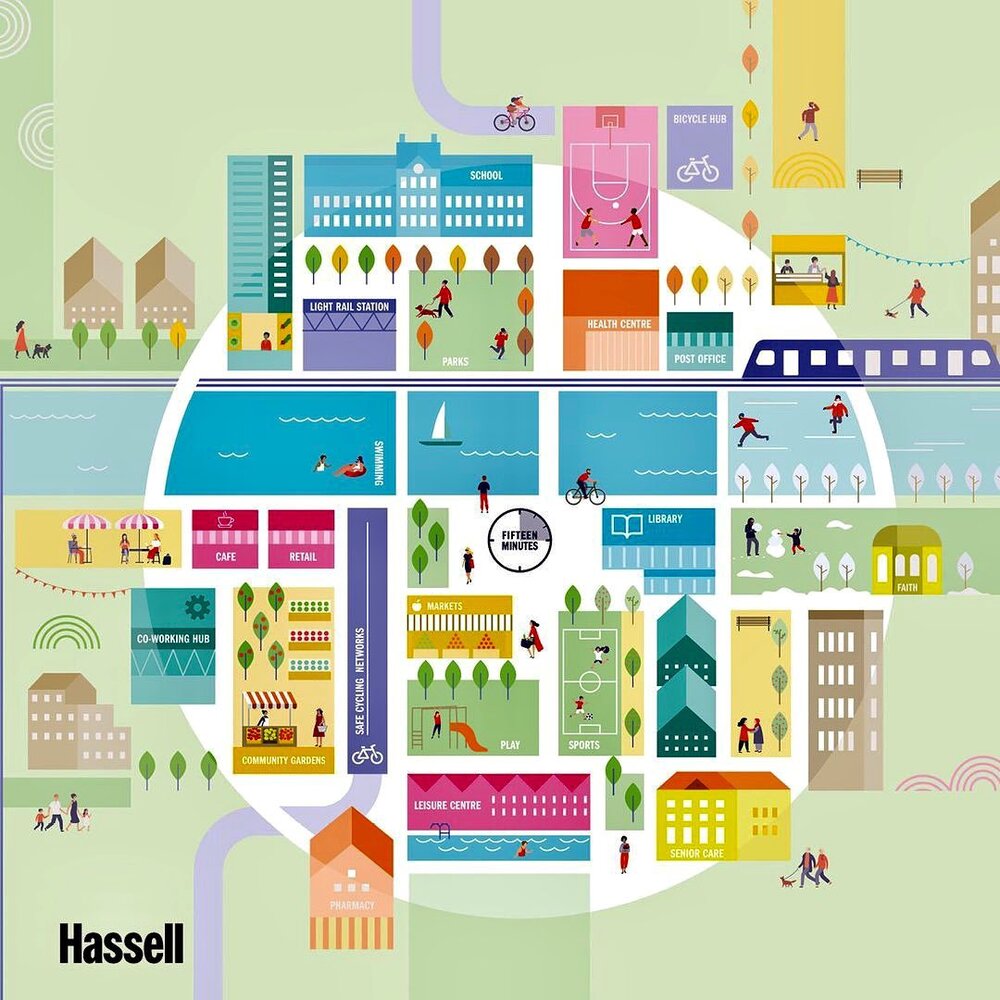

“Make no mistake, it’s not about your convenience, and it’s not about saving the planet. It will be a complete impoverishment and enslavement of all the people,” German MEP Christine Anderson said regarding the push for 15-minute cities. She’s right. The 15-minute city is marketed as a futuristic town where everyone will live within 15 minutes of essential services. They are marketing these cities as affordable, convenient, and virtuous as they combat climate change. The truth of the matter is that these cities are reminiscent of the Jewish ghettos during World War II or the Japanese internment camps in the US. They are designed to contain and control the people.

As Anderson said, governments can easily implement climate emergency lockdowns. “The looming existential threat of climate change and worsening income inequality require us to urgently rethink our existing cities, and rapid urbanization makes it imperative that we create a new and better city-building template for cities to house future city dwellers,” the website for the enclosures states.

Since governments have made homeownership completely unaffordable to many, they are marketing “accessory dwelling units” (ADUs) under 1,000 sq ft as a viable alternative to housing. They claim this will solve homelessness as well since we will all be completely equal. YOU WILL OWN NOTHING AND BE HAPPY.

The government will choose where we live and how we live. The globalists want us to rely solely on government, a government that they hope will be a united one-world unit. The majority will be the “have-nots.” The few elites at the top will prosper on their puppets in their doll house towns who they can play with like Sim characters. My computer model has been stating that the globalists will fail, but it will take a revolution.

Posted originally on the CTH on January 5, 2023 | Sundance

That slow grinding creak you hear in the background; that’s the U.S. economic engine running without oil and beginning that slowdown phase just before it stutters and stalls completely. Alas, the pretending continues…

As noted by the Wall Street Journal, an economic gaslighting institution with a central mission to maintain pretenses, “business surveys show U.S. factory activity declined in December, the Institute for Supply Management and S&P Global both said this week. Separately, S&P Global said Thursday that U.S. services-sector businesses reported a decline in output for the third month running in December.” This comes as “U.S. imports dropped more, by 6.4% on the month, as Americans cut back on holiday-related purchases, including items from other countries such as computers and autos.”

Keep in mind, November retail sales—which included consumer spending at stores, online and at restaurants—fell 0.6% from the prior month for their biggest decline of 2022, according to the Commerce Department. Manufacturing output declined in November as well, the Fed reported, while U.S. home sales fell for a record 10th straight month.

Into this mix of economic metrics, driven by a collapse in disposable consumer income and high energy prices, now we begin to see the number one business expense being curtailed.

(Market Watch) […] Amazon.com Inc layoffs will affect more than 18,000 employees, the highest reduction tally revealed in the past year at a major technology company as the industry pares back amid economic uncertainty.

The Seattle-based company in November said that it was beginning layoffs among its corporate workforce, with cuts concentrated on its devices business, recruiting and retail operations. At the time, The Wall Street Journal reported the cuts would total about 10,000 people. Thousands of those cuts began last year. (more)

Amazon is not alone, “Vimeo said Wednesday that it will cut its workforce by 11% as part of a broader effort to reduce costs, citing deteriorating economic conditions” (link). Additionally, Salesforce Inc. is laying off 10% of its workforce and reducing its office space in certain markets, extending a brutal period for tech job cuts into the new year.”

We can anticipate more reports like this from Reuters, “Samsung Electronics Co Ltd’s quarterly profit will likely plunge 58% to its lowest in six years as a global economic downturn saps demand for electronic devices and clouds the outlook for the memory chip industry. With consumers and businesses reducing spending and investment in the face of high inflation and climbing interest rates, smartphone makers and other clients held back memory chip orders, while smartphones sold for less as demand suffered, analysts said.”

Electronics, cars, furniture, durable goods of all types and varieties are plummeting in sales. Consumers are being squeezed by inflation, housing, energy and food costs, and spending priorities are being reevaluated yet again. Compare the impact on ‘real wages’ -vs- the 2007/2008 economic crisis.

From a purely fraudulent accounting perspective, however, the drop in U.S. imports will help boost calculations of U.S. economic growth in the fourth quarter because trade deficits subtract from overall output, or gross domestic product.

U.S. consumers not purchasing imported goods makes the health of the U.S. economy look less bad; but it’s an illusion akin to smiles in the bread lines.

In other economic news, I did some real estate analysis over the past several days and it’s safe to say there is a steep downward trajectory in the data I use. Again, home values are nuanced on a regional level, but my model is pretty close in averaging.

If buyers do not absorb the seller’s loss in equity (which no one should ever do), in my SWFL area a $450k home listing is going to sell around $380k at the high side (actual value based on economic indicators and buyer ability). That rough estimate, while slightly offset due to general inflation, should trend nationally over the next 12 to 18 months. That means macro home prices dropping around 15 to 20% nationally over the next 12 months.

If you are a home buyer, put your offers around 15 to 20% below current asking price without any emotional attachment to it. Don’t flinch, remain ambivalent and walk away if refused. The recovery to current price will take around a decade. If you are a seller and get an offer within -10% of asking, consider yourself lucky and jump on it.

Posted originally on the CTH on December 2, 2022 | Sundance

There’s a disconnect in the Main Street data that is perplexing from the standpoint of traditional economic and labor analysis.

There have been significant layoffs in the labor market as the result of diminished consumer spending activity. However, the Bureau of Labor and Statistics (BLS) is reporting a hotter than expected 263,000 new jobs in November [DATA HERE].

There were declines in jobs within the retail sector [-30,000 in Nov, -62,000 since August] and declines in warehousing and transportation [-15, 000 in November, -30,000 since July], which would indicate the outcome of lowered consumer spending on goods, or at least a change in consumer spending priorities.

Simultaneously, there were significant increases in jobs for leisure and hospitality [+88,000 in Nov], with the majority of those gains in food service and drinking. However, that sector is still lower than the pre-pandemic by -980,000 jobs. Also note people are not attending events with high ticket costs, the performing arts and spectator sports segment dropped 7,000 jobs [Table B-1]

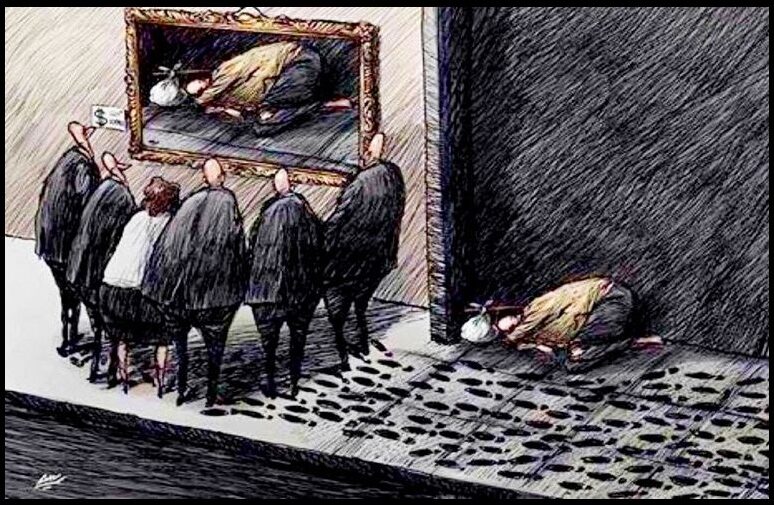

Overall, if you were to look at the macro level jobs report, anything attached to the traditional spending of durable goods (retail stores) is declining. However, the jobs related to the service or life experience are growing. Oddly, and perhaps creepily, this dynamic falls in line with the ‘you will own nothing and be happy‘ cliche’ that has been oft spoken about the new post pandemic ‘Build Back Better‘ economy as espoused by the World Economic Forum.

Job gains in the infrastructure of life such as, building and construction, as well as the labor sector associated with skilled domestic service trades like plumbing, electricians, maintenance, etc are continuing to hold stable. The major shift in the labor market surrounds the buying of durable goods which has disappeared along with the disappearance of discretionary income. Which brings us to the wage portion of the BLS report.

Wage growth was a very high 0.6% for November and brings the annual rate of wage growth to 5.1%. This outcome is almost certainly an outcome of workers demanding higher pay to cope with inflation, and employers needing to raise their wage rates in order to retain employees.

We also see an increase in the number of workers holding multiple jobs, as individuals are taking second jobs to cope with massive price increases in housing, food, fuel and energy. As noted within the BLS data:

“In November, the average workweek for all employees on private nonfarm payrolls declined by 0.1 hour to 34.4 hours. In manufacturing, the average workweek for all employees decreased by 0.2 hour to 40.2 hours, and overtime declined by 0.1 hour to 3.1 hours. The average workweek for production and nonsupervisory employees on private nonfarm payrolls decreased by 0.1 hour to 33.9 hours.”

Fewer people are working, but more jobs are being worked – with lowered hours.

Higher wages are good; however, higher wages lead to higher prices for goods and services; which drives inflation higher, which creates the need for higher wages. It’s an upward pressure spiral.

The supply side pressure on inflation, almost exclusively created by the BBB energy policy, shows absolutely no sign of lessening, despite the drop in demand for domestically produced finished consumer goods which has lowered overall industrial demand for energy.

The Build Back Better energy driven policy changes are creating very weird economic outcomes.

Prices are rising. Consumers are squeezed. Jobs attached to spending on goods are declining. Jobs attached to life experience and services expanding.

Ex.1 If you are working two jobs, now you might not have time to mow your grass – so you hire a lawn service. The lawn service guys are charging more because the gasoline and business costs are higher…. which means you need to work a little longer at the second job to pay for the lawn service you don’t have time to do on your own because you need to work the second job. That’s the dynamic we are seeing in the quantification of labor and job growth.

Ex.2 If you are working two jobs, you might not be cooking as much at home. So, you grab dinner/lunch away from home. The restaurants are charging more because the business costs are higher…. which means you need to work a little longer, ask for higher wages, in order to offset the time you don’t have to eat lunch/dinner at home.

This conflicting duality is what I always called the “serfesque driven economy.” It is an outcome of erosion of the middle-class. A status of individuality where your desires for life experience determine the need for your income.

You don’t own a car, you Uber. You don’t own a house, you rent. You don’t need a kitchen, you eat out. Things seem ok, but you eventually become a serf to the people who control transportation costs, housing costs, food costs, etc. Ultimately you have no control over the time you want to spend in enjoyment, because you don’t own the mechanisms of your life and need to work in order to afford maintaining the costs. It’s a weird mental exercise.

There is a real outcome in this dynamic where the wealth gap increases.

Even Jeffrey David Sachs, an American economist, has come out and said on TV, as the journalists go nuts, that the US destroyed Nord Stream. Everyone I have spoken to from around the world, including high levels, all believes the US did this and I know there is a think tank that has recommended the US now take out the South Stream through Turkey. This was a formal act of war. Russia sees it that way, as does most of the world. This is an attempt to destroy the economy of Russia where energy accounts for 50% of its GDP. The Biden Administration poses the greatest threat to the United States for this reckless behavior. I’m sure I will get the hate mail from the Democrats. At least lower your COVID mask, and take a deep breath just for once.

QUESTION #1: I live in the US. When the sovereign debt explodes, and I will “own nothing “, does that mean that any car, house or property that has a loan on it will become the property of the bank and or government? Does it mean property that is paid off and I hold the title or deed will be taken from me and I will have to pay “rent” to hold on to it? Please answer by my email or on one of your blogs.

Thanks for all you do.

MH

QUESTION #2: Would you ever consider running for politics? Your experience towers over everyone out there.

BB

ANSWER: No, I am not interested in getting into politics. I have always preferred to be standing behind the curtain. If I ever stepped in front, they would quickly figure out a way I could commit suicide with a remote rifle 100 yards away and you can bet the media will say absolutely!

Now insofar as the sovereign debt default, we are looking at governments collapsing which will take down banks that must retain reserves in government bonds. Klaud Schwab is an academic. He has ZERO real-world experience. His ideas will collapse just like Marx for the one element both ignore is human nature. It cost over 200 million lives for Marx to get his theory in place. Communism collapsed because without curiosity and freedom to explore, talk, and think, all advancement of society comes to an end.

Schwab’s idea will fail because the setup is different this time. Marxism succeeded because in Russia serfdom ended only during the 1860s. Therefore, the common people DID NOT own anything and it made sense to raid the rich. This time, people own houses and cars, and they save with pensions and to help their children. This time the common people would have to surrender all their assets so Schwab’s Marxist theories can be implemented.

It is a whole different board game this time around. Our computer has NEVER been beaten by anyone, even me. It sees the future because it is monitoring everything. So while people argue over what they “think” will happen, Socrates just plugs away and lacks that human emotion that interferes with objectivity.

Posted originally on the conservative tree house on October 2, 2022 | Sundance

During his weekly monologue Neil Oliver turns his attention to the “Big Club,” the bankers. WATCH:

[Transcript] – I want to tell you a story about money. To be more specific I want to tell you where money comes from. The truth, of which most people are unaware, is that money is created out of thin air. Furthermore, every single pound, dollar, euro, yen and all the rest is created out of thin air by unelected, unaccountable private business people who conduct their meetings in total secrecy and profit always from their actions.

Let’s imagine you want to borrow 200k to buy a house. When you go to the bank and ask for that money, the banker doesn’t give you existing funds, cash from a drawer for instance. Instead, he creates that 200k out of nowhere – money that previously did not exist. That money is not backed by anything real – no gold or anything else. It is conjured out of nowhere and exists now only because the banker says it does. He then says you have to pay him back the 200k plus – let’s say for the sake of example – another 200k in interest.

He is allowed to credit your account with money that did not exist until you asked for it and he pressed digits on a keyboard … and then he invites himself to charge you whatever interest he wants on that previously non-existent sum. Talk about a fool-proof way to make money. This is how all money is created in our world and this is why so many people are made to live crippled by debt. Every year the British people pay tens of billions of pounds to private bankers as interest on something that DID NOT EXIST IN THE FIRST PLACE.

How could I be sure, but I suspect that if you or I were to attempt something similar, we would be thrown in jail before our feet touched the ground.

William Paterson, cofounder of the Bank of England in 1694, noted that:

“… the Bank hath benefit of interest on all moneys which it creates out of nothing.”

1694 … that’s at least as long as this has been going on … how long we’ve been submitting to debt created by a handful of rich people to keep everyone else under their control.

The Bank of England is technically owned by the British government, and so, notionally, by the British people. The fact of the matter however is that the government does not tell the Bank what to do. Like all central banks, the Bank of England is answerable instead to an entity called the Bank for International Settlements. The BIS is run by more unelected, unaccountable, secretive people over which we the British – like all people in the world – have no say and no control. Most people have never even heard of the Bank for International Settlements, but it is housed in a great glass tower in Basle, in Switzerland.

It is the BIS that controls the making and flow of well over 95 percent of the world’s money supply – via, to name but a few, the Bank of England, the US Federal Reserve, the People’s Bank of China, the Central Bank of the Russian Federation and the European Central Bank. It also influences a host of other smaller central banks including in unstable and failed states like Afghanistan and Libya.

We need an honest and open conversation about banks – all banks – and about another way of doing things – a way of potentially freeing the people of the world from the yoke of debt placed across their shoulders by secretive, unaccountable, profiteering private bankers. It may or not offer the solution to our woes, but I believe it is time now to talk about it and, more importantly, to invite more people to understand what banks actually do and how they do it.

If you don’t trust me, how about Thomas Jefferson, founding father and third president of the US, who said:

“I believe that banking institutions are more dangerous to our liberties than standing armies. If the American people ever allow banks to control the issue of their currency … they will deprive people of all property until their children wake up homeless on the continent their fathers conquered. The issuing power should be taken from the banks and restored to the people, to whom it properly belongs.”

The Federal Reserve in the US was created at Christmas time 1913 – when most members were away for the holidays. By means of the Federal Reserve Act, all control over money creation was removed from Congress and given to the Federal Reserve Corporation, a private company controlled by bankers – all this despite Article 1 of the US constitution which declares:

“Congress shall have the Power to Coin Money and regulate the Value thereof.”

Federal was added to the name to trick the people into thinking they, via Congress, were in control.

Not anymore, not since that Christmas of 1913. The Fed is a private business corporation.

Or what about the words of Henry Ford, who transformed the car industry, who said:

“It is well enough that the people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning.”

The private bankers would have us believe their way of doing business, of making money, is the only way.

So here, let me tell you an astonishing bit of forgotten history – so forgotten you’d be forgiven for thinking some people don’t want us to remember.

Back in August 1914, with the First World War looming, people feared the future. More and more were converting their bank notes – bits of paper – into gold sovereigns and half-sovereigns, as was their right in those days when Britain was on the so-called gold standard. But by 1914, the Bank of England had already been involved in dodgy dealings, creating money out of nothing – and there were far more bank notes in circulation than there was gold in the vaults to honour them.

If everyone tried to get their gold out at once, such a ‘run on the bank’ would have been catastrophic. At a stroke, Britain would have lost its ability to pay for the upcoming war.

The Bankers ran for help to the government and to the Chancellor David Lloyd George. The August Bank holiday was extended by three days, an Act was rushed through parliament and when the banks reopened, people were offered a new kind of Treasury note – issued not by the bank but by HM Treasury, in lieu of their gold. Since the first batches bore the signature of Sir John Bradbury, the then Permanent Secretary to the Treasury, the public nicknamed them Bradbury Pounds. Because each was backed by the wealth of the nation, the familiar strap line … about a promise to pay the bearer on demand … was unnecessary and therefore absent entirely.

The people accepted the Bradbury Pounds, trusted them on sight as cash they could see and hold and spend as they liked, with perfect confidence, and the banks were saved from certain collapse.

It was sovereign money – underwritten by the wealth of the nation and, perhaps most valuable of all, by the creativity and potential of the people of that nation. Unlike the money created out of nowhere by private bankers it was interest free and unburdened by debt.

Britons were briefly beyond the clutches of private bankers. But their reprieve didn’t last long. Having been spared the consequences of creating money out of nothing, those bankers were soon back at the Treasury door – demanding the State stop issuing debt-free money. The War was up and running and as is true of all wars, there was a killing to be made, in among all the killing.

The war must be run, those bankers said, only on money borrowed from them and repayable with interest – three and a half percent interest, as it happened. By the end of the First World War, Britain’s national debt had ballooned from 600 million in 1914, to 7 billion pounds. In 1914, remember, a pound was worth 122 pounds in today’s money. That’s inflation for you.

This is no longer the world of 1914. Any solution for 2022 must be made by us … for us, in the world of today.

Henry Kissinger said:

“Who controls the food supply controls the people; who controls the energy can control whole continents; who controls money can control the world.”

Right now, all around us, the people are being nudged ever closer to digital enslavement by secretive, unaccountable bankers.

Right now, control of energy by others we do not know is marching us towards the coldest, hungriest winter many can remember. Right now, is the time to take back control of money – its creation, its value and its flow. By so doing, we can begin the task of regaining control of our world. (link)

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America