Armstrong Economics Blog/ECM Re-Posted Aug 21, 2023 by Martin Armstrong

QUESTION: Marty, I have tried to convince some family members of the deep state and the trend in front of their eyes. No matter what I say, they ignore it and call me crazy. Should I give up?

DP

ANSWER: Look, the vast majority are simply the herd. They prefer not to think analytically. They feel comfortable thinking the government really cares. They still want to live the dream that Santa Claus is real. I would estimate that this represents at least 70% of the population, and at times it has risen to as high as 85%. I based that on simply looking at the election cycle. No president has ever won even 70% of the popular vote. The real decision makes, I would put at about 10%. They are the independents who vote on issues and will vote for either party. The rest are core Democrats and Republicans.

Physiologically, the need to remain as part of the herd. You will NEVER convince them. You can only preach to the choir. Looking at history, this will change, but it must come with pain and sorrow that forces them to reassess their life. Consequently, do not try to beat your head against a brick wall. Just say, when you open your eyes and mind, call me. They will remember that. They MUST come voluntarily. You cannot drag them any more than you can drag a horse to water.

Historically, there comes a time for a paradigm shift. That is when we should see at least 40% of the people who then support change. In the case of the American Revolution, Thomas Paine wrote Common Sense. That publication moved the people finally, and an uprising against the king. His work was so influential that the English struck tokens targeting him with the slogan:

END OF PAIN

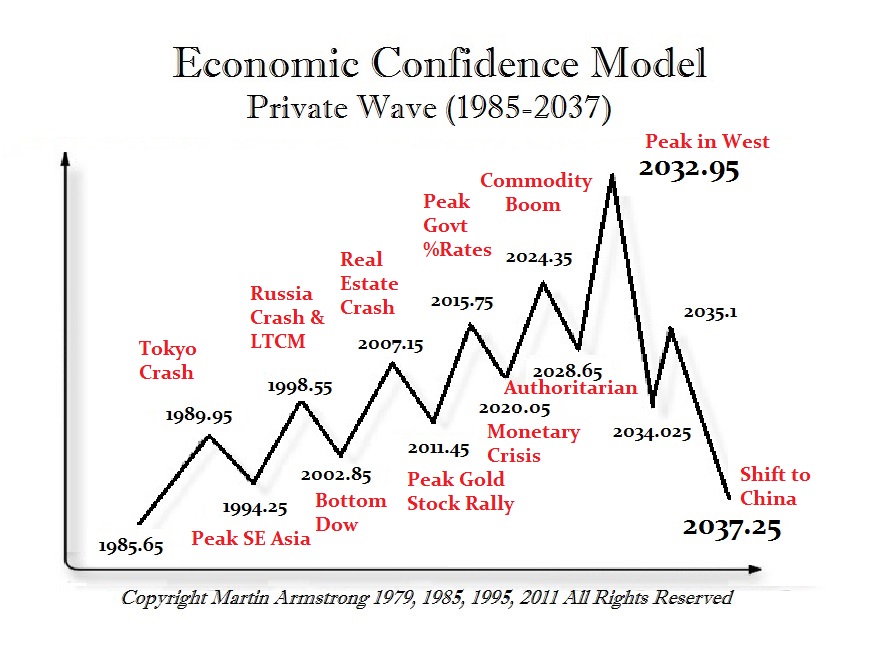

As we move closer and closer to 2032, we will see this shift post-2024. We should begin to witness this paradigm shift toward anti-government form by 2026. It will most likely explode in 2029. This is all necessary for the people must come voluntarily. It will be 2032 when we witness perhaps as much as 60%-75% of the people demanding the end of Republic forms of government.

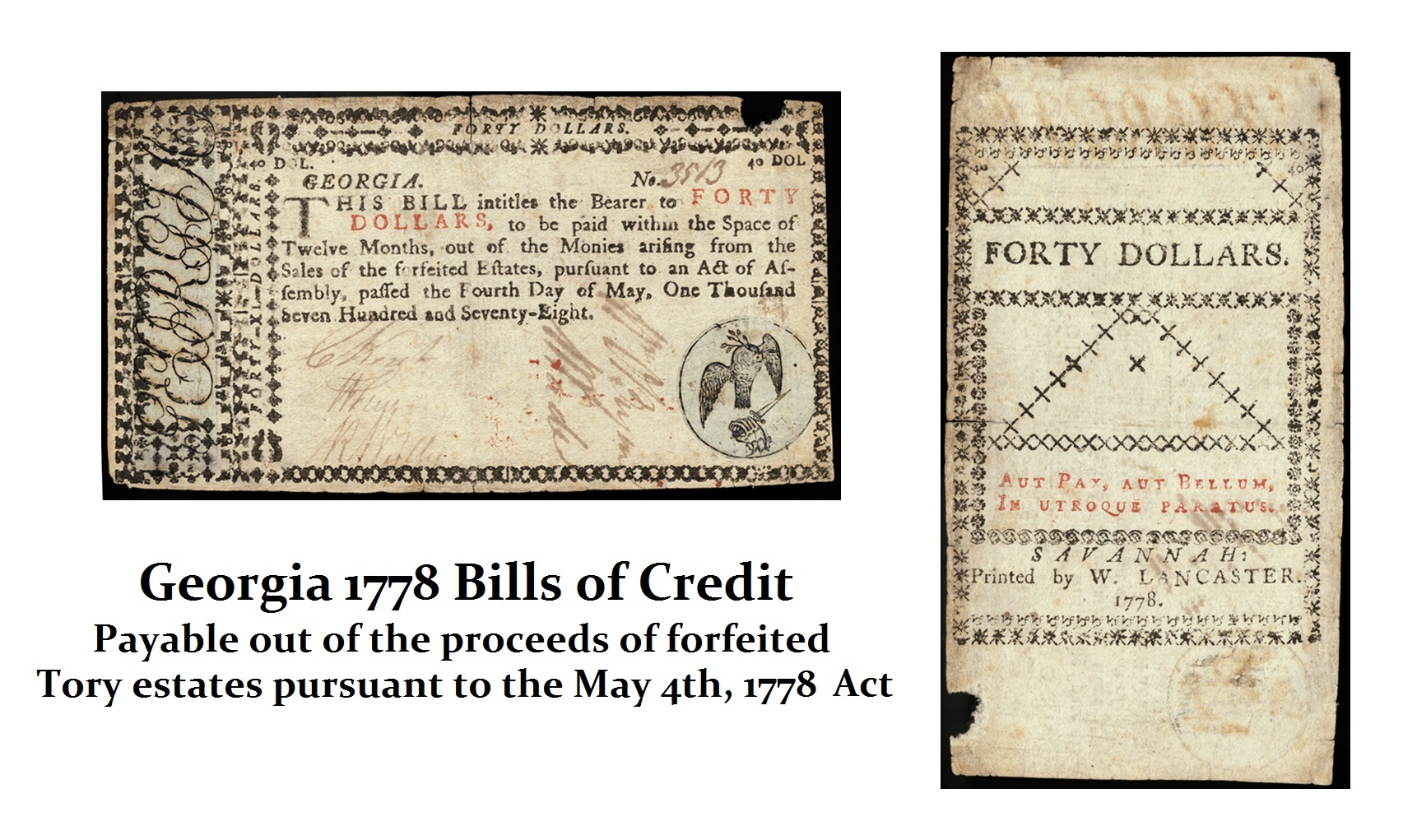

You will NEVER get 100% consensus on anything. Some people ask me what would happen if everyone used Socrates. I respond nothing different. But the question is rather absurd. There will NEVER be such a consensus. Here is a colonial note from George promising it is back by confiscating the assets of those who supported the king who could NOT voluntarily depart from the herd.

Categories: ECM