes rates those bonds have declined in value. When interest rates rise, newly issued bonds start paying higher returns to investors, which makes the older bonds with lower rates less attractive/valuable. The result is that most banks, and I suspect big reinsurance houses, have some amount of unrealized losses on their books.

Whatever the reason, the big reinsurance companies are now telling the insurance carriers their catastrophe rates are going up as high as 50%. Those insurance companies will then pass those rate hikes to the individual policy holders for commercial buildings, residential homes, cars, RV’s etc. Bottom line, homeowner insurance rates are about to go up again with policy renewals, especially in Florida and California.

LONDON, July 3 (Reuters) – U.S. property catastrophe reinsurance rates rose by as much as 50% at a key July 1 renewal date, broker Gallagher Re said in a report on Monday, with states such as California and Florida increasingly hit by wildfires and hurricanes.

Reinsurers insure insurance companies, and have been raising rates in recent years because of steepening losses, which industry players put down in part to the impact of climate change. Higher reinsurance rates can affect the premiums which insurers charge to their customers.

U.S. reinsurance rates for policies which previously faced claims for natural catastrophes rose 30-50%, Gallagher Re said.

Reinsurance rates for similar policies in Florida rose 30-40%, the broker added.

Some insurance firms have pulled out because of the risk of heavy losses. State Farm said in May it would stop selling new insurance policies to homeowners in California.

In Florida, “all the major carriers (insurers) left and so you ended up with this market which is populated by a large number of very small, very thinly capitalised insurers which is exactly what you don’t want,” James Vickers, chairman international, reinsurance, at Gallagher Re told Reuters. (keep reading)

In Florida specifically, homeowners insurance costs have now generally risen higher than the mortgage payment for a middle-class family. This is not sustainable.

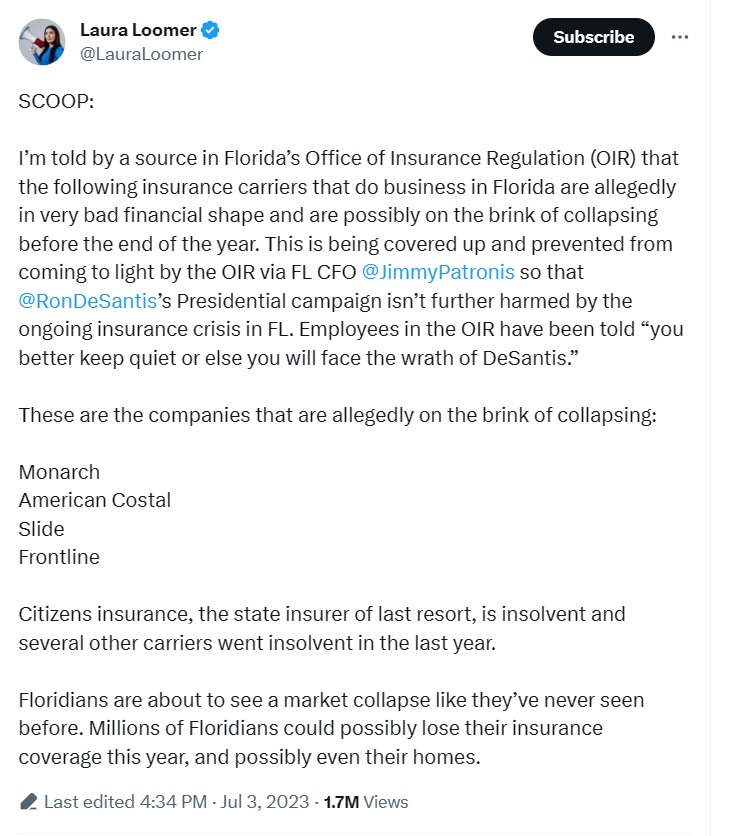

SCOOP:

I’m told by a source in Florida’s Office of Insurance Regulation (OIR) that the following insurance carriers that do business in Florida are allegedly in very bad financial shape and are possibly on the brink of collapsing before the end of the year. This is being covered…

Posted originally on the CTH on May 1, 2023 | Sundance

Everything about the process of cutting down energy exploitation, then driving supply side inflation, then raising interest rates to shrink demand (stem inflation) created by a desire to lower economic activity to the scale of diminished energy production, is a game of pretending.

The collateral damage from the rate hikes has been the banking destabilization, which shows the priority of the government officials and central banks to support the climate change agenda. Into the game of pretending comes the second unavoidable consequence with inflation continuing as a result of the energy policy.

They simply cannot cut energy demand enough to meet the diminished scale of production. There is no alternative ‘green’ energy system in place to make up the difference. That is the reality. Now, the fed is scheduled to raise rates again, then begin to debate the collateral damage as they continue the pretending game.

(Via Wall Street Journal) – […] Another quarter-percentage point increase would lift the benchmark federal-funds rate to a 16-year high. The Fed began raising rates from near zero in March 2022.

Fed officials increased rates by a quarter point on March 22 to a range between 4.75% and 5%. That increase occurred with officials just beginning to grapple with the potential fallout of two midsize bank failures in March.

The sale of First Republic Bank to JPMorgan Chase & Co. by the Federal Deposit Insurance Corp. announced early Monday is the latest reminder of how banking stress is clouding the economic outlook.

Fed officials are likely to keep an eye on how investors react to that deal ahead of Wednesday’s decision, just as they did before their rate increase six weeks ago when Swiss authorities merged investment banks UBS Group AG and Credit Suisse Group AG. (read more)

There is no other way to look at the combined policy without seeing a Central Bank Digital Currency (CBDC) in the future. All of these combined policies are creating a self-fulfilling prophecy.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America