Today is a very good day. Despite the professional punditry and their doomsayer predictions of Trump tariffs driving up costs for consumers, exactly the opposite is happening.

Despite large growth in the Main Street USA economy; and despite large wage gains by U.S. blue-collar workers; inflation remains low and mysteriously detached from the Fed monetary policy.

WASHINGTON (Reuters) – U.S. inflation was much weaker than initially thought in the first quarter amid a sharp slowdown in domestic demand, which could cast doubts on the Federal Reserve’s view that the benign price pressures were largely because of temporary factors.

The personal consumption expenditures (PCE) price index excluding the volatile food and energy components increased at a 1.0% rate last quarter, the government said. The so-called core PCE price index, which is the Fed’s preferred inflation measure, was previously reported to have risen at a 1.3% pace.

The increase last quarter was the smallest in four years and pushed inflation further below the Fed’s 2% target. (read more)

They just don’t get it. For over three years CTH has been explaining how President Trump’s maganomic policy will reverse three decades of stagnant Main Street economic growth. Today the Bureau of Economic Analysis (BEA) once again confirms our earlier predictions, and releases the data showing inflation is essentially nonexistent.

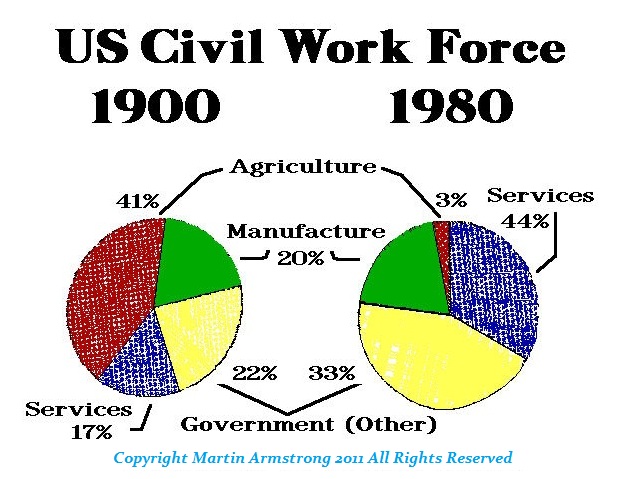

Since the mid-to-late 1980’s the U.S. economy split into two divergent economic engines. One traditional engine powered by Main Street, and a second engine powered by Wall Street. For thirty-plus years the distance between those engines was growing as federal monetary policy provided low interest rate support for investment, but the end destination for the investment was NOT in the U.S. [Hence, globalism]

For more than 30 years monetary policy has been driven by Wall Street influence. FED interest rates made borrowing cheap, but the money -the actual investment itself- flowed out of the United States. The end product from the investment, steered by multinationals, created products overseas. Within this flow of capital there was no benefit to Main Street.

President Trump’s America-First policy has reversed the dynamic. As a result of his focus and demand, the end product(s) from capital investment are now here in the U.S.A.

The MOUSE is money or investment. The CHEESE is end products, manufactured stuff.

Rather than beg the Wall Street investment mouse to change direction in the manufacturing maze, president Trump has simply moved the cheese to Main Street. The mouse’s travel changed accordingly.

(BEA Table 4 – pdf)

(BEA Table 4 – pdf)

The price index for gross domestic purchases increased 0.7 percent in the first quarter, compared with an increase of 1.7 percent in the fourth quarter (table 4). The PCE price index increased 0.4 percent, compared with an increase of 1.5 percent. Excluding food and energy prices, the PCE price index increased 1.0 percent, compared with an increase of 1.8 percent. (link)

As companies reevaluate the best place for investment (highest return), and they see that Trump’s policies (corp taxes, tariffs, material and labor costs) focus on greatest benefit being inside the U.S, then companies return to Main Street. This is what has been happening since Trump took office; and it continues through today.

The prices of highly consumable goods (food, fuel, energy) is kept low by Trump policies that increase energy production and return a genuine supply-side dynamic to domestic production prices. [The battle with Big AG]

Meanwhile multinationals, and some foreign governments, fight to keep their footing abroad (original investment) by keeping down the price of durable goods manufactured overseas. This is done by increase productivity, adjusted supply chains and retention incentives afforded by the benefiting nation. This is done to offset Trump tariffs which are designed to influence a shift in the manufacturing process.

The end result of both production dynamics, domestic and abroad, is low inflation.

This price dynamic is happening at the location of output, internally to the operations that are determining the output price, based on their determination of what U.S. market prices will absorb.

Key Point – The pricing is NOT a result of decision-making on new investment; and therefore the pricing dynamic is not able to be impacted or influenced by FED monetary policy.

Only when the majority of manufacturing investment fully returns to the U.S. will FED policy have any significant bearing on manufacturing prices. This is the parity point where Main Street’s economic engine is recoupled to inflation.

There was 30 years of distance in the FED disconnect, and it will take more than a few years for the recoupling of Main Street to FED monetary policy.

This dynamic is the basic thesis behind THE THEORY HERE.

DECEMBER 2016 – […] Additionally, inflation on durable goods will be insignificant – even as international trade agreements are renegotiated. Why? Simply because the originating nations of those products are going to go through the same type of economic detachment described above.

Those global manufacturing economies will first respond to any increases in export costs (tariffs etc.), by driving their own productivity higher as an initial offset, in the same manner American workers went through in the past two decades. The manufacturing enterprise and the financial sector remain focused on the pricing.

♦ Inflation on imported durable goods sold in America, while necessary, will ultimately be minimal during this initial period; and expand more significantly as time progresses and off-shored manufacturing finds less and less ways to be productive. Over time, durable good prices will increase – but it will come much later.

♦ Inflation on domestic consumable goods ‘may‘ indeed rise at a faster pace. However, it can be expected that U.S. wage rates will respond faster, naturally faster, than any monetary policy because inflation on fast-turn consumable goods become re-coupled to the ability of wage rates to afford them.

The fiscal policy impact lag, caused by the distance between federal monetary action and the domestic Main Street economy, will now work in our favor. That is, in favor of the middle-class.

Within the aforementioned distance between “X” and “Y”, a result of three decades traveled by two divergent economic engines, is our new economic dimension….