QUESTION: Hi Martin! Would you please clarify the difference between an economic collapse and the currency crisis? Are they one and the same?

In one of the pro-private blogs you mentioned a collapse in government debt before the slingshot move. Would that mean that my pension investment plan may disappear before the currency crisis and the slingshot move you have been talking about?

I just would like to know while I have time to pay off my home.

Thank you for all you do for us common folk.

Thank you

B

ANSWER: The volatility that surrounds a financial crisis depends upon the origin of the sector. When there is a crisis in confidence in the private sector, corporations or banks, the capital shifts and sells private assets and runs into government securities (bonds/notes), which we call the “Flight to Quality” that typically is used only in this context.

However, when capital realizes that the risk is on the government side, the Flight to Quality reverses and capital seeks the safety of the private sector. The decline in confidence in government will manifest in two primary manners. First, because capital responds in anticipation, we can find that markets move first based upon the perceived risk.

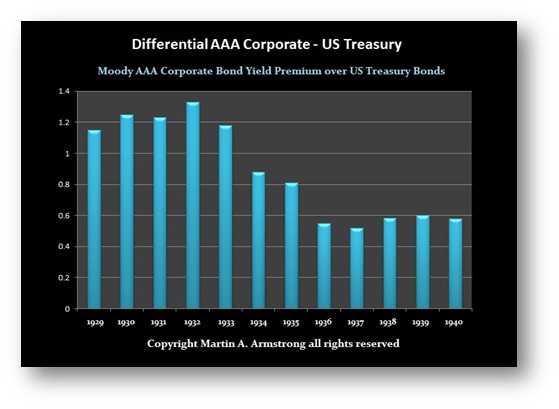

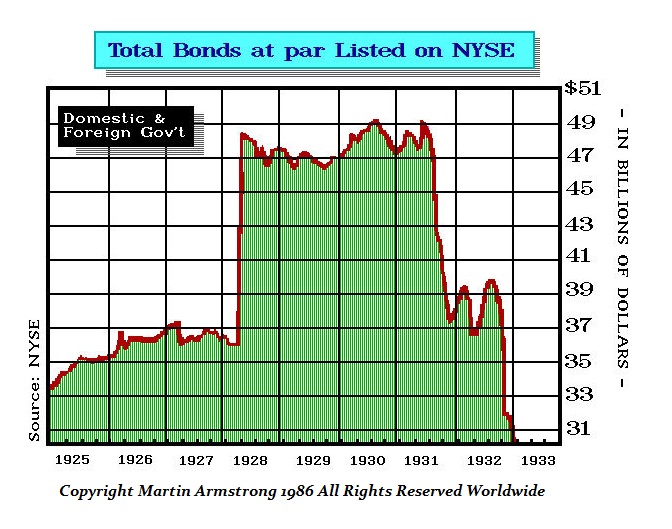

The spread between AAA Corporate bonds and those of the United States, initially rose in premium over the government when the perception was confined to the stock market crash. That dipped slightly in 1931 as all the foreign debt was going into default. It turned back up going into the final low in 1932. The Dow did drop nearly 50% at that time. The Dow closed 1931 at 77.90 and then fell to 40.56 in July 1932 for the low. Percentage-wise, that was a substantial decline in 7 months.

There were numerous foreign bonds that were trading on the New York Stock Exchange. When the Sovereign Debt Default of 1931 took place, the perception shifted to the point that it was then expected that the United States would default in some way because everyone else did. Then you see the spread between AAA corporate debt in the USA declined sharply against the federal debt levels.

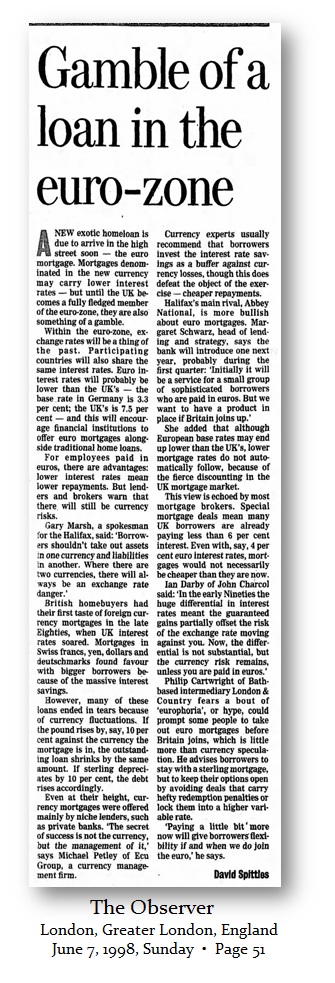

Now enters the nonsense of creating the euro. The promise was that creating the euro would make companies more competitive because there would be no more currency risk and they would all pay the same interest rates pointing to the dollar as a misrepresentation. The Observer in London, England, wrote on June 7th, 1998 (id/Page 51), “Within the euro-zone, exchange rates will be a thing of the past. Participating countries will also share the same interest rates. Euro interest rates will probably be lower than the UK’s – the base rate in Germany is 3.3 per cent; the UK’s is 7.5 per cent…”

Now enters the nonsense of creating the euro. The promise was that creating the euro would make companies more competitive because there would be no more currency risk and they would all pay the same interest rates pointing to the dollar as a misrepresentation. The Observer in London, England, wrote on June 7th, 1998 (id/Page 51), “Within the euro-zone, exchange rates will be a thing of the past. Participating countries will also share the same interest rates. Euro interest rates will probably be lower than the UK’s – the base rate in Germany is 3.3 per cent; the UK’s is 7.5 per cent…”

The fallacy of the entire euro project was the intentional lies that were spun just to sell the euro. Creating the euro was in effect a means of fixing the exchange rate as if they had returned to the days of Bretton Woods. However, even under Bretton Woods, despite the fact that the currencies were fixed, the volatility simply transferred to the debt market.

Under the Eurozone, Greece and others began to issue debt like it was going out of style because they were taking advantage of the stupidity of investors willing to buy debt believing that everyone would pay the same interest rates simply because they used the same currency.

There are many states that peg their currency to the US dollar. That does NOTmean that they will pay the same interest rates as the US government. That was NEVER true under Bretton Woods and within the United States, each of the 50 states pays according to its own credit risk.

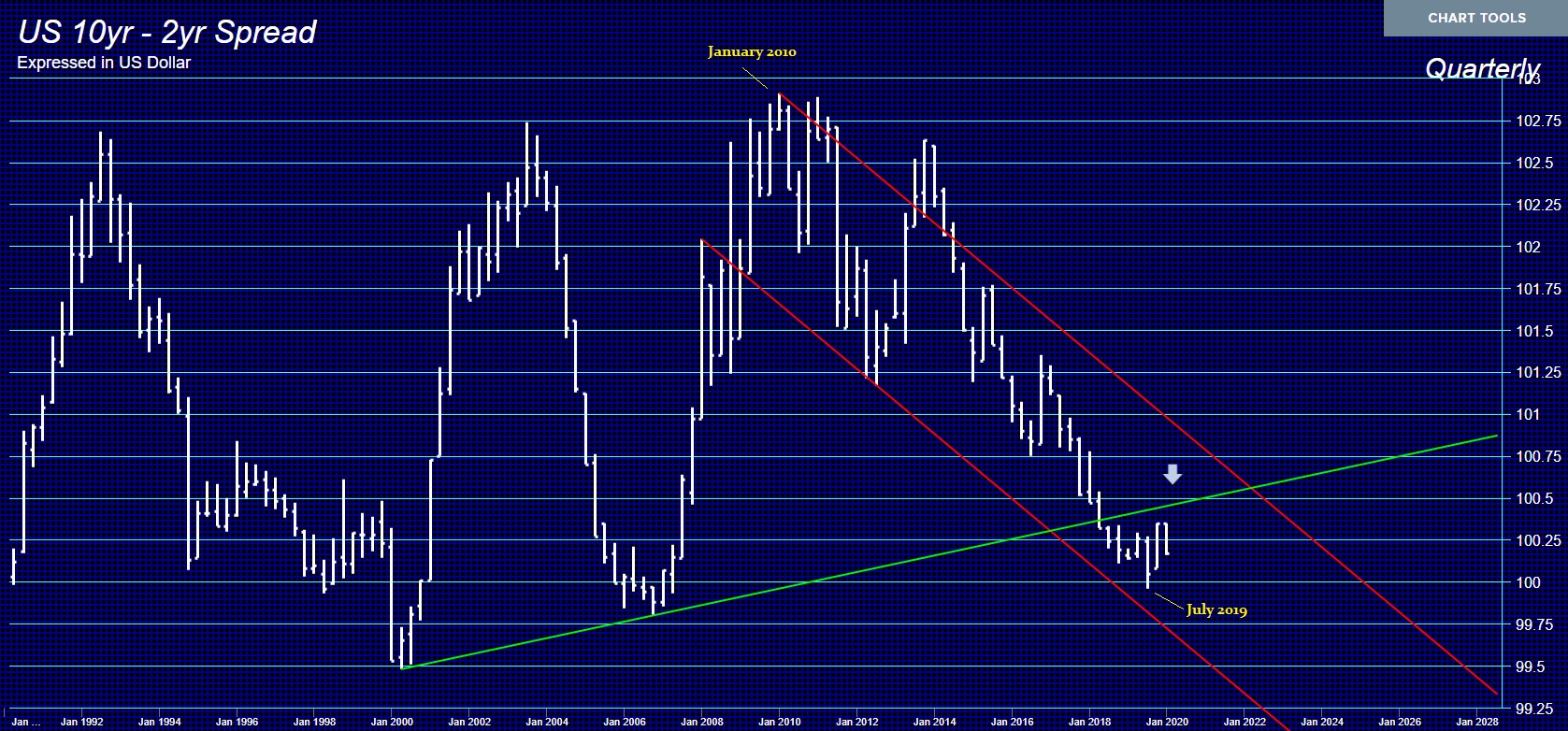

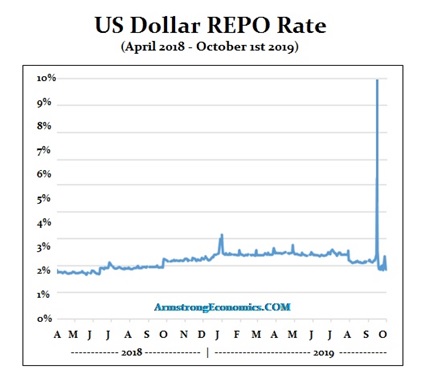

Hence, the crisis we face will be felt in the debt markets FIRST, which is why we have the Repo Crisisthat people are not paying attention to anymore. Therefore, your question of a collapse in government debt before the slingshot move means that “my pension investment plan may disappear before the currency crisis and the slingshot move you have been talking about.” It all depends upon the country you live in.

If you are in the United States, the debt crisis begins OUTSIDE the United States so the US market is the last to go into a bond crisis.