Armstrong Economics Blog/Cryptocurrency Re-Posted Nov 14, 2022 by Martin Armstrong

The collapse of the FTX Exchange is pretty straightforward insofar as this is the same lesson that constantly repeats in finance time and time again. Basically, FTX lent US$10bn of client funds to their trading arm Alameda, which used it for leveraged their own crypto speculation because the crypto market has been collapsing. Typically, someone like Sam Bankman-Fried had his whole life wrapped up in this venture. Lacking financial controls operating from the Bahamas, moving the money from client funds to his trading arm Alameda was possible. Historically, someone in this position sees his world collapsing but is not prepared to see that unfold for it requires admitting that he was wrong on crypto, to begin with. Consequently, such a person is not trying to actually rob clients’ money, they most likely see it as a temporary loan to save the company and the market will bounce back – or so they believe.

Our computer had picked the high in Bitcoin perfectly and has been projecting the collapse all along the way. But crypto has become a religion and in so doing it clouds the judgment of people who want to believe the story. Alameda blew up in a crypto meltdown because it did not want to accept that the crypto boom was over. The loan he probably thought would be temporary, vanished in the implosion. At first, I would have assumed they had actually invested the money and lost it on the bond market collapse. But that was perhaps too traditional. Here, it appears they were trying to defend their own cryptocurrency and trying to buy the low that kept moving lower. It appears he was allegedly simply using clients’ funds to trade keeping gains for his firm and the clients now suffer the risk.

It appears that they allegedly were trying to defend the crypto market and did not understand that the boom was over. The loans could not then be repaid. As crypto was crashing, some people needed to cash out. The attempt to pull out US$5bn from FTX exposed the fact that the cash was all gone. This is not so unusual. It has happened before. This time, the prosecutors are clamoring to be the one to charge him so they can become famous over his dead body.

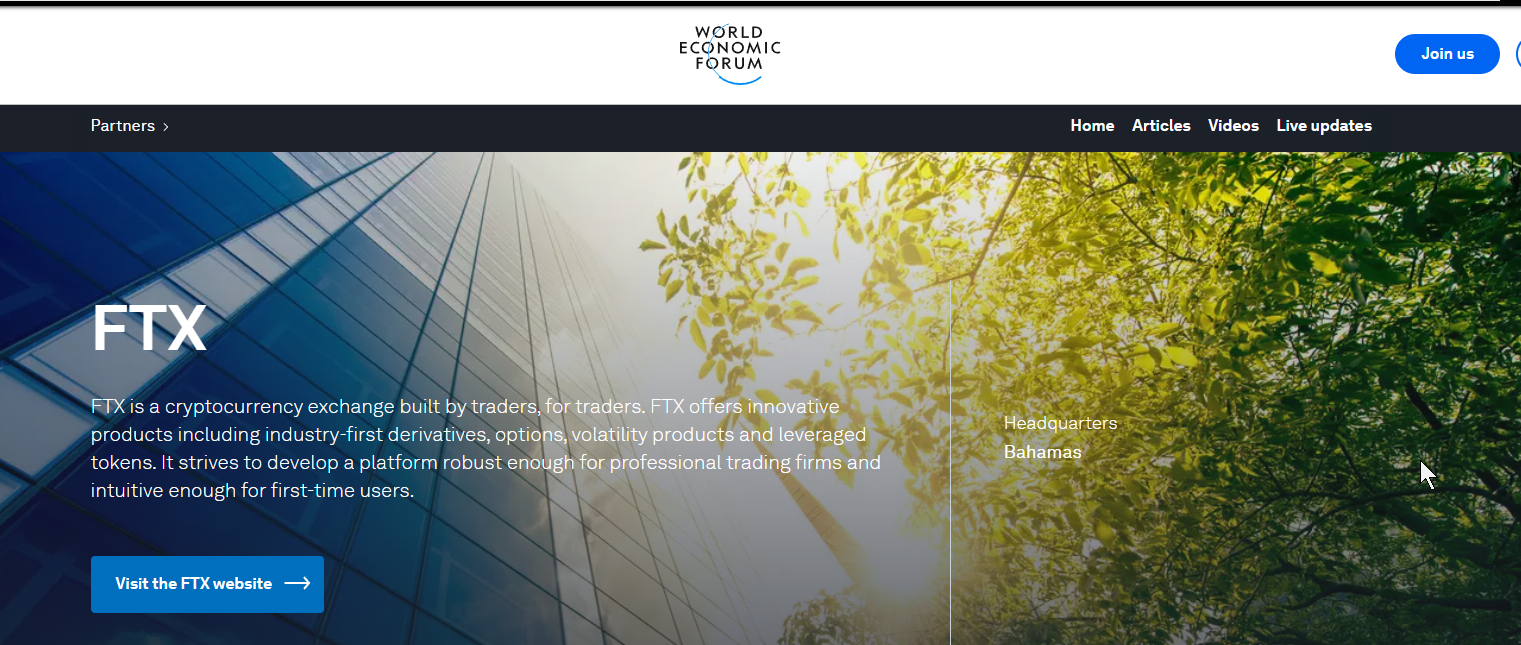

FTX was a partner with Klaus Schwab’s World Economic Forum (WEF). Of course, the WEF has suddenly removed the page and is desperately trying to hide their involvement with FTX and Sam Bankman-Fried. Naturally, eliminating paper currency has been the goal of the WEF because they support the end of not just capitalism, but also democracy. Schwab’s push has been his Great Reset and to control society to impose his economic philosophy inspired by Marx and Lenin.

This is by no means the first violation of fiduciary responsibility that presents a custodial risk. MF Global Holdings Ltd., you might recall, was a firm formerly run by New Jersey ex-Gov. Jon Corzine was accused in 2013 of unlawfully using customer money to meet his firm’s funding needs. When MF Global went bust because of trading by ex-Goldman Sach’s Jon Corzine’s trading using his client’s money in London also outside the regulatory eye of the USA, he was NEVER prosecuted for illegally using $1.6 billion of 26,000 client’s money. That is not going to be the case this time. So what is the difference between Corzine and Bankman-Fried? Corzine was ex-Goldman Sachs.

Indeed, Corzine was well-connected right into the White House with Obama. Nobody went to jail and clients had to wait in bankruptcy to get their money – even cash in the accounts was taken. There are clear risks with the broker and clearer. As long as the SEC is run with former Goldman Sachs staff, there will NEVER be an honest regulator. Even when all the banks pled criminally guilty, the SEC exempted everyone from losing their licenses. They would NEVER do that with anyone outside of New York City. The SEC will never prosecute the banks – EVER!!!!

Indeed, several federal investigations had been launched into MF Global, including probes by the Commodity Futures Trading Commission (its main regulator), the Securities and Exchange Commission, the Federal Bureau of Investigation, and Justice Department prosecutors in both Chicago and New York. The brokerage has also been the focus of several congressional hearings. Not a single one charged Corzine with trading with his client’s money. The losses that eventually drove MF Global into bankruptcy stemmed from high-risk bets on European sovereign bonds that Corzine made as he swung for the fences. Corzine bet big that the bond issuers would not default.

Commodity Futures Trading Commission simply fined Jon Corzine only $5 million over MF Global’s rapid descent into bankruptcy on Oct. 31, 2011, as an estimated $1.6 billion of customer money went missing. Anyone else would have been in prison for a minimum of 20 years.

It was Martin Glenn who was the judge in New York on M.F. Global bankruptcy. He was the first one to engage in FORCED LOANS by abandoning the rule of law to help the bankers by protecting them from losses taking client accounts to cover M.F. Global’s losses. He simply allowed the confiscation of client funds when in fact the rule of law should have been that the bankers were responsible and M.F. Global’s losses should have been reversed as they did even when Robert Maxwell’s companies failed in London from his illegal trading taking employee pension funds.

Yes, that was Ghislaine Maxwell’s father and the guy who was in control of the company that Bill Browder worked for before Edmond Safra. Never should the client’s funds be taken for M.F. Global’s losses to the NY Bankers. It was Judge Martin Glen who placed the entire financial; system at risk by trying to protect the bankers. Martin Glenn pampered these bankers making them the new UNTOUCHABLES. We have to be concerned that there really is no rule of law that will protect you in a crisis.

On Bloomberg TV, Sam Bankman-Fried explained why he even created FTX. He said he was experiencing his own frustration at Alameda Research, which was his crypto-focused proprietary trading firm. He was frustrated with the execution he was receiving at various crypto exchanges so he claimed that inspired FTX’s creation in May 2019. FTX grew rapidly to become the third largest crypto exchange in the world, with approximately $16 billion of customer assets under custody over 43 months.

Bankman-Fried stated that Alameda was making lots of money, but it could have been making more and he did not have access to venture capital. Claims of 100% annualized returns are not uncommon in a boom, but any experienced trader knows what goes up, also comes down. Alameda was relying on “cobbling together lines of credit” to expand its capital base. He then created FTX to solve his funding problem creating his own exchange that even the WEF cheered as a partner. He actually created a platform that was tailored for his own company, Alameda, to facilitate its trading needs. FTX coined the phrase “built by traders, for traders.”

There was an obvious conflict of interest questions regarding the close relationship between FTX and Alameda. Being operated from the Bahamas raised questions among those of us who are seasoned financial market observers whether the two were truly arm’s length from each other. However, people were so pumped up on adrenalin with crypto being the end of the dollar and central banks that this new free-wheeling crypto world believed what they wanted to believe and never looked too closely. FTX operated outside the reach of the US regulatory domain and there was a lack of any fiduciary confirmation. When the founder of Binance, the world’s largest crypto exchange, Changpeng Zhao, openly questioned the soundness of the FTX/Alameda nexus on Twitter saying he would sell over $500 million worth of FTX’s token FTT, that was the kiss of death weather or not he realized he would unleash a crypto panic that would engulf the entire industry in a matter of days.

The collapse of FTX will now become a contagion for the crypto world. This 20-something group of inexperienced traders has signaled the demise of an industry that was getting all the hype with no substance. This crypto world will be seen as the DOT COM Bubble of 2000. With a recession on the horizon, the collapse of sovereign debt, and the monetary system as a whole, people will be looking for more of the safe bets rather than roll the dice on crypto. Nothing ever goes straight down. But by year-end, the volatility should perk up everyone’s view of the world.