Armstrong Economics Blog/Understanding Cycles Re-Posted Mar 25, 2023 by Martin Armstrong

QUESTION: Hello Martin,

I have been reading you since your handwritten and from memory letters were getting out from your incarceration. You are truly an amazing man sir.

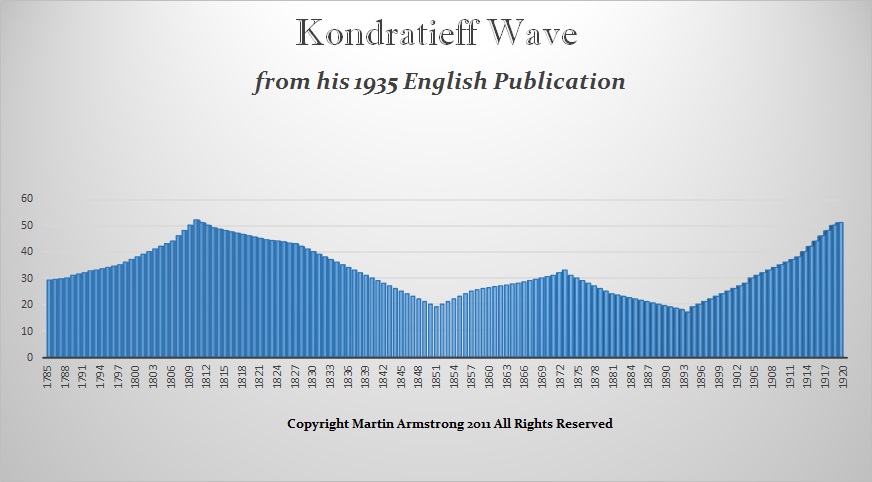

I realize that both the Kondratieff and the Brenner cycles are mostly just coincidental to market cycles today but my question is are both the Kondratieff and the Brenner cycles still accurate for agriculture goods and the farm economy to this day?

Thank you for your consideration of this question as well as for all the good you have done for mankind.

Thank you.

Respectfully,

Mark

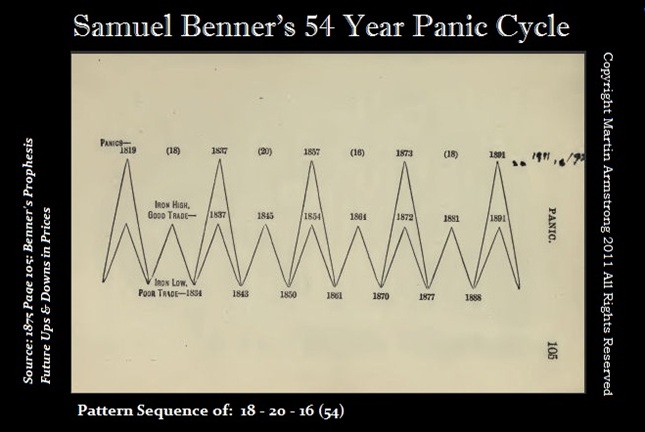

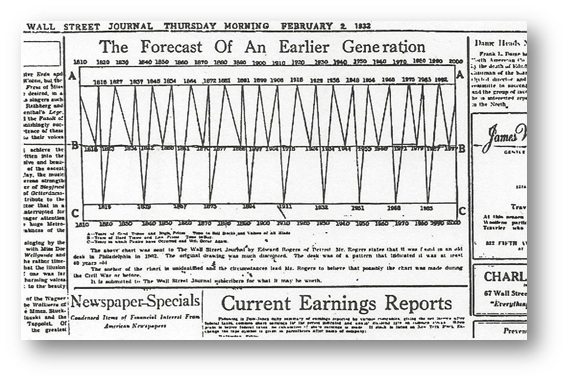

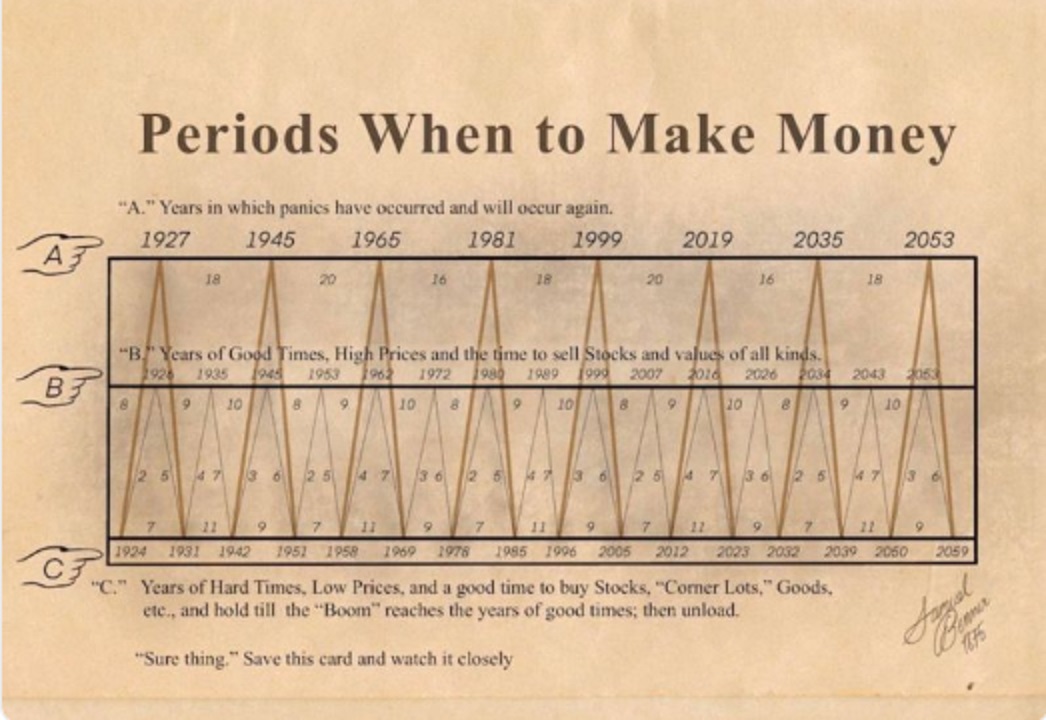

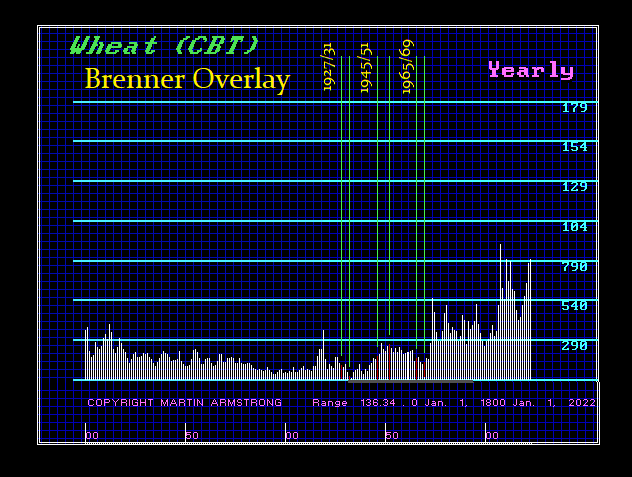

ANSWER: I think your question is very important. I have in my library Brenner’s actual publication. They are very rare, to say the least. Overlaying Brenner onto Wheat, we can see that during the 20th century, they did not work. The question then became why?

People are far too often confused when observing a market. They think that that instrument itself possesses some inherent trading character all by itself. I have often said that when I went to Economics class, the professor said there is no definable business cycle because everything is random. Then I went to Physics class and was told that nothing is random. I came to the conclusion that it was the economics professor who was wrong.

In Physics, we have two separate principles that are far too often confused as the same. The Uncertainty Principle was articulated by the German physicist Werner Heisenberg (1901-1976). It states that the position and the velocity of an object cannot both be measured exactly at the same time, even in theory. The very concepts of exact position and exact velocity together, in fact, have no meaning in nature. Effectively, if we increase the precision in measuring one quantity, we are forced to lose precision in measuring the other.

The Uncertainty Principle has been frequently confused with the Observer Effect whereby the disturbance of an observed system by the act of observation takes place as the result of utilizing instruments that alter the state of what is being measured. To put this in common terms, let’s say you take a gauge to test the tire pressure on your car. The very act of measuring the air pressure results in some air escaping. Hence, the act of observing changes the actual pressure in the tire even minutely.

This is one of the most fascinating aspects of Physics. Here is my favorite cartoon explaining an important aspect of cyclical analysis as well.

So what does this have to do with analysis in markets? What are we actually observing? The innate object be it gold, wheat, or the stock market. If a tree falls in a forest and nobody is around, does it make a sound? That all depends on your definition of a sound. If you define “sound” as requiring it to be heard by a person or animal, the answer is no. Yet is that the proper definition?

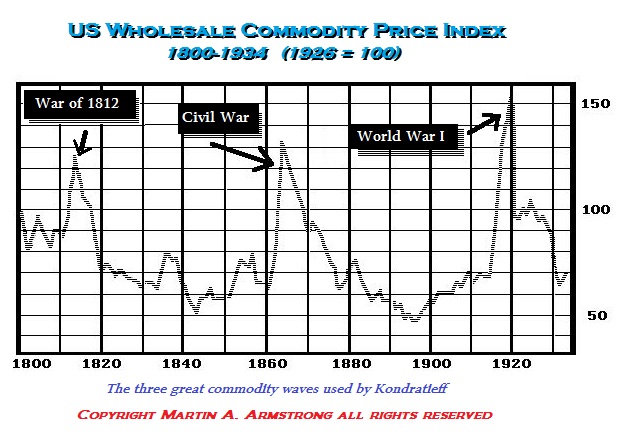

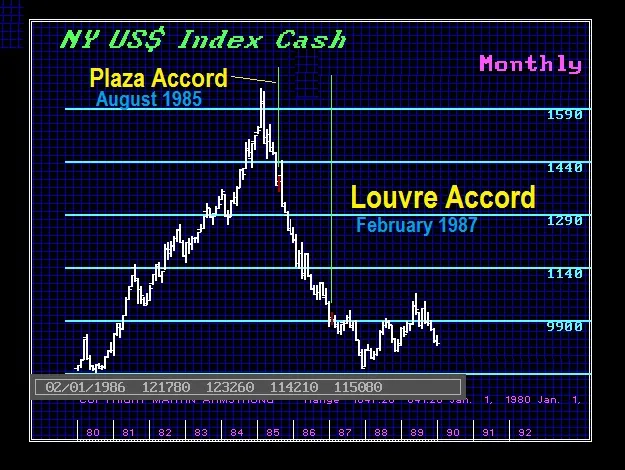

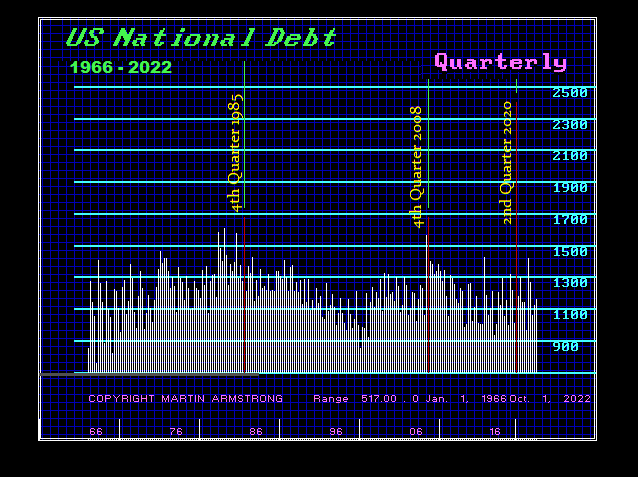

This brings us to Kondratieff and Benner waves. Were they actually measuring commodities, or were they measuring the cyclical interference of climate, war, and 70% of the GDP being confined to agriculture? We clearly have a problem with the human interpretation of an observation. We are then confined by our own prejudices formed in life. If we have NEVER read about war or experienced war, then is it possible to look at the 19th century and realize that there was an interference in the market behavior by war?

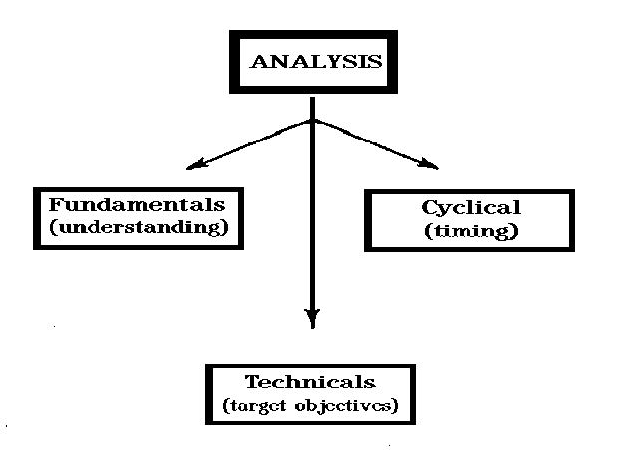

This is why fundamental analysis always fails. Claims that this is the guy who forecasts whatever based upon his opinion or fundamental analysis is simply nothing more than a broken clock is also correct twice a day. The vast array of fundamentals that are taking place simultaneously can never be sorted out by any human being. It depends upon the experience of the observer. I have often explained that people focus only domestically and often on whatever the Federal Reserve wants us to do. They do not see that in turn the Federal Reserve is influenced by international events. Thus, those who focus domestically, are blind to global trends. This is primarily why I developed Socrates for it is humanly impossible to monitor absolutely everything. No human being can do this and then it is impossible to sort out the fundamentals in advance – only hindsight. Many have ignored the fundamental approach and turned to Technical Analysis. Then the third branch is cyclical analysis focused on TIME.

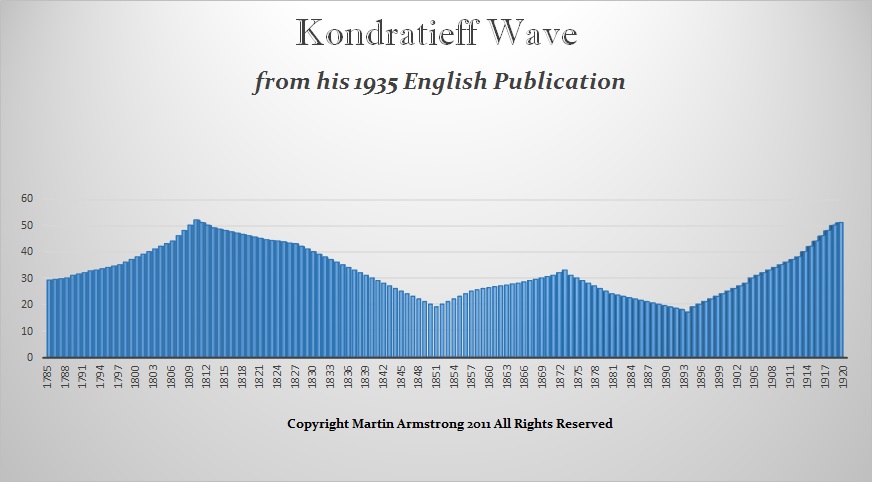

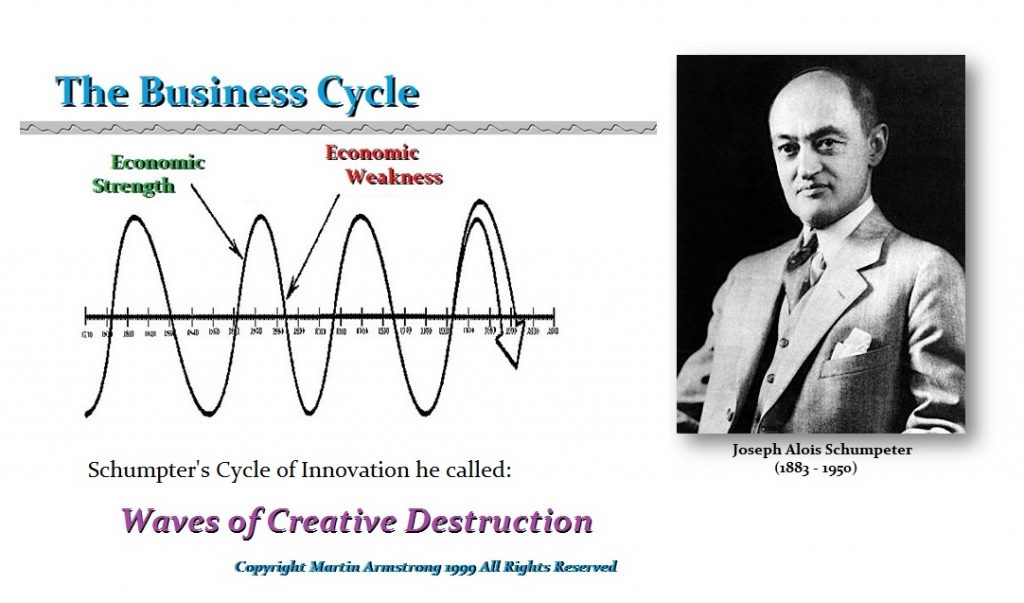

Cyclical Analysis must also incorporate physics to achieve accuracy. Otherwise, someone who then identifies some cycle of 25 units and says see, it worked 5 times in a row, will lose the house for that relationship will change. This is the question of the Kondratieff and Brenner cycles. Kondratief saw broad cyclical trends throughout history. But they were averages and he did not seek a definitive time frequency. Brenner focused on sunspots and agriculture for he was a farmer and saw the cyclical patterns unfolding before him.

However, the complexity of the market and economic behavior is much like the double-slit realization. A single particle moving through a single slit produces a linear output. But when a second slit is introduced, then cyclical waves emerge. This illustrates the complexity. Each market is like a separate particle in that cartoon. By itself with a single slit, the outcome tends to be linear as expected. But adding that second slit produces complexity and cyclical wave interference. Thus, in analysis, we must consider the entire global basket of particles to approach the cyclical waves and interference.

There are so many layers to price activity each displaying a unique frequency. This once again comes down to human interpretation and can the analyst even see the complexity. Our arrays are the best shot at accurate cyclical forecasting and there are 72 models inside that – not a simple one-time frequency of a linear cycle. It is the computer that projects the outcome, not any human interpretation. Then you have to have a database that is unprecedented to back-test the entire analysis. Without recreating the monetary system of the world, it would be impossible for the computer to forecast war, the collapse of communism, or the 1929-style even in Tokyo in 1989.

Fundamental analysis can ONLY be used to explain AFTER the fact – not to forecast the future. Consequently, the Kondratieff and Brenner cyclical waves are not accurate in trying to predict the economy or the next great crash in markets. We must respect that they observed the top layer of cyclical activity, but behind that mask was climate change coming out of the last ice age, the wave of innovation that brought the Industrial Revolution which diminished the commodity influence, and war.

It is not that their work was wrong. They were the leaders in cyclical analysis and pointed the way. It simply required more exploration to understand the complexity and wave interference from the impact of everything, everywhere. The analysis of Benner failed during the 20th century because what he was observing was the complexity of the times and one really needed to sort out each and every component that produced the wave structure during the 19th century to be able to accurately forecast the 20th century.