The proposal is to create a global tax rate as world leaders move to create a one-world government. The United Nations, behind the curtain, is preaching that ONLY they can solve the world crisis in climate change, for it requires a single government to control the world. On top of that, Bill Gates has taken over the funding for studies by Ivermectin & Fluvoxamine Clinical Trial Targeting COVID-19. We can bet that given his monopoly over vaccines, taking over the funding of studies to show an alternative to vaccines will by no means be legitimate. The conflicts of interest are vast.

As I have warned, they desperately needed to remove Trump from office because they viewed him as an outsider and someone elected by “populism,” which threatened the world establishment of political control by elite career politicians. They are now moving in high gear to eliminate democracy by 2022, but certainly, their goal is by 2024.

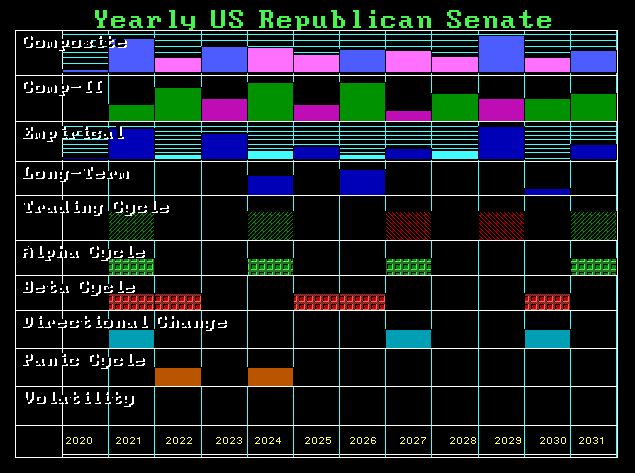

As I have warned, our models of politics have NEVER shown Panic Cycles since the 1930s. It appears that some states are trying to fight back where the Democrats want mail-in ballots that are not secure and same-day registration to vote to ensure there can be no verification of who the people even are. The Supreme Court has abandoned its role to protect our constitution by refusing to hear any of the cases, which may not have overturned the election but would have dealt with changing the rules as they went.

People have no idea what is at stake. These people in power want ABSOLUTE control, and they never want another popular person to run for office anywhere that would dare to threaten their goal of eliminating democracy. Then they want worldwide taxation, and this has been the goal of the United Nations. They argued that climate change could not be combated by a single country. It will take a one-world government, UNELECTED, of course, to rule the world and make regulations that dictate everything right down to what you can and cannot do in your home.

Posted originally on the conservative tree house April 8, 2021 | Sundance | 151 Comments

All of JoeBama’s economic policies mirror the Obama-Biden economic issues. Underline it; emphasize it; note the pattern. The policies that intentionally held down the U.S. economy during the Obama administration are once again being duplicated. It’s Déjà vu all over again.

JoeBama’s energy policy is crushing jobs in key regions where energy jobs are being lost in dramatic fashion. Simultaneously the costs of energy, including gas, are skyrocketing.

The longer-term costs have not yet hit the consumer, but they will soon as inflation will jump dramatically while employment will continue to struggle because consumer demand will drop… The issues create a cascading cycle.

The Biden administration is hiding their actual policy impact by blaming COVID, but that’s not the issue that will hurt blue-collar workers in the longest term. We are going back into the intentional disconnect I have talked about where the stock market (multinationals) will gain, but the U.S. worker economy will suffer lost jobs and lower wages. This dichotomy is by design and the corporate media economists never discuss it.

This reality is a big part of the reason why Pelosi and JoeBama needed to quickly pump money into the working class in order to avoid the pitchforks. However, that $2,000 injection will not last and will be eaten up quickly by the larger and longer term Biden economic policy.

The U.S. economy, which is 70% dependent on consumer spending, is going to contract. This contraction will be “unexpected” by the professional pundit class who check their stock holdings and smile. However, this contraction will not be unexpected by the blue-collar workers who watch their paychecks shrink and their costs to live (electricity, fuel, food prices) increase beyond their earnings.

If you are a blue-collar or white-collar worker in a BLUE region or state, you will feel the impact first. It is going to get very ugly, as noted by the disparity in the unemployment claims this week. Weekly unemployment claims [Dept of Labor pdf here] tell the story.

(CNBC) – […] First-time claims for unemployment insurance rose more than expected last week despite other signs of healing in the jobs market, the Labor Department reported Thursday.

First-time claims for the week ended April 3 totaled 744,000, well above the expectation for 694,000 from economists surveyed by Dow Jones. The total represented an increase of 16,000 from the previous week’s upwardly revised 728,000. The four-week moving average edged higher to 723,750. (link)

The negative results are continuing on a ‘Red State’ -vs- ‘Blue State’ dynamic as noted in the Bureau of Labor Statistics (BLS) reporting: “In February, the highest unemployment rates among the divisions were in Los Angeles-Long Beach-Glendale, CA, 10.9 percent, and New York-Jersey City-White Plains, NY-NJ, 10.8 percent.”

For the weekly jobless claims, here’s the breakdown by state:

Do not dismiss these results as just bad policy. There is also a strong ideological component as the Chicago Crew is driving the granular issues on a day-to-day basis. The Obama team intentionally work to diminish the economy of the United States because their “fundamental change” requires it. Joe Biden is an idiot and has no clue about what is structurally behind all the moves…. That’s why Obama installed Kamala Harris.

The professional republican class are corporatists; do not expect them to oppose any of these policies that undermine the U.S. economy and expand globalism. The GOP is paid by the corporations to act stupid and go along.

The road to serfdom is paved with fraudulent intentions….

The Archegos Capital was founded by the former Tiger Management equity analyst, Bill Hwang. Archegos Capital, the “home office” hedge fund owned by Bill Hwang, lost an unbelievable $110 billion in just five days. The strategy was the classic leverage using SWAPS. They never purchased shares of stocks in companies like ViacomCBS. Archegos Capital was entering into equity swaps with numerous different banks and investment banks in a similar manner to what would be called money laundering where we borrow from one bank to pay off another.

By engaging SWAPS, Archegos Capital never actually owned shares of the underlying stock. What they did was effectively leveraged themselves by as much as 500%, which would prove to be their undoing. The problem with such hedge funds is that they really take a personal view of the performance of the market going forward. This is ALWAYS the undoing of these hedge funds going back to Long-Term Capital Management which took a fundamental view that they would make a guaranteed fortune on the high interest of Russian debt and that bribes were being paid in the IMF that they thought would keep the loans going to Russia without end.

I cannot stress enough that ANY fund which is dominated by fundamental expectations that override quantitative models, should be AVOIDED like the plague. We are into a whole new world of finance which is moving in a counter-reaction to the Great Reset. There is NO QUESTION that the March 2020 crash was not only UNIQUE in history, it was clearly an assault that attempted to create another 2007-2009 economic contraction which would have made facilitated the Great Reset by the intentional destruction of the economy. They have had to rely upon the virus scare to accomplished what they had hoped would have be a far easier road.

QUESTION: Hello Martin, can you explain to me how a currency would sustain value for international trade if a country, like Canada (where I live), did what you suggested and stopped issuing debt and just printed money to level that was 5% – 10% of national GDP? would it depend on the attractiveness of what a country exports eg: Canada exports oil, lumber, crops like wheat/soy/canola, minerals – both precious and functional? What would happen to a country that didn’t have exports as a significant portion of it’s GDP? I am curious about how currencies would react to your restructuring plan that eliminated the need for a country to issue debt. Thanks for all your insights and theories. Very helpful.

Trapped in Canada with an egoistic misguided Prime Minister who doesn’t appear to like Canada (he keeps telling us how awful we are) or Canadians, he prefers spending time with global elites and is following their plan even though it damages Canada pretty significantly. MB

ANSWER: Right now, every country spends more than it takes in. The deficits are funded by selling debt, which then competes against the private sector. The interest rates rise and fall on sovereign debt based upon the confidence from one week to the next. If they stopped borrowing, then the capital investment would turn to the private sector, creating more economic growth. If income taxes were eliminated, the economy would grow based upon innovation which is what it should be driven by.

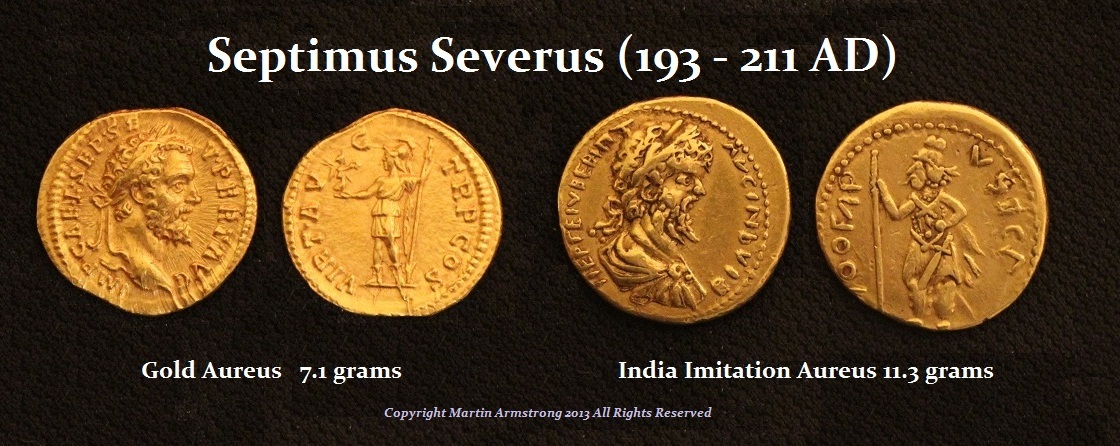

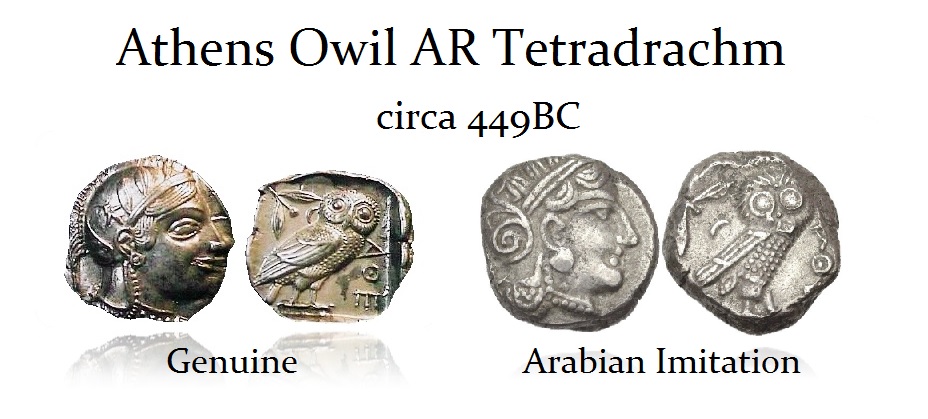

The confidence in the currency would simply depend upon the strength of the economy, as was the case for Athens and Rome in ancient times. Their coinage was imitated because they were the dominant economies of their time. The value of a currency is the strength of its economy. It has NEVER been about its backing, which is purely a theory that arrived with paper money. Rome had no national debt. The value of the currency was more than its metal content. Here we have a gold aureus of Septimus Severus (193-211 AD) and the imitation in gold made in India. The imitation weighed more than the original. Imitations were made in the same quality of metal, so it proves that it was not a counterfeit but that a coin from the core economy possessed a greater value than the raw metal.

Just compare Russia, which has tremendous resources, against China, Japan, and Germany that had really no gold reserves. Russia did not expand its economy while the others boomed because of its people. The value of a currency is the TOTAL productive capacity of its economy — the work ethic of its people. Russia has not been able to rise substantially because it never fully embraced the idea of capitalism. They moved from communism to an oligarchy.

COMMENT: Hi Mr. Armstrong…..this is a surprising (to me) summary, on John Law. Every piece I ever read about him, cast him as a complete scoundrel, yet you obviously write with admiration. Just another example of history depending on someone’s perspective. You never cease to surprise. And that’s good.

HS

REPLY: John Law was actually a brilliant man. His legacy is not so different from John Maynard Keynes. He advocated deficit spending ONLY in times of recession, but governments have spent relentlessly with deficits that never end. We call this “Keynesian economics” when in fact he never advocated such a system. Likewise, John Law never advocated what the French government did in creating the Mississippi Bubble.

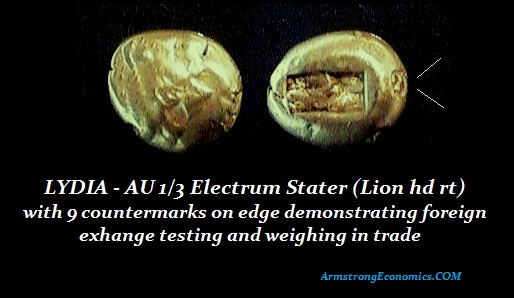

It is true that John Law fled to Amsterdam, but this is when he studied real banking operations and saw that money was actually virtual. Because coins were counterfeited or their edges shaved, bank money was more valuable than coins. Once the coins were deposited, each had to be inspected. So the bank became a sort of guarantor of the validity of the coins. Here is an ancient coin from Lydia with numerous banking marks applied, verifying that the coin had been inspected by them before for the same reasons.

It was this first-hand observation that led John Law to see that money was actually virtual, whereby people preferred bank money to actual coins. John then returned to Scotland, where he published in 1705 his Money and Trade Considered, with a Proposal for Supplying the Nation with Money. Law would later publish a second edition in 1720. He attempted to use his writing to convince the Scottish Parliament to adopt his ideas about money, but they declined, giving rise to the adage that a genius is never acknowledged in his native land (i.e. Columbus, Einstein to just mention two). Law had captured a glimpse of the virtual money supply as he was fascinated with the development of “bank money” that was displacing bullion in circulation.

Therefore, John Law has been hated by hard money people because they fail to understand that coins became second-best to actual paper money, for it relieved the problem of having to test every coin in a large transaction. Where Scotland refused to listen to John Law, France took him up on his observations. In 1716, John Law was invited by France to give it a shot. King Louis XIV (1643-1715) had squandered France’s resources on numerous wars and the construction of the Palace at Versailles. The idea of borrowing to fund wars and expansion had ruined the governments of men. Louis XIV had also adopted the theory that it was a divine right of kings to act as a dictator. This idea has persisted behind the curtain for centuries and dominates even American politics where you cannot sue the government without its permission.

For 54 years, Louis XIV worked daily for 8 hours, where he concerned himself with the very smallest of all details of state. He controlled everything from troop movements, infrastructure construction, court etiquette, and even theological disputes. He subordinated the nobles who had often instigated civil wars. Over the previous 40 years, there had been about 11 such civil wars.

The cost of this construction of his Palace at Versailles was far beyond the imagination. He effectively ran the country from Versailles and distanced himself from the people and Paris. Yet for all his extravagance, through the assistance of Jean-Baptiste Colbert (1619-1683), he was responsible more than anyone else for forging France into a more modern country.

John Law has been blamed for the Mississippi Bubble when, in fact, France was on the brink of its third bankruptcy when it contacted him. The government entered a partial default by consolidating its debt and changing its terms. Its new issue of billets d’etat was still required for more funding. The shortage of gold and silver coinage was plunging the economy into a depression. Law’s first proposal for a national bank issuing bank money was rejected. The second proposal to create a private bank was accepted and thus Banque Generale was established in May 1716.

The bank began to lend on its own shares, and the government intervened to support the price of its share by decree. Like the US government ordering the Federal Reserve to provide a floor to US bonds during World War II, likewise, the French government tried to maintain the value of the shares at 9,000 liver. Law begged the government to reduce the floor to 5,000, but they refused. They ended up blaming Law and arresting him no so unlike how the Democrats charged owners of S&Ls which failed when it was Congress who was changing the laws and creating a one-way market where everyone tried to sell.

The Democrats are out to end saving and passing on something for your children. I am sure those who voted for Biden simply because they hated Trump will find out what the real agenda is fairly soon. It might simply be a good time to die right now because the Democrats tear up everything that made America the land of opportunity.

The one thing that I would have to agree with Karl Marx on was his version of the “rich” in England was all about preventing the lower classes from ever obtaining wealth. You would take a house and basically pay full value, but it was for a 100-year lease, the way the Brits did in Hong Kong. The 100 years pass, and the property reverts to the historical owners. It was known as a “long lease.” The term “freehold” meant that it was a property you and your family could actually own.

The Democrats are back to the same philosophy of the old aristocratic families of England. Instead of the aristocratic families retaining the title, the Democrats want whatever wealth you have earned and saved to make your family well established to revert to the state. People fled Europe and came to America so they could actually own the property outright. The Financial Panic of 1792 inspired Ben Franklin to say, “In this world nothing can be certain, except death and taxes.”

Many people have criticized my solution that the government should be prohibited from borrowing and it should simply create money to cover its expenses each year capped at 5% of GDP — all federal taxes should be abolished. State and local taxes would still exist since they cannot create money. But they too should be prohibited from borrowing.

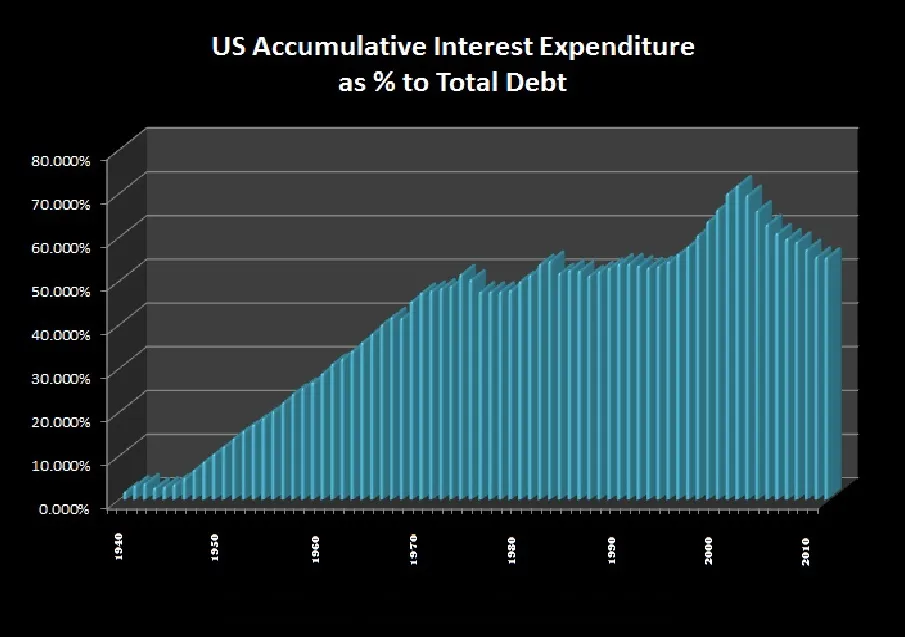

My critics will argue this will be inflationary. My point is that would be a dramatic improvement over the current system and eliminating federal debt means that the capital will be redirected into the private sector, creating far more economic growth. Politicians are incapable of managing the economy and should be prohibited from attempting anything. At times, up to 70% of the national debt is accumulated interest expenditures because they borrow year after year with NO intention of paying anything back.

Biden will not destroy the economy because he is spending recklessly, and then argues we must raise taxes to pay for this spending. Yet, the government will never pay for everything because they need to reduce the debt.

So, my solution would have kept your family and their future. Under the Democrats, they are wiping out the future of your family. We are returning to the days where private wealth is not something they will tolerate.

Remember one thing — 99% of all revolutions are created because of taxes! NO TAXATION WITHOUT REPRESENTATION!

COMMENT: Well it looks like the coronavirus is going to cause a major problem because everyone will be deducting their home offices.

HL

ANSWER: You better check with your accountant. It is my understanding that if you are a W2 employee, you cannot take a home office deduction. Currently, you need to have self-employment income to benefit from home office deduction. This is going to cause real problems now that so many people are forced to work remotely. I seriously doubt the Democrats will allow a deduction for working remotely.

Your post today on inflation(when people see it coming) reminds me how things have changed from the 1970s. Then, the inflation we saw came from oil rising(Opec raising prices), unions demanding wage increases, and currencies untethered to the abandoned Bretton Woods agreement. Governments then seemed clueless how to stem this rise, with interest rates rising relentlessly, pressuring bonds and eroding earnings of still largely manufacturing-based economies. Globalization was not an issue as half the world still lived under communism.

Today, it seems central banks have “learned” how to rig interest rates by flooding markets addicted to debt. What is different today is governments now, instead of fearing inflation, actually want it. In fact, desire it to bring about the Great Reset. They appear to want to drive oil prices higher to such levels that this makes Green Energy cheaper and helps to accelerate the conversion over to electric cars. All at the expense of the consumer. On top of this, taxing old tech, principally oil and gas, only helps to fuel shortages, since companies have cut back on oil exploration. When you force people to stay home, the demand for energy shifts from driving to people staying home, more demand for computers, more energy required to supply the grid, more companies delivering products to the home. What has been accomplished? People fleeing high tax states to ones that remain open, those with no state income taxes, those in the south. The burden shifts to northern states, the advantage gained by southern states.

Today, governments are deliberately fueling these shortages…encouraging them, to expedite the transition away from globalization to one centrally controlled. No longer do they need access to debt markets, they can supply guaranteed income without fear of inflation or failed bond auctions. This is truly diabolical. And with Big Tech doing their bidding, people too stupid to grasp what is happening, it appears today’s inflation is by design, intended to destroy a private business, which can’t compete with large companies, jobs destroyed, inflation today used as a weapon against private enterprise. This is pure evil, which stands out against the market-based inflation of the 1970s.

MS

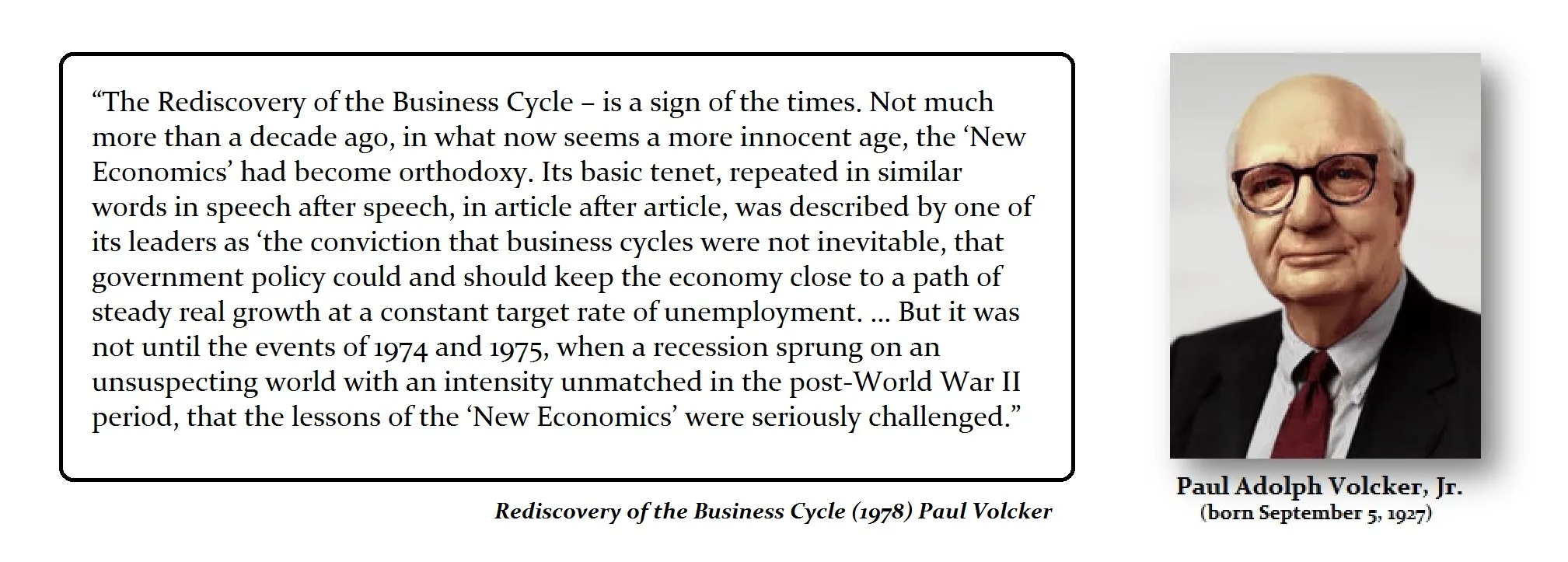

REPLY: You are correct that it was a period of unions demanding more, but it was more than just that aspect. There were two other major developments. First, there were rising prices with lower economic growth. This became known as STAGFLATION. This took place because COSTS were rising from an external price shock that rippled through the economy, which was created at the same time as an economic recession. That never took place before because previous recessions were entirely confined domestically, so prices declined with lower demand.

It was more than simply the collapse of Bretton Woods. It was the in-your-face collapse of Keynesian economics. Still, it was Paul Volcker who followed Keynesianism and raised interest rates into 1981 simply because he had no other theory available. I had a conversation with Volcker at the IMF Dinner in Washington. I did not bash him over his head with his mistake, he was so tall it would have been hard to do so, but we did have a frank discussion of the changes in the global economy.

Today, the central banks are still trapped by the same Keynesian economic theories. Now, they have painted themselves into a corner with artificially low interest rates that they cannot escape without a drastic alteration to the debt markets as a whole. Volcker could at least correct his mistake by lowering interest rates. Today, the central banks cannot raise rates without blowing up their own portfolios. It is a very different type of crisis they face today than what it was during the 1970s.

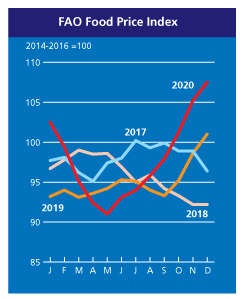

We are staring in the face of a serious food crisis in Europe as food prices rise continuously, and with further draconian COVID measures within the EU, they are bringing the food supply chains to a standstill. Our models have been warned that this 8.6-year cyclical wave into 2024 will be one of commodity inflation due to SHORTAGES rather than speculative demand. All the indications that the world is heading for a serious food price crisis are in play. The Food Price Index (FFPI) of the Food and Agriculture Organization of the United Nations (FAO) averaged 107.5 points in December 2020, an increase of 2.3 points (2.2%) compared to November 2020, which represents an increase for the seventh consecutive month.

With the exception of sugar, all sub-indices of the FFPI recorded slight gains in December, with the sub-index for vegetable oil again rising the most, followed by that for dairy products, meat, and cereals. For 2020 as a whole, the FFPI averaged 97.9 points, a three-year high, 2.9 points (3.1%) higher than in 2019, but still well below its 2011 high of 131.9 points. It is also interesting that the FFPI in 2002 was still 53.1 points. It only increased significantly from the financial crisis of 2007/08, only to then level off in the 90-point range. Since May 2020 it has increased by 18%.

Our models project that the upward trend in the FFPI will intensify going into 2024. With the coronavirus mutating, as we warned ALL viruses do, as such, we have these various strains from Africa, Brazil, UK, and even California, are inspiring politicians to use this as an opportunity to restrict the population even further. These corona measures have extended to the food supply chains, disrupting them just as we see in electronics. For example, the German Fruit Trade Association sees the supply of fruit and vegetables from abroad is at a substantial risk whereby imports are suspended. The reason is the tightening of the corona entry regulation by the federal government. The tightening of the lockdown in Europe is beginning to restrict the supply chains reducing the food supply

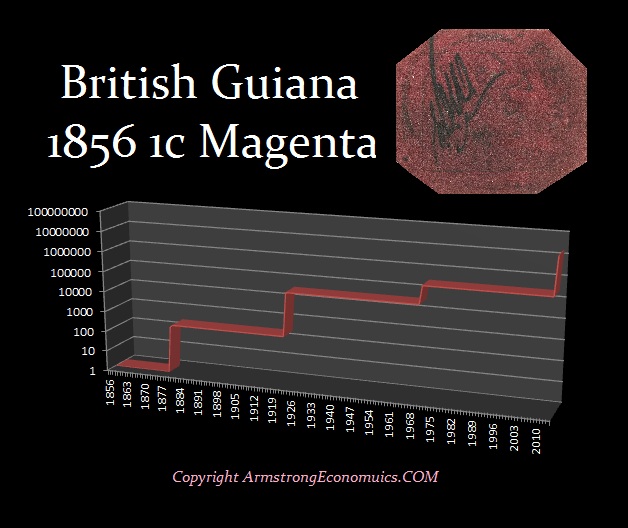

This June, Sotheby’s will be auctioning off three of the greatest rarities in the stamp and coin field. The 1933 Double Eagle $20 gold coin, the unique British Guiana One-Cent Black on Magenta, and the unique Inverted Jenny 1918 Plate Block. This is truly an incredible offering from a single collector to have captured three of the rarest and most unique collectibles in history.

It is a bit unusual that a unique stamp from a less than the mainstream region has emerged as the rarest and sole-surviving example of the British Guiana One-Cent Magenta from 1856. It was last sold in 2014 at Sotheby’s for $9.48 million. While it was rediscovered by a 12-year-old schoolboy living in South America in 1873, perhaps due to fantastic marketing, it has emerged as one of the most important stamps in famous collections that have ever assembled. In 1873 L. Vernon Vaughan, a 12-year-old schoolboy living with his family in British Guiana found the stamp among a group of family papers bearing many British Guiana issues. The young philatelist would later sell the stamp for several shillings to another local collector. The British Guiana then entered the UK in 1878, and shortly after, it was purchased in Paris by Count Philippe la Renotière von Ferrary who many considered to be perhaps the greatest stamp collector in history. Then following the war, France seized Ferrary’s collection, which had been donated to the Postmuseum in Berlin, as part of war reparations due from Germany following World War I. The stamp was then sold in 1922 at auction when it was purchased by Arthur Hind, a textile magnate from New York, for its first auction-record price of $35,000. The stamp changed hands moving from the collections of the Australian engineer Frederick T. Small; then a consortium headed by Irwin Weinberg; then by John du Pont of the famous chemical company. Du Pont paid $935,000 for the stamp in a 1980 auction, before it was last sold at auction to Weitzman for the record-setting price of $9.48 million.

Interestingly, a tradition emerged where previous owners of the British Guiana signed the back of the stamp. Weitzman added his own personal mark to the reverse of the stamp inscribing his initials “SW” along with a line drawing of a stiletto shoe as a nod to his legacy in fashion.

This 1933 Double Eagle ($20 gold coin) is the only example that may be legally owned by an individual. It was the coin acquired by King Farouk of Egypt. Stuart Weitzman purchased the coin at a Sotheby’s/Stack’s auction in 2002 for a world record price of US$7.59 million, nearly doubling the previous record. The Director of the United States Mint signed a Certificate of Monetization that, in return for twenty dollars, authorized the issuance of this single example.

In August 2005, the US Mint announced the recovery of ten additional stolen 1933 double eagle gold coins from the family of Philadelphia jeweler/coin dealer Israel Switt, who was the illicit coin dealer identified by the Secret Service as a party to the theft who admitted selling the first nine double eagles that were recovered. Israel Switt had many contacts and friends within the Philadelphia Mint. As the story goes, the Secret Service found that only one man, George McCann, had access to the coins at the time and served prison time for similar embezzlement in 1940. Israel Switt somehow obtained the stolen 1933 double eagles. One theory is that McCann swapped the previous year’s Double Eagles for the 1933 specimens prior to melting, thereby making sure the count was correct. The US mint began striking Double Eagles on March 15, 1933. Roosevelt’s executive order to ban gold was not finalized until April 5. Therefore, on March 6, 1933, the Secretary of the Treasury ordered the Director of the Mint to pay gold only under a license issued by the Secretary, and the United States Mint cashier’s daily statements do not reflect that any 1933 Double Eagles were paid out.

In September 2004, the claimed owner, Joan Switt Langbord, heir to Israel Swift, tried to sell the 10 coins and they had to be surrendered to the Secret Service. In July 2005, the coins were authenticated by the United States Mint after working with the Smithsonian Institution, as being genuine 1933 double eagles. Joan Switt Langbord claimed to have found them in a box and she went to court to have them returned. On October 28, 2010, US court ruled and the issue went to trial in July 2011. On July 20, 2011, after a ten-day trial, a jury ruled unanimously in favor of the United States government and Lanford appealed. At first, the Court of Appeals overruled the jury, but then it went En Banc and the Court of Appeals ruled in favor of the government. The Langbords appealed to the U.S. Supreme Court, which on April 17th, 2017 denied certiorari.

Hetty Green’s son, Edward Howland Robinson Green (1868-1936), was not so frugal and spent $3 million on coins and stamps. He was an avid collector and bought the famous sheet of 100 inverted airmail stamps in 1918, paying $20,000. The last time this Plate Block appeared on the market was 16 years ago when it sold at auction for $2.97 million.

Meanwhile, the classic Ferraris from the 1980s have nearly doubled in price over the past year.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America