Armstrong Economics Blog/Economics

Re-Posted Jul 4, 2019 by Martin Armstrong

QUESTION: You said the “crash is in the debt markets”. Can you please explain how that will evolve?

Liz M.

ANSWER: Once upon a time before 1971, there used to be a difference between debt and cash. Government bonds were not acceptable for collateral. You could not borrow against them. You had to liquidate them. This is why they once believed that it was LESS INFLATIONARY to borrow than print. Today, you can buy TBills and post them as collateral to trade futures contracts.

When paper money was beginning during the American Civil War, the government issued compound interest currency. In reality, this was merely currency that paid interest. Therefore, they were a hybrid where they were actually bonds that circulated as if they were a currency. We have returned to that whereby TBills are a street name and are good collateral so they have become the equivalent of bearer bonds that merely serve the purpose of currency.

Hong Kong Peg & Riots

Armstrong Economics Blog/Hong Kong

Re-Posted Jul 3, 2019 by Martin Armstrong

Civil unrest is continuing to rise in Hong Kong after crowds of mask and helmet wearing demonstrators fled the area to escape hundreds of riot police firing tear gas. The entire issue has arisen from Lam’s government pushing legislation that would allow extraditions to China, a move that alarmed locals and multinational companies. The clashes have embarrassed the government in Beijing. The demonstrations came on the anniversary of the former British colony’s return to Chinese rule.

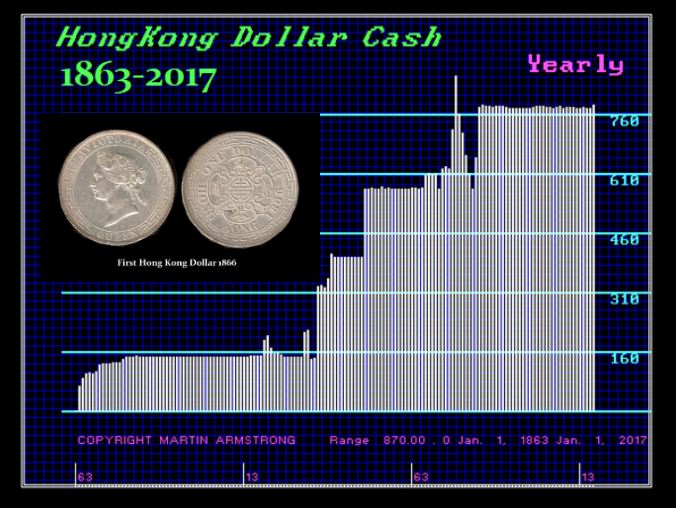

In 1863, the Hong Kong Government declared the silver dollar (a form of international currency issued by many nations) to be the legal tender for Hong Kong. In 1866, the government began issuing a Hong Kong version of the silver dollar. The silver standard became the basis of Hong Kong’s monetary system until 1935, when during a world silver crisis, the government announced that the Hong Kong dollar would be taken off the silver standard and linked to the pound sterling at the rate of HK$16 to the pound.

In 1972, the Hong Kong dollar was pegged to the U.S.dollar at a rate of HK$5.65 = US$1. Between 1974 and 1983, the Hong Kong dollar floated. On October 17, 1983, the currency was pegged at a rate of HK$7.8 = US$1 through the currency board system.

The problem Hong Kong will face is as the financial crisis in Europe erupts it will push the Greenback higher. If Hong Kong keeps desperately trying to hold the peg, they will import DEFLATION and turn their economy down very hard all because of international events. The models we showed at the Singapore Conference targeted 2019 for an important turning point.

The Hong Kong dollar peg climbed as much as 0.19% to 7.7987 a dollar on Tuesday, crossing the 7.8 threshold. Local interbank rates remain near a decade high, outstripping the income a trader can expect on U.S. dollars. That’s undermining a carry trade — sell Hong Kong dollars, buy greenbacks — that had been profitable for years.

The tight liquidity is coinciding with dramatic street protests. There has been a surge in borrowing costs suddenly. Companies are hoarding cash.

Custodial Risk in the Post MF Global Era

Armstrong Economics Blog/Corruption

Re-Posted Jul 2, 2019 by Martin Armstrong

QUESTION: Martin:

You have occasionally made short-quick comments that have made me loose sleep ! One of your past comments quipped that we equity/bond investors should entertain the idea of having the actual certificates to our stock/bond investments (which are typically digital entries held at brokerage houses) mailed directly to us instead of having them held in places like Depository Trust Company (Cede & Co). My question is—if a contagion occurs and/or mass panic erupts like in 2008, would this type of situation be a serious threat to getting our money/investments back, since the actual certificates for 98% of investors are not held personally, but instead seem to be held in a “step-ladder type of depository companies—supposedly for our benefit ??

PW.

ANSWER: The biggest danger is that the New York boys OWN the SEC and the TREASURY. When MF Global went bust because of trading by ex-Goldman Sach’s Jon Corzine, using their client’s money to trade in London, he was NEVER prosecuted for illegally using $1.6 billion of 26,000 client’s money. He was well connected right into the White House with Obama. Nobody went to jail and clients had to wait in bankruptcy to get their money – even cash in the accounts. There are clear risks with the broker and clearer. As long as the SEC is in gold of former Goldman Sachs staff, there will NEVER be an honest regulator. Trump promised to drain the swamp, but he is surrounded by too many swamp creatures. Even when all the banks pled criminally guilty, the SEC exempted everyone from losing their licenses. They would NEVER do that with anyone outside of New York City. The SEC will never prosecute the banks – EVER!!!!

Indeed, several federal investigations had been launched into MF Global, including probes by the Commodity Futures Trading Commission (its main regulator), the Securities and Exchange Commission, the Federal Bureau of Investigation, and Justice Department prosecutors in both Chicago and New York. The brokerage has also been the focus of several congressional hearings. Not a single one charged Corzine with trading with client’s money. The losses that eventually drove MF Global into bankruptcy stemmed from high-risk bets on European sovereign bonds that Corzine made as he swung for the fences. Corzine bet big that the bond issuers would not default.

Commodity Futures Trading Commission simply fined Jon Corzine only $5 million over MF Global’s rapid descent into bankruptcy on Oct. 31, 2011, as an estimated $1.6 billion of customer money went missing. Anyone else would have been in prison for a minimum of 20 years.

The MF Global incident establishes that the regulators protect the bankers before the customers. This is the same problem we have with the development of ending bailouts – the taking of customer money to bailout the bankers who are then never prosecuted. It is the ultimate collapse in public confidence.

Were Traders Forged in the Pits of Old?

Armstrong Economics Blog/Opinion

Re-Posted Jul 1, 2019 by Martin Armstrong

QUESTION: Mr Armstrong, love your blog, as with all your readers its opened my eyes to new ideas and ways of looking at the world.

I’m a recent computer science graduate who’s very interested in finance and trading so I read your blog every day and have a subscription to Socrates. I read a post where you said the soul of traders was forged in the pits, how does a new kid like me go about learning to trade really well in the age of tech? How does a computer science guy like me advance in the direction of finance and computer science like you have?

JB

![]()

ANSWER: I was told I had the last TransLux ticker-tape in the country. They came to my office and said they were taking it out. They would no longer support that service. Yes, I used to do my charts by hand in the 1970s. When the screen appeared in the ’80s, I still kept my paper tape. I would learn to trade from the sound. If something would be happening, it would sound like a machine-gun constantly shooting. Quiet days it would tick, tick, pause, tick.

ANSWER: I was told I had the last TransLux ticker-tape in the country. They came to my office and said they were taking it out. They would no longer support that service. Yes, I used to do my charts by hand in the 1970s. When the screen appeared in the ’80s, I still kept my paper tape. I would learn to trade from the sound. If something would be happening, it would sound like a machine-gun constantly shooting. Quiet days it would tick, tick, pause, tick.

I believe it was the sound that helped me learn to trade. I would just get a “feeling” or sixth-sense so to speak. You could smell the blood on the floor by the tape.

I believe it was the sound that helped me learn to trade. I would just get a “feeling” or sixth-sense so to speak. You could smell the blood on the floor by the tape.

Trading in the pits was like playing poker. You had to read the faces around you and get a sense if they were bluffing or real. That was the real trader environment. You had to know when to press and when to fold.

I have some ideas to help with getting that sixth-sense. It is on my bucket list of things to accomplish. I am trying to pass on what I have learned before it is my time to pray to beam up, please.

With pit trading closing and moving to electronic, we are losing a lot. I fear the next crisis for there will be even less liquidity with people only looking at screens. It will lack the “feeling” and the smell of blood on the floor to know when the trend will shift.

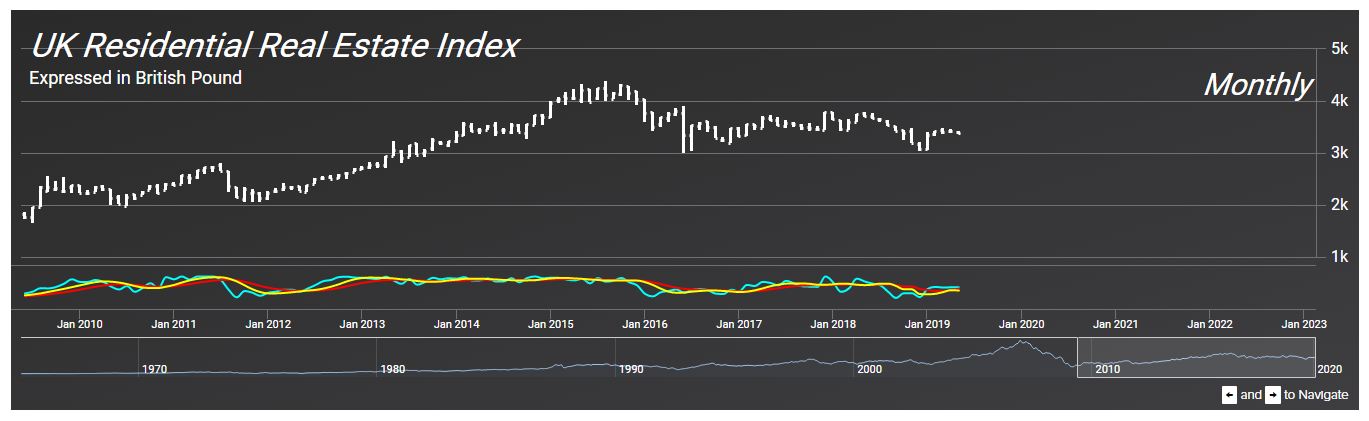

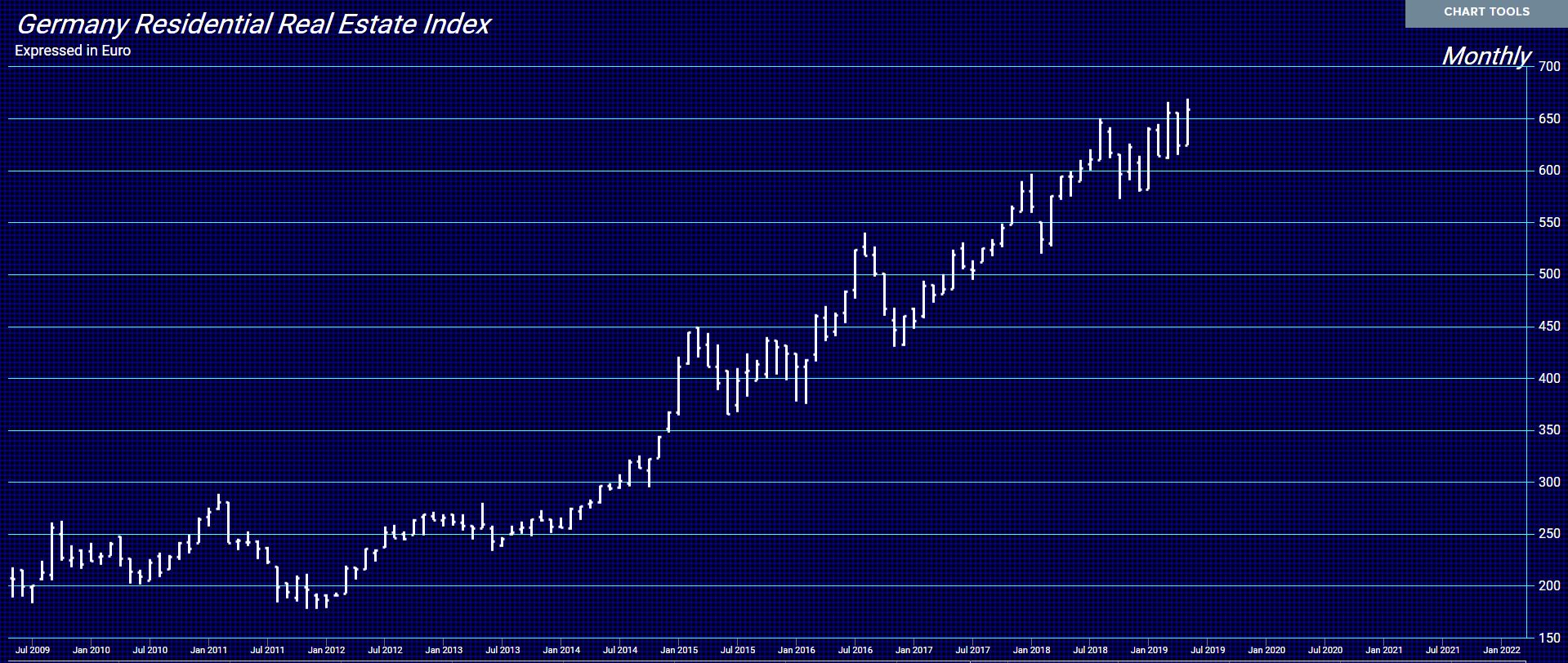

German Real Estate – the Peripheral Market Rally

Armstrong Economics Blog/Real Estate

Re-Posted Jul 1, 2019 by Martin Armstrong

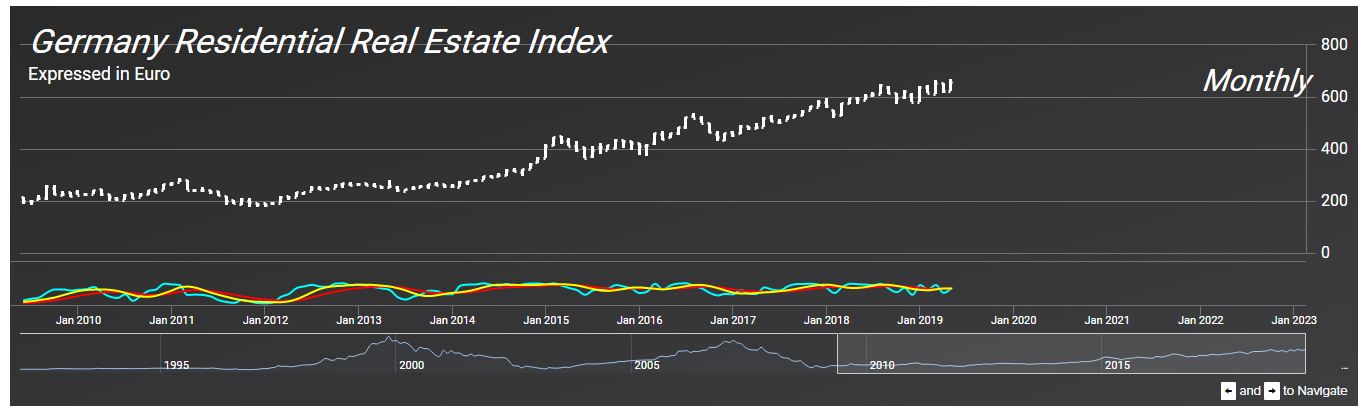

QUESTION: During the WEC I came to understand Real Estate will crash. Then when looking at Socrates, it shows real estate indices, however I do not recognise these trends. First I thought they were in $, I need to translate them to euro base to recognise the trend. But no, the real estate indices in Socrates are in terms of euro already and going down, while currently prices are again going thru the roof. Can you please explain what I am missing here?

M

ANSWER: It all depends upon which market you are looking at. The core markets where there was a lot of speculation like Britain saw a peak in 2015 and has been declining. London is far worse. The German market was not the object of massive foreign capital inflows. They were primarily internal shifts within the Eurozone. I was in Bavaria recently and looked at houses and I thought they were cheap in comparison to the United States.

Nevertheless, the rise in the German market has been about 50% since 2015. When we look at it in dollars, the gain is about 10% less. Insofar as German real estate, it has been a peripheral market to the speculation. That means it will rise after others decline.

Keep in mind that as the currency weakens, tangible assets become the haven.

The International Criminal Court the US Refuses to Recognize

Armstrong Economics Blog/Rule of Law

Re-Posted Jun 30, 2019 by Martin Armstrong

Will Shipping Turn in 2020?

Armstrong Economics Blog/Economics

Re-Posted Jun 28, 2019 by Martin Armstrong

COMMENT: HI MA,

Well, I know you’ve written about Germany many times as the next big country in Euro to hit the skids…I kept with Italy for a long period BUT now it is neck and neck…

What changed my mind? Independent of your writings…. It is shipping…there are a significant amount of German banks in shipping finance and that sector is coming unglued fast and there is no reversal in sight… and with the car sector in Germany as you have noted Germany is coming up behind Italy rather fast IMHO….

IT is a 2 horse race in my book… Socrates already knows which country is going to hit skids first…

YEP, Turkey has a very bad smell under it… Some European banks exposure to Turkey is going to result in them getting their arses kicked. Just add in ECB stupid policy to help the problem… How that ex G Sachs person was named ECB head and there isn’t/hasn’t been a revolve from European banks towards HIM I’LL NEVER KNOW… THEY are asleep at the wheel over there in Euroland MA (and not just in Europe I might add.. try Australia also), Europeans sending billions to US of A only goes to show some investors know the game is up in Europe ..and now lies eco ruins and perhaps WAR.

Cheers and have a Happy Easter,

Thanks for everything..what a world we live in….

F

REPLY: As car sales drop sharply, shipping is also declining. The Baltic Dry Index appears to be in a position to rally with the turn in the ECM come 2020.

Austria Sell 100-Year Bonds – But Who Are the Buyers?

Armstrong Economics Blog/Interest Rates

Re-Posted Jun 28, 2019 by Martin Armstrong

Austria was able to sell its second 100-year bond in history at just a yield of just over 1.00%. Some argue that capital has been forced to buy anything that has a yield which the ECB has been forcing negative interest rates. Why would anyone in their right mind buy a 100-year bond for 1%? The buyers appear to be pension funds who MUST own government debt as a matter of law.

Austria launched the sale of a 100-year bond on Tuesday after overwhelming investor interest gave its debt officials confidence it could become the first Eurozone country to sell a “century” bond publicly through a group of banks. There has been no paper on this part of the yield curve. Because of comments by Draghi, it is also expected that positive yielding paper will vanish in the Eurozone. As it stands, it will take investors 44 years to recoup their original capital. That will surely be a huge loss.

Austria is planning to sell the bonds via syndication to help access a wider base of investors. The banks involved are Bank of America Merrill Lynch, Erste Group, Goldman Sachs, NatWest Markets and Societe Generale. There is a serious problem brewing where as a matter of law pension fund must buy government paper and at low rates, the pension funds face massive failures going into the next 6 years.

Income or Privilege Tax?

Armstrong Economics Blog/The Hunt for Taxes

Re-Posted Jun 28, 2019 by Martin Armstrong

QUESTION:

Hi Marty,

Mini AOC sure is funny isn’t she?

Here is a tax story for you. I’m considering a summer sublet in Sedona AZ, and while I tried to sell all my CA property by the end of last year – well long story short I am still a landlord out here. So I was curious, what is it like to be a landlord in AZ these days in comparison? So I just did a search on it expecting well – nothing much. Shocker!

Guess what? AZ has a “privilege tax” – what is that privilege you say?

Well it is the privilege of doing business in Arizona! ta da!

Excerpt from Article Below:

Arizona transaction privilege tax is a tax on the privilege of doing business in Arizona. TPT applies when an owner of Arizona rental real estate is engaged in business under the residential rental classification by the Model City Tax Code.

If you rent Arizona residential real estate all payments made by the tenant or on behalf of the landlord are taxable.

Happy (Florida) Weekend,

A

ANSWER: Florida tends to be better for there are enough retired people here to keep the school taxes down and they present a stiff level of resistance to taxes. Believe it or not, I was shocked to see my property taxes go down. They are indexed to property values. However, there is a sales tax on rentals, not income taxes. This is a classic example. When you buy insurance it is typically named for the risk (fire, burglary, flood, etc.). However, when you buy death insurance, they called it “life insurance,” because no one is ready to buy death insurance. Here you have an income tax by just calling it a “privilege tax.” There are others who impose an occupation tax. That is a fixed tax depending upon your job to get around income taxes.

Portugal’s Miracle?

Armstrong Economics Blog/Economics

Re-Posted Jun 27, 2019 by Martin Armstrong

The Portuguese economy was bailed out by the European Union eight years ago. It is now booming, also in part for its aggressive attraction of courting foreign investors. If you want to live in Portugal long-term or permanently, you will need to apply for Portuguese citizenship or Portuguese permanent residency. Portuguese permanent residency is available after five years of residence, while Portuguese citizenship is available after six years, or three years if claiming Portuguese citizenship by marriage. Both Portuguese citizenship and permanent residency allows you to remain in Portugal indefinitely and access similar benefits, although there are some differences between the two. While residents can stay in Portugal indefinitely by continually renewing their permanent residency, there are certain added Portuguese citizenship benefits to entice foreigners to take on the Portuguese citizenship application process.

This movement has been a major factor behind Portugal enjoying its highest economic growth in nearly two decades, with the major trend fueled by record tourism, an upswing in the housing market from foreign investors, a growing tech sector, and strong exports. Private investment has returned to 2009 levels, helped by foreign investors including Chinese companies who have focused on Portugal.

But for every glitzy new hotel and fancy restaurant in Lisbon, there is growing concern that the infrastructure is aging. This was illustrated by the locomotive that fell apart in late February, which was rented from Spain as a stopgap measure. There has been a lack of public investment which is beginning to become obvious. Its total debt is close to 120% GDP, which is one of Europe’s highest. The ruling socialists have limited room to finance their dreams under the EU rules and at the current artificially low interest rates maintained by the ECB. The budget deficit of the 2010 era of 11% of GDP has been reduced by attracting foreign capital and cutting spending on public infrastructure. The problem that Portugal faces is that its success of late has been constructed on the immediate results, not long-term.