Sudan is the new site for the ongoing proxy war between Russia and the West, reminiscent of the Syrian conflict. The media had turned a blind eye to the internal conflict in Sudan under the idea that it did not involve us, unlike other global wars that can be used for profit and power. Then Russia became involved, and the world began to notice the destruction happening in the African country. Russian oligarch Yevgeny Prigozhin is allegedly providing weapons and humanitarian aid to the RSF under the Wagner Group, a Russian paramilitary organization. Prigozhin claims Russia has not been involved with Sudan for two years, but numerous sources state otherwise. No one cared about the people of Sudan until Russia became involved, and now there is an international outcry with false flags galore.

“We do have deep concern about the engagement of the Prigozhin group, the Wagner Group, in Sudan,” US Secretary Anthony Blinken told reporters. “It’s in so many different countries in Africa — an element that, when it’s engaged, simply brings more death and destruction with it.” Wagner Group does operate in numerous countries in Africa and even has a naval base in the Red Sea that was established in 2019. Moscow has gained access to natural resources, military bases, and satellite locations, as well as securing arms deals, in exchange for providing mercenaries through Wagner. Most importantly, Russia has access to the gold mines in Sudan. The West is accusing Russia of using the proceeds from these mines to fund the war in Ukraine. There are also reports of Russian mercenaries surrounding the port of Sudan, and there are claims they are preventing people from evacuating.

The biggest false flag in Sudan — there is a risk of a “germ bomb” spreading across the globe after Sudanese soldiers hijacked a biolab. The World Health Organization (WHO) says the biolab poses a “huge biological risk,” and trained medical technicians can no longer access the facility. The facility has no power, and “it is not possible to properly manage the biological materials that are stored in the laboratory for medical purposes.”

Polio, measles, and cholera are the only diseases that they are reporting on. Coincidentally, these are illnesses with developed vaccinations, although the cholera vaccine is not widely used in the US. This could be a method to encourage vaccinations on the global population once again. It is also an excuse for foreign nations to invade under the premise of health vs. wanting to expel Russia.

What happened in Sudan is precisely what happened to all nations, empires, and city-states before their demise. Change happens once the people protecting those in power side with the disgruntled people pleading for revolution. The military generals who stick by the government are in direct conflict with those who wish for a regime change. As in Sudan, the military is no longer one unified body but becomes multiple warring armies fighting for power. This has been going on in Africa (e.g., Somalia) and countries in the Middle East for a long time. We will soon see the same course of action in the West—it’s just a matter of time.

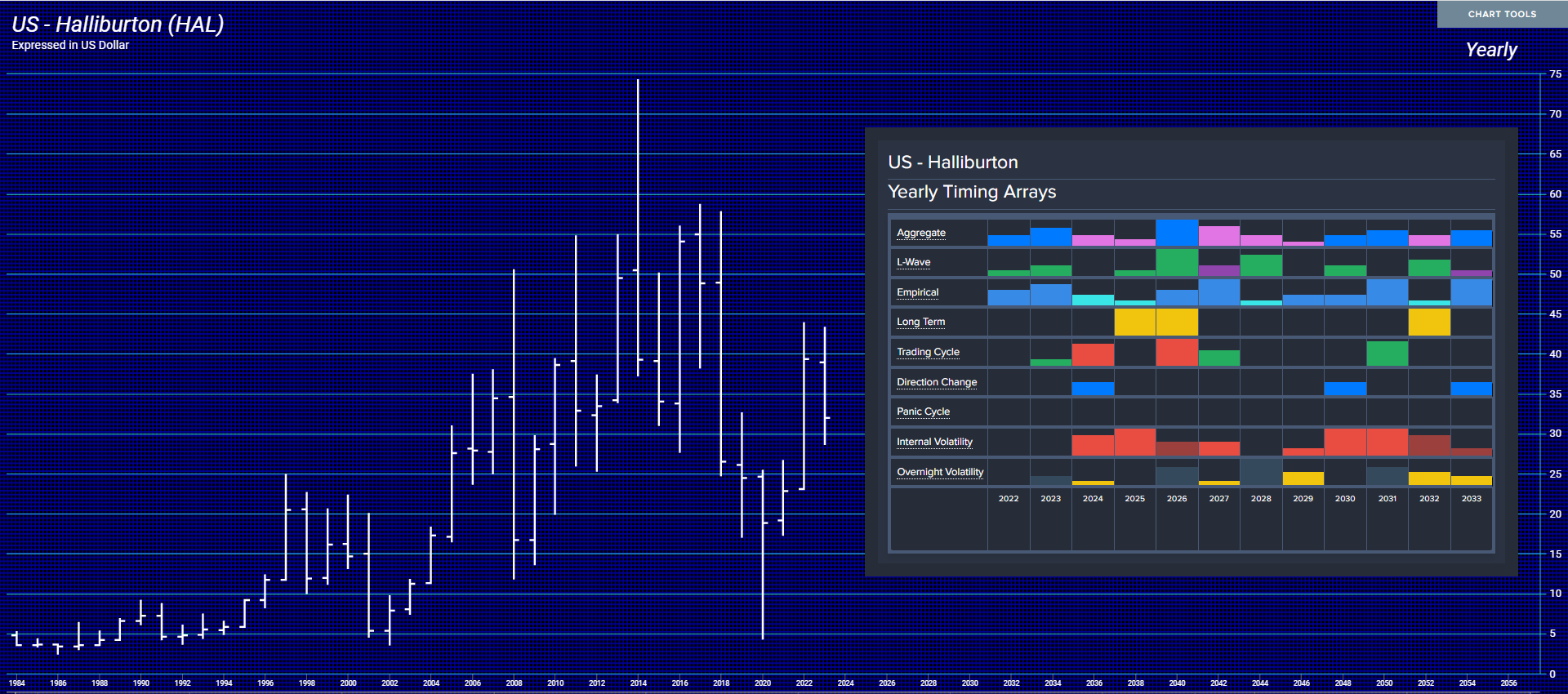

Zelensky is slick. He is now lining his pockets with the goal of becoming a billionaire when he flees to his estate in Miami. He is now trying to sell off all state assets in the fossil fuel sector to corporations like ExxonMobil, Chevron, and Halliburton. Of course, these companies are all showing that war is coming. The volatility rises sharply from 2024 on and a critical target will be 2026. This is what makes me think that the Neocons will do whatever it takes to stop Trump and that will include even assassinating him as they did to JFK to wage their war against Russia in Vietnam.

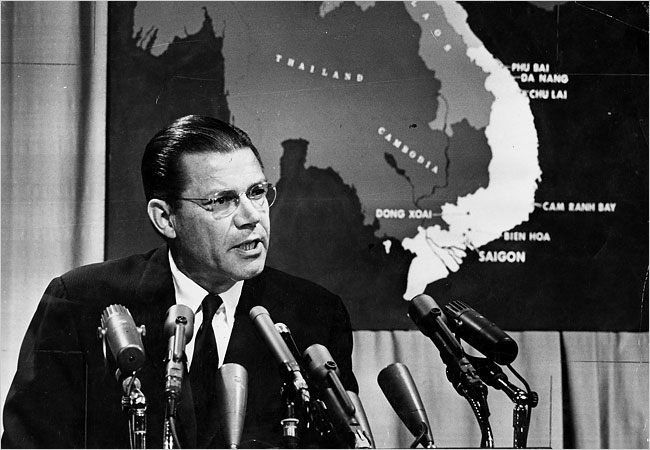

Robert McNamara (1916 – 2009) was a leading Neocon that pushed the country into the Vietnam War. He was famous for saying: “I learned early on never answer the question that is asked of you. Answer the question that you wish had been asked of you. And quite frankly, I follow that rule. It’s a very good rule.”

Before he died, McNamara wrote a book, perhaps to clear his conscience, and finally admitted that they were wrong, particularly in their assessment of Russia as a threat. The Neocons today regard him as a traitor and wrong. I have yet to hear even any kind word about him from their camp of endless wars.

The perception that Russia is a threat is still dominating the agenda today. The propaganda that Putin is a KGB guy who wants to re-establish the Soviet Empire is absurd. In the 22 years that he has been in power, he has neither tried to re-establish communism nor has he sought to retake the old Soviet states like Poland, the Czech Republic, or even Ukraine. The same claims today about Russia are the very same ones that justified Vietnam.

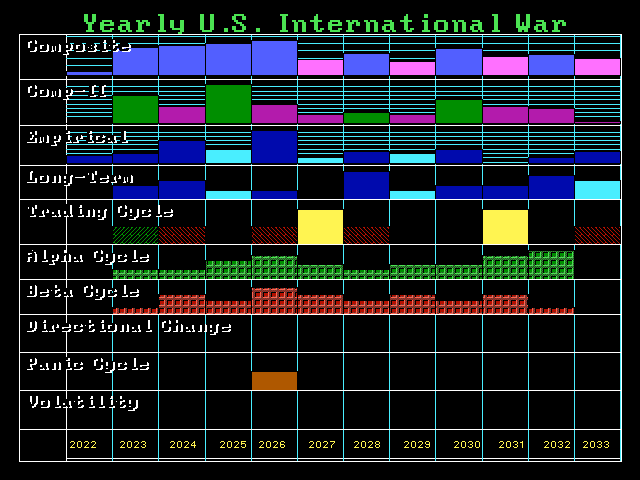

Looking at the cycles in the markets and war, these people will destroy Western Civilization. The Ukrainian people are absolute fools, for their leadership is also so wrapped up in their hatred of all the Russian people that they are leading their country into total destruction. Ukraine will cease to exist as a country that they dreamed of. They are surrendering their lives all for the dreams of the Neocons with Blinken in charge.

Several families with people in the military are reporting that soldiers are being informed we will be at war as soon as this year. Then Army aviators, who are entitled to leave, have been told they suddenly now owe 3 more years instead. People are suddenly finding out that we are not in Kansas anymore. We have no rights, and the Neocons have seized control of Washington. Welcome to their version of democracy.

Writing on Twitter, Mykhailo Podolyak said the U.S. and other Western nations encouraged Ukraine to give up nuclear weapons as the former Soviet Union collapsed, offering safeguards in return. This was misinterpreted by Russia, leading to conflict, Podolyak is the warmonger who argues that there shall be no surrender of the Donbas despite the fact that the population there are Russians and that Kyiv began the civil war on the order of the American Neocons. It is not that Ukraine surrendered its nuclear weapons; that is a fool’s argument. Europe and the US have nukes and so do Russia and China yet we are headed into war anyway. He will not let the people of the Donbas vote in a democracy when they are treated like vermin and are hated as Russians. This is why Ukraine has become an evil empire destined to create World War III just as our computer forecast back in 2013 one year before their revolution of 2014.

Posted originally on the CTH on May 1, 2023 | Sundance

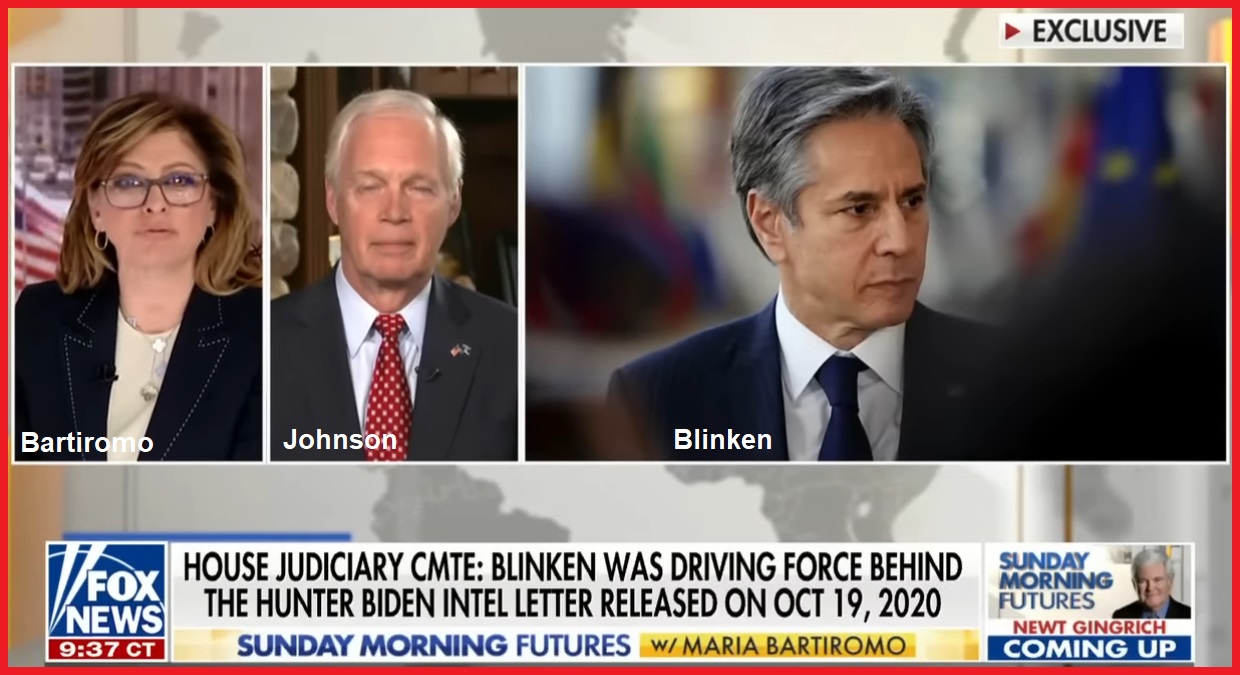

During an interview on Sunday conducted by Maria Bartiromo with Senator Ron Johnson, ranking member of the Senate Homeland Security Committee, Senator Johnson revealed that Republicans on his own committee refused to investigate the issues that surfaced from the Hunter Biden laptop, because they were worried about the appearance of politics during a 2020 election year. Note, that’s an outcome of a Mitch McConnell decision.

Additionally, following revelations from the laptop of Hunter Biden, Senator Johnson outlines that current Secretary of State Anthony Blinken lied to congress when he said he never had any email contact with Hunter Biden. Emails from Secretary Blinken are on the Biden laptop. WATCH:

Posted originally on the CTH on May 1, 2023 | Sundance

Everything about the process of cutting down energy exploitation, then driving supply side inflation, then raising interest rates to shrink demand (stem inflation) created by a desire to lower economic activity to the scale of diminished energy production, is a game of pretending.

The collateral damage from the rate hikes has been the banking destabilization, which shows the priority of the government officials and central banks to support the climate change agenda. Into the game of pretending comes the second unavoidable consequence with inflation continuing as a result of the energy policy.

They simply cannot cut energy demand enough to meet the diminished scale of production. There is no alternative ‘green’ energy system in place to make up the difference. That is the reality. Now, the fed is scheduled to raise rates again, then begin to debate the collateral damage as they continue the pretending game.

(Via Wall Street Journal) – […] Another quarter-percentage point increase would lift the benchmark federal-funds rate to a 16-year high. The Fed began raising rates from near zero in March 2022.

Fed officials increased rates by a quarter point on March 22 to a range between 4.75% and 5%. That increase occurred with officials just beginning to grapple with the potential fallout of two midsize bank failures in March.

The sale of First Republic Bank to JPMorgan Chase & Co. by the Federal Deposit Insurance Corp. announced early Monday is the latest reminder of how banking stress is clouding the economic outlook.

Fed officials are likely to keep an eye on how investors react to that deal ahead of Wednesday’s decision, just as they did before their rate increase six weeks ago when Swiss authorities merged investment banks UBS Group AG and Credit Suisse Group AG. (read more)

There is no other way to look at the combined policy without seeing a Central Bank Digital Currency (CBDC) in the future. All of these combined policies are creating a self-fulfilling prophecy.

Posted originally on the CTH on May 1, 2023 | Sundance

The topline story from the announcement by JPMorgan Chase [SEE HERE] there are no banking rules/laws in the Biden Fed/Treasury system.

The Dodd-Frank laws are still on the books, but the FDIC decision to insure all deposits, regardless of size, now means those laws, rules and regulations are not required to be followed. Additionally, as a result of JPMorgan gaining another $100+/- billion in deposit assets, the law(s) surrounding the 10% U.S. deposit maximum, within too big to fail banks, no longer exists. Noted in the announcement, “JPMorgan Chase is assuming all deposits – insured and uninsured.”

JPMorgan is also assuming assets consisting of $173 billion in loans and approximately $30 billion in securities. The FDIC is going to assume risk (with a risk sharing agreement) for current First Republic Bank mortgage and commercial loans acquired by JPMorgan, guaranteeing JPMorgan a 5-year fed fixed rate on $50 billion in mortgage bonds.

The Federal Deposit Insurance Corporation (FDIC) rule requiring the holding of 1.5% of deposits for all depositors up to $250k in all institutions is now essentially moot. If the FDIC is guaranteeing all deposits, there’s no way for the insurance corporation to capture or hold $1.5% of all banking deposits. The law is in conflict with the outcome action of the Fed/Treasury and ultimately the FDIC, ergo the law is nulled by the ignoring of it.

Mohamed El-Erian gives his take below, but seemingly missed the part of the announcement where JPMorgan states, “no systemic risk exception was required” in the deal. This means the FDIC is completely free-range with the agreement, they are not even trying to justify why they would make a too big to fail bank even bigger. WATCH:

.

The only reason the FDIC violated its own rules and banking regulations, was because the FDIC didn’t, likely -almost certainly- couldn’t, take the financial hit from a full takeover of First Republic Bank against the backdrop of the prior terms for Silicon Valley Bank (SVB).

When the FDIC made the (SVB) decision to guarantee all deposits regardless of size, they put themselves in a position of an insurance declaration they could never fulfill. The FDIC cannot structurally guarantee all of the First Republic Bank (FRB) deposits; they need a structure to avoid the government regulators absorbing the bank. This reality is also why the FDIC violated their own laws, rules and regulations in allowing JPM to exceed the legal U.S. deposits maximum.

In essence, what the FDIC is saying is they cannot maintain the premise of their charter without the big banks helping them. The biggest banks now control all of the leverage, with JPMorgan Chase and Jamie Dimon now controlling more financial power than the government that is supposed to regulate them.

FUBAR… All of it. Everything Biden touches turns to shit.

This is going to be a major hot mess now for Main Street investment and borrowing needs. The economy is going to feel the ramifications of this in less financing available to maintain domestic investment.

Last point. Look at the big picture, there’s no intervention protocol the legislative branch can trigger as a security against the reckless decisions of the FDIC (Fed and Treasury), without creating even bigger issues that could collapse the banking system. If the legislative branch forced the FDIC to follow the laws currently on the books, the domino of banks starts to collapse.

Posted originally on the CTH on April 30, 2023 | Sundance

Victor Davis Hanson often has a unique big picture perspective on current events, linking and contrasting the disconnected high-brow outlook to the pragmatic perspectives of the modern populist movement.

Hanson takes an academic approach to the reality of current social constructs, yet in his own unique way he can describe the current status in a thoughtful and practical way. In this analysis VDH contrasts the goals of the ideological media, specifically the goals of those in the Republican wing of the media control apparatus, to the reality they have created by removing the voice of Tucker Carlson. WATCH:

.

In their quest to control the mounting opposition to the corporate manipulation behind the DC Potemkin Village, the corporate media are creating a nimbler and more consequential army of opposition to their efforts. The need for control is a reaction to fear.

There is a particular type of spider that carries several hundreds of young on her body after birth. If you spot one of these in your shower, and your irrational fear instinct is to smash what seems to be a big scary spider, what you discover in the aftermath is the bathtub walls moving. Yes, you may have squished the spider, but hundreds of smaller spiders are now crawling all around you.

Posted originally on the CTH on April 30, 2023 | Sundance

Gary Cohn is connected to the banking and finance industry, well connected. In this interview with Face The Nation earlier today, Cohn is discussing the current status of First Republic Bank, another big player in the California banking system that is about to collapse. Cohn notes something at the 1:15 mark that just seems obvious yet is undiscussed in most outlines of the FRB discussion.

Six weeks ago, in an effort organized by the FDIC, $30 billion was pushed into FRB by eleven larger banks to stabilize it. However, the only thing that infusion of capital did was allow institutional depositors time and ability to withdraw their funds. A complete racket. Once the at-risk group exits, suddenly the collapse is back on the tee. WATCH:

[Transcript] – MARGARET BRENNAN: We want to turn now to Gary Cohn, who is the vice chairman of IBM, former Goldman Sachs president and a former Trump administration top economic adviser. Good morning to you. Lots of titles, Gary, Lots of experience. That’s why we like having you here. I want to ask you about what’s happening with First Republic. It’s been under pressure. We know they’ve been looking for a buyer, the FDIC, the government is looking to arrange, moving it into government control and then maybe selling it. What are you hearing about how this would roll out?

GARY COHN: Margaret, thanks for having me. I think you’re portraying the situation as we find ourselves again on a weekend. As we closed business of Friday, the FDIC was in a process of looking for acquirers or bidders for the assets over the course of the weekend. I think the FDIC has asked potentially three banks for their final bids for the entire bank. The FDIC would prefer to sell the bank in its entirety than the pieces. What will most likely happen is the FDIC will seize control and then simultaneously resell the asset to the successful bidder. I think that will happen sometime later this afternoon before the markets open in Asia this evening.

MARGARET BRENNAN: And this will be a faster process than what happened with SVB?

COHN: It will be- it will be a much faster process. Now, we’ve been going down this process for the last two weeks or so as first republics continues to be under pressure and continues to lose deposits. Unfortunately, First Republic reported this week that they had a massive outflow of deposits over the last quarter.

MARGARET BRENNAN: So if First Republic is sold, then the acquirer would take on the deposits. So what do you think about the conversation we had earlier with Congressman Khanna about whether Congress needs to do something here? Because it seems like we’re just going into emergency mode now for three banks.

COHN: Yeah.

MARGARET BRENNAN: Does there need to be a broader change to the regulatory system and to the laws?

COHN: Well, it’s an interesting question. So, look, I don’t agree with Congressman Khanna that we want unlimited FDIC insurance. I think that to me is a bit of a race to the bottom.

MARGARET BRENNAN: You had picked like two, 2 million. 5 million, 10 million.

COHN: Yeah. I mean, there’s got to be some limit. It’s- at some point you have to limit because you don’t want to race to the bottom where you know, the weakest bank with the weakest balance sheet in the world can offer you the highest rate of return on your deposits. And therefore, you take your deposits there because guess what? They’re insured by the federal government. That’s not what we want to see. We want to see some type of discipline in the system. When you talk about more and more regulation, I smiled because if you look at the report that came out that you referenced with Ro Khanna as well, you know, one of the findings in the report is that the regulators did not do a very good job enforcing the existing rules. So if you can’t enforce the rules you already have on the books and by- it’s hard to enforce the rules because there are so many rules, do you want to create more and more rules when you can’t enforce the one you already have? Part of me feels like we need to get a simpler, more coherent set of rules so the bank regulators can actually enforce them and they know what the important rules are.

MARGARET BRENNAN: But the bank regulators here are at the Fed. That’s what we’re talking about here.

COHN: They’re at the Fed and at the States. Remember–

MARGARET BRENNAN: That’s true.

COHN: –we have state regulated banks and federally regulated banks.

MARGARET BRENNAN: Well, that’s a big conversation for California since they just had two banks–

COHN: It is.

MARGARET BRENNAN: –have some big problems. But Fed Chairman Powell is going to face questions from the press midweek.

COHN: Yes.

MARGARET BRENNAN: They- he gives a press conference around the decision on interest rates that he is expected to be making. Do you think these banking problems are going to interfere with his plan?

COHN: I don’t think these problems are going to interfere with his plans. I actually think they’re helpful to his plans.

MARGARET BRENNAN: Because they’re slowing the economy?

COHN: Exactly. What the- what the chair has been trying to do is slow the economy down. He’s been trying to tamp down inflation. Inflation is too many goods chasing too few products. And part of the chasing has been the easy availability of credit. Now that we’ve seen deposits lose- the- leave the system and we’ve seen banks in tighter financial position, they are not offering loans as easily as they were before and the loans have become more expensive. So people are borrowing less money, they have less access to credit, so their ability to purchase is going down. Purchasing power is waning in the United States, which is exactly what the chairman’s been trying to do by raising interest rates. So he’s in essence, getting enormous amount of help out of this banking crisis, not what he wanted to see happen in any way, shape or form, but the unintended consequence is very helpful to slowing down the economy and tamping down inflation.

MARGARET BRENNAN: So does it up the odds of a recession being more than mild?

COHN: It probably ups the odds. Yes. I mean, it definitely ups the odds. It takes control out of the Fed. The Fed is no longer in total control of slowing down the economy. They’ve now got the banking industry playing along with them. But as we’ve seen in the economic data recently, the consumer in the United States still is in relatively good shape. They are starting to run out of savings. The money that they got during COVID, we put an enormous amount of stimulus into consumers bank accounts and that administrations, both administrations, every every administration put enormous amount of stimulus in the bank accounts. We see from the savings data that’s starting to to wear down. It’s starting to run off. So is that runs off further and further. The economy would become more credit dependent to keep thriving. So I think we will see a slowdown. And I still think we’re in a relatively decent shape. We may have a recession, but I still. I think we could muddle through the bottom here without a real deep recession.

MARGARET BRENNAN: The chair of the House Financial Services Committee, Congressman McHenry, called the Fed’s report a self-serving justification of Democrats long held priorities. He may be venting. It doesn’t look like Congress is doing anything to change regulation or laws related to banking. There was an FDIC report on the collapse of Signature Bank, which blamed bad management, but it also said regulators just didn’t have enough staff. In New York. I mean, there’s some pretty damaging bits of information in here. If you put aside the politics, the regulators don’t have enough staff. They didn’t act. So who are they being held accountable by unless it’s Chair Powell?

COHN: Well, it is Chair Powell. And I think- I think when the chairman goes to Congress and remember, he testifies in front of both the House and the Senate a couple of times a year. Historically, all of the questions have been on monetary policy. I think we’re going to start seeing a lot more questions on the regulatory and the regulatory policy. How is regulation working? Are they keeping up to what they need to do? Do they have proper staff or there are issues that are going by that are not being covered? This is a huge finding. I mean, this is a bit of a seismic moment because we believe in the United States and I think the US population believes that the banks where they deposit their hard earned money are well regulated. And we have found out this week in the Fed’s own report that these banks are not well regulated, and they admitted it themselves. I ran a regulated bank. I know that if we would have ever told our regulator that we did not have a enough people to regulate ourselves, they would have shut us down. So we cannot be in a position where the regulators themselves say we do not have enough staff to regulate you properly.

MARGARET BRENNAN: You ran one of the biggest banks. Gary, we’ve got to leave it there. We’ll be back in a moment.

Posted originally on the CTH on April 30, 2023 | Sundance

Despite no one knowing ‘how’ Jeffrey Epstein actually made his money, one of the great mysteries amid a labyrinth of rabbit hole mysteries, the network of government officials and high-profile names who associated with and met Epstein has never been fully outlined or absorbed.

Other than a few random and specific names that surface from time-to-time, the lack of media curiosity into the bigger context of the Epstein story has always been somewhat perplexing. One would ordinarily think the opportunity for a Pulitzer might entice an intrepid media outlet to do a lengthy dive into the matrix of Epstein; alas, no effort toward that objective ever surfaced.

Today, another fragment in the story seemingly finds its way to the surface as the Wall Street Journal outlines a list of names that were not included in the “black book” story, but nonetheless were intertwined with Epstein *after* his first conviction as a sex offender [STORY HERE].

Two of the names within documents, schedules and calendars attributed to the Epstein life include current CIA Director Bill Burns and former White House lawyer Kathryn Ruemmler. In addition to being the White House legal counsel, Ms. Ruemmer was also the foundation lawyer for Bill and Hillary Clinton as well as the personal lawyer for Susan Rice.

(Wall St Journal) – The nation’s spy chief, a longtime college president and top women in finance. The circle of people who associated with Jeffrey Epstein years after he was a convicted sex offender is wider than previously reported, according to a trove of documents that include his schedules.

William Burns, director of the Central Intelligence Agency since 2021, had three meetings scheduled with Epstein in 2014, when he was deputy secretary of state, the documents show. They first met in Washington and then Mr. Burns visited Epstein’s townhouse in Manhattan.

Kathryn Ruemmler, a White House counsel under President Barack Obama, had dozens of meetings with Epstein in the years after her White House service and before she became a top lawyer at Goldman Sachs Group Inc. in 2020. He also planned for her to join a 2015 trip to Paris and a 2017 visit to Epstein’s private island in the Caribbean.

[…] The documents show that Epstein arranged multiple meetings with each of them after he had served jail time in 2008 for a sex crime involving a teenage girl and was registered as a sex offender. The documents, which include thousands of pages of emails and schedules from 2013 to 2017, haven’t been previously reported.

[…] Mr. Burns met with Epstein about a decade ago as he was preparing to leave government service, said CIA spokeswoman Tammy Kupperman Thorp. “The director did not know anything about him, other than that he was introduced as an expert in the financial services sector and offered general advice on transition to the private sector,” she said. “They had no relationship.”

Ms. Ruemmler had a professional relationship with Epstein in connection with her role at law firm Latham & Watkins LLP and didn’t travel with him, a Goldman Sachs spokesman said. Epstein introduced her to potential legal clients, such as Microsoft Corp. co-founder Bill Gates, the spokesman said. “I regret ever knowing Jeffrey Epstein,” Ms. Ruemmler said.

A spokeswoman for Latham & Watkins said Epstein wasn’t a client of the firm.

[…] Mr. Burns, 67 years old, a career diplomat and former ambassador to Russia, had meetings with Epstein in 2014 when Mr. Burns was deputy secretary of state.

A lunch was planned that August at the office of law firm Steptoe & Johnson in Washington. Epstein scheduled two evening appointments that September with Mr. Burns at his townhouse, the documents show. After one of the scheduled meetings, Epstein planned for his driver to take Mr. Burns to the airport.

Mr. Burns recalls being introduced in Washington by a mutual friend, and meeting Epstein once briefly in New York, said Ms. Thorp. “The director does not recall any further contact, including receiving a ride to the airport,” she said.

The following month, October 2014, Mr. Burns stepped down from his role at the State Department to serve as president of the Carnegie Endowment for International Peace, a think tank. He ran the Carnegie Endowment until he was nominated in early 2021 by President Biden to serve as CIA director.

The documents show that Epstein appeared to know some of his guests well. He asked for avocado sushi rolls to be on hand when meeting with Ms. Ruemmler, according to the documents. He visited apartments she was considering buying. In October 2014, Epstein knew her travel plans and told an assistant to look into her flight. “See if there is a first class seat,” he wrote, “if so upgrade her.”

[…] Epstein and his staff discussed whether Ms. Ruemmler, now 52, would be uncomfortable with the presence of young women who worked as assistants and staffers at the townhouse, the documents show. Women emailed Epstein on two occasions to ask if they should avoid the home while Ms. Ruemmler was there. Epstein told one of the women he didn’t want her around, and another that it wasn’t a problem, the documents show.

Ms. Ruemmler didn’t see anything that would lead her to be concerned at the townhouse and didn’t express any concern, the Goldman spokesman said.

[…] Over the next few years, Ms. Ruemmler, then a partner specializing in white-collar defense at Latham & Watkins, had more than three dozen appointments with Epstein, including for lunches and dinners.

“In the normal course, Epstein also invited her to meetings and social gatherings, introduced her to other business contacts and made referrals,” the Goldman spokesman said. “It was the same kinds of contacts and engagements she had with other contacts and clients.”

In 2015, she was scheduled to fly with Epstein to Paris and in 2017 he planned to stop in St. Lucia to take her to his island home in the U.S. Virgin Islands for the day, according to the documents. (read more)

Sketchy… All of it!

Dirty people, working amid a system that trades dirt as currency…

Posted originally on the CTH on April 29, 2023 | Sundance

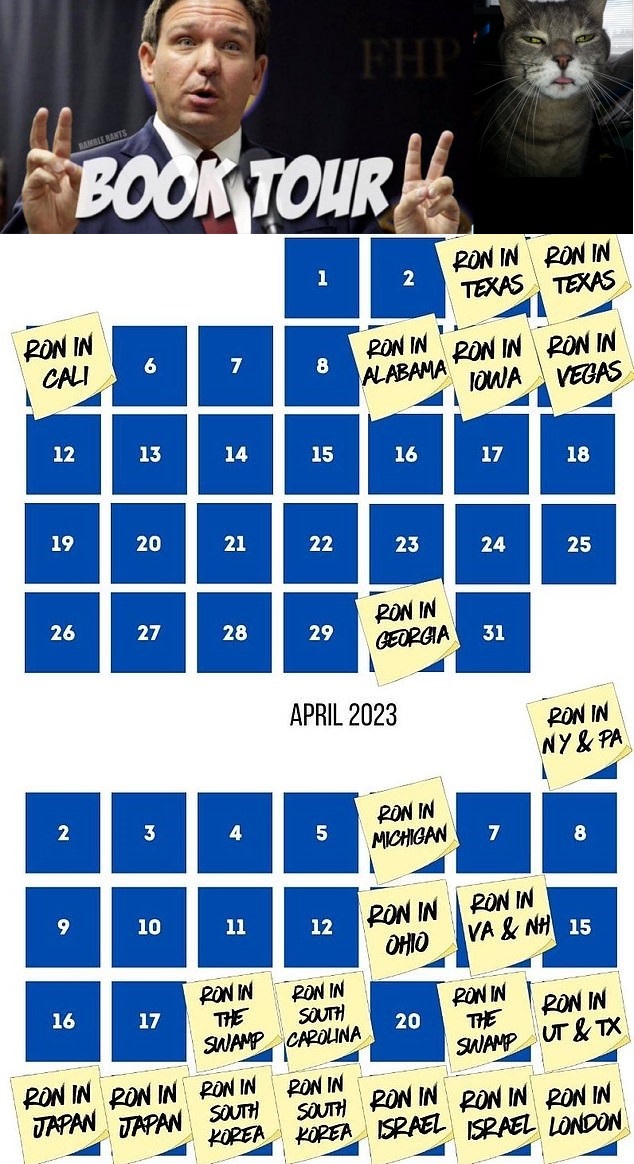

As Florida Governor Ron DeSantis finishes up his long-scheduled foreign policy tour, he finishes the trip on a down note in London, England. Apparently, the political and business leaders were unimpressed by the diminutive stature of the Top-Gov and had lots of uncomplimentary things to say about him.

Meanwhile, on the domestic front, the most recent Trump -vs- DeSantis poll shows another slip for the DeSantis brand managers, despite the considerable lifts they put in his shoes to assist the optics. President Trump now leads Ron DeSantis 62% to 16% in polling, a 46-point advantage {link}.

Governor DeSantis is scheduled to arrive back in Florida this week as the consultants organize bill signing ceremonies for legislation completed during his absence. The bills will include a change to the Florida election laws permitting Ron to start officially campaigning for president instead of pretending not to run. The ‘official’ announcement, which appears to have been planned for several years, is scheduled for mid-May next month.

LONDON — He hopes to win the hearts and minds of devoted Donald Trump supporters ahead of next year’s U.S. election.

But Republican presidential hopeful Ron DeSantis failed to impress British business chiefs at a high-profile London event Friday, in a tired performance described variously as “horrendous,” “low-wattage” and “like the end of an overseas trip.”

The Florida governor, expected to launch his bid next month to challenge Trump as the Republican nominee for the 2024 presidential race, met with more than 50 representatives of major U.K. firms and business lobbying groups as a part of a four-country “trade mission” ending in London Friday.

For several of those present, however, the statesmanship was lacking.

One U.K. business figure said DeSantis “looked bored” and “stared at his feet” as he met with titans of British industry in an event co-hosted by Lloyd’s of London — the world’s largest insurance marketplace.

“He had been to five different countries in five days and he definitely looked spent, but his message wasn’t presidential,” they told POLITICO. “He was horrendous.”

A second business figure who was in the room said it was a “low-wattage” performance and that “nobody in the room was left thinking, ‘this man’s going places’.”

They said: “It felt really a bit like we were watching a state-level politician. I wouldn’t be surprised if [people in attendance] came out thinking ‘that’s not the guy’.” “There wasn’t any stardust.” (Read More)

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America