Posted originally on the CTH on March 16, 2023 | Sundance

Small to medium sized banks along with credit unions are the best vehicle for Main Street USA small businesses. Somehow in all the conversations about banking customers, this little factoid is seemingly, perhaps purposefully, overlooked. WATCH:

In an interview on May 11, 2014, I explained on USAWatchdog that confidence always outweighs reality. “It’s basically what you believe. There have been all sorts of studies on fundamentals that say if interest rates go up, stocks go down. It is simply not true. The stock market has never peaked with interest rates twice in history. If you think you are going to make 25% in the market, you’ll pay 10% interest; but if you really think the market is only going to go up 10%, you won’t pay 10%. So, it’s always the difference between what you believe and reality.”

The people have lost all confidence in government. We have heard rumors of a “soft landing” from the Fed for the past year, but the situation continues to worsen. Washington maintains that everything is stable as banks continue to fail and inflation rages on. There can be no price stability when war is at play. Biden just released his latest budget plan that no reasonable person would condone. I explained in 2014 that great empires all come crashing down after piling on massive debt. People believe hyperinflation would cause such a scenario, but debt is the major player. Once the government accumulates enormous debt, it targets its citizens aggressively. That is what we are seeing today.

So where should you put your money? I said in 2014: “One of the number one questions I get all the time is where do I put my money? If the banks can just take whatever they want now, there will be bail-ins rather than bail-outs. People are afraid. What do you do with the cash? So, people are buying things like real estate and stocks, just trying to get money out of the banking system.” That sentiment is continuing and the latest CPI report even showed that shelter costs are rising at the highest rate since June 1982. Smart money has been trying to escape the banks for years. There was no incentive until very recently to park money in the banks due to artificially low rates.

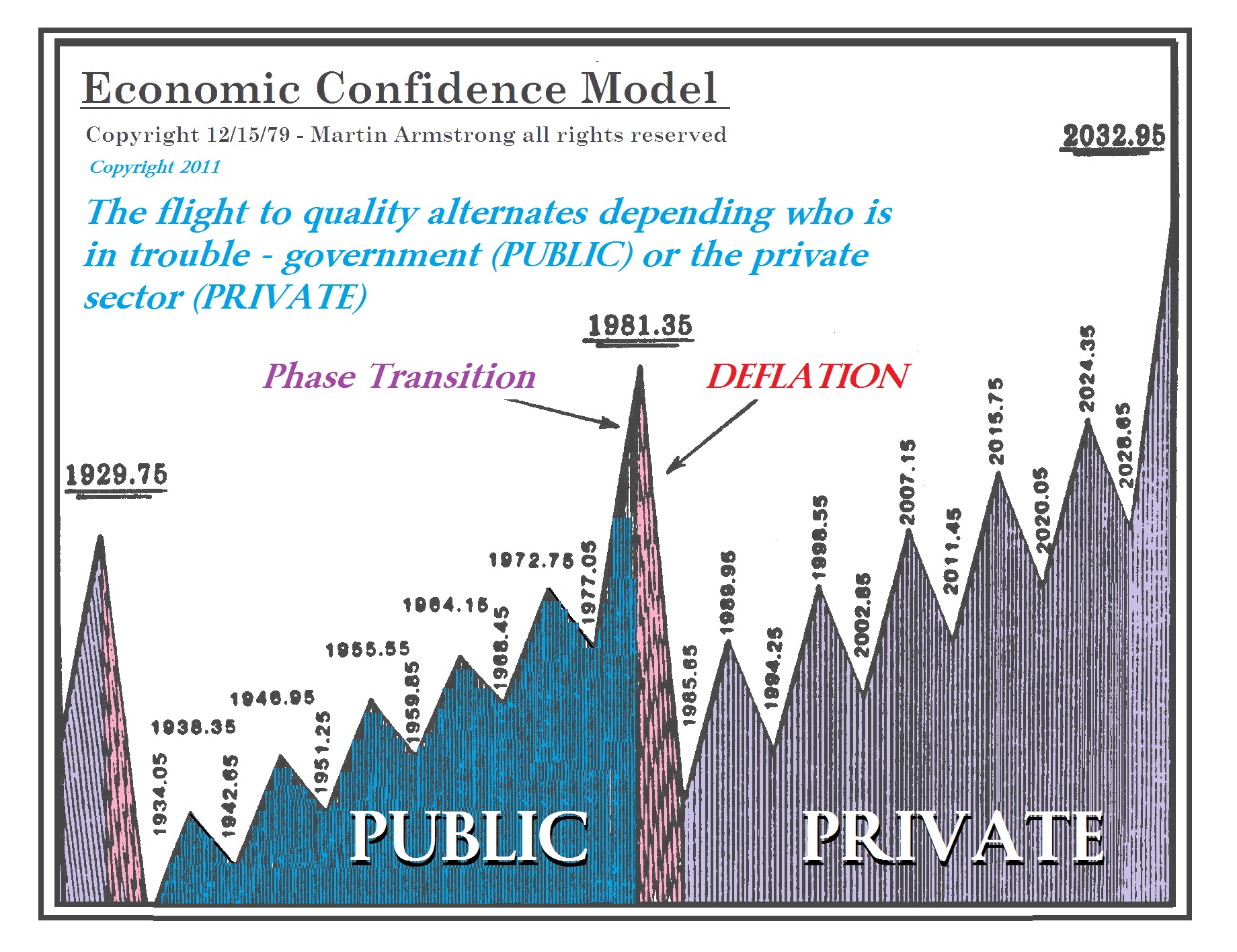

I also explained that the Fed would only bail out deposits and had been asking institutions to change their models. “Everybody knows I advise some of the big institutions around, and I can tell you that they have told me directly that the Fed went to them and told them they will not be bailed out for proprietary trading. It will be only on deposits. That’s it,” I stated. “The Fed has been going around telling them, ‘hey, you better change your models.’ They don’t think it will be a flight to quality as it was before. You buy the long term (Treasuries) and that saves you. They don’t think that’s going to happen. It’s quite interesting. . . . It looks like the long term (Treasury bonds) is going to end up starting to rise.”

Sound familiar to the current situation? People have moved from the public sector into the private sector. We are well into a private wave, and the public will not go back to the public sector for many years to come.

Posted originally on the CTH on March 13, 2023 | Sundance

The CNN panel was jaw-agape as Kevin O’Leary appeared earlier today to inform them the decision by Joe Biden to guarantee every deposit in U.S. regional banks is akin to “Joe Biden just nationalized the U.S. banking system.”

O’Leary is correct, and anyone who is holding assets like stocks or bonds in U.S. banks now needs to reconsider the disappeared line between government and the bank assets. If the government can assume, control and backstop every single account balance within the bank, the government can assume and control all activity of the bank. WATCH:

.

Downstream…. think about the consequences. Remember the frozen bank accounts in Canada as a result of defining truck protest supporting Canadian citizens as domestic extremists?

Now think about the government no longer needing to ask the bank to take action, the govt has a regulatory ability to demand the bank to take action. This takes “debanking” to an entire new level. People are wondering why cryptocurrencies went up in value today. There’s your answer.

Comrade citizens, at the end of this rainbow of bank nudges, we will find ourselves at the footsteps of a government controlled central bank digital currency.

The installed occupant of the White House said something today that is just brutally false on its face.

From the words typed into the teleprompter of Joe Biden you hear, “No losses will be borne by the taxpayers. Instead, the money will come from the fees that banks pay into the Deposit Insurance Fund.” Who the hell does Biden think are paying those “fees”? Those fees paid into banks, and then out of banks, from all around the nation are paid by the people using the bank, that’s taxpayers.

The United States government does not create a single dollar of revenue. They transfer revenue from people to processes and systems of government. Charles Payne has a good perspective on this entire dynamic. {Direct Rumble Link} WATCH:

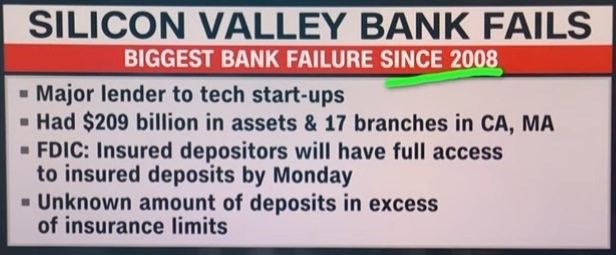

A bank failure of this proportion has not been seen since 2008 when Washington Mutual failed. The majority of deposits in Silicon Valley Bank (SVB) are uninsured, meaning the FDIC’s $250,000 protection does not apply. Uninsured depositors will be provided receivership certificates and should receive an advanced dividend this week. The FDIC must sell off the remaining assets of SVC to determine how much it can provide to those uninsured depositors. The FDIC is encouraging borrowers to continue paying their existing loans. The bank was said to host $209 billion in assets and $175.4 billion in deposits as of December 2022. Washington Mutual held around $307 billion in assets when it went down.

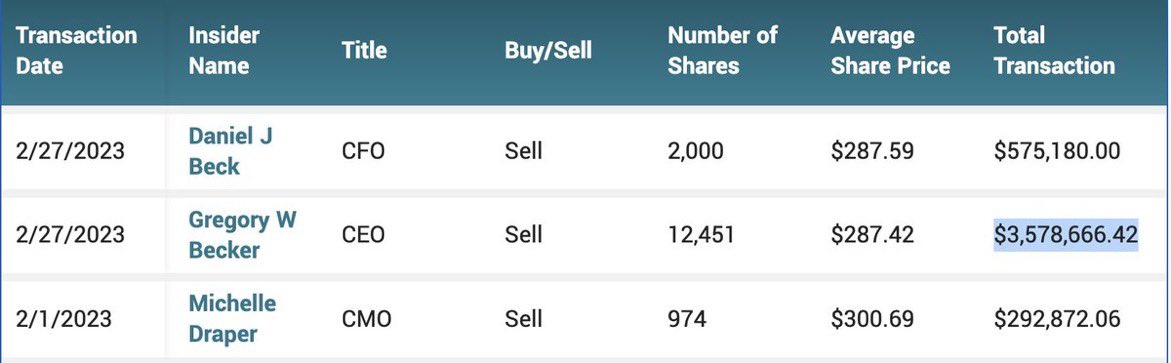

Tons of people and businesses will be completely screwed over. Who could have seen it coming? Silicon Valley Bank CEO, CFO, and CMO sold off millions in stock over the past two weeks. President and CEO Greg Becker sold 12,451 shares on February 27 for $3.6 million at $287.42 per share. Later that day, he purchased options for the same amount of shares at $105.18 a piece. He did the same thing in December 2021, as this is not an uncommon albeit unethical practice. Banks commonly trade against their own clients. Becker sold about $3.57 million worth of SVB stock over the past two weeks and is now making TV appearances saying he did not see this coming.

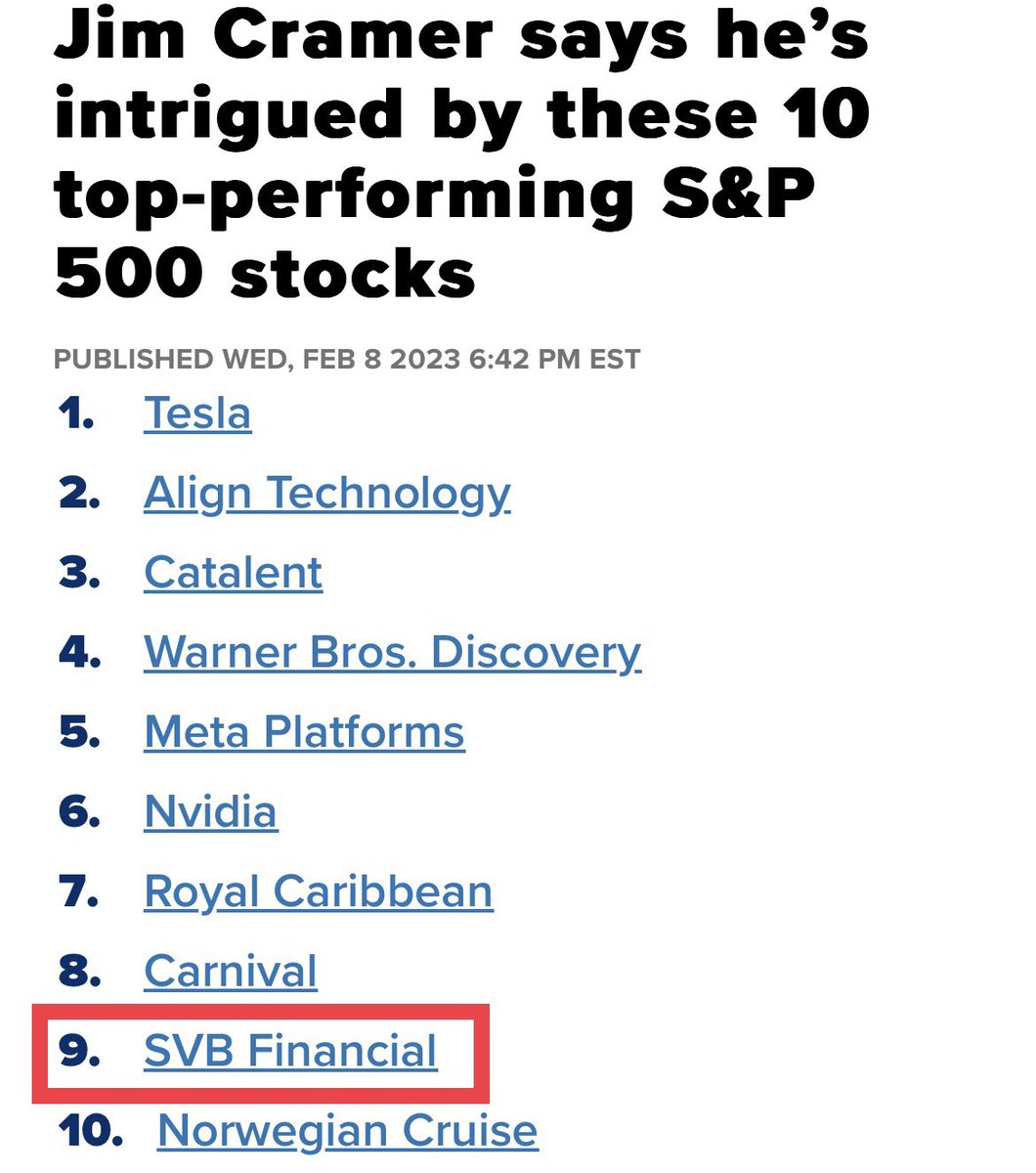

There were signs of trouble, but the talking heads said otherwise. Forbes even listed SVB Financial Group as #20 on its list of America’s Best Banks in an article published on February 14, 2023. Talking/screaming head Jim Cramer came out last month to say that SVB Financial would become one of the top performers on the S&P. This is why you cannot listen to information based on biased opinions. I hesitate to call this negligence technical analysis.

Companies are now at a complete loss, many cannot make payroll, and this situation will only worsen once the uninsured depositors realize their IOUs are worthless.

COMMENT: Marty; Two former Merrill Lynch traders were each sentenced to a year and a day in prison Thursday for manipulating the precious metals markets, the US Department of Justice announced. Of course, —- —–, which is forever bullish metals, claims they moved the metals in the “direction they wanted from 2008 to 2014.” It just seems that people claim it is always manipulation when they have been wrong. They only look at gold in dollars as you have said it’s a global market. They would have to manipulate all the currencies as well.

This latest affair of so-called manipulating trades during the day proves what you have been saying. They have always been gunning for stops during the day, but they cannot manipulate the trend between a bull or bear market. Do you think people will ever understand this is a global economy?

HD

ANSWER: I know. Unless people have actually been a trader, they will never understand the market. They will blame people like this to pretend they were not wrong. The problem is that this nonsense of manipulation is driving a stake through the heart of the market. Trading is like a poker game. Do you reveal your hand before everyone starts to bet? Sometimes you bluff, but the point is if you are bluffing, you have to stand behind your bet.

The mere fact that someone is blaming this type of “manipulation” for being the reason they have been wrong demonstrates that they know nothing about investing no less trading. The DOJ is now big on calling placing large “spoof” orders as manipulation. That is absurd and it is no more than bluffing in a poker game. This is the way all the markets have always functioned. Everyone would know where the stops were anyway. Sometimes they traded ahead of them using the stops as your risk point to exit the trade, and other times they would sell or buy to push the market through the stops when it was obvious that was even possible.

When I was trading in precious metals back in the ’90s, the biggest “local” dealer on the floor was Oni Morrison. He would do “spoof” orders all the time which I called “flash” bids or offers. The difference was he was good for it if hit. I was long one time in gold and I wanted out for the computer projected a crash was coming. But if you offer a thousand lots and the market was heading lower, everyone will read that and jump in front of you. That is how the Hunts went bankrupt. The Hunts did not know how to trade. Just as in poker, you cannot show your hand and expect to trade.

Oni would do “flash” bids or offers. I told my broker not to offer anything. I told him just to watch Oni and as soon as he would do a 1,000 flash to buy – say done! Sure enough, Oni was trying to push the market back up and he did one of his famous flash bids for 1,000 lots. My broker, Emerald Trading, instantly said “DONE!” Oni did it again, and they said “DONE!” Again he did a fash for 1,000 and again they said “DONE!” That was it. Oni was full and everyone began selling as the metals tumbled.

That is the way you have to trade SIZE. This is the very foundation of trading all markets for everything is just a poker game. To now call a “spoof” trade manipulation is just wrong. It is totally different when you do not have the backing. Now that would be a fraud and trying to manipulate the market for that moment – not changing the overall trend. But when you have the backing to honor your “spoof” it is just a “flash” bid or offer that you must stand behind when hit. That is just trading.

It is total BS to pretend that these guys manipulated the entire market. That is just absurd. Not even the central bank can manipulate the economy. You cannot “manipulate” a market against the trend for everything is connected. That caused the Panic of 1893 when the Silver Democrats overpriced silver. The Europeans hit the arbitrage and dumped silver in the US and took the gold back to Europe. That led J.P. Morgan to have to arrange a $100 million gold loan to bail out the treasury. That alone proved that you CANNOT manipulate ANY market against its trend for it will be arbitraged internationally – plain & simple.

Gold trading around the world in different exchanges is arbitraged. You cannot have gold $20 high in one market v another. It will be arbitraged instantly. Those who claim this as “proof” that the metals have been manipulated so that is why they have not rallied and why they have been wrong are fools who have been separated from the money. They will never understand the markets no less be able to see beyond the end of their nose. It will be instantly arbitraged.

The collapse of the Soloman Brothers was precisely that. They were putting in bids at the Treasury Auction using other people’s names to goose the market. They got caught and the firm was taken down. I know PhiBro from the ’70s and ’80s. They took over Solomon Brothers and brought that style of trading from the commodity pits to Wall Street.

This excuse by goldbugs that the metals were actually “manipulated” in their long-term trend, shows their hopeless ignorance of the markets and how they even trade. There is NOBODY who could possibly do such a thing for everything connected. As soon as the dollar would rise, the metals in terms of foreign currency would be so overvalued they would all sell and they will end up broke the same as the Silver Democrats bankrupted the country by overvaluing silver.

Trading internationally, with clients in all currencies, we have to look at each market in terms of their currency for that will determine if they made a profit or loss. Anyone who claims the metals have been manipulated and that is why they have not rallied is obviously oblivious to the world around them.

Gold does NOT rise with inflation – that is the sales pitch of a used car salesman. Gold rises in times of UNCERTAINTY with respect to the government. In times of war, it rises because it is NEUTRAL and you are not betting on who will win.

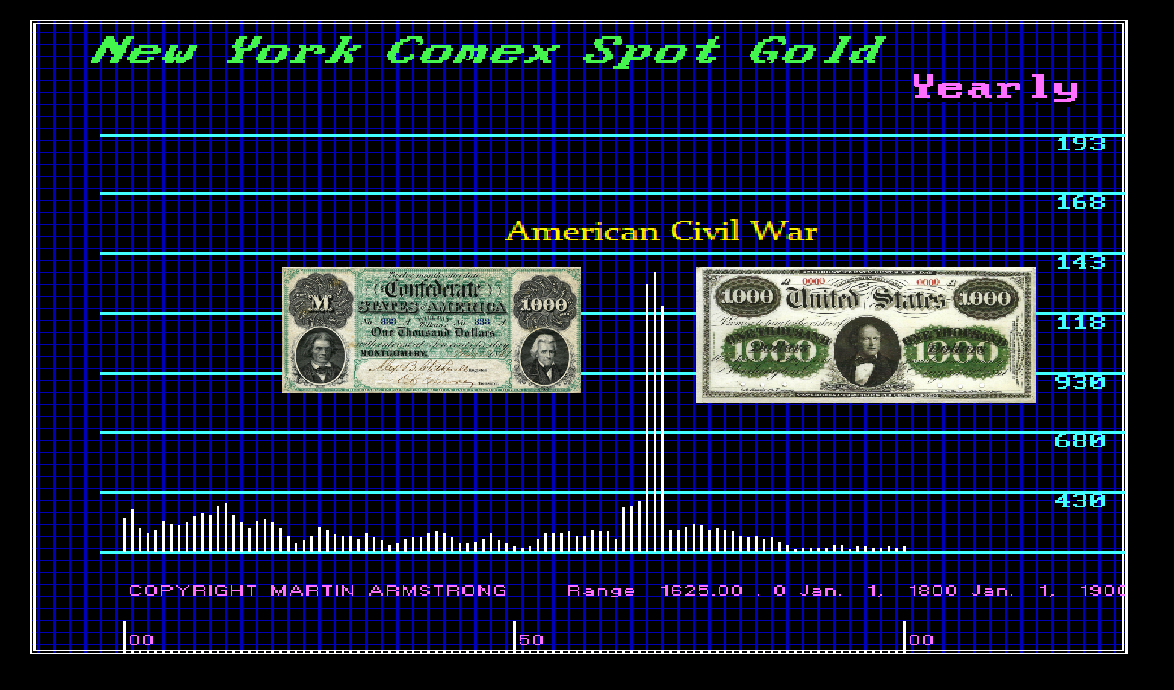

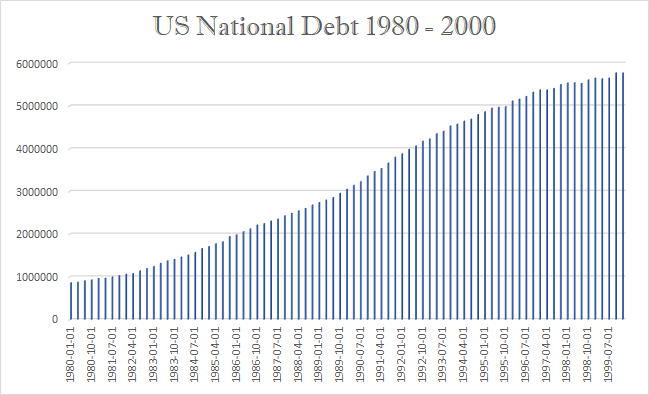

All we hear is that the debt is rising and therefore gold will explode. Once again, they offer no proof of their sophistry because there is no such proof. Gold declined for 19 years while the national debt climbed endlessly.

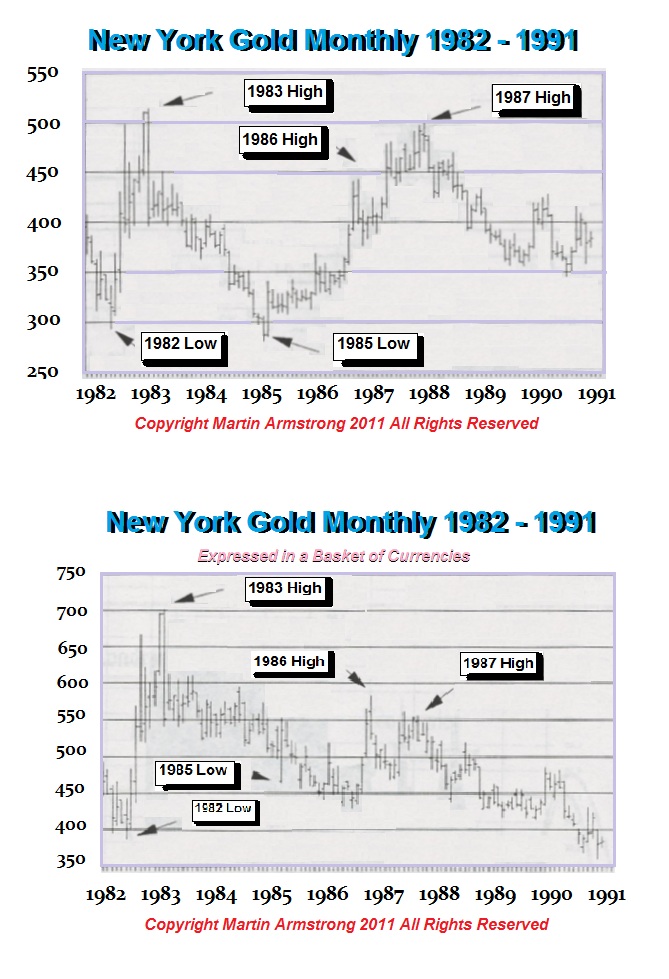

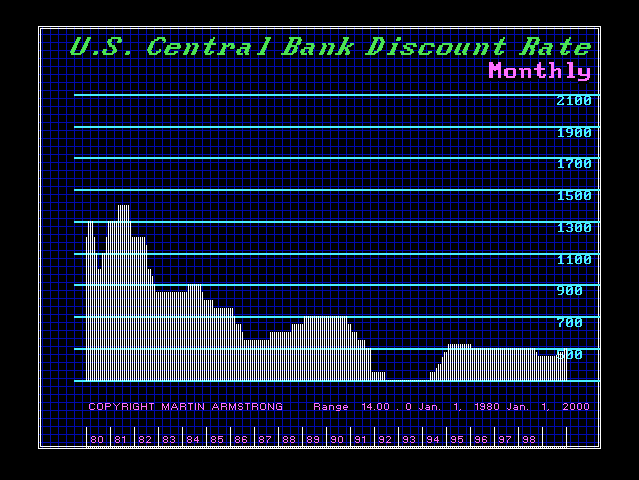

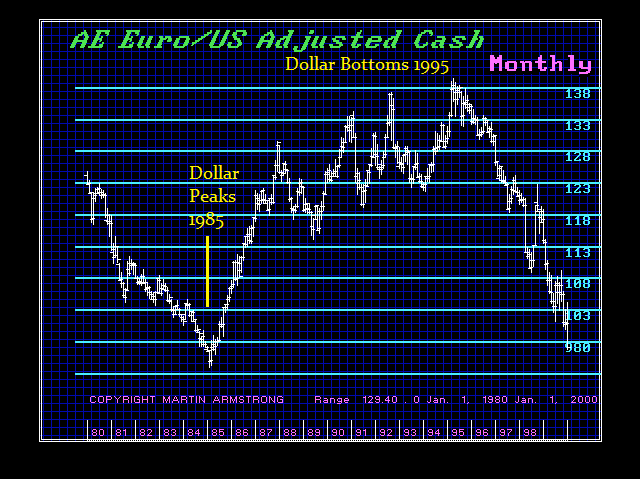

Then there is the myth about interest rates and gold that higher rates are bearish and lower rates are bullish. Well, interest rates peaked in 1981 and declined in 1994 before they began to rise marginally into 1995. Yet then contrast that myth with the performance of the dollar. There the greenback rose to a record high in 1985 but then declined for 10 years into 1995 all the while gold declined into 1999.

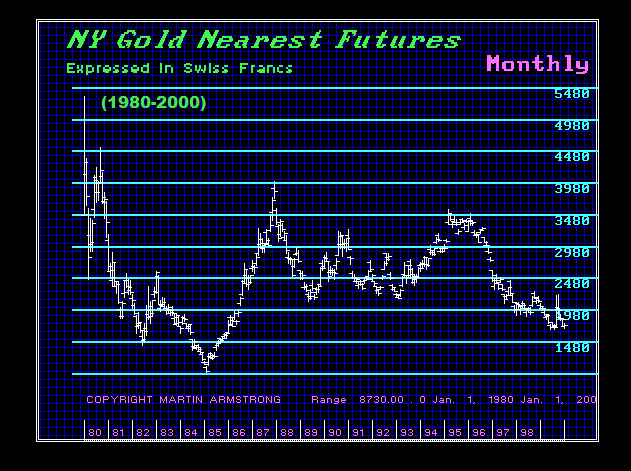

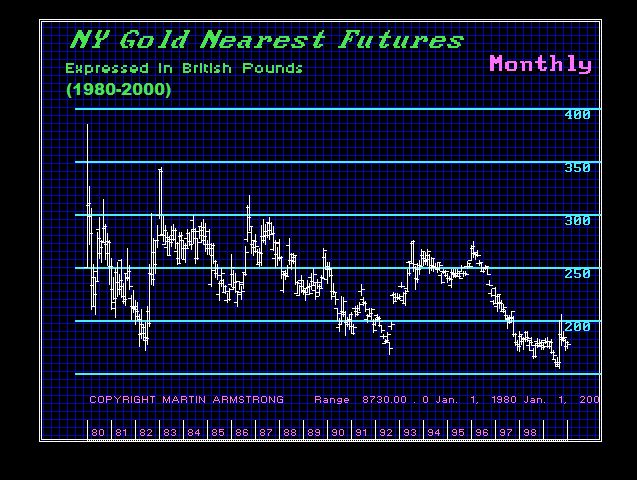

OK, so now let’s look at gold between 1980 and 200 in terms of Swiss francs and British pounds. We can instantly see that gold bottomed in 1985 in terms of the Swiss franc. In terms of British pounds, gold did not bottom until 1999.

People come up with theories all the time. However, they always try to reduce everything to a single cause and effect. They are doing that with climate change. They are telling the world it is CO2 that has changed the climate without ever addressing anything else.

The world we live in is not only complex, but it is also so dynamic it appears that no human can correctly forecast the future with an “I think” scenario. Sometimes they will be right, and others they will be wrong. Typically, they fail because they try to reduce the world to a single cause and effect.

Gold Rises with UNCERTAINTY with respect to the question of will the government survive its own madness.

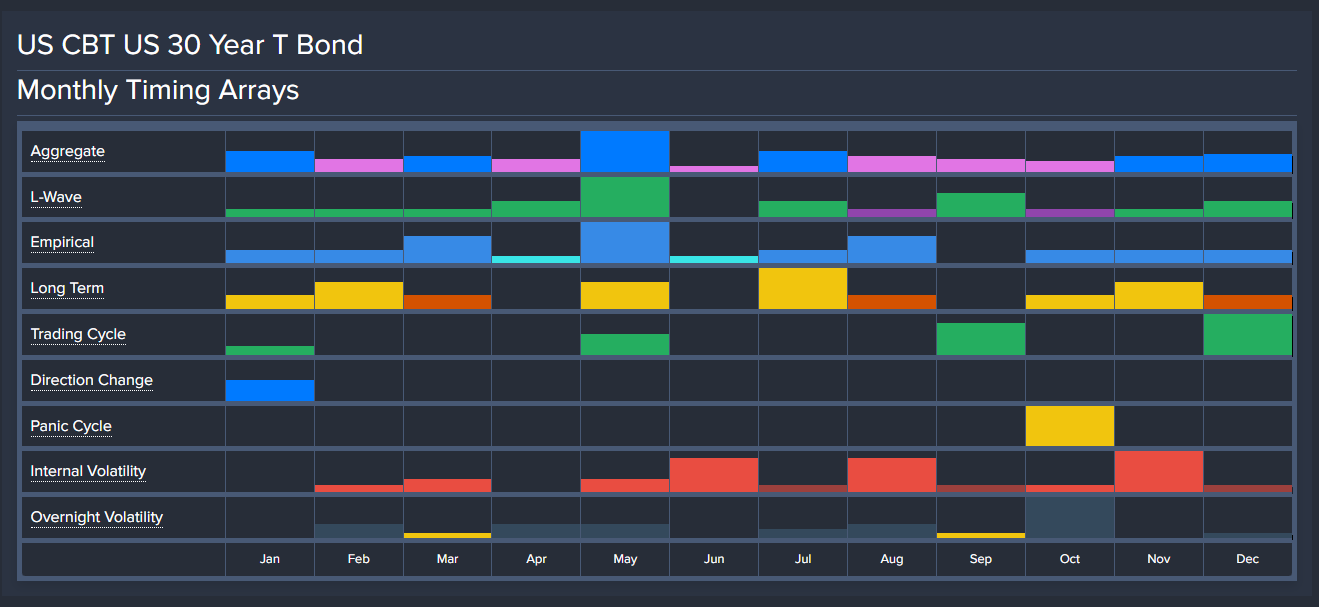

The Biden Administration is responding to the panic phone calls that their Marxist philosophy will bring down the entire financial system. My ear is red as can be. I have had enough of the phone calls today to last the balance of the month. Trying just to do the right thing! Three banks have effectively gone down in the week of March 6th, which our computer was targeting. There have been Silicon Vally Bank, Signature Bank, and Silvergat Bank.

The Regulators perhaps saw the handwriting on the wall. This NO BAILOUT claiming that no taxpayer money will be used for a bailout of their hated rich, how about just using the taxpayer’s money you are throwing down the train in Ukraine? Depositors in Signature and SVB they are now saying would be made whole. If they do not cover ALL deposits, the monumental banking failure will be catastrophic.

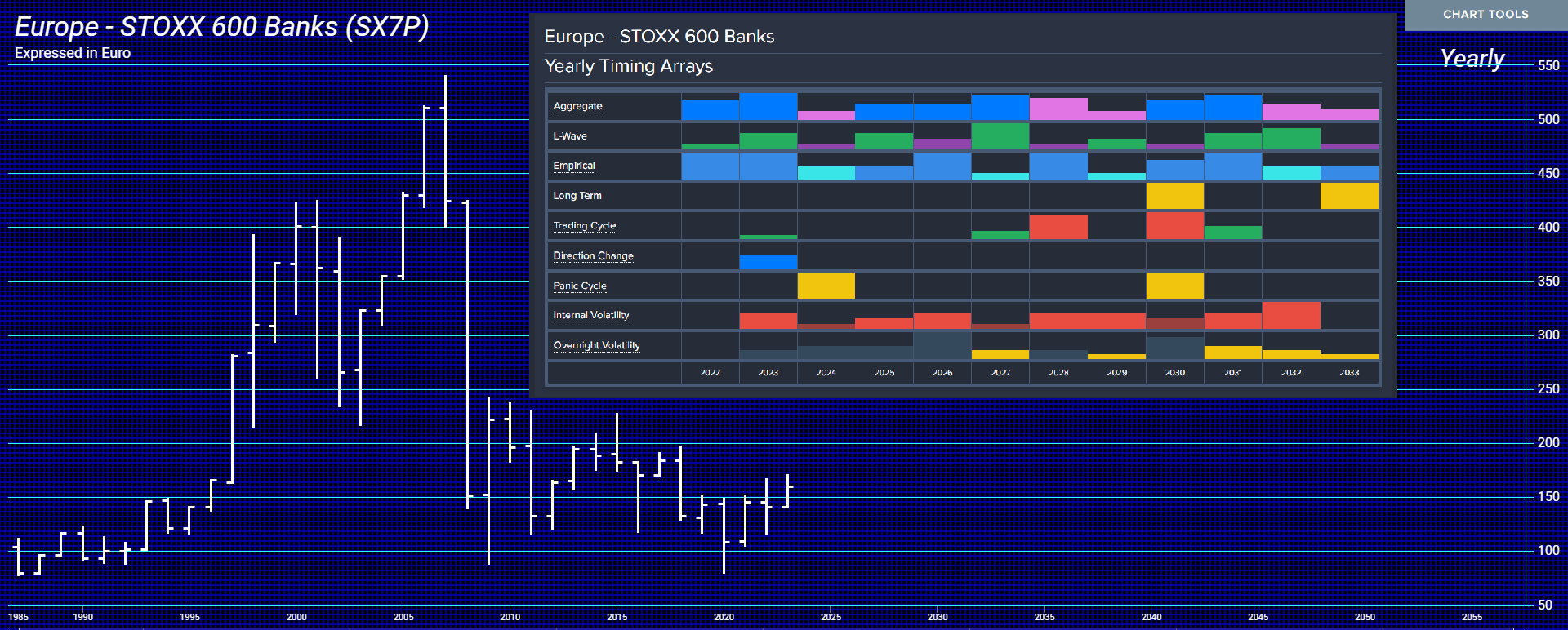

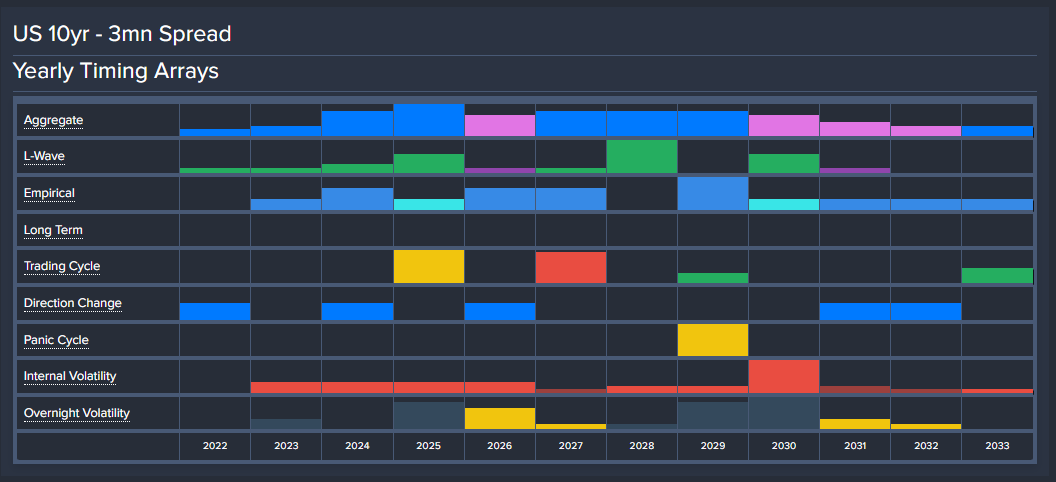

Our forecast for a Banking Crisis is by NO MEANS confined to the United States. It will be far worse in Europe. We can see our computer not only targeted 2023 for a key turning point with a Directional Change but a Panic Cycle next year in bank stocks, but interest rates will be rising higher as also the risk of banks and governments escalated especially when they insist on waging war against Russia.

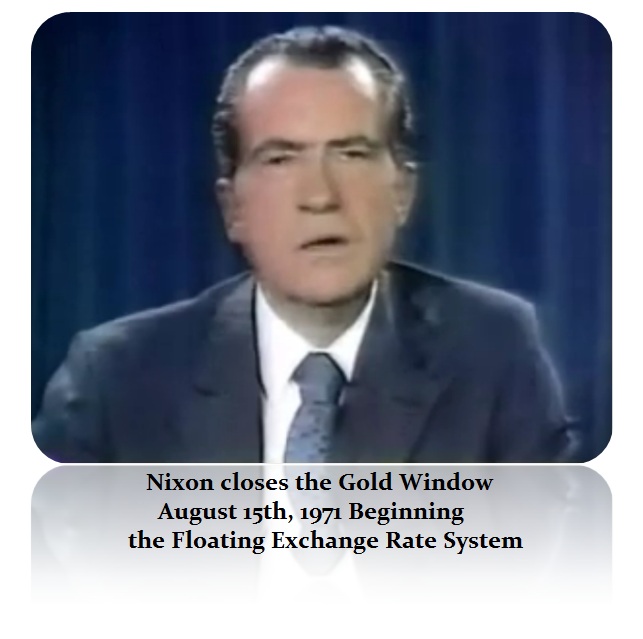

The yield curve is critical and we must understand that this insane war against Russia, even economically, will be a major financial disaster not much different from Vietnam which brought down Bretton Woods and forced Nixon to close the gold window on August 15th, 1971. It was that unrestrained spending directed by the Neocons. Then too, it was all about Russia they assumed was behind Vietnam.

Once more, the reckless spending on war promoted by the Neocons is undermining the entire economy. They have lost every war they have promoted – Vietnam, Afghanistan, Iraq, proposed Syria, Libya regime change, and now Ukraine. These people are never held accountable for all the devastation and the lives lost.

War is the primary driver of inflation and the central banks will not even address it for they do not want to “criticize” the Neocons. They might wake up with their dog’s head in the bed as in the Godfather. The central banks will NOT be able to contain this inflation or ever reach their 2% target regardless if the economy turns down just as what happened during Vietnam.

This is a warning to all small banks. Understand the REAL trend or you will NOT survive. Major capital is fleeing the long-term and rising into the short-term because they see rates are rising and any long-term bond investment during a period of war is going to be a major losing trade. Do not get trapped by the yield curve and understand that this trend is in play into 2025.

This Banking Crisis has been caused by Governments who artificially kept interest rates too low since 2008 and in the process, this banking crisis is unfolding because too many banks are UNSOPHISTICATED in forecasting and have been listening to the talking heads on TV and the desperate hope that inflation will decline while ignoring Ukraine entirely. Get that wrong – and you will NOT survive.

I strongly urge small banks to take our business services for access to real forecasting that is not biased or tarnished by human opinion with the two most dangerous words in forecasting:

Posted originally on the CTH on March 10, 2023 | Sundance

SVB is Silicon Valley Bank, the almost exclusive banking network for Venture Capitalists (VC), tech sector start-ups and tech industry holding accounts. 48 hours ago, SVB was a “grade A” Moodys rating. As of tonight, they are insolvent.

“All told, customers withdrew a staggering $42 billion of deposits by the end of Thursday, according to a California regulatory filing. […] “The precipitous deposit withdrawal has caused the Bank to be incapable of paying its obligations as they come due,” the California financial regulator stated. “The bank is now insolvent.” (link)

Now, as ridiculous as this sounds outside Silicon Valley, the powers that be are concerned about a ‘contagion‘ effect, and openly discussing the need for a taxpayer funded bailout. Blood-boiling doesn’t even begin to describe the sensation.

Let the Silicon Valley companies who started with the funds from the bank sell some of their capitalization on the market and finance the bailout themselves. After all, this is one interconnected system of lenders, borrowers and investors. This is not a crisis for the guy making their catered lunches, mowing their lawns, or washing their clothes.

♦The system. A tech guy/gal has an idea or product. Venture Capitalists (VC) organize the funding for the idea/product and go to SVB for money to start the company. The bank funds the startup and takes an equity position in the company. The VC brokers the deal, takes payment and also takes an equity position. The company launches and if successful builds a multi-billion enterprise. If they IPO (most do) then shares of the company are sold and the value of the company rises with the increased stock purchasing.

The shares of the company are capital. The shares can be sold to create funds that can support SVB. If SVB needs funds, let the networked companies sell some of their capital and fund the bank that generated their venture. They do not need outside ‘bailouts’. That’s just the way I look at it.

Listening to some voices saying the guy who mows the lawn of the tech company executive has a responsibility to ‘bailout’ the bank that created the wealth for the tech company executive, is just, well, another absurd example of how corrupt this entire financial system has become. Sorry, but this beyond annoys me.

CALIFORNIA – Regulators shuttered SVB Friday and seized its deposits in the largest U.S. banking failure since the 2008 financial crisis and the second-largest ever. The company’s downward spiral began late Wednesday, when it surprised investors with news that it needed to raise $2.25 billion to shore up its balance sheet. What followed was the rapid collapse of a highly-respected bank that had grown alongside its technology clients.

Even now, as the dust begins to settle on the second bank wind-down announced this week, members of the VC community are lamenting the role that other investors played in SVB’s demise.

“This was a hysteria-induced bank run caused by VCs,” Ryan Falvey, a fintech investor at Restive Ventures, told CNBC. “This is going to go down as one of the ultimate cases of an industry cutting its nose off to spite its face.”

The episode is the latest fallout from the Federal Reserve’s actions to stem inflation with its most aggressive rate hiking campaign in four decades. The ramifications could be far-reaching, with concerns that startups may be unable to pay employees in coming days, venture investors may struggle to raise funds, and an already-battered sector could face a deeper malaise.

The roots of SVB’s collapse stem from dislocations spurred by higher rates. As startup clients withdrew deposits to keep their companies afloat in a chilly environment for IPOs and private fundraising, SVB found itself short on capital. It had been forced to sell all of its available-for-sale bonds at a $1.8 billion loss, the bank said late Wednesday.

The sudden need for fresh capital, coming on the heels of the collapse of crypto-focused Silvergate bank, sparked another wave of deposit withdrawals Thursday as VCs instructed their portfolio companies to move funds, according to people with knowledge of the matter. The concern: a bank run at SVB could pose an existential threat to startups who couldn’t tap their deposits. (read more)

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America