A bank failure of this proportion has not been seen since 2008 when Washington Mutual failed. The majority of deposits in Silicon Valley Bank (SVB) are uninsured, meaning the FDIC’s $250,000 protection does not apply. Uninsured depositors will be provided receivership certificates and should receive an advanced dividend this week. The FDIC must sell off the remaining assets of SVC to determine how much it can provide to those uninsured depositors. The FDIC is encouraging borrowers to continue paying their existing loans. The bank was said to host $209 billion in assets and $175.4 billion in deposits as of December 2022. Washington Mutual held around $307 billion in assets when it went down.

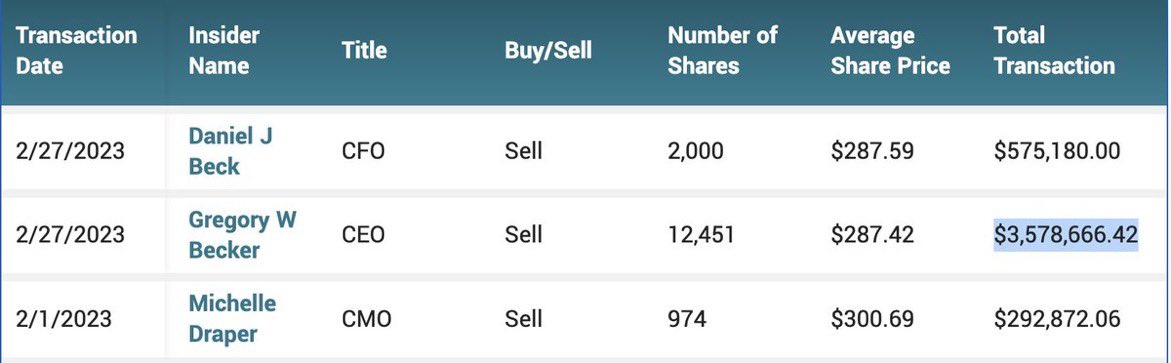

Tons of people and businesses will be completely screwed over. Who could have seen it coming? Silicon Valley Bank CEO, CFO, and CMO sold off millions in stock over the past two weeks. President and CEO Greg Becker sold 12,451 shares on February 27 for $3.6 million at $287.42 per share. Later that day, he purchased options for the same amount of shares at $105.18 a piece. He did the same thing in December 2021, as this is not an uncommon albeit unethical practice. Banks commonly trade against their own clients. Becker sold about $3.57 million worth of SVB stock over the past two weeks and is now making TV appearances saying he did not see this coming.

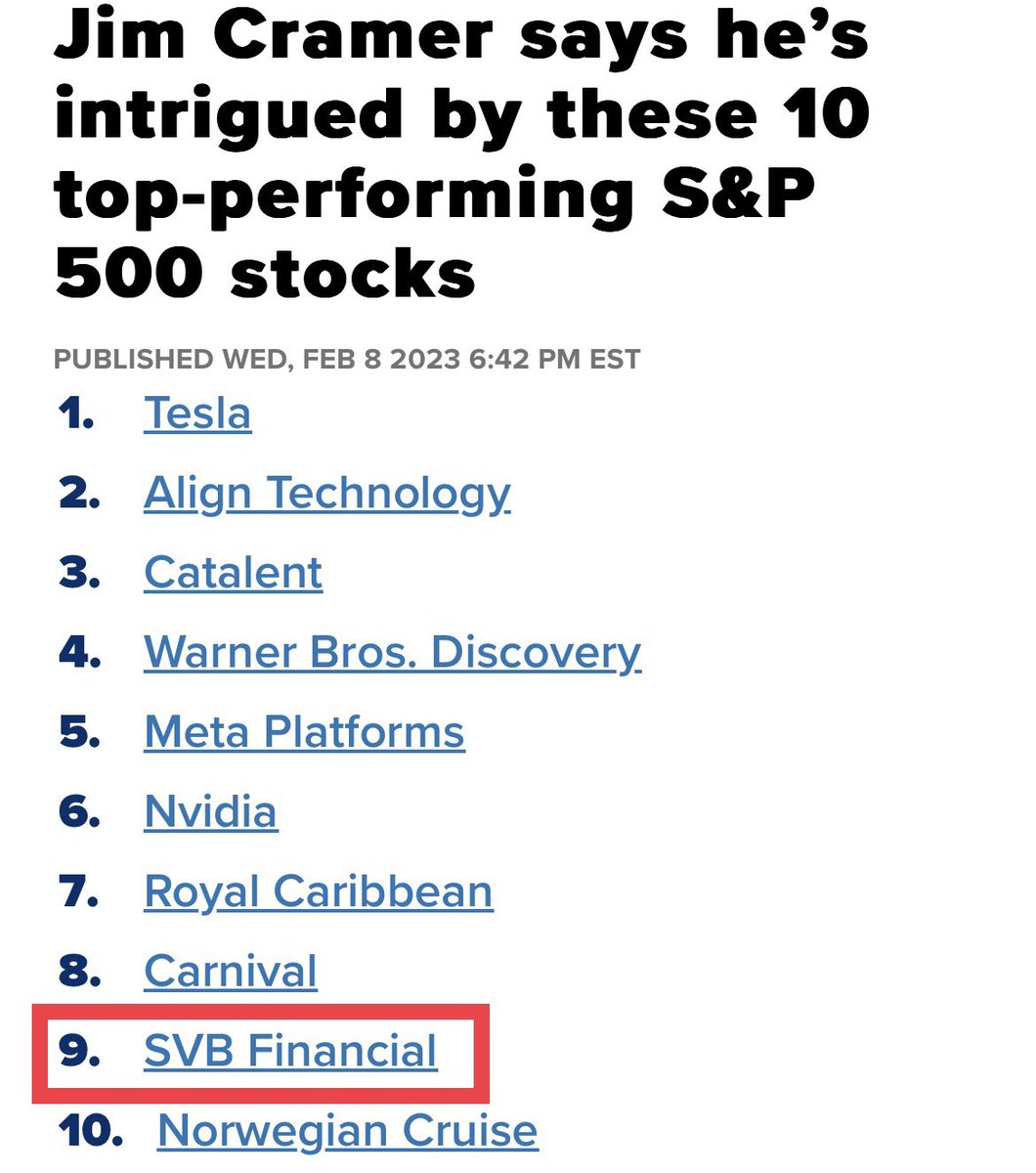

There were signs of trouble, but the talking heads said otherwise. Forbes even listed SVB Financial Group as #20 on its list of America’s Best Banks in an article published on February 14, 2023. Talking/screaming head Jim Cramer came out last month to say that SVB Financial would become one of the top performers on the S&P. This is why you cannot listen to information based on biased opinions. I hesitate to call this negligence technical analysis.

Companies are now at a complete loss, many cannot make payroll, and this situation will only worsen once the uninsured depositors realize their IOUs are worthless.

COMMENT: Marty; Two former Merrill Lynch traders were each sentenced to a year and a day in prison Thursday for manipulating the precious metals markets, the US Department of Justice announced. Of course, —- —–, which is forever bullish metals, claims they moved the metals in the “direction they wanted from 2008 to 2014.” It just seems that people claim it is always manipulation when they have been wrong. They only look at gold in dollars as you have said it’s a global market. They would have to manipulate all the currencies as well.

This latest affair of so-called manipulating trades during the day proves what you have been saying. They have always been gunning for stops during the day, but they cannot manipulate the trend between a bull or bear market. Do you think people will ever understand this is a global economy?

HD

ANSWER: I know. Unless people have actually been a trader, they will never understand the market. They will blame people like this to pretend they were not wrong. The problem is that this nonsense of manipulation is driving a stake through the heart of the market. Trading is like a poker game. Do you reveal your hand before everyone starts to bet? Sometimes you bluff, but the point is if you are bluffing, you have to stand behind your bet.

The mere fact that someone is blaming this type of “manipulation” for being the reason they have been wrong demonstrates that they know nothing about investing no less trading. The DOJ is now big on calling placing large “spoof” orders as manipulation. That is absurd and it is no more than bluffing in a poker game. This is the way all the markets have always functioned. Everyone would know where the stops were anyway. Sometimes they traded ahead of them using the stops as your risk point to exit the trade, and other times they would sell or buy to push the market through the stops when it was obvious that was even possible.

When I was trading in precious metals back in the ’90s, the biggest “local” dealer on the floor was Oni Morrison. He would do “spoof” orders all the time which I called “flash” bids or offers. The difference was he was good for it if hit. I was long one time in gold and I wanted out for the computer projected a crash was coming. But if you offer a thousand lots and the market was heading lower, everyone will read that and jump in front of you. That is how the Hunts went bankrupt. The Hunts did not know how to trade. Just as in poker, you cannot show your hand and expect to trade.

Oni would do “flash” bids or offers. I told my broker not to offer anything. I told him just to watch Oni and as soon as he would do a 1,000 flash to buy – say done! Sure enough, Oni was trying to push the market back up and he did one of his famous flash bids for 1,000 lots. My broker, Emerald Trading, instantly said “DONE!” Oni did it again, and they said “DONE!” Again he did a fash for 1,000 and again they said “DONE!” That was it. Oni was full and everyone began selling as the metals tumbled.

That is the way you have to trade SIZE. This is the very foundation of trading all markets for everything is just a poker game. To now call a “spoof” trade manipulation is just wrong. It is totally different when you do not have the backing. Now that would be a fraud and trying to manipulate the market for that moment – not changing the overall trend. But when you have the backing to honor your “spoof” it is just a “flash” bid or offer that you must stand behind when hit. That is just trading.

It is total BS to pretend that these guys manipulated the entire market. That is just absurd. Not even the central bank can manipulate the economy. You cannot “manipulate” a market against the trend for everything is connected. That caused the Panic of 1893 when the Silver Democrats overpriced silver. The Europeans hit the arbitrage and dumped silver in the US and took the gold back to Europe. That led J.P. Morgan to have to arrange a $100 million gold loan to bail out the treasury. That alone proved that you CANNOT manipulate ANY market against its trend for it will be arbitraged internationally – plain & simple.

Gold trading around the world in different exchanges is arbitraged. You cannot have gold $20 high in one market v another. It will be arbitraged instantly. Those who claim this as “proof” that the metals have been manipulated so that is why they have not rallied and why they have been wrong are fools who have been separated from the money. They will never understand the markets no less be able to see beyond the end of their nose. It will be instantly arbitraged.

The collapse of the Soloman Brothers was precisely that. They were putting in bids at the Treasury Auction using other people’s names to goose the market. They got caught and the firm was taken down. I know PhiBro from the ’70s and ’80s. They took over Solomon Brothers and brought that style of trading from the commodity pits to Wall Street.

This excuse by goldbugs that the metals were actually “manipulated” in their long-term trend, shows their hopeless ignorance of the markets and how they even trade. There is NOBODY who could possibly do such a thing for everything connected. As soon as the dollar would rise, the metals in terms of foreign currency would be so overvalued they would all sell and they will end up broke the same as the Silver Democrats bankrupted the country by overvaluing silver.

Trading internationally, with clients in all currencies, we have to look at each market in terms of their currency for that will determine if they made a profit or loss. Anyone who claims the metals have been manipulated and that is why they have not rallied is obviously oblivious to the world around them.

Gold does NOT rise with inflation – that is the sales pitch of a used car salesman. Gold rises in times of UNCERTAINTY with respect to the government. In times of war, it rises because it is NEUTRAL and you are not betting on who will win.

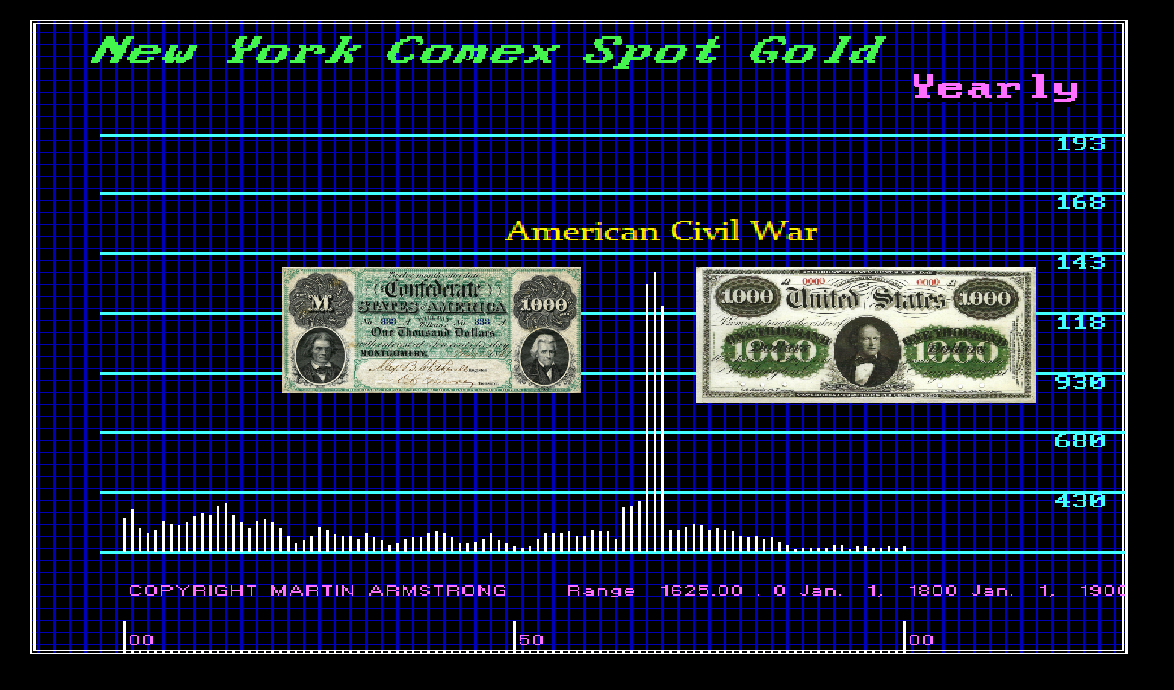

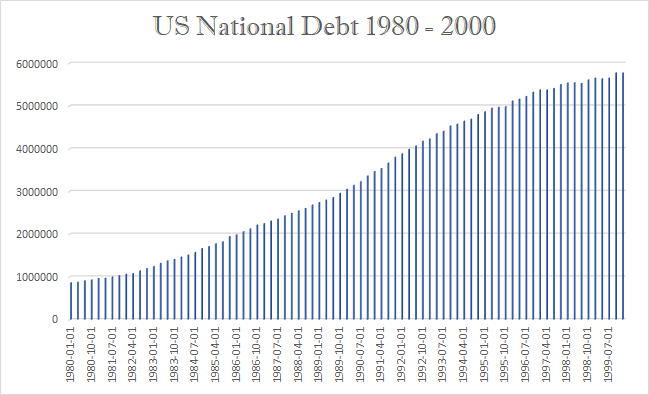

All we hear is that the debt is rising and therefore gold will explode. Once again, they offer no proof of their sophistry because there is no such proof. Gold declined for 19 years while the national debt climbed endlessly.

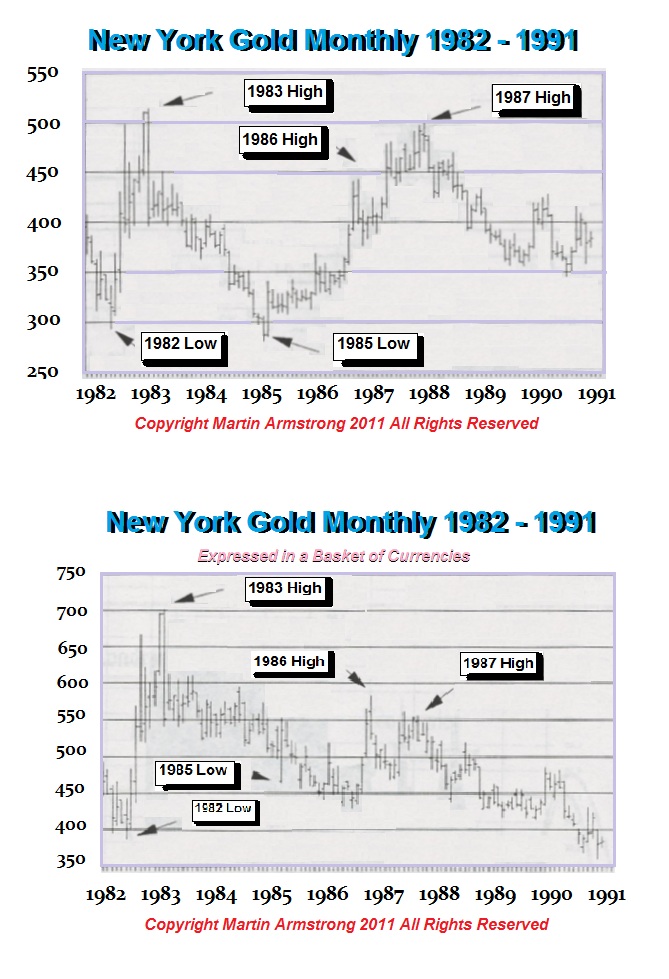

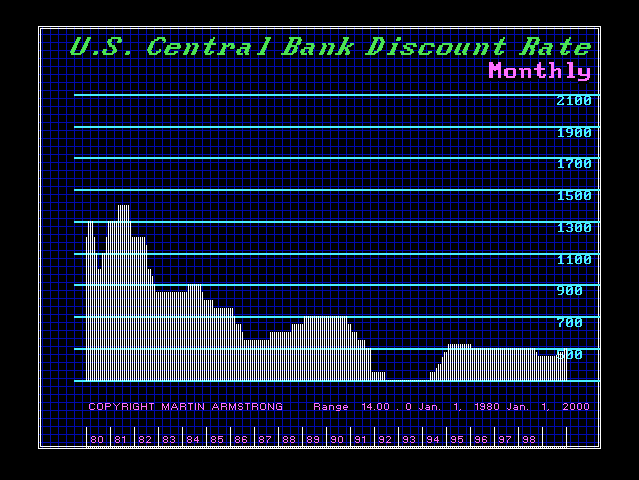

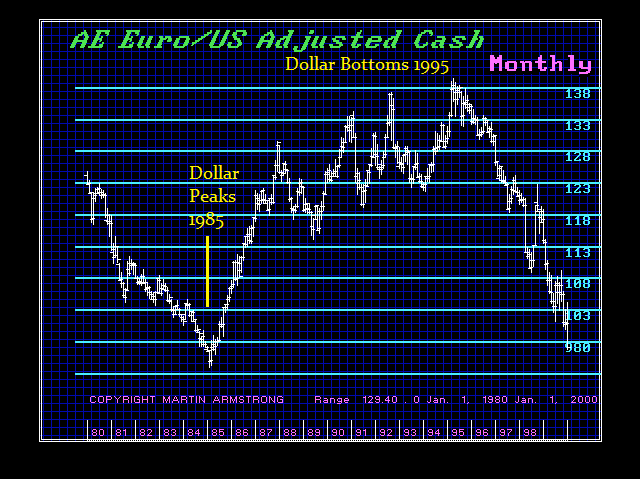

Then there is the myth about interest rates and gold that higher rates are bearish and lower rates are bullish. Well, interest rates peaked in 1981 and declined in 1994 before they began to rise marginally into 1995. Yet then contrast that myth with the performance of the dollar. There the greenback rose to a record high in 1985 but then declined for 10 years into 1995 all the while gold declined into 1999.

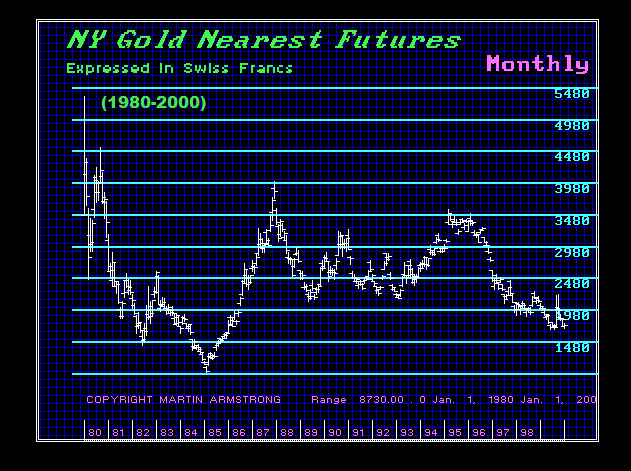

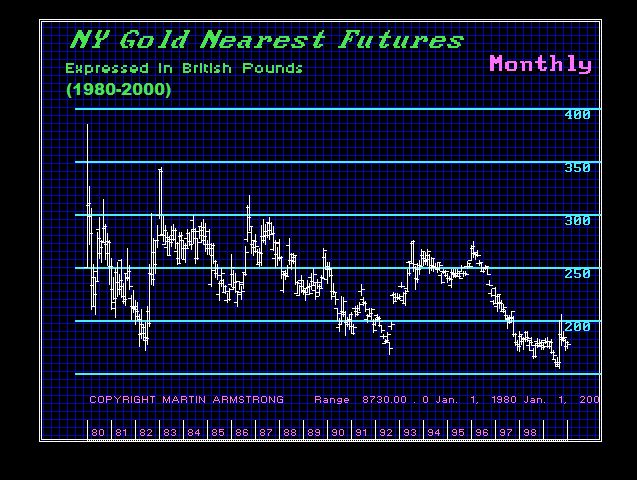

OK, so now let’s look at gold between 1980 and 200 in terms of Swiss francs and British pounds. We can instantly see that gold bottomed in 1985 in terms of the Swiss franc. In terms of British pounds, gold did not bottom until 1999.

People come up with theories all the time. However, they always try to reduce everything to a single cause and effect. They are doing that with climate change. They are telling the world it is CO2 that has changed the climate without ever addressing anything else.

The world we live in is not only complex, but it is also so dynamic it appears that no human can correctly forecast the future with an “I think” scenario. Sometimes they will be right, and others they will be wrong. Typically, they fail because they try to reduce the world to a single cause and effect.

Gold Rises with UNCERTAINTY with respect to the question of will the government survive its own madness.

The Biden Administration is responding to the panic phone calls that their Marxist philosophy will bring down the entire financial system. My ear is red as can be. I have had enough of the phone calls today to last the balance of the month. Trying just to do the right thing! Three banks have effectively gone down in the week of March 6th, which our computer was targeting. There have been Silicon Vally Bank, Signature Bank, and Silvergat Bank.

The Regulators perhaps saw the handwriting on the wall. This NO BAILOUT claiming that no taxpayer money will be used for a bailout of their hated rich, how about just using the taxpayer’s money you are throwing down the train in Ukraine? Depositors in Signature and SVB they are now saying would be made whole. If they do not cover ALL deposits, the monumental banking failure will be catastrophic.

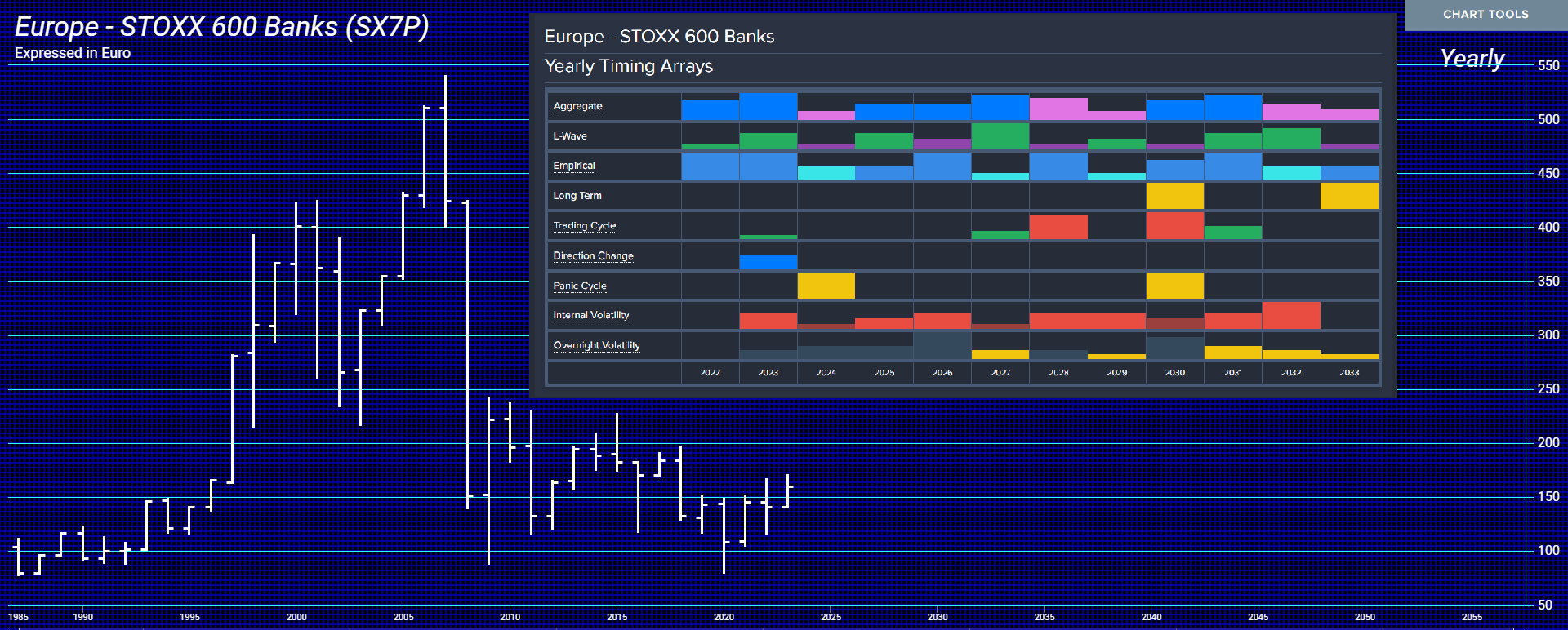

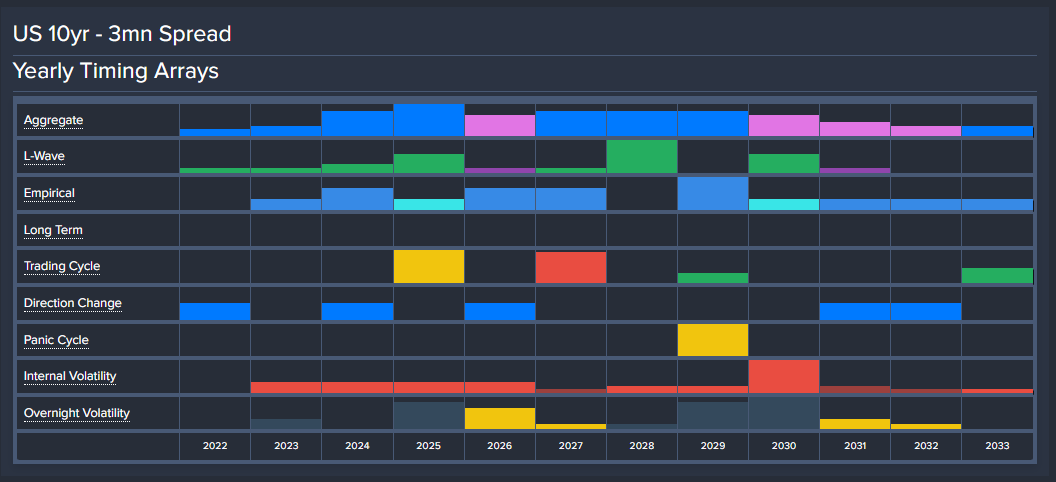

Our forecast for a Banking Crisis is by NO MEANS confined to the United States. It will be far worse in Europe. We can see our computer not only targeted 2023 for a key turning point with a Directional Change but a Panic Cycle next year in bank stocks, but interest rates will be rising higher as also the risk of banks and governments escalated especially when they insist on waging war against Russia.

The yield curve is critical and we must understand that this insane war against Russia, even economically, will be a major financial disaster not much different from Vietnam which brought down Bretton Woods and forced Nixon to close the gold window on August 15th, 1971. It was that unrestrained spending directed by the Neocons. Then too, it was all about Russia they assumed was behind Vietnam.

Once more, the reckless spending on war promoted by the Neocons is undermining the entire economy. They have lost every war they have promoted – Vietnam, Afghanistan, Iraq, proposed Syria, Libya regime change, and now Ukraine. These people are never held accountable for all the devastation and the lives lost.

War is the primary driver of inflation and the central banks will not even address it for they do not want to “criticize” the Neocons. They might wake up with their dog’s head in the bed as in the Godfather. The central banks will NOT be able to contain this inflation or ever reach their 2% target regardless if the economy turns down just as what happened during Vietnam.

This is a warning to all small banks. Understand the REAL trend or you will NOT survive. Major capital is fleeing the long-term and rising into the short-term because they see rates are rising and any long-term bond investment during a period of war is going to be a major losing trade. Do not get trapped by the yield curve and understand that this trend is in play into 2025.

This Banking Crisis has been caused by Governments who artificially kept interest rates too low since 2008 and in the process, this banking crisis is unfolding because too many banks are UNSOPHISTICATED in forecasting and have been listening to the talking heads on TV and the desperate hope that inflation will decline while ignoring Ukraine entirely. Get that wrong – and you will NOT survive.

I strongly urge small banks to take our business services for access to real forecasting that is not biased or tarnished by human opinion with the two most dangerous words in forecasting:

COMMENT #1: Marty; Thank you so much for your warning at the WEC that we would now face a banking crisis with rising rates into 2024. You are always so far ahead of the pack. Live forever – please!

KQ

REPLY #1: Thank you, but that would sentence me to perpetual taxation indefinitely. No thanks.

COMMENT #2: Hello. I read your FREE blog because I am poor. Would you please stop posting PRIVATE stuff and post stuff that us peons can read?

Thank you kindly.

Ms. Terri

REPLY #2: My concern is since we forecast this last year, they will only blame me. That blog is only $15 a month, but it is blocked by Google so it is more free speech if you get my drift. I simple MUST be guarded in what I say publicly because they simply always view me as having too much influence.

I will offer this recommendation (publicly) for my ear is turning red from all the phone calls. As for the Biden Administration, if they DO NOT heed my warning, our forecast will be devastating. The Biden Administration MUST stand behind ALL deposits – not the $250,000 FDIC limit. If they do not, small businesses will pul; excess cash from banks, switch to 30-day T-Bills at a brokerage house, and say screw the FDIC and the Biden Administration’s anti-rich (small business which employs 70% of the workforce).

The compromise here is that we need a shotgun wedding where a larger bank takes over SVB at the raw price of the deposits. The shareholder loses, but ALL depositors are covered. Any value of the shares should be attributed to tangible assets only, not goodwill. You will penalize your “hated rich” and even the small businesses will be saved. If not, you will wipe out numerous businesses that cannot even pay employees. That will set off a contagion as you try to uphold your hatred of the “rich” while you pour money into the most corrupt government in the world at the real expense of taxpayers.

Of course, SVB can simply declare they “identify” as a Ukrainian Bank and then everything would be covered right down to the pensions of the CEO.

Posted originally on the CTH on March 12, 2023 | Sundance

BREAKING NEWS – The U.S. Treasury, Federal Reserve Board, FDIC and Joe Biden collectively announce that *all* depositors with Silicon Valley Bank (SVB) will have access to their funds – regardless of amount deposited. Also, all senior bank management has been terminated.

This announced action appears to cover those under FDIC protection ($250k or less) and those above FDIC protection (deposits greater than $250k). The only vulnerability is that SVB “shareholders and certain unsecured debtholders will not be protected.”

WASHINGTON DC – The following statement was released by Secretary of the Treasury Janet L. Yellen, Federal Reserve Board Chair Jerome H. Powell, and FDIC Chairman Martin J. Gruenberg:

Today we are taking decisive actions to protect the U.S. economy by strengthening public confidence in our banking system. This step will ensure that the U.S. banking system continues to perform its vital roles of protecting deposits and providing access to credit to households and businesses in a manner that promotes strong and sustainable economic growth.

After receiving a recommendation from the boards of the FDIC and the Federal Reserve, and consulting with the President, Secretary Yellen approved actions enabling the FDIC to complete its resolution of Silicon Valley Bank, Santa Clara, California, in a manner that fully protects all depositors. Depositors will have access to all of their money starting Monday, March 13. No losses associated with the resolution of Silicon Valley Bank will be borne by the taxpayer.

We are also announcing a similar systemic risk exception for Signature Bank, New York, New York, which was closed today by its state chartering authority. All depositors of this institution will be made whole. As with the resolution of Silicon Valley Bank, no losses will be borne by the taxpayer.

Shareholders and certain unsecured debtholders will not be protected. Senior management has also been removed. Any losses to the Deposit Insurance Fund to support uninsured depositors will be recovered by a special assessment on banks, as required by law.

Finally, the Federal Reserve Board on Sunday announced it will make available additional funding to eligible depository institutions to help assure banks have the ability to meet the needs of all their depositors.

The U.S. banking system remains resilient and on a solid foundation, in large part due to reforms that were made after the financial crisis that ensured better safeguards for the banking industry. Those reforms combined with today’s actions demonstrate our commitment to take the necessary steps to ensure that depositors’ savings remain safe. (LINK)

Will this action help stop any contagion related to California’s largest bank?

…The odds are, yes.

Despite Friday’s action to stop trading of FRB, with this action, I doubt First Republic Bank (FRB) is now at risk.

Posted originally on the CTH on March 11, 2023 | Sundance

South Dakota Governor Krisi Noem appeared on Tucker Carlson’s television broadcast last night to send a warning to fellow governors. According to the background story, the South Dakota legislature passed a bill redefining currency and creating rules for a Central Bank Digital Currency (CBDC) that would block all other digital currencies from being used in the state. Governor Noem vetoed the bill.

When asked why her legislature would do this, Noem responded the state politicians likely did not read the bill as it was constructed by lobbyists. Noem is exactly correct and hits on a subject we have discussed here frequently {GO DEEP}. However, one of the more alarming aspects to Noem’s discussion of the issue is that around 20 other states are considering similar legislation. WATCH:

In times of economic distress, people will hoard their wealth. This is as true in ancient times as it is in modern times. I was called in about a hoard of gold – one thousand $20 St Gaudians gold coins all dated 1924 – uncirculated. As you see, I have a reputation for buying hoards as well as funding major archaeological digs. This was a hoard of US$20 gold coins. So I took the lot. As for those who say I hate gold, no, I have always loved the $20 st Gaudens.

Obviously, this was a stash. It was the year of a Presidential election and in 1925, Calvin Coolidge was the first President to have his inauguration broadcasted on radio. In 1921 the Chinese Communist movement began and in 1924 Stalin came to power after poisoning Lenin and his wife. The flight from Russia began in 1917, but it escalated by 1919. It is hard to say why this hoard was stashed away. But they are all dated 1924 and may have been connected to the upheaval in Russia. By the end of 1919, it was clear to almost everyone that the Bolsheviks had won the Civil War. The White armies were defeated on all fronts: Siberia, the Russian North, and Petrograd (as St Petersburg was then called). Pravda on Aug. 31, 1918:

“Our cities must be mercilessly cleansed of the bourgeois rot. All these gentlemen will be put on file, and those who pose a danger to the revolutionary class will be destroyed … Henceforth, the hymn of the working class will be a song of hatred and revenge! ”

It was the White Russians who fled. It was estimated that at least 2 million fled Russia at the time. That was about 2%-3% of the surviving population by 1919. Given the date of this hoard and the condition, they were tucked away and never saw circulation. They may have been related to the turmoil in Russia.

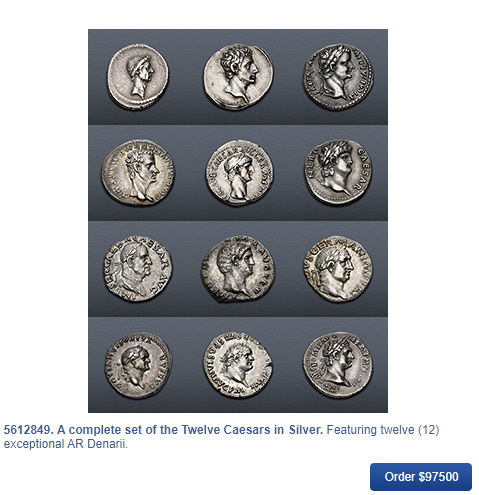

A number of people have asked if I could put together sets of the 12 Caesars because I had mentioned I thought that could be done for half the price of the set being offered elsewhere. I am trying to get a small hoard of Caligula denarii. They are very difficult to find. I believe because he was so hated, they may have just melted down his coinage.

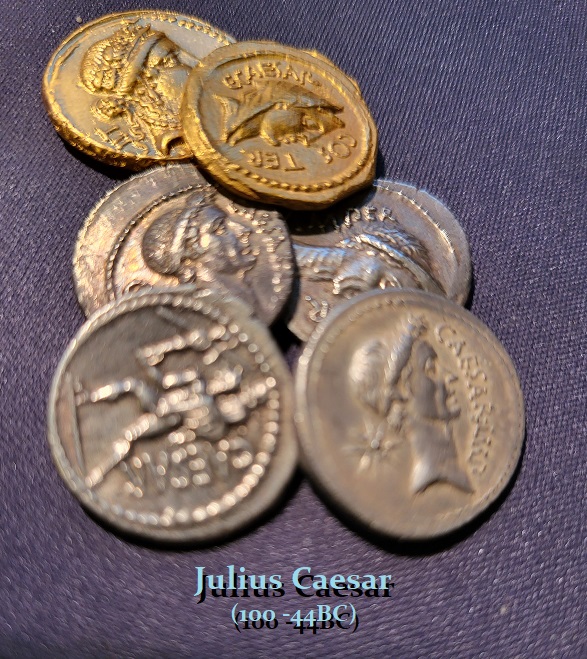

It all depends on quality. I have purchased a small hoard of Julius Caesar coinage. I will try to see If I get these Caligula denarii. If I do, I will try to see if I can put together some sets with much more realistic prices.

I have purchased a hoard of late Constantine bronze. They are very reasonable.

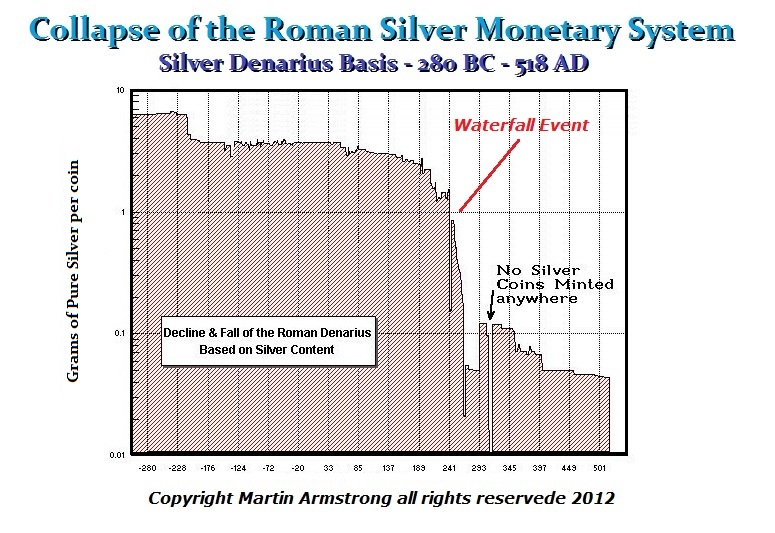

I have purchased an early hoard of Gallic coinage of Postumus which is silver. I also have purchased a hoard of Victorinus which are bronze. This is the period of both the split in the Roman Empire as well as the collapse of the monetary system.

Others have asked if I can put together a progression of the coinage showing the debasement. I will try. Here is a photo showing the stark difference between the beginning of the region of Gallienus (253-268AD) and its end.

QUESTION: The sales pitch seems to be that there is this $2 quadrillion in global debt that overhangs everything. Paper assets, therefore, will all implode! They seem to be saying that everything has risen due to this debt bubble and it was all created with Zero interest rates. Now that they are going up, the debt bubble will burst and everything will decline. The story seems to be that this decades-long Boom Bust cycle was created over and over by the Federal Reserve.

This seems to be like you have said, they try to reduce everything to a single cause and effect.

What really happens?

PCJ

ANSWER: These people seem to keep preaching the same story but have no historical understanding whatsoever of how the monetary system has ever worked. Their focus on the Federal Reserve shows that they are not looking at the world economy and they do not even comprehend how bad things really are outside the United States. They do not comprehend what is an interest rate. It is the compensation to a lender for his anticipation of inflation plus a profit. If I think the dollar will decline by 50%, why would I lend you dollars for a year if when you pay me back it buys half of what it did when I lent it to you?

Debt can be a performing asset. I advised many of the Takeover Boys during the 1980s. We would borrow in one currency to buy the asset in another using the computer to distinguish the long-term trends. I would not recommend that to someone just operating on a gut feeling.

We were also advising on real values, which Hollywood distorted and based the movie Wall Street with Michael Douglas and his famous speech on greed. What they did not really understand was that after a Public Wave that peaked in 1981, stocks were suppressed and the full-faith in government created the broadly supported bond market. Hence – bonds were conservative and stocks were risky. There were two aspects that were behind the entire Takeover Boom.

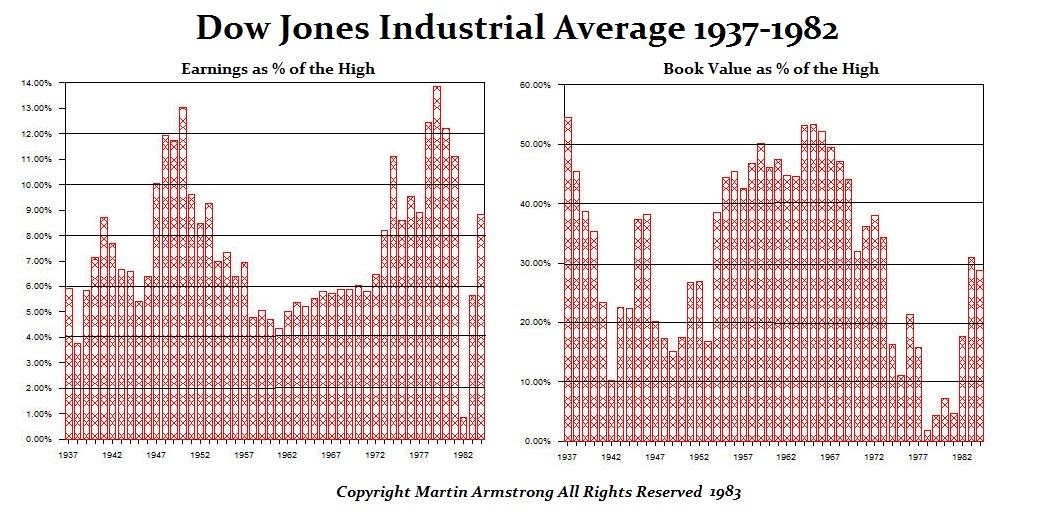

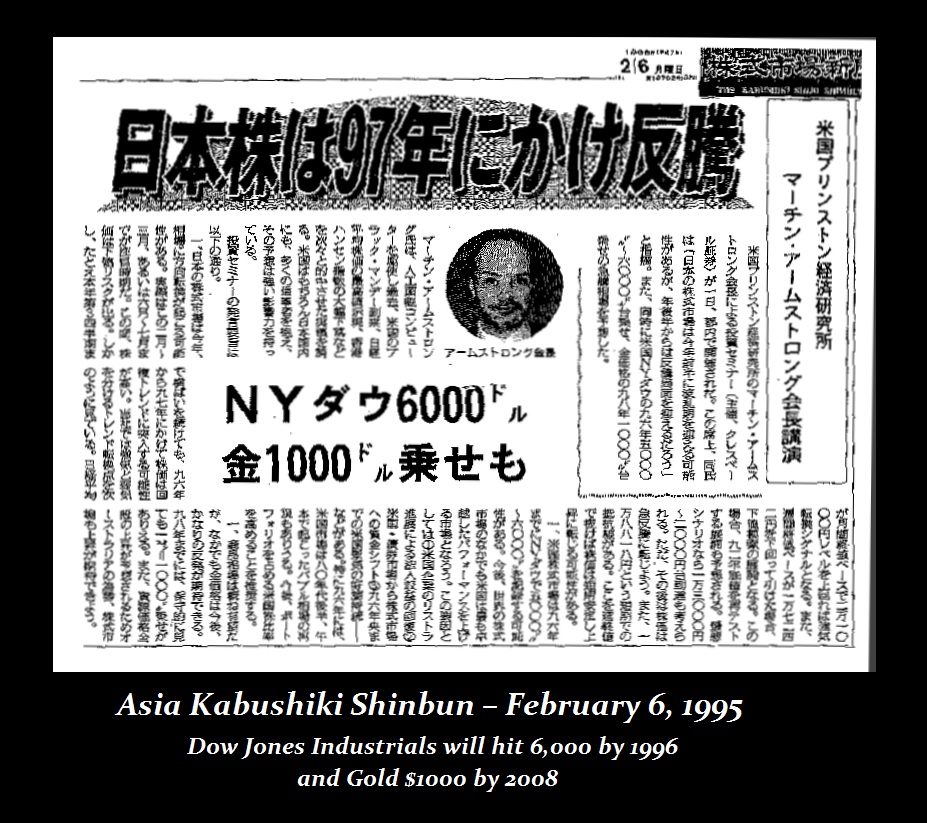

First, I was showing these charts and how in terms of book value, the Dow Jones bottomed in 1977. It was obvious that if you could buy a company, sell its assets, and double or triple your money, then the market was obviously not overpriced. We had forecast that the Dow was undervalued and that it would rise from the 1982 low of 769.98 and test the 2500 level in two years in 1985. Indeed, it reached 2695.47 by September 1987. We also projected that by the next decade, the Dow would test 6,000 on its next rally.

Even the press in Japan was shocked. We were also projected that Crude would fall below $10 in 1998. Indeed, that forecast was covered by Mark Pitman at Bloomberg News. It bottomed at $10.65 in 1998. In gold would forecast that it would drop to test $250 by 1999 completing a 19-year cycle low. Then gold would rally to test 1,000. Gold reached the $1,000 level by 2008. The Japanese press thought those forecasts were wild, to say the least.

The SECOND aspect of our advice to the takeover boys of the ’80s was something the press NEVER understood. We would advise borrowing in one currency for an asset in another. We were able to turn debt into a performing asset. We would make 20-40% profit on the currency alone. Often, the press would just look at the debt and not understand what we were even doing.

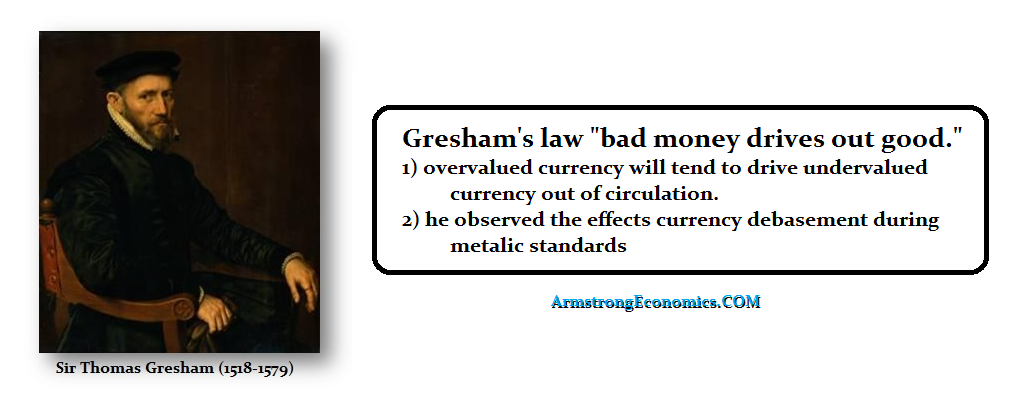

Most of this reasoning stems from Sir Tomas Gresham’s observations when he represented England at the Amsterdam exchange during the reign of Henry VI’s reign and debasement. As Henry debased the silver coinage as was taking place in Spain, the more they debased the coinage, the higher the inflation took place. His observation that bad money drives out the good has been grossly misunderstood. When I was growing up, they took the silver out of the coinage in 1965. People were culling out the silver showing that the debased new coinage of 1965 drove out of circulation the old silver coinage. The same thing has taken place with the copper pennings.

Because people hoard old coinage, the money supply shrinks. That then forces the government to issue far more debased coinage to compensate for the coinage that has been withdrawn from hoarding. Consequently, inflation unfolds for all tangible assets to rise in value as expressed in the newly debased coinage.

What these people always try to sell is the same old scenario that they cannot point to a single instance in history where everything collapses to dust but only gold survives. Such periods will typically result in revolution. When Caesar crossed the Rubicon, that was also all bout a debt crisis.

You must also understand that interest rates will be at their LOWEST internationally in the core economy of the Financial Capital of the World – which is the USA right now. The further you move from the center, the higher the interest rate will be. Hence, I have warned that the United States will be the LAST to fall – never the first. This is not based upon my opinion, this is simply historical fact.

The Bottom Line is very simple. There is just no such period as people describe where everything turns to dust and only gold survives. Even if that were true, they what good would the gold do if everything else is worth ZERO? Gold would have also ZERO value since nothing would have value.

The real issue is that as government defaults unfold, tangible assets will rise in value for the amount of money in debt always dwarfs that in even the stock market. We are in a Sovereign Debt Crisis and that is very different from a private debt crisis.

Federal Reserve Chairman Jerome Powell has made it clear that he sees higher interest rates ahead in his battle against inflation and their unrealistic 2% target. Many traders are now scrambling talking about how Powell said the Fed will probably raise rates more and possibly faster than previously anticipated. They are now taking that as a warning he may do a 50-bp hike this month. Our computer projected a Directional Change in 2022 and everything is on schedule for the rise into 2024.

Powell also restated his warnings to US banks about the risks of getting involved in the crypto industry. He expressed very clearly that lenders must take “great care” when engaging with cryptocurrencies. He added that the central bank didn’t want to prevent innovation, but it is not bullish on this industry and views it more like the DOT.COM Bubble.

Posted originally on the conservative tree house on March 7, 2023 | Sundance

Federal Reserve Chairman Jerome Powell delivers testimony today before the Senate Banking and Finance Committee. During his statements Powell says, “The latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated.” Powell continued, “If the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes.“… “We will continue to make our decisions meeting by meeting.” … “Although inflation has been moderating in recent months, the process of getting inflation back down to 2% has a long way to go and is likely to be bumpy.”

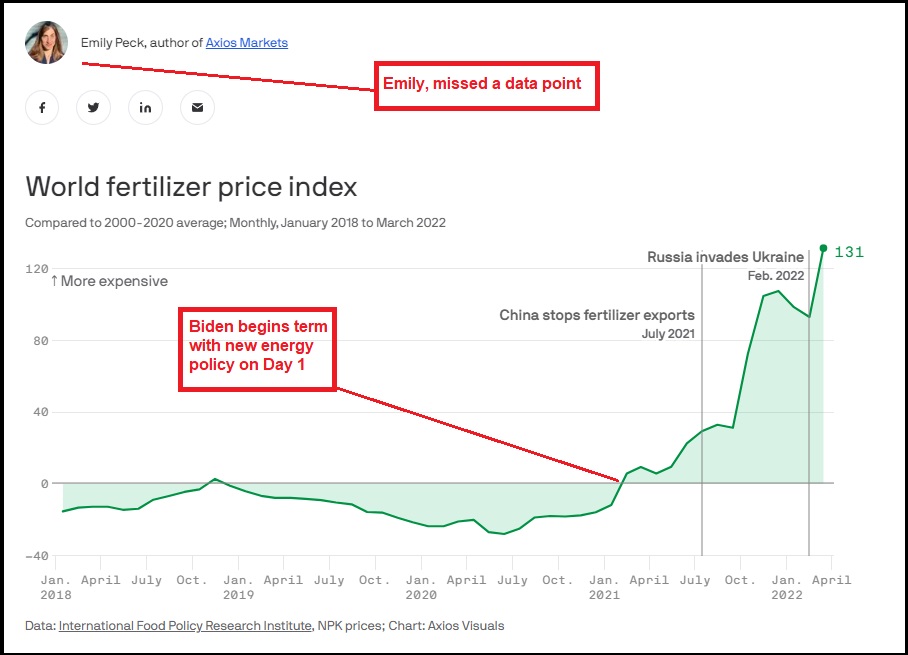

Everything about the testimony to the Senate, and almost everything within the questioning as presented, ignores the key and central component that inflation is being driven by energy policy. The scale of the pretending around this issue is jaw dropping.

Western governments, including the U.S. through Joe Biden, have limited and curtailed the production and exploitation of Oil, Coal and Natural Gas. At the core of the inflation within those same governments, this is the issue at hand. Energy prices have skyrocketed, driving the cost of everything through the roof. The central banks are raising interest rates in an attempt to shrink the economy to match the drop in energy production. This is their monetary policy (interest rates) attempting to support economic policy (Green New Deal / Build Back Better).

There are no lines for consumers in the U.S and Europe of people buying durable goods, electronics or shopping for non-essential items. Prices on the products within the durable goods economy are not being driven by excess consumer demand. There are not 25% more people buying lemons and milk than this time last year. The prices for goods in general, and for essential goods specifically, have risen as an outcome of the input costs around energy skyrocketing.

Everything is impacted by diminished energy production, and losses in infrastructure due to drops in investment, that contribute to the efficiency of energy distribution. Oil prices have jumped, gasoline prices, diesel prices, natural gas prices and electricity prices have all skyrocketed.

With those raw material production policies, farming costs, fertilizer costs, cooling and heating costs, electricity costs, home heating costs, transportation costs, packaging costs, storage and warehouse costs, refrigeration costs and everything impacted by major energy costs have increased. This is the main driver of consumer inflation.

When Jerome Powell says they are raising interest rates to “cool the economy,” the raw truth behind the statement is the central banks are trying to reduce the western economies in order to meet the diminished energy production created by policy. If they can make the economy smaller, less energy is needed….. and this should stem the rising costs from limiting the resource development.

Their problem is that baseline energy demand remains high. This is keeping energy prices high…. this is keeping inflation high. Their approach to continue raising interest rates, will only work if they achieve an economic outcome similar to the pandemic lockdown period.

Yes, excessive money does create devalued money, which in turn does create inflation. However, in the current inflationary dynamic it is not excessive money in the hands of working-class people that is driving high demand for goods. All of the consumer and sales data show that cash carrying consumers are not chasing limited goods. Consumers and workers are trying to afford essential goods and services that have increased in price as a result of energy policy.

Every economic analysis that does not take this majority factor into consideration is either: (a) making a mistake; (b) being intentionally obtuse and willfully blind; or (c) intentionally not discussing it because the motives of the analyst are to support the climate change agenda.

Once you accept that energy policy is the majority driving influence of current inflation (6.4%), then you can estimate how much economic damage will be needed in order to drop energy demand to a level that matches the diminished energy development, production and investment.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America