Reposed from Armstrong Economics Blog Posted Apr 25, 2023 by Martin Armstrong

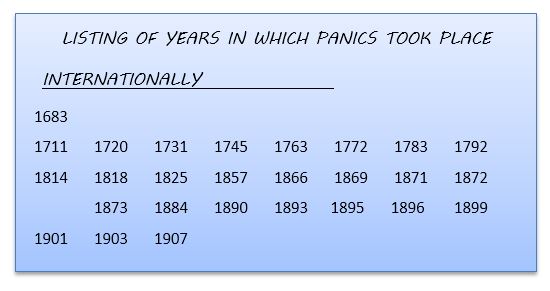

QUESTION: Mr. Armstrong, Your knowledge and database on financial crises is really unprecedented. I googled the first banking crisis and it brought up only the Crisis of 1763, which started in Amsterdam. Yet that list published in the WSJ which showed 1683 as the first panic and the siege of Vienna was most interesting. I know you have written about the sovereign defaults on the ancient central bank in Delos. My question is, was there any major financial banking crisis between antiquity and 1683? I figured if anyone would know, he had to be you.

PF

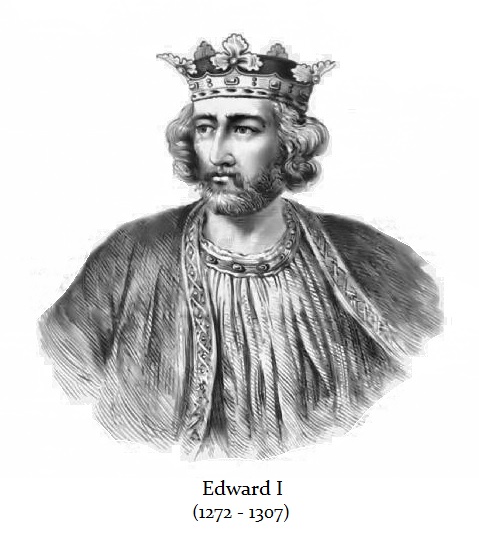

ANSWER: As the 13th century unfolded, the cost of endless Crusades burdened both the crowns of England and France. Throughout the remainder of the 13th century, a variety of Crusades were aimed not so much at toppling Muslim forces in the Holy Land but to combat any and all groups seen as enemies of the Christian faith. Edward began his reign in 1275 with heavy debts incurred from the Crusades.

These endless wars resulted in the time of major sovereign defaults by Edward I of England and Philip IV of France. In 1275, Edward secured a financial monopoly and negotiated a grant of export duties on wool, woolfells, and hides that brought in an average of £10,000 a year. He then used this as collateral to borrow substantially from Italian bankers granting them the security of these customs revenues to fund his endless wars of aggression.

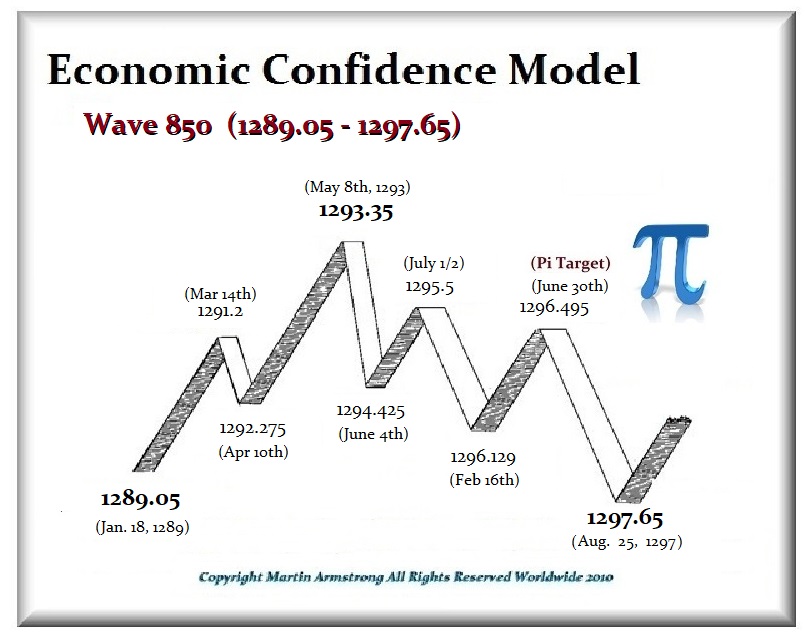

Edward imposed heavy taxes on the value of movable goods. At the beginning of this Wave 850, Edward defaulted on his loans from the English Jewish bankers, and then as 1290 began, to cover that default he expelled all of the Jews from England and confiscate all their property.

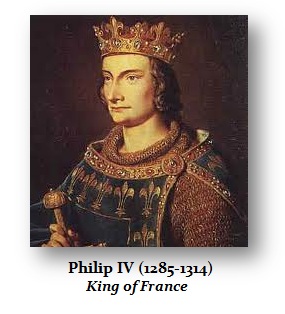

Moreover, this was the Edward Langshakes of the movie “Brave Heart” when in 1291 he attacked Scotland. As this 8.6-year Wave 850 peaked, Edward launched his very costly war against Philip IV (1295-1314) of France which lasted until the end of this 8.6-year wave came to an end in 1297.

The Riccardi of Lucca was perhaps one of the major international merchant banking houses to emerge during the 13th century. The Riccardi established branches in Rome, Bordeaux, Paris, Flanders, London, York, and Dublin, Ireland. They engaged in trade with Edward I of England. Prior to 1272, the English kings were customers of the Italian merchant who had exotic imports as they were purchasing luxury goods and would use them to transfer money to Rome. With the outbreak of war against Philip IV in 1294, a major credit crunch and inflation erupted which impacted the entire international money markets throughout Europe at the time. The value of gold rose against silver from 10:1 to virtually 15:1, which was a monumental distortion of the European monetary system as a consequence of these endless wars.

Cash-strapped, Edward sought financial support from the Riccardi establishment but they refused to lend him any funds. In response, Edward seized all of Riccardi’s assets in England, effectively bankrupting them. The Riccardi had derived significant benefits in dealing with the English monarchy. They held contracts with special access to the English wool market. The Riccardi banking establishment was involved in about 50% of all the forward contracts with English wool producers, which were in effect futures contracts in the cash market. When Edward confiscated all the assets of the Riccardi, his action backfired. Nobody else would then deal with England in international money markets. This led Edward I to impose heavy levels of domestic taxation, which led to civil unrest. This led to a constitutional crisis of 1297.

We all may know that Magna Carta established rights that were forced on King John on June 15th, 1215. After John’s death, the regency government of his young son, Henry III, reissued the document in 1216, but it removed some of its more radical content. This led to civil unrest and at the end of the war in 1217, it became part of the peace treaty when it acquired the name “Magna Carta.” Henry III was compelled to reissue the charter again in 1225 in exchange for a grant of new taxes. Edward I was his son who was then once more compelled to reaffirm the Magna Carta in 1297 at the end of the 8.6-year Wave 850. That is when Edward I was forced to confirm that the Magna Carta was England’s statute law. That is when it actually became England’s rule of law.

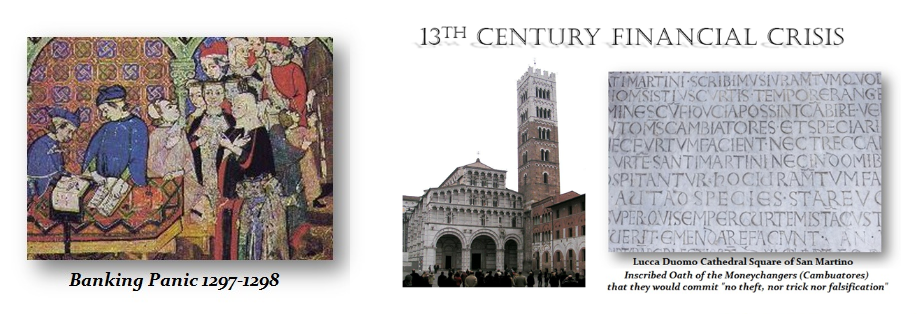

The Bonsignori bank was known as the Gran Tavola, which had become the most powerful of the Italian merchant banking firms throughout Europe between 1255 and 1298. The Gran Tavola was indeed the greatest bank of the 13th century with branches in Paris, Marseille, Genoa, Bologna, and Pisa in addition to the main office in Siena.

Philip IV of France was also strapped for funds. He chose the debasement of the coinage which was massive. Philip had no other course of action to meet the expenses of the war. He began as a massive debasement of the coinage. Silver began to migrate out of France. This debasement only accelerated after 1298 when Philip IV confiscated all the assets Italian bank known as the Gran Tavola in France on claims that they owed him money, without netting anything with respect to his loans owed to them. This caused a major banking crisis in 1298 with the collapse of the institution which also held funds for the Papacy resulting in their loss of 80,000 gold florins. This was the first Banking Panic post-Dark Age. This confiscation of assets wiped out Siena and the city never again rose to the forefront of European commerce. By 1320, Siena was no longer a significant city in international commerce whatsoever which was a direct attack on the Papacy by Philip IV. This resulted in shifting the banking power to Florence.

A full-blown financial panic unfolded as silver migrated overseas. People hoarded the old currency and by 1301 there was virtually no silver remaining in the open market in France. Currency depreciation let Philip cover the cost of the war but it destroyed the credit of France and that ultimately led to France seizing the Papacy and strip-mining all its assets moving the Church to Avignon where a French Pope was installed. They then seized all the assets of the Knights Templar and burned all resistance alive. The Knights Templar were effectively an international transfer agent. If you were in France and needed to pay someone in Italy, you gave the money to the local office in France and they instructed the brank in Italy to pay. It was a 13th-century version of a wire transfer service. That is why the French crown seized the Knights and strip-mined all their wealth as well.

Obviously, this banking crisis of 1298 was far beyond anything most people would have read about in a financial crisis. This is what I mean when I warn that those in power will do WHATEVER it takes to retain power, and religion never means anything at the end of the day.

Categories: Banking Crisis

Tags: 1290, 1301, Banking Crisis, Crusades, debasement, Edward I, Magna Carta, Philip IV, silver, sovereign defaults, wave 850

« Is Your Money Safe in a Regional Bank?

REGISTER FOR BLOG UPDATE ALERTS

BLOG CATEGORIES

- !Private Blog Content (User Login Required)

- +Armstrong Economics 101

- +Armstrong in the Media

- Behavioral Economics

- Books

- +Forecasts

- +History

- Hong Kong

- Humor

- Immigration

- +International News

- Market Talk

- +Markets by Sector

- Plagues

- +Products and Services

- Q&A

- Real Estate

- Uncategorized

- +Upcoming Events

- webinars

- +World Events

PROMOTIONS

Institutional Service for Small Business

Instructional Videos

Socrates

Models and Methodologies

2019 World Economic Conferences

BLOG ARCHIVES

©2023