Honest journalism has become a crime. I have appeared numerous times on Maria Zaric’s program, Zeee Media. Maria is a professional journalist who asks thought-provoking questions to the experts that appear on her show. Her content goes against the grain and traditional narrative. The Australian-based journalist has been questioning COVID, the Great Reset, governments, globalists, the war in Ukraine, and many other topics that are completely taboo in the mainstream media. They attempted to shut down her channel in the past. Now, she has been de-banked with no explanation.

“Do you shut down peoples accounts due to their political views by any chance?” Maria asked the bank representative, only to be met with silence. Maria had been banking with ING Bank for numerous years without issues. Her account was suddenly shut down shortly after releasing a story on domestic terrorism in Australia. ING Bank has been unable to explain why her account was canceled.

Interestingly, ING is a partner of the World Economic Forum. Maria has extensively covered the WEF’s agenda to “enslave humanity.” Is Australia secretly keeping track of journalists’ “social credit scores” to silence skepticism?

The idea of eliminating someone’s ability to bank is essentially eliminating them from society. We saw Canadado the same thing to those protesting the Trucker Convoy. Trudeau took things a step further by also de-banking people who simply donated to the cause. The Canadian government used the premise of money laundering as a way to coerce the banks into reporting any activity that could have been intended to help the protestors. I know of numerous people who were frantically attempting to remove their funds from the bank during this time.

As if the public needed more reasons to lose trust in the banking system. This is not limited to one bank or country. I discussed how banks have the ability to “cancel” someone after JPMorgan Chase de-banked the rapper Kanye West for antisemitic remarks. The bank acts as the jury and judge. Epstein was permitted to hold funds at JPMorgan Chase despite an ongoing pedophile ring trial. Bernie Madoff banked with JPMorgan Chase. The bank has secret ties to the Third Reich and helped the group funnel money through South America during World War II. Again, the bank acts as the jury and judge; anyone can be de-banked anytime for any reason.

Most countries may not openly have social credit scores, but they’re keeping tabs on us. They are keenly aware that resistance to this New World Order is building. So they are now using professional journalists as examples hoping that people will stop asking questions to learn the truth. That is one of the reasons why this blog is free of charge – you deserve to know the truth.

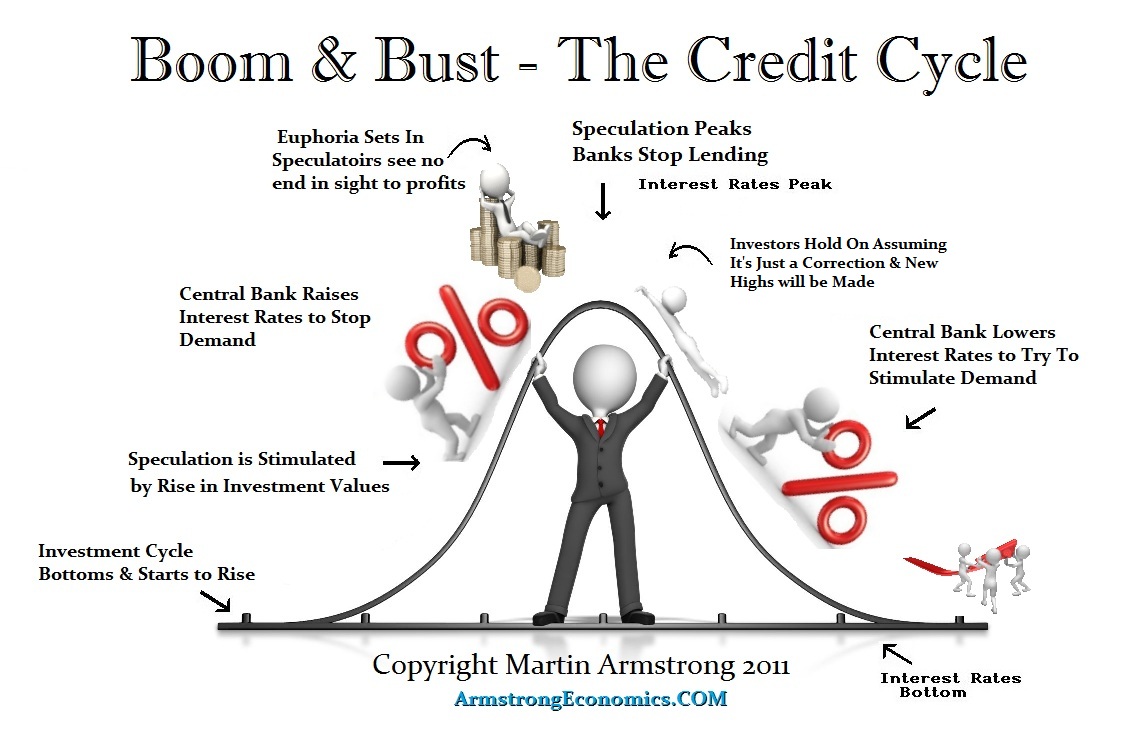

QUESTION: Marty there are a lot of people who seem to be trying to create a panic. Some are claiming the stock market will plunge by 50%. Others are saying nothing will survive other than gold. It seems like none of these people have any sense of what is really unfolding. They were saying the same thing for different reasons before the banking crisis. Can you offer any historical perspective?

Thank you. You seem to be the only real source these days.

Pete

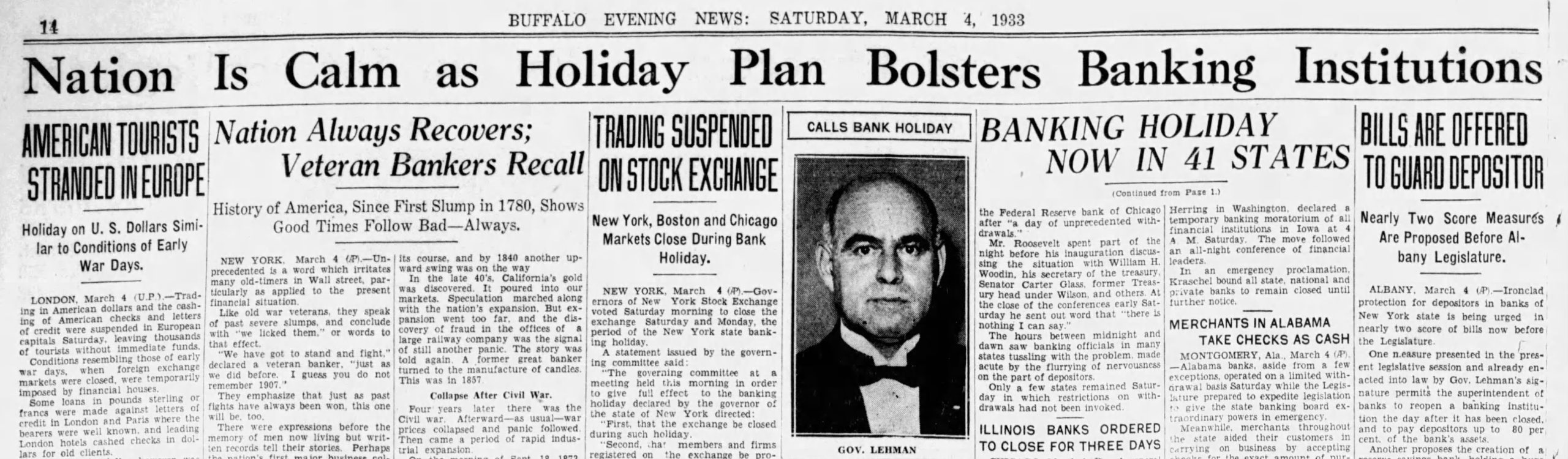

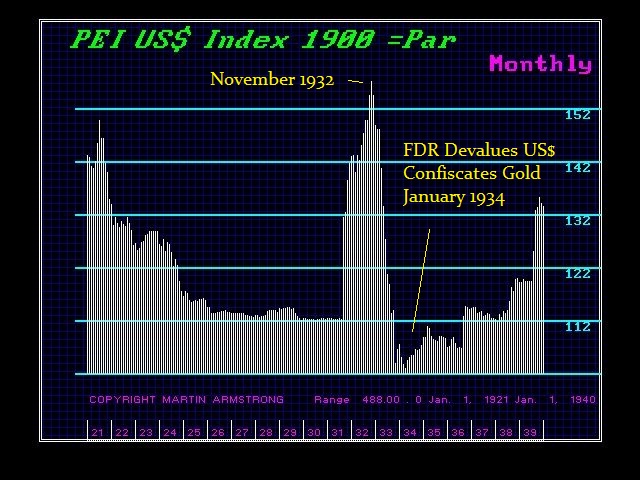

ANSWER: The Bank Holiday took place the first week of March 1933. It began with governors closing down the banks in their states. Once one began, like COVID rules, they quickly jumped on the bandwagon. As reported by March 4th, 1933, some 41 states had already declared a banking holiday. Back then, the president took office in March – not January. Thus, Roosevelt was sworn in on March 4th, 1933. As the new president, FDR delivered what is arguably his best-known speech.

“So, first of all, let me assert my firm belief that the only thing we have to fear is…fear itself — nameless, unreasoning, unjustified terror which paralyzes needed efforts to convert retreat into advance. In every dark hour of our national life a leadership of frankness and of vigor has met with that understanding and support of the people themselves which is essential to victory. And I am convinced that you will again give that support to leadership in these critical days.”

The following day, Roosevelt declared a national banking holiday on March 5th, 1933. Then Congress responded by passing the Emergency Banking Actof 1933 on March 9th, 1933. This action was combined with the Federal Reserve’s commitment to supply unlimited amounts of currency to reopened banks. Back then, they effectively created a de facto 100% deposit insurance and this was before the FDIC was created.

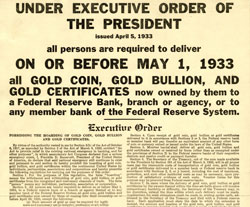

However, what the history books have omitted because it revealed the real reason for the major banking crisis, was the confiscation of gold precisely as Germany did in December 1922 seizing 10% of all assets which unleashed hyperinflation in 1923.

In Herbert Hoover’s memoirs (1951), he documents the fact that Franklin D. Roosevelt (FDR) played a very dirty game of politics. There were rumors that FDR would confiscate gold in 1932 BEFORE the election. These rumors spread and people ran to banks to withdraw their funds. The night before the election in 1932, FDR denied that he would do such a thing. After FDR won the election, the real bank panic began. FDR would not take office until March 1933.

The run on banks began as the Great Depression started. In 1929 alone, 659 banks closed their doors due to mismanagement and speculation. Ironically, to save money on paper, it was also in 1929 when the currency was reduced in size to save money. This time, they want to move to digital and save 100% on printing money. Here in 2023, the failures are due to the WOKE agenda which has deprived the banks of risk management rather than speculation.

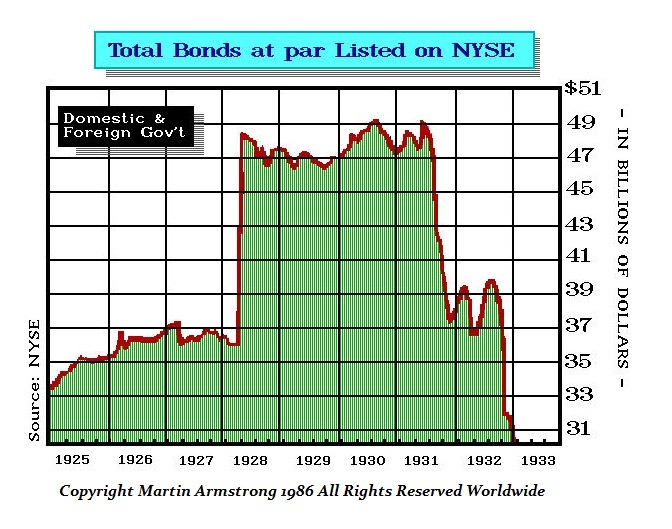

However, as the 1931 Sovereign Debt Crisis hit, the number of bank failures skyrocketed. Goldman Sacks and others were selling foreign bonds to Americans in small denominations., As Europe began to default, US banks holding foreign debt and individuals in need of cash led to a banking panic for external reasons. Here is a chart showing the listing of bonds on the NYSE. We can easily see the collapse in the bond market thanks to the 1931 Sovereign Debt Crisis.

By 1932, an additional 5,102 banks went out of business. Families lost their life savings overnight. Thirty-eight states had adopted restrictions on withdrawals in an effort to forestall the panic. By March 4th, 41 states had declared a bank holiday shutting down banks. Bank failures increased in 1933, and Franklin Roosevelt deemed remedying these failing financial institutions his first priority after being inaugurated.

However, it was actually the election of FDR that started the banking crisis post-1931. Hoover pleaded with FDR to please come out and address the gold confiscation rumors. People had been hoarding their gold coins fearing the rumored confiscation. Despite Hoover’s plea for FDR to come out and deny the rumors after the election, he remained silent. Given FDR’s manipulation of Japan and the attack on Pearl Harbor which he appeared to instigate with sanctions confiscating Japanese assets in the USA, denying the sale of any energy to Japan, and then threatening to use the fleet to block them from buying fuel from anywhere else, They Japanese attacked Pearl Harbor. There were Senate investigations afterward about FDR’s role because the US had already broken the Japanese code and knew in advance about the attack on Pearl Harbor. He did that to force the US into World War II.

It was in his character to remain silent and create the worst banking crisis in history before he was sworn in as president. FDR was a radical socialist and many viewed that he admired Lenin. If it were not for Mr. Jones exposing the truth behind Stalin, even the corrupt New York Times journalist promoting Stalinism was meeting with FDR. The run on the banks became massive when FDR won the election on November 8th, 1932. FDR allowed the banking system to implode with people rushing to withdraw the money in gold coins.

At 1:00 a.m. on Monday, March 6th, 1933, President Roosevelt issued Proclamation 2039 ordering the suspension of all banking transactions, effective immediately. Roosevelt had taken the oath of office only thirty-six hours earlier.

The terms of the presidential proclamation specified:

[N]o such banking institution or branch shall pay out, export, earmark, or permit the withdrawal or transfer in any manner or by any device whatsoever, of any gold or silver coin or bullion or currency or take any other action which might facilitate the hoarding thereof; nor shall any such banking institution or branch pay out deposits, make loans or discounts, deal in foreign exchange, transfer credits from the United States to any place abroad, or transact any other banking business whatsoever.

For an entire week, Americans would not have access to banks or banking services. They could not withdraw or transfer their money, nor could they make deposits. The entire economy ran simply on cash in your pocket.

While the first phase of the banking crisis unfolded after 1929 due to speculation losses (hence Glass–Steagall Act), then the second phase was the 1931 Sovereign Debt Crisis, it was the third phase with the election of FDR that led to thousands of banks failing as there was a mad rush to withdraw your gold coin. But a new round of problems that began in early 1933 placed a severe strain on New York banks, many of which held balances for banks in other parts of the country. About 4,000 banks failed during this period alone bringing the total to over 9,000.

Much to everyone’s relief, when the institutions that could reopen for business on March 13th, 1933 saw depositors standing in line to return their stashed cash to neighborhood banks. Within two weeks, Americans had redeposited more than half of the currency that they had withdrawn post-FDR’s election on November 8th, 1932. This would prove to be a sneaky trick of FDR to get people to redeposit all the gold coins they had withdrawn – as we are about to explore.

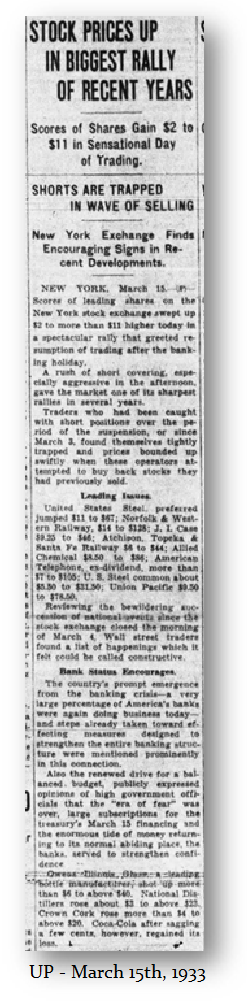

The stock market was also ordered closed when FDR came to power. With the cleverness of a real con artist operating a Ponzi Scheme to gain the confidence of the people, FDR needed the gold coin to be deposited for Phase 4 of the banking crisis. On March 15th, 1933, (The Ides of March), the stock market was allowed to reopen. On the first day of trading, the New York Stock Exchange recorded the largest one-day percentage price increase ever.

The week before the closure, the Dow Jones Industrials fell to 49.68. The week following the closure, the Dow rallied to 64.56 – a percentage gain of virtually 30% over the banking holiday. The shorts who were better on the collapse of the market once it reopened were devastated. It was a major short-covering rally.

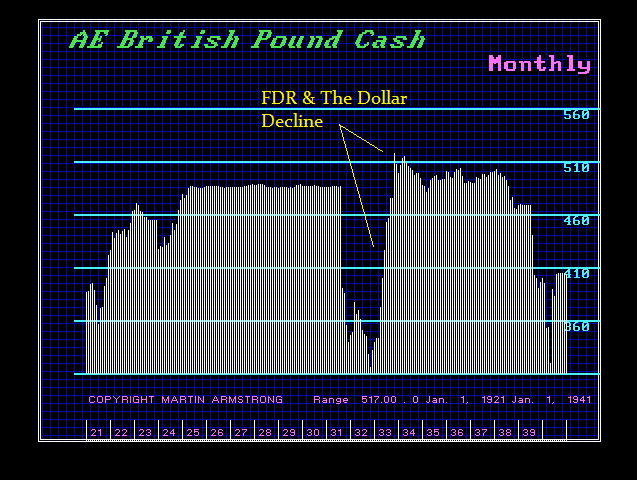

With the benefit of hindsight, the nationwide Bank Holiday and the Emergency Banking Act of March 1933, ended the bank runs that had plagued the Great Depression, but it also set the stage for the confiscation of gold. What you have to understand is that Franklin Delano Roosevelt’s (FDR) actions in 1933 were not directed simply at gold. He was embarking on what he called the New Deal, which was a Marxist Agenda that was very popular at the time. His New Deal would end austerity, whereby they were maintaining a balanced budget in the belief that they needed to inspire confidence in the currency.

It was this balanced budget philosophy that also inspired John Maynard Keynes who argued that in times of economic distress when the demand has collapsed, that is when the state needs to run a deficit and increase the money supply. There was a simultaneous international flight of capital from Europe to the United States in the face of European sovereign debt defaults. That capital flight lasted for nearly two years until FDR won the election in 1932. There was much concern that Roosevelt would do what Germany did in 1922 in confiscating assets. That was the rumor about the possible confiscation of gold.

Milton Friedman criticized the Fed because the capital flows poured into the US but they refused to monetize it. We can see that as Europe defaulted on its debts in 1931, the capital rushed head-first into the dollar. Then we see that the dollar peaked in November 1932 with the election of FDR fearing that would weaken the dollar and exploit the economy. All this gold came to the USA pushing the dollar higher, but the Fed refused to monetize it, was Milton’s criticism. The backing of gold behind the dollar doubled in supply between 1929 and 1931.

So, you must separate gold and the devaluation of the dollar to comprehend what the issue was all about. FDR could have simply abandoned the gold standard, as did Britain, and not confiscated gold. However, that would have also been sufficient to end austerity. But the bankers would have profited and sold the gold overseas at higher prices. Roosevelt in his confiscation of gold was intended to deprive the private sector of profiting from his devaluation of the dollar which was rising the price of gold from $20 to $35. You must keep in mind that he even degraded Pierre du Pont (1870-1954) and called him the “Merchant of Death” because he produced arms for World War I and made a profit off of that war demand. Many saw Roosevelt as a traitor to his own class.

The confiscation of the gold was for two reasons. First, FDR was changing the monetary system from one where there was no distinction domestically from internationally to a two-tier system. Gold would freely circulate without restriction only internationally. Therefore, the confiscation of gold was altering the monetary system moving to a two-tier monetary system with gold only used in international transactions.

Consequently, FDR confiscated gold to move to a two-tier system and to deprive Americans of any profit from his devaluation. What FDR then did was confiscate gold from all institutions ordering them to turn over whatever they had. Ironically, this move was intended to target bankers rather than the public. FDR did not have people knocking on every door demanding all their gold. That is why there are plenty of US gold coins that have survived. If individuals possessed them rather than an institution, then they kept what they owned

Therefore, Roosevelt was able to seize whatever gold existed in banks. He declared all contracts void that had gold provisions for payment. It was in Perry v. United States – 294 U.S. 330 (1935) that the US Supreme Court ruled that Congress, by virtue of its power to deal with gold coin as a medium of exchange, was authorized to prohibit its export and limit its use in foreign exchange. Hence, the restraint thus imposed upon holders of gold coins was incidental to their ownership of it, and gave them no cause of action. id/P. 294 U. S. 356.

The Supreme Court held that it could not say that the exercise of this power by Congress was arbitrary or capricious. id/P. 294 U. S. 356. They held that even if the Government’s repudiation of the gold clause in the government bonds was unconstitutional, it did not entitle the plaintiff to recover more than the loss he has actually suffered, and of which he may rightfully complain. id/P. 294 U. S. 354. Therefore, the Joint Resolution of June 5, 1933, held:

“insofar as it undertakes to nullify such gold clauses in obligations of the United States and provides that such obligations shall be discharged by payment, dollar for dollar, in any coin or currency which at the time of payment is legal tender for public and private debts, is unconstitutional.” id/P. 294 U. S. 349.

Yet, swapping gold for dollars created no loss that was cognizable even though the taking of gold was unconstitutional. Clearly, the Supreme Court did not consider the loss in terms of foreign exchange. The Court reasoned:

“Plaintiff has not attempted to show that, in relation to buying power, he has sustained any loss; on the contrary, in view of the adjustment of the internal economy to the single measure of value as established by the legislation of the Congress, and the universal availability and use throughout the country of the legal tender currency in meeting all engagements, the payment to the plaintiff of the amount which he demands would appear to constitute not a recoupment of loss in any proper sense, but an unjustified enrichment.”

In my understanding of the law, those who argued before the Court made purely a domestic argument. A dollar was still a dollar in domestic terms so there was no cognizable loss and the Court did not reach the constitutional question. Had they argued that their loss was with respect to some debt owed in British pounds, they there was a loss. Purely domestically, the only loss would have been to inflation and the Court would never rule against the government on such an issue.

All of that said, there does not appear to be any historical precedent for the stock market to collapse by 50%, all tangible assets to turn to dust, and only gold will survive given a banking crisis where Biden and Yellen sit on each other’s hands and do nothing. Trust me. Every major Democratic donor will be screaming. And as for those claiming the Fed will reverse its position, say inflation is suddenly no longer a problem, and monetize everything in sight, this is even too big for the Fed. have to create QE and absorb all the debt, there to things have changed. If the Fed does that, it will also lose all credibility. It squarely understands that inflation comes from handing Ukraine a black check to the most corrupt government in the world. The Fed raised rates yesterday for it cannot back down. It is choreographing the best it can but the bankers do not listen.

If they simply stand behind all the deposits, then there will be no panic. That is what they did in 1933 and the market rallied in confidence thereafter.

There once was a time when cash was the undisputed king. Merchants preferred cash payments over credit, and there were often incentives for paying with paper. I recall receiving lower gas prices when paying with cash, for example. It is increasingly common to see “no cash accepted” signs at establishments as the world moves toward a cashless society. At the Federal level, there are no laws protecting consumers who wish to pay in cash. The Federal Reserve stated on its website:

There is no federal statute mandating that a private business, a person, or an organization must accept currency or coins as payment for goods or services. Private businesses are free to develop their own policies on whether to accept cash unless there is a state law that says otherwise.

"Section 31 U.S.C. 5103, entitled "Legal tender," states: "United States coins and currency [including Federal Reserve notes and circulating notes of Federal Reserve Banks and national banks] are legal tender for all debts, public charges, taxes, and dues." This statute means that all U.S. money as identified above is a valid and legal offer of payment for debts when tendered to a creditor."

Yet, the Federal Reserve also recognizes that as of 2021, 4.5% of US households were “unbanked.” This means that 5.9 million households are unable to pay by card. This is the lowest unbanked rate since the Fed began keeping track in 2009. The most common reason for not having an account, reported by 21.7% of unbanked households, is that they do not meet minimum balance requirements. The second most reported reason (13.2%) is that people simply do not trust banks, while the third most cited reason (8.4%) was the desire for privacy.

If merchants refuse to accept cash, these people cannot participate in consumerism. Their legal tender is simply not accepted. Unbanked households are more likely to contain persons with lower levels of education, lower incomes, disabilities, single mothers, and minorities. As the Fed reported:

“Differences in unbanked rates between Black and White households and between Hispanic and White households in 2021 were present at every income level. For example, among households with income between $30,000 and $50,000, 8.0 percent of Black households and 8.4 percent of Hispanic households were unbanked, compared with 1.7 percent of White households.”

If cash is legal tender, then it should be accepted everywhere. Numerous merchants not only refuse cash but they charge an additional fee for using credit. Tennessee, Arizona, Delaware, District of Columbia, Idaho, Maine, Massachusetts, Michigan, Mississippi, New York, North Dakota, Oklahoma and Pennsylvania, New Jersey, Rhode, Colorado, and Connecticut have laws at the state level protecting cash payments. Some cities such as Washington D.C., Berkley, Chicago, New York City, Philadelphia, and San Francisco also have laws in place. However, I can assure you that many retailers in these areas still do not accept cash.

Washington wants to move us toward a cashless society to tax everyone, even those with the least to give, on every transaction we make.

A bank failure of this proportion has not been seen since 2008 when Washington Mutual failed. The majority of deposits in Silicon Valley Bank (SVB) are uninsured, meaning the FDIC’s $250,000 protection does not apply. Uninsured depositors will be provided receivership certificates and should receive an advanced dividend this week. The FDIC must sell off the remaining assets of SVC to determine how much it can provide to those uninsured depositors. The FDIC is encouraging borrowers to continue paying their existing loans. The bank was said to host $209 billion in assets and $175.4 billion in deposits as of December 2022. Washington Mutual held around $307 billion in assets when it went down.

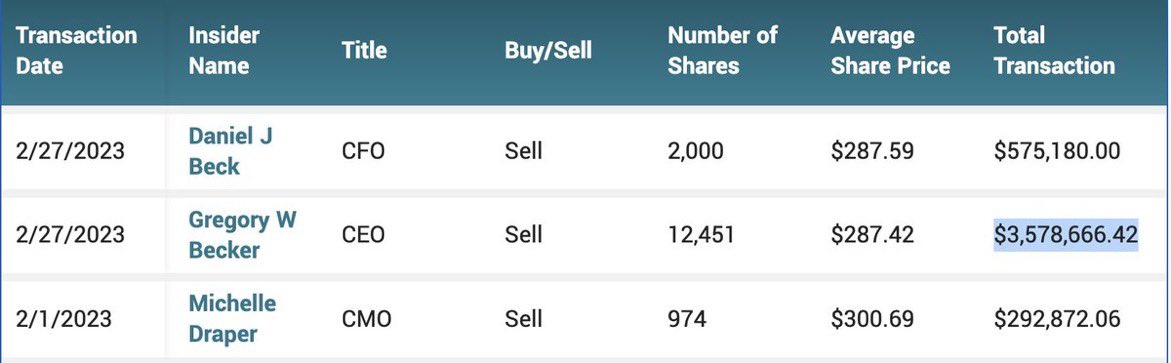

Tons of people and businesses will be completely screwed over. Who could have seen it coming? Silicon Valley Bank CEO, CFO, and CMO sold off millions in stock over the past two weeks. President and CEO Greg Becker sold 12,451 shares on February 27 for $3.6 million at $287.42 per share. Later that day, he purchased options for the same amount of shares at $105.18 a piece. He did the same thing in December 2021, as this is not an uncommon albeit unethical practice. Banks commonly trade against their own clients. Becker sold about $3.57 million worth of SVB stock over the past two weeks and is now making TV appearances saying he did not see this coming.

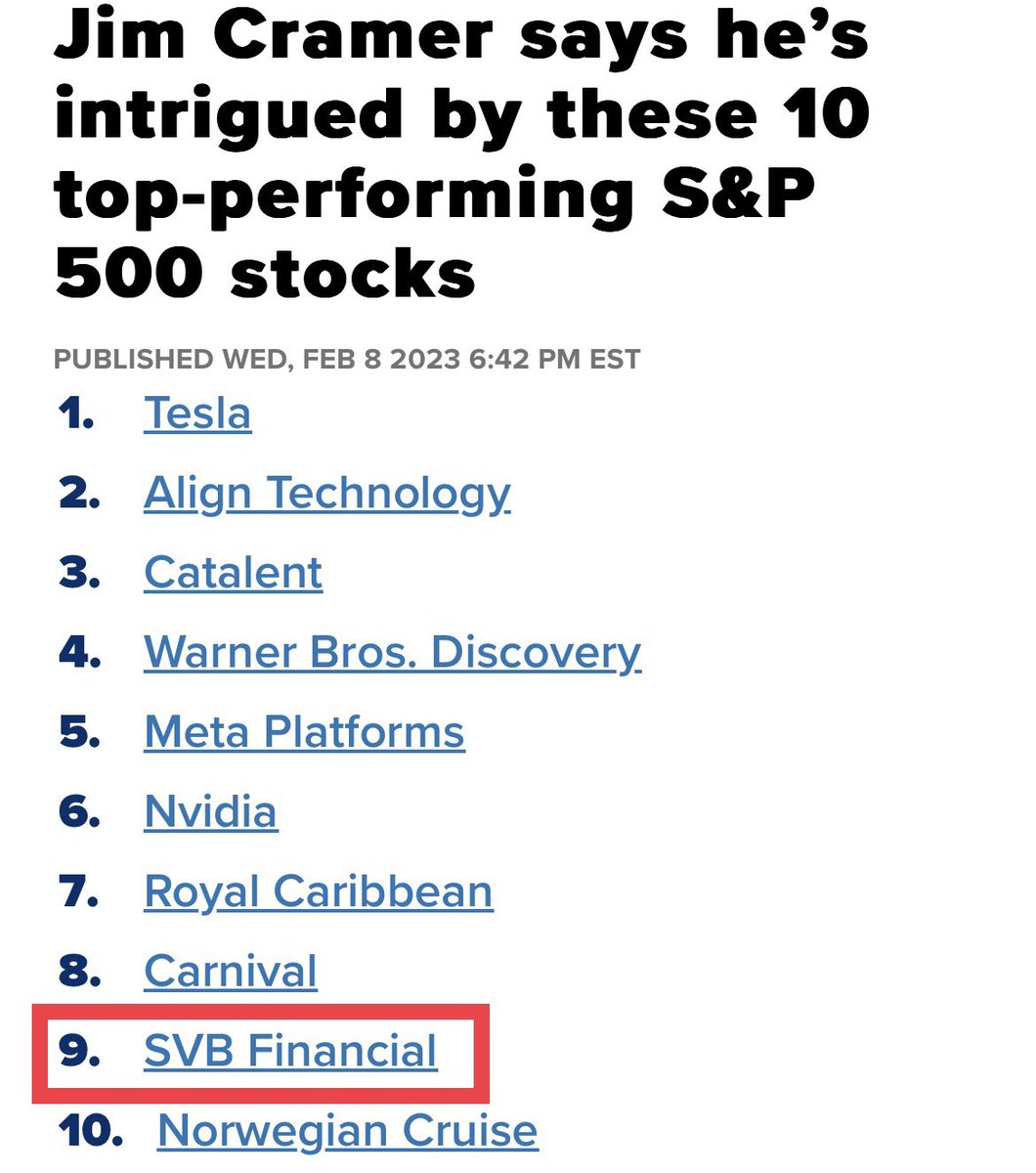

There were signs of trouble, but the talking heads said otherwise. Forbes even listed SVB Financial Group as #20 on its list of America’s Best Banks in an article published on February 14, 2023. Talking/screaming head Jim Cramer came out last month to say that SVB Financial would become one of the top performers on the S&P. This is why you cannot listen to information based on biased opinions. I hesitate to call this negligence technical analysis.

Companies are now at a complete loss, many cannot make payroll, and this situation will only worsen once the uninsured depositors realize their IOUs are worthless.

Posted originally on the CTH on March 11, 2023 | Sundance

South Dakota Governor Krisi Noem appeared on Tucker Carlson’s television broadcast last night to send a warning to fellow governors. According to the background story, the South Dakota legislature passed a bill redefining currency and creating rules for a Central Bank Digital Currency (CBDC) that would block all other digital currencies from being used in the state. Governor Noem vetoed the bill.

When asked why her legislature would do this, Noem responded the state politicians likely did not read the bill as it was constructed by lobbyists. Noem is exactly correct and hits on a subject we have discussed here frequently {GO DEEP}. However, one of the more alarming aspects to Noem’s discussion of the issue is that around 20 other states are considering similar legislation. WATCH:

In times of economic distress, people will hoard their wealth. This is as true in ancient times as it is in modern times. I was called in about a hoard of gold – one thousand $20 St Gaudians gold coins all dated 1924 – uncirculated. As you see, I have a reputation for buying hoards as well as funding major archaeological digs. This was a hoard of US$20 gold coins. So I took the lot. As for those who say I hate gold, no, I have always loved the $20 st Gaudens.

Obviously, this was a stash. It was the year of a Presidential election and in 1925, Calvin Coolidge was the first President to have his inauguration broadcasted on radio. In 1921 the Chinese Communist movement began and in 1924 Stalin came to power after poisoning Lenin and his wife. The flight from Russia began in 1917, but it escalated by 1919. It is hard to say why this hoard was stashed away. But they are all dated 1924 and may have been connected to the upheaval in Russia. By the end of 1919, it was clear to almost everyone that the Bolsheviks had won the Civil War. The White armies were defeated on all fronts: Siberia, the Russian North, and Petrograd (as St Petersburg was then called). Pravda on Aug. 31, 1918:

“Our cities must be mercilessly cleansed of the bourgeois rot. All these gentlemen will be put on file, and those who pose a danger to the revolutionary class will be destroyed … Henceforth, the hymn of the working class will be a song of hatred and revenge! ”

It was the White Russians who fled. It was estimated that at least 2 million fled Russia at the time. That was about 2%-3% of the surviving population by 1919. Given the date of this hoard and the condition, they were tucked away and never saw circulation. They may have been related to the turmoil in Russia.

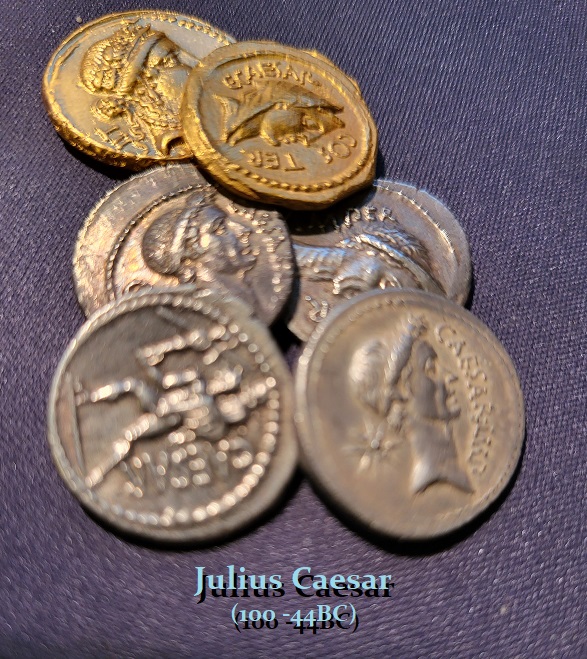

A number of people have asked if I could put together sets of the 12 Caesars because I had mentioned I thought that could be done for half the price of the set being offered elsewhere. I am trying to get a small hoard of Caligula denarii. They are very difficult to find. I believe because he was so hated, they may have just melted down his coinage.

It all depends on quality. I have purchased a small hoard of Julius Caesar coinage. I will try to see If I get these Caligula denarii. If I do, I will try to see if I can put together some sets with much more realistic prices.

I have purchased a hoard of late Constantine bronze. They are very reasonable.

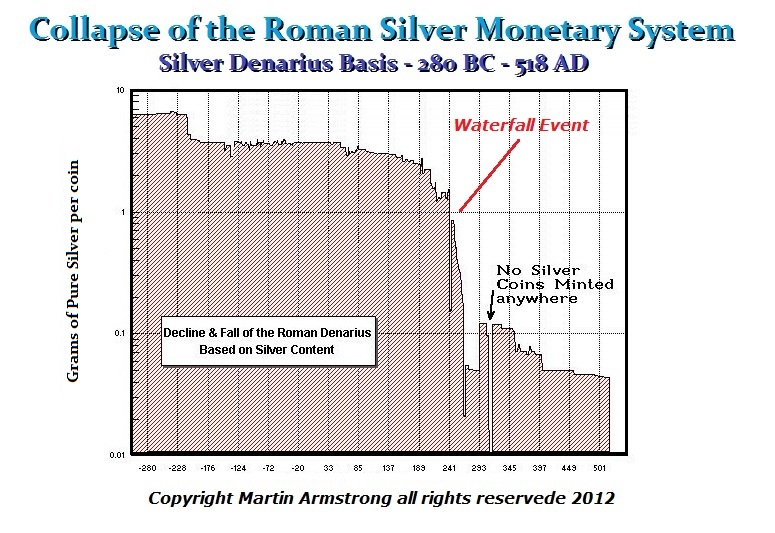

I have purchased an early hoard of Gallic coinage of Postumus which is silver. I also have purchased a hoard of Victorinus which are bronze. This is the period of both the split in the Roman Empire as well as the collapse of the monetary system.

Others have asked if I can put together a progression of the coinage showing the debasement. I will try. Here is a photo showing the stark difference between the beginning of the region of Gallienus (253-268AD) and its end.

COMMENT: Mr. Armstrong, Now with Switzerland outlawing a cashless society, I understand your point that cryptocurrency is really a dead end. Without power, it cannot exist and as you said in times of war, you take down the power grid and they can do that with an EPM pulse. These Bitcoin zealots are clueless about history and humanity. It’s just another way to separate a fool from his money.

Thank you for the education

BH

REPLY: The whole blockchain was the perfect creation of a totalitarian state. They can trace everything. How would you bribe politicians? It would all have to revert to barter. Do this and I will give you that – off the grid. This is why people are still buying real estate, precious metals, ancient coins, art, collectibles, and various things that are tangible and are thus off the grid.

Having funds in any cryptocurrency is still on the grid. When I was one of the three top market-makers in gold back in the ’70s, the IRS walked in and said they declared me to be a bank. Thus, I was supposed to report every transaction of $10,000 or more. They acknowledged I did not realize I was a bank, so they waived the fines. They seized all my records and went off to audit over 3,000 clients. They claimed that gold was not DEMONETIZED as money, just suspended for a while. I retired because I was supposed to report customers but not everyone else in the field. My lawyers said I could fight it. It would take years. My model warned that gold would decline for 19 years anyway so I choose to retire. The clients still wanted the research and thus Princeton Economics was spun off separately.

They can declare every person running an exchange in crypto is now a bank and must report every transaction. They can be put them out of business in the blink of an eye. These people have no idea who they are messing with. You will not win. All this is because of their twisted view of fiat money. They no more understand money and assets any more than Karl Marx.

During inflation, assets rise in value, and money declines. That took place during the 19th century when a gold coin was money. MONEY has NEVER been of a constant value – NEVER! These people yelling fiat simply do not comprehend that for thousands of years, there has always been a business cycle and that means money rises and calls in purchasing power REGARDLESS of whatever it has been. The fiscal irresponsibility of governments is well documented throughout history long before paper money.

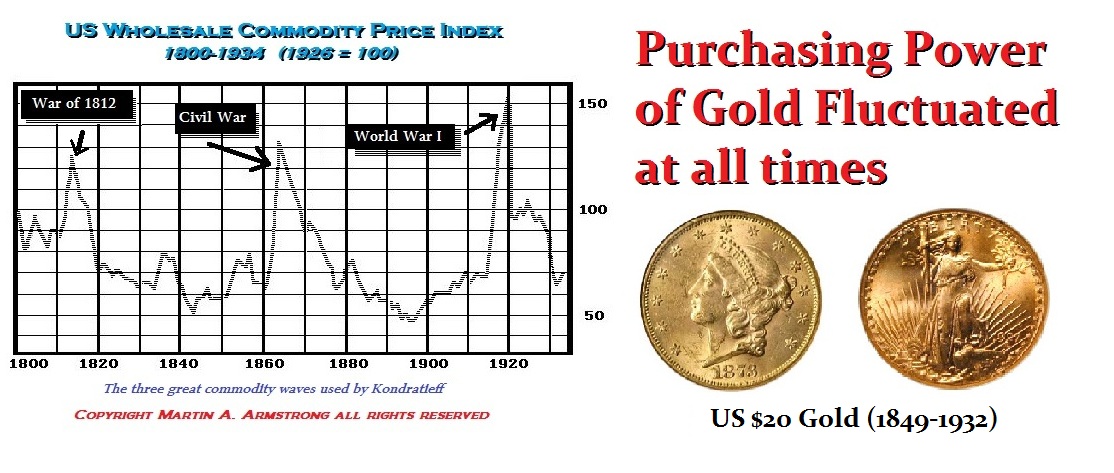

Even under a gold standard, there were periods of inflation and deflation. Read the history of the California Gold Rush. During the 1849 Gold Rush in California, the journalist for the New York Tribune, Bayard Taylor (1825-1878), arrived in San Francisco by ship during the summer of 1849. He was shocked at what he encountered and did not think that anyone would even believe what he was going to write. His dispatches about the gold rush economy in California stunned many and helped to create the 1849 Gold Rush.

The average wage for a laborer in New York was about one or two dollars a day. In California, individual hotel rooms were rented to professional gamblers for upwards of $10,000 a month, which is the equivalent of about $300,000 today. The degree of inflation in terms of gold was astounding and lacks comparison in modern times. There was so much gold, that the value of goods rose even though they did not in New York. The inflation phenomenon was local.

Gold became so common; they were even striking $50 gold coins in California when $20 was the highest denomination elsewhere and $1-dollar coins down to 25 cents all in gold. Eventually, there were $1 gold coins minted in the United States for general circulation throughout the USA. Indeed, Taylor wrote:

“[One] citizen of San Francisco died insolvent to the amount of forty-one thousand dollars the previous autumn. His administrators were delayed in settling his affairs and his real estate advanced so rapidly in value meantime that after his debts were paid, his heirs had a yearly income of $40,000 [$1.2 million today].

“These facts were indubitably attested; everyone believed them, yet hearing them talked of daily, as matters of course, one at first could not help feeling as if he had been eating ‘of the insane root.’”

It does NOT matter what is money. It will always rise and fall as measured against tangible assets as it has done since Babylonian times. In fact, the very first attempt to control inflation, as the central banks are doing right now, were the wage and price controls put in place by the legal codes of the Assyrians and Babylonians.

So – stop the BS. Understand that there are times when CASH will be king regardless of what money is at that moment in time, and then it will fall in value when everyone wants tangible assets. There is a business cycle – learn to live with it and we will be better off. The hard-nosed cryptocurrency zealots will never admit they are wrong. They are like politicians and will cling to their theories no matter what evidence you show them.

I asked one once, to name a single period in history where money was constant and never declined in value. He could not!

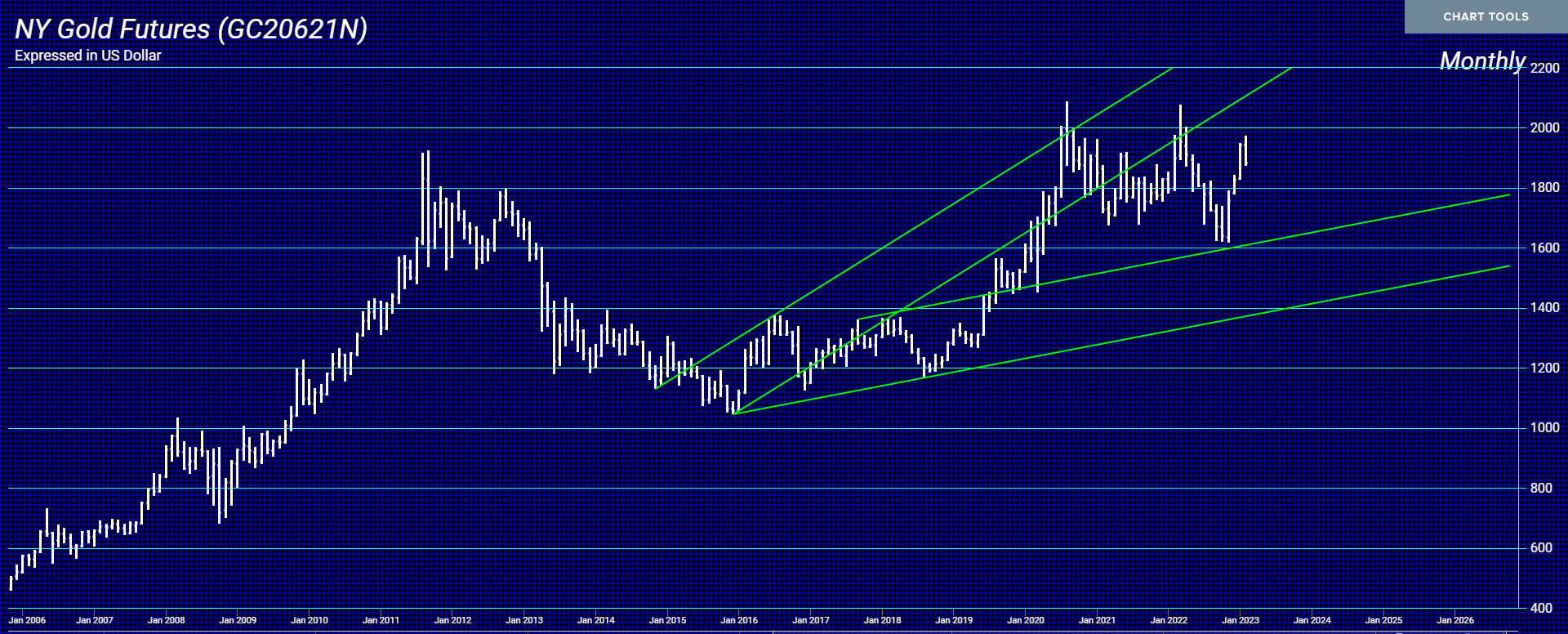

Bitcoin is an instrument for trading. This very chart CONFIRMS it is by no means a store of wealth. It rises and falls like ant commodity of stock. It is still influenced as part of the business cycle. Sorry – there is NOTHING that is a perfect store of wealth. Everything fluctuates. Trade Bitcoin, that is fine. But do not make a religion out of it for you will lose not just your shirt, but your pants as well.

Of course, the Goldbugs always misinterpret a rally in gold. The buying coming from China is in preparation for war – not bullish gold for the sake of gold. I have warned that if war was coming, then you will see China start to sell off US Treasuries. You certainly do not fund your adversary’s war against yourself.

China was buying aggressively during January, but they have backed off slightly. January was simply the standard 3-month reaction. The strong gold buying from China corresponded to China’s accelerated selling of U.S. Treasuries.

China is not buying gold because they think it will rally. It is perfectly fine if the price declines and just consolidates. They know war is coming and they can no longer maintain their reserves in dollars, euros, or yen no less than anyone else in the West – it all must go! Gold offers a non-political affiliation – neutrality. This is not buying gold as if it were an investment. We have completely different motives going on. Our own model warns that by 2032, there will be no United States acting as the reserve currency. The Biden Administration has done everything perfectly to destroy the world economy and the sad part about it, these morons do not even understand what they have done.

Tony, a reader, sent in a question. Message: “Mr. Armstrong what do you make of attorney general Merrick Garland’s recent approval to seize all of Russia’s assets that had been frozen in the United States to be given to the Ukraine?” Garland is violating every principle of international law. Denying Due Process of Law which comes from the Bible. When Cain killed Abel, God summoned him and gave him an opportunity to be heard, despite the fact he knew what he did. That is Due Process of Law – the right to be heard. What Garland is doing is outright unconstitutional and it is Treason to the foundation of every principle upon which this nation was founded.

The right to be heard resides in both the Sixth Amendment as well as the Fourteenth Amendment. A right to hearing entails that an individual maintains and be afforded the legal right to be heard in the venue of a court of law with adequate due process attached. Garland has shown he is violating the Civil Rights Act and is unworthy of holding any office whatsoever. If he were not in charge of the Department of Justice, he would be criminally prosecuted under 18 U.S.C. § 241.

18 U.S.C. § 241

Section 241 makes it unlawful for two or more persons to agree to injure, threaten, or intimidate a person in the United States in the free exercise or enjoyment of any right or privilege secured by the Constitution or laws of the United States or because of his or her having exercised such a right.

You cannot take anyone’s assets without Due Process of Law – PERIOD!

The confiscation of Russian assets is a clear violation of international law. They are including money confiscated from individuals as well. The destruction of NordStream was an act of economic warfare. These are acts that demonstrate what I have been saying – this is a war to DESTROY Russia. That is why Zelensky has instructed no peace negotiations. This has been planned for the fake Minsk Agreement. The West wanted to conquer Russia and they are prepared to see every Ukrainian die to weaken Russia so they will then send in Poland with tanks to conquer Moscow.

We are the aggressor. This is a Climate Change War and the end goal is a New World Order with one government. The current monetary system is collapsing. I believe Schwab’s Great Reset is our 2032. He knows our model. He realizes it is all collapsing. He is out to push it in his direction when the tree of liberty falls.

The current administration of the United States is out of control. It is destroying everything that we have worked for generations since World War II and it now even supports the nazis we once fought against.

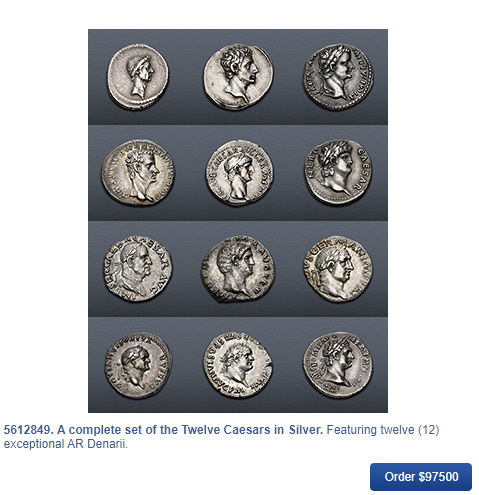

A lot of people have been asking if we have any more coins to sell from hoards. Another sent this photo in and asked what would a set of the 12 caesars cost. I personally think that the price of $97,500 is too high. I think a Very Fine set would probably be half that price. The hardest coins to find are Caligula and Otho.

I may be able to put together sets of Gallienus from the various mints after the debasement. Also a set of Constantine the Great, with Constans, Constantine II and Constantius II small bronze AE3s.

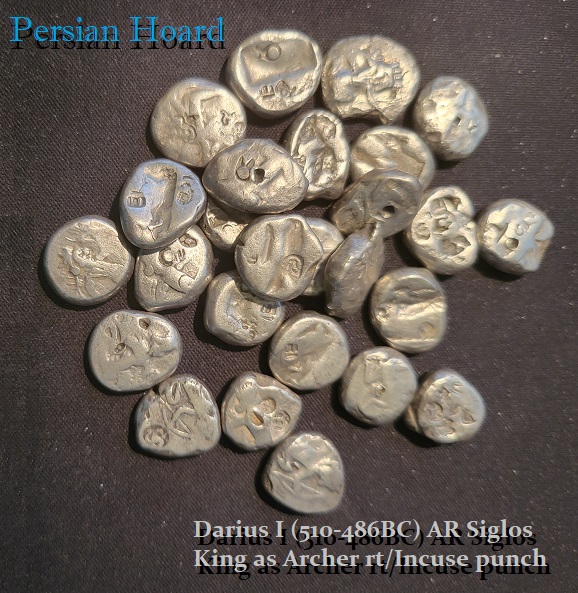

I have only a few of the Persian Darius I (510-386BC), the Persian king who invaded Greece. These are worn siglos all counter-stamped with banker marks. The image is that of the King as an archer with the reverse just a punch mark. I also have some late Constantine family small bronze issues. I will look to see what sets I can make up.

I have been asked if I can still offer some of the later sets once again.

(1) 253AD until the Tetrarchy of Diocletian and Maximinus in 284AD runs about $2500 for 18 coins.

(2) Denarii from Domitian to Gordian III in VF-XF condition (14 coins) runs about $2,000.

(3) Then the silver Antoniniani from Gordian III to Volusion (6 coins) are about $900

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America