President Biden’s decision earlier on Monday to veto a bill that would have killed a Labor Department rule on environmental, social, and governance (ESG) investing, has effectively seized your pension and expropriated it directing it to invest in this failed green agenda. That is UNCONSTITUTIONAL and there needs to be an immediate class action suit brought against this outrageous agenda.

In the land of the most insane left-wing Democrats, California, CALPERS, the California pension system for state employees, was directed to invest in “GREEN” projects for political reasons and lost big time. They have been trying to cover-up their politically correct investment decisions ever since. Whenever a politician sticks their foot into how to invest money to carry out their own personal political agenda, not only is that UNCONSTITUTIONAL, but it is really criminal. They are expropriating your pension fund for their agenda.

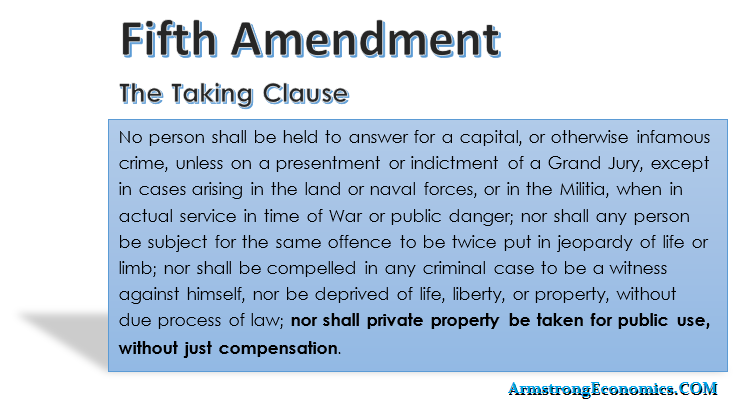

The Takings Clause of the Fifth Amendment to the United States Constitution reads as follows: “Nor shall private property be taken for public use, without just compensation.” In understanding this provision, we must look to the “intent” of the law when enacted. The Clause was intended to uphold the principle that the government should not single out isolated individuals to bear excessive burdens, even in support of an important public good. What Biden and the Democrats have done is so unconstitutional it is no longer funny. Anyone who voted for this act is NOT qualified to be in Congress for they obviously are ignorant of the Constitution which they have sworn to uphold.

The Democrats, to further their climate agenda, have gone way too far. They have violated the Taking Clause and when this happens, the payment of “just compensation” provides a means of removing any special burden. That would be ALL losses incurred by this order are to be borne by the government. The most important statement of this principle is found in Armstrong v. United States 364 U.S. 40 (1960), where the Supreme Court wrote:

“The Fifth Amendment’s [Takings Clause] . . . was designed to bar Government from forcing some people alone to bear public burdens which, in all fairness and justice, should be borne by the public as a whole.”

Only two Senate Democrats voted with Republicans to overturn the rule on March 1st. Sen. Joe Manchin (D-W.Va.) called Biden’s decision “absolutely infuriating” in a statement remarking that the Biden administration is putting its “radical” and “progressive agenda” ahead of the country’s needs.

The point is that this is TOTALLY Unconstitutional. They can no more do that than order everyone must invest in an abortion clinic.

I have mentioned before, we have some of the largest funds in the entire world as our clients. We were actually asked if we could design a “green portfolio” where they did not lose money. A break-even would be fantastic. Biden has now undermined everyone’s retirement savings by making it illegal to consider risk factors that make NO investment sense.

Biden & the Democrats Have NO basis in law to seize your retirement funds to fund their radical leftist agenda! This has gone way too far!

There once was a time when cash was the undisputed king. Merchants preferred cash payments over credit, and there were often incentives for paying with paper. I recall receiving lower gas prices when paying with cash, for example. It is increasingly common to see “no cash accepted” signs at establishments as the world moves toward a cashless society. At the Federal level, there are no laws protecting consumers who wish to pay in cash. The Federal Reserve stated on its website:

There is no federal statute mandating that a private business, a person, or an organization must accept currency or coins as payment for goods or services. Private businesses are free to develop their own policies on whether to accept cash unless there is a state law that says otherwise.

"Section 31 U.S.C. 5103, entitled "Legal tender," states: "United States coins and currency [including Federal Reserve notes and circulating notes of Federal Reserve Banks and national banks] are legal tender for all debts, public charges, taxes, and dues." This statute means that all U.S. money as identified above is a valid and legal offer of payment for debts when tendered to a creditor."

Yet, the Federal Reserve also recognizes that as of 2021, 4.5% of US households were “unbanked.” This means that 5.9 million households are unable to pay by card. This is the lowest unbanked rate since the Fed began keeping track in 2009. The most common reason for not having an account, reported by 21.7% of unbanked households, is that they do not meet minimum balance requirements. The second most reported reason (13.2%) is that people simply do not trust banks, while the third most cited reason (8.4%) was the desire for privacy.

If merchants refuse to accept cash, these people cannot participate in consumerism. Their legal tender is simply not accepted. Unbanked households are more likely to contain persons with lower levels of education, lower incomes, disabilities, single mothers, and minorities. As the Fed reported:

“Differences in unbanked rates between Black and White households and between Hispanic and White households in 2021 were present at every income level. For example, among households with income between $30,000 and $50,000, 8.0 percent of Black households and 8.4 percent of Hispanic households were unbanked, compared with 1.7 percent of White households.”

If cash is legal tender, then it should be accepted everywhere. Numerous merchants not only refuse cash but they charge an additional fee for using credit. Tennessee, Arizona, Delaware, District of Columbia, Idaho, Maine, Massachusetts, Michigan, Mississippi, New York, North Dakota, Oklahoma and Pennsylvania, New Jersey, Rhode, Colorado, and Connecticut have laws at the state level protecting cash payments. Some cities such as Washington D.C., Berkley, Chicago, New York City, Philadelphia, and San Francisco also have laws in place. However, I can assure you that many retailers in these areas still do not accept cash.

Washington wants to move us toward a cashless society to tax everyone, even those with the least to give, on every transaction we make.

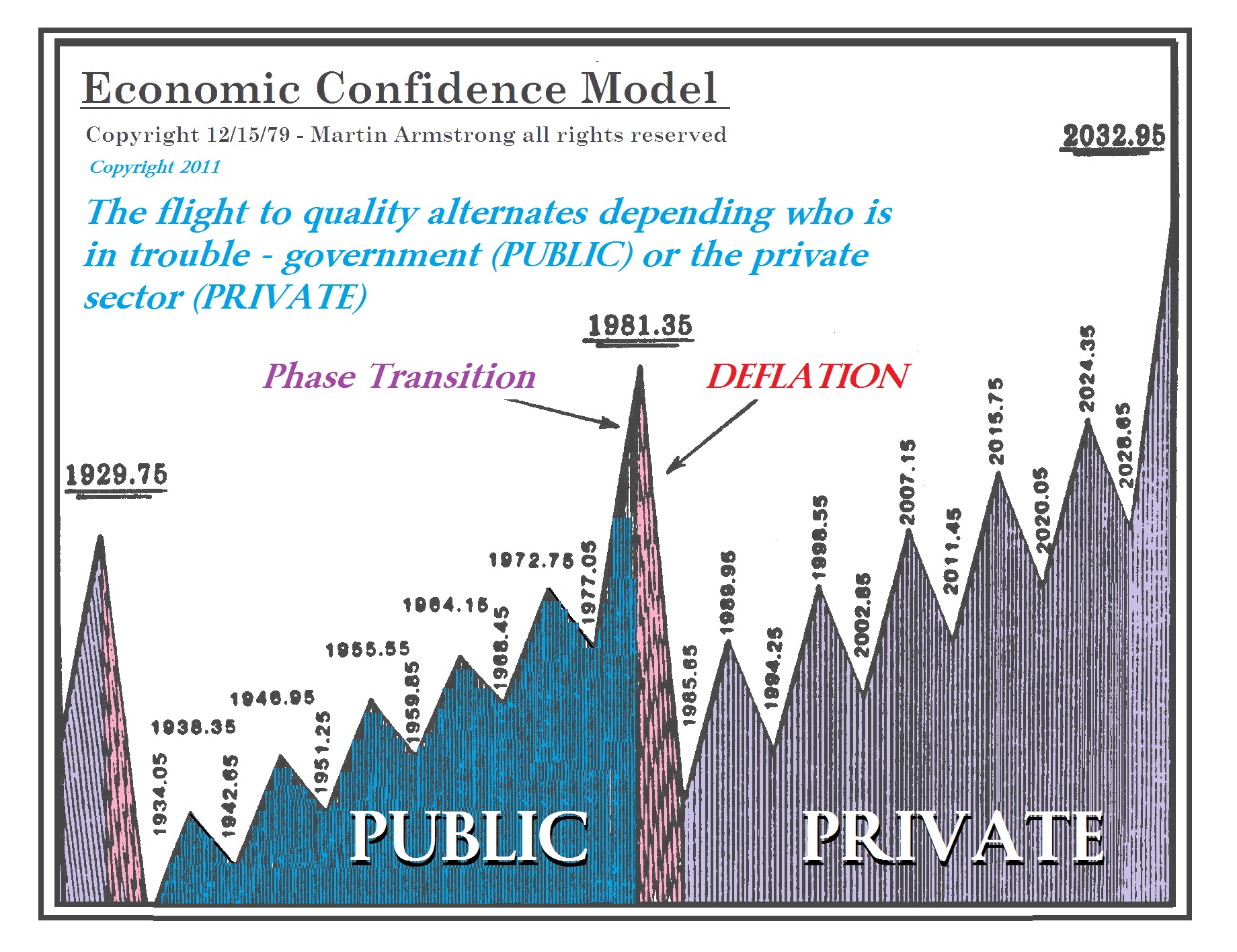

In an interview on May 11, 2014, I explained on USAWatchdog that confidence always outweighs reality. “It’s basically what you believe. There have been all sorts of studies on fundamentals that say if interest rates go up, stocks go down. It is simply not true. The stock market has never peaked with interest rates twice in history. If you think you are going to make 25% in the market, you’ll pay 10% interest; but if you really think the market is only going to go up 10%, you won’t pay 10%. So, it’s always the difference between what you believe and reality.”

The people have lost all confidence in government. We have heard rumors of a “soft landing” from the Fed for the past year, but the situation continues to worsen. Washington maintains that everything is stable as banks continue to fail and inflation rages on. There can be no price stability when war is at play. Biden just released his latest budget plan that no reasonable person would condone. I explained in 2014 that great empires all come crashing down after piling on massive debt. People believe hyperinflation would cause such a scenario, but debt is the major player. Once the government accumulates enormous debt, it targets its citizens aggressively. That is what we are seeing today.

So where should you put your money? I said in 2014: “One of the number one questions I get all the time is where do I put my money? If the banks can just take whatever they want now, there will be bail-ins rather than bail-outs. People are afraid. What do you do with the cash? So, people are buying things like real estate and stocks, just trying to get money out of the banking system.” That sentiment is continuing and the latest CPI report even showed that shelter costs are rising at the highest rate since June 1982. Smart money has been trying to escape the banks for years. There was no incentive until very recently to park money in the banks due to artificially low rates.

I also explained that the Fed would only bail out deposits and had been asking institutions to change their models. “Everybody knows I advise some of the big institutions around, and I can tell you that they have told me directly that the Fed went to them and told them they will not be bailed out for proprietary trading. It will be only on deposits. That’s it,” I stated. “The Fed has been going around telling them, ‘hey, you better change your models.’ They don’t think it will be a flight to quality as it was before. You buy the long term (Treasuries) and that saves you. They don’t think that’s going to happen. It’s quite interesting. . . . It looks like the long term (Treasury bonds) is going to end up starting to rise.”

Sound familiar to the current situation? People have moved from the public sector into the private sector. We are well into a private wave, and the public will not go back to the public sector for many years to come.

A bank failure of this proportion has not been seen since 2008 when Washington Mutual failed. The majority of deposits in Silicon Valley Bank (SVB) are uninsured, meaning the FDIC’s $250,000 protection does not apply. Uninsured depositors will be provided receivership certificates and should receive an advanced dividend this week. The FDIC must sell off the remaining assets of SVC to determine how much it can provide to those uninsured depositors. The FDIC is encouraging borrowers to continue paying their existing loans. The bank was said to host $209 billion in assets and $175.4 billion in deposits as of December 2022. Washington Mutual held around $307 billion in assets when it went down.

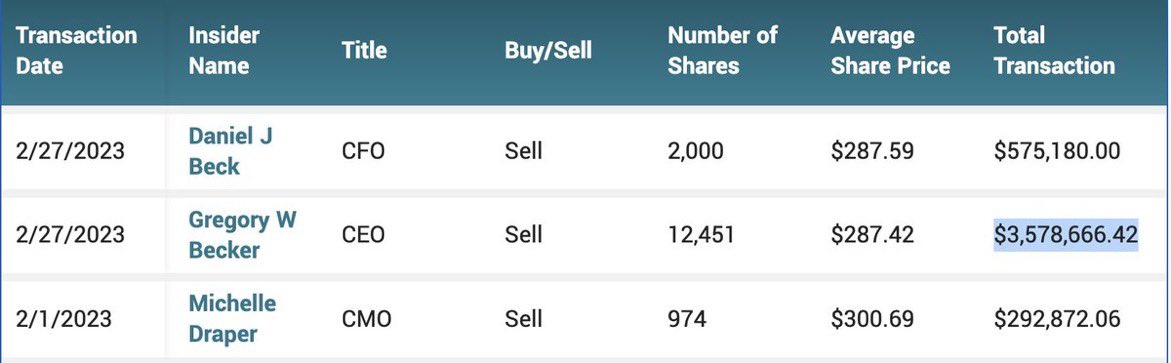

Tons of people and businesses will be completely screwed over. Who could have seen it coming? Silicon Valley Bank CEO, CFO, and CMO sold off millions in stock over the past two weeks. President and CEO Greg Becker sold 12,451 shares on February 27 for $3.6 million at $287.42 per share. Later that day, he purchased options for the same amount of shares at $105.18 a piece. He did the same thing in December 2021, as this is not an uncommon albeit unethical practice. Banks commonly trade against their own clients. Becker sold about $3.57 million worth of SVB stock over the past two weeks and is now making TV appearances saying he did not see this coming.

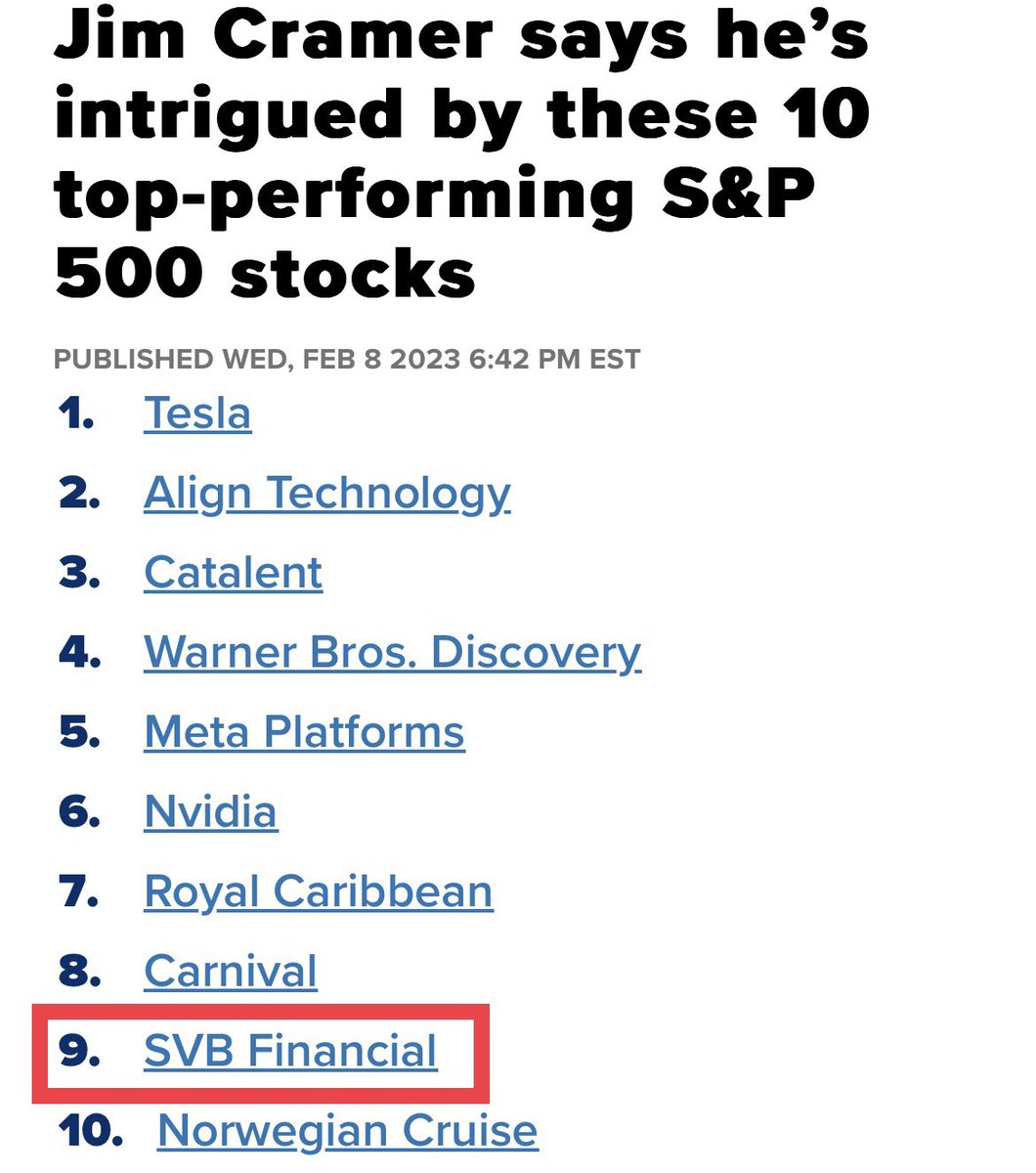

There were signs of trouble, but the talking heads said otherwise. Forbes even listed SVB Financial Group as #20 on its list of America’s Best Banks in an article published on February 14, 2023. Talking/screaming head Jim Cramer came out last month to say that SVB Financial would become one of the top performers on the S&P. This is why you cannot listen to information based on biased opinions. I hesitate to call this negligence technical analysis.

Companies are now at a complete loss, many cannot make payroll, and this situation will only worsen once the uninsured depositors realize their IOUs are worthless.

COMMENT: Marty; Two former Merrill Lynch traders were each sentenced to a year and a day in prison Thursday for manipulating the precious metals markets, the US Department of Justice announced. Of course, —- —–, which is forever bullish metals, claims they moved the metals in the “direction they wanted from 2008 to 2014.” It just seems that people claim it is always manipulation when they have been wrong. They only look at gold in dollars as you have said it’s a global market. They would have to manipulate all the currencies as well.

This latest affair of so-called manipulating trades during the day proves what you have been saying. They have always been gunning for stops during the day, but they cannot manipulate the trend between a bull or bear market. Do you think people will ever understand this is a global economy?

HD

ANSWER: I know. Unless people have actually been a trader, they will never understand the market. They will blame people like this to pretend they were not wrong. The problem is that this nonsense of manipulation is driving a stake through the heart of the market. Trading is like a poker game. Do you reveal your hand before everyone starts to bet? Sometimes you bluff, but the point is if you are bluffing, you have to stand behind your bet.

The mere fact that someone is blaming this type of “manipulation” for being the reason they have been wrong demonstrates that they know nothing about investing no less trading. The DOJ is now big on calling placing large “spoof” orders as manipulation. That is absurd and it is no more than bluffing in a poker game. This is the way all the markets have always functioned. Everyone would know where the stops were anyway. Sometimes they traded ahead of them using the stops as your risk point to exit the trade, and other times they would sell or buy to push the market through the stops when it was obvious that was even possible.

When I was trading in precious metals back in the ’90s, the biggest “local” dealer on the floor was Oni Morrison. He would do “spoof” orders all the time which I called “flash” bids or offers. The difference was he was good for it if hit. I was long one time in gold and I wanted out for the computer projected a crash was coming. But if you offer a thousand lots and the market was heading lower, everyone will read that and jump in front of you. That is how the Hunts went bankrupt. The Hunts did not know how to trade. Just as in poker, you cannot show your hand and expect to trade.

Oni would do “flash” bids or offers. I told my broker not to offer anything. I told him just to watch Oni and as soon as he would do a 1,000 flash to buy – say done! Sure enough, Oni was trying to push the market back up and he did one of his famous flash bids for 1,000 lots. My broker, Emerald Trading, instantly said “DONE!” Oni did it again, and they said “DONE!” Again he did a fash for 1,000 and again they said “DONE!” That was it. Oni was full and everyone began selling as the metals tumbled.

That is the way you have to trade SIZE. This is the very foundation of trading all markets for everything is just a poker game. To now call a “spoof” trade manipulation is just wrong. It is totally different when you do not have the backing. Now that would be a fraud and trying to manipulate the market for that moment – not changing the overall trend. But when you have the backing to honor your “spoof” it is just a “flash” bid or offer that you must stand behind when hit. That is just trading.

It is total BS to pretend that these guys manipulated the entire market. That is just absurd. Not even the central bank can manipulate the economy. You cannot “manipulate” a market against the trend for everything is connected. That caused the Panic of 1893 when the Silver Democrats overpriced silver. The Europeans hit the arbitrage and dumped silver in the US and took the gold back to Europe. That led J.P. Morgan to have to arrange a $100 million gold loan to bail out the treasury. That alone proved that you CANNOT manipulate ANY market against its trend for it will be arbitraged internationally – plain & simple.

Gold trading around the world in different exchanges is arbitraged. You cannot have gold $20 high in one market v another. It will be arbitraged instantly. Those who claim this as “proof” that the metals have been manipulated so that is why they have not rallied and why they have been wrong are fools who have been separated from the money. They will never understand the markets no less be able to see beyond the end of their nose. It will be instantly arbitraged.

The collapse of the Soloman Brothers was precisely that. They were putting in bids at the Treasury Auction using other people’s names to goose the market. They got caught and the firm was taken down. I know PhiBro from the ’70s and ’80s. They took over Solomon Brothers and brought that style of trading from the commodity pits to Wall Street.

This excuse by goldbugs that the metals were actually “manipulated” in their long-term trend, shows their hopeless ignorance of the markets and how they even trade. There is NOBODY who could possibly do such a thing for everything connected. As soon as the dollar would rise, the metals in terms of foreign currency would be so overvalued they would all sell and they will end up broke the same as the Silver Democrats bankrupted the country by overvaluing silver.

Trading internationally, with clients in all currencies, we have to look at each market in terms of their currency for that will determine if they made a profit or loss. Anyone who claims the metals have been manipulated and that is why they have not rallied is obviously oblivious to the world around them.

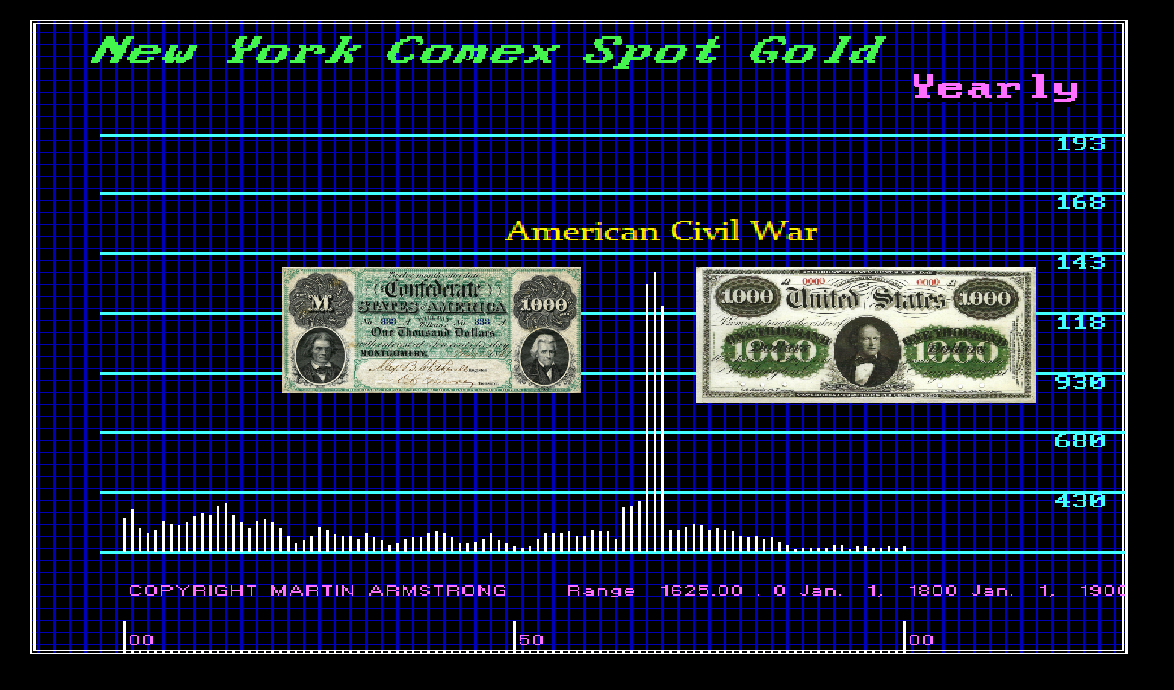

Gold does NOT rise with inflation – that is the sales pitch of a used car salesman. Gold rises in times of UNCERTAINTY with respect to the government. In times of war, it rises because it is NEUTRAL and you are not betting on who will win.

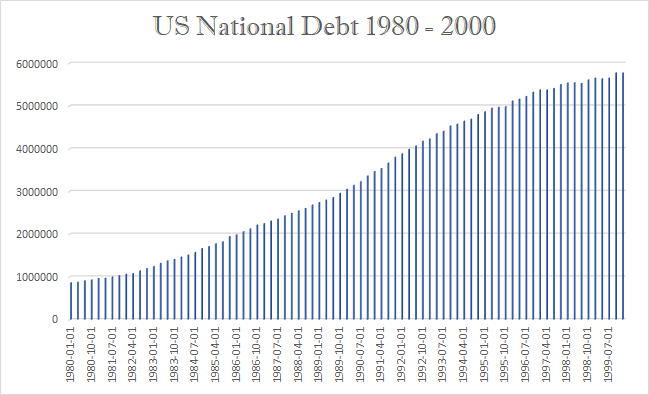

All we hear is that the debt is rising and therefore gold will explode. Once again, they offer no proof of their sophistry because there is no such proof. Gold declined for 19 years while the national debt climbed endlessly.

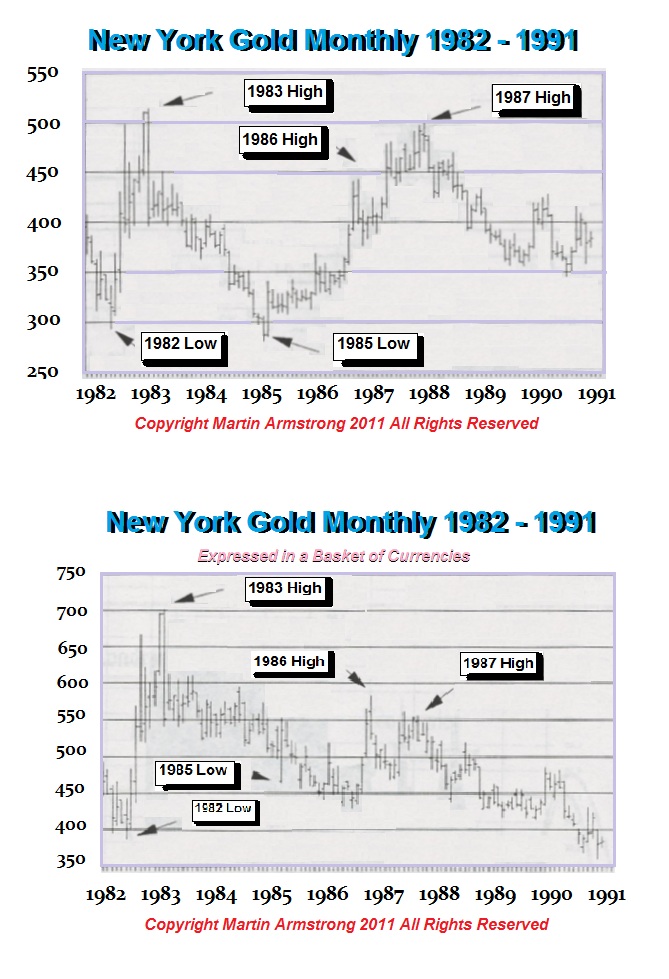

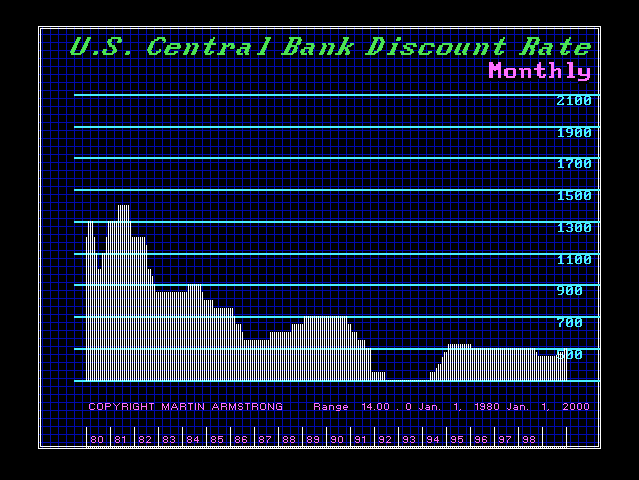

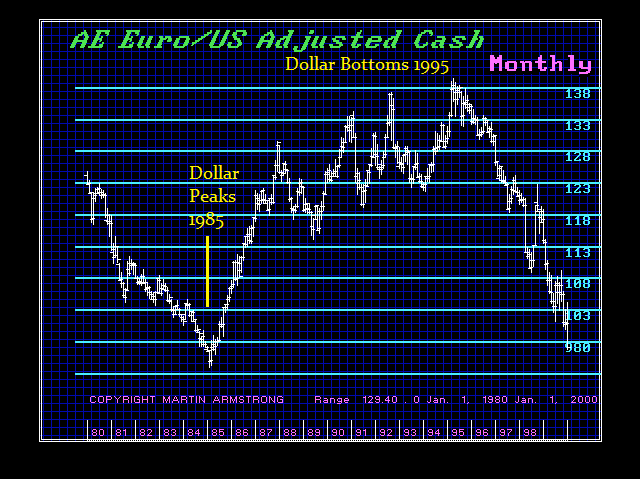

Then there is the myth about interest rates and gold that higher rates are bearish and lower rates are bullish. Well, interest rates peaked in 1981 and declined in 1994 before they began to rise marginally into 1995. Yet then contrast that myth with the performance of the dollar. There the greenback rose to a record high in 1985 but then declined for 10 years into 1995 all the while gold declined into 1999.

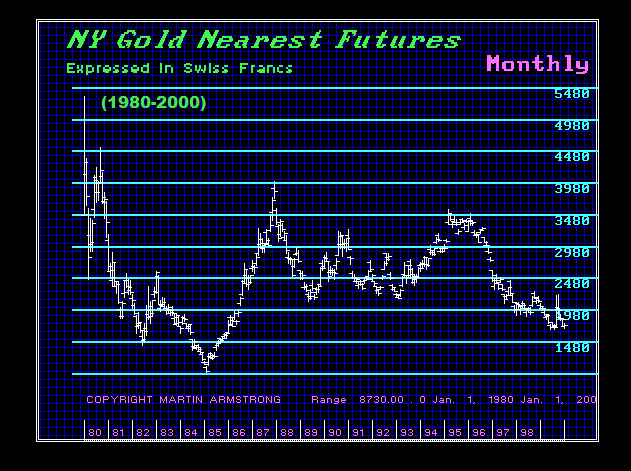

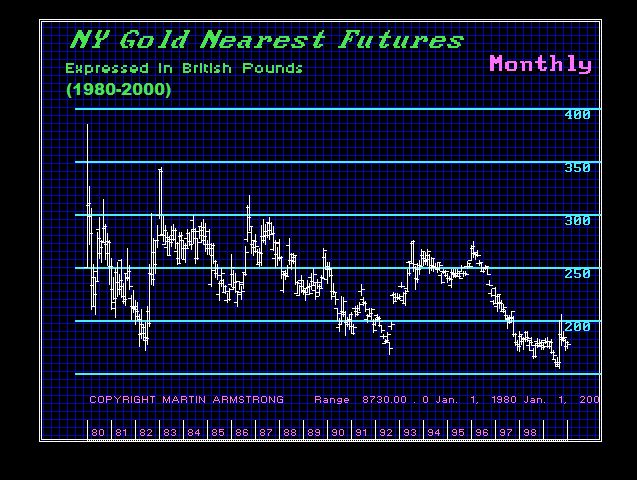

OK, so now let’s look at gold between 1980 and 200 in terms of Swiss francs and British pounds. We can instantly see that gold bottomed in 1985 in terms of the Swiss franc. In terms of British pounds, gold did not bottom until 1999.

People come up with theories all the time. However, they always try to reduce everything to a single cause and effect. They are doing that with climate change. They are telling the world it is CO2 that has changed the climate without ever addressing anything else.

The world we live in is not only complex, but it is also so dynamic it appears that no human can correctly forecast the future with an “I think” scenario. Sometimes they will be right, and others they will be wrong. Typically, they fail because they try to reduce the world to a single cause and effect.

Gold Rises with UNCERTAINTY with respect to the question of will the government survive its own madness.

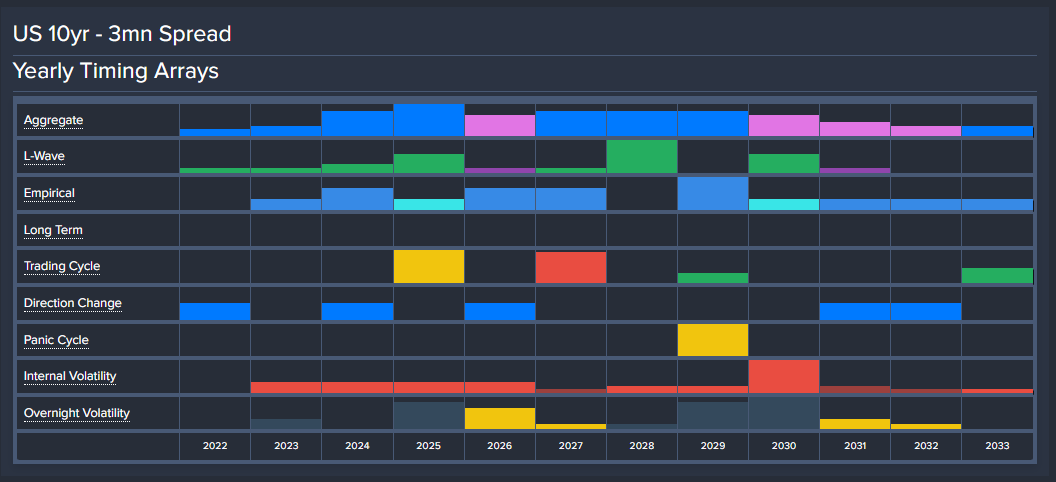

The Biden Administration is responding to the panic phone calls that their Marxist philosophy will bring down the entire financial system. My ear is red as can be. I have had enough of the phone calls today to last the balance of the month. Trying just to do the right thing! Three banks have effectively gone down in the week of March 6th, which our computer was targeting. There have been Silicon Vally Bank, Signature Bank, and Silvergat Bank.

The Regulators perhaps saw the handwriting on the wall. This NO BAILOUT claiming that no taxpayer money will be used for a bailout of their hated rich, how about just using the taxpayer’s money you are throwing down the train in Ukraine? Depositors in Signature and SVB they are now saying would be made whole. If they do not cover ALL deposits, the monumental banking failure will be catastrophic.

Our forecast for a Banking Crisis is by NO MEANS confined to the United States. It will be far worse in Europe. We can see our computer not only targeted 2023 for a key turning point with a Directional Change but a Panic Cycle next year in bank stocks, but interest rates will be rising higher as also the risk of banks and governments escalated especially when they insist on waging war against Russia.

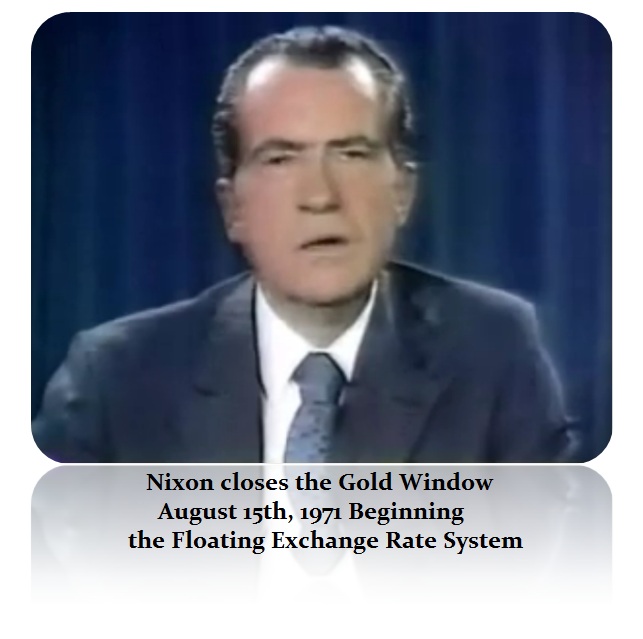

The yield curve is critical and we must understand that this insane war against Russia, even economically, will be a major financial disaster not much different from Vietnam which brought down Bretton Woods and forced Nixon to close the gold window on August 15th, 1971. It was that unrestrained spending directed by the Neocons. Then too, it was all about Russia they assumed was behind Vietnam.

Once more, the reckless spending on war promoted by the Neocons is undermining the entire economy. They have lost every war they have promoted – Vietnam, Afghanistan, Iraq, proposed Syria, Libya regime change, and now Ukraine. These people are never held accountable for all the devastation and the lives lost.

War is the primary driver of inflation and the central banks will not even address it for they do not want to “criticize” the Neocons. They might wake up with their dog’s head in the bed as in the Godfather. The central banks will NOT be able to contain this inflation or ever reach their 2% target regardless if the economy turns down just as what happened during Vietnam.

This is a warning to all small banks. Understand the REAL trend or you will NOT survive. Major capital is fleeing the long-term and rising into the short-term because they see rates are rising and any long-term bond investment during a period of war is going to be a major losing trade. Do not get trapped by the yield curve and understand that this trend is in play into 2025.

This Banking Crisis has been caused by Governments who artificially kept interest rates too low since 2008 and in the process, this banking crisis is unfolding because too many banks are UNSOPHISTICATED in forecasting and have been listening to the talking heads on TV and the desperate hope that inflation will decline while ignoring Ukraine entirely. Get that wrong – and you will NOT survive.

I strongly urge small banks to take our business services for access to real forecasting that is not biased or tarnished by human opinion with the two most dangerous words in forecasting:

COMMENT #1: Marty; Thank you so much for your warning at the WEC that we would now face a banking crisis with rising rates into 2024. You are always so far ahead of the pack. Live forever – please!

KQ

REPLY #1: Thank you, but that would sentence me to perpetual taxation indefinitely. No thanks.

COMMENT #2: Hello. I read your FREE blog because I am poor. Would you please stop posting PRIVATE stuff and post stuff that us peons can read?

Thank you kindly.

Ms. Terri

REPLY #2: My concern is since we forecast this last year, they will only blame me. That blog is only $15 a month, but it is blocked by Google so it is more free speech if you get my drift. I simple MUST be guarded in what I say publicly because they simply always view me as having too much influence.

I will offer this recommendation (publicly) for my ear is turning red from all the phone calls. As for the Biden Administration, if they DO NOT heed my warning, our forecast will be devastating. The Biden Administration MUST stand behind ALL deposits – not the $250,000 FDIC limit. If they do not, small businesses will pul; excess cash from banks, switch to 30-day T-Bills at a brokerage house, and say screw the FDIC and the Biden Administration’s anti-rich (small business which employs 70% of the workforce).

The compromise here is that we need a shotgun wedding where a larger bank takes over SVB at the raw price of the deposits. The shareholder loses, but ALL depositors are covered. Any value of the shares should be attributed to tangible assets only, not goodwill. You will penalize your “hated rich” and even the small businesses will be saved. If not, you will wipe out numerous businesses that cannot even pay employees. That will set off a contagion as you try to uphold your hatred of the “rich” while you pour money into the most corrupt government in the world at the real expense of taxpayers.

Of course, SVB can simply declare they “identify” as a Ukrainian Bank and then everything would be covered right down to the pensions of the CEO.

Posted originally on the CTH on March 12, 2023 | Sundance

BREAKING NEWS – The U.S. Treasury, Federal Reserve Board, FDIC and Joe Biden collectively announce that *all* depositors with Silicon Valley Bank (SVB) will have access to their funds – regardless of amount deposited. Also, all senior bank management has been terminated.

This announced action appears to cover those under FDIC protection ($250k or less) and those above FDIC protection (deposits greater than $250k). The only vulnerability is that SVB “shareholders and certain unsecured debtholders will not be protected.”

WASHINGTON DC – The following statement was released by Secretary of the Treasury Janet L. Yellen, Federal Reserve Board Chair Jerome H. Powell, and FDIC Chairman Martin J. Gruenberg:

Today we are taking decisive actions to protect the U.S. economy by strengthening public confidence in our banking system. This step will ensure that the U.S. banking system continues to perform its vital roles of protecting deposits and providing access to credit to households and businesses in a manner that promotes strong and sustainable economic growth.

After receiving a recommendation from the boards of the FDIC and the Federal Reserve, and consulting with the President, Secretary Yellen approved actions enabling the FDIC to complete its resolution of Silicon Valley Bank, Santa Clara, California, in a manner that fully protects all depositors. Depositors will have access to all of their money starting Monday, March 13. No losses associated with the resolution of Silicon Valley Bank will be borne by the taxpayer.

We are also announcing a similar systemic risk exception for Signature Bank, New York, New York, which was closed today by its state chartering authority. All depositors of this institution will be made whole. As with the resolution of Silicon Valley Bank, no losses will be borne by the taxpayer.

Shareholders and certain unsecured debtholders will not be protected. Senior management has also been removed. Any losses to the Deposit Insurance Fund to support uninsured depositors will be recovered by a special assessment on banks, as required by law.

Finally, the Federal Reserve Board on Sunday announced it will make available additional funding to eligible depository institutions to help assure banks have the ability to meet the needs of all their depositors.

The U.S. banking system remains resilient and on a solid foundation, in large part due to reforms that were made after the financial crisis that ensured better safeguards for the banking industry. Those reforms combined with today’s actions demonstrate our commitment to take the necessary steps to ensure that depositors’ savings remain safe. (LINK)

Will this action help stop any contagion related to California’s largest bank?

…The odds are, yes.

Despite Friday’s action to stop trading of FRB, with this action, I doubt First Republic Bank (FRB) is now at risk.

Posted originally on the CTH on February 3, 2023 | Sundance

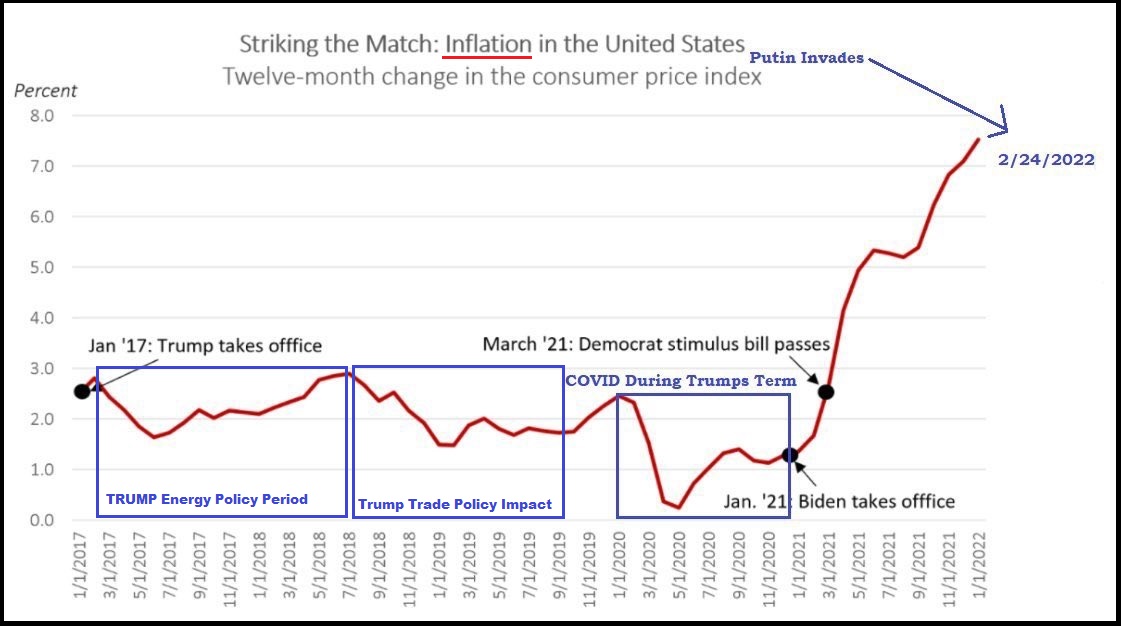

Not only does the buck not stop with Biden, the installed occupant of the White House refuses to admit the buck even started with him. It did!

During remarks to the press today, even Brian Deese looked stunned as Joe Biden incredulously claimed he didn’t cause the rampant inflation that is crushing middle class Americans. Oh, he started it alright…. He not only started it, but he also created it.

The combination of the January 2021 immediate move to block any domestic energy development, in combination with the April 2021 unneeded explosion of deficit spending triggered both a supply side and demand side inflationary impact; with the former continuing to put massive upward pressure on prices still. WATCH:

The lies from the lying, liar who lies, just flow so easily from his mouth.

Fox Business is reporting that economic conditions are much worse than you are being told. Unfortunately, this is the conclusion when you have ZERO understanding of the historical trends and economic conditions. It is true that the shortages of COVID have caused prices to rise faster than economic growth and most incomes. Therefore, they conclude that our standard of living has been rapidly declining. The number reveals that more than one-third of all U.S. young adults are being supported in part by their parents. Thanks to COVID, this disrupted society far greater than anyone is reporting. In addition to the shortages because of the lockdowns, by the end of 2020, more than half of young adults in America were living with one or both parents. That statistic actually exceeded the record high of the Great Depression.

Here is the worst part of this analysis. Many are jumping on the bandwagon claiming that the decline in real disposable income has been the largest since 1932 and therefore, this is a warning sign of a Great Depression is coming. They seem to be focused on the fact that the GDP report showed a significant decline in real disposable income, which fell over $1 trillion in 2022. Now let’s look closer!

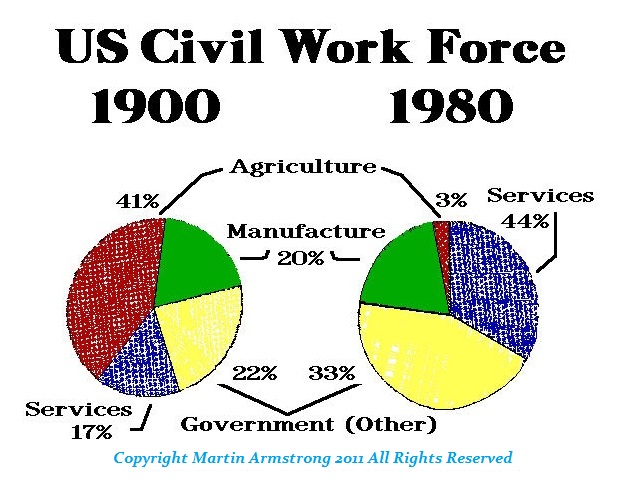

First of all, the entire reason why unemployment rise to 25% during the latter part of the Great Depression was the Dust Bowl. Why? At that time, about 40% of the civil workforce was still agrarian. The Dust Bowl meant job loss. If you could not even plant crops, there was no need for people to pick crops.

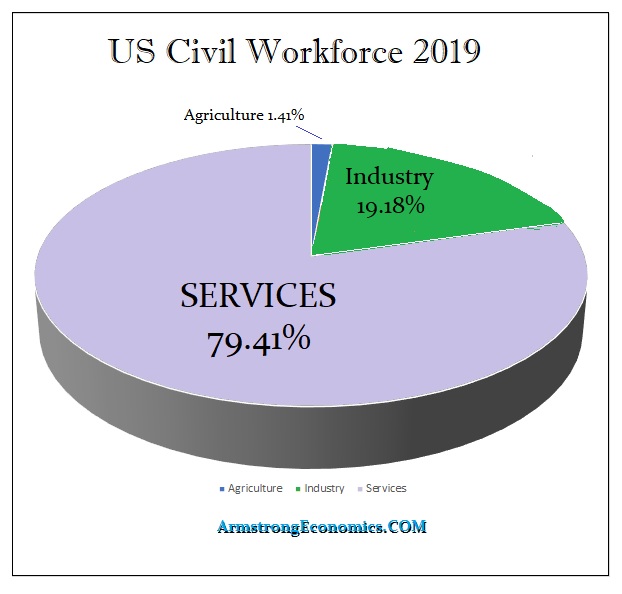

Service during the Great Depression accounted for 17% of the workforce compared to 44%+ today. Government, federal, state, and local, was 22% of the civil workforce during the Great Depression compared to 33% by 1980. Things have continued to evolve and by 2019, services represent 79.41%. Agriculture is now a tiny fraction of what it once was – 1.41%.

In the USA, at the state level, their share of the civil workforce varies greatly. Florida is at about 11.3% compared to New Mexico which is 22.5% – a government employee’s paradise. The lowest is Michigan at 10.1%.

During the Great Depression, the entire reason for the collapse in disposable income was the collapse in agriculture which created a collapse in income due to massive unemployment. That is totally different from the crisis we have today.

Here we have rising prices due to shortages and then central banks raising interest rates in a fool’s quest to stop inflation when it is not based on speculation. Moreover, the biggest borrower is the government, and rising interest rates will only increase their exposure to keep rolling over the debt. Therefore, governments have been borrowing year after year. What happens when the public no longer buys their debt? Real disposable income has been collapsing for completely different reasons since 1932. Here we have the costs of everything rising and then these people want war with Russia and China. Every war since the start of recorded history has resulted in inflation. Add to this, the total insanity of trying to end climate change by outlawing fossil fuels at a time when the climate is prone to getting colder.

We are already witnessing riots around the world BECAUSE of inflation. During the Great Depression, people were suffering from DEFLATION. So comparing just that statistic of a decline in personal income and projecting we now face a Great Depression, does not even qualify to be classified as analysis. That is no different from someone warning that carrots must be lethal because everyone who has ever eaten a carrot has obviously died.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America