Posted originally on Sep 25, 2024 By Martin Armstrong

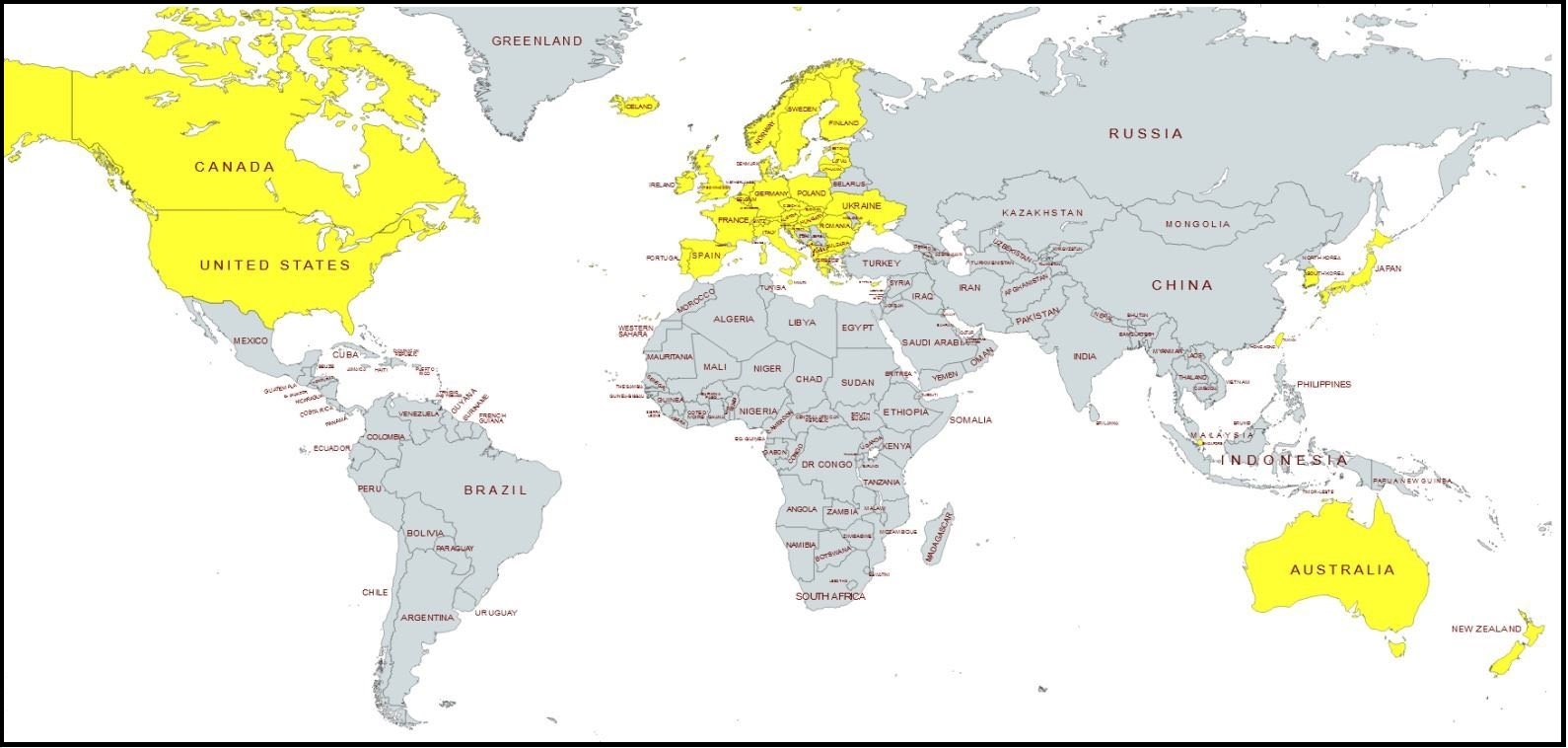

Over 130 nations are attempting to create a digital currency as we move toward a cashless society. I recently explained how Australia is prioritizing a wholesale CBDC with a retail one to follow. The Bank of Canada recently shelved plans to create a digital Loonie, but rest assured this is a mere pause as the world will move to digitalization.

“The Bank has undertaken significant research towards understanding the implications of a retail central bank digital currency, including exploring the implications of a digital dollar on the economy and financial system, and the technological approaches to providing a digital form of public money that is secure and accessible,” the bank said in an email statement. The fact of the matter is that Canada simply could not determine how to execute a digital Loonie properly. The bank will now focus on “evolving” its payment system.

One aspect most nations are facing is that it would be easier, seamless even, if every developed nation agreed to go digital. But, more on that later.

The Bank of Canada released “The Role of Public Money in the Digital Age” in July 2024 to discuss the importance of creating a digital currency to “uniform money.” The central bank identified the following risks:

“Over that horizon, three interrelated and overlapping trends pose risks to the monetary system. First, the overall digitalization of the economy and financial system is increasing demand for digital payments. Second, due to the first trend and other conditions, use of cash has been declining at the point of sale for many years. The third trend is the emergence and proliferation of private cryptocurrencies and digital assets, including foreign CBDCs. These trends pose risks to the monetary system through three mechanisms: • increased potential that fragmentation of the monetary system could create inefficiencies • increased ability of issuers of private forms of money to exert market power • increased difficulty implementing timely and adequate regulation due to the rapid pace of change”

Unlike Australia, Canada sought to tackle retail immediately and stated cash was “no longer a viable payment option.”

The central bank recognized their legal right to have a monopoly over the money supply and noted that cryptocurrencies were threatening their overall power. Central banks DO NOT want people to use crypto as an alternative to their currency and will do everything to prevent it from happening. “When different forms of money (including alternative units of account) compete in a jurisdiction, users need to monitor both risks and exchange rates, and the resulting frictions provide scope for the issuers of these alternative forms of money to exert market power. Ultimately, these frictions and abuse of market power reduce the efficiency of the economy,” the report stated.

Now the central bank recognized it could not simply cancel the currency without public backlash. They fear that the public will use alternative payment methods, and so the plan was to slowly phase out physical money. “We do not suggest a “CBDC alone” approach. On the contrary, in the status quo policy, the availability of retail public money interplays with the evolution of the regulatory components of the monetary system to ensure their continued effectiveness.”

As I have stated countless times, money is whatever someone is willing to accept as payment, be it gold or seashells, as in ancient times. The public at large is not ready to accept a CBDC if they are presented with a choice. If Canada were to implement a digital Loonie, it would run the risk of people using other currencies or crypto to complete transactions.

The bank said it will continue monitoring GLOBAL retail CBDC progress as all financial institutions await the moment when they can align their activities. This is why we see a heightened need for biometric data and digital identifications, which will one day tie into your financial accounts and you simply will not have a choice in digital or physical currency if paying on the grid.

Governments will become increasingly tyrannical as we move towards 2032 and the end of this private wave. The globalists’ ideal monetary system would entail one universal currency, similar to what the International Monetary Fund has been developing for years. Canada, an IMF member, has decided to await future global developments, but do not mistake this pause for a ceasefire in the war on cash.