The Biden Administration is responding to the panic phone calls that their Marxist philosophy will bring down the entire financial system. My ear is red as can be. I have had enough of the phone calls today to last the balance of the month. Trying just to do the right thing! Three banks have effectively gone down in the week of March 6th, which our computer was targeting. There have been Silicon Vally Bank, Signature Bank, and Silvergat Bank.

The Regulators perhaps saw the handwriting on the wall. This NO BAILOUT claiming that no taxpayer money will be used for a bailout of their hated rich, how about just using the taxpayer’s money you are throwing down the train in Ukraine? Depositors in Signature and SVB they are now saying would be made whole. If they do not cover ALL deposits, the monumental banking failure will be catastrophic.

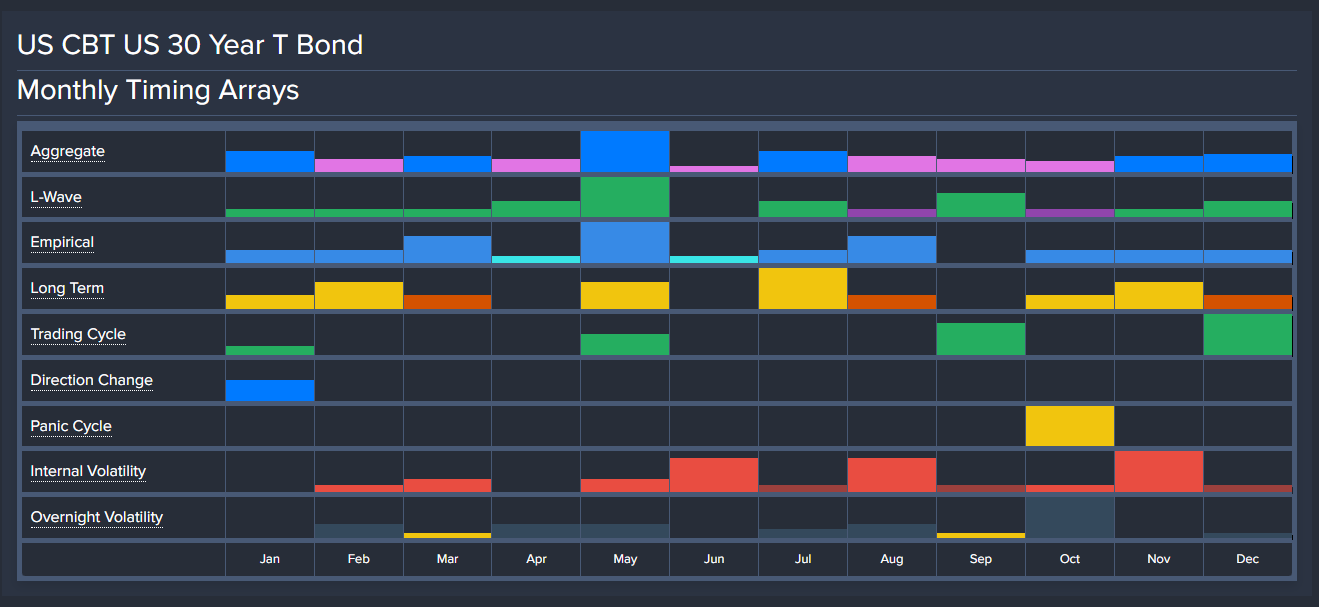

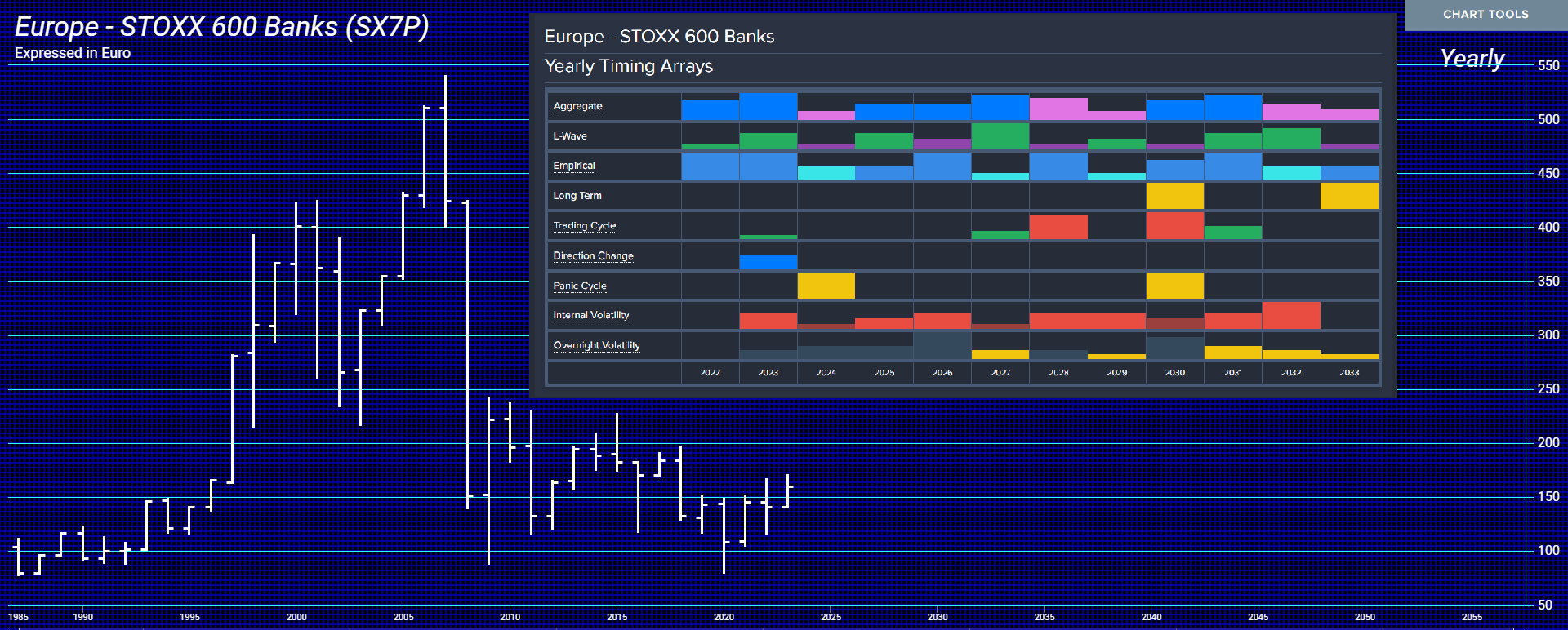

Our forecast for a Banking Crisis is by NO MEANS confined to the United States. It will be far worse in Europe. We can see our computer not only targeted 2023 for a key turning point with a Directional Change but a Panic Cycle next year in bank stocks, but interest rates will be rising higher as also the risk of banks and governments escalated especially when they insist on waging war against Russia.

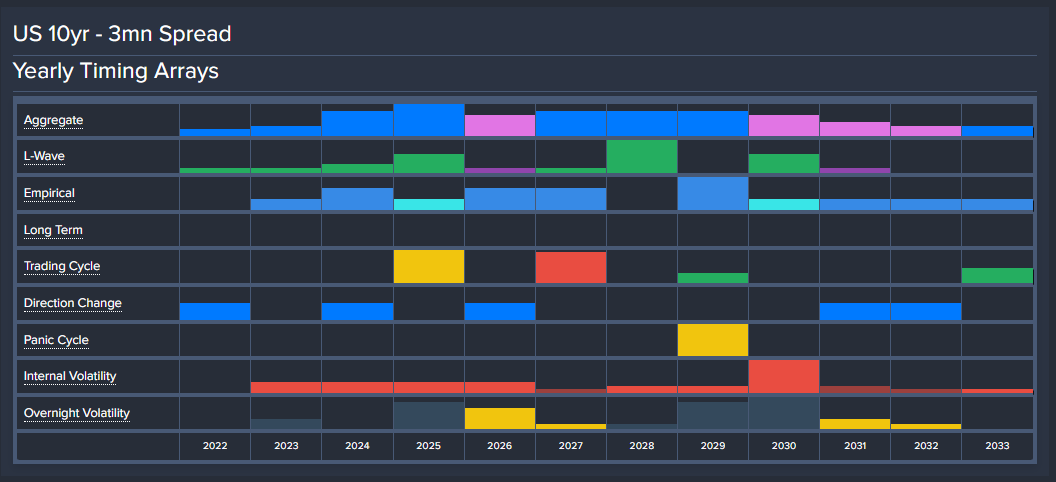

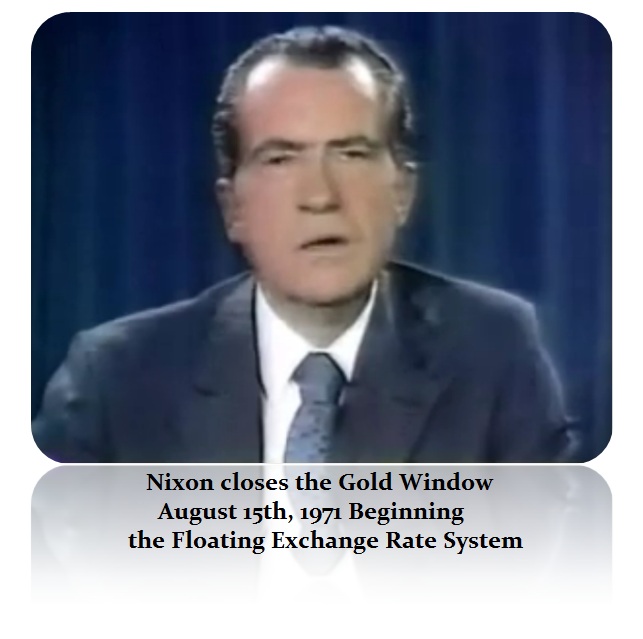

The yield curve is critical and we must understand that this insane war against Russia, even economically, will be a major financial disaster not much different from Vietnam which brought down Bretton Woods and forced Nixon to close the gold window on August 15th, 1971. It was that unrestrained spending directed by the Neocons. Then too, it was all about Russia they assumed was behind Vietnam.

Once more, the reckless spending on war promoted by the Neocons is undermining the entire economy. They have lost every war they have promoted – Vietnam, Afghanistan, Iraq, proposed Syria, Libya regime change, and now Ukraine. These people are never held accountable for all the devastation and the lives lost.

War is the primary driver of inflation and the central banks will not even address it for they do not want to “criticize” the Neocons. They might wake up with their dog’s head in the bed as in the Godfather. The central banks will NOT be able to contain this inflation or ever reach their 2% target regardless if the economy turns down just as what happened during Vietnam.

This is a warning to all small banks. Understand the REAL trend or you will NOT survive. Major capital is fleeing the long-term and rising into the short-term because they see rates are rising and any long-term bond investment during a period of war is going to be a major losing trade. Do not get trapped by the yield curve and understand that this trend is in play into 2025.

This Banking Crisis has been caused by Governments who artificially kept interest rates too low since 2008 and in the process, this banking crisis is unfolding because too many banks are UNSOPHISTICATED in forecasting and have been listening to the talking heads on TV and the desperate hope that inflation will decline while ignoring Ukraine entirely. Get that wrong – and you will NOT survive.

I strongly urge small banks to take our business services for access to real forecasting that is not biased or tarnished by human opinion with the two most dangerous words in forecasting:

Posted originally on the CTH on February 5, 2023 | Sundance

Axios is positioning this announcement as FTX asking for political donations to be returned. However, the request is realistically from the FTX debtors.

(Via Axios) – Bankrupt crypto exchange FTX is sending notices to former donor recipients asking for the donated funds to be returned, the company said in a press release Sunday.

Why it matters: Former FTX CEO Sam Bankman-Fried and FTX Digital Markets Co-CEO Ryan Salame were two of the largest political donors during the last election cycle. Now the company’s debtors want the money back.

Bankman-Fried primarily backed Democrats and was the party’s second-largest donor last cycle with around $37 million in contributions.

Salame’s $19 million to Republicans made him the party’s 10th largest donor.

The big picture: FTX’s debtors are confidentially contacting “political figures, political action funds and other recipients of contributions or other payments.” (more)

Additionally, the Twitter Account “Unusual Whales” which tracks and researches financial transactions, has published the first list I have seen that makes it easy to see who FTX donated to. The list IS HERE and is alphabetized.

Posted originally on the CTH on February 5, 2023 | Sundance

This is one of those interviews where you don’t have to take my word for what is being said, Gary Cohn and Margaret Brennan are gleeful about the January jobs report and the overall return of the U.S. economy to a service driven system with low wages. Seriously, this is them celebrating out loud.

In order to calm the Wall Street apoplexy about his election victory, President Trump selected Gary Cohn to be an economic advisor early in the administration. However, it was also no surprise that President Trump did not follow Cohn’s advice, and quickly dispatched him after Cohn protested. In this interview the worldview of Cohn is typically globalist, multinational and Wall St centric.

Talking about the January jobs report, Cohn literally gets everything wrong from the position of Main Street USA. Cohn also celebrates what he calls the “renormalization of the new economy.” Continuing with his thought process Cohn states, “A lot of the jobs that we saw were jobs in the service industry, the service, the industries coming back very strong because we’re starting to see the economy go back to what we historically think of the economy,” he said. This is exactly how Wall Street, and the multinationals look at the U.S. economy.

The next part that both Cohn and Margaret Brennan celebrate is even more sunlight. “The interesting thing about last month’s unemployment numbers is we brought people back to work, but we did not have to entice them with pay,” Cohn stated. “So, the monthly, the month over month number in wage gains was 30 basis points. The prior month was 40 basis points. So, we’re seeing we’re getting people back into the labor force for a lower wage than we were prior to this,” he said. With higher prices (inflation) crushing the middle-class and service workers, the multinationals Cohn represents are celebrating that they don’t have to pay workers higher wages. WATCH:

[Transcript] – MARGARET BRENNAN: So 517,000 new jobs, but a lot of companies, particularly in tech, are announcing layoffs. So exactly where’s the economy headed?

GARY COHN: So, it’s interesting. We did see the 500,000 plus new jobs, which was quite surprising, I think, to many of us. But I think what we’re actually seeing here is a renormalization of the new economy. A lot of the jobs that we saw were jobs in the service industry, the service, the industries coming back very strong because we’re starting to see the economy go back to what we historically think of the economy. For the first time, we’ve seen occupancy rates in offices in major cities over 50%. When you see occupancy rates go up, you need the service sector to work. Think about people going back into the office. They need parking attendants. They need people to work in the buildings. They need security. They need people to clean the buildings. People stop for coffee when they go into the buildings. They go out to lunch. They go to bars. For the- for that to happen, you need the service sectors to come back to work. So the 120,000 service sector employees that came back to work, that 100% correlates with people going back to what is the new normal. It may not be five days a week in the office, but it’s enough days in the week in the office where you need the service sector to come back to work. The interesting thing about last month’s unemployment numbers is we brought people back to work, but we did not have to entice them with pay. So the monthly, the month over month number in wage gains was 30 basis points. The prior month was 40 basis points. So we’re seeing we’re getting people back into the labor force for a lower wage than we were prior to this.

MARGARET BRENNAN: And that’s a little bit hopeful for you on the inflation front.

GARY COHN: Yeah, and I think this is natural. I think what we’ve seen is, after all the stimulus that was put in the system over the last three months, people are running out of the stimulus money. We saw that in the fourth quarter of last year. We saw consumer spending slow down. We saw debit balances on credit cards go up. We started to see delinquencies go up. And you know what happened? People actually did the right thing and they went back to work. They’re engaged and they reenter the workforce. And I think we saw a lot of that in the January numbers.

MARGARET BRENNAN: So these more positive signs have led Bank of America, for example, to say recession still in the cards, but not until after March. I wonder what your thoughts are on that. And as CEOs warned about borrowing costs going up as a result of the Fed hiking. They are tightening belts. So how far off is this recession?

GARY COHN: Well, we’ve got a couple of phenomena going on. Interest rates have been going up, so borrowing costs have been going up for companies. On the flip side, the dollar has been weakening. So the multinational corporations in the United States who repatriate earnings from offshore, those repatriated earnings have become more valuable. I think the people that have been really worried about a recession in the first and second quarter of this year, I think after what we’ve seen this week with both Chairman Powell’s announcements and the data in unemployment, I think that recession is off the table for Q and one in Q2 of this year. You know, we’re going to get another employment report before the next Fed meeting and we’ll see where the economy’s going. But it does feel like we’re in relatively good shape here. The question is going to be how does the Federal Reserve handle what’s going on in the economy? Are we going to continue to have to increase wages to draw people back in the labor force, or are people coming back in the labor force because they need to? And we’re not going to have wage inflation if that happens. The Federal Reserve is actually in a very good place.

MARGARET BRENNAN: Let me ask you about something the Fed chair said this week. He said Congress has to lift this debt ceiling. I’m throwing one of the things that could screw up your- your rosy prediction at you. He said no one should assume that the Fed can protect the economy from the consequences of failing to act in a timely manner. He’s warning he’s not making plans for a default. You’re on your own if it happens.

GARY COHN: Yes.

MARGARET BRENNAN: Should there be a plan for the Fed to step in? I mean, I know legally it’s in question here, but I talk to people on Capitol Hill who say Wall Street is not taking this seriously enough. The politics are really bad around the debt ceiling.

GARY COHN: The politics are very bad. You know, the one thing is every American, every American is holding the US government to raise the debt ceiling. The full faith and credit of the US dollar and the US dollar being the reserve currency is imperative to our economic well-being as a country. We ultimately have to get the debt ceiling raised. That said, what’s going on here is not something out of the ordinary. If you look at debt ceiling raises over the last 40 or 50 years, no matter which party is in the minority, about 50% of the time, debt ceiling raises come with some amendments attached- attached to them from the other party. So this is quite an. Normal, the process that we’re going through.

MARGARET BRENNAN: You don’t sound overly concerned.

GARY COHN: Like I’m always concerned when we’re dealing with debt ceiling, but I have a feeling that we will get there in the end when we have no other choice. You had this- you had the speaker here last week and he felt confident that we would get there when we had no other choice. The speaker met with the president of the United States this week. The two of them came out of the meeting relatively confident. I feel they both understand there is no choice. In the end of the day, we have to raise the debt ceiling. The question is, can the Republicans get something in the legislation, attach the debt ceiling legislation that they want that they feel like is a win and the Democrats are willing to give it to? Historically, that is what’s happened numerous times.

MARGARET BRENNAN: Yeah. And the risk there is real. I want to ask you as well about China. Mark Warner was here with us last week and he said technology competition with China is the biggest issue of our time. He’s worried about things that- like your company does IBM, in terms of quantum computing. Is enough being done to keep America competitive on that front?

GARY COHN: Well, we’re starting you know, if you look at where we’ve been this year, you know, we passed the CHIPS Act in the United States, which, you know, is- is- is something that’s not a normal motion for us in the United States for the federal government to pick and choose–

MARGARET BRENNAN: To subsidize.

GARY COHN: –an industry, and and to subsidize. It really is not a normal action- is an action that, you know, historically I probably not would have been have supportive. I was extremely supportive of the CHIPS Act, we at IBM was extremely supportive of the CHIPS Act. If we learned nothing else from the pandemic, we learned that there are certain goods that are necessity goods for this country to have, and we are overly reliant on places like China. And if we don’t find ways to change the manufacturing system in the supply chain and move it back to the United States where we can take care of ourselves, we have made a catastrophic miscalculation. Chips are one of those areas where we cannot depend on the rest of the world and run our manufacturing business and continue to grow our economy. Pharmaceuticals is another area where we really have to move that industry and that manufacturing back to the United States. So I think we really have to evaluate what are the most crucial and sensitive businesses or industries that we cannot live within the United States. And we’re going to have to make real investments in those here in this country.

MARGARET BRENNAN: And we’ll keep talking about it with legislators. Have to figure out how to pass some of those laws. We’re going to take a quick break. And when we come back, we’ll be talking with four members of the freshman class and the 118th Congress.

Posted originally on the CTH on February 2, 2023 | Sundance

Of course, he is. President Trump is not only running against the Democrat candidate in 2024, likely Newsom, but he’s also running against the Republican establishment candidate in 2024, most certainly DeSantis.

As such, President Donald Trump is noting the same strategic plays that we are. Fortunately, he’s keeping an eye on how the Republican Governor’s Association (RGA) is intending to execute their anti-MAGA moves against the base working-class voters. [Trump Truth]

Again, for emphasis, despite accusations and ridiculously unfounded assertions, I have no affiliation or contact with anyone in/around the campaign. However, as with the prior election(s) in ’08 (McCain), ’12 (Romney), ’16 (Jeb!), and 2020 (Biden), the republican establishment roadmap is complex in a Machiavellian way, yet easy to spot if you know their objective. [Prior Resource Article on RGA ‘2022 Background Moves Here]

It is affirming to see that President Trump is watching these same tripwires as they are triggered.

As soon as Ron DeSantis makes his ’24 announcement (likely May, June or July – but he will be the last to enter), it will be the RGA who trigger the first wave of attacks against the MAGA base of voters. Together with the controlled GOPe field, they will trigger a sequential process for republican governors to align with DeSantis.

Ahead of the DeSantis announcement, those who are aligned with the playbook will start to come in next, beginning with Nikki Haley on February 15th. Each will have a billionaire donor class financier assigned to their specific SuperPAC support system. I would expect Chris Sununu to quickly follow Haley.

(National Rifle) […] The Republican Governors Association (RGA) donated almost $21 million to the Friends of Ron DeSantis PAC, a massive war chest that politicos believe the Florida Governor will use to take on Trump in 2024, with the backing of the GOP establishment.

Over the year and a half that the RGA was dumping millions into the Friends of Ron DeSantis PAC, they gave zero dollars to Doug Mastriano, the Trump-endorsed Republican nominee for Governor of Pennsylvania, effectively surrendering the pivotal state to Democrats. (more)

I also suspect, nothing but a hunch based on research, that Kristi Noem may have rejected the early entreaties from the professional Republicans who are coordinating the roadmap. If she didn’t reject something, the DeSantis crew would not be attacking her so hard. If my hunch is correct, this position could make Noem a wildcard.

Posted originally on the CTH on January 5, 2023 | Sundance

That slow grinding creak you hear in the background; that’s the U.S. economic engine running without oil and beginning that slowdown phase just before it stutters and stalls completely. Alas, the pretending continues…

As noted by the Wall Street Journal, an economic gaslighting institution with a central mission to maintain pretenses, “business surveys show U.S. factory activity declined in December, the Institute for Supply Management and S&P Global both said this week. Separately, S&P Global said Thursday that U.S. services-sector businesses reported a decline in output for the third month running in December.” This comes as “U.S. imports dropped more, by 6.4% on the month, as Americans cut back on holiday-related purchases, including items from other countries such as computers and autos.”

Keep in mind, November retail sales—which included consumer spending at stores, online and at restaurants—fell 0.6% from the prior month for their biggest decline of 2022, according to the Commerce Department. Manufacturing output declined in November as well, the Fed reported, while U.S. home sales fell for a record 10th straight month.

Into this mix of economic metrics, driven by a collapse in disposable consumer income and high energy prices, now we begin to see the number one business expense being curtailed.

(Market Watch) […] Amazon.com Inc layoffs will affect more than 18,000 employees, the highest reduction tally revealed in the past year at a major technology company as the industry pares back amid economic uncertainty.

The Seattle-based company in November said that it was beginning layoffs among its corporate workforce, with cuts concentrated on its devices business, recruiting and retail operations. At the time, The Wall Street Journal reported the cuts would total about 10,000 people. Thousands of those cuts began last year. (more)

Amazon is not alone, “Vimeo said Wednesday that it will cut its workforce by 11% as part of a broader effort to reduce costs, citing deteriorating economic conditions” (link). Additionally, Salesforce Inc. is laying off 10% of its workforce and reducing its office space in certain markets, extending a brutal period for tech job cuts into the new year.”

We can anticipate more reports like this from Reuters, “Samsung Electronics Co Ltd’s quarterly profit will likely plunge 58% to its lowest in six years as a global economic downturn saps demand for electronic devices and clouds the outlook for the memory chip industry. With consumers and businesses reducing spending and investment in the face of high inflation and climbing interest rates, smartphone makers and other clients held back memory chip orders, while smartphones sold for less as demand suffered, analysts said.”

Electronics, cars, furniture, durable goods of all types and varieties are plummeting in sales. Consumers are being squeezed by inflation, housing, energy and food costs, and spending priorities are being reevaluated yet again. Compare the impact on ‘real wages’ -vs- the 2007/2008 economic crisis.

From a purely fraudulent accounting perspective, however, the drop in U.S. imports will help boost calculations of U.S. economic growth in the fourth quarter because trade deficits subtract from overall output, or gross domestic product.

U.S. consumers not purchasing imported goods makes the health of the U.S. economy look less bad; but it’s an illusion akin to smiles in the bread lines.

In other economic news, I did some real estate analysis over the past several days and it’s safe to say there is a steep downward trajectory in the data I use. Again, home values are nuanced on a regional level, but my model is pretty close in averaging.

If buyers do not absorb the seller’s loss in equity (which no one should ever do), in my SWFL area a $450k home listing is going to sell around $380k at the high side (actual value based on economic indicators and buyer ability). That rough estimate, while slightly offset due to general inflation, should trend nationally over the next 12 to 18 months. That means macro home prices dropping around 15 to 20% nationally over the next 12 months.

If you are a home buyer, put your offers around 15 to 20% below current asking price without any emotional attachment to it. Don’t flinch, remain ambivalent and walk away if refused. The recovery to current price will take around a decade. If you are a seller and get an offer within -10% of asking, consider yourself lucky and jump on it.

Posted originally on the CTH on January 2, 2023 | Sundance

It’s almost painful to go to the grocery store today, not just because the prices for everything are so high, but also because seeing the stress amid the working-class shopping is palpable. Unfortunately, while we may have a momentary plateau on current pricing, there’s a strong possibility another wave of higher prices is yet to come.

At the core of the issue are energy prices which continue to rise. The immediate cycle of energy price hikes, a direct consequence of political policy, has lessened somewhat and we are now in that slow tick upward as the pressure on oil, gas, heating and electricity prices continues.

Michael Burry, famous for his predictions in/around the U.S. housing market, is noticing the same thing as CTH. “Inflation peaked. But it is not the last peak of this cycle,”he said. “We are likely to see CPI lower, possibly negative in 2H 2023, and the US in recession by any definition. Fed will cut and government will stimulate. And we will have another inflation spike. It’s not hard.”

Peak demand side inflation is long in the rearview mirror, but the peak of supply side inflation is questionable at best – I would say it’s a plateau, not a peak.

The price of goods, including industrialized and processed raw materials from China are going to increase again – and simultaneously become less consistent in availability. This is going to make prices extremely volatile in 2023.

Essentially, everything around price is tenuous as the western economies absorb the full impact of this Build Back Better energy policy, and into this foray comes China with production and processing challenges as a result of COVID bubbles being removed. We are seeing this problem right now in the pharmaceutical industry and with ordinary medicines becoming scarcer on store shelves.

With the macro economy showing a consumer collapse in spending on goods, the economy will contract again. However, the prices of essential products continue to sustain upward pressure. What does this look like in real terms? Less income amid the workforce and consistently higher prices. We need to be as prepared for this scenario as humanly possible.

Many people have written with sincere appreciation for the CTH forecasts delivered in the fall of 2021. I am thankful to have been of benefit to those who could take proactive measures to avoid the economic issues we faced in 2022. However, I am worried now.

I am worried because the downside to this economic contraction is going to hit the already tenuous and barely surviving middle class the worst. There’s only so much a person/family can do to offset rising energy costs. I listen to this woman’s voice, and it crushes me because I know and feel that pain (Twitter video):

I know just about every reader on these pages can relate to how financial fear can eat you from the inside. The life game of trying to figure out how to get from one week to the next, keep a roof over your head and keep the kids/grandkids safe and fed is fraught with trepidation. I get it. Believe me, I get it…. But you just gotta keep going; whatever it takes.

2023 is going to be rough for many working families and people on fixed incomes.

Then look to help/assist the neighbors, then the community, etc. But start by being proactive at home and do not isolate. Fear, worry, trepidation, foreboding etc, is worse when internalized. Do not swallow it – reach out to a loving God, pray, release it, and then embrace the central purpose in life, fellowship.

Posted originally on the CTH on January 1, 2023 | Sundance

This is an interesting interview in that International Monetary Fund Globalist Director Kristalina Georgieva seems to be laying the landscape for some truthful economic news to surface on the geopolitical level; albeit keeping up the globalist pretenses around western collective energy policy.

One of the more important points Mrs. Georgieva hits on is the reopening of China, from district level COVID bubbles as a containment feature, and the likely impact it will have on global supply chains. Mrs. Georgieva is correct on this issue.

China continued operating their industrial manufacturing base (despite COVID) because they built strict covid isolation bubbles around their industrial sectors geographically. However, with China lifting those isolation bubbles, there is a great potential for the manufacturing sectors to be hit hard by short to medium term virus outbreaks. This could/will have the potential ripple effect of global supply disruptions.

In an ironic twist, ‘deglobalization’ is now a 2023 catchphrase as various nations realize having their supply chains both dependent and interconnected is not good when there are interruptions. A new discussion centering around being dependent on China is the specific issue now being raised. However, the globalists are isolating their viewpoints only to raw material resourcing and development. WATCH:

[Transcript] -MARGARET BRENNAN: I want you to take us around the world and kind of us give us that global view. Let’s start in China. China has been this hub of cheap manufacturing for the world, we are all so dependent on it but right now it looks like COVID cases are exploding as they start pulling back those zero COVID restrictions. What will that mean for the global economy Longterm and short-term?

GEORGIEVA: In the short term, bad news. China has slowed down dramatically in 2022 because of this tight zero COVID policy. For the first time in 40 years China’s growth in 2022 is likely to be at or below global growth. That has never happened before. And looking into next year for three, four, five, six months the relaxation of COVID restrictions will mean bush fire COVID cases throughout China. I was in China last week, in a bubble in the city where there is zero COVID. But that is not going to last once the Chinese people start traveling.

MARGARET BRENNAN: Because they also- they don’t have an effective vaccine right now.

GEORGIEVA: The- the vaccinations fall behind. They have not worked on anti-viral treatments and how that can be offered to people, and so they will go through this tough time. If they stay the course, and this is our advice, stay the course, over time they would be able to catch up with the rest of the world, both in terms of focusing their vaccinations, bringing mRNA vaccines into China, expanding antiviral treatment, and the economy would function. But for the next couple of months, it would be tough for China, and the impact on Chinese growth would be negative. The impact on the region would- would be negative. The impact on global growth would be negative.

MARGARET BRENNAN: Because this is the second-largest economy in the world, and we’ve learned how dependent the world is on the Chinese supply chain. So do you expect then, a domino effect? Will inflation get worse, because all of a sudden there aren’t workers healthy enough to go to factories in China?

GEORGIEVA: We expect that there would be counterweight from the sheer opening of the economy, because up to now, the biggest impact on global value chains came from restrictions due to COVID. When you close down a big city or a big port, the repercussions for the economy is- are significant. Now, we would have the impact of people getting sick, not going to work, but the economy would be open. So the expectations we have for China is to gradually move to a higher level of economic performance, and finish the year better off than it is going to start the year. But you’re absolutely right, the world has relied on China’s growth for a long, long, long time. Before COVID, China would deliver 34, 35, 40% of global growth. It is not doing it anymore. It is actually quite a stressful for the- for the Asian economies. When I talk to Asian leaders, all of them start with this question, what is going to happen with China? Is China going to return to a higher level of growth?

MARGARET BRENNAN: You’ve said that you fear that we are sleepwalking into a world that is poorer and less secure because of a split in the global economy between the US and China. What do you mean by that? Do you see efforts here in Washington to stop it?

GEORGIEVA: It is very easy to reflect on the benefits of the world being more integrated. When we look back over the last three decades, the world economy tripled because of this reliance on an integrated world economy. Who benefited the most? Emerging markets and developing economies, they quadrupled. But rich countries also benefited, they doubled in size of the economy. So we have to be careful not to throw the baby out with the bath water. Yes, the way we have operated created excessive dependency in global chains. We were too focused on costs, how can we make products cheaper. And COVID and then the senseless war Russia started against Ukraine has shown that this is not enough. We cannot just concentrate on what is cheaper. We have to think of the security of supplies and that means diversify the sources of products that make the economy function well, lifting up the level of cost. That economic logic is not only appropriate, it is a must to follow. But we shouldn’t go beyond. We shouldn’t say, okay, we break the world into blocks, one works here, the other one works there because the costs are very, very high. We calculated that just trade, limiting trade into two blocks, would chop $1.5 trillion from the global GDP year after year after year.

MARGARET BRENNAN: If you tried to separate the US and China?

GEORGIEVA: You separate- you separate them, there is an excessive cost. So the logic should be where for security reasons there has to be careful recalibration of supply chains, do it, but don’t go beyond- don’t go into benign areas of products that have no strategic significance but they benefit the US consumer, they benefit the world economy. And this is what we are arguing for, don’t go in a direction in which this separation would make everybody poorer and the world less secure.

MARGARET BRENNAN: So you’re telling Beijing and Washington, figure it out. You can’t be in conflict.

GEORGIEVA: What we have seen in Bali is an indication that this rationale–

MARGARET BRENNAN: You’re talking about the G20 meeting–

GEORGIEVA: The G20 meeting in Bali, when the two presidents, President Biden and President Xi Jinping, met, they spent three and a half hours discussing exactly that. Where is the point of contact that makes both countries better off? And where is that- that there are differences that cannot be bridged and therefore we have to keep them–

MARGARET BRENNAN: The US is trying to block some Chinese technology companies from doing business here. They’re taking measures that are drawing some pretty bright lines between the US and China. Is that tolerable?

GEORGIEVA: We always prefer countries to seek their common interest in economic integration. And when you start breaking the interactions that are based on fair trade, you harm your own people, you not only harm the- the Chinese and therefore it has to be thought through very carefully. Again, I want to be very clear, some diversification of supplies for the security of supply chains is necessary. COVID taught us this lesson, the war taught us this lesson. So the U.S. is right to look into some areas where strategically they need to guarantee the functioning of the U.S. economy without interruptions. But do that keeping in mind the interests of the American people that would like to still have prices moderating, and actually, when we think about prices, one good news we have for 2023 is that towards the end of the year, we do expect inflation to trim down. So don’t take actions that may be contrary to that trend.

MARGARET BRENNAN: But you are predicting inflation to slow to six and a half percent from about 7%. Is that right?

GEORGIEVA: Well, towards the end of the year, we- we project it would go even further down towards the end of 2023, provided central banks stayed the course. Our big worry is that with the economy slowing down globally, we are projecting global growth to go down to 2.7%, maybe even lower next year. Remember, 2021, it was 6%. It dropped to 3.2 this year, 2022. And it will continue to drop down if central banks get the cold foot and say, ‘oh, my god, growth is slowing down, let’s slow down the fight against inflation.’ We risk then inflation to be more persistent. So our message is to central banks, you have to see credible decline in inflation and only then you can think about re-calibrating rate policy.

MARGARET BRENNAN: One of your IMF researchers gave a pretty dire prediction. Overall this year, shocks will reopen economic wounds that were only partially healed post-pandemic. In short, the worst is yet to come and for many people, 2023 will feel like a recession. What do you need to brace for?

GEORGIEVA: The- this is- this is what we see in 2023. For most of the world economy, this is going to be a tough year, tougher than the year we leave behind. Why? Because the three big economies, U.S., E.U., China, are all slowing down simultaneously. The US is most resilient. The U.S. may avoid recession. We see the labor market remaining quite strong. This is, however, mixed blessing because if the labor market is very strong, the Fed may have to keep interest rates tighter for- for longer to bring inflation down. The E.U. very severely hit by the war in Ukraine. Half of the European Union will be in recession next year. China is going to slow down this year further. Next year will be a tough year for China. And that translates into negative trends globally. When we look at the emerging markets in developing economies, there, the picture is even direr. Why? Because on top of everything else, they get hit by high interest rates and by the appreciation of the dollar. For those economies that have high level of that, this is a devastation.

MARGARET BRENNAN: And I want to- I want to come back to you on that. And just to explain that for some of our listeners, a stronger dollar, it’s good for Americans when they go shopping abroad. It’s not good for poor countries who have taken out loans, for example, and borrowed money in dollars. And according to the IMF, 60% of low income countries are in distress because of this- this debt. So what does that look like? Do you- do you see governments collapsing with defaults? Does that bleed into the global financial system? I mean, how much of a contagion does this become?

GEORGIEVA: So far the countries that are in that distress are not systemically significant to trigger a debt crisis. Let’s just look at the map, which are these countries? Chad, Ethiopia, Zambia, Ghana, Lebanon, Surinam, Sri Lanka, very important for their people that we find the resolution to the debt problem, but the risk of contagion is not as high. However, if that list continues to grow, and let’s remember, 25% of emerging markets are trading in distressed territory, then the world economy may be for a bad surprise. And this is why at the IMF, we are working very hard to press for debt resolution for these countries and we have engaged the traditional creditors, the Paris Club, the non-traditional creditors, China, India, Saudi Arabia. I would call this very simple: urgency, we have to act. When I look at the- the debt of the world. Yes, we have to be concerned. During COVID, what did we do? Everywhere governments borrowed, rightly so, to help their people.

MARGARET BRENNAN: Money was cheap.

GEORGIEVA: Money was cheap, and we prevented a collapse of the world economy. That was the right thing to do. But once Russia invaded Ukraine and that added impetus to inflation, money is not- not cheap anymore. So what is the advice we give to governments? Focus on your budgets, make sure that you have sufficient revenues to collect and that you spend very wisely.

MARGARET BRENNAN: That’s good advice, but it’s not always easy politics to follow that advice, as you know–

GEORGIEVA: Of course it is not.

MARGARET BRENNAN: And so that’s why I want to- if- if you can explain for our viewers. You know, we spoke to the CEO of JPMorgan Chase, Jamie Dimon, recently, and he said he sees the global risk as explosive right now. He was saying things like migration, energy, national security, liquidity in the banking system, war, these are all the knock on effects of a government not being able to pay its bills and not being able to deliver for its people. Is that what you are seeing too?

GEORGIEVA: Well, what we’re seeing is the world has changed dramatically. It is a more shock prone world. The lessons we learned from the last couple of years are that no more we operate with relative predictability of what the future would bring. And these shocks COVID, the war, costs of living crisis, they compound their impact. What does that mean for governments? First and foremost, it means that we need to change our mindset towards more resilience, more precautionary actions. And at the IMF, this is what we tell our members. Act early, don’t wait until the problems deepen. And for those who need help, this is why we exist for the developing countries. The fund is a source of resilience and I am- I am very pleased that many of our members are coming to us. Just since the war started we got 16 countries coming for programs to the IMF, $90 billion in support for these countries. And right now we have 36 requests. So that acting early, when you see trouble, look for ways to strengthen your fundamentals, to have buffers to protect you and your people. This is the advice we give to governments. For those who don’t know the IMF, we were created from the ashes of the Second World War to stabilize the world economy. And at a moment like this, we come strong to help our members. My message, don’t think that we are going to go back to pre-COVID predictability. More uncertainty, more overlap of crises wait for us. Rather than crying for the time we had, we have to buckle up and act in that more agile, precautionary manner I described.

MARGARET BRENNAN: I want to make sure I get to Ukraine because I know we’re running out of time. You’ve said- excuse me- you’ve said the single most negative factor in the global economy is the war in Ukraine. And Vladimir Putin says this is going to go on for some time. President Zelensky said they need $55 billion in foreign support next year. He expects $20 billion from the IMF, is he going to get it?

GEORGIEVA: We are working on providing support for Ukraine. So far, out to the international financial institutions, we have provided the largest amount of financing for Ukraine, $2.7 billion in emergency financing, and we are working for 2023 to be a significant part of the support for Ukraine. I expect that sometime early in the year we will go to our board with the request. We have assessed the needs of Ukraine to range somewhere between three and five billion dollars a month. What Putin did with destroying critical infrastructure in Ukraine, this is horrific, and it means that in the next months the country would be more on the high end of this range because it is put in an awful position to have to restore access to electricity, to heat, to water. I have relatives in Ukraine. What I- what I know from them is it is cold, it is dark, and it is scary. Bombardments of civilian areas continue. What I also want to say is that Ukraine has proven to be remarkably resilient. Ukrainian economy is functioning. Pensions are being paid. When there is bombardment, restoration of energy, water, heat is done very quickly and we see revenues collected in Ukraine in a very disciplined manner to support the functioning of the country.

MARGARET BRENNAN: So the government’s not going to collapse?

GEORGIEVA: The government is very well functioning under incredibly difficult circumstances. No, they’re not going to collapse. And then the other thing that is so remarkable is actually the world has proven to be more resilient than we feared, a year in the beginning of the year. We look at the response to the energy shock in Europe, and Europe is moving towards independence from Russia decisively. Yes, there will be a tough winter, maybe the next one would be even tougher, but freedom from dependence on Russia is coming. It is going to be there.

MARGARET BRENNAN: I want to ask you two questions before we go. How do you describe the state of U.S. economics and politics?

GEORGIEVA: The US economy is remarkably resilient. Decision making in the US because of the way the political set is at the moment, it is more difficult. But nonetheless the US has taken some very important steps that are helping to the US economy. Like the child tax-

MARGARET BRENNAN: The tax credit. It expired.

GEORGIEVA: The credit that is it. It is contributing so significantly to reducing poverty in the US, like the infrastructure bill, like the Inflation Reduction Act. These are things that are bringing more dynamism in the US. Good for the US, good for the world. And of course staying on that course is going to be more challenging. But I do hope that the US is not going to slip into recession despite all these risks. We expect one third of the world economy to be in recession. And yes, as you said, even countries that are not in recession, it would feel like recession for hundreds of millions of people. But if that resilience of the labor market in the US holds, the US would help the world to get through a very difficult year.

MARGARET BRENNAN: And as I let you go, my final question is what leaves you hopeful in 2023?

GEORGIEVA: What leaves me hopeful is that I know when we work together, we can overcome the most dramatic challenges. In 2020, the world came together in the face of tremendous threat and was able to overcome this threat. In 2023 we have to do the same. And in this world of ours, of more frequent and devastating shocks, we have to hold hands, we have to work together. And my institution is there to bring together economic policymakers so we can be wise and persistent in the face of truly dramatic challenges we face.

MARGARET BRENNAN: Madam managing Director, thank you for your time this morning.

Posted originally on the CTH on December 28, 2022 | Sundance

BlackRock, Inc. (together with its subsidiaries) is a massive publicly traded multinational investment firm with over $8.68 trillion in assets under management [December 31, 2020 financial statement] in more than 100 countries across the globe. To say that Blackrock is invested in globalism, climate change and leftist politics, would be a severe understatement {See Here}. Larry Fink is the CEO and people like Cheryl Mills, Hillary Clinton’s attorney of record, are on the board.

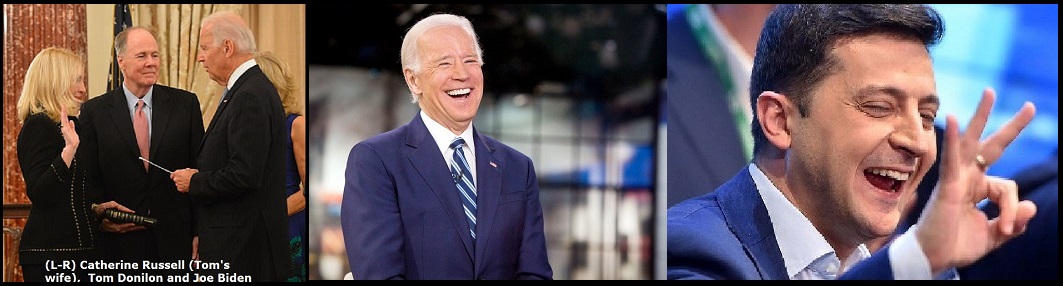

The Chairman of the BlackRock Investment Institute, the guy who tells the $8.7 trillion investment firm BlackRock where to put their money, is Tom Donilon; President Obama’s former National Security Advisor (before Susan Rice), and a key advisor to Joe Biden throughout his career in politics; who was also recently put in charge of U.S-China policy by the State Dept. {link}

Tom Donilon’s brother, Mike Donilon is a Senior Advisor to Joe Biden {link} providing guidance on what policies should be implemented within the administration. Mike Donilon guides the focus of spending, budgets, regulation and white house policy from his position of Senior Advisor to the President. Tom Donilon’s wife, Catherine Russell, was the Biden White House Personnel Director {link}. In that position Donilon’s wife controlled every hire in the Office of the Presidency. Tom Donilon’s daughter, Sarah Donilon, who graduated college in 2019, now works on the White House National Security Council {link}

Yes, Blackrock, the world’s largest investment firm, is essentially in a private-public partnership with the Biden White House fraught with massive financial conflicts of interest. Tom Donilon is the bagman. The Donilon family coordinates the Biden foreign policy toward Ukraine, and the Donilon family positions Blackrock financially to benefit as a specific outcome of the relationship with the Biden family and the White House. Now this….

WASHINGTON DC – Zelensky and BlackRock CEO Larry Fink met virtually on Wednesday, the president’s website revealed, and discussed plans for the financial behemoth to play a prominent role in the postwar reconstruction of Ukraine, which has been subjected to massive Russian depredations for most of this year. Plans for BlackRock leaders to visit Ukraine in the new year were finalized at the meeting.

Zelensky also announced that Ukraine would participate in next year’s WEF summit in Switzerland from Jan. 16-20 but didn’t specify if he would be attending in-person or virtually.

“I have spoken with the head of the world’s largest investment fund, BlackRock, and have been assured yet again that businesses from the developed world are ready to invest in our recovery,” the Ukrainian media quoted Zelensky as saying in a video address, Interfax reported. “Company specialists are already helping Ukraine structure the Recovery Fund.”

“We are preparing to partake in the World Economic Forum in Davos. The posture and prospects of Ukraine will be presented there,” he added.

Zelensky and Fink first met virtually in September, where plans for BlackRock’s participation in postwar reconstruction efforts were sketched out. BlackRock specialists are set to play a key advisory role in Ukraine’s economy. The Ukraine president’s website stated, “The BlackRock team has been working for several months on a project to advise the Ukrainian government on how to structure the country’s reconstruction funds. (read more)

We have written about the previous conflicts {Go Deep Here} and {Go Deep Here}. So, now we have the Biden administration positioning U.S. taxpayer funds going into Ukraine. That DC money will now blend with Blackrock rebuilding money and come out of the laundry operation to provide financial benefits to Blackrock, Zelenskyy and the Biden family syndicate.

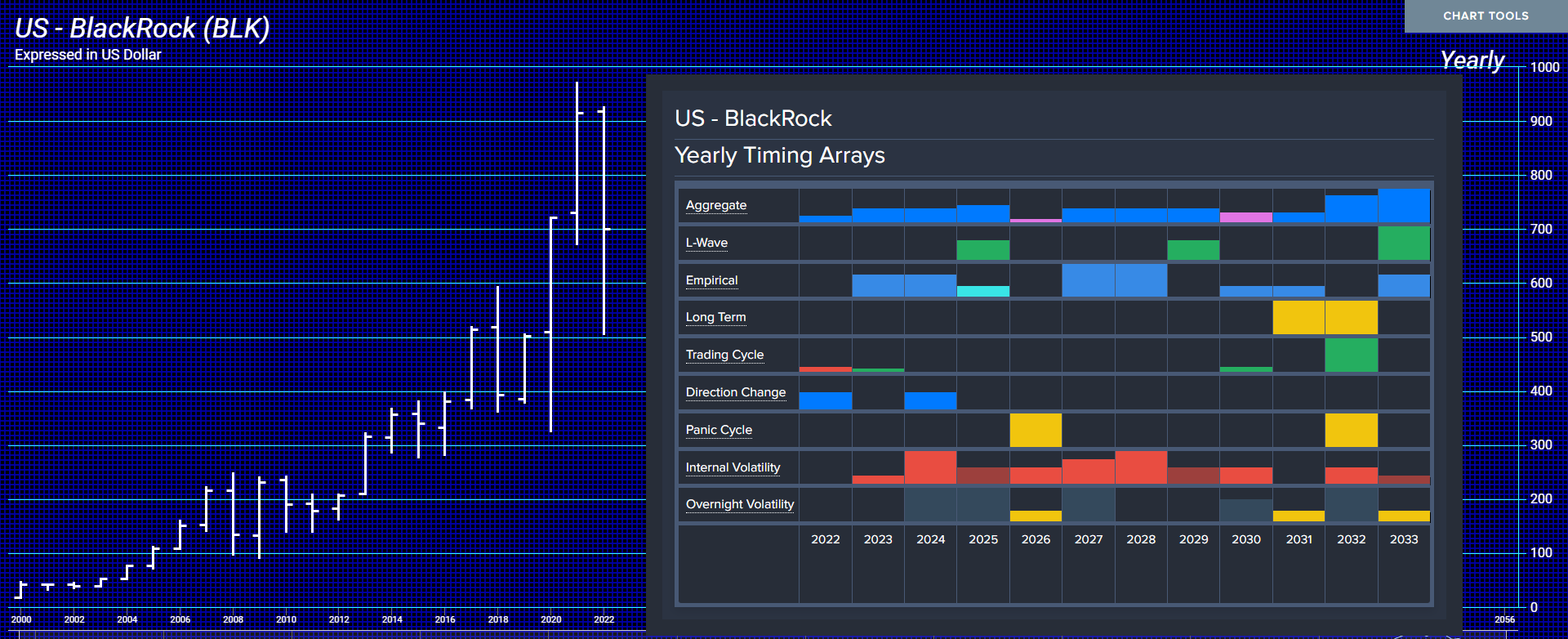

QUESTION: Marty, your Socrates predated Fink’s Aladdin by a decade. Blackrock’s stock dropped about 50% from 2007 into 2010 when Socrates got the whole crash right. It picked the very day of the high in 2007 and they were calling it on the floor Armstrong’s Revenge. Socrates called for a Directional Change here in 2022 and it was correct. Socrates is forecasting Aladdin. Cool!

Socrates has forecasted events years in advance. Nothing else does that. You warned at the WEC about the danger of a fund getting too big. My question is rather straightforward. Do you think that Fink’s influence can save Blackrock in the future?

ANSWER: Fink lost a ton of money before and left that firm. He is a good salesman, but I am a trader. I watched how the Hunt Brothers ended up in bankruptcy because their position in silver was too big and everyone knew it. If they tried to sell one ounce, the market assumed here it all comes and everyone and their 5th ex-wife jumped in front to sell. BlackRock is in a vulnerable position. It is TOO BIG and that may buy influence, but in a liquidity crisis, the danger becomes you are like the Hunts and everyone will front-run you.

The marketplace is so intricate and the regulators are corrupt, anything goes for there is no loyalty on the street – ask Lehman Brothers and Bear Sterns. I had the Aristotle Onasis estate precious metals positions I had to liquidate. He had the largest private holding of platinum in the world. It took me months to get approval from the CFTC just trade above exchange limits. When I got approval and called a dealer for a quote, everyone knew the position. Someone in the CFTC let their friends know.

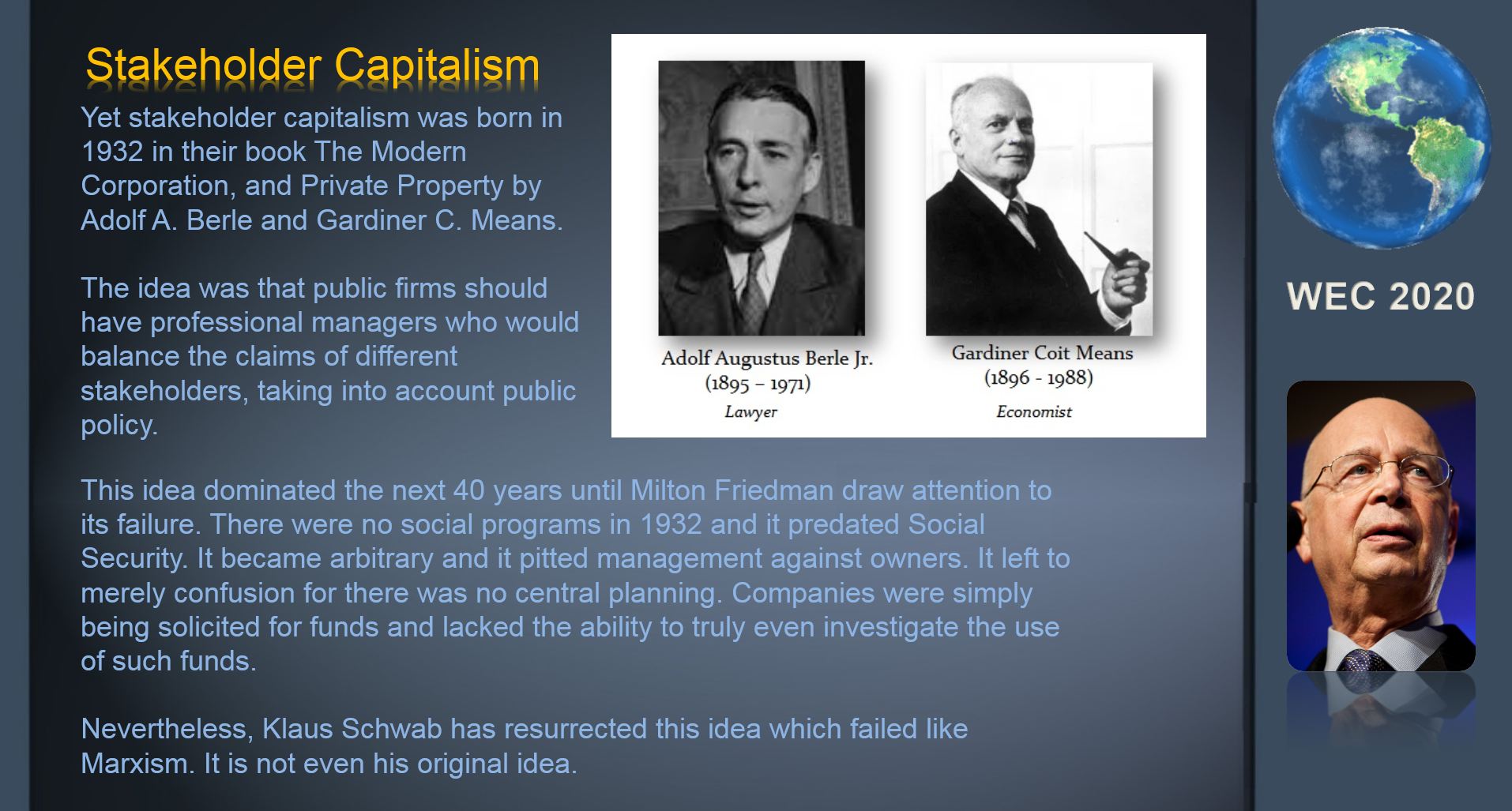

Fink is on board with Schwab and preaches Stakeholder Capitalism. That philosophy was never Schwab’s but was born during the Great Depression before there were social programs from the government. It was a complete disaster and set the stage for the takeover boom of the 1980s.

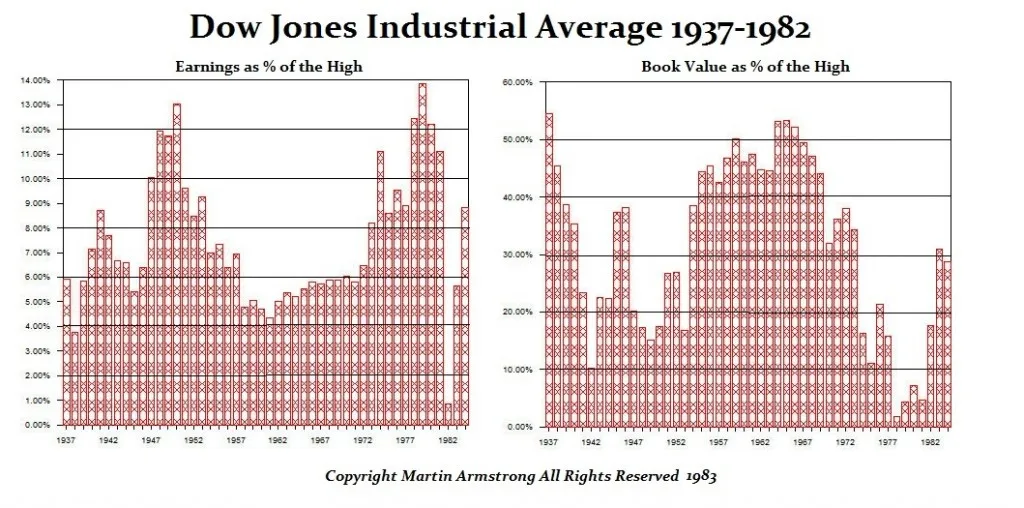

I was advising many of the takeover players back then. I showed these charts and how the Dow bottomed in 1977 in terms of book value thanks to Stakeholder Capitalism. I showed clients we could buy companies, sell the assets, and double or triple the money. That became the genesis of the movie Wall Street with Michael Douglas.

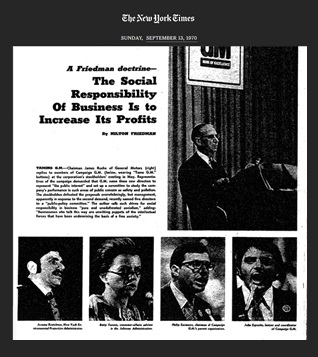

It was Milton Friedman, back in 1970, who exposed how Stakeholder Capitalism was inefficient and stupid. It was a derivative of Marxism that took down Communism. He laid out that such a role was that of government, not corporations, whose #1 fiduciary obligation was to its shareholder. Under Schwab, I could say, “OK I will go public; everyone sends in money. I will give you shares in return and then say — OMG, there are people starving in Africa!” So, I decide to give 50% of all the profits to them and not my investors. This is Stakeholder Capitalism that Fink endorses thinking it is something Schwab has invented. Worse still, he has adopted that I believe to raise money from Schwab’s disciples. It Ain’t Capitalism – It’s Marxism!

The problem I see is that you simply cannot collect that much money to manage without becoming the elephant in the room. By the time we get to 2025, it does not look like any amount of influence will matter. Aladdin is not the same as Socrates. It cannot project out decades. Fink is specializing in high-frequency trading and ETFs. This will be very interesting in the next couple of years. He claims he is investing for the long-term so don’t judge him by the fluctuations. Those who said that in 1929, “HOLD”, lost 90%. It took 26 years for the Dow to return to the 1929 levels.

Posted originally on the CTH on December 8, 2022 | Sundance

It is always worth a reminder when reviewing anything from Blackrock, that the institutional investment firm has strong ties to almost every sphere of White House policy.

Today Blackrock is warning of severe economic conditions looming, the unspoken origin traces to the collective western economic shift in energy policy, aka “Build Back Better.”

As noted in the Blackrock warning, under the auspices of inflation control, central banks can try and shrink economic activity – but they are limited. Organically, economies will free fall once the full weight of BBB energy policy accumulates.

(Business Insider) – […] A worldwide recession is just around the corner as central banks boost borrowing costs aggressively to tame inflation — and this time, it will ignite more market turbulence than ever before, according to BlackRock.

The global economy has already exited a four-decade era of stable growth and inflation to enter a period of heightened instability — and the new regime of increased unpredictability is here to stay, according to the world’s biggest asset manager.

That means policymakers will no longer be able to support markets as much as they did during past recessions, a team of BlackRock strategists led by vice chairman Philipp Hildebrand wrote in a report titled 2023 Global Outlook.

“Recession is foretold as central banks race to try to tame inflation. It’s the opposite of past recessions,” they said. “Central bankers won’t ride to the rescue when growth slows in this new regime, contrary to what investors have come to expect. Equity valuations don’t yet reflect the damage ahead.” (read more)

This type of macroeconomic prediction should not come as a surprise to most CTH readers, because we have been outlining the natural conclusion of consequence.

Once the decision was collectively made to shrink the use of oil, coal and natural gas for energy development, the subsequent inflationary impact would lead to a need to shrink economic activity. Raising interest rates to shrink demand does make the economy contract; however, the energy driven supply side inflation continues.

Nothing can stop supply side inflation, except a massive decline in energy use.

A severe reduction in energy use, similar in scale to the energy use reduction when pandemic lockdowns were in full effect, can only lead to the same overall economic conditions as present within the lockdown. Which is to say, almost no economic activity.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America