Honest journalism has become a crime. I have appeared numerous times on Maria Zaric’s program, Zeee Media. Maria is a professional journalist who asks thought-provoking questions to the experts that appear on her show. Her content goes against the grain and traditional narrative. The Australian-based journalist has been questioning COVID, the Great Reset, governments, globalists, the war in Ukraine, and many other topics that are completely taboo in the mainstream media. They attempted to shut down her channel in the past. Now, she has been de-banked with no explanation.

“Do you shut down peoples accounts due to their political views by any chance?” Maria asked the bank representative, only to be met with silence. Maria had been banking with ING Bank for numerous years without issues. Her account was suddenly shut down shortly after releasing a story on domestic terrorism in Australia. ING Bank has been unable to explain why her account was canceled.

Interestingly, ING is a partner of the World Economic Forum. Maria has extensively covered the WEF’s agenda to “enslave humanity.” Is Australia secretly keeping track of journalists’ “social credit scores” to silence skepticism?

The idea of eliminating someone’s ability to bank is essentially eliminating them from society. We saw Canadado the same thing to those protesting the Trucker Convoy. Trudeau took things a step further by also de-banking people who simply donated to the cause. The Canadian government used the premise of money laundering as a way to coerce the banks into reporting any activity that could have been intended to help the protestors. I know of numerous people who were frantically attempting to remove their funds from the bank during this time.

As if the public needed more reasons to lose trust in the banking system. This is not limited to one bank or country. I discussed how banks have the ability to “cancel” someone after JPMorgan Chase de-banked the rapper Kanye West for antisemitic remarks. The bank acts as the jury and judge. Epstein was permitted to hold funds at JPMorgan Chase despite an ongoing pedophile ring trial. Bernie Madoff banked with JPMorgan Chase. The bank has secret ties to the Third Reich and helped the group funnel money through South America during World War II. Again, the bank acts as the jury and judge; anyone can be de-banked anytime for any reason.

Most countries may not openly have social credit scores, but they’re keeping tabs on us. They are keenly aware that resistance to this New World Order is building. So they are now using professional journalists as examples hoping that people will stop asking questions to learn the truth. That is one of the reasons why this blog is free of charge – you deserve to know the truth.

QUESTION: Marty there are a lot of people who seem to be trying to create a panic. Some are claiming the stock market will plunge by 50%. Others are saying nothing will survive other than gold. It seems like none of these people have any sense of what is really unfolding. They were saying the same thing for different reasons before the banking crisis. Can you offer any historical perspective?

Thank you. You seem to be the only real source these days.

Pete

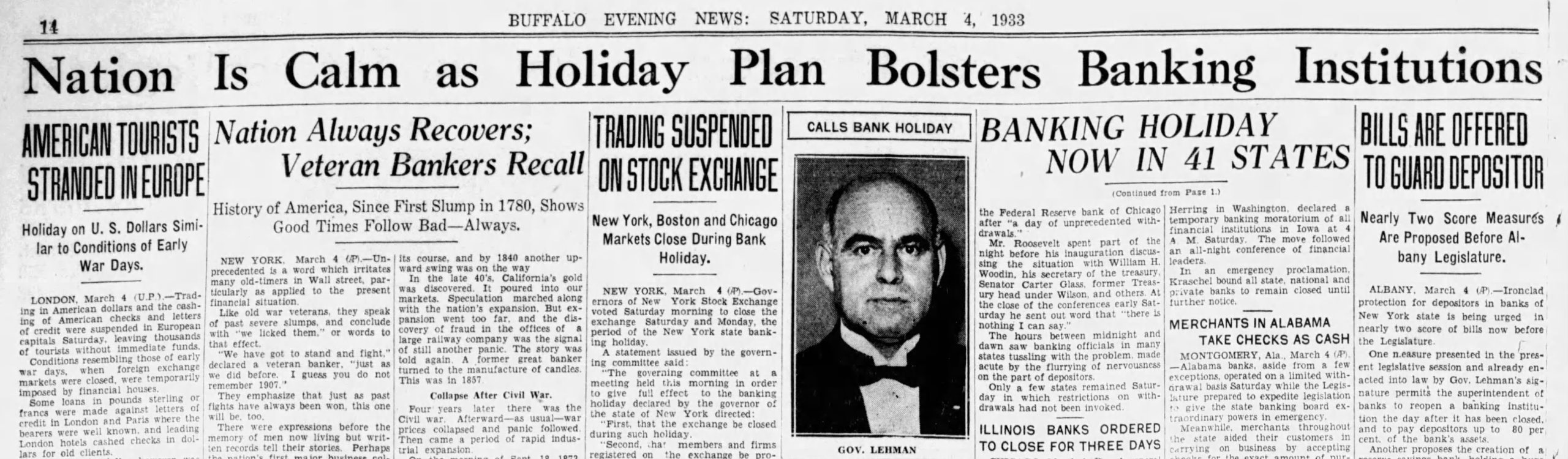

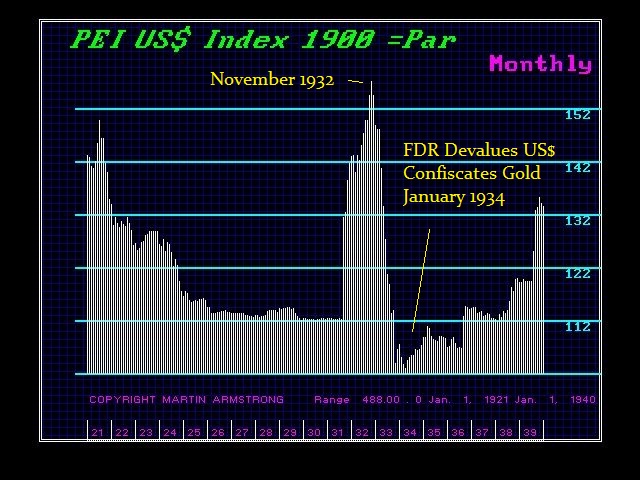

ANSWER: The Bank Holiday took place the first week of March 1933. It began with governors closing down the banks in their states. Once one began, like COVID rules, they quickly jumped on the bandwagon. As reported by March 4th, 1933, some 41 states had already declared a banking holiday. Back then, the president took office in March – not January. Thus, Roosevelt was sworn in on March 4th, 1933. As the new president, FDR delivered what is arguably his best-known speech.

“So, first of all, let me assert my firm belief that the only thing we have to fear is…fear itself — nameless, unreasoning, unjustified terror which paralyzes needed efforts to convert retreat into advance. In every dark hour of our national life a leadership of frankness and of vigor has met with that understanding and support of the people themselves which is essential to victory. And I am convinced that you will again give that support to leadership in these critical days.”

The following day, Roosevelt declared a national banking holiday on March 5th, 1933. Then Congress responded by passing the Emergency Banking Actof 1933 on March 9th, 1933. This action was combined with the Federal Reserve’s commitment to supply unlimited amounts of currency to reopened banks. Back then, they effectively created a de facto 100% deposit insurance and this was before the FDIC was created.

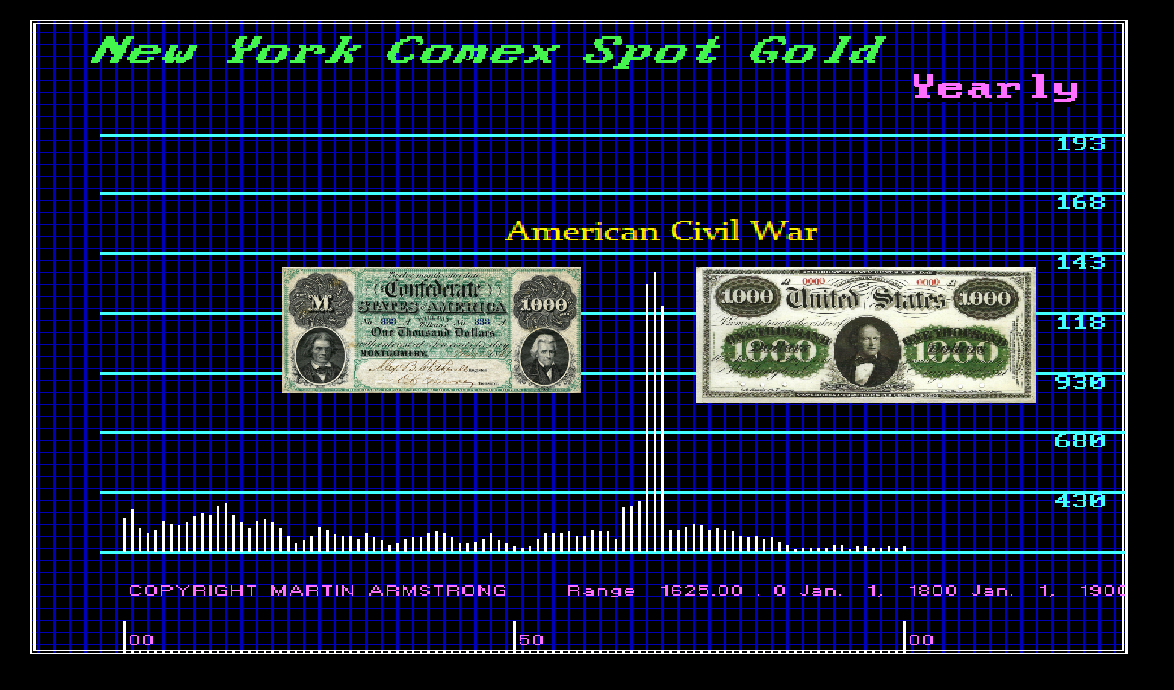

However, what the history books have omitted because it revealed the real reason for the major banking crisis, was the confiscation of gold precisely as Germany did in December 1922 seizing 10% of all assets which unleashed hyperinflation in 1923.

In Herbert Hoover’s memoirs (1951), he documents the fact that Franklin D. Roosevelt (FDR) played a very dirty game of politics. There were rumors that FDR would confiscate gold in 1932 BEFORE the election. These rumors spread and people ran to banks to withdraw their funds. The night before the election in 1932, FDR denied that he would do such a thing. After FDR won the election, the real bank panic began. FDR would not take office until March 1933.

The run on banks began as the Great Depression started. In 1929 alone, 659 banks closed their doors due to mismanagement and speculation. Ironically, to save money on paper, it was also in 1929 when the currency was reduced in size to save money. This time, they want to move to digital and save 100% on printing money. Here in 2023, the failures are due to the WOKE agenda which has deprived the banks of risk management rather than speculation.

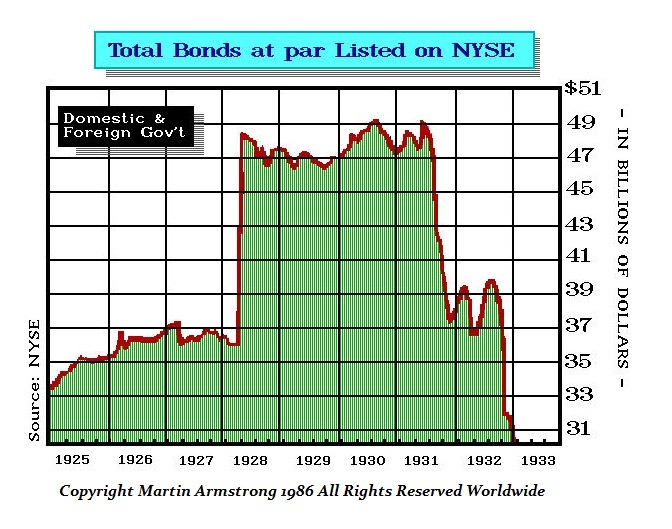

However, as the 1931 Sovereign Debt Crisis hit, the number of bank failures skyrocketed. Goldman Sacks and others were selling foreign bonds to Americans in small denominations., As Europe began to default, US banks holding foreign debt and individuals in need of cash led to a banking panic for external reasons. Here is a chart showing the listing of bonds on the NYSE. We can easily see the collapse in the bond market thanks to the 1931 Sovereign Debt Crisis.

By 1932, an additional 5,102 banks went out of business. Families lost their life savings overnight. Thirty-eight states had adopted restrictions on withdrawals in an effort to forestall the panic. By March 4th, 41 states had declared a bank holiday shutting down banks. Bank failures increased in 1933, and Franklin Roosevelt deemed remedying these failing financial institutions his first priority after being inaugurated.

However, it was actually the election of FDR that started the banking crisis post-1931. Hoover pleaded with FDR to please come out and address the gold confiscation rumors. People had been hoarding their gold coins fearing the rumored confiscation. Despite Hoover’s plea for FDR to come out and deny the rumors after the election, he remained silent. Given FDR’s manipulation of Japan and the attack on Pearl Harbor which he appeared to instigate with sanctions confiscating Japanese assets in the USA, denying the sale of any energy to Japan, and then threatening to use the fleet to block them from buying fuel from anywhere else, They Japanese attacked Pearl Harbor. There were Senate investigations afterward about FDR’s role because the US had already broken the Japanese code and knew in advance about the attack on Pearl Harbor. He did that to force the US into World War II.

It was in his character to remain silent and create the worst banking crisis in history before he was sworn in as president. FDR was a radical socialist and many viewed that he admired Lenin. If it were not for Mr. Jones exposing the truth behind Stalin, even the corrupt New York Times journalist promoting Stalinism was meeting with FDR. The run on the banks became massive when FDR won the election on November 8th, 1932. FDR allowed the banking system to implode with people rushing to withdraw the money in gold coins.

At 1:00 a.m. on Monday, March 6th, 1933, President Roosevelt issued Proclamation 2039 ordering the suspension of all banking transactions, effective immediately. Roosevelt had taken the oath of office only thirty-six hours earlier.

The terms of the presidential proclamation specified:

[N]o such banking institution or branch shall pay out, export, earmark, or permit the withdrawal or transfer in any manner or by any device whatsoever, of any gold or silver coin or bullion or currency or take any other action which might facilitate the hoarding thereof; nor shall any such banking institution or branch pay out deposits, make loans or discounts, deal in foreign exchange, transfer credits from the United States to any place abroad, or transact any other banking business whatsoever.

For an entire week, Americans would not have access to banks or banking services. They could not withdraw or transfer their money, nor could they make deposits. The entire economy ran simply on cash in your pocket.

While the first phase of the banking crisis unfolded after 1929 due to speculation losses (hence Glass–Steagall Act), then the second phase was the 1931 Sovereign Debt Crisis, it was the third phase with the election of FDR that led to thousands of banks failing as there was a mad rush to withdraw your gold coin. But a new round of problems that began in early 1933 placed a severe strain on New York banks, many of which held balances for banks in other parts of the country. About 4,000 banks failed during this period alone bringing the total to over 9,000.

Much to everyone’s relief, when the institutions that could reopen for business on March 13th, 1933 saw depositors standing in line to return their stashed cash to neighborhood banks. Within two weeks, Americans had redeposited more than half of the currency that they had withdrawn post-FDR’s election on November 8th, 1932. This would prove to be a sneaky trick of FDR to get people to redeposit all the gold coins they had withdrawn – as we are about to explore.

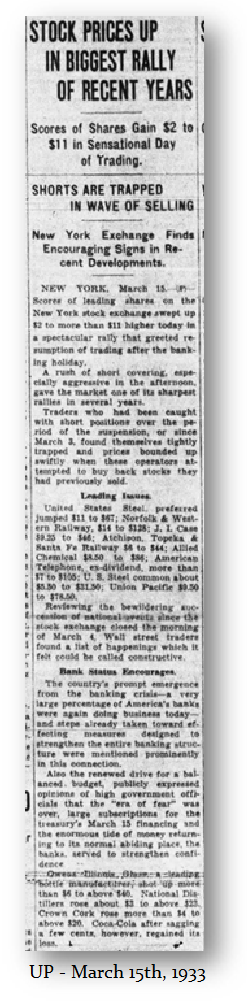

The stock market was also ordered closed when FDR came to power. With the cleverness of a real con artist operating a Ponzi Scheme to gain the confidence of the people, FDR needed the gold coin to be deposited for Phase 4 of the banking crisis. On March 15th, 1933, (The Ides of March), the stock market was allowed to reopen. On the first day of trading, the New York Stock Exchange recorded the largest one-day percentage price increase ever.

The week before the closure, the Dow Jones Industrials fell to 49.68. The week following the closure, the Dow rallied to 64.56 – a percentage gain of virtually 30% over the banking holiday. The shorts who were better on the collapse of the market once it reopened were devastated. It was a major short-covering rally.

With the benefit of hindsight, the nationwide Bank Holiday and the Emergency Banking Act of March 1933, ended the bank runs that had plagued the Great Depression, but it also set the stage for the confiscation of gold. What you have to understand is that Franklin Delano Roosevelt’s (FDR) actions in 1933 were not directed simply at gold. He was embarking on what he called the New Deal, which was a Marxist Agenda that was very popular at the time. His New Deal would end austerity, whereby they were maintaining a balanced budget in the belief that they needed to inspire confidence in the currency.

It was this balanced budget philosophy that also inspired John Maynard Keynes who argued that in times of economic distress when the demand has collapsed, that is when the state needs to run a deficit and increase the money supply. There was a simultaneous international flight of capital from Europe to the United States in the face of European sovereign debt defaults. That capital flight lasted for nearly two years until FDR won the election in 1932. There was much concern that Roosevelt would do what Germany did in 1922 in confiscating assets. That was the rumor about the possible confiscation of gold.

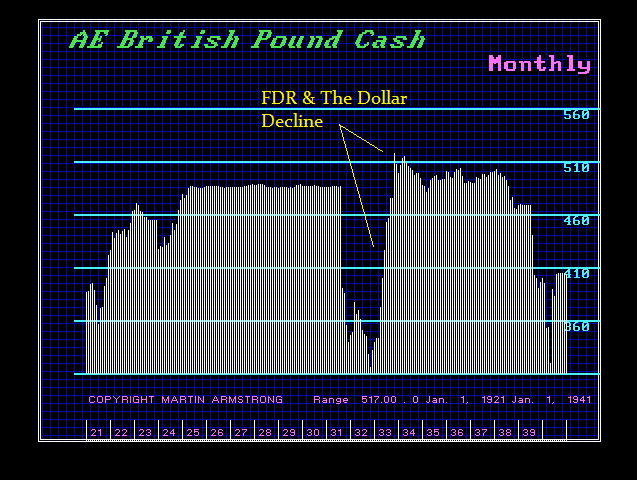

Milton Friedman criticized the Fed because the capital flows poured into the US but they refused to monetize it. We can see that as Europe defaulted on its debts in 1931, the capital rushed head-first into the dollar. Then we see that the dollar peaked in November 1932 with the election of FDR fearing that would weaken the dollar and exploit the economy. All this gold came to the USA pushing the dollar higher, but the Fed refused to monetize it, was Milton’s criticism. The backing of gold behind the dollar doubled in supply between 1929 and 1931.

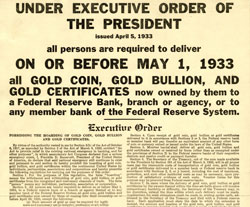

So, you must separate gold and the devaluation of the dollar to comprehend what the issue was all about. FDR could have simply abandoned the gold standard, as did Britain, and not confiscated gold. However, that would have also been sufficient to end austerity. But the bankers would have profited and sold the gold overseas at higher prices. Roosevelt in his confiscation of gold was intended to deprive the private sector of profiting from his devaluation of the dollar which was rising the price of gold from $20 to $35. You must keep in mind that he even degraded Pierre du Pont (1870-1954) and called him the “Merchant of Death” because he produced arms for World War I and made a profit off of that war demand. Many saw Roosevelt as a traitor to his own class.

The confiscation of the gold was for two reasons. First, FDR was changing the monetary system from one where there was no distinction domestically from internationally to a two-tier system. Gold would freely circulate without restriction only internationally. Therefore, the confiscation of gold was altering the monetary system moving to a two-tier monetary system with gold only used in international transactions.

Consequently, FDR confiscated gold to move to a two-tier system and to deprive Americans of any profit from his devaluation. What FDR then did was confiscate gold from all institutions ordering them to turn over whatever they had. Ironically, this move was intended to target bankers rather than the public. FDR did not have people knocking on every door demanding all their gold. That is why there are plenty of US gold coins that have survived. If individuals possessed them rather than an institution, then they kept what they owned

Therefore, Roosevelt was able to seize whatever gold existed in banks. He declared all contracts void that had gold provisions for payment. It was in Perry v. United States – 294 U.S. 330 (1935) that the US Supreme Court ruled that Congress, by virtue of its power to deal with gold coin as a medium of exchange, was authorized to prohibit its export and limit its use in foreign exchange. Hence, the restraint thus imposed upon holders of gold coins was incidental to their ownership of it, and gave them no cause of action. id/P. 294 U. S. 356.

The Supreme Court held that it could not say that the exercise of this power by Congress was arbitrary or capricious. id/P. 294 U. S. 356. They held that even if the Government’s repudiation of the gold clause in the government bonds was unconstitutional, it did not entitle the plaintiff to recover more than the loss he has actually suffered, and of which he may rightfully complain. id/P. 294 U. S. 354. Therefore, the Joint Resolution of June 5, 1933, held:

“insofar as it undertakes to nullify such gold clauses in obligations of the United States and provides that such obligations shall be discharged by payment, dollar for dollar, in any coin or currency which at the time of payment is legal tender for public and private debts, is unconstitutional.” id/P. 294 U. S. 349.

Yet, swapping gold for dollars created no loss that was cognizable even though the taking of gold was unconstitutional. Clearly, the Supreme Court did not consider the loss in terms of foreign exchange. The Court reasoned:

“Plaintiff has not attempted to show that, in relation to buying power, he has sustained any loss; on the contrary, in view of the adjustment of the internal economy to the single measure of value as established by the legislation of the Congress, and the universal availability and use throughout the country of the legal tender currency in meeting all engagements, the payment to the plaintiff of the amount which he demands would appear to constitute not a recoupment of loss in any proper sense, but an unjustified enrichment.”

In my understanding of the law, those who argued before the Court made purely a domestic argument. A dollar was still a dollar in domestic terms so there was no cognizable loss and the Court did not reach the constitutional question. Had they argued that their loss was with respect to some debt owed in British pounds, they there was a loss. Purely domestically, the only loss would have been to inflation and the Court would never rule against the government on such an issue.

All of that said, there does not appear to be any historical precedent for the stock market to collapse by 50%, all tangible assets to turn to dust, and only gold will survive given a banking crisis where Biden and Yellen sit on each other’s hands and do nothing. Trust me. Every major Democratic donor will be screaming. And as for those claiming the Fed will reverse its position, say inflation is suddenly no longer a problem, and monetize everything in sight, this is even too big for the Fed. have to create QE and absorb all the debt, there to things have changed. If the Fed does that, it will also lose all credibility. It squarely understands that inflation comes from handing Ukraine a black check to the most corrupt government in the world. The Fed raised rates yesterday for it cannot back down. It is choreographing the best it can but the bankers do not listen.

If they simply stand behind all the deposits, then there will be no panic. That is what they did in 1933 and the market rallied in confidence thereafter.

COMMENT: Marty, it’s refreshing to have Socrates that is totally unbiased. It projected continued rising rates into next year and the Fed just proved its point. It is not backing down.

Thank you. Socrates is very enlightening.

GS

ANSWER: I know there were a lot of talks that surely the Fed had to lower rates and start QE all over again. Most of those sorts of comments have no real experience in markets. They just mouth a lot of hot air. Perhaps instead of putting masks on cows, we should do that on the shills. The Federal Reserve had no choice but to raise interest rates although it was just by a quarter point. Not to do so and the Fed would lose all credibility and the market would then not take them seriously.

You MUST understand that this crisis has unfolded because too many banks were wrapped up in WOKE culture and hired people who were UNQUALIFIED to run risk management. Some were more excited about cross-dressing as a woman and winning the Rainbow award in banking than actually protecting the bank from the risk of rising interest rates.

In a statement released at the conclusion of the meeting, Fed officials acknowledged that recent financial market turmoil is weighing on inflation and the economy, though they expressed confidence in the overall system. “The US banking system is sound and resilient.” They had no choice but to make this statement.

“Recent developments are likely to result in tighter credit conditions for households and businesses and to weigh on economic activity, hiring and inflation. The extent of these effects is uncertain.”

The Fed is saying that their rise in rates will in fact reduce inflation and economic activity. The banks have this yield curve risk and that is different from the 2007-2009 crisis where the debt was based on fraud. Here, the debt is US Treasuries so they are not going bankrupt from that aspect, but it is a liquidity crisis.

If these people who scream loudly but know nothing really about finance keep up the nonsense, they will only add to the uncertainly. This inflation is accelerating thanks to the war.

There once was a time when cash was the undisputed king. Merchants preferred cash payments over credit, and there were often incentives for paying with paper. I recall receiving lower gas prices when paying with cash, for example. It is increasingly common to see “no cash accepted” signs at establishments as the world moves toward a cashless society. At the Federal level, there are no laws protecting consumers who wish to pay in cash. The Federal Reserve stated on its website:

There is no federal statute mandating that a private business, a person, or an organization must accept currency or coins as payment for goods or services. Private businesses are free to develop their own policies on whether to accept cash unless there is a state law that says otherwise.

"Section 31 U.S.C. 5103, entitled "Legal tender," states: "United States coins and currency [including Federal Reserve notes and circulating notes of Federal Reserve Banks and national banks] are legal tender for all debts, public charges, taxes, and dues." This statute means that all U.S. money as identified above is a valid and legal offer of payment for debts when tendered to a creditor."

Yet, the Federal Reserve also recognizes that as of 2021, 4.5% of US households were “unbanked.” This means that 5.9 million households are unable to pay by card. This is the lowest unbanked rate since the Fed began keeping track in 2009. The most common reason for not having an account, reported by 21.7% of unbanked households, is that they do not meet minimum balance requirements. The second most reported reason (13.2%) is that people simply do not trust banks, while the third most cited reason (8.4%) was the desire for privacy.

If merchants refuse to accept cash, these people cannot participate in consumerism. Their legal tender is simply not accepted. Unbanked households are more likely to contain persons with lower levels of education, lower incomes, disabilities, single mothers, and minorities. As the Fed reported:

“Differences in unbanked rates between Black and White households and between Hispanic and White households in 2021 were present at every income level. For example, among households with income between $30,000 and $50,000, 8.0 percent of Black households and 8.4 percent of Hispanic households were unbanked, compared with 1.7 percent of White households.”

If cash is legal tender, then it should be accepted everywhere. Numerous merchants not only refuse cash but they charge an additional fee for using credit. Tennessee, Arizona, Delaware, District of Columbia, Idaho, Maine, Massachusetts, Michigan, Mississippi, New York, North Dakota, Oklahoma and Pennsylvania, New Jersey, Rhode, Colorado, and Connecticut have laws at the state level protecting cash payments. Some cities such as Washington D.C., Berkley, Chicago, New York City, Philadelphia, and San Francisco also have laws in place. However, I can assure you that many retailers in these areas still do not accept cash.

Washington wants to move us toward a cashless society to tax everyone, even those with the least to give, on every transaction we make.

In an interview on May 11, 2014, I explained on USAWatchdog that confidence always outweighs reality. “It’s basically what you believe. There have been all sorts of studies on fundamentals that say if interest rates go up, stocks go down. It is simply not true. The stock market has never peaked with interest rates twice in history. If you think you are going to make 25% in the market, you’ll pay 10% interest; but if you really think the market is only going to go up 10%, you won’t pay 10%. So, it’s always the difference between what you believe and reality.”

The people have lost all confidence in government. We have heard rumors of a “soft landing” from the Fed for the past year, but the situation continues to worsen. Washington maintains that everything is stable as banks continue to fail and inflation rages on. There can be no price stability when war is at play. Biden just released his latest budget plan that no reasonable person would condone. I explained in 2014 that great empires all come crashing down after piling on massive debt. People believe hyperinflation would cause such a scenario, but debt is the major player. Once the government accumulates enormous debt, it targets its citizens aggressively. That is what we are seeing today.

So where should you put your money? I said in 2014: “One of the number one questions I get all the time is where do I put my money? If the banks can just take whatever they want now, there will be bail-ins rather than bail-outs. People are afraid. What do you do with the cash? So, people are buying things like real estate and stocks, just trying to get money out of the banking system.” That sentiment is continuing and the latest CPI report even showed that shelter costs are rising at the highest rate since June 1982. Smart money has been trying to escape the banks for years. There was no incentive until very recently to park money in the banks due to artificially low rates.

I also explained that the Fed would only bail out deposits and had been asking institutions to change their models. “Everybody knows I advise some of the big institutions around, and I can tell you that they have told me directly that the Fed went to them and told them they will not be bailed out for proprietary trading. It will be only on deposits. That’s it,” I stated. “The Fed has been going around telling them, ‘hey, you better change your models.’ They don’t think it will be a flight to quality as it was before. You buy the long term (Treasuries) and that saves you. They don’t think that’s going to happen. It’s quite interesting. . . . It looks like the long term (Treasury bonds) is going to end up starting to rise.”

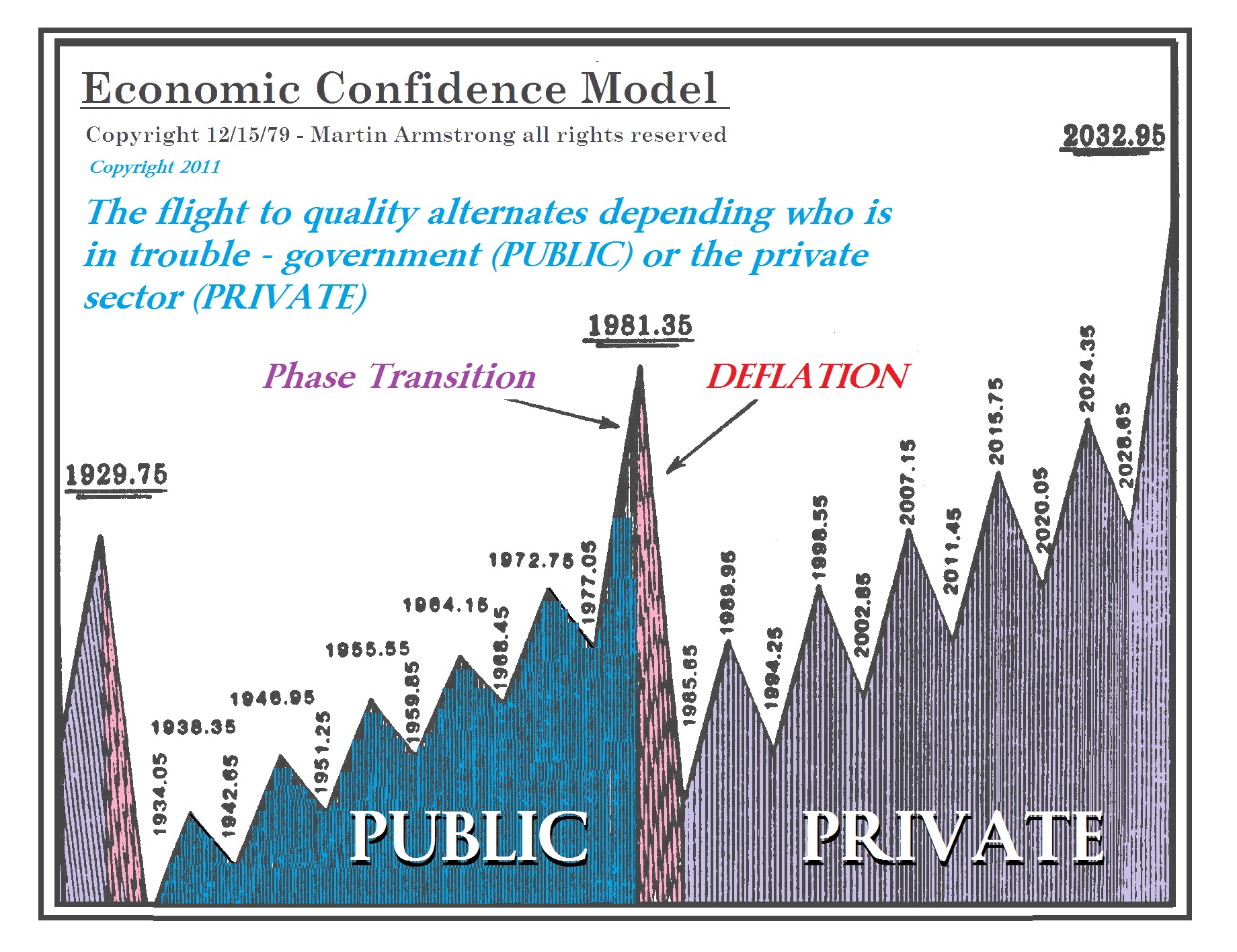

Sound familiar to the current situation? People have moved from the public sector into the private sector. We are well into a private wave, and the public will not go back to the public sector for many years to come.

The Chinese yuan has out-traded the US dollar by volume for one of the first times in recent Russian history. The dollar was king in 1991 when the Soviet Union collapsed, but that is no longer the case after Moscow branded the dollar a “toxic currency” along with the euro. Toxic currencies accounted for 87% of exports from Russia at the beginning of 2022, but this figure fell to 48% by the start of the new year. The Bank of Russia has reported that the proportion of USD/ruble pair in exchange fell to only 36% in February. The central bank is calling this a “broad structural transformation of the Russian economy.”

As “unfriendly countries” and their “toxic currencies” band together, those on the outskirts are winning. China has become the new go-to country for new trade partnerships as it bypasses Western-imposed sanctions. Toxic currencies represented 46% of imports in December 2022 but were at 65% in January 2022 before the war. In contrast, the yuan’s share rose from 4% to 23% during that time.

Those who were previously shunned from the big table are now pulling up a chair to discuss economic prospects with China. This will make it much easier to phase out toxic currencies because more people are willing to accept the yuan. The confidence in the yuan is growing. Everything occurring may seem odd, but it is precisely on target. As I mentioned in my report“China on the Rise,” China will dethrone the United States to become the world’s leading economic powerhouse by 2032. It’s just time.

Posted originally on the CTH on March 13, 2023 | Sundance

The CNN panel was jaw-agape as Kevin O’Leary appeared earlier today to inform them the decision by Joe Biden to guarantee every deposit in U.S. regional banks is akin to “Joe Biden just nationalized the U.S. banking system.”

O’Leary is correct, and anyone who is holding assets like stocks or bonds in U.S. banks now needs to reconsider the disappeared line between government and the bank assets. If the government can assume, control and backstop every single account balance within the bank, the government can assume and control all activity of the bank. WATCH:

.

Downstream…. think about the consequences. Remember the frozen bank accounts in Canada as a result of defining truck protest supporting Canadian citizens as domestic extremists?

Now think about the government no longer needing to ask the bank to take action, the govt has a regulatory ability to demand the bank to take action. This takes “debanking” to an entire new level. People are wondering why cryptocurrencies went up in value today. There’s your answer.

Comrade citizens, at the end of this rainbow of bank nudges, we will find ourselves at the footsteps of a government controlled central bank digital currency.

A bank failure of this proportion has not been seen since 2008 when Washington Mutual failed. The majority of deposits in Silicon Valley Bank (SVB) are uninsured, meaning the FDIC’s $250,000 protection does not apply. Uninsured depositors will be provided receivership certificates and should receive an advanced dividend this week. The FDIC must sell off the remaining assets of SVC to determine how much it can provide to those uninsured depositors. The FDIC is encouraging borrowers to continue paying their existing loans. The bank was said to host $209 billion in assets and $175.4 billion in deposits as of December 2022. Washington Mutual held around $307 billion in assets when it went down.

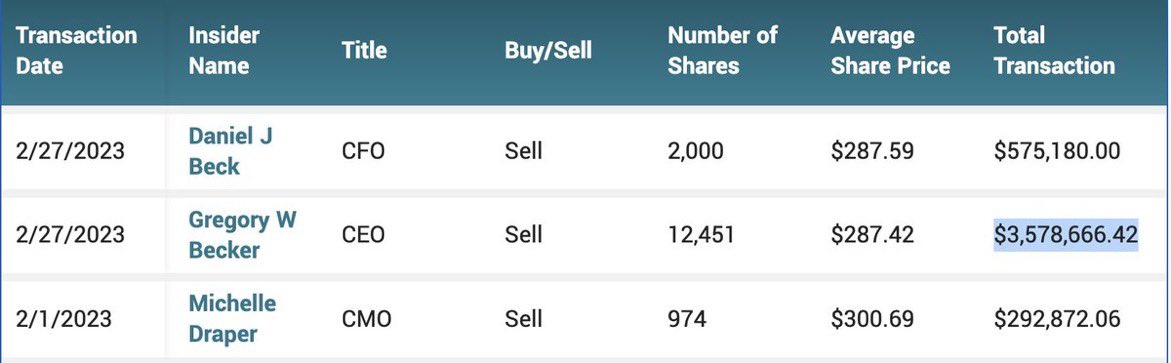

Tons of people and businesses will be completely screwed over. Who could have seen it coming? Silicon Valley Bank CEO, CFO, and CMO sold off millions in stock over the past two weeks. President and CEO Greg Becker sold 12,451 shares on February 27 for $3.6 million at $287.42 per share. Later that day, he purchased options for the same amount of shares at $105.18 a piece. He did the same thing in December 2021, as this is not an uncommon albeit unethical practice. Banks commonly trade against their own clients. Becker sold about $3.57 million worth of SVB stock over the past two weeks and is now making TV appearances saying he did not see this coming.

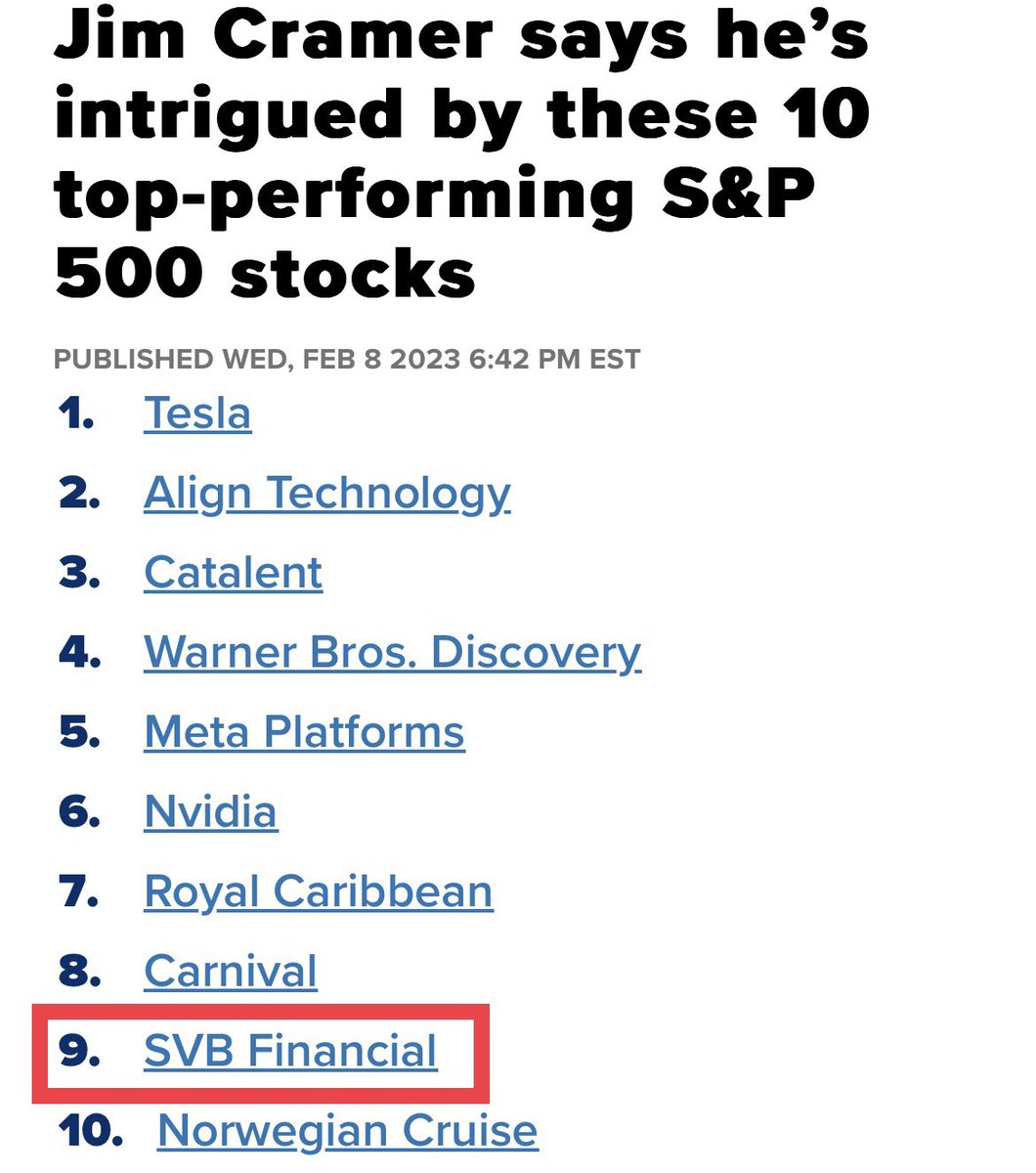

There were signs of trouble, but the talking heads said otherwise. Forbes even listed SVB Financial Group as #20 on its list of America’s Best Banks in an article published on February 14, 2023. Talking/screaming head Jim Cramer came out last month to say that SVB Financial would become one of the top performers on the S&P. This is why you cannot listen to information based on biased opinions. I hesitate to call this negligence technical analysis.

Companies are now at a complete loss, many cannot make payroll, and this situation will only worsen once the uninsured depositors realize their IOUs are worthless.

COMMENT: Marty; Two former Merrill Lynch traders were each sentenced to a year and a day in prison Thursday for manipulating the precious metals markets, the US Department of Justice announced. Of course, —- —–, which is forever bullish metals, claims they moved the metals in the “direction they wanted from 2008 to 2014.” It just seems that people claim it is always manipulation when they have been wrong. They only look at gold in dollars as you have said it’s a global market. They would have to manipulate all the currencies as well.

This latest affair of so-called manipulating trades during the day proves what you have been saying. They have always been gunning for stops during the day, but they cannot manipulate the trend between a bull or bear market. Do you think people will ever understand this is a global economy?

HD

ANSWER: I know. Unless people have actually been a trader, they will never understand the market. They will blame people like this to pretend they were not wrong. The problem is that this nonsense of manipulation is driving a stake through the heart of the market. Trading is like a poker game. Do you reveal your hand before everyone starts to bet? Sometimes you bluff, but the point is if you are bluffing, you have to stand behind your bet.

The mere fact that someone is blaming this type of “manipulation” for being the reason they have been wrong demonstrates that they know nothing about investing no less trading. The DOJ is now big on calling placing large “spoof” orders as manipulation. That is absurd and it is no more than bluffing in a poker game. This is the way all the markets have always functioned. Everyone would know where the stops were anyway. Sometimes they traded ahead of them using the stops as your risk point to exit the trade, and other times they would sell or buy to push the market through the stops when it was obvious that was even possible.

When I was trading in precious metals back in the ’90s, the biggest “local” dealer on the floor was Oni Morrison. He would do “spoof” orders all the time which I called “flash” bids or offers. The difference was he was good for it if hit. I was long one time in gold and I wanted out for the computer projected a crash was coming. But if you offer a thousand lots and the market was heading lower, everyone will read that and jump in front of you. That is how the Hunts went bankrupt. The Hunts did not know how to trade. Just as in poker, you cannot show your hand and expect to trade.

Oni would do “flash” bids or offers. I told my broker not to offer anything. I told him just to watch Oni and as soon as he would do a 1,000 flash to buy – say done! Sure enough, Oni was trying to push the market back up and he did one of his famous flash bids for 1,000 lots. My broker, Emerald Trading, instantly said “DONE!” Oni did it again, and they said “DONE!” Again he did a fash for 1,000 and again they said “DONE!” That was it. Oni was full and everyone began selling as the metals tumbled.

That is the way you have to trade SIZE. This is the very foundation of trading all markets for everything is just a poker game. To now call a “spoof” trade manipulation is just wrong. It is totally different when you do not have the backing. Now that would be a fraud and trying to manipulate the market for that moment – not changing the overall trend. But when you have the backing to honor your “spoof” it is just a “flash” bid or offer that you must stand behind when hit. That is just trading.

It is total BS to pretend that these guys manipulated the entire market. That is just absurd. Not even the central bank can manipulate the economy. You cannot “manipulate” a market against the trend for everything is connected. That caused the Panic of 1893 when the Silver Democrats overpriced silver. The Europeans hit the arbitrage and dumped silver in the US and took the gold back to Europe. That led J.P. Morgan to have to arrange a $100 million gold loan to bail out the treasury. That alone proved that you CANNOT manipulate ANY market against its trend for it will be arbitraged internationally – plain & simple.

Gold trading around the world in different exchanges is arbitraged. You cannot have gold $20 high in one market v another. It will be arbitraged instantly. Those who claim this as “proof” that the metals have been manipulated so that is why they have not rallied and why they have been wrong are fools who have been separated from the money. They will never understand the markets no less be able to see beyond the end of their nose. It will be instantly arbitraged.

The collapse of the Soloman Brothers was precisely that. They were putting in bids at the Treasury Auction using other people’s names to goose the market. They got caught and the firm was taken down. I know PhiBro from the ’70s and ’80s. They took over Solomon Brothers and brought that style of trading from the commodity pits to Wall Street.

This excuse by goldbugs that the metals were actually “manipulated” in their long-term trend, shows their hopeless ignorance of the markets and how they even trade. There is NOBODY who could possibly do such a thing for everything connected. As soon as the dollar would rise, the metals in terms of foreign currency would be so overvalued they would all sell and they will end up broke the same as the Silver Democrats bankrupted the country by overvaluing silver.

Trading internationally, with clients in all currencies, we have to look at each market in terms of their currency for that will determine if they made a profit or loss. Anyone who claims the metals have been manipulated and that is why they have not rallied is obviously oblivious to the world around them.

Gold does NOT rise with inflation – that is the sales pitch of a used car salesman. Gold rises in times of UNCERTAINTY with respect to the government. In times of war, it rises because it is NEUTRAL and you are not betting on who will win.

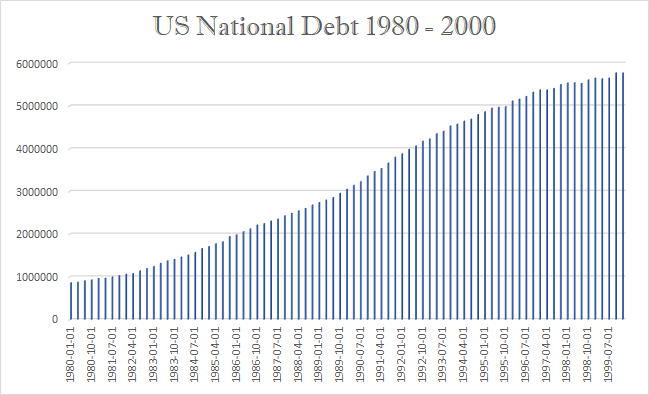

All we hear is that the debt is rising and therefore gold will explode. Once again, they offer no proof of their sophistry because there is no such proof. Gold declined for 19 years while the national debt climbed endlessly.

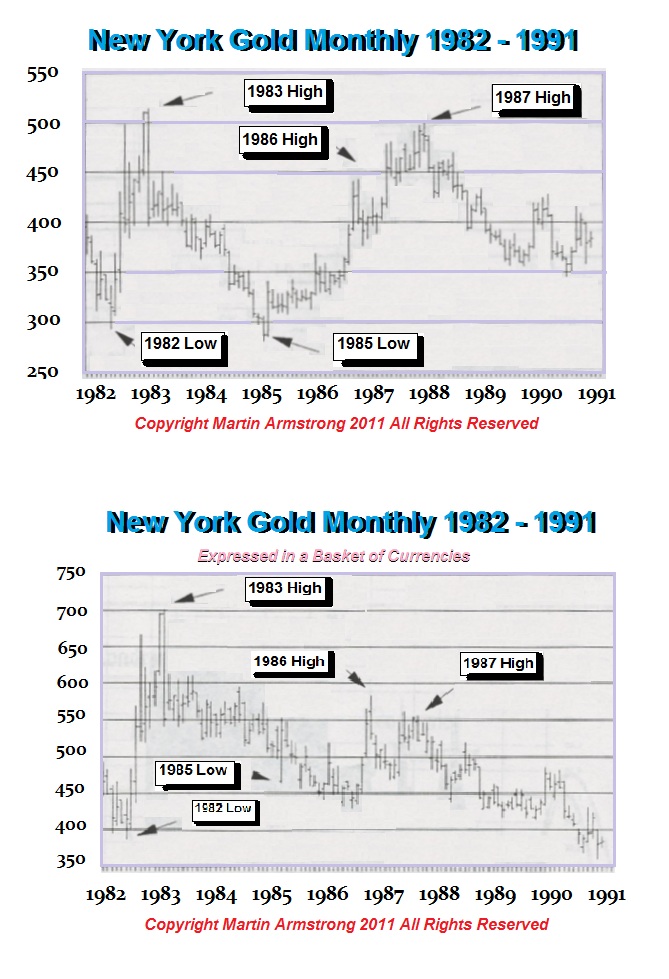

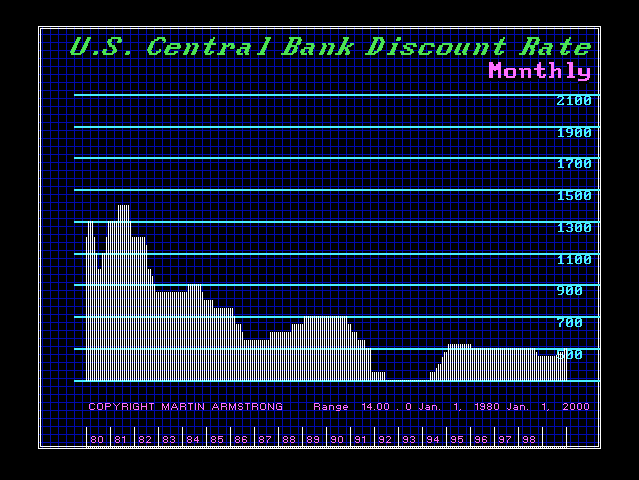

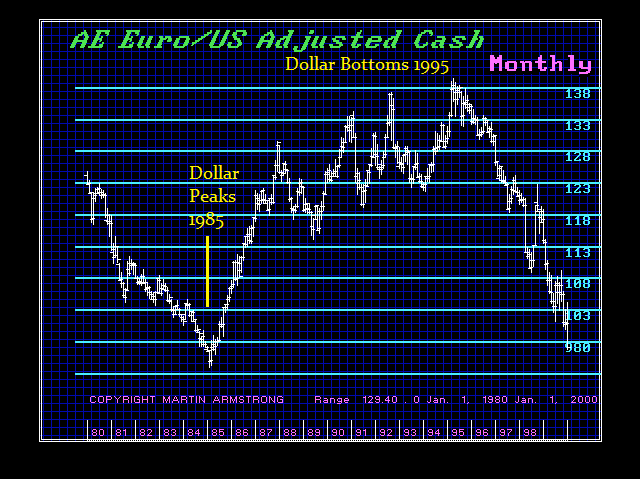

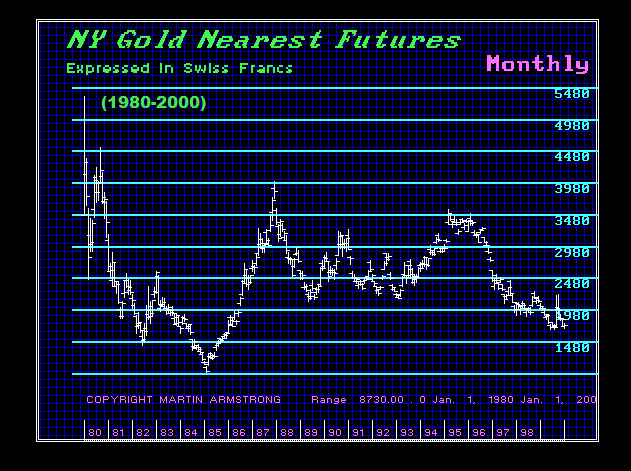

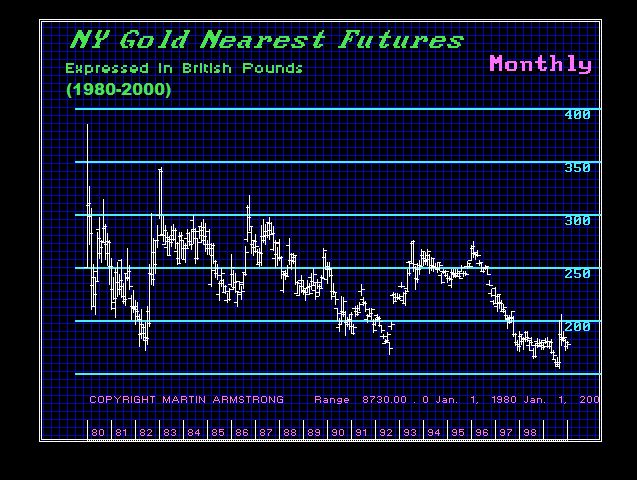

Then there is the myth about interest rates and gold that higher rates are bearish and lower rates are bullish. Well, interest rates peaked in 1981 and declined in 1994 before they began to rise marginally into 1995. Yet then contrast that myth with the performance of the dollar. There the greenback rose to a record high in 1985 but then declined for 10 years into 1995 all the while gold declined into 1999.

OK, so now let’s look at gold between 1980 and 200 in terms of Swiss francs and British pounds. We can instantly see that gold bottomed in 1985 in terms of the Swiss franc. In terms of British pounds, gold did not bottom until 1999.

People come up with theories all the time. However, they always try to reduce everything to a single cause and effect. They are doing that with climate change. They are telling the world it is CO2 that has changed the climate without ever addressing anything else.

The world we live in is not only complex, but it is also so dynamic it appears that no human can correctly forecast the future with an “I think” scenario. Sometimes they will be right, and others they will be wrong. Typically, they fail because they try to reduce the world to a single cause and effect.

Gold Rises with UNCERTAINTY with respect to the question of will the government survive its own madness.

The Biden Administration is responding to the panic phone calls that their Marxist philosophy will bring down the entire financial system. My ear is red as can be. I have had enough of the phone calls today to last the balance of the month. Trying just to do the right thing! Three banks have effectively gone down in the week of March 6th, which our computer was targeting. There have been Silicon Vally Bank, Signature Bank, and Silvergat Bank.

The Regulators perhaps saw the handwriting on the wall. This NO BAILOUT claiming that no taxpayer money will be used for a bailout of their hated rich, how about just using the taxpayer’s money you are throwing down the train in Ukraine? Depositors in Signature and SVB they are now saying would be made whole. If they do not cover ALL deposits, the monumental banking failure will be catastrophic.

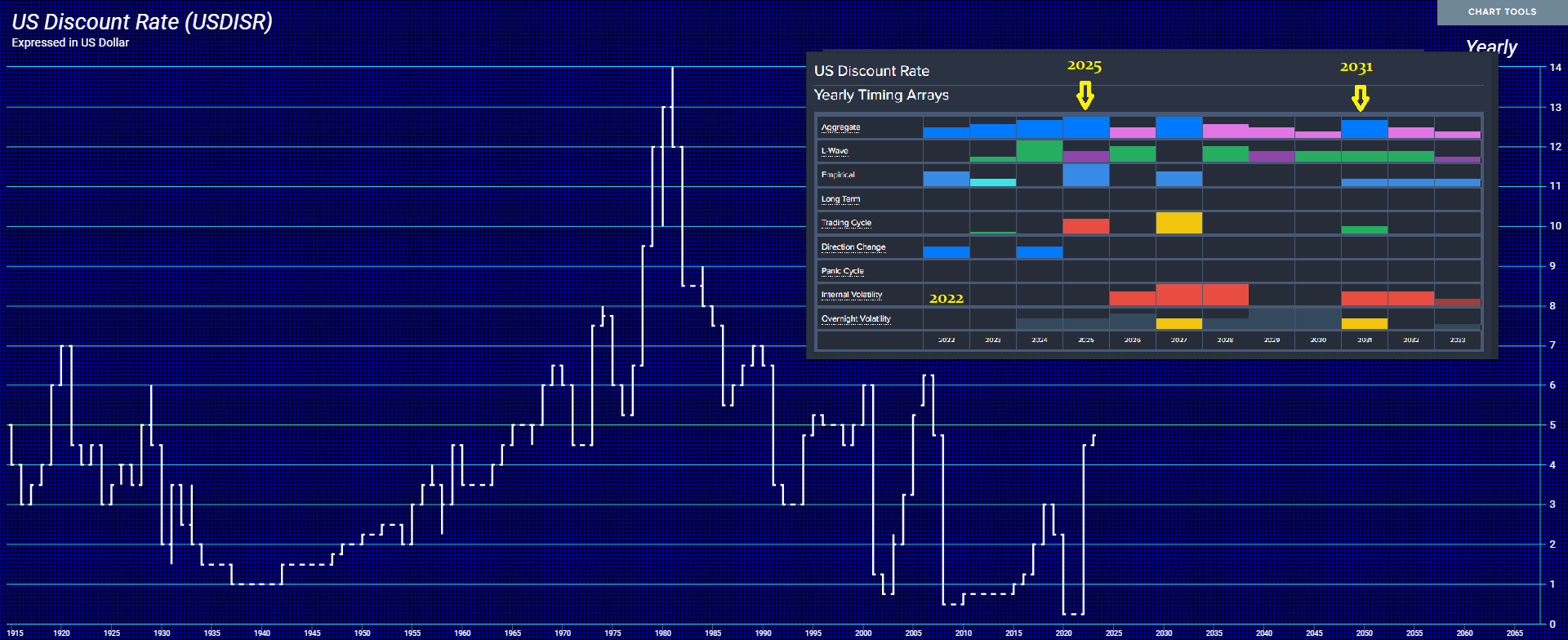

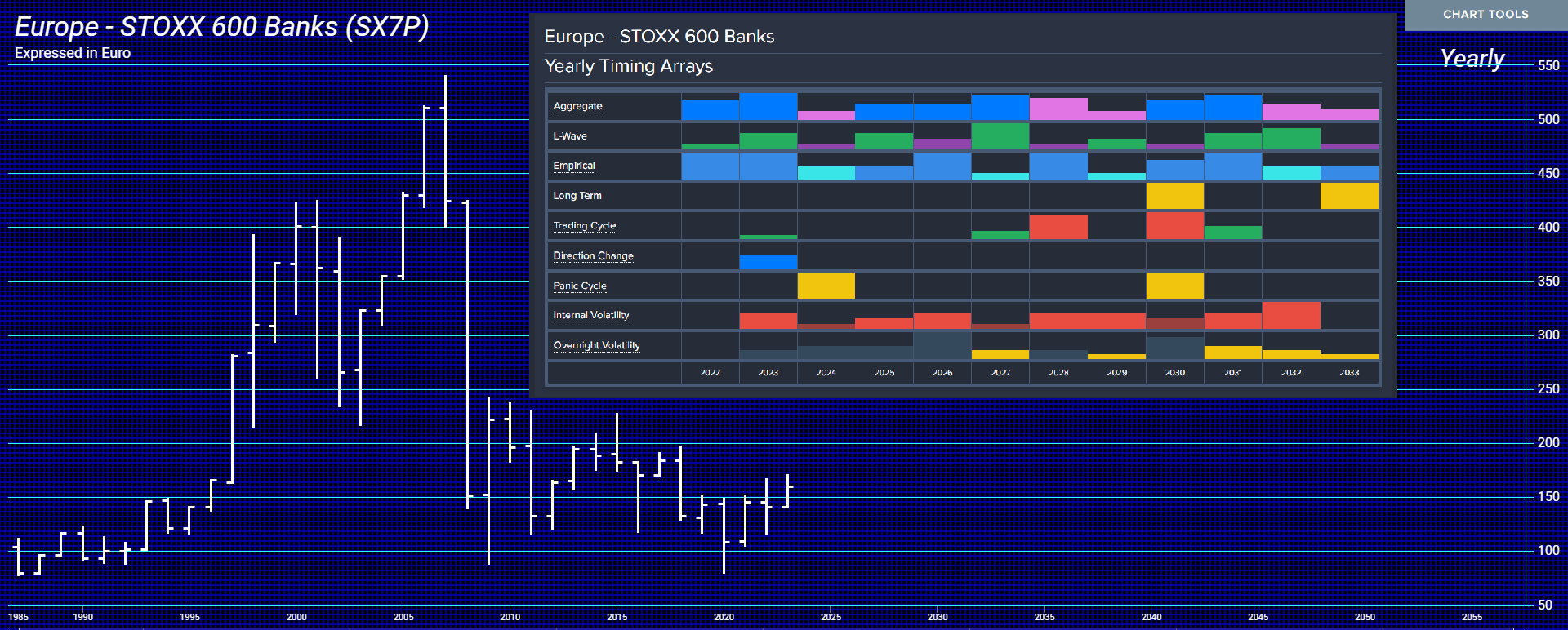

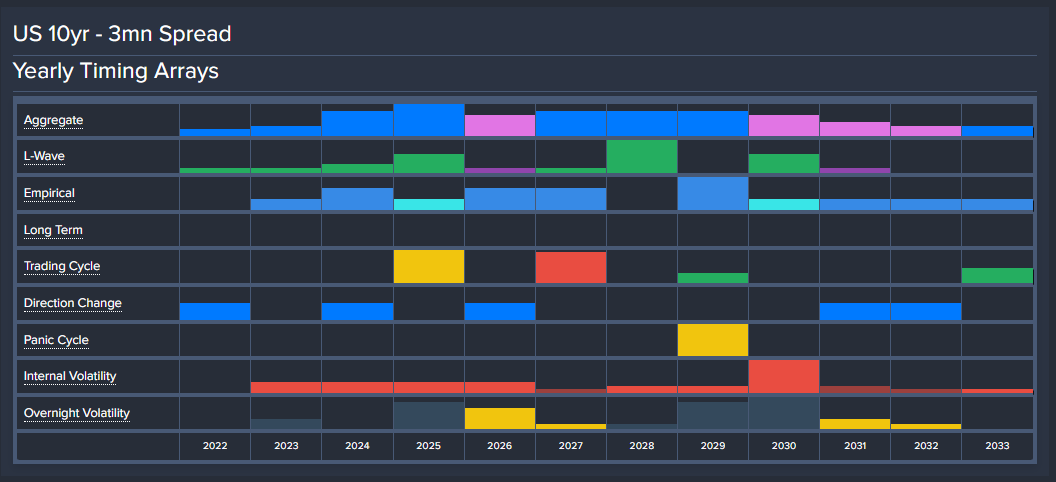

Our forecast for a Banking Crisis is by NO MEANS confined to the United States. It will be far worse in Europe. We can see our computer not only targeted 2023 for a key turning point with a Directional Change but a Panic Cycle next year in bank stocks, but interest rates will be rising higher as also the risk of banks and governments escalated especially when they insist on waging war against Russia.

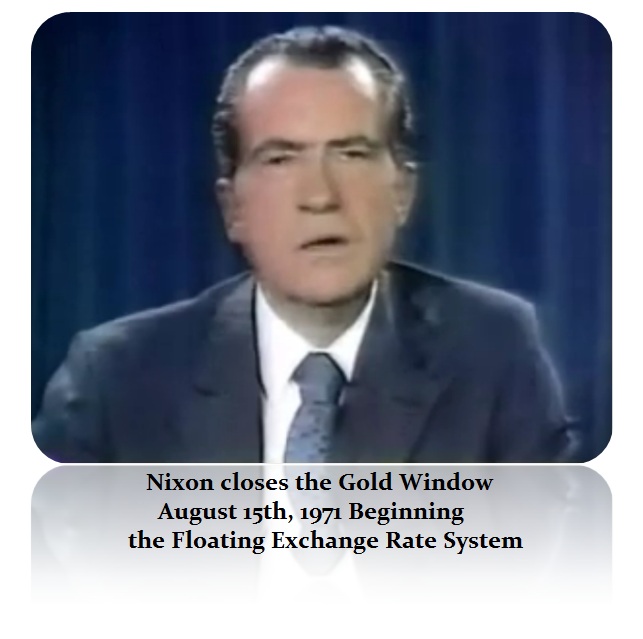

The yield curve is critical and we must understand that this insane war against Russia, even economically, will be a major financial disaster not much different from Vietnam which brought down Bretton Woods and forced Nixon to close the gold window on August 15th, 1971. It was that unrestrained spending directed by the Neocons. Then too, it was all about Russia they assumed was behind Vietnam.

Once more, the reckless spending on war promoted by the Neocons is undermining the entire economy. They have lost every war they have promoted – Vietnam, Afghanistan, Iraq, proposed Syria, Libya regime change, and now Ukraine. These people are never held accountable for all the devastation and the lives lost.

War is the primary driver of inflation and the central banks will not even address it for they do not want to “criticize” the Neocons. They might wake up with their dog’s head in the bed as in the Godfather. The central banks will NOT be able to contain this inflation or ever reach their 2% target regardless if the economy turns down just as what happened during Vietnam.

This is a warning to all small banks. Understand the REAL trend or you will NOT survive. Major capital is fleeing the long-term and rising into the short-term because they see rates are rising and any long-term bond investment during a period of war is going to be a major losing trade. Do not get trapped by the yield curve and understand that this trend is in play into 2025.

This Banking Crisis has been caused by Governments who artificially kept interest rates too low since 2008 and in the process, this banking crisis is unfolding because too many banks are UNSOPHISTICATED in forecasting and have been listening to the talking heads on TV and the desperate hope that inflation will decline while ignoring Ukraine entirely. Get that wrong – and you will NOT survive.

I strongly urge small banks to take our business services for access to real forecasting that is not biased or tarnished by human opinion with the two most dangerous words in forecasting:

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America