Armstrong Economics Blog/Economics Re-Posted Jul 28, 2023 by Martin Armstrong

QUESTION: Looking at Socrates, do you think that these people who were constantly calling for a recession because there were two quarters that declined with covid really need revision? Socrates was correct, no recession. But it is showing major turning points in 2024 which seem to align with your old ECM forecast calling for commodity inflation into 2024. How would you define a recession?

EJ

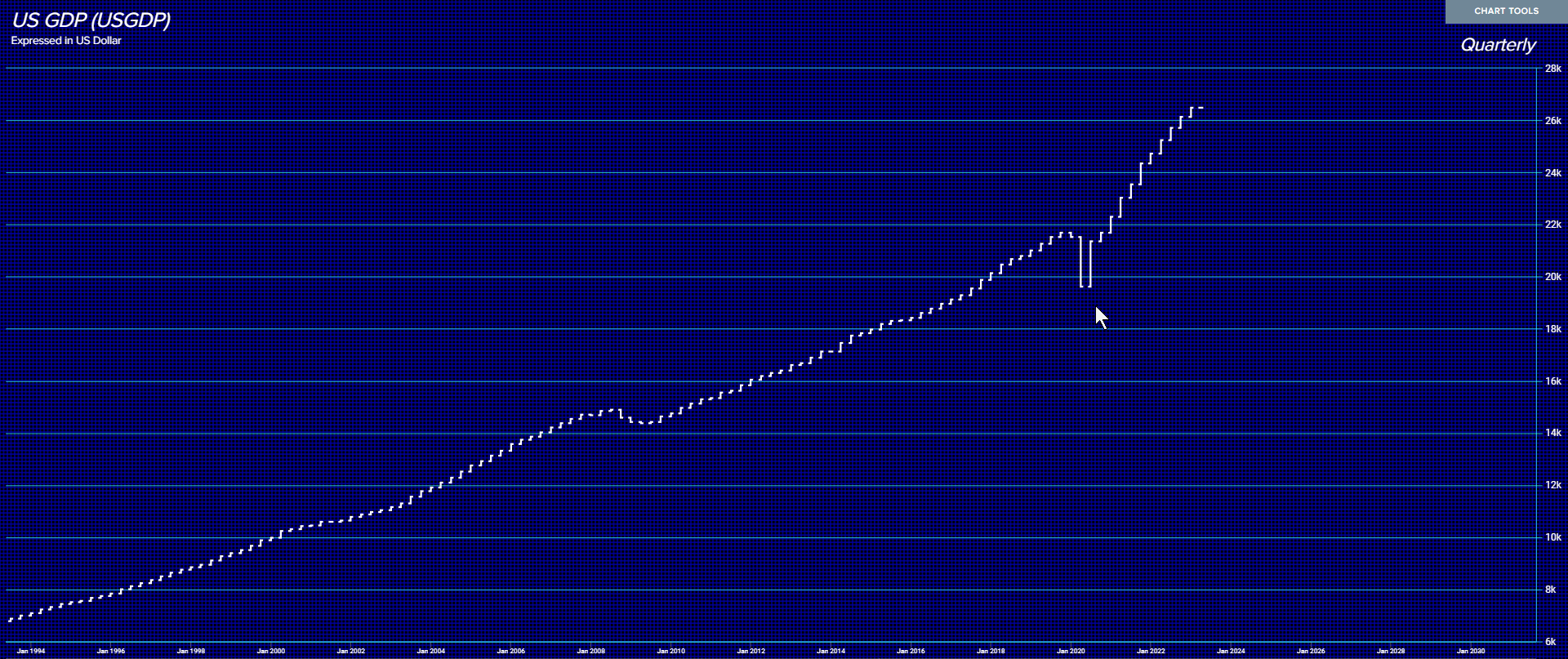

ANSWER: In trading, reactions are 1 to 3 time units. I believe that the same definition should be used for classifying a recession. They define a recession as two consecutive quarterly declines. If you look at the “Great Recession” of 2008-2009, you will see three consecutive quarterly declines and a rebound. If we look at the COVID recession caused by locking everyone down, that was just two consecutive quarterly declines.

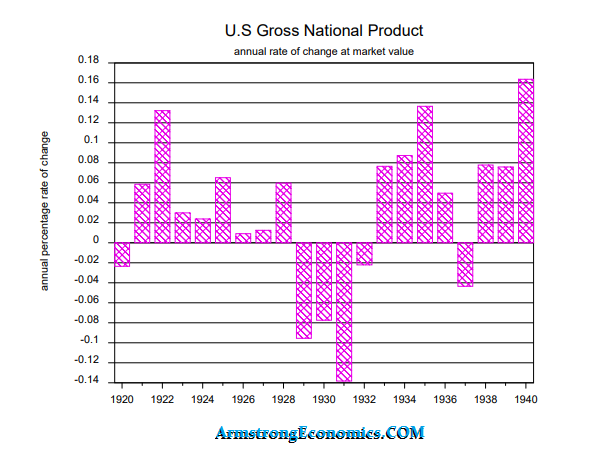

I personally would argue that a true economic recession MUST exceed three consecutive declines. Here is the chart of GNP from 1929 to 1940. There were three years of negative growth. I simply think that this definition of two quarters is wrong. You can have a slight decline of 1 to even 5%, but that does not suggest a recession. In the case of 1929, that was a decline of 9.5% in 1930 – the first year. Now look at the COVID Crash, which was also a decline of 9.53%. But the difference is that the COVID decline was forced and not natural. That is why it rebounded so quickly. Now the so-called “Great Recession” of 2008-2009 only saw a decline in GDP of 3.47%.

The “Great Recession” was not really so great. It wiped out real estate and bankers but did not fundamentally alter the economy. So who is right and who is wrong will always depend upon the definition. Yes, the AI Timing Arrays point to a recession starting Next Year by their definition. This will most likely be caused by the decline in confidence that will lead to UNCERTAINTY, and as such, the consumer will contract. Up to now, the continued expansion of the economy into 2024 has also been fueled by the shift in assets from public to private.

{kind=link}