Armstrong Economics Blog/Sovereign Debt Crisis

Re-Posted Oct 31, 2019 by Martin Armstrong

The Sovereign Debt Crises is almost here

The Sovereign Debt Crises is almost here

QUESTION:

Hi Martin,

I am originally from Saskatchewan and I still own farmland there. (Sask will separate along with Alberta). I currently live in British Columbia.

Given global cooling, earthquakes, the commodity boom, civil unrest, global war, Alberta Separation, the rise of China…..Where do I take my family and young son?

Thanks for all of this invaluable work,

NH

ANSWER: That is a difficult question to answer at this point in time. Normally, if there is a crisis in one part of the world there is always an alternative. This time, every place you look there is political uncertainty. There will be pockets of safe harbors. Alberta may be one if it separates from Canada. The issue stems from oppressive control coming from centralized governments that are not ready to reform. They will crackdown on society in a desperate attempt to retain power. There are some pockets in the United States, but we may be looking more outside the continent. So far, the best spot in Asia has been Thailand.

The Federal Reserve, as expected, cut rates a quarter-point. The Fed also warned that further moves to ease interest rate policy may be coming to an end. The rate cut of 25 basis points to a range of 1.5% to 1.75% has been the third cut this year, which Fed Chairman Powell characterized as a “mid-cycle adjustment” in a maturing economic expansion. The Liquidity Crisis that has emerged in the REPO Market has been deeply concerning behind the curtain as many remained clueless as to why it was even unfolding. Many analysts claimed the Fed was hiding something and US shares of banks tumbled when they were traceable to Deutsche Bank exposure.

The Federal Reserve, as expected, cut rates a quarter-point. The Fed also warned that further moves to ease interest rate policy may be coming to an end. The rate cut of 25 basis points to a range of 1.5% to 1.75% has been the third cut this year, which Fed Chairman Powell characterized as a “mid-cycle adjustment” in a maturing economic expansion. The Liquidity Crisis that has emerged in the REPO Market has been deeply concerning behind the curtain as many remained clueless as to why it was even unfolding. Many analysts claimed the Fed was hiding something and US shares of banks tumbled when they were traceable to Deutsche Bank exposure.

This year’s WEC was interesting since every part of the world was in crisis and we have gone into great detail with respect to the REPO Crisis. This year’s attendance set new records for the number of people flying in from around the world which included Russia down to South Africa, Europe, North, South, and Central America, all of Asia from China and Korea as well as Japan down to Singapore and India. The cross mix from fund managers, pension funds, banks, to central banks and even heads of separatist movements from around the world provided for a very interesting cocktail party this year.

This year’s WEC was interesting since every part of the world was in crisis and we have gone into great detail with respect to the REPO Crisis. This year’s attendance set new records for the number of people flying in from around the world which included Russia down to South Africa, Europe, North, South, and Central America, all of Asia from China and Korea as well as Japan down to Singapore and India. The cross mix from fund managers, pension funds, banks, to central banks and even heads of separatist movements from around the world provided for a very interesting cocktail party this year.

Even the third-day training session exceeded 400 attendees. We are looking at holding two conferences outside the USA in 2020 in addition to Orlando – Frankfurt, and Shanghai. Perhaps holding three sessions we can reduce the size of these events. When they reach 700 attendees they are getting just a little too big.

There was so much to cover this year we provided extensive materials because there was just no way we could have covered in detail all of the information when we have a REPO Crisis, Liquidity Crisis, Pension Crisis, Sovereign Debt Crisis, Monetary Crisis, and a Crisis in Democracy with rising civil unrest and growing separatist movements around the globe.

We want to thank everyone for all your loyalty and the show of so many who have been making this an annual gathering as if this were a university reunion.

Thank you very much. We will be posting photos in a special sector for attendees onl

During the last Mortgaged Backed Security scandal which undermined the entire world economy, they created mortgage modifications which enabled millions of delinquent homeowners to avoid having their home foreclosed. Since 2007, it has been estimated that some 8.7 million permanent mortgage modifications were created. There are still over $800 billion of these bubble-era loans outstanding. How were they allowed to survive? For at least the past five years, between 75% and 95% of all mortgage modifications have taken the past interest due that was in default, included it in a capitalization of interest arrears, which means the resolution was never for the benefit of the homebuyer.

By adding the past-due interest, they have been paying interest on the interest. This failure to address the issue by some partial debt forgiveness with respect to prior interest means that the mortgage crisis has been simply postponed. If a new financial crisis hits, the old one will simply be sent off into foreclosure and real estate values can still plummet even more in the low-end of the market.

Barrons did a good review of the problem. They came to the conclusion that re-defaults will be more likely as home values fail to get back to par and these people will just walk away. Indeed, the resolution should have been the forgiveness of past-due interest. Then the value of the homes would have been less impacted. But the bankers refused to accept the loss and as a result, real estate has been unable to recover on the low end of the market which is why the economy has not been robust as it should be boosted more by capital inflows than true economic recovery.

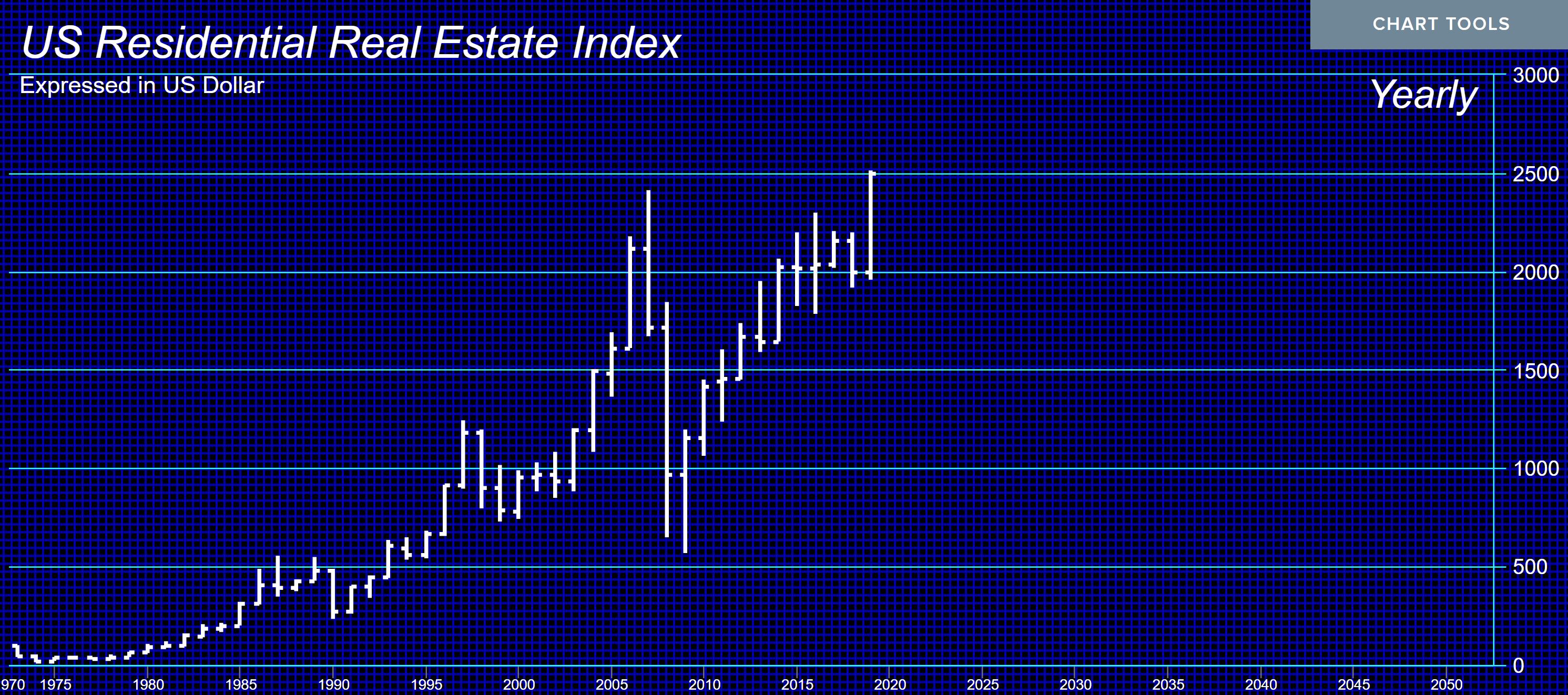

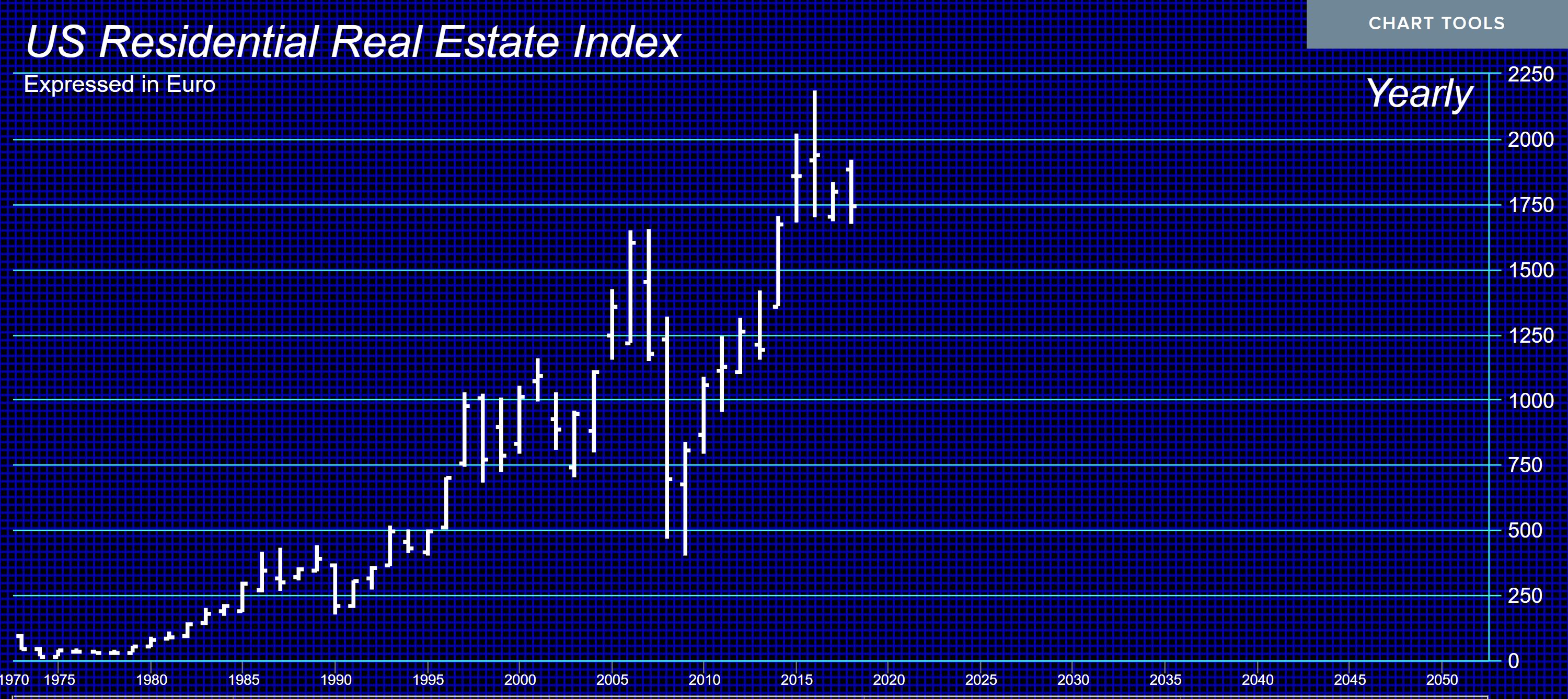

When we look at our broad real estate index, it has been making new highs in 2019. However, when we plot this in Euro, we can see why there have been foreign capital inflows. But the foreign capital has been buying the high-end, not the class where the mortgage bubble of 2007 impacted. From a foreign perspective, the high investment end of the markets has been above the 2007 high for the past 4 years. This is why the new highs have tended to be concentrated in the major centers like New York City and Miami – not local main streets.

Barrons reported that if we look at JPMorgan Chase (JPM) which holds the second-largest residential mortgage portfolio in the nation, we see in its second quarter of 2019 report, that almost $10 billion of modified loans (known as troubled debt restructuring)remained outstanding. Of this restructured debt, 43% were listed as having re-defaulted. Bank of America (BAC) has stated that 41% of its modified loans had re-defaulted.

QUESTION: Might you clarify this response you gave on one of your very recent blogs. You said bail-in may NOT be permitted on US soil. Did you mean that despite the laws written in the USA to allow it, you don’t think it is likely to happen to USA citizens banking in the USA?

OR were you only meaning in regards to overseas banks with locations within the USA would most likely not use bail-in.

OR because of all the EU money fleeing to USD/USA that the banks stable in the USA (for now) and thus no bail-in needed?

Do you think there would EVER be the case for a USA bank bail-in? Or is this just more conspiracy talk? For obvious reasons, this is of great concern to all of us as this USD repo madness, liquidity crisis and DB’s derivative contagion begins to spread throughout Europe into the next ECM turn in mid-January 2020.

Thank you in advance for your efforts and response to this question.

L

ANSWER: The bail-in laws were passed during the last crisis which was a popular response at that time because no bankers were ever punished for what they did in New York City. To the extent that FDIC exists, they would certainly honor that or it would be political suicide. However, the fine print is FDIC cover per person. Putting money at 5 different banks would seem to get around their limitations, but I would not count on that.

The gray area comes in two aspects.

The problem with a bail-in is that the ramifications would be far worse than the Great Depression. You would destroy businesses that would then be unable to make payroll and the unemployment would be massive – far greater than the 25% high of the Great Depression.

The BAIL-IN policy of Europe is a different animal altogether. This has nothing to do with bailing-out bankers. This stems from the refusal to consolidate debts. If banks failed in Southern Europe, then a bailout would mean money from the north could go to the south. This is the structural design. It is WHY Europe adopted the bail-in, quite different from the question of bankers’ conduct. Germany’s demand to join the Euro was that there would be no consolidation of debts. As I have said, the EU is like a family reunion with the cousin who is the drunk than people smile at, but would never lend him a dime. You can pretend it one happy family, but that is just the surface.

A bail-in would actually be devastating economically. It defeats the very idea of banking for if the burden is shifted to depositors to monitor banks when we have agencies who are supposed to do that, then why do we need governments or pay taxes?

Despite the laws, they were never thought threw and it is a huge difference between a regional bank and Goldman Sachs. The hatred was directed at the New York Banks – and rightly so. Because the federal court in New York City has protected the bankers, they have actually undermined the entire country by their stupid actions.

QUESTION: Hi Martin,

Recently you wrote: “Recently, this has manifested in laws that have attacked foreign investment in real estate, which is not the “hot” money that blew up the world in 1997. ”

I live in Vancouver where real estate prices are completely divorced from local wages. If it is not hot overseas money that is driving our real estate market then what is? Your analysis is appreciated as always.

Nick

ANSWER: It is foreign money pouring into Vancouver seeking to park in a world that is in economic and political chaos. This has been accelerated by the decline in the C$, which has made the prices appear cheap in other currencies. When you look at our Canadian Real Estate Index in terms of different currencies, you can see that it has been attracting capital. The problem is rather clear. Foreign capital buys the trophies. Others may raise the price of houses because they see the high-end rising, but it is not foreign capital that is bidding for the average home in general. The problem comes when they put in punitive laws that become permanent because of a trend based entirely upon currency.

QUESTION: You commented that the central banks had a difficult position when they were on the gold standard compared to post-1971. Could you explain that difference?

Thank you for the education. Its better than any classroom.

EJ

ANSWER: The United States created the Federal Reserve in 1913. Prior to World War I, central banks were long-established in Europe like the Bank of England in 1694. What you have to understand is that BEFORE World War I, the central banks of Europe were faced with two duties because there was the gold standard.

1.) The first was to defend their currency’s parity with gold and thereby the entire edifice of the international gold standard. This required raising interest rates and keeping the total volume of money and credit under control, often with contractionary effects.

2.) The second responsibility was to act as a lender of last resort for their banking system by supplying emergency liquidity. This necessitated an expansion of credit and a lowering of interest rates.

Post-1971, the central banks were no longer required to intervene to maintain the exchange rate relative to the gold standard, which is more or less similar to Hong Kong managing the peg to the dollar today.

Paul Volcker raised interest rates insanely into 1981 to stop inflation, but he ignored the consequences that would have on the value of the dollar on world markets. This was the stone that hit the standing pool of water which then at the 1985 Plaza Accord suggested that Europe create a single currency. One mistake is never corrected and never acknowledged. They constantly create a new scheme to solve the last one they created.

Release Date

January 8, 2018

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

De Oppresso Liber

A group of Americans united by our commitment to Freedom, Constitutional Governance, and Civic Duty.

Share the truth at whatever cost.

De Oppresso Liber

Uncensored updates on world events, economics, the environment and medicine

De Oppresso Liber

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America

Australia's Front Line | Since 2011

See what War is like and how it affects our Warriors

Nwo News, End Time, Deep State, World News, No Fake News

De Oppresso Liber

Politics | Talk | Opinion - Contact Info: stellasplace@wowway.com

Exposition and Encouragement

The Physician Wellness Movement and Illegitimate Authority: The Need for Revolt and Reconstruction

Real Estate Lending